Quick Answer

A US citizen can get paid reliably by a Brazilian company by setting contract terms before work starts, choosing a payment provider that gives clear fee, FX, and transfer records, and saving each payment packet for U.S. reporting. Confirm the payer, currency, required ID fields, and proof-of-payment process up front, then reconcile each payment monthly.

--- Getting paid from Brazil can feel like dealing with unfamiliar rules, exchange-rate swings, and tax follow-up all at once. For many US-based professionals, the hardest part is not any single fee or form. It is the loss of control.

You fix that by designing the process before the first invoice goes out. This is not about finding one perfect app. It is a three-step plan: lock the contract terms, choose a payment route that gives you usable records, and keep each transaction ready for U.S. reporting. Do that, and payment from Brazil becomes predictable instead of improvised.

Step 1: Engineer a Bulletproof Service Agreement#

Lock payment terms before work starts. To make payment from a Brazilian client predictable, confirm the transfer setup early and write it into the contract before kickoff.

In Brazil, vague payment language can create avoidable delays and disputes. Cross-border FX operations run through institutions authorized by Banco Central do Brasil, and those institutions may require or waive documents depending on the transaction.

Brazil's Civil Code sets a local-currency baseline for money debts. Lei 14.286 allows foreign-currency stipulations in specific cases, including certain foreign-trade service scenarios. The practical rule is simple: do not assume USD or BRL is automatically acceptable. Have the client's bank, provider, or finance team verify current requirements, then document the agreed currency and payment route.

Use this checklist before signing#

Before you sign, confirm the client's actual payment process and collect the fields their team needs. That gives you terms to put in the agreement instead of guessing from a generic invoice flow.

| Checkpoint | Confirm | Notes |

|---|---|---|

| Paying entity | The exact legal payer and whether funds come from the Brazilian company, an affiliate, or another finance setup | Use the client's actual payment process before drafting terms |

| Currency and invoice format | Whether they require BRL invoicing for this payment flow or can process foreign-currency invoicing for this service type | Do not assume USD or BRL is automatically acceptable |

| Beneficiary tax-ID field | Which tax ID field they need and in what format | In BRL wire formatting, this is often CPF or CNPJ (11 or 14 digits), but requirements vary by institution and rail |

| Purpose-of-payment coding | Who provides the purpose field if BRL wire formatting applies | Some bank guides require a mandatory 5-digit PoP code plus description in PURP format |

| Proof package owner | The person or team responsible for sending transfer confirmation after each payment | Assign responsibility clearly in the agreement |

- Paying entity

Confirm the exact legal payer and whether funds come from the Brazilian company, an affiliate, or another finance setup.

- Currency and invoice format

Confirm whether they require BRL invoicing for this payment flow or can process foreign-currency invoicing for this service type.

- Beneficiary tax-ID field

Confirm which tax ID field they need and in what format. In BRL wire formatting, this is often CPF or CNPJ (11 or 14 digits), but requirements vary by institution and rail.

- Purpose-of-payment coding

If BRL wire formatting applies, confirm who provides the purpose field. Some bank guides require a mandatory 5-digit PoP code plus description (PURP format), and missing fields can cause rejection or delay.

- Proof package owner

Name the person or team responsible for sending transfer confirmation after each payment.

Once you know how the client will actually send the money, turn that into contract language and assign responsibility clearly.

| Clause | Protects against | Who is responsible | Evidence to retain |

|---|---|---|---|

| Net payment | Short payment from fees/deductions | Client | Signed agreement, invoice, receipt showing sent vs received |

| Exchange-rate source | FX disputes and hidden spread risk | Shared (client executes) | Contract clause, invoice currency, posted-rate record |

| Payment method | Rejected or delayed transfer from wrong rail or missing fields | Client sends correctly; you provide accurate details | Final instructions, client confirmation, transfer receipt |

| Proof of payment | "Paid already" disputes and weak records | Client | PDF confirmation, transaction ID, date, amount, fee or FX details if shown |

Net payment clause Intent: the amount priced is the amount you receive. Include: the invoiced amount is net to you; the client covers sending, intermediary, and related transfer fees. Prevents: underpayment caused by fee deductions you did not price for.

Exchange-rate source clause Intent: one shared conversion reference. Include: the exact benchmark and timing rule, for example, BCB Ptax or a posted provider benchmark like Wise mid-market. If you use a Wise-style posted benchmark, record the quoted rate display (typically 6 significant digits). Prevents: later disputes when each side uses a different market rate.

Payment method clause Intent: use a workable rail with complete instruction fields. Include: the approved method, required beneficiary details, and the client's responsibility for institution-required fields, including tax-ID and, where applicable, purpose-code fields. Prevents: avoidable rejection or delay from incomplete instructions.

Proof of payment clause Intent: make payment status verifiable. Include: transfer confirmation for every payment with date, amount, and transaction or confirmation ID, plus fee or FX detail if available. Prevents: reconciliation disputes and weak audit records. If paid through Wise, keep the downloadable PDF transfer confirmation with the signed agreement and invoice.

If the client cannot confirm currency, the required ID field, or payment-purpose handling before signing, pause the start date until they can. That short delay is often less disruptive than fixing a failed transfer after an invoice is due.

If you want a deeper dive, read Separating Business and Personal Finances: An Important Step for LLCs.

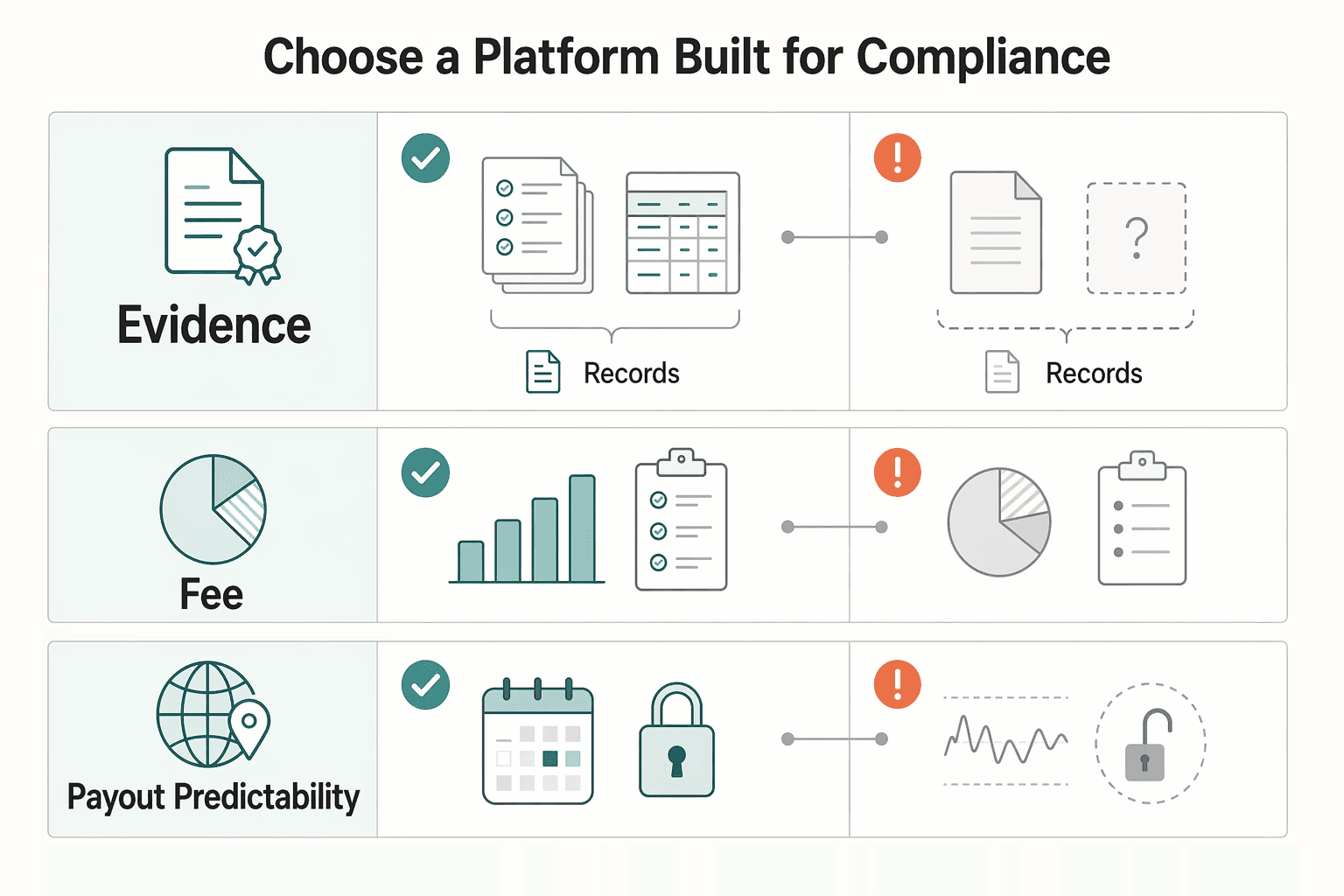

Step 2: Choose a Platform Built for Compliance, Not Just Convenience#

Once the contract is set, platform choice becomes a compliance decision. If a provider cannot show you, before onboarding, how fees, FX, and transfer evidence appear, treat that as a fail.

| Check | What to verify | Fail signal |

|---|---|---|

| Documentation | A transfer confirmation or statement you can retain outside the platform, with core reconciliation fields such as amount, date, and reference | Only a status email or no sample completed transfer record |

| Fee and FX | The quote flow shows the rate basis and fee line items | Only a final payout with no fee breakdown or no stated rate basis |

| Payout predictability | A clear expected timing window before approval, plus route notes each time | Speed claims alone or no clear timing window before approval |

1. Documentation pass/fail#

Start with records. You need a transfer confirmation or statement you can retain outside the platform, not just a status email. Before you commit, ask for a sample of the transfer record the platform provides. If you cannot verify that it includes core reconciliation fields, such as amount, date, and reference, move on.

2. Fee and FX pass/fail#

Your contract already sets the FX rule. Now confirm the platform shows it clearly in the quote flow. Wise states that it uses the mid-market rate and shows fee line items, including examples like 6.11 USD wire fee, plus a total included fee.

Run a live quote yourself. If a provider shows only a final payout with no fee breakdown or no stated rate basis, you are taking hidden-spread risk.

3. Payout predictability pass/fail#

Do not optimize for speed claims alone. Choose a provider that gives you a clear expected timing window before approval. Wise quote screens can show an arrival estimate, for example, "Should arrive by Wednesday," and a sample rate-lock window (20h).

Also check route notes each time. Wise flags that additional Swift fees may apply in some cases.

| Option | Statement quality | Fee visibility | FX transparency | Payout predictability | Exportable records |

|---|---|---|---|---|---|

| Wise | Verify with a sample completed transfer record | Quote flow shows line-item fees and total included fees | Mid-market rate is stated | Expected arrival shown in quote | Regulator-standardized fee-format link is available; verify the transfer-record export format yourself |

| Payoneer | Not established here; request sample records | Not established here | Not established here | Not established here | Not established here |

| Brazil-focused local rail/provider | Not established here; request sample records | Not established here | Not established here | Not established here | Not established here |

That comparison only helps if you test the route you plan to use and keep the evidence it produces. After each transfer, save:

- If available, download the receipt or statement in a saveable format.

- Save the original amount and currency.

- Save the FX rate or FX line item shown.

- Save the fee breakdown, not only the net received.

- Save the transaction or confirmation reference and transfer date.

Use Wise only if your own test flow meets these checks and matches your contract terms. If it does not, choose the provider that gives you the cleanest documented evidence.

Before you lock a provider, run your planned scenarios in the payment fee comparison tool and save the output with your contract notes. Related: Hungary's White Card for Digital Nomads: A Complete Guide.

Step 3: Build Your Compliance Firewall for US Taxes#

Once the money arrives, the main risk shifts from delivery to records. Treat each payment as a same-day filing task so every transaction is ready for review later.

1. Run one fixed post-payment workflow#

After each payment clears, create one folder and store the full packet before you move on. The IRS allows any recordkeeping system that clearly shows income and expenses, so consistency matters more than tool choice.

Use one naming pattern by year, income type, client, and invoice:

2026/Income/Brazil/ClientName/2026-03-24_INV-004_BRL-12500

Inside that folder, use matching file names: 2026-03-24_contract_ClientName.pdf 2026-03-24_INV-004_BRL-12500.pdf 2026-03-24_transfer-receipt_ClientName.pdf

Checkpoint: if a preparer cannot understand the transaction from that folder alone, the packet is incomplete.

2. Verify the three core artifacts before archiving#

Signed agreement Save the executed version, not a draft. Verify that the client identity, service description, and payment terms match what you invoiced.

| Artifact | Save | Verify |

|---|---|---|

| Signed agreement | The executed version, not a draft | Client identity, service description, and payment terms match what you invoiced |

| BRL invoice | The exact BRL invoice sent | Invoice number, date, client name, service description, gross amount, currency, and due date |

| Transfer receipt or confirmation | The platform proof of payment; for Wise, the transfer receipt PDF | Sender or reference, payment date, amount, and transaction reference |

BRL invoice Save the exact BRL invoice sent. Verify invoice number, date, client name, service description, gross amount, currency, and due date.

Transfer receipt/confirmation Save the platform proof of payment. For Wise, the transfer receipt is a PDF with payment details banks can use to track funds. Verify sender or reference, payment date, amount, and transaction reference. If FX or fee detail is missing, attach the supporting quote or statement export from your Step 2 process.

3. Map each payment packet to filing tasks#

Your U.S. return is filed in USD, and your functional currency is generally USD unless you are required to use a foreign currency. Use one posted exchange-rate method consistently and document it.

| Filing task | Required evidence | Your action | If evidence is missing |

|---|---|---|---|

| FBAR (FinCEN Form 114) | Foreign account or platform records showing balances, plus identifiers and transfer records where relevant | Check whether your aggregate value crossed the current filing threshold; if required, file electronically by the applicable due date | Request missing exports immediately; keep supporting FBAR records for five years |

| FEIE (Form 2555) | Income packet (agreement, invoices, receipts) plus eligibility support, for example, travel-day records for physical presence | Confirm eligibility before claiming; apply the current annual limit only after verification | Rebuild day-count and income support first; do not estimate |

| General income reporting | BRL invoice, payment proof, deposit record, FX translation record | Book income in USD using your documented rate method | Attach invoice, deposit proof, and translation memo when receipt detail is incomplete |

FBAR is separate from Form 1040 and filed electronically. It has an automatic extension to October 15 after the April 15 due date. FEIE can reduce regular income tax when you qualify, but it does not reduce self-employment tax.

4. Reconcile monthly, not at year-end#

Do this monthly, not at year-end, while the records are still easy to verify. It keeps bookkeeping, tax prep, and payment evidence aligned while the details are still fresh:

- Match each BRL invoice to a transfer receipt or account-statement entry.

- Confirm booked USD amounts follow your documented exchange-rate method.

- Pull any missing receipts, quotes, or statements while records are still easy to retrieve.

- Update one tax handoff sheet with invoice number, client, BRL amount, USD booked amount, payment date, and FBAR or Form 2555 review flags.

You might also find this useful: A Guide to Tax Residency in Brazil for Digital Nomads.

From Transactional Anxiety to Strategic Control#

Predictable results come from controlling three checkpoints: your agreement, your payment rail, and your records.

- Agreement first (risk allocation)

Set terms before work starts so disputes do not appear at invoice time. In Brazil practice, contracts are used to anticipate uncertainty, and the risk allocation defined by the parties is expected to be upheld. Use that moment to lock who absorbs fees, how payout is executed, and what client details must be confirmed up front.

- Choose rails for evidence quality

Choose Pix or boleto based on traceability, not speed alone. Pix is operated by Banco Central do Brasil, available 24/7, and QR payments settle immediately; boletos can take days to clear. With the newer boleto rules, boleto payment can run through Pix rails with a Pix QR code, which makes it even more important to confirm what receipt you can download, who appears as sender of record, and where funds settle. Confirm any CPF-related onboarding requirement early instead of assuming.

- Keep a single evidence pack (operations + U.S. reporting)

Store the signed contract, final invoice, transfer confirmation, and matching statement entry together. If you use Wise, download the transfer confirmation PDF. Its banking partner reference matters when a bank cannot locate a transfer, and a transfer marked sent can still take a few working days. Keep this same file set ready for FinCEN Form 114 review if your aggregate foreign account value exceeds $10,000 at any point in the year, and keep reportable-account records for generally five years.

| Process | Documentation quality | Fee visibility | Payment predictability |

|---|---|---|---|

| Reactive | Details scattered across chats or email | Fees discovered late | Delays are harder to diagnose |

| Controlled | Contract, invoice, receipt, and statement stored together | Terms set in contract and verified at transfer | Clearer expectations by rail, faster troubleshooting |

Your repeatable system#

- Before work starts: confirm the rail, confirm any CPF onboarding detail, and lock fee and payout terms in the contract.

- When invoicing: match contract terms exactly and verify any Pix, boleto, or local-field request before sending.

- After payment lands: download the available receipt or confirmation PDF, save the statement entry, and file both with the contract and invoice.

For a step-by-step walkthrough, see The Best Way for a UK Freelancer to Get Paid by an Australian Client.

If you want one operational flow for invoicing and getting paid, with compliance checks and traceable records where supported, review Gruv for freelancers.

Frequently Asked Questions

What is the best way for a US freelancer to get paid from Brazil?

There is no single best method in this guide. Use a payment route you can fully document from payment initiation through final deposit. Keep the transfer receipt and the matching deposit entry from your account statement.

How do I invoice a company in Brazil?

This guide does not provide Brazil-specific invoice field requirements. Match your signed contract and follow the payer's written instructions. Keep the final invoice PDF and proof that you sent it.

Do I need a Brazilian CPF to receive money from a Brazilian company?

This guide does not establish a universal CPF requirement. Confirm onboarding requirements before work starts, not near the payment date. Keep the written request, what you submitted, and any approval message.

How are payments from Brazil taxed for a US expat?

Report the income on your U.S. tax return, then review FEIE and FBAR separately. FEIE can reduce regular income tax when you qualify, but it does not reduce self-employment tax. Keep travel-day records, invoices, receipts, and filing workpapers.

Can a Brazilian company pay me with Pix?

This guide does not provide Pix-specific setup or eligibility rules. Before you agree to this rail, confirm what records your provider can produce and where funds are shown as settled. Keep provider confirmation and the final transfer record.

What is a Boleto Bancário and can I be paid with it?

This guide does not provide Boleto-specific setup or eligibility rules. Use it only if your provider can supply a clear record trail from the payment request to final payout. Keep the issued payment request, payment confirmation, and payout proof.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

How LLC Owners Separate Business and Personal Finances

For an LLC, separating business and personal money is best treated as a weekly habit, not a one-time bank setup. It keeps records cleaner, cuts month-end cleanup, and creates clearer boundaries as the company grows.

Hungary White Card Guide for Digital Nomads: Eligibility, Documents, Fees, and Timeline

Treat this like an audit, not a hope-and-pray submission. Your job is to decide whether your real-world setup fits the permit logic, pick the right filing route, then build one evidence pack that stays coherent even if someone reviews it line by line.

A Guide to Tax Residency in Brazil for Digital Nomads

**Stop treating Brazil tax residency as a guess and run it as a monthly decision system with written rules, clear triggers, and conservative defaults.** If you run a business-of-one in South America, you do not need a risky tax hack. You need a repeatable check that turns legal triggers into actions. Build the ledger and checklist once, then keep the review short and consistent so your tax position stays aligned with how you actually live and work. A practical system starts with triggers you can verify, not opinions you can debate.