Quick Answer

Use a hybrid design: rules for hard stops, machine scoring for shifting patterns, and human review for ambiguous high-impact cases. For fraud detection payment platforms machine learning decisions, the strongest setup is the one your team can audit end to end, including the triggering signal, policy version, and final disposition. Start strict on new payout routes, then tune in small steps as false positives and chargeback trends stabilize.

How Payment Platforms Detect Fraud#

For cross-border payout platforms, effective fraud detection is less about a single model or rule than about controls you can document, explain, and defend under audit or incident pressure.

In the EU RTS context cited by the European Banking Authority, payment service providers must have transaction monitoring mechanisms to detect unauthorized or fraudulent payment transactions. That monitoring applies in addition to Strong Customer Authentication. In practice, decisions to approve, hold, or block are easier to defend when they are traceable to the transaction data, the rule or score that triggered them, and the policy owner responsible.

Your fraud scope also has to extend beyond card checkout. EEA industry reporting says payment fraud amounted to EUR 4.2 billion in 2024, with most fraud by value arising from credit transfers and card payments. Fast, often irreversible payment flows also increase exposure to authorized push payment scams, where users are manipulated into authorizing the transfer themselves.

This article compares rule-based controls, machine learning, hybrid decisioning, and manual review for cross-border payout environments. The goal is to help you choose based on coverage, false-positive impact, explainability, and whether your team can produce the records that matter when something goes wrong, including what triggered a decision and which policy version was in force.

That documentation standard matters in regulatory review. U.S. suspicious activity examination language emphasizes policies, procedures, and processes for monitoring, detecting, and reporting suspicious activities. The Financial Stability Board's 12 December 2024 recommendations also reinforce focus on consistent supervision of banks and non-banks in cross-border payments. For machine-enabled monitoring governance, a practical frame is NIST AI RMF: govern, map, measure, and manage. For an adjacent payment-policy issue, see Tipping and Gratuity Features on Gig Platforms: Payment and Tax Implications.

Selection Criteria and Fit#

Choose the approach your team can explain and govern end to end, not the one with the best demo. If your current setup cannot clearly reconstruct why a payment was approved, held, or blocked, treat that as an explainability and governance gap before you scale.

| Criterion | What to check | Why it matters |

|---|---|---|

| Payment risk coverage | Rails and payment speeds you actually run | Coverage built mostly for card checkout may miss some payout risk; instant payments show higher fraud rates than traditional credit transfers |

| Merchant risk coverage | Account-level risk, not only transaction-level risk | Account changes and payout behavior need clear ownership and follow-up |

| False positives impact | Held-payment volume, release rates after review, and complaint patterns | Threshold changes should be based on visible tradeoffs |

| Audit traceability | Source event, triggered rule or model reason, policy version, and reviewer notes | Supports a decision record you can defend and specific reasons if needed under 12 CFR 1002.9 |

| Escalation clarity | When automation should hand off to people and who owns the final decision | Makes escalation triggers explicit when evidence conflicts or outcomes are challenged |

This framework is for compliance, legal, finance, and risk owners managing payout programs. Supervisory focus is broader than detection accuracy alone. The FCA reviews onboarding, monitoring, and reporting controls, and FFIEC framing also emphasizes monitoring, detecting, and reporting suspicious activity. GDPR safeguards and U.S. adverse-action requirements also raise the bar for explainability and challenge paths.

Use the criteria below to compare options:

- Payment risk coverage. Match controls to the rails and payment speeds you actually run. The EBA opinion dated 29 April 2024 says instant payments show higher fraud rates than traditional credit transfers, so coverage built mostly for card checkout may miss some payout risk.

- Merchant risk coverage. Include account-level risk, not only transaction-level risk. Use an onboarding, monitoring, and reporting lens so account changes and payout behavior have clear ownership and follow-up.

- False positives impact. Measure the operational cost of stopping legitimate payouts. Track held-payment volume, release rates after review, and complaint patterns so threshold changes are based on visible tradeoffs.

- Audit traceability. Keep a decision record you can defend: source event, triggered rule or model reason, policy version, and reviewer notes. If you may need to provide specific reasons in writing under 12 CFR 1002.9, this is a core control.

- Escalation clarity. Define when automation should hand off to people, especially when evidence conflicts or outcomes are challenged. Stronger designs make escalation triggers explicit and assign final decision ownership.

Best for Fast Baseline Control with Rule-Based Systems#

Rule-based systems are a practical way to deploy immediate, explainable controls. They put clear policy guardrails around a payment flow with explicit action-and-condition logic.

- Best fit: often useful for teams that need fast guardrails and clear policy logic in a new payment flow.

- Pros: deterministic decisions, straightforward explainability, and clear routing to human review when needed.

- Cons: ongoing tuning burden, false-positive pressure, and slower adaptation as fraud behavior changes.

A rule follows a simple structure: {action} if {condition}. When a payment matches, the action is applied, and rule evaluation can stop for that payment. This works well for concrete patterns such as geography mismatches or explicit amount and card-type conditions.

Use review rules so you do not turn every medium-risk signal into a hard block. For example, you can review payments above a defined threshold, such as 1,000 USD, made with a prepaid card so analysts can add judgment without auto-declining.

For a new payout route, start with strict rules for the clearest risk signals and route the middle band to Manual review. Then monitor review outcomes and adjust thresholds as needed before expanding rule coverage.

Best for Adaptive Detection with Machine Learning#

Machine learning earns its place when fraud patterns are changing and you have trustworthy labeled history to train on. It should extend your rules, not replace them.

Best fit#

Use supervised learning when your historical cases include both transaction inputs and consistent final outcomes. In practice, that means labels like confirmed fraud or confirmed legitimate activity are applied the same way over time.

If labels are inconsistent, model quality can drop. Before live scoring, confirm your training data reflects final case outcomes, not only early analyst suspicion.

Why it earns its keep#

Rules handle known patterns well. Models help surface behavioral anomalies that are not yet captured in static policy logic. That makes ML useful for novel or evolving patterns that are weakly represented in past labels.

A common operating pattern is per-transaction risk scoring that feeds approve, challenge, or decline decisions. Some providers describe scores on a 0 to 99 range, but the score is an input to your decision process, not the decision itself.

This is especially useful for account behavior shifts that may indicate account takeover, including malware-enabled credential theft. The stronger design is layered. Use model scoring for adaptive detection, with rule gates for hard controls.

Where it breaks#

One major tradeoff is explainability. Higher-complexity models can improve performance, but they can also be harder for stakeholders to interpret and manage.

Concept drift is a persistent implementation risk, so monitoring cannot be a one-time setup. Model risk guidance, including Federal Reserve SR 11-7, April 4, 2011, emphasizes ongoing reassessment and, when conditions change, adjustment, redevelopment, or replacement.

Practical recommendation#

Use machine learning to score, and keep rules as the final control layer, especially for suspected identity-theft or malware-linked cases. Treat behavioral anomalies as triggers for corroboration, not proof on their own.

Before rollout, make sure you can produce three records for any disputed payment:

- the data used to generate the score at decision time

- the rule or threshold that translated the score into approve, hold, review, or decline

- the final case outcome fed back into later labeling

If you cannot produce these cleanly, keep the model in a support role and let rules plus transaction monitoring drive final actions. Related: Machine Learning Feature Engineering for Payment Fraud: The 50 Signals That Matter Most.

Best for Most Platforms with a Hybrid Decision Stack#

For many mature payment platforms, a hybrid stack is the most defensible operating model. Use rules for deterministic actions, ML-informed checks for risk prioritization, and manual review for ambiguous, high-impact cases.

-

Start with deterministic controls. Use monitoring signals and rules to trigger explicit actions you can audit. Keep decision outputs explicit, such as allow, block, review, or request 3DS. Verify rule order before launch. Stripe documents sequential evaluation, and once one rule triggers, later rules are not evaluated.

-

Use ML to prioritize unresolved risk. Use ML-informed checks to score unresolved cases and map score bands to controlled actions. Stripe describes default rules informed by AI model judgments, which supports this combined approach. Keep evidence for each disputed decision: the event snapshot, the score or score band, and the rule or threshold that produced the action.

-

Use manual review as the uncertainty backstop. Route suspicious payments that need a human decision to review rather than forcing binary automation. Review quality depends on context, so include the triggered signals, rule outcome, model score band, and relevant account or payment history in the analyst packet.

-

Tighten early in high-volume phases, then adjust with recurring monitoring. Make control changes in small steps based on observed outcomes, not on a single short-term trend. Mastercard reports survey context that 83% of industry leaders say AI reduced false positives and churn, but your own results should still govern threshold changes. Keep monthly exposure checks in place. Visa monitors monthly and, from 1 June 2025, flags acquirer portfolios as Above Standard at

>=50bpsVAMP ratio and Excessive at>=70bps, with required mitigation when thresholds are exceeded.

If you use Stripe-style allow rules, note that Stripe says merchants must have processed more than $100,000 before they can write allow rules. Treat approval shortcuts as high-governance controls because they change normal decision flow.

Best for High-Risk Queues with Manual Review#

Manual review is the right lane when an automatic decline is not clearly warranted. Use it for events that may need further investigation, not for every elevated signal.

- Route only ambiguous, high-impact cases

Use review when signals are serious but not final, such as elevated risk indicators or linked-entity anomalies. A review rule lets payment processing continue while flagging the case for investigation, instead of forcing an immediate hard decline. If account-takeover risk is the concern, use account review with payouts paused as a temporary control if your setup supports it.

- Give reviewers a complete evidence packet

Include the triggering rule or score reason, phishing or account-access risk indicators, and prior disputes and chargeback fee exposure. Related payments that share email, IP address, or card are especially useful for showing whether the event is isolated or part of a pattern. The packet should make both the current event and surrounding history clear enough for a defensible decision.

- If evidence is incomplete or contradictory, escalate through policy

Consider a temporary hold plus compliance escalation rather than an irreversible decline when evidence conflicts. That is an internal control choice. For regulated institutions, this aligns with suspicious-activity escalation obligations and with maintain-or-close decisions being made under documented internal policy.

A practical example: a suspicious payout pattern appears with signs of possible phishing-linked account access. Route the account to Manual review, pause payouts if available, and work to your documented internal decision SLA. If ownership and behavior check out, release the hold. If the evidence still conflicts, escalate under your compliance process.

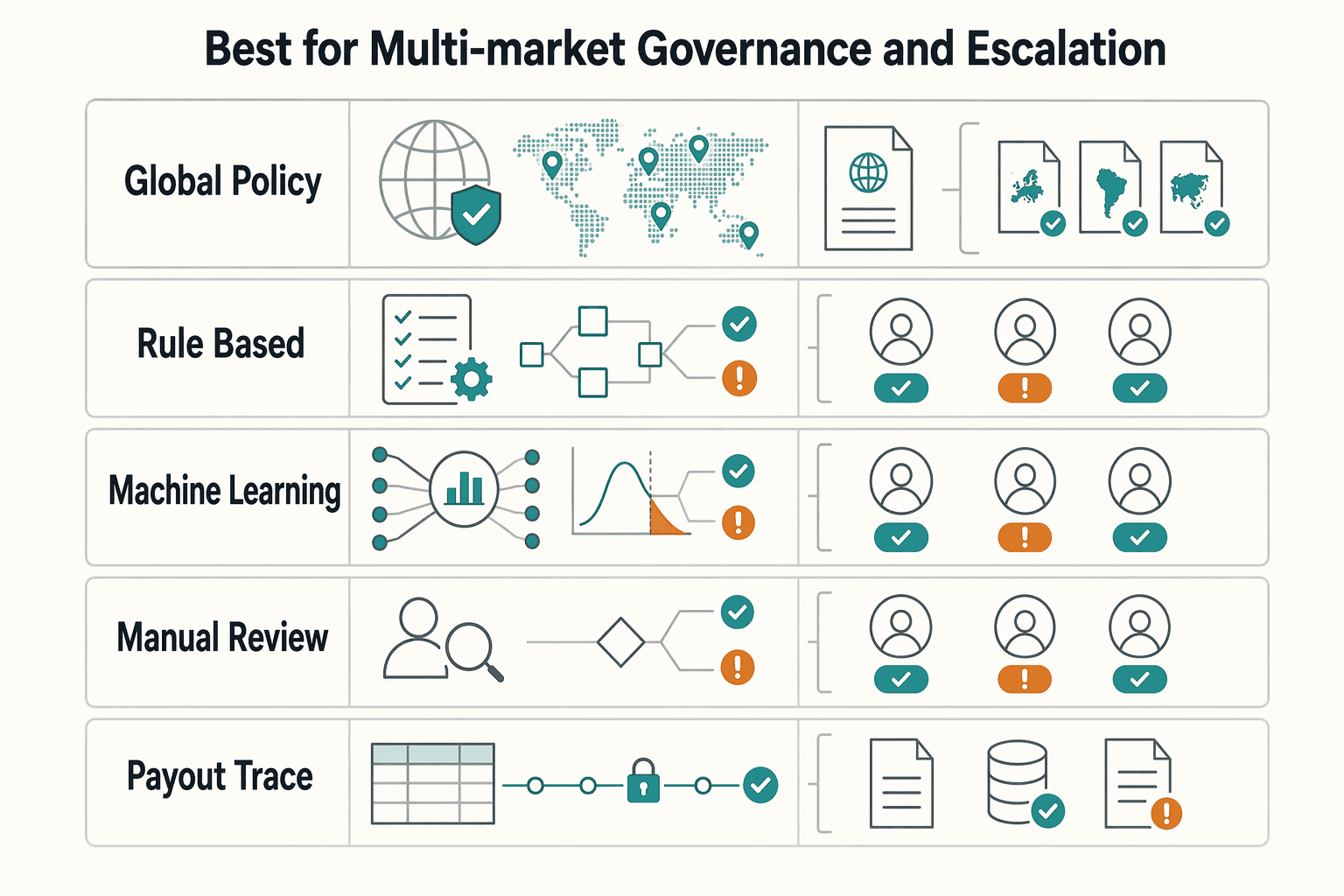

Best for Multi-Market Governance and Escalation#

Once you operate across multiple markets, the hard part is usually governance, not detection logic. The setup works when each decision class has a named owner, escalation triggers are written, and every critical outcome is traceable in transaction monitoring records from input to final action.

| Area | Owner or rule | What to retain |

|---|---|---|

| Global policy spine | Use one global policy spine, then localize by market | Local annexes where legal triggers and reporting obligations differ |

| Rule-based systems | Give Rule-based systems a named policy owner | Owner, jurisdiction scope, rationale, exceptions, version history, triggering inputs, active rule version, and approval trail |

| Machine learning | Give Machine learning a model owner and an independent challenger | Assumptions, limitations, validation, threshold changes, and a documented reason path for score-based actions |

| Manual review | Make Manual review a case-ownership function, not a shared inbox | Written triggers for potential regulatory exposure and unusual-activity patterns, plus case ownership for evidence gathering and coordination |

| End-to-end traceability | Treat end-to-end traceability as a release gate | Source event ID, timestamp, jurisdiction, triggered rule or model version, score or reason code, reviewer notes, escalation recipient, and final action; where a U.S. SAR is filed, supporting documentation for five years |

- Use one global policy spine, then localize by market.

Anchor cross-border policy in a globally recognized standard, then adapt it by jurisdiction. FATF frames its Recommendations as an international standard implemented through local measures, and notes amendments through October 2025. If your model includes non-bank entities, FATF's R18/R23 clarification supports a group-wide programme approach, with local annexes where legal triggers and reporting obligations differ.

- Give Rule-based systems a named policy owner.

Rules should have clear ownership, not live only in tickets or vendor consoles. This aligns with governance expectations for defined, transparent lines of responsibility. For each critical rule, document owner, jurisdiction scope, rationale, exceptions, and version history. Then verify you can show triggering inputs, active rule version, and approval trail for the decision.

- Give Machine learning a model owner and an independent challenger.

ML governance should cover assumptions, limitations, validation, threshold changes, and ongoing use, not just model performance. SR 11-7, dated April 4, 2011, is still useful here because it emphasizes objective challenge by informed parties who can identify model limits and require changes. If ML affects merchant or payment risk decisions, separate day-to-day model ownership from independent challenge and keep a documented reason path for score-based actions.

- Make Manual review a case-ownership function, not a shared inbox.

Escalations need defined communication lines and clearly designated individuals for investigation and reporting. Assign a case owner for each escalated review to gather evidence, coordinate risk, compliance, and legal input, and close the case. Use written triggers for potential regulatory exposure and other unusual-activity patterns relevant to your risk profile. Where U.S. MSB-like flows apply, suspicious activity escalation may involve transactions that involve or aggregate at least $2,000, while activity near $10,000 alone is not enough to require a SAR.

- Treat end-to-end traceability as a release gate.

If a reviewer or examiner cannot follow an alert through the full process, the control is not ready for scale. For each critical decision, retain a complete trail: source event ID, timestamp, jurisdiction, triggered rule or model version, score or reason code, reviewer notes, escalation recipient, and final action. Where a U.S. SAR is filed, retain supporting documentation for five years under 31 CFR 1022.320(c). Local retention obligations can differ by market.

Use this operating rule: do not launch a cross-border control unless you can name the owner, name the escalation path, and prove the full decision trail from event input to outcome.

Best for Lower False Positives Without Raising Fraud Loss#

If customer friction is rising, a practical tuning pattern is to clean up overfiring rules, calibrate ML thresholds, and then use selective step-up checks like 3D Secure before hard declines. It is not a universal order, but it can reduce false positives while you watch fraud outcomes.

1. Clean up overfiring rules first#

Start with rules that are most likely too blunt. Hard-coded logic can block legitimate payments, including broad conditions like blocking all cards used abroad. Because rules are deterministic, you can usually identify the condition creating friction.

Prioritize a ranked view of block and hold rules by volume, approval impact, and dispute outcomes. If a rule drives a large share of declines while fraud outcomes stay flat, narrow or loosen that rule and re-measure. For ACH or SEPA flows, test draft allow and block rules before relying on them in production. If you cannot show trigger condition, active rule version, and pre and post results in transaction monitoring records, you are tuning blind.

2. Calibrate machine learning cutoffs, not just the model#

After rule cleanup, tune the threshold that converts a risk score into allow-or-block decisions. Threshold choice directly controls friction: above a threshold, a transaction is blocked; below it, it proceeds.

If risk settings include projected payment impact, use that signal before broad policy changes. Change one threshold at a time, document the prior setting, and use a defined observation window. Track dispute rate rather than raw dispute counts, because dispute rate is the better fraud and dispute signal on successful payments by charge date. The commonly cited excessive marker is 0.75%, and cardholders can dispute up to 120 days after payment, so early results can look better than they are.

3. Add step-up checks before hard declines#

For borderline traffic, step-up authentication can be used instead of immediate hard declines. 3D Secure is an extra authentication layer for card payments and can be applied selectively to higher-risk transactions instead of all traffic.

Use this lane for payments that need stronger proof but do not clearly justify an immediate block. Stripe describes adaptive 3D Secure for high-risk payments, and Visa positions 3DS as helping reduce fraud while improving approval accuracy. Visa also reports about a 45% fraud reduction for authenticated vs. non-authenticated ecommerce transactions. The control risk is over-expansion. If false positives rise while fraud outcomes stay flat, test one control change at a time and re-measure before wider policy changes.

For a step-by-step walkthrough, see AI Fraud Detection for Subscription Platforms Beyond Rules-Based Approaches.

Best for API and System-Level Fraud Coverage#

If fraud risk reaches your APIs, account layer, and backend actions, checkout controls alone are too narrow. Broaden scope first. API abuse, phishing aimed at credential theft or malware delivery, malware-related activity, and duplicate-request handling can all raise fraud risk before a payment event is reviewed.

- Broaden scope beyond the payment screen

Use F5's framing as a control reminder: cover APIs, the services they enable, and the systems and data they access. Include API abuse, phishing-linked credential theft, and malware-related patterns in scope, not only card or payout event rules. As a practical check, review every endpoint that accepts an object ID and confirm object-level authorization is enforced. OWASP's guidance is explicit on this point.

- Feed API anomalies into transaction monitoring

Treat unusual API behavior as a fraud signal, not only a security alert. F5's API security framing includes anomaly monitoring, and F5 also reports API-targeted bot activity in account-takeover attacks. In transaction monitoring records, keep traceability from API event to risk action: request path, actor or account ID, object touched, anomaly type, and resulting action decision. For a deeper design pattern, see Transaction Monitoring for Platforms: How to Detect Fraud Without Blocking Legitimate Payments.

- Use idempotent retries so risk actions do not duplicate

Retry handling should prevent duplicate risk actions for one business event. PayPal documents that omitting PayPal-Request-Id can duplicate a request, and Stripe documents that repeated requests with the same idempotency key return the original result, including 500 errors. Where the endpoint supports idempotency, use one client-generated key per business action and bind holds, reviews, and declines to that event rather than raw request count. Verify support by API and endpoint.

You might also find this useful: Device Fingerprinting Fraud Detection Platforms for Payment Risk Teams.

Comparison Table for Choosing the Right Control Mix#

At this point, the decision is less about which control sounds smarter and more about which one your team can defend later. Compare rules, machine learning, and hybrid controls on explainability, review load, and evidence quality before you scale automation.

| Control type | Best for | Explainability | False positives risk | Manual review dependency | Implementation complexity | Evidence that proves the decision path |

|---|---|---|---|---|---|---|

| Rule-based systems | Policy-heavy launches and flows where deterministic actions are required | High when rule logic is explicit | Tuning-dependent; assess with your own baseline and measurement window | Medium for edge cases and review-rule outcomes | Low to medium | Rule ID or name, matched condition or threshold, transaction or event ID, timestamp, action taken, and decision inputs. Where available, retain triggered-rule details, such as mode, version, transaction ID, and rule descriptions. |

| Machine learning | Real-time risk scoring | Medium to low unless explainability outputs are available | Calibration-dependent; measure with your own baseline and window | Medium to high for suspicious or policy-sensitive cases | High | Risk evaluation result, risk rating or score, action, timestamp, explainability output if provided, plus reviewer notes and override records when escalated. |

| Hybrid controls | Programs that need both AI risk scoring and explicit real-time rule actions | Medium to high if you keep both model and rule traces | May improve gray-area handling, but only if your own before/after cohort measurement shows it | Targeted to defined score bands, exceptions, or high-impact case types | Medium to high | Full sequence: input event, rules run, rules triggered or bypassed, model result, final action (approve, review, block, or step-up), reviewer disposition, timestamps, and override reason. |

Treat the evidence column as a control requirement. A real-time decision is not automatically audit-ready unless you can reconstruct how that outcome was produced.

Use vendor material here as market context, not benchmark proof. Stripe documents real-time AI risk evaluation, configurable actions like allow, block, review, and request 3DS, and a human review lane. Airwallex describes a hybrid model-plus-rules approach. Mastercard highlights explainability layers and cites average cloud latency of 100-120 ms. Kount, via NMI documentation, describes supervised and unsupervised ML, and Nexio's Kount response model shows practical triggered-rule and review evidence fields.

One operational check is review-queue timeout behavior. Nexio documents that some review-status transactions can auto-approve after 48 hours if no manual action is taken, so queue age and pending volume should be monitored as control signals, not just ops metrics.

FinMkt belongs here only as adjacent risk context. Merchant underwriting, onboarding, monitoring, and checks across over 60 global organizations are relevant for broader merchant-risk programs, not head-to-head transaction fraud performance claims.

Reporting Checklist and Audit Evidence Pack#

After you choose a control mix, the next requirement is evidence. You should be able to show what was decided, why it was decided, and how oversight worked.

1. Monthly reporting set#

Use a monthly reporting pack so trend shifts are visible early and reviewable. That cadence is consistent with external monitoring programs such as Visa's, which monitors fraud, disputes, and enumeration levels each month and uses a count-based ratio: fraud plus disputes over settled transactions. Visa also states identification levels effective 1 June 2025, at least 50 bps for Above Standard and at least 70 bps for Excessive acquirer portfolios.

Your internal pack does not need to copy VAMP, but it should answer one management question clearly: are controls reducing risk without creating avoidable friction? A practical set can include fraud rate trend, disputes trend, false positives trend, review backlog, and escalation outcomes. Treat false positives in the plain NIST sense: indicating something is present when it is not. Keep each metric audit-usable by defining the denominator, date window, and owner.

2. Evidence pack contents#

Build the evidence pack so a third party can reconstruct the decision path later, not just see the final outcome.

| Record | What it includes |

|---|---|

| Decision logs | Transaction or event ID, timestamp, action, rule hit or model output, and any override |

| Transaction-monitoring snapshots | The signal state at decision time |

| Manual review case notes | What evidence was reviewed and why the disposition was chosen |

| Policy-change history | What changed, who approved it, and when it went live |

Include:

- Decision logs: transaction or event ID, timestamp, action, rule hit or model output, and any override

- Transaction-monitoring snapshots: the signal state at decision time

- Manual review case notes: where manual review is used, what evidence was reviewed and why the disposition was chosen

- Policy-change history: what changed, who approved it, and when it went live

Retention and record-keeping anchors matter:

- If your system is in scope as high-risk AI under the EU AI Act, Article 12 requires technical capability for automatic event logging over the system lifetime.

- NYDFS requires annual transaction-monitoring certification by April 15, for the prior calendar year, via the DFS Portal, with supporting records maintained for examination.

- In U.S. SAR contexts, filing support records are retained for five years from filing.

3. Governance checkpoint#

Treat risk-tolerance updates as governance decisions, not only fraud-team tuning. For material changes tied to risk assumptions, use a documented governance checkpoint with risk analysis attached and clear ownership.

Federal Reserve model risk guidance supports this posture. Senior management should regularly report significant model risk and policy compliance through governance channels, and monitoring and validation work should be documented.

4. Change control and post-change verification#

For major rule or model updates, set a post-change verification window and document contingency steps if outcomes degrade. This aligns with model-risk expectations, where adverse outcomes can result from incorrect or misused model outputs.

In the verification window, check decision-rate shifts, false-positive behavior, confirmed-fraud outcomes, escalation quality, and log completeness. Also reassess whether changes in products, exposures, activities, clients, or market conditions require adjustment, redevelopment, or replacement of the model.

For implementation detail on monitoring design, see Transaction Monitoring for Platforms: How to Detect Fraud Without Blocking Legitimate Payments.

This pairs well with our guide on How Platforms Detect Free-Trial Abuse and Card Testing in Subscription Fraud.

If you are turning this checklist into operating controls, map each metric to status events and retry-safe payout actions in Gruv Docs.

Conclusion#

For teams evaluating fraud controls on payment platforms, including machine-learning options, a defensible design is layered rather than single-method. Use rules for defined actions, model scoring for changing patterns, and manual review for ambiguous or high-impact cases.

- Use a hybrid decision stack

Start with rule logic for known triggers, since rules can take action when a payment matches defined criteria. Add adaptive scoring for harder cases, and reserve manual review for transactions that remain unclear after automation. In practice, these controls can run in one flow: allow, block, review, or request an extra step such as 3DS.

A score is only useful if the action policy is explicit. One real example uses a 0-99 risk range, with example thresholds like 65 for elevated risk and 75 for high risk. Those are examples, not universal settings, so thresholds should be tested and tied to clear actions, reviewer paths, and documented fallback steps when false positives rise.

- Treat ownership and evidence as core controls

Program credibility comes from decision ownership and audit-ready records, not model sophistication alone. SR 11-7, dated April 4, 2011, emphasizes model development, implementation, validation, governance, policies, and controls. OCC model governance guidance also highlights documentation, internal controls, audit, and model inventory.

Set a strict traceability standard: for material approve, hold, or block outcomes, you should be able to reconstruct the event input, rule hit if any, risk evaluation outcome, and final case note. Manual review should supplement automation with human expertise, so review records should clearly capture trigger conditions and final disposition.

- Make reporting and escalation part of the design from day one

Reporting should be built into control design, not added later. In PSD2 scope, Article 96 requires payment service providers to provide fraud statistics at least annually. Outside that scope, decision-level evidence still helps teams defend reporting, incident review, and policy tuning.

A practical rollout is to set rules, scoring policies, and review paths early, then tune thresholds and escalation as operating history and governance mature. Keep reporting artifacts current: outcome logs, monitoring snapshots, review notes, and approved policy-change history.

When your team is ready to pressure-test cross-border hold/release workflows, review Gruv Payouts to see how compliance-gated status tracking can fit your model.

Frequently Asked Questions

Should payment platforms choose Machine learning or Rule-based systems for fraud detection?

Many platforms use a hybrid setup instead of choosing only one method. Rules provide deterministic actions, and documented implementations also combine rules with AI judgments in default controls. Use the mix that still lets your team explain, review, and audit each approve, hold, or block decision.

What should trigger Manual review instead of an automatic block?

Send a payment to manual review when risk signals justify a pause and human confirmation before capture. High transaction values and expansion into high-risk regions are common review triggers, and criteria should be explicitly defined by the platform. If reviewers cannot see the exact trigger, tighten case criteria before relying on fast auto-blocks.

How do you reduce False positives without increasing fraud losses and Chargeback fees?

Adjust controls in small steps and verify impact after each change instead of loosening multiple thresholds at once. This matters because some chargeback monitoring programs are monthly and use count and rate measures tied to transaction volume. If false positives drop but first-presentment chargebacks rise, roll back the last change and re-test.

Which metrics should compliance, finance, and risk teams review each month?

At minimum, review fraudulent-transaction data alongside total transaction data over the same defined period, plus chargeback count or rate. Keep denominator, time window, and owner fixed for each metric so results are comparable and defensible. This aligns with reporting logic that compares fraudulent transactions and total transactions over the same defined period, including payment-means breakdowns where required.

What changes when fraud controls run across multiple markets and payout rails?

Controls must handle local reporting obligations and rail-specific data requirements, not just different fraud patterns. In relevant EU PSP contexts, fraud statistics are reported by payment means, and revised FATF Recommendation 16 includes targeted beneficiary address data (country and town) with alignment checks via pre-validation, post-validation, or holistic monitoring. A low-risk score does not remove data-completeness obligations for the rail or market.

When should a fraud case be escalated to legal or specialist compliance review?

Escalate when the case may trigger regulatory reporting duties, when suspicious facts remain unresolved, or when activity appears ongoing and urgent. In the U.S. bank SAR context, filing is due within 30 calendar days from initial detection, with delay only up to an absolute maximum of 60 days if no suspect is identified. For urgent violations such as ongoing money laundering, immediate phone notification to law enforcement is required.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- airc.nist.gov/airmf-resources/airmf/5-sec-coretrusted

- bsaaml.ffiec.gov/docs/manual/06_AssessingComplianceWithBSAReg...trusted

- bsaaml.ffiec.gov/manual/AssessingComplianceWithBSARegulatoryR...trusted

- cisa.gov/sites/default/files/publications/Phishing%25...trusted

- cisa.gov/news-events/news/cisa-nsa-fbi-ms-isac-publis...trusted

- csrc.nist.gov/glossary/term/False_Positivetrusted

- dfs.ny.gov/industry_guidance/transaction_monitoringtrusted

- eba.europa.eu/single-rule-book-qa/qna/view/publicId/2018_4090trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How Payment Platforms Apply AI in Accounts Payable for Faster Invoices

AI in AP is most useful when it speeds up invoice handling without weakening approvals, payment controls, or record matching. The real question is not whether a tool can read an invoice. It is whether your process still holds when documents are messy, approvals are conditional, and payment release has to stay controlled. Three points should frame your decision before you compare tools:

Transaction Monitoring for Platforms: How to Detect Fraud Without Blocking Legitimate Payments

The job is to catch fraud without choking legitimate payouts. If your controls stop more fraud by freezing every unusual payout, the loss shows up somewhere else: false declines, delays, and avoidable friction for real contractors and sellers.

Payment Fraud Feature Engineering: 50 Signals That Matter

Fraud ML is useful only when it leads to decisions your compliance, legal, finance, and risk leads can defend. This article stays on action paths, ownership, and evidence, not model taxonomy or abstract accuracy claims.