Quick Answer

Start with Stripe Connect for baseline connected-account verification, then add Stripe Identity only on defined risk triggers. Use one decision map for every outcome: allow, hold, or review, tied directly to payout and feature access. For early testing, the article notes Stripe’s first 50 Identity verifications are free, which supports a narrow pilot before broad rollout. Keep unresolved mechanics out of production assumptions until they are confirmed in current Stripe documentation.

Stripe Identity for Platforms in One Decision#

If you are building platform payments with connected accounts, the first step is to separate what is known from what is not.

This is not a generic debate about whether to verify users. The real architecture question is what you can decide now from confirmed pricing, and what verification behavior still needs direct validation in Stripe docs or support channels.

- Decide for the actual operating model

This guide is for CTOs, engineering leads, and solution architects who own onboarding, connected account state changes, and payout dependencies. In practice, that means you are not just collecting identity data. You are deciding which verification outcomes block payouts, delay feature access, or force manual review. Tie the decision to product actions, not vendor labels. A reliable checkpoint is to map every expected verification outcome to one of three actions: allow, hold, or review. If your team cannot explain that mapping before launch, the design is not ready.

- Treat Connect and Identity as separate decisions until mechanics are confirmed

The core decision is not "verification or no verification." It is how you will handle connected-account verification and fraud checks once you confirm product behavior from current Stripe documentation. The excerpts here do not confirm exact API mechanics, event handling, connected-account verification behavior, or supported regional patterns. Compliance checks and fraud control can overlap, but they are not the same job. A common failure mode is assuming that once onboarding passes, the fraud problem is solved. If you expect step-up checks, queue handling, or document-review evidence, plan that explicitly and verify support before payouts are live.

- Be strict about what is known versus what still needs validation

The hard boundary in the available evidence is pricing and scope. Stripe's general pricing page shows 2.9% + 30¢ per successful domestic card transaction, and Stripe states that Managed Payments adds 3.5% per successful transaction on top of standard processing fees. Those are published numbers, but they are payments pricing, not proof of Identity pricing, Connect verification behavior, or regional availability. Stripe also notes that provider fees can change, so you should recheck them before you choose. Do not let unrelated pricing pages drive your verification design. At this stage, keep the evidence pack short and practical: the exact Stripe documentation page you are relying on, the account states that affect payouts, the verification artifact you will store, and the open questions you still need to confirm with Stripe or counsel. That discipline prevents expensive rework later.

For synthetic identity detection in contractor onboarding, read How Platforms Detect Synthetic Identity Fraud in Contractor Onboarding.

Selection Criteria and Who Each Path Is For#

Choose the path by five filters, in order: KYC coverage needs, fraud-loss tolerance, onboarding conversion sensitivity, ownership of risk operations, and integration complexity. If your main goal is baseline connected-account verification and payout readiness, start with Connect-native verification. If your threat model includes synthetic identity fraud or higher-risk behavior after onboarding, plan layered controls early.

| Filter | Question | Grounded detail |

|---|---|---|

| KYC coverage needs | Do you only need baseline KYC for connected accounts, or additional trust checks at higher-risk moments? | If rules mostly track standard account verification states, Connect is the practical default. |

| Fraud-loss tolerance | How costly is a bad payout? | If the business impact of a bad payout is high, assume you will need extra controls, review handling, and stored decision artifacts. |

| Onboarding conversion sensitivity | How much friction can onboarding absorb? | Extra verification steps can reduce completion, so keep the default path lean and add step-ups only on defined triggers. |

| Ownership of risk operations | Who owns holds, retries, queue aging, and exception handling? | If no team clearly owns manual review and user messaging, stay closer to native patterns. |

| Integration complexity and pricing ownership | Do you want Stripe to set and collect processing fees from users, or do you want more control? | If you want more control, expect more fee and operations ownership; in the "You handle pricing for your users" model, Stripe lists $2 per monthly active account and 0.25% + 25¢ per payout sent. |

- KYC coverage needs

Start with the narrow question: do you only need baseline KYC for connected accounts, or do you also need additional trust checks at higher-risk moments? For many marketplaces at launch, baseline verification is the immediate requirement because it drives onboarding, feature access, and payout gating. If your rules mostly track standard account verification states, Connect is the practical default.

- Fraud-loss tolerance

KYC completion and fraud control are related but not identical. If the business impact of a bad payout is high, assume you will need extra controls, review handling, and stored decision artifacts instead of relying on baseline verification alone. If one bad payout can trigger internal escalation, design for layered controls from the start.

- Onboarding conversion sensitivity

Extra verification steps can reduce completion, so keep friction proportional to risk. For growth-sensitive onboarding, keep the default path lean and add step-ups only on defined triggers. Map outcomes to clear actions (allow, hold, review) before you add more checks.

- Ownership of risk operations

Verification only works operationally if someone owns holds, retries, queue aging, and exception handling. If ownership is unclear, blocked users and stalled reviews become product problems quickly. If no team clearly owns manual review and user messaging, stay closer to native patterns.

- Integration complexity and pricing ownership

Connect pricing is described as pay-as-you-go and capability-dependent, with options that range from offloading maintenance to taking full payments ownership. In the "You handle pricing for your users" model, Stripe lists $2 per monthly active account and 0.25% + 25¢ per payout sent; an account is "active" in any month payouts are sent to its bank account or debit card. If you want Stripe to set and collect processing fees from users, choose the path optimized for that. If you want more control, expect more fee and operations ownership.

This section is not legal or country-specific policy advice. Use Stripe Documentation and counsel for market-by-market obligations, and validate exact connected-account verification mechanics and identity.verification_report decision logic there before implementation.

For bank-debit rail choices that often sit beside identity controls, read GoCardless vs Stripe ACH vs Plaid: Which Bank Debit Rails Win for Subscription Platforms?.

Option 1 Use Stripe Connect Verification Only#

Use this path when your goal is baseline KYC completion for connected accounts and payout readiness through Stripe's native Connect flow.

Best fit#

This is a strong fit for an early-stage marketplace launching payouts in one region, where the core decision is whether the account has submitted the required verification information. Keep your implementation anchored to Stripe's Required verification information page under Platforms and marketplaces so your launch evidence is clear and auditable.

Pros#

- Fastest onboarding path with fewer system dependencies.

- Simpler product and engineering ownership when you stay close to Connect-native verification states.

- Clear operational mapping if each verification outcome drives one action: continue, hold, or retry.

Cons#

- Thin for custom trust-and-safety decisions beyond baseline onboarding and payout gating.

- Easy to over-assume KYC completion equals full fraud control.

- Exception handling still matters for document failures (for example, expired-document outcomes), even in a Connect-first setup.

Concrete use case#

A marketplace is going live in a single region, needs standard KYC gating for connected accounts, and does not yet have dedicated internal risk tooling or manual review operations.

For the payables handoff question, read Accounts Payable Outsourcing for Platforms When and How to Hand Off Your Payables to a Third Party.

Option 2 Add Stripe Identity Step-Up Checks on Top of Connect#

Use this when Connect covers baseline KYC, but you need extra proof at specific high-risk moments. Keep Connect as the default path, then invoke Identity only when your suspicious-activity checks justify escalation.

Best fit#

This option fits growth-stage teams that want stronger fraud controls without forcing every user through document checks. Stripe Identity is positioned to programmatically confirm identity to help prevent fraud while minimizing friction, so it works best as a selective step-up layer, not a full replacement for Connect.

Pros#

- Stronger trust signals for risky actions by reviewing

identity.verification_reportoutcomes. - Support for document-based checks, including verified examples for

"type": "passport"and"type": "id_card". - A practical pilot path, since Stripe states the first 50 verifications are free.

Cons#

- More product and ops complexity once you add escalation logic.

- You need clear handling for failed checks, including cases like

"code": "document_expired". - Extra implementation work to test connected-account scenarios and ensure results reach the right decision point.

Concrete use case#

A common pattern is: run standard onboarding with Connect, then require an Identity document check before a withdrawal when suspicious-activity checks fire. Review the identity.verification_report and map the result to one action: proceed, hold, or route to review.

For an Australia-specific compliance branch, read Australian GST for Digital Platforms When to Register and Remit.

Option 3 Keep Connect for KYC and Add a Separate Risk Layer#

Use this option when Connect onboarding is necessary but not sufficient for your risk model. Connect can stay your baseline KYC path, while your own scoring and review logic decides which accounts are held, reviewed, or blocked before high-value platform payments are enabled.

Best fit#

This is best for mature platforms with a real risk operations function and measurable synthetic-identity exposure. The advantage is policy control: you can set different escalation thresholds by marketplace, business line, or region instead of forcing every account through one path.

The tradeoff is operational burden. You need tight alignment between Connect states and internal controls, or you create policy drift where an account looks approved in one system and restricted in another.

What changes in practice#

Your core requirement is an explicit decision map between Connect status and internal risk status across product logic, ops queues, and user messaging.

If you use Stripe Identity in this layer, treat identity.verification_report as one input, not your whole policy. Stripe positions Identity to "programmatically confirm the identity of global users so you can prevent attacks from fraudsters while minimizing friction," and sample outcomes include "status": "unverified" and "code": "document_expired". Your team should define retry handling, failure handling, and clear action rules for those outcomes.

Keep an evidence pack for each escalated decision:

- connected account ID and current Connect onboarding state

- internal trigger or score that caused escalation

identity.verification_reportoutcome and failure code (if present)- reviewer notes, final action, and decision timestamp

Concrete use case#

A practical pattern is a multi-region platform that uses Connect for baseline KYC, then runs proprietary scoring before enabling higher-value payments. Lower-risk accounts proceed, while stronger fraud signals route to manual review before payment access is granted.

Pilot on a narrow slice first. If Identity is part of the stack, Stripe states the first 50 verifications are free, which is useful for testing trigger quality before broad rollout. Keep legal interpretation separate from risk policy, since Stripe's public legal content says it is not legal advice. For teams seeing synthetic-identity patterns, see Synthetic Identity Fraud: What Payment Platforms Must Know.

For payout holds tied to tax documentation, use FATCA and W-8 Tax Compliance for Platforms: When to Release, Hold, or Withhold Foreign Payouts.

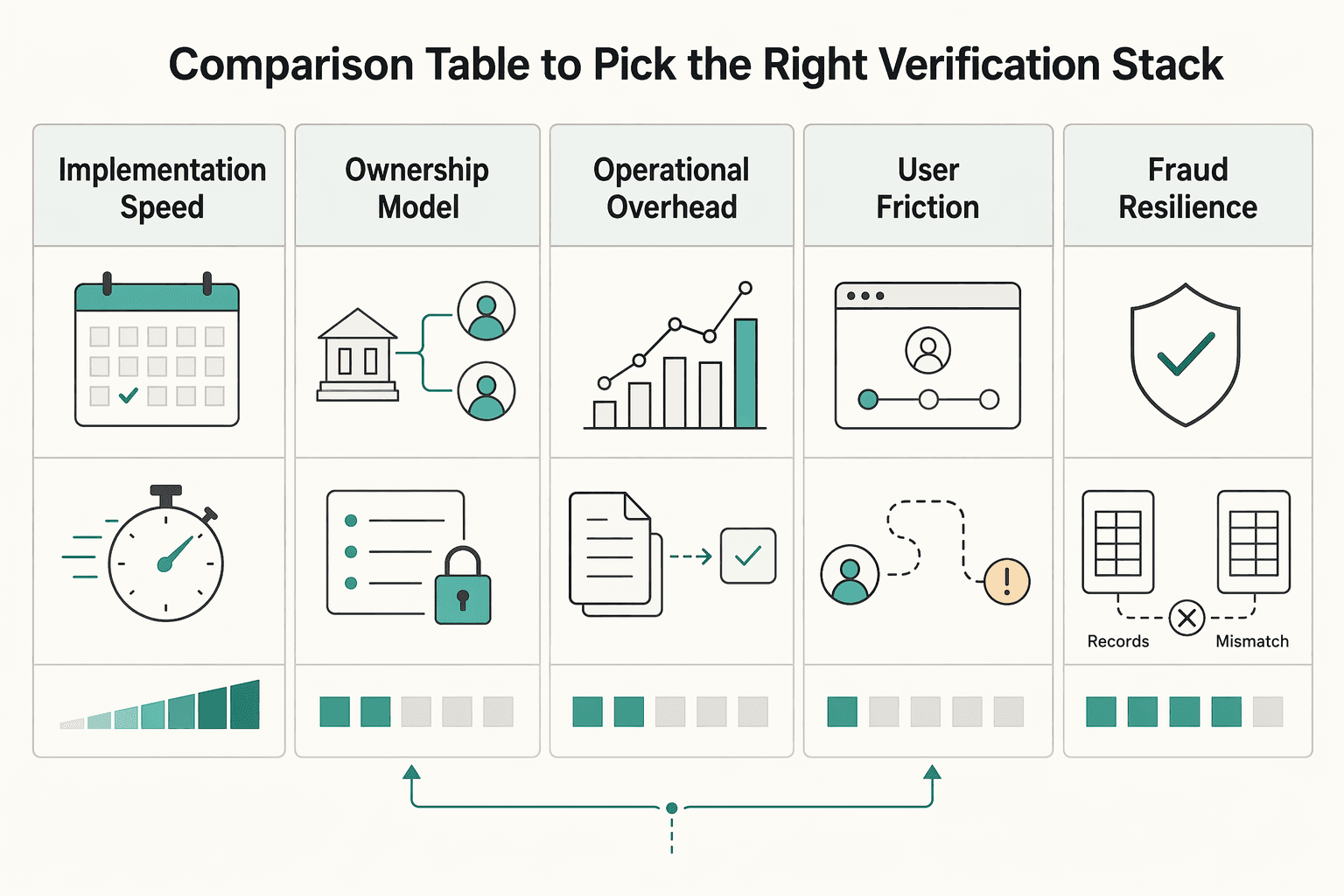

Comparison Table to Pick the Right Verification Stack#

Start with Connect-only if speed is your priority, then add controls only when your own suspicious-activity checks show clear gaps. Stripe's documented position is that Connect can help you go live faster with hosted or embedded functionality, including a "weeks instead of quarters" implementation path. What Stripe documentation does not decide for you is your internal review policy, escalation rules, or product-side hold/review/release logic.

| Comparison point | Option 1 Connect only | Option 2 Connect plus Identity step-up | Option 3 Connect plus separate risk layer | Confirmed vs validate |

|---|---|---|---|---|

| Implementation speed | Fastest path if you stay close to Stripe-hosted or embedded onboarding. | Slower than Option 1 because you add trigger logic, messaging, and retry paths. | Slowest because you add internal scoring, queues, and review operations. | Confirmed from Stripe docs: Connect is positioned for faster go-live with hosted/embedded functionality. Validate with Stripe support: program-specific setup when adding Identity or custom review steps. |

| Ownership model | More onboarding surface is handled through Connect; your team maps outcomes to access/payout behavior. | Shared ownership: Connect baseline plus your trigger and decision logic. | Highest internal ownership: your team governs hold/review/release decisions. | Confirmed: Connect provides onboarding and embedded components. Validate: exact boundary between Stripe-managed and platform-managed controls for your setup. |

| Operational overhead | Lowest ongoing ops load. | Medium: more exception handling and support workflows. | Highest: manual review and policy maintenance become continuous work. | Confirmed: Stripe says tooling can reduce extra dedicated merchant-fraud resources. Validate: actual team load after step-up and review policy are in place. |

| User friction | Lowest friction. | Higher but more targeted if escalation is narrow and event-driven. | Variable to high, depending on how aggressively you escalate. | Validate internally: where verification appears and how often legitimate users are interrupted. |

| Fraud-resilience depth | Baseline onboarding/KYC posture. | Stronger control at selected risk points. | Deepest control because you combine Connect outcomes with internal review policy. | Confirmed: Connect is positioned for onboarding plus merchant-fraud-related tooling. Validate: Identity capabilities and any review artifacts you depend on. |

| Best for | Teams optimizing for fast launch and simpler operations. | Teams that need targeted fraud checks without standing up full manual review. | Teams with established risk operations and segment-specific policy needs. | Decision guidance, not an official Stripe classification. |

| Main risk if misused | Assuming onboarding completion equals full fraud control. | Over-triggering step-up checks and creating unnecessary friction. | Policy drift: account appears complete in one system but blocked in another. | Validate internally: support, ops, and product should be able to explain each hold/block clearly. |

| First escalation trigger | Usually none beyond baseline onboarding. | A defined suspicious event triggers fraud-prevention review. | A defined event or internal score routes to manual review before sensitive actions. | Stripe docs do not define your internal trigger thresholds; set and test them in your program. |

| Artifacts to plan for | Connected-account onboarding outcomes and your mapped product states. | Same baseline artifacts, plus (if enabled for your program) review artifacts you choose to use, such as identity.verification_report and document-check flows (for example, passport or driving license). | Same as Option 2 plus internal evidence linking account status, risk reason, reviewer decision, and timestamp. | Validate with Stripe docs/support: exact identity.verification_report fields, document support, and connected-account state-transition semantics for your program. |

Checkpoint before committing: define the exact event that moves an account from allow to hold to review, and make sure your product can show that reason clearly to the user. If that is vague, Option 2 or 3 will cost more operationally than expected.

Keep one caveat visible: you may see third-party summaries of Standard, Express, and Custom account types. Treat those as directional until you confirm account-type behavior and rollout-critical details directly in Stripe documentation or with Stripe support.

For database controls that support payment-platform evidence, read Database Architecture for Payment Platforms: ACID, Sharding, and Read Replicas.

Implementation Sequence That Avoids Platform Debt#

Use a strict sequence: ship baseline onboarding and payout gating first, then add targeted step-up checks, then add manual review.

| Phase | Primary action | Grounded note |

|---|---|---|

| Phase 1: Connect-first baseline | Map onboarding outcomes to product status and payout eligibility. | Stripe Standard pricing is presented as pay-as-you-go with no setup fees, monthly fees, or hidden fees; domestic cards are listed at 2.9% + 30¢ per successful transaction. |

| Phase 2: Targeted Identity step-up | Add Identity only for predefined triggers and build clear failure states, idempotent retries, and a handoff path to risk operations. | The pricing sources do not confirm Identity API mechanics, retry behavior, or report-field handling; Managed Payments is listed at 3.5% per successful transaction in addition to standard payment processing fees. |

| Phase 3: Manual review with evidence packs | Keep the verification artifact, trigger event history, and final decision log together. | Introduce manual review only after automated outcomes are stable and you can name which cases truly need escalation. |

| Verification checkpoint before scaling | Map every verification outcome to allow, hold, or review. | Recheck fee assumptions as you scale; Stripe notes gateway-related costs can change, and Managed Payments examples include 2.99% to 5.99% for some methods. |

- Phase 1: Connect-first baseline. Start with Connect for connected accounts and keep scope tight: map onboarding outcomes to product status and payout eligibility. The goal is a small set of states your team can explain consistently before adding more paths.

Keep pricing context in view while you scope this phase. Stripe Standard pricing is presented as pay-as-you-go with no setup fees, monthly fees, or hidden fees, and domestic cards are listed at 2.9% + 30¢ per successful transaction. Treat that as launch-cost context, not a reason to skip clean status and payout decision mapping in your own product.

- Phase 2: Targeted Identity step-up. Add Identity only for predefined triggers (for example, risky account changes, payout activation, or other events you define). Build clear failure states, idempotent retries, and a handoff path to risk operations when retries are exhausted.

If your program exposes artifacts such as identity.verification_report, attach them to the account or case record so decisions are traceable. Also keep the limit clear: the pricing sources do not confirm Identity API mechanics, retry behavior, or report-field handling, so validate those implementation details directly before hardening.

Cost discipline still applies here. Managed Payments is listed at 3.5% per successful transaction, and Stripe states this is in addition to standard payment processing fees.

- Phase 3: Manual review with evidence packs. Introduce manual review only after automated outcomes are stable and you can name which cases truly need escalation. For each reviewed case, keep the verification artifact, trigger event history, and final decision log together.

If synthetic identity risk is in scope, this evidence pack is what keeps reviews consistent across engineering, risk operations, and support. See also Synthetic Identity Fraud: What Payment Platforms Must Know.

- Verification checkpoint before scaling. Scale traffic only after every verification outcome maps to one product action: allow, hold, or review. This catches undefined edge states, duplicate retry behavior, and user-facing messaging mismatches early.

Recheck fee assumptions as you scale. Stripe notes gateway-related costs can change, and Managed Payments examples include variable ranges such as 2.99% to 5.99% for some methods.

For a step-by-step walkthrough, see Net Payment Terms for Platforms: How to Offer Net 30 60 90 and When to Use Each.

Failure Modes That Break Trust and Throughput#

Most breaks in trust and throughput come from implementation choices, not one failed check. The pattern is predictable: teams blur verification and fraud decisions, leave ownership ambiguous, and ship flows before coverage is confirmed.

-

Treating KYC completion as full fraud control. Passing Know Your Customer (KYC) checks is not the same as solving fraud risk. Stripe's fraud guidance explicitly flags false positives as a real design consideration, so keep identity verification outcomes separate from fraud, payout-timing, and review decisions.

-

Missing ownership boundaries for review work. Queues stall when product defines triggers, engineering emits events, and risk operations has no explicit intake rule. Define one handoff path per verification result so each case has one owner and one next action.

-

Document-failure UX that traps legitimate users. Failed driving license or ID card attempts should lead to a clear recovery path, not vague messaging and duplicate retries. Keep progress intact, show a clear retry state, and prevent multiple parallel cases for the same user action.

-

Rolling out on assumptions instead of confirmed coverage. The Stripe page in scope is for Identity verification for connected accounts, but this excerpt does not fully confirm regional limits, program coverage, or document acceptance rules. If Stripe Documentation leaves a country, account type, or document path unclear, pause rollout assumptions and confirm before launch.

The Practical Recommendation for Most Platform Teams#

For most platform teams, start with Connect for onboarding and verification, then add Identity only where clear risk signals justify extra friction. This keeps the core flow simpler and aligns with Stripe's own framing: onboarding/verification and risk/support are separate operating jobs.

- Start with Connect, and make product actions explicit

Use Connect as your first layer, then map each verification outcome to a clear product action (allow, hold, or review). Keep those mappings visible to product, engineering, and support so the same case is handled the same way across teams.

- Add step-up checks only behind written trigger rules

If risk pressure grows faster than your ops capacity, prioritize the step-up model (Option 2) before jumping to a fully custom risk stack. Keep trigger rules simple enough that an operator can explain each hold or review decision in one sentence, and tighten rules if similar cases produce different outcomes.

- Maintain a known-vs-unknown log tied to Stripe Documentation

Treat this as architecture hygiene, especially across markets. Stripe's materials separate compliance, FX, and settlement concerns, and the Services Terms also state that the services list is not a country-availability guarantee, so confirm country/program availability in Stripe Website/Documentation before locking decisions. Keep a lightweight log with: decision, what documentation confirms, what is still unknown, and owner.

For 1099 and W-8 routing around foreign contractors, read When Platforms File 1099 for Foreign Contractors and When W-8 Applies.

Frequently Asked Questions

What is Stripe Identity for platforms?

Here, Stripe Identity for platforms is a shorthand for using identity checks during onboarding or step-up review for connected accounts. The excerpts provided here do not define Identity’s full scope or a required architecture, so treat implementation details as decisions to confirm in current Stripe documentation.

Is Stripe Connect required for connected account verification?

Based on the public evidence used here, you should not say Connect is strictly required. What is supported is that Connect gives you different options to integrate payments into your product, with different ownership levels, and Stripe publishes connected-account pricing there. If your design assumes Connect is mandatory for every verification path, confirm that in Stripe documentation before you hard-code the architecture.

When is Connect verification enough on its own?

The excerpts here do not establish a universal point where Connect verification is enough on its own. What is evidenced is that Connect offers multiple integration approaches with different ownership levels and pricing models. Use your compliance and risk requirements, then confirm the exact verification path in current Stripe documentation.

When should a platform add extra verification or risk controls?

The excerpts here do not provide a prescriptive trigger list for adding extra verification or risk controls. Add controls when your internal risk or compliance thresholds require more than the default flow, and document those thresholds clearly before implementation.

Does Stripe Identity improve onboarding conversion while supporting fraud prevention?

The excerpts here do not prove a measured onboarding-conversion lift from Stripe Identity or quantify fraud-impact outcomes. Treat that as a product hypothesis and validate it with your own completion, retry, and risk metrics before making commitments.

What is publicly known about Stripe Identity pricing from current SERP evidence?

There is no supported Identity-specific price in the evidence provided here, so do not budget from guesswork. What is public: Stripe standard pricing says there are no setup, monthly, or hidden fees and shows 2.9% + 30¢ for domestic card transactions. Connect also shows a $2 per monthly active account model plus 0.25% + 25¢ per payout sent, where an account is active in any month payouts are sent to its bank account or debit card. Stripe also says there can be "No fees for your platform" in the Connect setup where Stripe handles pricing for users. For Managed Payments scope, support content says there is a 3.5% fee per successful transaction in addition to standard Stripe payment processing fees, and country payment-method pricing pages can supersede listed fees. Stripe’s own fee explainer says costs are subject to change, so recheck live pricing pages before you commit.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- codes.ohio.gov/ohio-administrative-code/chapter-3342-5trusted

- docs.stripe.com/connect/identity-verificationtrusted

- docs.stripe.com/identity/verify-identity-documentstrusted

- dot.ca.gov/-/media/dot-media/programs/design/documents/...trusted

- hammer.purdue.edu/ndownloader/files/60391775trusted

- leginfo.legislature.ca.gov/faces/billCompareClient.xhtmltrusted

- sandiego.gov/sites/default/files/2025-08/k-25-2371-db2-3-...trusted

- sec.gov/Archives/edgar/data/1141391/0001193125051859...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

What Payment Platforms Must Know About Synthetic Identity Fraud

For cross-border payouts, your job is to set enough control depth to reduce synthetic identity abuse without turning contractor, seller, or creator onboarding into needless manual drag.

GoCardless vs Stripe ACH vs Plaid for Subscription Platform Rails

This is not a brand pick. It is an operating-model decision for recurring payments on bank rails. At the role level, these options are not interchangeable:

How Platforms Detect Synthetic Identity Fraud in Contractor Onboarding

Contractor onboarding is the control point because it gives you an early chance to challenge identity before broader account access raises the stakes. If a synthetic or impersonated profile clears that gate, later remediation gets slower and harder to manage.