Quick Answer

Yes - use written payment terms before work starts: set asset (such as USDC or Bitcoin), network, due date, and the exact event that marks an invoice paid. For get paid in crypto freelance, treat a transaction hash as “sent,” not “settled,” until funds arrive at the agreed destination and invoice details match. Keep one invoice evidence bundle with terms, payment instructions, confirmations, and conversion records so delayed-payment disputes stay factual and easier to resolve.

Why freelancers use crypto payments and where most setups fail#

Freelancers use crypto payments for a practical reason: slow payouts and high transfer costs can squeeze monthly cash flow. Traditional rails are still slow in many cases, and crypto-freelance payment guides report regional fee pressure that can land around 5% to 10%. When a client wants to pay this way, the goal is not novelty. It is predictable settlement, clean records, and fewer avoidable disputes.

That only works if the payment rules are explicit before work starts. Platform labels, fee rules, verification steps, and status wording change. A process that worked six months ago can fail today if someone is relying on old screenshots or copied help text. Check current terms every time you set up a new client flow.

Most payment conflicts are not technical failures. They are process failures under time pressure. Someone skips confirmation, treats a hash as final settlement, or waits too long to define what happens when status is unclear. Then urgency turns a simple mismatch into a trust problem.

Use one shared baseline before kickoff:

- Define the payment promise in one approved place. Lock the asset, network, receiving address format, due date, milestone schedule, and the exact event that counts as paid.

- Keep

sentandsettledseparate in your records. A transaction hash alone does not close an invoice. The transfer still has to match the invoice, and funds have to arrive at the agreed destination. - Set the failure path before the first issue. Decide who investigates first, what proof is required, and when delivery pauses if status stays unresolved.

- Keep escalation language factual. Neutral updates tied to records lower conflict and protect the client relationship when timing gets tight.

Before kickoff ends, have both sides restate the payment rule in one sentence and confirm it in writing. That small step catches interpretation gaps before money moves and gives you one clean reference if status later becomes disputed.

Freelancers who stay reliable under pressure usually do three things well. They remove ambiguity early, verify every transfer against the agreed terms, and keep records together from invoice through conversion. Speed matters, but consistency is what keeps a project moving.

Start with the payment sequence you can execute every time. Once that is stable, optimize for speed. If you need a simple template, try the free invoice generator.

What to prepare before you accept your first crypto invoice#

Do the setup work before the first invoice goes out, not after the first mistake. A client should see one clear way to pay, one standard for verification, and one path for escalation if status is unclear.

Start with the receiving side. Use a dedicated crypto wallet for client payments and keep that activity separate from personal holdings. That makes reconciliation easier and reduces confusion when you need to review invoice history later. Decide in advance how you will handle USDC or other stablecoins after receipt, including whether you hold or convert.

Then publish terms a client can follow without interpretation:

- Accepted assets and accepted networks

- Confirmation requirements

- Due-date rules

- The exact condition that marks an invoice paid

Put this in place before work starts so both sides are aligned before anyone is under deadline pressure.

Next, build your invoice records pack template now, not after something goes wrong. For each invoice, keep the terms, invoice file, payment instruction message, payment proof, approval trail, and conversion records in one place. The goal is simple: if a question comes up later, you can answer it from one complete record set instead of rebuilding the story from scattered chats.

Also check the friction points that can slow payouts even when everyone is acting in good faith. Confirm whether your payout path can trigger verification checks, who can resolve those checks, and where delays usually show up. A route that feels smooth in normal conditions can still stall the moment verification is requested.

Assign client-side owners before kickoff. Identify who approves invoices, who sends payment, and who confirms release if status is disputed. Missing ownership is one of the most common causes of avoidable delays, especially when finance and project delivery sit with different people.

Set one correction rule now: if the address, network, or asset details change, require a revised invoice and written reconfirmation before transfer. Do not process critical payment changes across a string of chat edits.

This prep work lowers dispute risk and gives clients a path they can follow correctly the first time. Before the first live invoice goes out, run one internal dry run so you can issue details, verify receipt, and close records without guesswork. Once that groundwork is in place, you can choose the payment route. For broader cash flow planning, How to Set Financial Goals for Your Freelance Business is useful reading.

Pick your payment route based on control, speed, and client behavior#

Route choice is less about preference than about execution. The right option is the one your client can complete reliably when the project is busy and people are rushing.

| Route | Best fit | Speed profile | Control profile | Main tradeoff |

|---|---|---|---|---|

| Direct wallet transfer | Mature client with clear approvals | Can be fast, depending on network and payer execution | High control over terms and verification | Requires strict checks on asset, network, and receipt proof |

| Platform-mediated flow (for example Upwork, LaborX, CryptoTask) | New client or unclear internal operations | Can add processing steps before payout | Can provide structured status checkpoints | Platform rules may reduce flexibility |

| Hybrid (platform for discovery, direct for repeat clients where allowed) | Relationship starts uncertain, then stabilizes | Early phase may be slower, repeat phase can speed up | Balanced after trust is established | Needs clear switch criteria to avoid confusion |

The tradeoff is straightforward. Direct transfer can be efficient when the client has stable owners and a clean approval path. A platform-mediated flow usually gives you clearer status checkpoints when ownership is messy or the relationship is new. A hybrid approach can work well, but only if the handoff from platform to direct transfer is defined before anyone assumes it has already happened.

These kickoff checks make the route decision more objective:

- Go by behavior, not promises. If approvals are slow, owners are unclear, or finance and project leads disagree, use a route with clearer status checkpoints.

- Match asset handling to cash flow reality. Stablecoins are commonly used to reduce transfer volatility. Some gateways settle in crypto or auto-convert to fiat, but behavior varies by provider. Confirm conversion and withdrawal behavior before you issue the invoice.

- Set fallback triggers in writing. Cross-border payouts can trigger compliance checks, and requirements differ by country. Define exactly when you switch routes if status stays unresolved beyond the agreed window.

- Document switch ownership. Clarify who can authorize moving from platform-mediated flow to direct transfer for repeat work where allowed. Unclear ownership here leads to duplicate invoices and conflicting status updates.

A simple rule of thumb: if client ownership and approvals are clear, direct transfer can be efficient. If ownership is unclear or handoffs are frequent, a platform with structured status can reduce ambiguity. If the relationship is new, start where status tracking is easiest to document, then switch only after repeated on-time settlements. A route is only trustworthy if it still works when something goes wrong.

If you are unsure which route to trust, run one low-stakes pilot invoice before you commit the next milestone. The pilot does not need to be elaborate. It only needs to prove approval, transfer, receipt, and reconciliation with the real people involved. Once you know the route, put those terms in writing.

Set payment terms in writing before work starts#

If your core payment terms live in chat, you will eventually argue about what was agreed. Put them once in the SOW or contract and treat that document as the single source of truth.

At minimum, lock these points before work begins:

- Settlement asset (USDC or Bitcoin)

- Approved network

- Due date

- Milestone payment schedule

- Late-payment handling

Add a mismatch clause so a status question does not become a negotiation when details conflict. Define how payment-status issues are handled if the amount, asset, network, or destination does not match the approved terms.

For larger scopes or higher-risk projects, staged milestone payments with explicit deliverables reduce ambiguity. Both sides can see what each payment covers, what has been accepted, and what remains open. That makes it much easier to pause one milestone cleanly without turning the whole project into a payment dispute.

Be specific about the asset. USDC is typically used for dollar-linked stability. Bitcoin can move between invoice issue and settlement. State when value is measured and what amount is due at that moment so payment status stays objective instead of becoming a debate about market movement.

Set late-payment expectations before you need them. One major payments guide reports that 74% of freelancers are not paid on time. You do not need aggressive contract language to manage that risk. You need clear trigger points, documented reminders, and defined next actions for unpaid milestones.

Keep the wording plain enough that someone outside legal or finance can restate it after one read. If they cannot, your terms are still too vague. Once those terms are fixed, decide which asset policy you actually want to run.

Should you accept Bitcoin or require USDC#

For most freelance work, stable settlement is more useful than price exposure. USDC or another stablecoin is usually the safer default when cash flow comes first, and operator reports on crypto payout preferences often point to the same tradeoff. Accept Bitcoin when value timing and variance handling are explicit in writing.

Keep pricing in fiat and settle in the agreed crypto asset. That keeps scope and commercial terms understandable even when market prices move between approval and payment.

Use these rules to keep the decision practical:

- Use a stablecoin-first rule for predictable receivables. USDC and similar stablecoins are commonly used in freelancer payments and are described as dollar-tied with lower volatility than Bitcoin.

- Accept Bitcoin with timing language, not assumptions. If a client pays in Bitcoin, define when value is measured and what counts as fully paid at that point. If funds arrive outside those terms, keep the milestone open until corrected.

- Tie conversion timing to runway needs. If most expenses are in fiat and runway is tight, convert from USDC soon after receipt. If you intentionally keep crypto exposure, set a cap on what stays unconverted.

- Check payout economics before kickoff. Conversion fees, spread, and withdrawal constraints vary by provider and program. Verify the total cost path before you issue the first invoice, not after funds arrive.

Keep client discussions concrete with this comparison:

| Priority | Preferred settlement choice | Why |

|---|---|---|

| Predictable monthly expenses in fiat | USDC or similar stablecoin | Reduces large value swings during transfer and settlement |

| Client only pays in Bitcoin | Bitcoin with strict value-timing terms | Keeps invoice status objective when prices move |

| Mixed goals: cash flow plus some crypto exposure | Settle in USDC, convert only a planned portion | Protects operating stability while allowing controlled exposure |

The key is consistency. Apply one acceptance policy across clients so invoice handling does not change case by case. Once the asset rule is clear, the next job is to make the invoice sequence easy for clients to execute correctly.

Build an invoicing sequence clients can execute without mistakes#

Most payment mistakes happen in the handoff between invoice and transfer. A consistent sequence prevents more errors than extra reminders.

Keep the client-facing message simple, and keep your internal checks strict. Clients need one short set of instructions they can act on. You need a repeatable process that catches mismatches before you close the invoice.

Use this sequence for every invoice:

- Issue the invoice with complete details. Include client information, scope, invoice ID, due date, and payment terms. For milestone work, list each milestone amount. If VAT applies in your jurisdiction, include it.

- Confirm payment details in writing before transfer. Ask the payer to confirm the invoice ID, asset, network, destination, and amount in one thread tied to the current invoice terms.

- Send one fixed payment instruction block. Put the payable amount, payment details, and deadline in one message. If proof is required after transfer, say so in that same message.

- Verify receipt before marking paid. Only close the invoice when funds are visible in your records and the details match the approved terms.

- Define

sent but not settledhandling. Set who investigates first, what proof is required, and when delivery pauses or resumes. - Restart confirmation after any late change. If payment details change after issue, reissue the details and reconfirm in writing before transfer.

A client-ready instruction format helps reduce mistakes:

- Invoice ID:

- Amount due:

- Payment details:

- Payment deadline:

- Required proof after transfer (if required):

- Contact for payment-status issues:

Keep your internal acceptance checks separate from client communication. The client message should stay concise. Your internal checklist can be stricter and should include verification points, timeline notes, evidence storage actions, and any conversion decision after receipt.

In practice, the failure modes are usually operational, not technical. Payment details do not match the invoice. Proof does not match your records. The wrong internal owner confirms transfer. Or the invoice gets updated after transfer with no version trail. When any of those shows up, keep the status pending until the evidence lines up with the written terms.

This also protects handoffs. If someone else has to cover billing while you are offline, a fixed sequence and a complete invoice thread let them continue without guessing what was agreed or what is still missing.

It also makes escalation cleaner later. If there is a delay or mismatch, you are not inventing a response in the moment. You are pointing back to a sequence both sides already accepted. That same sequence should feed the records you keep after settlement.

Keep an evidence pack for disputes, tax prep, and reconciliation#

A clean evidence pack turns a tense payment question into an administrative task. Do not treat wallet receipt as the end of the process. An invoice is closed when your records can explain the full timeline without relying on memory.

Build one complete evidence pack per invoice:

- Store the core bundle together. Keep approved terms, the invoice, payment instructions, transfer confirmation details, and client approvals in one location.

- Maintain a chronological status timeline. Record issuance, approval, transfer, receipt, mismatch notices, corrections, and final closeout.

- Separate transfer proof from settlement proof. A send event and a settled invoice are different states. Mark paid only when the invoice terms and transfer details align.

- Keep export-ready reconciliation records. If you use ledger-backed events, including Gruv capabilities where enabled, store the data in an exportable format.

- Limit sensitive data exposure. Keep what is needed for disputes, reconciliation, and tax prep, and avoid collecting extra personal data that is not required.

- Set one unresolved-status rule. If status is

sent but not settled, assign an owner, collect the required proof pack, and pause delivery until verification is complete.

A practical pack usually includes the final approved terms, invoice PDF or equivalent, payment instruction copy, client confirmation message, transfer confirmation details, and a final close note with the settlement date.

Close each invoice pack right after settlement while the details are still easy to verify. Waiting until month-end is a common failure mode because artifacts go missing, screenshots disappear, and people remember the sequence differently. Once you know what good records look like, you can use the same standard to compare payment channels.

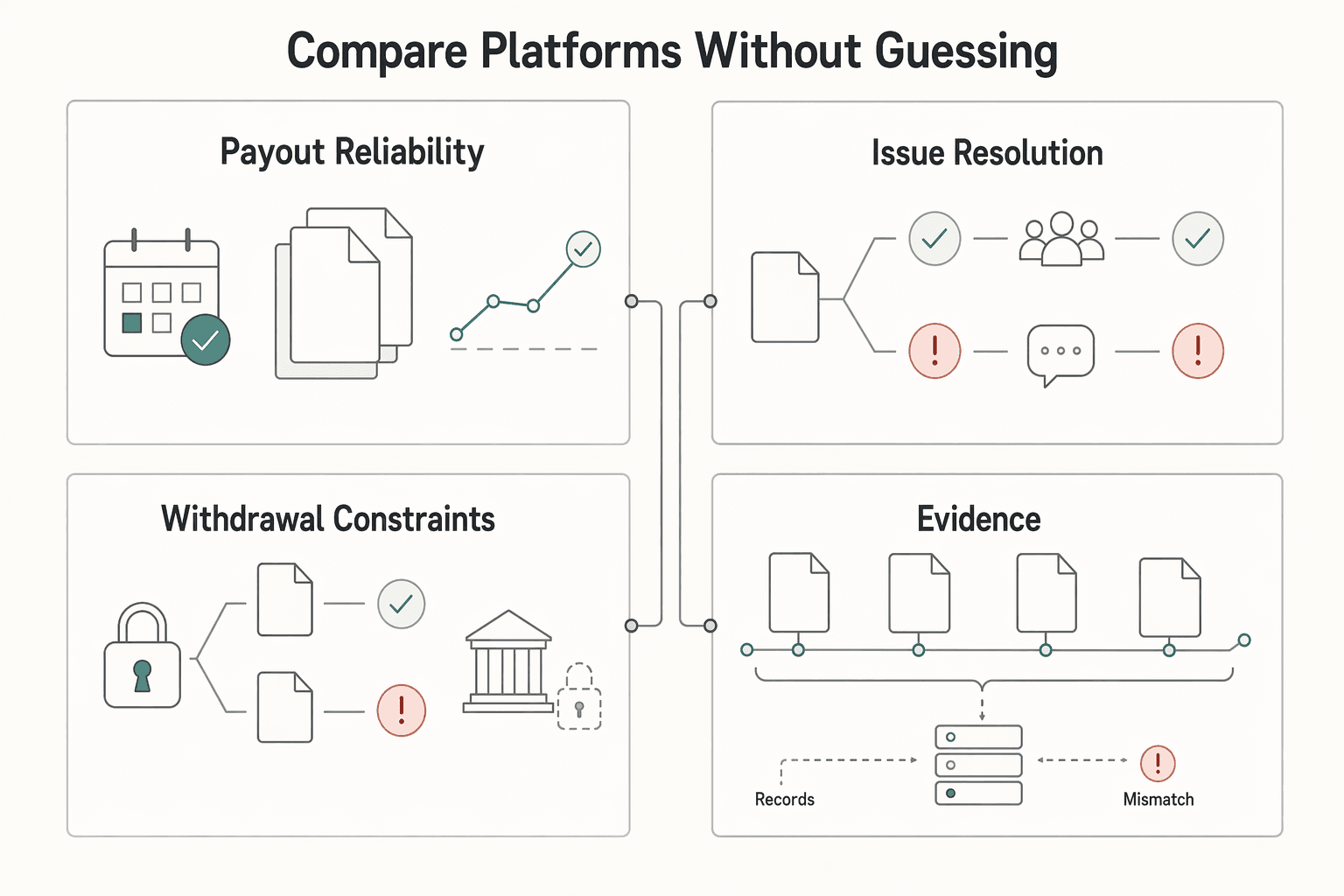

Compare platforms without guessing#

Do not choose a platform from marketing copy or listing volume. A small paid test tells you more than feature pages will.

Before routing meaningful revenue through any of them, run the same controlled test on Upwork, LaborX, CryptoTask, and GoLance. What matters is end-to-end payout behavior, not the best-looking promise on a landing page.

Use the same test method every time:

- Use one repeatable setup. Keep service scope, invoice format, and payment window identical so results are comparable.

- Treat public fee claims as provisional. A March 16, 2021 Hacker News post described CryptoTask as a 0% fee platform, while a commenter in the same thread referenced 3% and a 70% freelancer-share figure. Treat that fee picture as unresolved until your own paid test clarifies it.

- Verify each test end to end. Log invoice approval time, payment initiation, receipt timing, status transitions, and export quality. Mark a test as pass only when funds are visible and records reconcile cleanly.

- Review channels monthly. Keep channels that repeatedly pay on time with manageable withdrawal friction. Replace channels that repeatedly fail your criteria.

Use a consistent scorecard:

| Criteria | What to capture in your first paid test | Red flag |

|---|---|---|

| Payout reliability | Invoice sent time, client paid time, funds available time | Payment marked sent but still unavailable by your deadline |

| Issue resolution process | First support response time, required evidence, closure time | No clear owner or repeated requests for the same proof |

| Withdrawal constraints | Steps, hold states, conversion limits, final receipt time | Unplanned holds that block cash flow |

| Records quality | Export fields for invoice ID, payment ID, status history | Missing fields that break reconciliation |

Add one pass or fail question to every test: could a teammate read this invoice pack and understand what happened without follow-up questions? If the answer is no, records quality is still weak even if the payout eventually arrives.

After testing, stay disciplined:

- Keep a route only after repeated clean outcomes.

- Do not scale volume on routes that fail basic payout verification.

- Do not ignore small friction that repeats each cycle, because repeated friction becomes cash flow risk.

Once your channel choices are grounded in real tests, delay handling gets much easier because the escalation paths are already visible.

Handle delayed, failed, or ambiguous payments without damaging the client relationship#

When a payment is late, the fastest way to damage the relationship is to improvise. Stay factual, keep the record trail tight, and avoid language that turns a verification gap into a personal conflict.

Use this sequence when payment is late or ambiguous:

- Set expectations before work begins. Even without a formal contract, your approved email terms should cover payment method, invoicing process, payment period, and any late-payment fee.

- Send a neutral reminder once the period passes. Reference the invoice ID, due date, and agreed terms, then ask for a written status update.

- Verify confirmation against approved details. Check payment method, amount, and invoice details before changing status.

- Pause delivery factually if status is unclear. If confirmation is incomplete, send a short pause notice tied to the written terms and state what you need to resume.

- Restart only after documentation is complete. Resume when the terms, invoice records, and payment status are clear in writing. If delays repeat, require part-payment upfront for the next milestone.

Useful escalation language sounds like this:

We have not yet verified payment for invoice [ID] under the approved terms.Please share written payment confirmation so we can complete verification.Until verification is complete, this milestone remains pending and new deliverables are paused.

This keeps the discussion centered on records rather than blame.

The common relationship-damaging mistakes are predictable: accusing the client before verification is complete, restarting work on verbal assurance alone, splitting decisions across several channels without one final written record, or rewriting accepted terms in the middle of a dispute. A calm, specific message tied to what was already agreed protects both cash flow and trust.

The point is not to sound cold. It is to stay precise while the facts are still being checked. For related subcontractor controls, see Using a Data Processing Agreement (DPA) with Subcontractors. Once delayed-payment handling is clear, the next risk to get ahead of is tax and compliance.

Cover tax and compliance checkpoints before they become emergencies#

Tax trouble usually starts with incomplete records, not with one difficult filing task. Handle these checkpoints early so filing periods do not turn into cleanup emergencies.

Start with jurisdiction-specific guidance from a qualified advisor before you use this payment model at scale. Treatment of crypto income, disposals, and active trading can differ by location. In UK HMRC context, treatment can differ between investor and trader, and Capital Gains Tax can apply to disposals above the annual allowance. The cited UK 2024/25 figures are a £3,000 CGT exemption and rates of 10% and 20% by tax band.

Once you know the local treatment, keep your records aligned with how events are handled:

- Separate receipt events from disposal events. Getting paid and later selling, swapping, or converting can be treated as different tax events depending on jurisdiction.

- Export records on a recurring cadence. Save invoices, wallet transactions, and conversion records regularly, then review for unmatched entries before filing periods.

- Treat authority notices as urgent. In UK context, authorities have issued nudge letters to people known to have disposed of crypto assets.

- Recheck treatment if activity becomes frequent and active. In UK HMRC context, active trading may be treated differently from passive investing.

- Close missing-record gaps immediately. If a key payment artifact is absent, treat compliance status as incomplete and collect the missing item before filing pressure builds.

Short, regular reviews work better than quarter-end cleanup. It is easier to fix one unmatched invoice this week than ten unclear entries months later. That is especially true when you have conversions, corrected invoices, or status disputes that need to be mapped back to the original payment event.

A practical advisor handoff pack can include the invoice register with IDs and dates, a wallet receipt log mapped to invoice IDs, a conversion or disposal log mapped to receipt events, and notes on unresolved or corrected payment-status incidents.

For the U.S. context reflected here, keep in mind that IRS digital-asset guidance treats digital assets as property, income from digital assets as taxable, and many digital-asset transactions as reportable, including the Yes or No digital-asset question on the federal return. Local treatment varies, so confirm your own requirements directly.

Keep your notes plain and chronological. Clear records are more useful than elaborate formatting when you need to defend treatment later.

Start this week with a repeatable crypto payment checklist#

The goal is not a perfect policy deck. It is a sequence you can run every time, even when work is busy and billing is rushed. Use the same checklist at four points: before kickoff, when invoicing, during verification, and at closeout.

Use this operating sequence:

- Lock terms before work starts. Put scope, pricing, payment schedule, asset (USDC, USDT, or Bitcoin), network, destination address or QR code, due date, and proof-of-payment requirement in approved written terms.

- Issue invoice details in one package. Send the invoice ID, amount, asset, network, destination, deadline, and required post-transfer proof. Ask the client to confirm all items in one written reply.

- Verify before changing status. Keep the invoice pending until amount, asset, network, destination, and proof align with the written terms. If anything is missing or mismatched, pause new deliverables and request corrected records.

- Close records right after settlement. Execute your hold or convert decision, store the final proof artifacts, and export records while the timeline is still fresh.

- Review routes on a recurring cadence. Compare payout reliability, issue handling clarity, withdrawal friction, and records quality. Keep routes that pass repeatedly and replace routes that do not.

Use this weekly checklist:

- Asset agreed (USDC/USDT/Bitcoin), network agreed, destination confirmed, due date confirmed, and proof-of-payment requirement confirmed.

- Invoice issued with full metadata, client confirmation captured in writing, and release conditions documented when used.

- Payment status verified against invoice metadata before marking paid, with the evidence pack stored in one location.

- Hold or convert decision completed and recorded, with conversion records captured when conversion occurred.

- Escalation path documented for

sent but not settledcases, including required proof and pause or resume language. - Platform route performance reviewed and channel decisions updated based on observed outcomes.

Pick one active client and run this sequence end to end on the next invoice. Reliable execution on one real invoice beats a broad plan that no one follows. If you also need to tighten your operating targets before scaling this flow, revisit How to Set Financial Goals for Your Freelance Business. If you want support for your specific country or program, Talk to Gruv.

Frequently Asked Questions

How can I get paid in crypto safely as a freelancer without adding payout risk?

Define payment terms before work begins: asset, network, destination address, due date, and the exact event that marks an invoice paid. Use a dedicated receiving wallet and keep each invoice in one evidence bundle so proof and records stay together. Mark paid only after funds are visible and transfer details match invoice metadata. If status is unclear, hold delivery until the proof pack is complete.

What should I confirm with a client before accepting a crypto payment?

Confirm who approves payment, who sends it, and who handles exceptions. Then confirm asset (USDC or Bitcoin), network, destination address, invoice amount, and deadline in one written thread tied to the invoice ID. If any item changes, reissue details and reconfirm before transfer.

Is Upwork, LaborX, or CryptoTask better for getting paid in crypto?

There is no supported basis here to name one universal winner. Use controlled paid tests with the same service scope and invoice pattern, then compare payout timing, dispute clarity, withdrawal friction, and export quality. Keep routes that repeatedly meet your criteria and replace routes that do not.

Should I invoice in Bitcoin or USDC?

If steady cashflow is the priority, USDC or similar stablecoins are usually the safer choice because value is described as dollar-tied and designed to reduce large swings. Bitcoin is generally more volatile, so use explicit value-timing terms if you accept it. One practical approach is to price in fiat and settle in the agreed crypto asset.

Do I need tax tracking if clients pay me in stablecoins?

Yes. Keep clear payment and transaction records, including for stablecoin payments. In U.S. treatment, digital assets are considered property, income from digital assets is taxable, and digital-asset transactions may need reporting, including the Yes/No digital-asset question on the federal return. Local treatment differs, so confirm requirements with a qualified advisor in your jurisdiction.

What should I do if a client says payment was sent but my wallet has not received it?

Ask for the transaction hash and verify it against invoice details: asset, network, destination address, amount, and timestamp. Keep status pending until details align and receipt is visible at the agreed destination. If information is incomplete or mismatched, send a factual pause notice and resume only after written verification is complete.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 4 external sources outside the trusted-domain allowlist.

- irs.gov/filing/digital-assetstrusted

- bitrates.com/news/p/why-more-freelancers-are-getting-paid...external

- mymanagementguide.com/getting-paid-in-crypto-as-a-freelancer-or-pr...external

- nasdaq.com/articles/im-freelancer-heres-why-i-prefer-ge...external

- request.finance/crypto-freelance/how-to-get-paid-in-crypto-a...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Using a Data Processing Agreement with Subcontractors

Put your data processing agreement in place before a processor or sub-processor gets access to personal data. If you use a processor, UK GDPR guidance requires a [written contract or other legal act](https://ico.org.uk/for-organisations/uk-gdpr-guidance-and-resources/accountability-and-governance/contracts-and-liabilities-between-controllers-and-processors-multi/when-is-a-contract-needed-and-why-is-it-important). Set that contract boundary before support logins, shared folders, or troubleshooting access turn into live processing.

Vancouver Digital Nomad Guide 2026 for Long-Stay Remote Work

If you are planning a longer stay in Vancouver, make the go or no-go call before you commit to non-refundable flights, deposits, or a long lease. This guide is about remote work planning in Canada, not short-trip sightseeing. The goal is to help you validate route, documents, and budget in the right order so one weak assumption does not force a rushed decision later.

How to Set Financial Goals for Your Freelance Business

**Build your goals as repeatable policies and habits you can actually follow, not motivational slogans.** You run a business-of-one. Your job is to install a system that still works when you're busy, tired, or too close to the work to think clearly.