Quick Answer

Start by locking role ownership for each channel, then decide registration and remittance at the legal-entity level. In Australia, GST is 10%, but the key controls are buyer classification, threshold monitoring, and evidence tied to invoice or transaction IDs. Use ABN-plus-declaration records for business treatment, escalate supplier-of-record conflicts, and reconcile transaction totals to ledger and BAS or quarterly return data before lodgment.

Australian GST decisions that break digital platforms#

For digital platforms, Australian GST starts with a fixed 10% rate, but you still need a clean role map and records you can retrieve later. We start by mapping the transaction correctly. Then you classify the buyer, test whether you need to register for Australian GST, choose the registration model your team can actually run, and set up how you will remit Australian GST from records you can pull on demand.

We wrote this guide for compliance, legal, and finance owners who need a practical Australian GST decision path: when you may need to register, where your remittance responsibility may sit, what you need to lodge, and when you should escalate.

Step 1 Define the decision before tax treatment#

Before you decide GST treatment, confirm three basics for each channel: who the legal seller is, who controls the payment flow, and whether an electronic distribution platform (EDP) is involved. If those answers come from assumptions rather than contracts, checkout design, and settlement reality, fix the role map first.

Step 2 Set scope tightly#

This guide is limited to imported services and digital products sold to Australian consumers, especially where a platform sits between seller and customer. In ATO terms, that sits within sales connected with Australia where GST can apply.

Within that scope, you are usually deciding who must act and whether the entity should use Standard GST registration or Simplified GST registration. According to the ATO guidance cited here, the registration turnover threshold is A$75,000, or A$150,000 for non-profit organisations. The same guidance says you need to register within 21 days once the obligation is triggered.

Do not force one answer across every channel. Two flows can look nearly identical to a customer and still raise different GST responsibility questions.

Step 3 Use this as an operating guide, not legal advice#

This is an operating guide, not legal advice. It does not replace current ATO procedural guidance. The ATO specifically points readers to EDP responsibility guidance, which means remitter outcomes can turn on details this article cannot settle for your exact fact pattern.

Use a simple escalation rule: if responsibility is unclear between entities for the same flow, document the uncertainty and escalate before invoicing and filing logic are locked.

Step 4 Leave with five working artifacts#

By the end, we want five working artifacts in place:

| Artifact | Contents |

|---|---|

| Role map | seller, EDP involvement, payment-flow owner, and relevant non-resident entity |

| Buyer-classification rules | internal data requirements before treating a buyer as business or consumer, with edge cases escalated |

| Registration decision log | threshold view, chosen registration path, and rationale |

| Evidence pack | tied to transaction or invoice identifiers |

| Remittance checklist | pre-lodgment and payment checks |

If you cannot support a conclusion from records, treat it as provisional and escalate.

Related: ASC 606 for Platforms: How to Recognize Revenue When You're the Merchant of Record.

Start with your Australian GST perimeter and role map#

Get the Australian GST role map right before you make any tax call. We treat each digital platform revenue stream as its own fact pattern and confirm which entity and role you are assessing.

Step 1 Build a one page matrix for each revenue stream#

Do not use one master row for all Australian sales. Split by channel and checkout path, because similar buyer experiences can still produce different role questions. At minimum, include:

- Revenue stream or channel name

- Contracting entity shown to the customer

- Legal seller

- Merchant of Record (MoR), if any

- Electronic distribution platform (EDP), if any

- Payment flow owner, meaning who takes payment first

- Settlement recipient

- Evidence links: contract, checkout screen, invoice sample, settlement report

Use one verification rule across the matrix: each row must tie to a real contract and a sample transaction ID. If either is missing, treat the row as a hypothesis, not a decision.

Step 2 Separate merchant roles from intermediary roles#

For your Australian GST analysis, do not mix flows where your non-resident entity is the merchant with flows where it only intermediates, even if the buyer-facing brand is the same.

That split matters when you assess registration paths. The ATO simplified pathway expressly covers non-resident businesses, including merchants and EDP operators. That is a strong signal that role mapping comes before treatment. It does not, by itself, resolve remitter responsibility for every multi-entity sale.

If one row says your entity is both the legal seller and only an intermediary, stop there and fix the row before moving on.

Step 3 Name the channel, not just the business model#

In working papers, name the actual channel: direct checkout, Google Play, Apple App Store, Amazon Kindle, not a generic tag like "marketplace flow." Use those labels to keep evidence organized, not as a shortcut to GST liability conclusions. For each named channel, attach the supporting evidence set:

- Customer or seller terms

- Store or distribution agreement

- Settlement statement

- Invoice or receipt format

- Checkout and post-purchase screenshots

This helps you avoid collapsing all digital revenue into one GST conclusion before the channel contracts have been reviewed.

Step 4 Freeze GST conclusions until legal and finance sign off#

Do not treat any GST decision as final until legal and finance sign off on the role map for that flow. That is an internal governance rule, not an ATO legal requirement, but it is useful.

Record at least the channel name, approved roles, approvers, approval date, and any open issues. If registration has already happened, store the registration artifact with the row as well. For standard registration, that means the ATO written notice with the effective date. For simplified registration, it means the 12-digit ARN.

Do this early. Once registration is required, the ATO says you must register within 21 days, and unresolved ownership questions can burn through that window quickly.

For a side-by-side view of digital marketplace GST rules in Australia, Canada, and India, see GST Digital Marketplace Platform Comparison for Australia, Canada, and India.

Classify the buyer before you classify Australian GST#

Your buyer-classification rule should drive the Australian GST branch before you lock invoicing and remittance. Define that test before you decide the tax outcome.

Step 1 Define the buyer test in two separate gates#

Treat Australian consumer as a policy term, not a billing-country shortcut. Write the test in two gates. First, determine whether the buyer is treated as Australian under the definition approved by tax and legal. Second, determine whether the buyer should be treated as business-side based on GST registration and business-use conditions in your policy.

Keep those gates separate on paper. For the scope covered here, the ATO position is that Australian GST-registered businesses importing services or digital products generally should not be charged GST, while businesses that are not GST-registered need to pay GST on those purchases. If your policy collapses that into one proxy rule, treat it as a control defect.

Step 2 Build the B2B branch around ABN plus declaration evidence#

For B2B treatment in your policy, capture an Australian Business Number (ABN) and the buyer declaration evidence your tax team requires. An ABN field on its own is not enough.

The point here is narrower. In relevant overseas-supplier cases, the ATO says the business purchaser determines whether GST is payable. Your record therefore needs to show why the buyer was accepted into the business branch, not just that an ABN was entered.

Store the ABN, declaration version, timestamp, account ID, and order or invoice ID together. If the record is incomplete, send it to an exception queue before treatment is finalized.

Step 3 Define explicit checkout or onboarding fields#

Capture the classification signals directly instead of inferring them from payment data alone. At minimum, capture the residency and business-use signals your policy depends on, plus ABN and related business details where your B2B branch needs them.

Treat missing fields as exceptions, not silent defaults. Then run an end-to-end transaction sample so those fields appear in the tax engine output and invoice records, not just in front-end logs.

Step 4 Escalate conflicts before invoicing treatment is locked#

As an internal control, treat conflicting signals as a review trigger before classification is finalized. Billing country, card country, IP, and device indicators can be operational clues, but they are not a substitute for your approved policy test.

Set a red-flag rule for conflicts between declared status and operational signals, and resolve them before invoice logic is locked. This matters even more if the remitting entity uses simplified GST registration, because that path cannot issue tax invoices or claim GST credits.

Decide if Australian GST registration is triggered and who should register#

Once the buyer branch is clear, make the next decision explicit: is GST registration required, and which legal entity is the candidate registrant for each flow? If you assess this only at group level, you can miss the trigger or assign it to the wrong party.

Step 1 Build a threshold tracker by entity and supply type#

Track this at the legal-entity level, then by supply model. Use GST turnover for the test, meaning gross income from all businesses minus GST, not a generic management revenue view. At minimum, track:

- legal entity

- channel and supply type

- whether sales are treated as connected with Australia

- buyer branch used

- turnover counted toward the registration test

- source report and reconciliation reference

Keep direct non-resident merchant sales separate from marketplace or EDP flows unless tax and legal confirm they belong in the same registration analysis.

Use threshold values as controlled inputs, not permanent assumptions. In scope here, the cited figures are A$75,000, or A$150,000 for non-profit organisations. Add a mandatory current-page check before each formal decision, including the ATO page URL and last-updated date, which in these materials is 11 September 2025.

Step 2 Assign the candidate registrant from your role map#

Do not pick the registrant based on brand ownership or on who happens to collect cash first. Tie it back to the flow-level role map.

In some flows, the non-resident merchant may be the candidate registrant and remitter. In others, the EDP structure may change that analysis. What the materials support clearly is that simplified registration is available to non-resident businesses, including merchants and EDP operators. Log the candidate entity for each flow, and avoid blanket statements like "the platform will register."

Step 3 Escalate any two-entity supplier question before locking treatment#

If two entities could plausibly be the supplier of record, escalate immediately and pause final GST treatment for that flow. The ATO excerpts in scope do not give you a universal tie-breaker for every merchant, MoR, and EDP structure, so this needs to be controlled internally.

Freeze the interim assumption in writing:

- temporary candidate registrant

- affected transaction set

- missing evidence

- approver and decision date

Step 4 Record legal basis and start the compliance clock when triggered#

Your decision log should record the basis used: sales connected with Australia and the requirement to register when the relevant enterprise and turnover conditions are met. For each in-scope flow, link the internal legal memo or reference you rely on to the role map and buyer-classification rule.

Once you decide registration is required, start the compliance clock. Complete registration within 21 days, and account for penalties if you fail to register when required.

Choose the Australian GST registration model your operating model can support#

When registration is triggered, choose the Australian GST model your finance and invoicing process can actually support cleanly. The tradeoff is practical: if you need GST credits or tax invoices in practice, assess Standard GST registration first, because Simplified GST registration supports neither.

Step 1 Match the model to the operating need first#

Start with operating need, not setup speed. The grounded differences are:

| Model | What the source guidance supports | Identity / operations signal |

|---|---|---|

| Simplified GST registration | For non-resident businesses making in-scope Australia-connected consumer sales, including imported services and digital products, and low value imported goods at A$1,000 or less. | You do not need an ABN. After registration, the ATO issues an ARN, which is 12 digits. You cannot claim GST credits or issue tax invoices. |

| Standard GST registration | For non-residents entitled to or holding an ABN, including cases where claiming GST credits matters. | An ABN is required before registration. BAS lodgment and payment are monthly or quarterly. |

| Standard claim only GST registration | Not defined in the provided excerpts. | Treat this as a separate validation item, not as interchangeable with the two models above. |

Step 2 Run the two hard tradeoff tests before committing#

First, do you need GST credit recovery? If yes, simplified is usually the wrong fit because a limited registration entity cannot claim GST credits.

Second, do you need tax invoices in your billing flow? If yes, simplified is usually the wrong fit because it cannot issue tax invoices.

A common failure mode is choosing simplified because it looks administratively easier, then discovering that finance expected credits or tax-invoice behavior that the model does not support.

Step 3 Lock identity and filing implications at decision time#

Capture the identifier consequence immediately. Simplified uses an ARN, not an ABN. Standard requires an ABN before registration. Capture the filing cadence at the same time:

- Simplified: GST returns and payments are quarterly.

- Standard: BAS lodgment and GST payment are monthly or quarterly.

Keep registration evidence from day one, including the issued identifier and, for standard registration, the effective date. For standard registration, require the ATO written notice of registration details, including the effective date, before you treat mapping and compliance setup as final.

Step 4 Set change control before anyone switches models#

Do not let teams switch models casually. Require tax-owner approval and a downstream impact review before a change is made. At minimum, review:

- identifier handling, including ARN versus ABN

- document behavior, including tax-invoice expectations

- filing process and cadence, including quarterly simplified returns versus BAS

Also surface operating friction early. For standard registration, electronic lodgment is not available from outside Australia, and an Australian registered tax agent may be needed. If registration is required, keep the 21-day statutory timing in view, because penalties may apply for failing to register when required.

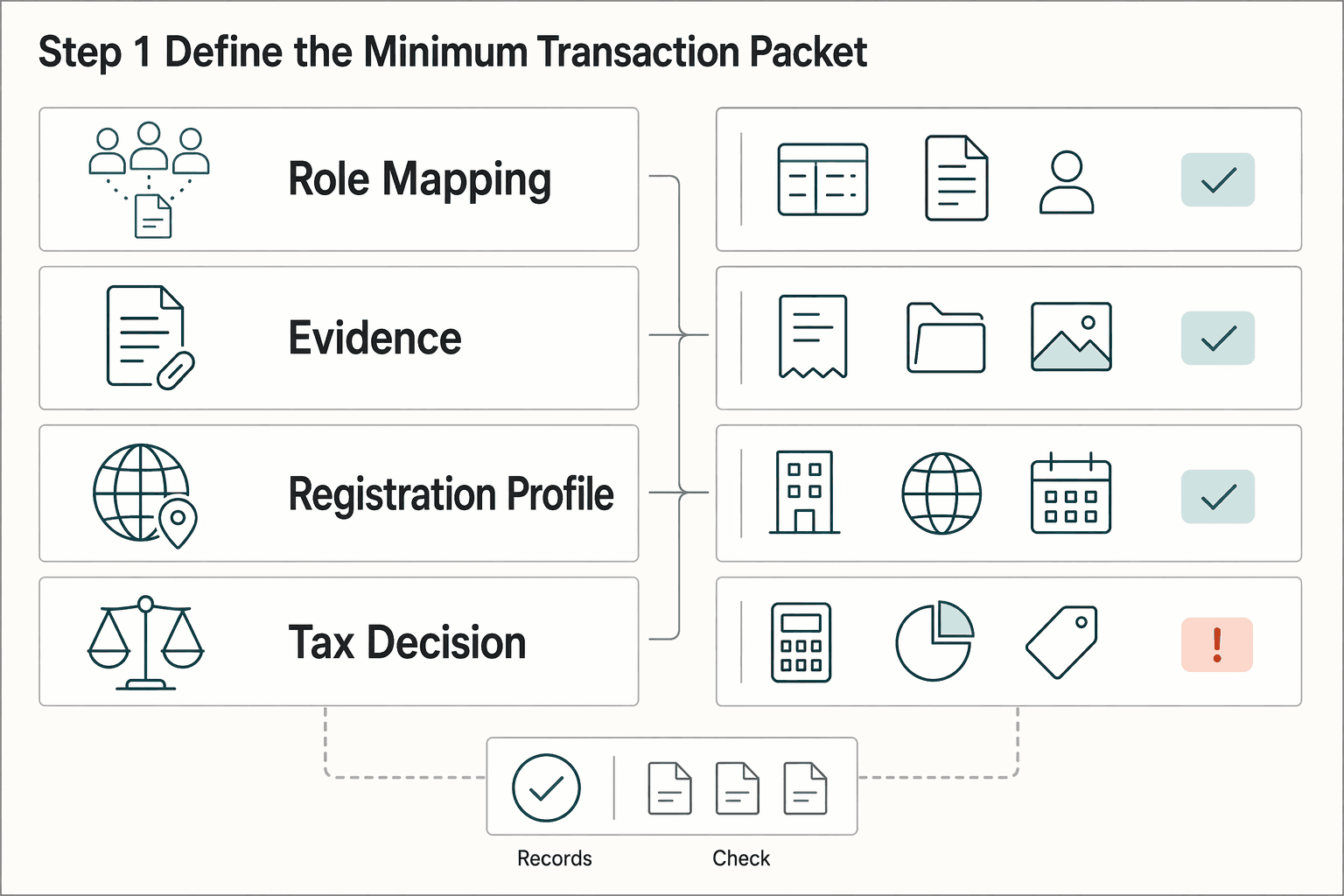

Build the minimum evidence pack for every taxable and non-taxable sale#

For every sale treated as taxable or outside scope, keep enough evidence to recreate the tax decision as it stood at the time of sale.

Step 1 Define the minimum transaction packet#

Set one internal packet that must exist for each sale before it enters GST reporting. This is not an ATO-prescribed checklist, so keep it tight and consistent.

| Evidence item | What to store | Why it matters |

|---|---|---|

| Role mapping reference | The approved scenario or flow ID used for that transaction | Shows how supplier and remitter treatment were assigned |

| Buyer classification evidence | The checkout or onboarding data used to assess consumer versus business treatment | Supports why GST was charged or not charged |

| Business identifier records | Where your process relies on business identifiers or declarations, retain the exact record used at the time | Supports business-versus-consumer treatment decisions without assuming one universal test |

| Registration profile | Registration model, identifier, and effective date for the seller entity | Distinguishes ABN-based standard records from ARN-based simplified records |

| Tax decision timestamp | Date and time of the tax outcome, plus decision source or rule version | Shows which controls were in force when the decision was made |

Do not rely on invoice PDFs alone. Keep the invoice or receipt with the classification data and registration context used on the sale date. As a quick checkpoint, pick one recent transaction and confirm all five items are retrievable in under five minutes.

Step 2 Key evidence to the transaction#

Evidence should be traceable from transaction to filing, not rebuilt later from a side spreadsheet. Store records against stable keys such as invoice ID, payment ID, order ID, or refund ID.

Use one sale-level record with linked artifacts so finance and tax can both drill from filing lines back to source data. For standard registration, retain the ABN and BAS cadence, monthly or quarterly. For simplified registration, retain the ARN and quarterly return and payment context.

Checkpoint: trace one draft filing line back to the source transaction and confirm the identifier matches the entity's active registration model.

Step 3 Retain exception decisions, especially non-taxable outcomes#

Non-taxable decisions need explicit retained reasons. Avoid a generic "non-taxable" bucket with no decision context behind it.

For each exception, keep a short reason, the supporting evidence state, and the decision timestamp. If the treatment relied on a business identifier or declaration, retain the exact record used at that time, not just a refreshed value pulled later. As a checkpoint, review a small sample of non-taxable sales and confirm each reason is understandable without asking the original analyst.

Step 4 Sample-test completeness before filing#

Before filing, test evidence completeness against the population being reported. Under standard registration, sample from BAS preparation. Under simplified registration, sample from the quarterly GST return population.

The material here does not prescribe a sampling percentage, so set an internal method and use it consistently. The goal is supportability: each sampled line should tie back to a sale record with buyer-classification evidence and the correct registration context, ABN for standard or ARN for simplified.

Checkpoint: do not approve a BAS or quarterly return until sampled gaps are resolved, documented, or assigned to an owner for follow-up.

For a step-by-step walkthrough, see Accounts Payable Outsourcing for Platforms When and How to Hand Off Your Payables to a Third Party.

If you need a control baseline for audit-ready records and reconciliation, use our docs to map evidence references, ledger postings, and payout status flows into your GST process.

Set Australian GST remittance operations that survive month-end pressure#

Remittance has to survive month-end pressure. Build it as a controlled cycle, not a last-minute filing task. We anchor it to the registration model first, then run reconciliation and payment approval inside that same cycle.

Step 1 Build the calendar from your registration model#

Start with the filing model you are actually on. Under Standard GST registration, the entity lodges a Business Activity Statement (BAS) and pays GST on a monthly or quarterly cadence. Under Simplified GST registration, the entity lodges GST returns and pays GST quarterly, with returns lodged online at the end of each quarter.

Turn that into a calendar with clear owners for invoice or receipt tax treatment, reconciliation cutoff, draft return or BAS preparation, and payment authorization. Keep identifiers consistent in every handoff: ABN for standard registration, or the 12-digit Australian reference number (ARN) for simplified registration.

Before each cycle, confirm the entity's registration model, identifier, and effective date against the ATO registration details on file. For standard registration, retain the written ATO registration notice showing the effective date.

Step 2 Reconcile three views before lodgment approval#

Before anyone approves lodgment or payment, reconcile three views: transaction-system totals, ledger totals, and draft GST return or BAS totals. If they do not align, treat that as a data or process issue to resolve first.

Use consistent cutoff logic across all three views so the variances mean something. Record the population window, entity, registration model, and source reports used for the cycle.

Verification point: trace one draft BAS or simplified return line back to ledger totals and then to source transactions, and confirm the same ABN or ARN is used across all layers.

Step 3 Control late data with an adjustment log#

Late data will happen. Control it explicitly instead of letting it disappear into close notes.

Log each late item with the owner, root cause, affected period, discovery date, and a documented correction path for a later filing cycle, with links to the underlying sale or refund evidence. That keeps adjustments visible and supportable instead of being reconstructed from memory in the next close. Repeated root causes should be treated as process defects, not normal exceptions.

Step 4 Validate cadence and lodgment path each cycle#

Treat filing cadence and lodgment path as controlled settings. Revalidate them each cycle against current ATO requirements for the registration type rather than relying on a static SOP.

For mixed-model operations, keep the distinction explicit: standard GST uses BAS on a monthly or quarterly cadence, while simplified GST is quarterly online. Also account for the standard-registration constraint that a non-resident cannot lodge electronically from outside Australia and may need an Australian registered tax agent.

At cycle start, require tax-owner signoff on registration type, cadence, lodgment path, and payment approver.

Define escalation triggers before edge cases hit production#

Do not wait for production issues to tell you where the edge cases are. We set escalation rules now so unclear role ownership, buyer status, or registration timing gets paused and reviewed before the pattern scales.

| Escalation case | Required detail |

|---|---|

| Role dispute | contracting entity, checkout seller display, payment descriptor, and current registration identifier |

| Unclear buyer status | transaction ID, captured buyer fields, any ABN collected, the declaration text shown, and the approver for any temporary treatment |

| Threshold proximity | escalate as soon as threshold tracking shows an entity could move into required registration within the same reporting period |

| Escalation ownership | primary decision owner, backup approver, and written SLA for triage, evidence collection, and signoff |

Step 1 Escalate role disputes immediately#

Escalate any mismatch in who appears responsible for GST. If the contract, checkout seller display, payment flow, or Merchant of Record role points to different entities, treat GST role ownership as unresolved.

Use a four-way verification check: contracting entity, checkout seller display, payment descriptor, and current registration identifier. For standard GST, verify the ABN and the ATO registration notice with the effective date. For simplified GST, verify the 12-digit ARN. If those records do not align, route the issue to tax and legal before invoicing or remittance handling is finalized.

Step 2 Escalate unclear buyer status before B2B treatment is applied#

Do not default into B2B treatment when the buyer record is weak. If buyer evidence is incomplete or conflicting, escalate before the business branch is applied.

Require the escalation ticket to include the transaction ID, captured buyer fields, any ABN collected, the declaration text shown, and the approver for any temporary treatment. That keeps a clear record if the treatment is reviewed later.

Step 3 Escalate threshold proximity while there is still time to act#

Escalate as soon as threshold tracking shows an entity could move into required registration within the same reporting period. The ATO states registration is required within 21 days once required, and penalties may apply for failing to register when required.

Also escalate when the registration path could change operations materially. Standard GST requires BAS lodgment and GST payment monthly or quarterly. Simplified GST is lodged online each quarter and does not allow tax invoices or GST credit claims.

Step 4 Assign named approvers and written SLAs#

Escalation only works if ownership is assigned before the first exception hits. Define owners across tax, legal, finance, and payments operations, and assign a primary decision owner, backup approver, and written SLA for triage, evidence collection, and signoff.

At minimum, include the role map, buyer evidence snapshot, threshold tracker extract, current registration model, and proposed interim handling in each escalation pack. If tax treatment goes live before those checks are complete, the trigger came too late.

Integrate tax controls into product and finance systems#

The control objective is simple: the same transaction facts should drive the same GST outcome in checkout, invoicing, ledger posting, and filing support.

Step 1 Encode the registration model into transaction logic#

Make registration status and model machine-readable inputs for each relevant entity where Australian GST may apply. Store the model, identifier type, and the ATO registration effective date from the written notice.

Your product and invoicing logic needs separate paths for standard and simplified registration:

| Control point | Standard GST | Simplified GST |

|---|---|---|

| Identifier | ABN-based registration | 12-digit ARN |

| Lodgment/payment cadence | BAS, monthly or quarterly | GST return, quarterly |

| Document/credit capability | Can issue tax invoices and claim GST credits | Cannot issue tax invoices or claim GST credits |

At go-live, verify that the production identifier matches the selected model and align taxable treatment to the recorded effective date.

Step 2 Persist the tax decision on the transaction and post it to the ledger#

Do not let downstream systems recalculate the answer. Persist the tax decision on the transaction itself, including fields such as supplier entity, registration model, taxable or not taxable outcome, rate applied, tax amounts, and decision timestamp or version.

Then post that outcome to the ledger as the finance and compliance source of truth. Build reconciliation views from those ledgered outcomes by registration entity and model so standard GST, with BAS cadence, and simplified GST, with quarterly cadence, stay separated cleanly.

Step 3 Attach evidence references where the transaction lives#

Make filing support retrievable by transaction ID. Attach evidence references to the same record used for invoicing and ledger posting, including the registration model, the registration identifier used at the time of sale, and the transaction details used for the GST decision. That keeps exception review out of spreadsheet reconstruction and lets finance sample support directly from system records.

Step 4 Add release gates for checkout, invoicing, and payout changes#

Treat GST regression checks as a release gate for changes to checkout fields, seller display, payment routing, invoice rendering, or payout ownership. At minimum, confirm that routing still selects the right treatment, the correct entity and identifier are used, and the standard-versus-simplified document rules still hold.

Require recorded tax signoff before any change that can alter GST routing in production. Also account for standard GST operating constraints in the design. Electronic lodgment from outside Australia is not available for that path, and some businesses may need an Australian registered tax agent.

Common Australian GST failure modes and how to recover fast#

Australian GST failures often show up as classification and evidence breakdowns, not just calculation errors. The fastest recovery move is to isolate the failure mode and fix it at the right control point before the next lodgment cycle.

1. Re-run role mapping by channel, not by product. If one GST model was copied across unlike flows, treat that mapping as unreliable until it is revalidated. Re-check each channel and contract variant separately, including supplier role, invoice owner, and remitting entity, then get legal and finance signoff on each mapped flow.

Do not carry an assumption from a non-resident merchant flow into an intermediary flow just because the front-end experience looks similar.

2. Quarantine weak evidence before it contaminates filing. If a tax treatment cannot be supported by retrievable transaction-level evidence, quarantine those transactions from remittance totals until the record is fixed. Keep the exception pack tied to the transaction ID with whatever buyer evidence is available, plus the approver decision.

Use a binary control. The evidence is attached and reviewable, or the transaction stays in exception handling.

3. Re-anchor remittance to the ledger and filing form. If you prepared remittance from operational exports alone, rebuild it from ledgered tax outcomes. For standard registration, reconcile to BAS. For simplified registration, reconcile to the quarterly GST return and confirm that the correct registration identifier was used, whether that is the ABN path or the 12-digit ARN.

If lodged figures do not reconcile, escalate immediately and assess whether a filing correction is needed. Keep the ATO written notice of registration details, including the effective date, and align taxable treatment to that date.

4. Revalidate old assumptions against current ATO guidance. Before you reuse any prior rule, re-check current ATO guidance on registration timing, registration model limits, and filing operations. Two assumptions to check first: simplified registration cannot issue tax invoices or claim GST credits; standard registration has operating constraints, including electronic lodgment limits from outside Australia and possible reliance on an Australian registered tax agent.

If your review shows registration was required earlier, treat it as urgent. Once required, registration must be completed within 21 days, and penalties may apply for failing to register when required.

90-day Australian GST rollout sequence#

Use this 90-day plan to get one defensible GST operating model live before you automate it further. We are using it as an internal sequencing plan, not an ATO-required timetable. The goal is clear ownership, valid evidence, and filing mechanics that hold up in a real close.

1. Complete the perimeter and ownership in Weeks 1 to 2. Start by locking the transaction perimeter flow by flow, because role ambiguity can drive downstream errors. For each channel, confirm the legal seller, whether the platform is acting as an electronic distribution platform (EDP), the invoice owner, and the entity that would register if GST is triggered.

Assign escalation ownership across tax, legal, and finance at the same time. Your checkpoint is simple: every in-scope flow has a signed role map and one named approver for disputed cases. If non-resident merchant and intermediary flows still share one treatment by assumption, split them before moving on.

2. Finalize the registration model and evidence fields in Weeks 3 to 6. Next, choose the registration path based on operating constraints. Simplified GST registration is for non-resident businesses and does not provide ABN entitlement or GST credit claims. Standard GST registration is the ABN-based path for non-resident businesses and supports BAS lodgment and payment.

Build those setup dependencies into the workplan. Simplified registration requires the non-resident setup path, including AUSid and an Online services for non-residents account, and issues a 12-digit ARN. Standard registration requires an ABN first. If registration is required, do not let this decision drift past the 21-day registration window.

3. Dry-run remittance from production-like data in Weeks 7 to 10. Before go-live, run a mock close from ledgered outcomes, not just from operational exports. For standard registration, prepare a draft BAS and reconcile transaction totals, ledger totals, and exception queues. For simplified registration, dry-run the quarterly return dataset and confirm the ARN-linked entity is used consistently.

Require documented signoff on all three views before go-live. Keep every unmatched item in an exception log with an owner, root cause, and correction path.

4. Control the first close and publish operating rules in Weeks 11 to 12. Treat the first live cycle as controlled, with manual review still in place. Publish SOPs that define the chosen registration model, filing cadence, required transaction evidence, and approval paths for buyer-status or role disputes.

Schedule quarterly control testing immediately after go-live. Include one sample-based evidence-completeness test and one filing-operations test, especially for offshore teams on standard registration, where electronic lodgment from outside Australia is not available and an Australian registered tax agent may be needed.

Frequently Asked Questions on Australian GST for digital platforms#

When does a digital platform need to register for Australian GST?#

Register the relevant entity for Australian GST as soon as the obligation is triggered. The ATO states registration must be completed within 21 days once required, and penalties may apply for failing to register when required. In practice, track this by entity and flow, because responsibility can differ by channel and platform role.

Who remits GST in a marketplace flow: seller, MoR entity, or EDP operator?#

It depends on the actual role in the flow, not the label used internally. According to the ATO, an electronic distribution platform (EDP) operator will generally be responsible for GST on certain merchant sales made through the platform, but payment processing alone does not make a service an EDP. If ownership is unclear, escalate and document a clear role map before filing.

What exactly qualifies a buyer as an Australian consumer?#

Use your approved policy test, not a shortcut. The ATO confirms that imported services and digital products sold to Australian consumers are in scope; review ATO guidance for the full legal test. If buyer signals conflict, move the transaction to exception review instead of auto-assigning treatment.

How should teams choose between Simplified GST registration and Standard GST registration?#

Choose based on operating needs, not speed alone.

| Path | Best fit | Key constraints |

|---|---|---|

| Simplified GST registration | Non-resident businesses that do not need GST credits | No ABN entitlement, no GST credit claims, cannot issue tax invoices, uses a 12-digit ARN |

| Standard GST registration | Non-resident businesses that need tax invoices and GST credit capability | BAS lodgment and GST payment obligations, monthly or quarterly |

How is GST remitted in practice through BAS, and what must be reconciled before lodgment?#

Under Standard GST registration, non-resident businesses must lodge BAS and pay GST monthly or quarterly. The ATO also states you cannot lodge electronically from outside Australia and may need an Australian registered tax agent. Before lodgment, reconcile transaction-system totals, ledger totals, and draft BAS totals, and confirm that the filing entity and registration effective date align with the transactions for the period.

What minimum documents should be retained to defend GST treatment decisions?#

Keep a defensible evidence trail for each treatment decision. As a practical baseline, retain the role allocation, the buyer-classification evidence used, the registration identifier used for filing, ABN or ARN as applicable, and a dated record of the decision. The risk to avoid is having filed totals with no transaction-level support for why the treatment was applied.

What should a platform do when role allocation is unclear across multiple entities?#

Escalate immediately and document the dispute. Registration, invoicing, and remittance can all be affected by the same role decision, so unresolved ownership can create downstream filing risk. Do not let separate teams proceed with different assumptions before legal, tax, and finance approve one owner for that flow.

Copy-paste Australian GST checklist for compliance owners#

Use this Australian GST checklist to turn GST decisions into controls you can defend later: clear ownership, documented choices, and transaction-level evidence.

| Checklist item | Key detail |

|---|---|

| Approve a role map for each revenue stream | Keep a signed version tied to the exact entity names used in billing and filings |

| Test buyer-classification logic before production | Route conflicting buyer signals to exception review instead of auto-assigning treatment |

| Assign a named owner to registration-trigger monitoring | Once registration is required, it must be completed within 21 days |

| Document the registration model choice and tradeoffs | Simplified uses a 12-digit ARN and requires quarterly returns and payments; Standard fits cases needing an ABN, tax invoices, or GST credit capability |

| Capture registration evidence, not only status | Retain ABN for standard and ARN for simplified; for standard registration, keep the ATO written confirmation showing the effective date |

| Make evidence-pack fields mandatory and transaction-retrievable | Store the role-map version, buyer-classification outcome, filing identifier, and dated decision record |

| Build remittance controls around reconciliation and exceptions | For Standard GST, align BAS and payment cadence, monthly or quarterly, with close-calendar checks and documented exception handling before lodgment |

| Document escalation triggers and run quarterly control tests | Retain both failures and remediation records |

- Approve a role map for each revenue stream.

Record, for each channel, who is the non-resident merchant, who is the EDP, if any, and whether a Merchant of Record model is used. Do not reuse one map across direct checkout, app store, and marketplace flows unless legal and finance confirm the contract and payment flow are the same. Keep a signed version tied to the exact entity names used in billing and filings.

- Test buyer-classification logic before production.

Implement and test your internal Australian-consumer classification rules. Do not leave them as policy-only text. Because the excerpts here do not provide the full legal test, route conflicting buyer signals to exception review instead of auto-assigning treatment.

- Assign a named owner to registration-trigger monitoring.

Monitor by entity and flow, and escalate when registration responsibility is unclear. Once registration is required, the ATO says it must be completed within 21 days, and penalties may apply for failing to register when required. If monitoring shows turnover nearing the cited A$75,000 figure, escalate before period close.

- Document the registration model choice and tradeoffs.

Record why the entity is on Simplified or Standard GST registration. Simplified GST can suit non-resident merchants, EDP operators, or goods redeliverers that do not need an ABN or GST credits and cannot issue tax invoices; it uses a 12-digit ARN and requires quarterly returns and payments. Standard GST fits cases needing an ABN, tax invoices, or GST credit capability, with BAS lodgment and GST payment monthly or quarterly.

- Capture registration evidence, not only status.

Retain the identifier used by the filing entity, ABN for standard and ARN for simplified. For standard registration, keep the ATO written confirmation showing the effective date.

- Make evidence-pack fields mandatory and transaction-retrievable.

At minimum, store the role-map version, buyer-classification outcome, filing identifier, and dated decision record. If these cannot be pulled by transaction or invoice reference, period-end review becomes hard to defend.

- Build remittance controls around reconciliation and exceptions.

For Standard GST, align BAS and payment cadence, monthly or quarterly, with close-calendar checks and documented exception handling before lodgment. Treat the exact reconciliation method as an internal control choice. Also plan for an operating constraint: non-residents cannot lodge electronically from outside Australia and may need an Australian registered tax agent.

- Document escalation triggers and run quarterly control tests.

Define owners and response expectations for disputed role ownership, unclear buyer status, and trigger-monitor changes that could force registration. Test controls quarterly and retain both failures and remediation records.

Related reading: GDPR for Marketplace Platforms: How to Handle Contractor and Seller Personal Data Compliantly.

If your role map spans MoR, EDP, and direct merchant flows, contact Gruv to validate an implementation path with compliance gates and traceable remittance operations.

Your next move on Australian GST registration and remittance#

If you need one operator summary, use this: for Australian GST, confirm the legal seller, the buyer branch, and the entity that will register before you automate remittance. According to the ATO guidance cited above, GST is 10%, the registration turnover threshold is A$75,000, or A$150,000 for non-profit organisations, and you need to complete registration within 21 days once the obligation is triggered.

| Control point | What you should lock now |

|---|---|

| Rate | 10% Australian GST for in-scope sales |

| Threshold | A$75,000, or A$150,000 for non-profit organisations |

| Standard path | ABN, BAS, monthly or quarterly filing, tax invoices, and GST credit capability |

| Simplified path | 12-digit ARN, quarterly return, no tax invoices, and no GST credits |

If you run a digital platform, your safest next step is to document who sells, who collects, who registers, and who remits for each Australian flow. We recommend that you keep the ABN or 12-digit ARN, the effective date, the transaction ID, and the evidence packet together so you can support every BAS line or simplified return line without rebuilding the file at month-end.

Your team does not win Australian GST compliance by moving fast. You win when you can show why you need to register, why you did not need to register, and how you will remit for each digital platform flow.

Frequently Asked Questions

When does a digital platform need to register for Australian GST?

Register as soon as the relevant entity is required to register. The ATO states registration must be completed within 21 days once required, and penalties may apply for failing to register when required. In practice, track this by entity and flow, because responsibility can differ by channel and platform role.

Who remits GST in a marketplace flow: seller, MoR entity, or EDP operator?

It depends on the actual role in the flow, not the label used internally. According to the ATO, an electronic distribution platform (EDP) operator will generally be responsible for GST on certain merchant sales made through the platform, but payment processing alone does not make a service an EDP. If ownership is unclear, escalate and document a clear role map before filing.

What exactly qualifies a buyer as an Australian consumer?

Treat this as a controlled classification decision, not a shortcut. The ATO confirms that imported services and digital products sold to Australian consumers are in scope; review ATO guidance for the full legal test. If buyer signals conflict, move the transaction to exception review instead of auto-assigning treatment.

How should teams choose between Simplified GST registration and Standard GST registration?

Choose based on operating needs, not speed alone. | Path | Best fit | Key constraints | | --- | --- | --- | | Simplified GST registration | Non-resident businesses that do not need GST credits | No ABN entitlement, no GST credit claims, cannot issue tax invoices, uses a 12-digit ARN | | Standard GST registration | Non-resident businesses that need tax invoices and GST credit capability | BAS lodgment and GST payment obligations, monthly or quarterly |

How is GST remitted in practice through BAS, and what must be reconciled before lodgment?

Under Standard GST registration, non-resident businesses must lodge BAS and pay GST monthly or quarterly. The ATO also states you cannot lodge electronically from outside Australia and may need an Australian registered tax agent. As an internal control before lodgment, confirm that the filing entity and registration effective date align with the transactions for the period.

What minimum documents should be retained to defend GST treatment decisions?

Keep a defensible evidence trail for each treatment decision. As a practical baseline, retain the role allocation, the buyer-classification evidence used, the registration identifier used for filing (ABN or ARN, as applicable), and a dated record of the decision. The risk to avoid is having filed totals with no transaction-level support for why the treatment was applied.

What should a platform do when role allocation is unclear across multiple entities?

Escalate immediately and document the dispute. Registration, invoicing, and remittance can be affected by the same role decision, so unresolved ownership can create downstream filing risk. Do not let separate teams proceed with different assumptions before legal, tax, and finance approve one owner for that flow.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Register for a Business Number (BN) in Canada

--- Getting control of your operation starts with the right question: not whether you might eventually need a Canadian Business Number, but when it becomes worth setting up. This is less about bureaucracy than about operating cleanly, reducing onboarding friction, and avoiding rushed compliance work later.

ASC 606 Revenue Recognition for Merchant of Record Platforms

If you run a Merchant of Record flow, cash movement is not your revenue policy. Under ASC 606, the hard part is that customer payment, processor settlement, and the point when revenue is actually earned can sit on different dates and in different records.

How Platforms Accept Overseas Client Payments Through Inward Remittance

Your core promise is traceable cross-border receipt, not an "international checkout" button. For platform teams, that means tracking who initiated the payment, who the designated recipient is, what amount was expected, what arrived, which provider statuses came back, and whether funds can move to the next internal step.