Quick Answer

Prepare your payment platform for an acquisition by proving, with current records, that compliance controls work in production, transactions are traceable end to end, and financial reporting ties back to support files. Use one market-by-market scorecard with go, conditional-go, or no-go labels, named owners, verification dates, caveats, and clear evidence for every claim.

What Buyers Will Review Before Acquiring Your Payment Platform#

Acquisition prep for a payment platform is a cross-functional evidence test, not a finance-only exercise. Frame readiness around whether you can show compliance controls in production, trace money movement, and validate reporting without last-minute rework.

Use one market-by-market scorecard to make explicit internal calls: go, conditional-go, or no-go. These are operating labels, not regulator-defined categories. Use them to make expansion and M&A decisions from documented evidence rather than assumptions.

Keep the scorecard document-first. Formal acquisition planning frameworks emphasize written plan content, and the practical takeaway applies here: documented claims are stronger claims. That does not mean FAR Part 7 governs private payments M&A. It means undocumented claims are weak claims.

Use the same standard for compliance checks. A concrete verification pattern from the Federal Reserve's Regulation CC examination guide is to compare actual deposit transactions with disclosure statements and verify disclosures and notices tied to funds-availability rules. Keep the guide's own limitation in view too: it is an overview, not a complete legal statement.

Technical readiness also needs proof. In automated payments contexts, idempotency is an essential control, and known failure modes include isolation breaking under concurrency and retry-driven inconsistency. A scorecard entry like "reconciliation works" is not enough unless you can show operational evidence that controls hold under concurrency and retries.

Financial readiness is the third pillar. Treat it as a qualifier for scrutiny, not just a growth story, and be ready to show financial preparedness with records that support reported performance.

Before you start#

Use these assumptions throughout this guide:

- Evidence should be verifiable against live operations, not only policy documents.

- Open control gaps should sit on decision gates, not in an undefined post-close backlog.

- The useful output is one scorecard per market with owners, dates, caveats, and a clear decision label.

If a market needs extensive verbal explanation to appear ready, treat it as conditional-go until the evidence catches up.

For a finance and ops view of diligence, read How Platform Finance Leaders Decide M&A Payment Ops Readiness.

Define acquisition readiness in operator terms#

Treat readiness as an internal evidence test, not a slogan. In diligence, use a definition that forces decisions from documented proof, not presentation quality.

Step 1: Set a three-pillar working definition#

Use three pillars as your internal operating lens: Compliance Management System (CMS) maturity, technical traceability, and GAAP-ready finance. This is a working framework, not a universal standard.

| Pillar | Verification question | Not ready when |

|---|---|---|

| Compliance Management System (CMS) maturity | Can compliance show current policies, monitoring activity, and documented handling of non-compliance findings? | It depends on verbal explanation instead of records |

| Technical traceability | Can engineering trace a transaction from request through ledger impact and exception handling? | It depends on verbal explanation instead of records |

| GAAP-ready finance | Can finance tie reported numbers back to support files? | It depends on verbal explanation instead of records |

Ground that lens in documented diligence: show that you understand the requirements and have a repeatable process for keeping participants informed on requirements and acquisition approach.

If a pillar depends on verbal explanation instead of records, mark it not ready. Keep evidence current with an owner, version marker, and review date.

Step 2: Define outputs before scoring#

Define the outputs before you start scoring: an evidence pack, a market decision matrix, and a Day 1 integration risk log. Treat these as internal working artifacts, not source-mandated deliverables.

Each market decision should map to proof, and each open issue should be either a dated remediation item or a blocker. If a control gap could affect monitoring, findings, handoffs, reconciliation, or reporting, log it with an owner and decision date.

Do not label unresolved controls as "post-close" work without defined impact and dependencies.

Step 3: Separate deal-critical from nice-to-have#

Separate what you will need to defend early in diligence and control review from everything else. The first group is deal-critical. The rest is secondary.

In practice, polished plans are secondary. Current evidence for live controls is deal-critical. Where unresolved issues could drive a less-than-satisfactory evaluation outcome, keep them blocked until remediation is bounded, owned, and verifiable.

Related reading: How Modern CFOs Make Payment Platform Expansion a Strategic Driver.

Assemble prerequisites before you score markets#

Before you score any market, lock ownership and evidence so decisions are based on records, not live explanations.

| Scoring gate | What to verify | If missing |

|---|---|---|

| Designated owner | A designated Authorized Negotiator who is an employee completes the readiness assessment | Mark the item as unproven |

| Recency check | In eOffer, acknowledge the readiness assessment was completed within the past year | Mark the item as unproven |

| Request terms | Build the working file set from the MAS solicitation and its attachments | Do not score the claim as proven |

| Financial support | Include two years of financial statements, or other documentation that demonstrates financial responsibility | Mark the item as unproven |

Step 1: Assign a designated owner for readiness#

For MAS readiness, a designated Authorized Negotiator who is an employee must complete the readiness assessment. Treat completion as a recency-gated checkpoint; in eOffer, acknowledge it was completed within the past year.

Step 2: Anchor your review to the formal request terms#

Build your working file set from the MAS solicitation and its attachments, which define required offer elements, evaluation criteria, and terms to comply with. If a claim is not supported by that pack, do not score it as proven.

Step 3: Make financial-responsibility evidence explicit#

Include financial-history evidence in the diligence folder. If you do not have two years of financial statements, add other documentation that demonstrates financial responsibility and label that substitution clearly.

Step 4: Score only what is documented and current#

Apply a simple gate before scoring: owner assigned, readiness checkpoint current, solicitation-aligned evidence present, and financial-responsibility support documented. If one of those is missing, mark the item as unproven instead of forcing a precise score.

For a step-by-step walkthrough, see How to Hire a CFO for Your Payment Platform.

Build a market-by-market readiness scorecard#

Use one scorecard for each market or vertical so readiness decisions come from one evidence set. If a row cannot show current compliance, technical, and financial evidence together, mark it unknown or caveated.

The point is decision quality, not spreadsheet polish. A readiness assessment should help you decide before you commit.

Step 1: Keep each market/vertical in one row#

Create rows for real market and vertical combinations you may support, and keep all proof points in that same row. Use one working table with these columns:

| Market / vertical | Compliance evidence | Technical and operational fit | Financial evidence | Diligence confidence |

|---|---|---|---|---|

| [Market / Vertical] | Required controls/policies for this market; payment-specific gates marked unknown until documented | Due-diligence activities completed (site visits, industry days, one-on-one sessions, pre-proposal conferences); open operational constraints | GAAP support; internal-controls support; audit-ready documentation | Owner; evidence freshness; verification date; material caveats |

If evidence lives in a diligence folder, name the exact artifact in the cell. If support is verbal only, label it verbal and unverified.

Step 2: Treat hard gates as explicit fields#

Do not collapse gates into a single "compliance okay" note. Track each required field separately and give each one both:

- a status:

documented,partial,unknown, ornot applicable - a named artifact: policy, procedure, flow, decision log, training record, or other evidence-pack document

Include a recency check. Where readiness depends on formal acknowledgment, record whether it was verified within the past twelve months.

Step 3: Capture operational fit in the same row#

Keep operational fit next to compliance so false greens are obvious. At minimum, track which diligence activities were completed and what is still unverified.

Write specific states, not vague labels. Flag technology limitations or data bottlenecks directly in the row, since those can become scaling risks.

Step 4: Record confidence the way diligence will test it#

Add owner, evidence freshness, verification date, and material caveats to every row. Without those fields, claims are hard to defend.

For financial readiness, anchor to documented support for GAAP statements, internal controls, and audit-ready documentation. Note whether close processes are reliable each month and quarter. Keep caveats plain: if evidence is stale, partially tested, or still depends on unresolved steps, say so.

Use a strict rule: no market gets a confident status without a named owner, a verification date, and current artifacts for critical fields.

For a deeper look at KYC controls, see KYC best practices to reduce money laundering risks on a payment platform.

Step 1 audit compliance evidence and policy gates#

Start by stress-testing your own claims. If your Compliance Management System (CMS) is documented but not enforced in daily operations, treat that market as higher risk. If any core payout flow can bypass a required gate, flag that row as high risk and consider no-go until remediated.

Step 1.1 Test the CMS in operation#

Audit for operational proof, not policy text. The FDIC describes CMS as learning compliance duties, embedding requirements into processes, reviewing operations, and taking corrective action, with compliance as part of daily routines and with board and management oversight.

Use a practical test: pick a live flow and ask the owner to show where the requirement is enforced, how exceptions are detected, and what corrective action was recorded. Strong evidence is current and dated, and can include control ownership, training records, monitoring output, issue logs, and corrective-action records. If you only see polished policies without proof of review or remediation, treat the control as weak.

Step 1.2 Validate third-party controls with named evidence#

Apply the same evidence standard to your Third-Party Risk Management Program. The OCC Payment Systems handbook identifies Third-Party Risk Management and internal controls as core risk topics and includes an Internal Control Questionnaire, so third-party controls should be demonstrable in records, not summaries.

For each material third party, as an internal diligence check, verify onboarding evidence, recent monitoring evidence, and a clear escalation path with named ownership. Then confirm a live example showing the control cycle after launch, not just at onboarding.

If customer information is in scope and you are covered by the FTC Safeguards Rule, verify that your evidence reflects current rule changes. The rule took effect in 2003, was amended in 2021 and 2023, and certain breach and security incident reporting requirements took effect in May 2024.

Step 1.3 Verify policy gates by product and jurisdiction#

Check the gates that actually block activation or money movement. For each product and jurisdiction in your scorecard, record each required gate as documented, partial, or unknown, and attach the exact artifact for each status.

Do not rely on policy names alone. Confirm each gate is tied to the specific product variant and market and is enforced before the relevant action. If a core payout path can bypass a required gate in a target market, flag that row as high risk and consider keeping it no-go until the bypass is closed.

For more on audit trails and approval records, see Internal Payment Audit Trail for Platform Compliance.

Step 2 validate technical controls buyers test first#

Technical readiness is a diligence decision, not a narrative. If your production evidence is incomplete, keep expansion at conditional-go.

Step 2.1 Start with a technology stack assessment#

Start with a focused technology stack assessment based on real production evidence, not architecture diagrams. A reviewer should be able to reconstruct what happened from your records and outcomes without relying on one engineer's memory.

If evidence breaks at key handoffs or exception paths, log that immediately as a technical due-diligence risk.

Step 2.2 Check for technical due-diligence alarm bells#

Before buyer review, explicitly test for known technical due-diligence alarm bells: heavy technical debt, incompatibility with existing systems, and non-compliance issues. If any appears in a critical flow, assign an owner, document the remediation path, and state current exposure plainly.

Where a control expectation is deal-specific or not yet evidenced, mark it as unknown rather than asserting certainty.

Step 2.3 Capture findings in a repeatable checklist#

Turn your review into a repeatable checklist so technical assessment stays consistent across markets and product lines. A 20-point checklist format can be a practical model. Keep each line item evidence-linked and decision-oriented, and include integration hazards in the same log so risks are visible before integration planning starts.

Step 3 prove financial readiness without cleanup fire drills#

Once your transaction path is technically traceable, finance should be traceable too. From the provided materials, the defensible standard is documentation discipline: keep definitions stable, make changes explicit, and keep evidence connected as systems become more connected and complex.

Step 3.1 Align reporting definitions before you polish the deck#

Start with definition control, not formatting. If you use GAAP labels or GAAP-based views, keep the meaning consistent across periods and record any change instead of silently shifting categories.

Use a versioned change record format: Date | Change | Rationale. When a policy view or presentation rule changes, log what changed, when, and why so reviewers can follow the history without relying on memory.

Step 3.2 Prepare Audited Financial Statements and market-level views from the same base#

If you present both, build them from the same underlying records and keep the reconciliation path explicit.

A practical evidence pack can still help: the statements, the management view for the same periods, support schedules, and the change record. Prioritize reproducibility over slide polish.

Step 3.3 Tie finance outputs to compliance and operations evidence#

Treat alignment as a consistency check: period labels, entity scope, and incident references should not conflict across finance, compliance, and operations materials.

In connected environments, integration and security pressures increase complexity, which can make inconsistencies harder to track during review. A reviewer should be able to move from a financial claim to supporting operational evidence without contradiction.

Step 3.4 Flag accounting-policy assumptions while there is still time to explain them#

If an accounting-policy assumption is unresolved, mark it plainly and track it in the same change-controlled record. Include the current treatment, open question, owner, and expected decision timing.

This keeps diligence focused on known open items instead of late-stage rework.

Related: Financial Crime Compliance for Platforms: SAR Filing and Suspicious Activity Monitoring.

Set go conditional-go no-go decisions by market#

Set each market decision from evidence, not sentiment. Mark a market go only when compliance checks, technical controls, and financial support are verifiable in documents and operating proof.

Step 1 Apply one standard across markets#

Use the same decision test for the United States, Europe, and any narrower market slice. If one market gets a lighter bar because the upside looks attractive, the framework stops being reliable.

For each market, confirm three things:

- compliance checks are evidenced for the product scope you actually plan to run

- technical controls are evidenced, including traceability and exception handling

- financial support is evidenced with clear reconciliation to your reporting base

For every market row, record the owner, verification date, and evidence location. If support is only verbal, treat that gate as unverified.

Step 2 Use conditional-go only for bounded remediation#

Conditional-go should mean one incomplete pillar, a bounded fix, one named owner, and a dated checkpoint for closure.

Treat that checkpoint like a formal exception record, not a chat note. A concrete dated-checkpoint example is within 30 days of approval; use the same discipline for conditional market decisions.

If you cannot state the missing control or artifact, owner, and closure proof in one sentence, it is probably not a true conditional-go.

Also screen for founder dependency. If a market can operate only through one person for critical functions, buyers may view that as a single point of failure and may walk away.

Step 3 Call no-go early when the dependency is structural#

Use no-go when the blocker is structural rather than cleanup work, including operating models that still rely on one person to keep the market functioning.

A practical check is the 90 days question: can this market run profitably for 90 days without the founder as the operational bottleneck? If not, treat readiness as unresolved.

If the route decision and control boundaries are still unclear, mark no-go until they are defined.

Step 4 Compare United States and Europe side by side#

Use one method in both regions, then compare evidence side by side before final route selection.

| Market | Route being tested | What must be verifiable before go | If missing |

|---|---|---|---|

| United States | Merchant Acquiring or Merchant of Record (MoR) | Compliance evidence, technical traceability, and financial support tied to the same records base | conditional-go for one bounded gap; no-go for structural gaps |

| Europe | Merchant Acquiring or Merchant of Record (MoR) | The same three pillars, evidenced for planned product scope | Same rule |

| Cross-market ownership | Selected route in both regions | Named ownership, dated checkpoints where needed, and no single-person dependency | no-go if one-person dependency remains |

The key decision is not which region looks better in theory. It is which route in each region is supported by verifiable evidence now. Keep the decision log under records discipline so checkpoints, waivers, and assumption changes are dated and easy to retrieve.

If a market stays conditional-go, document the remaining gaps and reassess route assumptions with the same evidence standard: Explore Merchant of Record options.

Sequence execution from pre-LOI through Day 1#

Sequence this work as one evidence chain from pre-LOI through Day 1, because uncertainty anywhere in that chain is where buyers start discounting value or walking away.

| Phase | Primary action | Evidence focus |

|---|---|---|

| Pre-LOI | Complete preliminary diligence, lock scope claims, finalize owners, and keep a short red-flag list | Each claim points to a dated record and clear source location |

| Confirmatory diligence | Run a multi-pronged, multi-month diligence process in a virtual data room | Documents stay versioned with clear as-of dates, owners, and revision history |

| Pre-close window | Use the signing-to-close period as a readiness checkpoint | Check whether books can close within five business days and whether investor-grade reporting outputs are reproducible |

| Day 1 | Operate within already-supported scope and log exceptions immediately | Follow the same documented evidence trail used in diligence |

| Post-Day 1 | Keep launch-critical controls separate from the broader improvement backlog | Track each remediation item with owner, due date, and closure evidence |

Step 1 Freeze supported scope before the LOI#

Before issuing an LOI, complete preliminary diligence and lock scope claims to what you can evidence now. Finalize owners, keep a short red-flag list, and make sure each claim points to a dated record and clear source location.

If a claim is still verbal or inconsistent across teams, treat it as a gap rather than a completed capability. The pre-LOI output should be simple: an external reviewer can see what is in scope, who owns it, and what proof supports it.

Step 2 Publish versioned evidence during confirmatory diligence#

After LOI, run confirmatory diligence as part of a multi-pronged, multi-month diligence process and manage documents as versioned artifacts, not loose files. Use a virtual data room and keep finance and operating evidence organized with clear as-of dates, owners, and revision history.

This is where consistency matters most. A buyer should be able to trace a claim across records without conflicting dates, definitions, or owners.

Step 3 Use the pre-close window as a readiness checkpoint#

If your deal includes a signing-to-close period, use it to prove your reporting and documentation discipline under transaction pressure. Keep measurable checkpoints visible, such as whether books can close within five business days, and whether investor-grade reporting outputs are reproducible from your current records.

If those checkpoints drift, record the gap explicitly and assign ownership before Day 1. Do not let unresolved items sit as implied assumptions.

Step 4 Run Day 1 against documented evidence, not new promises#

On Day 1, follow the same documented evidence trail used in diligence. The goal is controlled continuity: operate within already-supported scope, keep records and ownership clear, and log exceptions immediately.

Avoid expanding claims or scope on Day 1. If something is not already evidenced, treat it as post-close remediation.

Step 5 Keep post-Day 1 remediation separate from launch-critical controls#

After Day 1, separate launch-critical controls from the broader improvement backlog so unresolved risk stays visible. Track each remediation item with owner, due date, and closure evidence, and update the underlying records when the gap is closed.

This keeps post-close cleanup from being mistaken for completed readiness.

Common mistakes that kill deals and how to recover#

Deals often break on avoidable credibility gaps, not just hidden complexity. The practical fix is to narrow claims to what you can evidence now, then close gaps with dated artifacts before you expand the story.

1) Overstating readiness when controls are still partly manual#

If core controls still depend on manual review, treat that as a scope boundary, not a fully scaled capability. Manual steps can be workable. Undocumented boundaries are what create diligence surprises and can change buyer risk perception.

Recovery:

- Reduce claims to the exact flow, segment, and geography you can prove today.

- Publish those boundaries in the data room with owner, date, and exception path.

- Mark unsupported areas as conditional or out of scope until evidence is complete.

2) Treating GAAP normalization as a late-stage cleanup task#

Starting normalization during active outreach can weaken trust in your numbers at the worst moment. Audited financials help, but transaction readiness also depends on a normalized earnings view, for example through Quality of earnings (QoE) report work that starts from GAAP net income.

Recovery:

- Build the GAAP bridge well before buyer outreach, not during it.

- Keep support for adjustments and core diligence records organized in the data room.

- Make sure the same revenue, cost, and margin story is consistent across internal and external reporting.

If that bridge is still moving, consider pausing outreach until it is stable. For a deeper finance checklist, see IPO Readiness for Payment Platforms: The Financial Operations Checklist.

3) Polishing the growth narrative before the evidence pack#

A strong narrative cannot compensate for thin diligence artifacts. Buyers can move quickly when records are missing.

Recovery:

- Prioritize concrete artifacts first: vendor contracts, tax returns, entity docs, governance records, and clear ownership.

- Version documents with as-of dates so claims are traceable.

- Use a "go to market with your data room" standard, not a pitch-deck standard.

4) Launching new scope with unresolved dependency ownership#

If a rollout depends on unresolved operational ownership, treat it as not ready for signed scope. Integration planning is often underfunded in the deal lifecycle, so unresolved dependencies should be explicit blockers, not assumptions.

Recovery:

- Pause expansion claims for that scope.

- Re-score readiness and document blockers, owner, and closure evidence.

- Keep Day 1 scope limited to what is already evidenced, then handle remaining items as post-close remediation.

A practical Day 1 checkpoint is aligned leadership communication within 48 hours after close, then disciplined execution through the first 100 days.

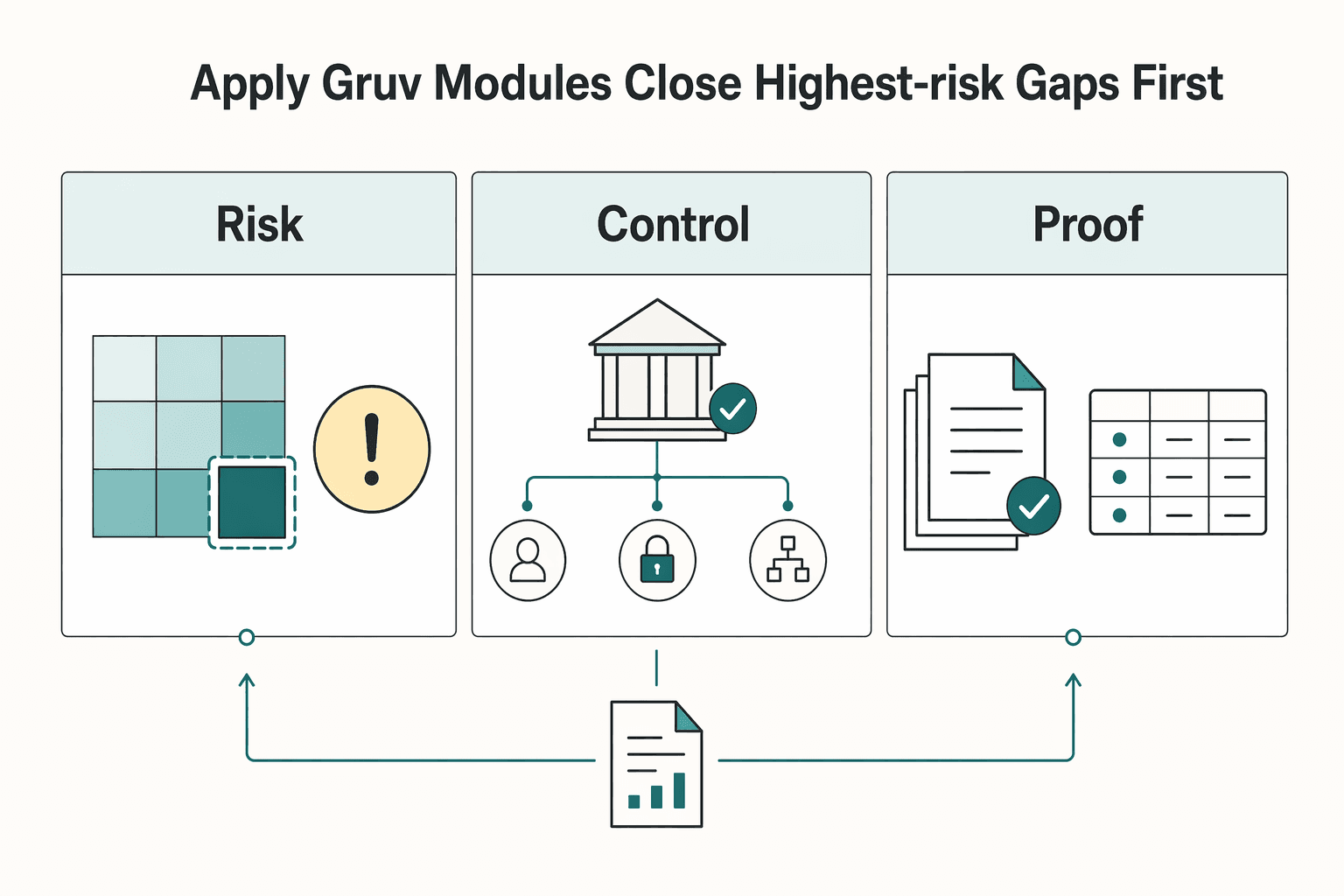

Apply Gruv modules to close the highest-risk gaps first#

Use modules to close the highest-risk gap you can evidence now, not to imply broader readiness. Readiness is only proven when the enabled capability is governed with clear oversight, accountability, and audit-ready records.

Step 1: Scope Merchant of Record (MoR) vs Merchant Acquiring by market and program. Treat this as an operating design choice, not a universal answer. For each scope, document what is enabled, who owns approvals, and how regulatory accountability remains with your institution. If ownership is unclear, keep the scope conditional.

Step 2: Use Virtual Accounts and Payout Batches only where control evidence is explicit. Do not treat a module label as proof of control quality. In your evidence pack, show the transaction path, who approved key actions, and how exceptions are handled. If those records are incomplete, treat the gap as open.

Step 3: Define and evidence required compliance policy gates in the flow. Policy text alone is not enough. Enforcement must be visible in records. Keep audit-ready trails for approvals, denials, overrides, and exceptions with dates and accountable owners. If sensitive actions can proceed without resolved checks where required, treat that as a governance gap.

Step 4: Qualify every claim by market and program. Coverage varies, and some capabilities are available only when enabled. For each claim, include jurisdiction, product scope, enablement status, verification date, and caveats. If you cannot prove scope cleanly, do not present it as ready.

Conclusion and copy-paste readiness checklist#

Treat this section as not ready if any check below lacks a dated CMS excerpt, a named owner, and a working evidence link. Use one shared tracker so teams are not reporting different readiness states from separate files.

Step 1 Confirm one scorecard exists for every core claim#

Use one scorecard with one row per core claim and one status per row: supported, partial, or unsupported. Each row should include the owner, last verification date, and the caveat behind the status. Verification point: every concrete claim has one current row, and unsupported areas are marked as out of scope.

Step 2 Confirm CMS evidence is current and mapped to PPS/IPPS mechanics#

Your CMS evidence should show payment-system mechanics, not policy assumptions from other domains. Map evidence to PPS predetermined reimbursement, IPPS payment per inpatient case or discharge, and annual update elements (base rates, wage indexes, MS-DRG definitions and weights). Verification point: each area has attributable, current records that can be reviewed directly.

Step 3 Confirm rate-update statements keep their qualifying conditions#

For FY 2026, keep the 2.6% IPPS increase tied to its stated conditions (general acute care hospitals that participate in IQR and are meaningful EHR users). Keep the related rate-change context intact (3.3% market basket update reduced by a 0.7 percentage-point productivity adjustment). Verification point: no percentage is presented without the condition or context in the source.

Step 4 Confirm episode and timing details are stated exactly#

State that IPPS pays per inpatient case or discharge, and keep episode timing details aligned with the source. Verification point: timing details are stated exactly and not paraphrased.

Step 5 Confirm unverified areas are explicitly marked as unverified#

If support is verbal only, label it verbal and unverified. If one of the prerequisite gates is missing, mark the item as unproven instead of forcing a precise score. Verification point: unverified areas are explicitly marked as unverified, unknown, partial, or unsupported.

Frequently Asked Questions

What does acquisition-ready mean for a payment platform in practical terms?

It means Day 1 readiness: the buyer, target, or combined company can function legally and operationally at closing. Core operations and controls need to work in production, not just in presentations. If controls, approvals, or customer support break at close, readiness was overstated.

What must be ready before buyer diligence starts?

Before diligence starts, have a clear, current operating evidence set that can be reviewed quickly and updated as diligence progresses. The process is systematic and typically runs through stages rather than a single upload. Be ready for periodic reassessment and risk-profile updates.

Which compliance artifacts do acquirers expect first?

Start with records showing the compliance program is operating, not just documented. Useful first artifacts include current monitoring output, issue logs, corrective-action records, training records, and named control ownership. Buyers want evidence the program can stay effective through disruption.

How do technical controls change valuation and integration risk?

They affect buyer confidence because they shape expected integration effort. Heavy technical debt, incompatibility with existing systems, and non-compliance issues are known due-diligence alarm bells. Unresolved technical debt can raise execution risk and increase post-close remediation work.

How should founders prioritize country expansion against compliance complexity?

Use a risk-based approach instead of giving every market equal effort. Apply deeper review to higher-risk relationships and lighter review to lower-risk services. Prioritize markets where your operating model and controls are already demonstrable, and hold conditional markets until the evidence is solid.

What are the most common Day 1 post-merger failure points?

The most common Day 1 failures are operational: payroll, systems, customer support, controls, approvals, or leadership decisions are not ready to function together at closing. Another recurring risk is post-acquisition vendor disruption, including product sunsets and support degradation from personnel loss. These failures are especially damaging because the compliance program is still expected to remain effective through disruption.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- acquisition.gov/afars/chapter-5-definitionstrusted

- acquisition.gov/far/part-7trusted

- cms.gov/Outreach-and-Education/Medicare-Learning-Net...trusted

- comptroller.war.gov/portals/45/documents/fmr/volume_02b.pdftrusted

- department.va.gov/procurement-acquisition-and-logistics/nation...trusted

- dodcio.defense.gov/Portals/0/Documents/Library/RequirementsAcqu...trusted

- dodcio.defense.gov/Portals/0/Documents/CMMC/AssessmentGuideL2.pdftrusted

- fdic.gov/consumer-compliance-examination-manual/ii-3-...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: