Quick Answer

Prioritize control depth over feature volume: for synthetic identity fraud payment platforms should pair onboarding KYC with ongoing AML monitoring, then require one case record that captures alert rationale, analyst actions, and hold-release decisions. Use architecture choice as an evidence decision: unified platforms reduce fragmented timelines, API-led stacks preserve flexibility, and in-house builds demand sustained governance. Escalate when identity results conflict with transaction behavior, and keep SAR-supporting documentation and timeline artifacts ready for audit and legal review.

Synthetic identity fraud is a controls problem not just a model problem#

For cross-border payouts, your job is to set enough control depth to reduce synthetic identity abuse without turning contractor, seller, or creator onboarding into needless manual drag.

- Set control depth before you chase model lift

Synthetic identity fraud uses combined PII to fabricate a person or entity for dishonest gain. Better model output helps, but it is not enough on its own. The durable standard is a risk-based approach where controls match the risk you actually face, not one checklist for every case. In practice, that means calibrating onboarding checks, payout review, and account restrictions to the patterns you are seeing.

- Run KYC and AML as one connected control surface

In cross-border payout flows, KYC and AML controls often intersect, and customer due diligence is ongoing, not one-and-done. If a user passes onboarding but later shows suspicious payout behavior, that is still a live control issue. Before you resume normal payout on a flagged account, make sure identity records, transaction history, alert rationale, and analyst actions are documented together in the case record.

- Implement now, and retain evidence you can defend later

The practical target is simple: define what you will implement now, what evidence you will retain, and when escalation is required under your policies. A usable evidence pack includes verification results, why the alert triggered, what the analyst reviewed, what restriction was applied, and who approved release, continuation, or closure. Where suspicious activity review applies, retention duties become concrete. In the cited U.S. bank SAR rule, supporting documentation is retained for five years from filing.

- Treat vendor claims as inputs, not proof

Feature claims and dashboards can be useful signals, but evidence quality and operational fit matter more. The Federal Reserve launched its synthetic identity initiative in 2018 and released a toolkit in early 2022; its synthetic identity fraud definition is intended to improve consistency, not create a standalone reporting obligation. FATF's Recommendation 16 updates approved on 18 June 2025 likewise reinforce stronger cross-border payment transparency for financial-crime detection. If release or closure decisions are happening ad hoc instead of through documented policy and process, escalate internally before you scale the tooling. Related: Payment Fraud Patterns: The Top 10 Scams Targeting Freelancers and Platforms.

Who this list is for and how to choose the right option#

This list is for compliance and risk owners at payment platforms that need synthetic identity controls and reporting-ready investigation workflows across markets. The right choice usually comes down to one question: can your team detect risk and still produce a defensible case record when scrutiny rises?

- Use this list if your team is accountable for both fraud mitigation and suspicious-activity monitoring or reporting quality.

- Skip this list if you are looking for a pure growth optimization guide or a lightweight SMB anti-fraud setup.

- Compare options on three criteria: synthetic identity coverage, investigation depth, and compliance reporting quality.

- Prioritize providers that support a multi-layered control approach and clear case documentation, not just broad feature catalogs.

- Decision rule: if audit defensibility is your biggest pain, weight explainability and case logs above marginal detection-feature breadth.

For a practical look at device-level controls, see Device Fingerprinting Fraud Detection Platforms for Payment Risk Teams.

What every credible solution must cover before you compare vendors#

Treat these as table stakes. If a provider cannot show all four, you are comparing gaps, not mature options.

| Scope | Minimum coverage | Grounded detail |

|---|---|---|

| Detection | Synthetic Identity Fraud, Account Takeover, Authorized Push Payment (APP) Scams, and Money Mule Activity | Use a consistent fraud taxonomy; test APP patterns explicitly; reported APP losses in the UK reached £459.7 million in 2023 |

| Control | Onboarding KYC checks plus transaction-level AML controls | KYC should identify and verify identity with reliable, independent information; AML should act on transactions your team knows, suspects, or has reason to suspect |

| Reporting | A case record that preserves timeline and why the activity was suspicious | Support who, what, when, where, why, plus the method of operation; where U.S. MSB rules apply, suspicious activity can trigger SAR obligations at at least $2,000 with a 30 calendar day filing window after initial detection of supporting facts |

| Governance | A clear accountable owner for day-to-day compliance and escalation decisions | In U.S. MSB frameworks, a person must be designated for day-to-day compliance, and the business remains responsible even when work is delegated |

- Detection scope

A credible solution should cover Synthetic Identity Fraud, Account Takeover, Authorized Push Payment (APP) Scams, and Money Mule Activity, not just one label. It should also use a consistent fraud taxonomy, because inconsistent definitions create inconsistent categorization and reporting. APP patterns should be tested explicitly rather than buried under generic fraud labels. In the UK context, reported APP losses reached £459.7 million in 2023.

- Control scope

Minimum control scope should combine onboarding Know Your Customer (KYC) checks with transaction-level Anti-Money Laundering (AML) controls. KYC should identify and verify identity with reliable, independent information. AML controls should act on transactions your team knows, suspects, or has reason to suspect, not only after confirmed loss.

- Reporting scope

Minimum reporting output is a case record that preserves timeline and why the activity was suspicious. For SAR-ready work, the record should support who, what, when, where, why, plus the method of operation in one coherent narrative. Where U.S. MSB rules apply, suspicious activity can trigger SAR obligations at at least $2,000, with a 30 calendar day filing window after initial detection of supporting facts.

- Governance scope

Governance should assign a clear accountable owner for day-to-day compliance and escalation decisions, with control depth proportionate to the business's risk profile and scale. In U.S. MSB frameworks, a person must be designated for day-to-day compliance, and the business remains responsible even when work is delegated. When you review vendors, ask who can place or release restrictions and what evidence standard they apply.

For a step-by-step walkthrough, see How Platforms Stop Affiliate Fraud Before Commissions Are Paid.

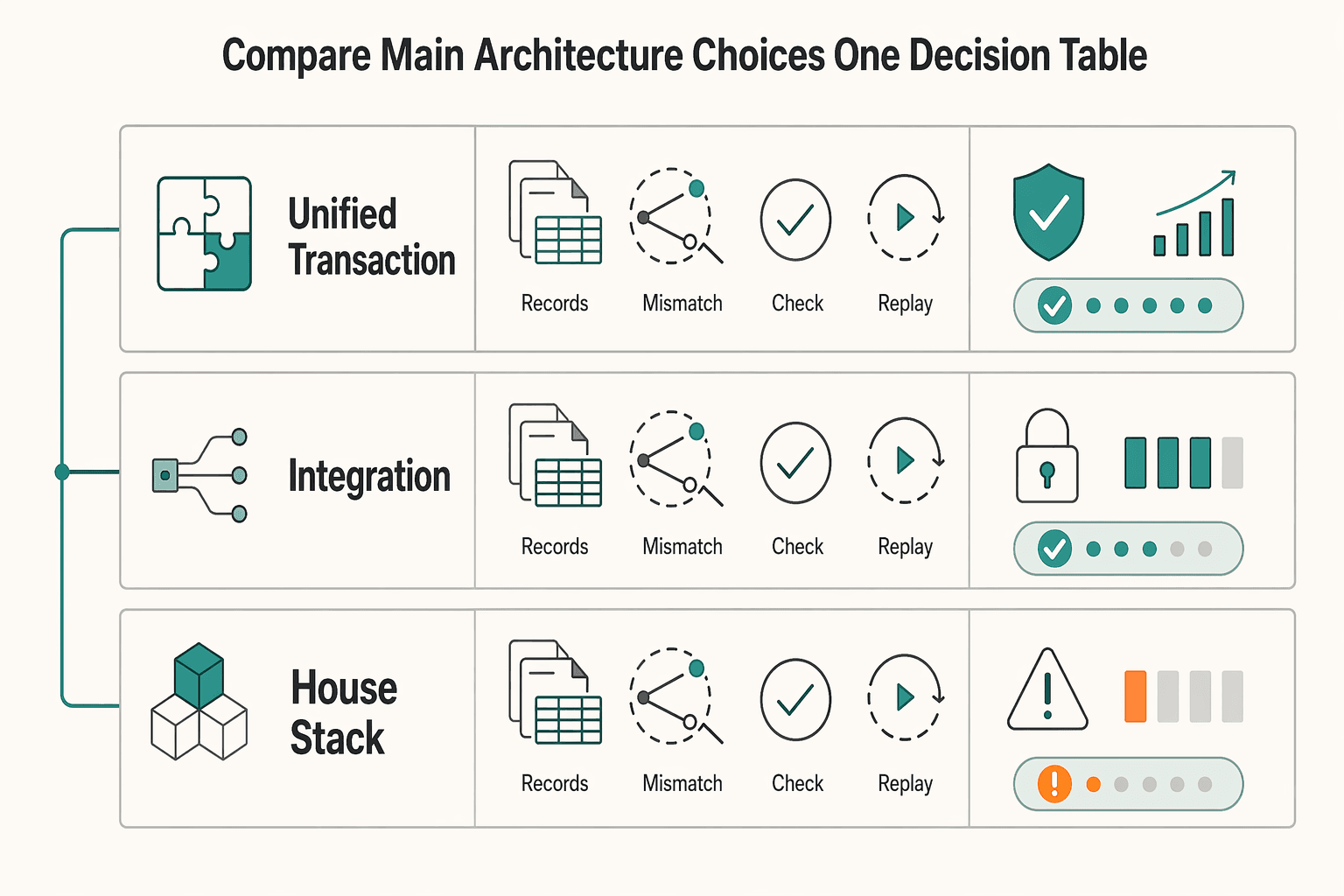

Compare your main architecture choices in one decision table#

This decision is about ownership over time. If you need unified controls and evidence trails, start with a unified platform. If you already run strong investigations and reporting internally, an API-led approach can be a better fit. Build in-house only if you are ready to own detection and reporting quality for years, not just launch.

Synthetic identity abuse is often delayed-loss fraud. Fraudsters can mature identities over time before a later cash-out, and payments risk leader Mike Timoney has described it as long-term rather than short-term. In practice, the winner is the architecture that can reconstruct one chronology across onboarding, transactions, analyst actions, and reporting.

| Path | Grounded market examples and what they claim | Implementation speed | Analyst workload | Explainability quality | Compliance Reporting readiness | Unknowns to force into due diligence |

|---|---|---|---|---|---|---|

| 1. Unified Transaction Intelligence Platform | DataVisor markets lifecycle coverage from onboarding and account access to transaction monitoring and AML workflows, plus 30B+ events processed annually and <100ms latency as vendor claims. FraudNet is positioned as centralized detection with integrated case management. Feedzai markets unified risk operations with SAR filing support. Vyntra frames end-to-end payment observability, and investor material describes it as a union of Intix and NetGuardians. | Variable (scope and integration dependent) | Variable (depends on how well built-in case views fit your process) | Variable to High (depends on visible alert rationale, timeline, and analyst actions) | Potentially High when case records support who, what, when, where, why narratives | Exportability of full case records; visibility into model reasons; handling of cross-market policy exceptions; whether outcome metrics are customer-specific |

| 2. API-led detection plus internal operations | Stripe describes integration into existing workflows via webhooks and real-time notifications. Sift markets a Score API that preserves internal workflow control. You usually keep internal case management and reporting. | Variable (depends on existing tooling and integration depth) | Variable to High (internal teams keep case management and reporting ownership) | High with disciplined internal tooling; Low if context is fragmented | Medium to High (depends on your ability to produce regulator-ready narratives consistently) | Whether KYC, transaction, and analyst data can be joined into one chronology; alert-time context quality; reporting consistency under volume spikes |

| 3. In-house stack | You build rules, models, storage, case views, and reporting outputs. Microsoft notes real-time fraud programs require planning across data architecture, security, integration, and operations management. | Variable (requires full-stack build and ongoing operations planning) | High | Potentially High (you define the standard) | Variable, and can be weaker early unless reporting is designed from day one | Long-term engineering commitment; early legal and compliance design input; resilience of deadlines and evidence retention through staffing and product change |

Here is the quick read on the tradeoffs.

- Unified platform

Use this when your biggest risk is fragmented evidence or weak cross-functional escalation. Ask for a closed-case walkthrough, not just detection screens. Verify that one record can show event order, analyst actions, and the logic behind who, what, when, where, and why.

- API-led plus internal operations

Use this when decision ownership is a hard requirement and your investigations process is already mature. A key risk is split context across tools, which can weaken narrative quality when reporting pressure rises.

- In-house stack

Use this only with stable engineering capacity, strong data governance, and explicit compliance ownership. If your operating context can trigger U.S. bank-style SAR expectations, pressure-test your design against structured narratives and timing windows of 30 calendar days, with up to 60 calendar days when suspect identification is pending. Those rules are not universal across all platform types or jurisdictions.

If you are undecided, use one tie-breaker: choose the path that can reliably reconstruct delayed-loss cases without manual detective work. That is where architectures tend to break down.

Option 1 unified platform with built-in detection and reporting#

If your main risk is fragmented evidence, a unified platform can be a practical path to stronger control and reporting readiness. It fits teams that need one operating surface for detection, investigation, and regulatory reporting instead of stitching multiple tools together during escalations.

The core benefit is shared case context. Providers in this category are often positioned as alternatives to separate fraud detection, investigation, and reporting systems. That maps to a real operational problem. Fraud and AML handoffs can slow decisions and break the narrative. When identity signals, transaction activity, and analyst actions live in one case record, risk and compliance teams can work from the same chronology.

Where this option earns its keep#

This option can be effective when one account shows different abuse patterns over time. In a contractor payouts lifecycle, you might first see synthetic identity abuse, where mixed PII is used to fabricate an identity. Later, you may see money mule behavior, where illegally acquired funds are moved for someone else. If those signals sit in separate tools, your team can end up rebuilding the story by hand. If they sit in one case, escalation is cleaner and faster.

It is also useful in reporting-heavy environments. PSD2 fraud-reporting guidelines are aimed at payment service providers and competent authorities, and SWIFT CSP requires users to compare implemented controls against CSCF controls and attest annually. A unified platform can make evidence easier to retrieve and explain, but it does not make you compliant by default.

What you gain and what you give up#

The upside is cleaner handoff and more consistent documentation. If your U.S. operating model can trigger SAR expectations, case quality gets stress-tested by short timelines. That includes 30 calendar days after initial detection, an additional 30 calendar days when no suspect is identified, and five-year retention of SAR-supporting documentation.

The tradeoff is dependency on one vendor's data model, case design, and export behavior. Transparency can still vary, and cross-market policy fit often needs custom governance.

What to verify before you buy#

Ask for a closed-case walkthrough, not a feature tour. Confirm that the record shows:

- event order from onboarding through disposition

- clear alert rationale, analyst action history, and linked evidence

- exportable case records that preserve who did what and when

A common red flag is a "single pane" that is really multiple connected systems. If the vendor cannot produce one exportable, sequence-preserving case file, you are still buying reconciliation work.

This option makes sense when speed to control and evidence continuity matter more than maximum tooling flexibility.

For a broader view of payment fraud controls, read Fraud Detection for Payment Platforms: Machine Learning and Rule-Based Approaches.

Option 2 detection API plus internal case management#

Choose this route when your team already runs strong internal investigations and mainly needs better detection inputs. It works when you can keep onboarding, transaction review, and reporting evidence connected inside your own case process.

Where this option makes sense#

This option fits teams with a mature case queue, documented review steps, and clear fraud and compliance ownership. A common setup is solid analyst tooling but weaker Know Your Customer (KYC) risk signals for synthetic identity abuse, where combined personal data is used to fabricate an identity. In that setup, adding a detection API can strengthen early signals without replacing the investigation tools your team already relies on.

The modular upside is flexibility. You can layer in additional identity signals without rebuilding your full stack, though finding synthetic-identity-focused options that fit your organization's needs can still take work. A risk-based model still helps you adapt controls to local requirements.

What you gain and what you take on#

The gain is operating control. If your case management already matches your escalation rules, payout holds, and analyst workflows, you can improve detection while keeping the process your team knows.

The tradeoff is that reporting quality stays with you. FFIEC describes suspicious activity reporting as a cornerstone of the U.S. BSA model and emphasizes that SAR content quality is critical. If your detection API returns scores and tags, your internal case still needs to support a clear narrative: who, what, when, where, and why. SAR narratives should also include relevant account-opening and due-diligence information when available.

You also carry the burden of ongoing monitoring discipline. For covered U.S. financial institutions, CDD is defined around four core elements: customer identification, beneficial ownership, customer risk profiling, and ongoing monitoring. Exact obligations vary by entity and market, but the operating expectation is the same: keep customer information current and document why decisions were made.

What to verify before you buy#

Ask the vendor and your internal team to prove the handoff is auditable, not just integrated. Check for:

- a durable case link between KYC alerts, transaction alerts, and analyst actions

- preserved detection detail, including reason codes, model or rule version, and alert timestamp

- exports that let compliance reconstruct a regulator-ready chronology without manual stitching

A common failure mode is better detection with thinner case records. Analysts see a score, close an alert, and later cannot show what evidence was reviewed or whether customer information was updated after new behavior appeared. Another is split ownership across fraud and AML teams, where no one can view the full account story in one place.

Decision rule#

Pick this option if your internal case management already captures chronology, evidence, and reviewer decisions well enough for regulatory reporting. If it does not, modular detection can increase signal while also increasing ambiguity.

Option 3 in-house controls stack with rules and models#

This is the high-control path only if you can also own model governance and reporting quality. It fits mature teams with engineering bandwidth, established data governance, and clear ownership across risk, compliance, and legal.

Best fit#

Choose an in-house stack when your platform has enough volume, historical case data, and distinct abuse patterns to justify custom rules and models. In a U.S. payment system context, the key test is not just whether you can build detection, but whether you can show how it was built, validated, changed, and used. SR 11-7 sets that expectation through robust development, effective validation, and sound governance and controls.

Use this option when your own loss reviews show repeat patterns that need platform-specific treatment. If fraud, AML, and legal still operate from separate records, address that first so detection outcomes and case evidence stay aligned.

What you gain#

The gain is a tighter fit to your actual business logic and risk profile. You can tune controls to your seller, contractor, or creator flows. That matters because the Federal Reserve has said synthetic identities can evade current identity verification and credit-screening processes. It also published a dedicated white paper on Synthetic Identity Fraud in the U.S. Payment System on July 09, 2019.

You also gain evidence precision if you design for it. Build alerts so you can reconstruct what triggered a score, what data was considered, what version of the rule or model ran, and who approved or overrode the outcome. If you cannot reproduce why a score fired last quarter, you do not fully control the stack.

What most teams underestimate#

The hard part is not just model build. It is ongoing monitoring, process verification, benchmarking, outcomes analysis, and case records that can support compliance reporting, and supervisory guidance notes direct resource costs to develop and implement models properly. FFIEC describes suspicious activity reporting as foundational to the BSA reporting system, and SAR narratives should cover who, what, when, where, why, and method of operation.

A failure mode is strong model performance with weak case evidence. You may rank risk well but still fail to reconstruct why an account was restricted, escalated, or cleared. Use this route only if documentation quality is treated as part of the control, not as post hoc cleanup.

Build the evidence pack regulators and auditors will actually request#

Once you choose a control stack, make your case file reconstruction-ready. In U.S. BSA/AML practice, strong control is less about alert volume and more about whether you can show what happened, what was reviewed, what was known at each step, and how that led to a reporting decision.

This matters especially on payment platforms investigating synthetic identity cases across onboarding and payments. The Federal Reserve defines synthetic identity fraud as combining PII elements to fabricate a person or entity, and these cases may not look suspicious from payment behavior alone.

1. Case core tied to SAR-ready facts#

Use a fixed internal artifact set in every case, even if your labels differ: alert rationale, analyst action log, identity verification records, and a recorded decision outcome. This is not a regulator-mandated label set. It is an internal baseline that keeps the file SAR-ready if risk escalates.

Capture the following:

- why the alert triggered and when initial detection occurred

- what the analyst checked, in sequence, and what decisions followed

- account-opening and due-diligence information already available to your institution

- the final disposition and any escalation or override

Before you move on, ask whether this file can clearly answer who, what, when, where, why, and method of operation without rebuilding the case from chat logs or memory.

2. Timeline that shows who knew what and when#

For synthetic identity incidents, sequence is critical. Keep a timestamped chain from account opening through signal conflicts, reviews, restrictions, contacts, and final disposition.

At minimum, preserve:

- first detection time

- first human review time

- each restriction or hold event, if applied

- each escalation or team handoff

- final decision time

This protects filing discipline. In bank context, SAR timing runs from initial detection: 30 calendar days, with an additional 30 calendar days if no suspect is identified, and never beyond 60 calendar days from initial detection.

| Obligation area | Bank context | MSB context |

|---|---|---|

| Suspicious transaction trigger | At least $5,000 aggregated | At least $2,000 aggregated |

| Filing timing | 30 calendar days from initial detection; additional 30 if no suspect; max 60 | Not provided in this section pack |

| Record retention | Supporting documentation treated as filed with the SAR and must be available on request | SAR and supporting documentation retained for 5 years from filing |

3. Linked evidence across onboarding and transaction monitoring#

If a case spans multiple rails or lifecycle stages, link records intentionally. This is a control design choice, not a quoted mandate, but it aligns with AML program expectations that connect identification, reporting, record retention, and law-enforcement response.

In practice, keep onboarding checks, due-diligence records, identity signals, transaction monitoring alerts, and related-account links in one case view or a clearly cross-referenced package. Otherwise, the narrative can read like disconnected incidents instead of one evolving risk pattern.

Continuity matters because synthetic cases can show limited payment-behavior signals until losses materialize. Preserve early identity evidence alongside later activity. For a deeper onboarding checklist, see How Platforms Detect Synthetic Identity Fraud in Contractor Onboarding.

4. Closure gate for completeness, audit, and retention#

Before you close the case, run a completeness gate. The goal is practical defensibility. Supporting SAR documentation is treated as part of the filing record and must be available to FinCEN or law enforcement on request. Independent testing also evaluates BSA compliance against your risk profile.

Use a closure check to confirm the following:

- the file can support SAR drafting, including account-opening and due-diligence facts already available

- the event timeline is complete for detection, review, action, and outcome

- onboarding and transaction-monitoring records are attached or directly linked

- retention routing is correct, including the 5-year MSB SAR documentation period

Internal policy recommendation: if evidence is incomplete, keep the case in restricted or enhanced review until the record meets your standard. This can add customer friction, but it reduces the higher-risk failure of being unable to support your reporting decision or audit response.

Related reading: SOC 2 for Payment Platforms: What Your Enterprise Clients Will Ask For. Before finalizing your control design, map each required artifact and escalation checkpoint to concrete implementation patterns in Gruv docs.

Escalation rules that prevent regulatory surprises#

Escalation works best when it is triggered by conflict, not certainty. Do not wait until a case looks fully proved before you move it up the chain. The right moment is usually when identity results and transaction behavior no longer support the same story.

- Escalate when profile and behavior conflict

A passed KYC result is not a stop signal if activity no longer matches what that customer would normally be expected to do. In a U.S. bank context, that mismatch is part of suspicious-activity analysis, not only a fraud signal. If the account narrative and payment behavior diverge, move the case from routine analyst handling to compliance and legal review without delay.

- Use a clear if-then ladder for money-mule activity

Treat suspected money-mule patterns as a higher-severity path than weak anomalies.

- If facts indicate coordinated pass-through behavior or a potentially ongoing laundering pattern, escalate immediately to compliance and legal and assess whether urgent U.S. bank law-enforcement phone notification is triggered for a qualifying case.

- If signals are limited or ambiguous, route the case to enhanced review with documented follow-up checkpoints.

- Define hold-release authority and evidence standards in advance

Do not allow ad hoc hold releases. Predefine who can approve release and require a consistent minimum record: KYC outcome, behavior analysis, hold rationale, newly obtained evidence, and named approver. Before release, confirm the file includes enough supporting documentation if SAR reporting later becomes necessary. If not, release is premature.

- Add jurisdiction gates for PSD2 and SWIFT CSP where applicable

Escalation is sometimes jurisdiction-driven, not only pattern-driven. For PSD2 exposure, test whether the event could qualify as a major operational or security incident requiring notification without undue delay, and whether user-impact communication obligations may apply. If you are a SWIFT user, include a SWIFT CSP check: mandatory controls form a baseline, attestation requires independent assessment, and the annual cycle runs from July with a 31 December attestation deadline.

Synthetic-identity risk can look acceptable at onboarding and appear riskier later. Escalate on emerging conflict signals, not on the original pass result alone.

Common mistakes that cause overbuilding or under-control#

The usual failure is imbalance. Teams either overbuild detection they cannot defend, or underbuild the monitoring and evidence needed when risk changes after onboarding.

- Treating vendor detection claims as the control, not an input

A model score alone is rarely a reporting-ready control. If your team cannot explain a vendor model's capabilities, applicability, and limits, you are carrying model risk without enough governance. A practical test: does one case file clearly show alert reason, analyst actions, identity records reviewed, and final decision in a way that supports regulatory reporting or SAR preparation where applicable? If not, control design is still weak, even when detection demos look strong. Validation should also be ongoing, not a one-time exercise.

- Overbuilding KYC and underinvesting in AML monitoring

Customer due diligence at onboarding is only a baseline. Ongoing due diligence and transaction scrutiny across the relationship are required, especially because synthetic identities can look normal early and become risky later. If controls focus on onboarding checks but not post-onboarding behavior, you miss late-emerging risk. Your monitoring should be able to pull in account-opening and due-diligence context when behavior changes.

- Keeping fraud and compliance in separate case histories

Split case records can create inconsistent facts, timelines, and rationales. Reporting quality depends on a coherent narrative that covers who, what, when, where, and why. Use a single timeline that links onboarding, transaction activity, analyst interventions, and approval decisions. Where SAR support applies, remember that supporting documentation may need to be retained for five years from filing.

- Ignoring delayed-loss behavior in synthetic identity fraud

Early account activity can look clean while risk builds over time. Traditional fraud models are often not designed for fabricated identities, and losses may appear later as activity scales. The Federal Reserve toolkit cites estimated U.S. synthetic identity losses of $20 billion in 2020, which reinforces the cost of late detection. Reopen risk review when transaction behavior shifts beyond what the original customer narrative supports, even if onboarding checks passed.

- Testing only one fraud type and assuming controls generalize

Controls tuned for synthetic identity abuse may miss Account Takeover and Authorized Push Payment (APP) fraud because the mechanisms and evidence patterns differ. ATO involves unauthorized access to a real account, while APP fraud involves a real user being manipulated into authorizing payment. Testing should include adjacent abuse scenarios before controls are treated as complete. UK Finance reported over £1.1 billion in fraud losses in 2024 and warned that closing one vulnerability in isolation can shift criminals to another.

Choose control depth by evidence burden not by feature volume#

Pick the option that can detect synthetic identity fraud, preserve the investigation record, and support defensible escalation when identity-check results and transaction behavior no longer support the same customer story.

In practice, that means proving minimum controls before expanding tool volume. A larger stack may look stronger in a demo, but it does not help if your team cannot explain why an alert fired, what evidence was reviewed, and who approved the outcome.

- Choose the architecture that produces a usable case record

Start with evidence quality, not feature count. You should be able to produce one case file with account-opening data, due-diligence records, alert rationale, analyst actions, and a clear who, what, when, where, why narrative. That aligns with SAR narrative expectations, and in the U.S., SAR supporting documentation must be retained for 5 years from the report date. Key differentiator: choose the option that is easier to defend in reporting and review, not just easier to operate day to day.

- Validate minimum controls before expanding coverage

Use a risk-based approach first: stronger AML measures where risk is higher, lighter measures where risk is lower. Phase one should prove that core controls are working together: onboarding identity-validity checks, post-onboarding transaction monitoring, unified case ownership, and a documented escalation path. This matters because synthetic identities can evade standard identity and credit screening, so onboarding checks alone are not enough. Key differentiator: phase one should prove your controls catch clear misses and create a defensible record before advanced features are added.

- Expand only where incident data shows a real gap

After baseline controls are working, add depth where your own losses, false positives, or escalations show blind spots. If issues appear as transaction activity rises, strengthen post-onboarding monitoring before adding another identity vendor. If analysts cannot connect onboarding evidence to suspicious movement, fix case linkage first. A practical checkpoint is whether a second reviewer can reconstruct the full case without asking for missing context. Keep definitions consistent across teams, because inconsistent categorization weakens trend reporting and comparability of mitigation outcomes. Key differentiator: incident-backed expansion gives each added control a clear purpose and a cleaner governance trail.

- Prefer clear ownership over tool sprawl

Operating ownership matters as much as architecture choice. Modular setups can add flexibility, but they can also increase coordination risk if records and decisions are fragmented across teams or systems. Before implementation, confirm who owns the final narrative, who signs off escalations, and how applicable reporting and retention requirements are mapped. The Federal Reserve released a Synthetic Identity Fraud Mitigation Toolkit in early 2022, but control depth still needs to match your jurisdictions, product flows, and obligations. Key differentiator: confirm coverage and reporting needs before go-live so the control set fits the business you actually run.

If you want a market-by-market read on payout policy gates and audit-ready reporting fit for your workflow, contact Gruv.

Frequently Asked Questions

What is synthetic identity fraud in payment platforms?

Synthetic identity fraud is the use of a fabricated identity built from real and/or invented personal data elements for dishonest gain. In platform payments, that can look like an account that appears credible enough to pass onboarding and transact before risk is detected. It is not the same as copying a real person’s profile end to end.

Why can synthetic identity fraud pass traditional KYC checks?

Because KYC checks whether submitted identity data appears valid, and synthetic profiles can be assembled to pass those checks. U.S. Payments Forum and Federal Reserve materials both note that synthetic identities can evade common identity verification and credit-screening processes. If controls stop at onboarding, later risk shifts can be missed.

Which controls are table-stakes for platforms paying contractors and sellers?

You need onboarding controls and post-onboarding monitoring together. A practical baseline can include identity-validity checks at entry, AML transaction monitoring, consistent case records across the lifecycle, and clear escalation ownership when identity signals conflict with behavior. Your team should be able to show a case file with alert rationale, analyst actions, records reviewed, and final decision.

What records should we retain for audits and regulator requests?

Retain the investigative record, not only the final disposition. In practice, that includes identity records, transaction history, alert reasons, analyst notes, timestamps, approvals, and the core narrative elements: who, what, when, where, and why. Under U.S. MSB SAR rules (31 CFR 1022.320), a filed SAR and supporting documentation must be kept for five years, but that is not a single global standard for all entities or jurisdictions.

When should legal or compliance be escalated during an investigation?

Escalate when onboarding results and transaction behavior no longer support the same customer story, or when activity suggests coordinated money movement. For U.S. MSBs, 31 CFR 1022.320 sets a 30 calendar day SAR filing deadline after initial detection of reportable facts, and suspicious activity involving at least $2,000 can trigger SAR analysis. If immediate attention is required, such as an ongoing money laundering scheme, the rule calls for immediate telephone notification rather than waiting for the normal cycle.

Should we choose a unified platform or combine APIs with internal tooling?

Choose based on evidence quality and operating maturity, not feature count alone. Unified systems can make it easier to maintain one investigation timeline, while API-plus-internal tooling can offer more flexibility if your team can keep records and decisions consistent across tools. Under U.S. MSB rules, outsourcing tools does not transfer AML accountability from the regulated business.

How do we evaluate vendor claims when benchmark evidence is unclear?

Require evidence that can withstand independent challenge, not just model scores or sales claims. Validate applicability, limits, and failure modes on your own cases, and keep a clear audit trail of what was tested and who approved it. That standard matters in an enforcement environment where AI claims have been challenged when testing support was missing, including FTC actions announced on September 25, 2024.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bsaaml.ffiec.gov/manual/Appendices/13trusted

- bsaaml.ffiec.gov/manual/AssessingComplianceWithBSARegulatoryR...trusted

- eba.europa.eu/activities/single-rulebook/regulatory-activi...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- fbi.gov/how-we-can-help-you/scams-and-safety/common-...trusted

- fdic.gov/news/financial-institution-letters/2017/adop...trusted

- federalregister.gov/documents/2016/05/11/2016-10567/customer-due...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: