Quick Answer

Use a three-stage routine: confirm payer identity, GST path, and contract controls before kickoff; send an AP-ready invoice in AUD with the right reference format; then reconcile payment before converting to GBP. Keep a dated file for each cycle with the invoice, settlement confirmation, and FX record, and retain self-employed records for at least 5 years after the 31 January submission deadline.

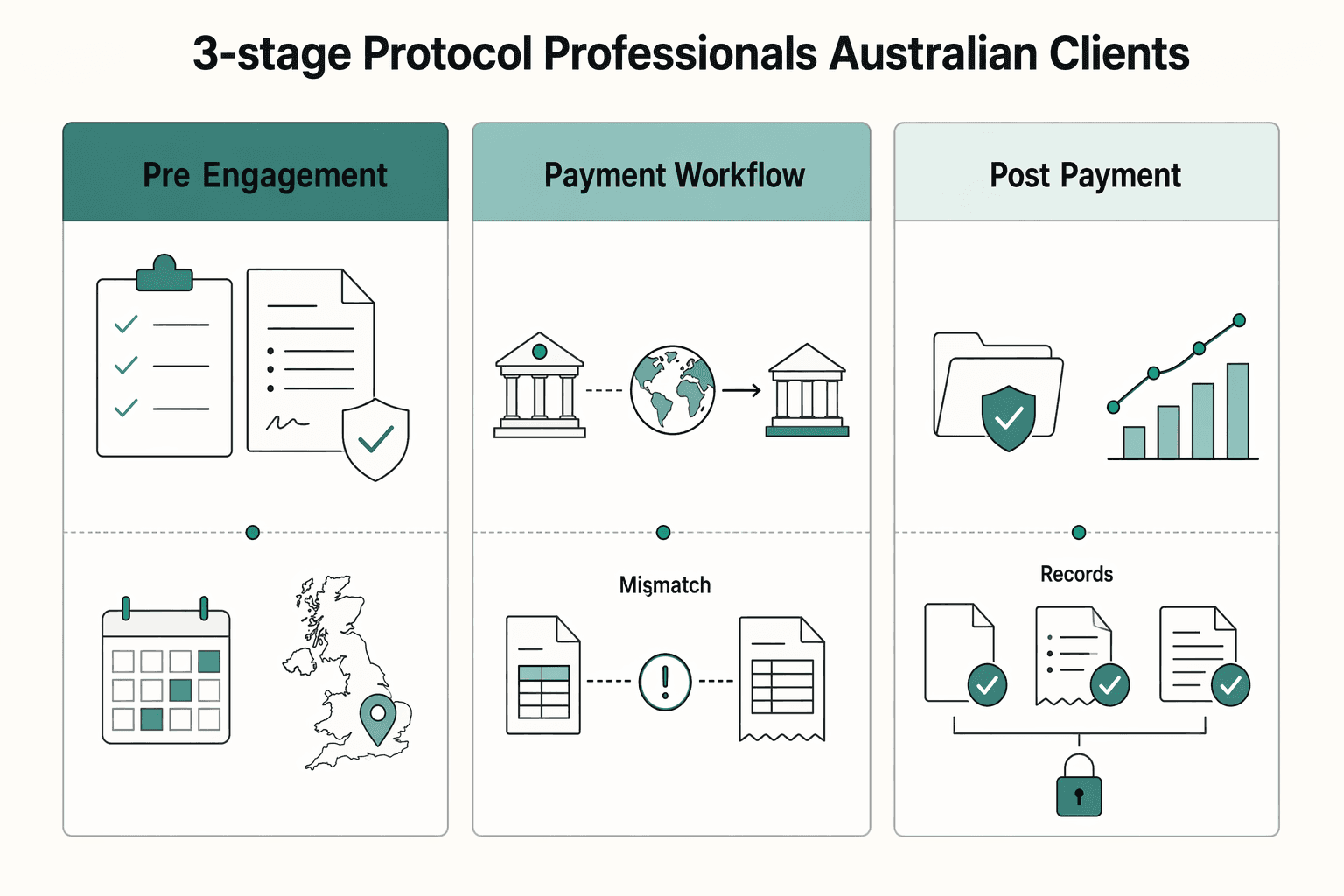

From Compliance Anxiety to Complete Control: A 3-Stage Protocol for UK Professionals with Australian Clients#

If you want predictable outcomes with an Australian client, manage three risks in order: contract scope, payment execution, and post-payment compliance. That sequence is what turns uncertainty into control.

| Stage | Main risk | What control looks like |

|---|---|---|

| 1. Pre-engagement | Wrong assumptions about contract scope, UK connection, or VAT treatment | You confirm key facts early and lock terms before work starts |

| 2. Payment workflow | Opaque fees, poor rate visibility, and AUD to GBP exposure | You use a route that shows the exchange rate, markup, and fees before transfer |

| 3. Post-payment | Missing records and unclear UK tax handling | You keep a complete evidence pack and treat compliance as part of delivery |

Stage 1 sets the baseline. HMRC says your UK residence status affects whether foreign income is taxed in the UK. One automatic residence test looks at whether you spent 183 days or more in the UK in the tax year (6 April to 5 April).

Where off-payroll rules are relevant, you also need to check UK-connection questions. For B2B services, place of supply generally follows where the recipient belongs, which affects whether UK VAT is chargeable.

Stage 2 protects margin. Before you accept any transfer route, check the applied exchange rate, the reference-rate markup, and any variable fees. That can matter even more when AUD to GBP is moving within the Bank of England's published 52-week range.

Stage 3 is about record discipline. Keep a defensible file for each payment, including the contract, invoice, payment confirmation, and FX conversion record. HMRC requires self-employed records to be kept for at least 5 years after the 31 January submission deadline for the relevant tax year.

From there, you can run the same protocol on every new Australian client engagement. For the residence piece, see Understanding the UK's Statutory Residence Test (SRT).

Stage 1: The Pre-Engagement Protocol - Securing Your Foundation#

Before you start work, lock three items in writing: who is paying you, how the contract handles predictable failure points, and which payment rail the client's AP team will actually use.

1. Compliance check#

Start with identity and status, not scope. For your compliance file, get written confirmation of the legal payer entity. Keep that confirmation with the signed agreement and onboarding emails in one dated compliance folder. Settle the Australia-side GST path before you finalize invoice wording.

| Checkpoint | Standard GST registration | Simplified GST registration |

|---|---|---|

| ABN position | Requires ABN entitlement | Does not require ABN |

| Identifier after registration | ATO written GST registration details (including effective date) | ARN (12-digit) issued after registration |

| Filing and payment cadence | BAS and GST monthly or quarterly | GST returns and payment quarterly |

| Operational limits | You cannot lodge electronically from outside Australia; you may need an Australian registered tax agent | Cannot issue tax invoices; cannot claim GST credits |

Keep these timing and threshold checks on your kickoff checklist: GST registration is due within 21 days once required, and ATO general guidance includes the $75,000 GST turnover trigger. Catch ABN assumptions early too: ABR says employee-type engagements are not ABN-entitled for that activity, and a sole trader is legally responsible for business debts.

2. Contract design#

Your contract should reduce common payment risks before work starts. Use this as a pre-signature control table, and get final legal wording reviewed before kickoff.

| Contract control | Risk it addresses | What you confirm before work starts |

|---|---|---|

| Payment start terms | Work starts before approvals are complete | Who pays, payment timing, and the agreed start trigger |

| Milestone billing terms | Invoices stay in review | Deliverables, approval windows, and billing points |

| Late-payment process | Overdue or short-paid invoices | Due dates, escalation steps, and shortfall handling |

| Scope-change process | Extra work treated as "included" | Written approval for scope, fee, and timing changes |

| Dispute process | Confusion on venue/process | Governing law, venue, notice method, and escalation order |

3. Payment-term setup#

Choose the payment rail before signature, then mirror it in both the contract and invoice template. The goal here is operational clarity: fee visibility, hold or review expectations, clean references, and something the client's AP team can actually use.

| Payment rail | Fee visibility check | Hold/review check | Reconciliation check | AP usability check |

|---|---|---|---|---|

| Local transfer to a multi-currency account | Confirm what the client sees before sending and whether deductions can still occur | Ask what can delay first payment or beneficiary setup | Require invoice number and client code in transfer reference | Confirm AP can pay local AUD details |

| International bank transfer | Confirm sender fees, intermediary deductions, and FX location | Ask which compliance checks can delay crediting | Require remittance advice and match invoiced vs received | Confirm AP cross-border wire process |

| Card or payment-link rail | Confirm processing, payout, and currency-conversion fees | Ask about reserves, disputes, or review conditions | Match payment ID, settlement ID, and invoice ID | Confirm client can pay through required portal or process |

Before kickoff, save one evidence pack with payment instructions, AP setup confirmation, and your registration notice details, including the effective date or ARN as applicable. That file is what keeps Stage 2 and Stage 3 predictable.

You might also find this useful: A Guide to Tax Residency in Australia for Digital Nomads.

Stage 2: The Payment Workflow Protocol - Controlling Your Cash Flow#

Once the contract is live, make payment boring. Receive AUD through a business rail your client's AP team can process, issue an AP-ready invoice, convert on a pre-set rule, and run collections on fixed triggers.

1. Receive in AUD through a business rail#

Start by giving AP a rail they already use. A business multi-currency setup can provide local AUD receiving details. That can reduce setup friction and let you choose when to convert AUD to GBP.

Before you send the first invoice, confirm three things with AP. Ask what they see when adding you as a payee. Ask whether first-payment or beneficiary review can delay release. Confirm which reference field they can pass through, such as invoice number plus client code.

| Rail | Hold risk | Fee clarity | Settlement speed | Reconciliation quality |

|---|---|---|---|---|

| Multi-currency local transfer | Varies by provider and client process, so confirm first-payment checks with AP | Can be clearer than cross-border wire, but still verify deductions | Can be fast on local rails; Australia's NPP supports near real-time availability 24/7 | Strong when AP includes invoice reference |

| Card wallet / payment link | Higher hold or reversal risk on some flows | Fee outcomes can vary across processing, FX, and dispute costs | Availability can vary, and some platforms may hold funds in rare cases | Weaker unless you capture payment ID, settlement ID, and invoice ID |

| Traditional bank transfer | Bank or routing reviews can delay release | Fee visibility can be incomplete; other banks may add charges | Typically 1-3 business days, sometimes longer | Mixed; often needs remittance advice to reconcile deductions |

Decision rule: use local AUD business receiving details when available, use bank transfer when required, and keep wallet rails as an exception.

2. Send an AP-ready invoice#

Your invoice should pass AP review the first time, so keep this checklist as your default:

| Invoice item | Article detail |

|---|---|

| Invoice number and date | Use a unique invoice number and issue date |

| Seller details | Include your UK business name, address, and contact details |

| Client details | Include the client legal entity name and billing contact |

| Amount and due date | Show the amount due in AUD, due date, and payment method |

| Payment instructions | Include full AUD payment instructions, including beneficiary name and required payment reference format |

| Service description | Tie the service description to the agreed milestone or period |

| Client ABN | Include the client ABN after checking ABN Lookup, if provided |

| Buyer identity or buyer ABN | Include buyer identity or buyer ABN if this is an Australian tax invoice for sales of A$1,000 or more |

| GST wording | Add GST wording only after registration-path verification |

| PO or vendor fields | Include client-required PO or vendor fields, if required by AP |

Two controls prevent avoidable delays: verify ABN details before invoicing, and only label a document a tax invoice when that label is accurate for your GST position. If a customer requests a tax invoice, it must be provided within 28 days.

3. Convert by rule, and keep consumer flows in their lane#

Reconcile first, convert second. Match received funds to the invoice, record any deductions, and store the remittance or payment confirmation with the invoice record.

Then convert by policy, not by guesswork. For example, convert immediately when GBP outflows are due soon. Otherwise, convert on scheduled sweeps, such as once or twice weekly, so the process stays consistent.

When choosing a platform, use this risk framework:

- Avoid consumer personal-payment flows for invoice-based B2B work

- Escalate to business rails when a hold or reversal would hurt cash flow, or when AP needs clean invoice-to-payment matching

- If a platform is required, keep it on a business product, document dispute handling, and confirm current limits directly with the provider

4. Follow up on fixed trigger points#

Collections work better when you run them on fixed triggers instead of ad hoc chasing. Automated due and overdue reminders are supported in common accounting tools, and Xero allows up to five reminder steps.

| Trigger | Action |

|---|---|

| 3 business days before due date | Send a friendly reminder with invoice and payment instructions |

| Due date | Send a short "due today" notice |

| 1 business day overdue | Ask if payment is scheduled and request remittance advice |

| 7 days overdue | Send a firmer follow-up; request either payment date or written dispute detail |

| No response | Move to letter of demand, then mediation |

| Disputed invoice | Pause automated reminders, request disputed line items and reasons in writing, and set a response deadline |

Set one exception path for disputed invoices: pause automated reminders, request disputed line items and reasons in writing, and set a response deadline so "under review" does not become open-ended.

For a step-by-step walkthrough, see The Best Way for a US Citizen to Get Paid by a Brazilian Company.

Before you lock your payment route, run your real transfer options through a payment fee comparison so you choose based on net GBP received, not headline fees.

Stage 3: The Post-Payment Protocol - Automating Your Peace of Mind#

Once payment arrives, fix your reporting position first, reserve funds by rule, and close each cycle with a complete evidence set. That keeps reporting, reserves, and records aligned while the details are still fresh.

1. Fix your reporting position before you label anything#

Treat your cross-border tax position as a checkpoint, not an automatic answer. Confirm where you performed the services, what type of sale you made, and whether GST registration is required. If your facts are not a simple remote-services setup, such as travel, local presence, or mixed sales, verify current treatment with a qualified adviser before you finalize invoice or reporting treatment.

For Australia, the immediate decision is usually the GST path. The ATO states penalties may apply if you fail to register when required, and required registration must be completed within 21 days. The ATO also lists a $75,000 GST turnover threshold, but you should check your sales type and obligations instead of relying on one number in isolation.

If you need to issue Australian tax invoices or claim GST credits, review the non-resident standard GST registration path. If you do not need an ABN and do not need GST credits, simplified GST registration may fit, but it does not allow tax invoices or GST credit claims. That mismatch matters if a client AP team requires a tax invoice. Keep two proof records on file:

- Standard path: ATO written confirmation, including effective registration date

- Simplified path: your 12-digit Australian reference number (ARN)

Also plan for the admin differences: standard registration may require an Australian registered tax agent because electronic lodgment from outside Australia is unavailable, with BAS lodged monthly or quarterly. Simplified returns are quarterly.

2. Reserve tax money by rule, not by mood#

After reconciliation, run the same steps every time. Convert AUD to GBP using your Stage 2 policy. Then move a reserved amount to a separate tax account on the same day or on a fixed weekly sweep.

| Monthly close step | What to confirm |

|---|---|

| Invoice match | Match invoice number to settlement record |

| FX record | Attach the FX conversion record for the AUD to GBP conversion used |

| Bookkeeping category | Post the receipt to the correct bookkeeping category |

| Deductions | Record bank or platform deductions as separate lines, not inside revenue |

| Tax reserve | Confirm the tax-reserve transfer date and amount |

Set the tax-reserve percentage only after the current provision rate has been verified, then keep that rate in your operating notes and standing instructions.

Use this monthly close checklist for each payment cycle, and if any item is missing, keep the cycle open until it is complete.

3. Build an evidence pack you can actually search#

Your records only help if you can find them quickly. Keep everything in one client folder with consistent filenames and clear cross-references between Stage 1 client-status evidence and Stage 3 payment records. That gives you a straight path from client status to invoice to payment treatment.

Use a consistent naming pattern such as YYYY-MM_Client_Invoice#_document-type. For each invoice cycle, keep at least:

- Invoice

- Settlement confirmation

- FX conversion confirmation

- Bookkeeping export or ledger note

In the invoice note or ledger memo, add a short reference to the related Stage 1 client-status file. Keeping that chain intact each month turns reviews into checks instead of reconstructions.

We covered this in detail in The Best Way for a German Agency to Pay a US-Based Freelancer.

Conclusion: You Are the CEO of Your Global Business#

Treat this as a working method, not a cleanup exercise. As a UK freelancer paid by an Australian client, you get better control when you set clear terms, make deliberate AUD to GBP decisions, and keep complete records from day one.

-

Stage 1: lock the facts before work starts. Confirm the commercial and reporting position before invoicing, especially where GST may or may not apply. If registration is required, the ATO says you must register within 21 days, and the path matters because simplified registration does not let you issue tax invoices or claim GST credits.

-

Stage 2: control how money arrives and when it converts. Where practical, use one payment route, one invoice format, and one conversion decision point for each UK to Australia payment. That helps keep each transfer traceable instead of forcing you to reconstruct decisions later.

-

Stage 3: close every payment with evidence. Reconcile the invoice, payment confirmation, and FX record while details are fresh. Keep the ATO written confirmation and effective date for standard registration, or the 12-digit ARN for simplified registration. Also track the cadence differences between monthly or quarterly BAS under standard and quarterly returns under simplified.

In practice, this means cleaner client terms up front, more consistent conversion decisions, and documentation that is ready when finance or compliance questions come in.

On your next Australia-facing engagement, run the same checklist logic from contract through payment close. Execute all three stages in order and keep the evidence chain intact so each new client follows a repeatable process.

If you want a deeper dive, read Separating Business and Personal Finances: A Important Step for LLCs.

If you want a single operational setup for invoicing, payment tracking, and payout workflows with traceable records where supported, explore Gruv for freelancers.

Frequently Asked Questions

Do you pay tax in Australia if you are a UK freelancer working for an Australian client?

Treat the tax position as fact-specific and get a current cross-border tax review for your exact situation.

What is the best way to receive AUD in the UK?

There is no default winner. Prioritize providers that can issue local AUD receiving details and clearly show their FX basis and route-level fees before you send. Wise, for example, describes usage-based pricing, says it uses the mid-market rate, and warns that extra Swift fees can apply on some routes.

How should you invoice an Australian client from the UK?

Make the invoice easy to approve and pair it with the receiving details exactly as your provider issues them for that payment route. Keep the currency and payment path consistent end to end, and confirm the account details match the method your client will use before sending.

Does IR35 apply to your Australian client?

This grounding pack does not provide enough evidence to determine IR35 status. Treat IR35 as a separate UK status question and get a current review of your specific contract and working practices.

How should you handle the AUD to GBP conversion?

Check the FX basis and total cost before you convert. Wise says it uses the mid-market rate and route-based transfer fees (starting from 0.57%), with volume discounts above 25,000 USD per month. Confirm the exact route first, because extra Swift fees can apply on some transfers.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- abr.gov.au/business-super-funds-charities/applying-abn/...trusted

- assets.publishing.service.gov.uk/media/60abbfc1e90e071b55dcafa4/Off-payroll_w...trusted

- ato.gov.au/businesses-and-organisations/international-t...trusted

- ato.gov.au/businesses-and-organisations/international-t...trusted

- business.gov.au/Finance/Payments-and-invoicing/How-to-invoicetrusted

- business.gov.au/finance/financial-trouble/what-to-do-when-yo...trusted

- community.ato.gov.au/s/question/a0J9s0000001Dmq/p-00029303trusted

- legislation.gov.uk/ukpga/1994/23/section/7Atrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How LLC Owners Separate Business and Personal Finances

For an LLC, separating business and personal money is best treated as a weekly habit, not a one-time bank setup. It keeps records cleaner, cuts month-end cleanup, and creates clearer boundaries as the company grows.

Understanding the UK's Statutory Residence Test (SRT)

Treat SRT like ops, not folklore. You want a repeatable workflow you can run monthly so your tax-year answer is boring, documented, and easy to defend.

Australia Tax Residency for Digital Nomads With GST and ABN Checkpoints

The goal is a defensible, low-drama position the Australian Taxation Office (ATO) can follow from your records, not a clever workaround. For a digital nomad, that usually means keeping two tracks straight: residency and GST/ABN admin. Consistency is what holds up over time: use real facts, take steps in a clear order, and keep documents that still match months later.