Quick Answer

Match the role to the risk most likely to stop execution first. For how to hire a cfo for a payment platform, define boundaries across Treasury Management, Controllership, and FP&A, then select Controller, VP Finance, Fractional CFO, or full-time CFO based on the active bottleneck. Put decisions in writing with a 180-day mandate, including 30/60/90/180 deliverables and clear pause authority when reconciliation or payout evidence is incomplete.

What a CFO for a Payment Platform Needs to Own#

Hiring a Chief Financial Officer (CFO) for a Payment Platform is a risk decision first, not a routine finance hire. If your product touches money movement, processor oversight, new-market rollout, or always-on settlement, the operating bar is higher than it is for a typical SaaS finance leader.

That bar is higher for concrete reasons. If your activities include accepting funds or other value from one party and transmitting them onward, you may be in money transmission scope depending on your structure and facts. Some businesses in that scope can be treated as money services businesses, which can trigger Bank Secrecy Act recordkeeping and reporting obligations and federal registration requirements.

Even when legal and compliance define the perimeter, finance feels the impact fast. Processor relationships are treated as higher risk and need stronger diligence and monitoring. Instant payments settle on a 24x7x365 basis, which makes treasury a live operating constraint.

That is why how to hire a cfo for a payment platform is not the same as hiring a first finance leader at a standard software company. In payments, weak finance ownership can show up as control gaps, liquidity strain, and rollout decisions made without enough finance input.

Expansion raises the stakes further. State money-transmission regimes are moving toward more common standards around capital, bonding, and liquidity, but they are not universal. As of February 26, 2026, 31 states had enacted the Money Transmission Modernization Act in full or in part.

Before you start#

Before you open the search, confirm three points in writing. The three points below should shape the scope, level, and ownership split before candidates start reframing the role:

| Check | What to confirm |

|---|---|

| Actual risk perimeter | Document what your platform does with funds, where finance depends on legal or compliance input, and which activities create treasury or reporting obligations. |

| Current failure point | If close quality and reconciliation are weak, consider a Controller. If planning cadence and business partnering are the core gap, consider a VP Finance. If expansion governance, capital decisions, and treasury pressure are active, you are closer to true CFO scope. |

| Ownership split | Define the split between FP&A and the close-and-controls function so you do not hire someone who is strong in narrative and modeling but weak on controls around cash, settlement, and launch approvals. |

- Your actual risk perimeter. Do not assume you are or are not in MSB scope. Document what your platform does with funds, where finance depends on legal or compliance input, and which activities create treasury or reporting obligations.

- Your current failure point. If close quality and reconciliation are weak, consider starting with a Controller. If planning cadence and business partnering are the core gap, consider starting with a VP Finance. If expansion governance, capital decisions, and treasury pressure are all active, you are closer to true CFO scope.

- Your ownership split. FP&A and the close-and-controls function are different jobs, and many leaders are stronger in one than the other. If you skip this split, you increase the risk of hiring someone who is strong in narrative and modeling but weak on controls around cash, settlement, and launch approvals.

The core promise of this guide is simple: do not default to a full-time CFO just because the stakes are high. Choose the model that matches the work now, whether that is a Fractional CFO, VP Finance, Controller, or full-time CFO, and set clear ownership for treasury, the controller-side work, and planning from day 0.

What follows is a practical hiring sequence with decision checkpoints, interview proof, and a 180-day execution plan your Finance Team can run against. The goal is not just to fill a seat. It is to de-risk rollout decisions before market conditions, processor requirements, or liquidity pressure make the decision for you.

Where generic CFO advice breaks for payment platforms#

Generic CFO hiring guidance can help you design the role, but it is not enough to de-risk payment operations. Mainstream guides from Bessemer Venture Partners, GHJ Advisors, Shiny, K-38 Consulting, and oCFO mostly help you choose structure: full-time versus fractional, interim versus permanent, and FP&A versus the controllership track.

That is useful for defining the seat. It does not by itself prove a candidate can run finance where payouts, settlement, and expansion readiness can fail in production.

Step 1. Use mainstream guidance to scope the role, not prove operating fit#

Bessemer explicitly frames its guidance through SaaS finance leaders and separates the controllership function from FP&A. GHJ defines fractional CFO support as part-time or contract-based, while Shiny, K-38, and oCFO also center the engagement model and role type. Use that material to set the hiring architecture, then move quickly to payments-specific proof.

Step 2. If money movement and expansion are your top risks, prioritize payment-operations depth#

When rollout risk is tied to charges, payouts, and compliance obligations, payment-operations depth should outrank generic SaaS scaling experience. Stripe states that enabling charges and payouts requires collecting and verifying specific information, and that charges or payouts can be paused if required information is not provided or verified to required thresholds. IRS guidance also notes that businesses engaged in fund transfers can be treated as MSBs, and that many MSBs must meet BSA recordkeeping and reporting requirements.

Keep the interview test operational: who owns verification exceptions, which metric signals a launch blocker, and who can stop rollout when onboarding data is incomplete. If the answers stay at board-deck level, you are probably seeing FP&A strength without enough operating control.

Step 3. Pressure-test reconciliation and treasury judgment before trusting the forecast#

Copied SaaS playbooks can break at reconciliation and cash timing. Stripe states that you are responsible for reconciling manual payouts against transaction history, and Adyen documents transaction-level settlement reconciliation with per-transaction cost visibility.

Ask for one concrete walkthrough: how settlement was tied to the ledger, how open breaks were tracked, what daily evidence was reviewed, and how treasury decisions changed when cash timing shifted. A key interview risk is polished planning without clear evidence of close discipline and treasury execution.

Related: How to Measure AP Automation ROI: A CFO's Framework for Payment Platform Finance Teams.

What to prepare before you start the search#

Before you think about recruiters or candidate outreach, get your operating facts in order. If you are working out how to hire a cfo for a payment platform, start with written scope, a usable finance baseline, and clear role constraints.

Step 1. Define scope in writing#

Write a short search brief before opening the role. At minimum, document why you are building a payments business, how you will integrate payments, and your payments strategy. Then translate that into hiring scope and where finance should review launch decisions before go-live.

Use one practical test: could a candidate read this and identify where finance should intervene? If not, you may attract broad SaaS narratives instead of payment-operations judgment.

Step 2. Assemble a baseline evidence pack#

Build the search around your current finance baseline, and separate the close-and-controls track from FP&A on purpose. FP&A covers analytical business partnering, forecasting, and budgeting. The controller-side work is about getting the books right and keeping close operations reliable.

Include, at minimum:

- close quality signals from the books and the close function

- forecast reliability and budgeting assumptions from FP&A

- unresolved payment reconciliation breaks and their current status

This is the readiness check: you should be able to point to open mismatches and explain whether they are timing differences, errors, or possible fraud risk.

Step 3. Set role constraints before interviews shape them#

Decide expected ownership across CFO, VP Finance, and Controller before candidate conversations start. Be explicit about decision rights, what requires shared input, and where finance review is needed before launch decisions.

Set the engagement model up front too: a full-time hire path, or a bounded Fractional CFO bridge during the search period. If you use fractional support, document the end point, required decisions, and handoff expectations so interim ownership does not stay vague. For a step-by-step walkthrough, see How to Build a Deterministic Ledger for a Payment Platform.

Step 1 Choose the right role now#

Match the role to the finance failure most likely to disrupt execution in the next few quarters, not to the most senior title. For how to hire a cfo for a payment platform, use this bias: a Controller is often the better fit when close and reconciliation quality are the urgent gap; a VP Finance is often the better fit when planning cadence is weak; and a Chief Financial Officer (CFO) is usually the better fit when capital, risk, treasury, and expansion governance are all active together.

| Role | Choose this role when | First ownership focus | Verification point |

|---|---|---|---|

| Controller | Close is unreliable, reconciliations are aging, finance operations need tighter control | Close operations, close discipline, reconciliation remediation | You can track each open reconciliation break by age, owner, and whether it is timing or error |

| VP Finance | Budgeting and forecasting are inconsistent, and leaders do not have a decision-ready view | FP&A cadence, forecast assumptions, budget ownership, management reporting | A regular forecast exists, assumptions are documented, and leaders are using one version of the numbers |

| CFO | Capital decisions, risk oversight, treasury pressure, and expansion decisions need one accountable owner | Company-level finance direction across the controller function, FP&A, treasury, and launch governance | Finance sign-off is clear on major launch or funding decisions, with one leader resolving cross-functional tradeoffs |

Use the table as guidance, not as a universal rule. FP&A and the controller function are distinct, and expecting one hire to cover deep book-close execution, forward planning, and company-level risk ownership from day one often creates strain early.

Improve treasury sooner if payouts can be blocked#

If treasury mistakes can delay payouts or launch timing, consider moving treasury to CFO-level ownership earlier rather than deferring it. In platform operations, payouts are transfers from the platform account to external destinations, and paused payouts stop those transfers. Missing required tax or account information can also pause payouts.

That is why treasury cannot be treated as a back-office afterthought in payments. Liquidity risk is a core risk category in payment, clearing, and settlement systems. If payout timing and funding decisions are already affecting launches, one finance leader should own the decision path end to end.

Write the boundary map before you post the job#

Define boundaries across Accounting, Controllership, and Financial Planning and Analysis (FP&A) before interviews begin:

- Accounting: financial records and statement inputs

- Controllership: close quality, reconciliations, and reporting-reliability discipline

- FP&A: budgeting, forecasting, and management decision support

Use one checkpoint: every recurring finance decision should have one named owner. If ownership is shared by default, you are building overlap before the hire even starts.

Define the VP Finance to CFO upgrade trigger now#

Set the upgrade trigger before opening the role so scale does not force a rushed reorg. One practical trigger to consider is when one leader must simultaneously coordinate the close-and-controls track, FP&A, treasury, and expansion decisions as operating complexity increases.

Watch for this pattern: planning stays on track, but the same leader is repeatedly pulled into payout exceptions, risk reviews, and launch-approval tradeoffs. When that becomes routine, the role may already be CFO-shaped, and the title should catch up. Related reading: How to Build a Subscription Billing Engine for Your B2B Platform.

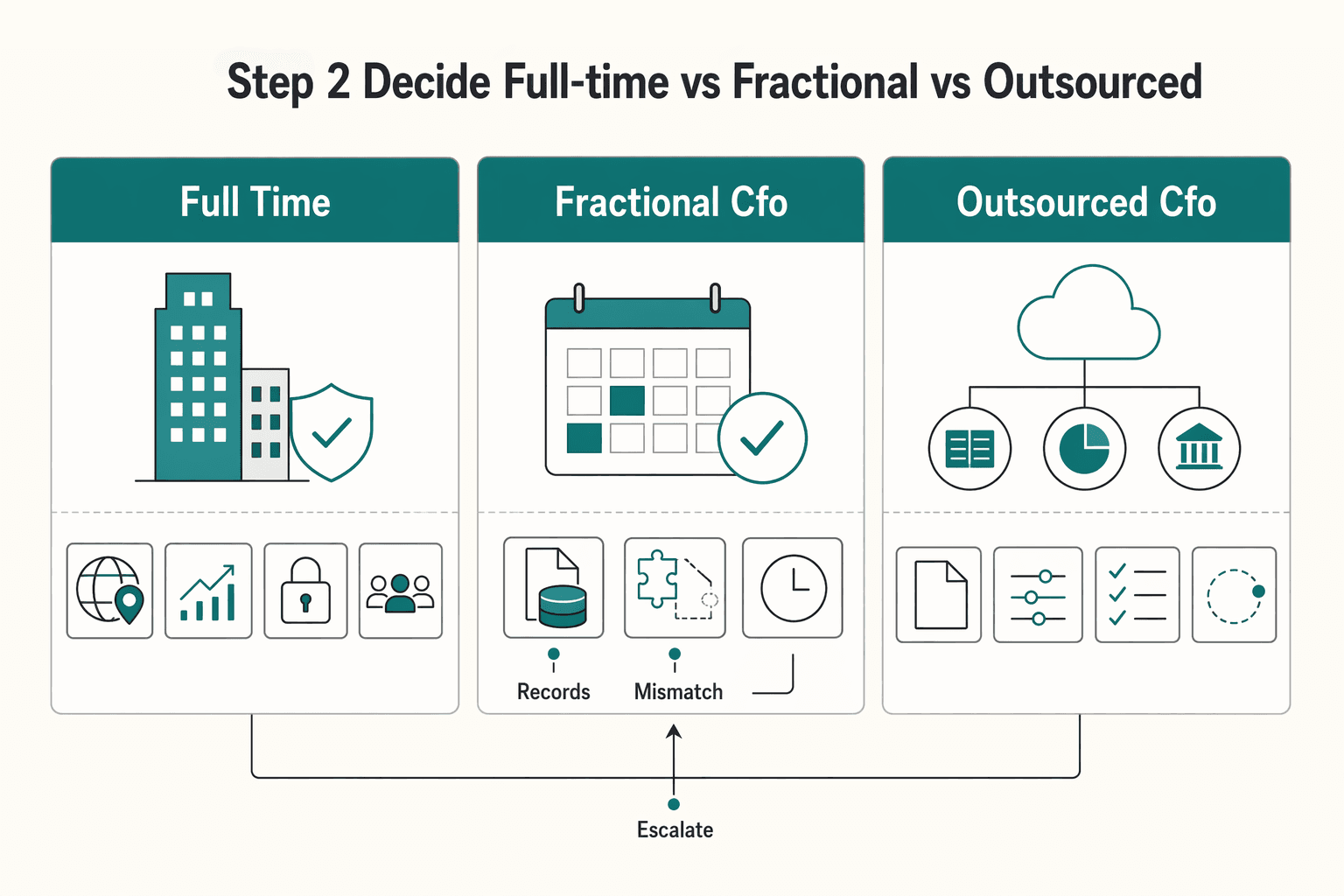

Step 2 Decide full-time vs fractional vs outsourced#

Once the role is clear, choose the model based on decision speed and continuity. If you are entering new markets while redesigning controls, default to full-time Chief Financial Officer (CFO) leadership. Use fractional or outsourced support for a clearly bounded phase, not as a long-term substitute for accountable ownership.

| Model | Cost structure | Decision latency | Domain depth to prove | Continuity and failure risk |

|---|---|---|---|---|

| Full-time CFO | Fixed salary plus broader employment cost. Higher committed spend, but no hourly meter on escalation time. | Typically the lowest latency when launch, treasury, and control decisions happen daily. One accountable owner can resolve tradeoffs across Product, Ops, the books team, and FP&A. | Must show payment-domain decisions, not only SaaS finance leadership. Ask for examples tied to market entry, treasury pressure, control design, or safeguarding remediation. | Usually lower continuity risk when embedded well. A common failure mode can be strong strategy but weak integration with the controller function and day-to-day book-close execution. |

| Fractional CFO | Usually hourly, part-time, or fractional. CFO.com cites outsourced CFO pricing in the ballpark of $150 to $200 per hour, or more by region. | Moderate latency. Works when scope is planned and bounded; can weaken when issues surface between scheduled blocks. CFO.com also raises accountability concerns when support is only 10 hours per month. | Needs proof of payment-specific decisions made in limited-time seats, not advisory-only positioning. | Dependency risk can rise when one advisor holds key context. Failure modes can include weak integration with the Controller or books owner, and gaps between strategy and day-to-day close, reconciliation, or control follow-through. |

| Outsourced CFO | Variable spend, often through a firm. May look cheaper at the start versus a full-time hire. | Can be slower than full-time when requests queue through provider workflows or rotate across people. | Require proof of payments experience in delivered work, not firm branding or generic growth claims. | Higher third-party dependency risk. FCA guidance stresses that firms relying on providers and outsourcers still must manage that dependency to reduce disruption. Failure modes can include diluted ownership, handoff gaps, and concentrated reliance outside your team. |

Use one rule when expansion and controls collide#

Use this rule: if market entry and control redesign are happening together, pick full-time leadership.

Under PSD2 Article 5, authorization includes both a business plan with a forecast budget for the first 3 financial years and governance and internal-control descriptions, including administrative, risk-management, and accounting procedures. When both tracks move at once, finance ownership has to connect forecast, controls, and execution continuously.

The control-risk backdrop is active too. The FCA has said some payments firms do not currently have sufficiently strong safeguarding practices, and some present unacceptable risk of harm to consumers and market integrity. In that setting, slower finance decision cycles become an operating risk.

Keep fractional or outsourced support bounded and testable#

Fractional support is often most useful when the scope has a defined end state, such as bridging a search or cleaning up ownership before a full-time start date.

Set one practical check: name the internal books owner and internal close owner, then define which decisions the external or fractional lead can make immediately versus what still requires founder sign-off. If launch finance gates stall when that person is unavailable, the model is too thin.

Apply the same check to outsourced providers. Outsourcing does not transfer accountability. FCA guidance also notes that arrangements outside strict outsourcing definitions still sit within expectations for governance, risk management, and systems and controls. You still need an internal owner for evidence, follow-up, and escalation.

Ask for payment evidence, not polished resumes#

Before you select any model, require proof of payment-domain judgment, not just generic SaaS experience. SaaS heuristics like $5 million to $25 million ARR for full-time finance hiring are not payment-platform rules. Ask for evidence in three forms:

| Evidence form | What it should show |

|---|---|

| Redacted market-entry or authorization support package | Finance input on forecasts, governance, or internal controls. |

| Decision balancing growth speed against a control requirement | A concrete decision in treasury, safeguarding, or reporting reliability. |

| Implementation with Controller or books counterparts | Evidence of implementation with Controller or books counterparts, not strategy advice alone. |

Use one screening question: what did they personally change when growth and controls conflicted? Strong answers identify the decision, document, counterpart, and operating consequence. In payments, treasury is a control function tied to business growth, not a background planning task.

Before you lock the hiring model, sanity-check how payout controls, status visibility, and reconciliation surfaces would work in your target rollout.

Step 3 Write the mandate for the first 180 days#

Write this mandate before the search advances. In a payment business, the first 180 days should assign day-0 ownership and tie launch authority to money-movement evidence, not to broad goals.

Step 3.1 Name one accountable owner for each finance track#

Set one rule up front: Treasury Management, FP&A, and Accounting each need one named owner from day 0. That owner may delegate execution, but accountability cannot be shared or vague.

| Track | Day-0 scope |

|---|---|

| Treasury Management | Cash positioning, funding visibility, safeguarding-related evidence where relevant, and approval design around money movement. |

| FP&A | Forecast ownership, scenario planning, market-entry economics, and founder reporting cadence. |

| Accounting / Controllership | Close, reconciliations, policy ownership, and control execution. |

Keep the tracks separate in writing. FP&A is analytical business partnering. The controller-side work is about getting the books right. "Not a lot of people are good at both." If you collapse these into a single "finance" label, close quality and reconciliation risk can stay hidden until launch pressure exposes it.

- Treasury Management: cash positioning, funding visibility, safeguarding-related evidence where relevant, and approval design around money movement

- FP&A: forecast ownership, scenario planning, market-entry economics, and founder reporting cadence

- Accounting / Controllership: close, reconciliations, policy ownership, and control execution

Step 3.2 Set 30/60/90/180 outputs#

Treat this as an operating template, not a regulator-mandated format. The first three months are a critical transition window, and many CFOs use roughly six months to learn the business before driving larger change.

| Timing | Required deliverable | What to verify |

|---|---|---|

| Day 30 | Finance operating model with named owners across Treasury Management, FP&A, Accounting, plus Product and Ops counterparts | Each critical process maps to one accountable owner and a documented escalation path |

| Day 60 | Close and reconciliation remediation plan | Open reconciliation items, close-calendar reality, and control gaps are documented with priority order |

| Day 90 | Market-launch sign-off criteria and founder reporting cadence | Launch criteria include explicit finance conditions, and founder reporting runs on a fixed cadence |

| Day 180 | Updated control design and failure-scenario readiness | Written policies, internal controls, and risk-based audit expectations are reflected in key payment flows; segregation-of-duties gaps and return-of-funds readiness are addressed where relevant |

Use artifact language, not intent language. "Improve reporting" is too vague. A defined reporting pack and cadence is testable.

Step 3.3 Tie launch gates to money movement#

State directly that finance review is required before enabling new payout or money-movement flows on the Payment Platform. Treat this as an internal control requirement, not a velocity preference.

Before launch, require an evidence pack that shows:

- current control gaps on the flow

- who initiates, approves, records, and reconciles movement

- any segregation-of-duties exceptions

- escalation steps if evidence is incomplete or a control fails after launch

You do not need a generic industry quorum model. You do need an internal rule for what happens when control evidence is not ready.

If your firm is in the FCA safeguarding perimeter, include timing pressure explicitly in the mandate. The supplementary safeguarding regime takes effect on 7 May 2026, so launch sequencing and remediation priorities should reflect that date.

Step 3.4 Document the interface with Product and Ops#

The mandate is not complete until the handoff with Product and Ops is explicit. Finance strategy is expected to be developed in close collaboration with other leaders, and in payment contexts the interface can extend into analytics, credit, and compliance-related decisions.

Keep it operational: what Product must provide, what Ops must confirm, what finance returns, and how that output changes launch sequencing. The mandate works when ownership, evidence, and decision points are explicit from the start. If you want a deeper dive, read Lean Finance and the Modern CFO: How Payment Platform Leaders Evolve from Cost Center to Strategic Driver.

Step 4 Lock ownership boundaries with Ops, Product, and Compliance#

Once the mandate is set, lock decision rights before launch pressure blurs accountability. Without explicit ownership, pricing, rollout, treasury, and control decisions get bundled together and gaps in evidence are easier to miss.

Use a simple RACI matrix with named people, not just departments. In payment-service governance, some regimes explicitly require clear lines of responsibility and named responsible individuals, so treat this as a live governance control rather than a static org-chart artifact.

Step 4.1 Map the decision rights#

Use one matrix for recurring launch, pricing, and exception decisions, with one accountable owner per row.

| Decision area | CFO | VP Finance | Controller | Ops | Product | Compliance |

|---|---|---|---|---|---|---|

| New market launch | A | R | C | R | R | C |

| Pricing and unit economics change | A | R | C | C | R | C |

| Treasury or accounting exception before launch | A | C | R | C | I | C |

This is not a universal template, and smaller teams may combine titles. If you do not yet have all three finance roles, map each responsibility to the person covering it today and mark temporary overlap.

Step 4.2 Separate controllership from FP&A#

Write the boundary in plain language and keep it explicit. The close-and-controls function covers records, reporting, and internal controls. FP&A covers planning, budgeting, forecasting, and decision-oriented analysis.

Keep those tracks distinct even if one leader temporarily owns both. Require controller-side review when decisions affect money movement, settlement, recognition, or reconciliation. Require FP&A review when decisions affect assumptions, margin, market-entry economics, or capital needs. Require both perspectives before approval when decisions affect both tracks, including:

- pricing changes that alter fee timing, reserves, or payout behavior

- market launches with uncertain reconciliation or close impact

- product changes that improve conversion but increase cash-timing risk

Step 4.3 Set exception and pause authority#

Define pause authority before the next launch review. If Treasury Management or book-close evidence is incomplete, your escalation path should state who can block readiness, who can escalate to an executive pause, and who must be consulted when regulatory obligations are affected.

Record the decision and outcome when a pause is raised, maintained, or lifted. Where applicable rules require retained compliance records, keep the supporting decision log and evidence; in some payment regimes, that retention period is at least five years.

Step 4.4 Verify before every launch#

Set one hard internal gate: no new market launch without signed finance ownership and a traceable decision log. The sign-off can be electronic, but it should identify the accountable finance owner, date, decision ID, open exceptions, and accepted residual risk. Reconfirm the matrix at least annually so role drift does not become launch debt.

Step 5 Build the interview scorecard and case test#

Hire on evidence, not storytelling. For this role, use a structured interview and a job-relevant case, keep one scorecard across all finalists, ask the same questions in the same order, and use the same rating scale for each answer.

Keep the scorecard job-derived and tight. Structured interviews typically assess 4 to 6 competencies, and for this role that can include treasury, controllership, FP&A, finance-team leadership, and payment-risk judgment.

Step 5.1 Build the scorecard first#

Agree the scorecard before writing interview questions so the panel defines "good" before meeting candidates.

| Domain | What good sounds like | Evidence to capture |

|---|---|---|

| Treasury Management | Clear ownership of cash visibility, liquidity, payout timing, and partner dependencies | Specific treasury decision, tradeoff, and control used |

| Controllership | Strong command of close reliability, reconciliations, policy ownership, and internal controls | Example of fixing close or reconciliation risk with clear accountability |

| FP&A | Turns uncertainty into usable forecasts, scenarios, and decision support | How assumptions changed, confidence was communicated, and decisions adjusted |

| Finance Team leadership | Builds capability across finance roles without blurring ownership | Hiring, coaching, and org-design examples with explicit decision rights |

| Payment-risk judgment | Connects growth decisions to money-movement controls and pause criteria | Example of escalating or pausing launch readiness based on missing evidence |

If your model includes UK safeguarding exposure, test that directly. FCA expectations include daily safeguarding checks, with the supplementary regime effective 7 May 2026. In that context, the interview should confirm the candidate can translate customer-funds separation into practical control design.

Step 5.2 Use a real case, not a strategy conversation#

Add a work-sample case that mirrors the actual job. Ask candidates to prioritize fixes across close reliability, forecast confidence, and expansion sequencing, then explain their first actions and what they would pause.

Use the case to test boundary discipline: can they separate the controller track from FP&A, and can they justify expansion timing based on treasury and book-close evidence? Treat polished SaaS narrative without clear reconciliation and control-execution detail as a warning sign.

Step 5.3 Use panel scoring and written evidence#

Run panel interviews, document detailed notes, then score independently before discussion to reduce groupthink. Require written pass, mixed, or fail evidence for each competency. If the panel cannot point to concrete evidence on treasury judgment or reconciliation execution, mark it as not yet proven.

Step 6 Run references and make a decision memo#

Use references to verify evidence, not to collect general praise. At this stage, references should confirm what you already saw in interviews and the case test, or help you choose between closely matched finalists. Keep the process structured, job-related, and documented so you are still hiring on the same criteria.

Step 6.1 Ask the same reference questions for every finalist#

Use one reference script across candidates, and ask each referee the same core questions so answers stay comparable. A practical set for this role is:

- How does this person respond to pressure when stakes are high?

- When they worked with a controller or books lead, how clear were handoffs and decision boundaries?

- Tell me about a treasury or payment incident they handled. What decision did they make, and what was the outcome?

- What did they personally own versus what the finance team owned across FP&A, close, and reporting?

- Would you hire them again into a role with this level of scope?

For a payment platform, treasury-incident judgment is important. Breakdowns in payment, clearing, settlement, or recording activities can affect cash flow and business continuity, so prioritize observed behavior over broad endorsements.

Step 6.2 Verify case claims against prior outcomes#

Use references to validate the strongest claims from the interview case. If a candidate said they improved outcomes in planning, close, or reporting, ask what changed in practice and what the reference directly observed.

Capture concrete facts: title, responsibilities, years of service, ownership boundaries, and whether the claimed outcome was delivered. If references cannot connect a polished story to real scope and results, mark it as unproven.

Step 6.3 Write a concise decision memo before the offer#

Write a concise decision memo (often one page) that compares finalists on the same criteria: FP&A, Controllership, Accounting, treasury judgment, finance leadership, and open risks. Keep planning separate from the close-and-controls track, and in the books area focus on evidence of historical record quality and core financial-statement rigor, not just strategic fluency.

End with a clear recommendation: hire, hire with conditions, or do not hire. Do not let one strong executive reference outweigh weak evidence on controller-side handoffs or treasury-incident judgment.

Step 7 Onboard with 30-60-90 checkpoints#

Treat the first 90 days as a control-and-risk test, not a soft landing. In a payment platform, this period should show whether control quality, cash visibility, and finance decision discipline are improving.

Step 7.1 Map controls and cash exposure in week 1#

Start with money-movement and loss-visibility risks. Build a current-state control map across payment, clearing, settlement, and recording activities, with a named owner for each key reconciliation, approval, and exception path.

Week-1 outputs should be inspectable, not narrative-only:

- all cash locations, processor balances, settlement accounts, and material exposures

- reconciliation points across product data, processor reports, bank activity, and the general ledger

- immediate books-and-close risks tied to financial-data integrity or asset protection

Ask for evidence: source reports, open-item aging, and where exception handling sits today. If you rely on Federal Reserve intraday credit, confirm intraday balance-monitoring capability. If you operate in the UK payments context, include daily safeguarding checks aligned with FCA rules effective 7 May 2026.

Step 7.2 Establish the operating cadence by day 30#

By around day 30, set an operating rhythm across finance leadership roles (for example, the Chief Financial Officer (CFO), VP Finance, and Controller) so ownership gaps do not stall FP&A, Treasury Management, or book-close work.

Set recurring meetings with named owners:

- weekly cash and liquidity review

- close and reconciliation review

- forecast and business-review cadence

Use a one-sentence ownership test: who owns forecast assumptions, close quality, treasury decisions, and launch-pause escalation when finance evidence is incomplete? If those answers are unclear, boundary risk is still active.

Step 7.3 Build a staged expansion plan by day 60#

By around day 60, draft a staged finance plan for expansion, with clear gates and rollback triggers. Expansion should not move on product readiness alone.

For each expansion step, document:

- exposure

- required evidence

- approving owner

- pause or rollback trigger

Finance gates should cover documented cash-flow assumptions, feasible reconciliation, ICFR-aligned control design, and liquidity contingency readiness if settlement timing or funding shifts.

Step 7.4 Review day 90 outcomes and turn them into the next hiring plan#

At day 90, evaluate measurable finance quality changes, not presentation quality. For FP&A, review forecast accuracy and variance analysis versus actuals, using observed accuracy as the benchmark approach.

For Treasury Management and the close-and-controls track, check trend direction:

- are open reconciliation issues reducing in age or count?

- is cash visibility faster and more reliable?

- is there a real liquidity contingency plan with risk identification and monitoring?

Use these outputs to inform the next Finance Team hire. If the CFO is still deep in reconciliation triage, adding Controller or books capacity may be the priority. If close quality improves but planning remains weak, adding VP Finance or FP&A depth may help.

Common mistakes and how to recover#

If your 30/60/90 review shows weak ownership, correct it fast. In many cases, the issue is role fit and unclear risk ownership, not effort.

1. Re-test the polished SaaS candidate#

A strong planning and storytelling profile does not automatically cover books-and-close depth. FP&A and the controller track are distinct, and many leaders are stronger in one than the other.

Before finalizing the hire, run a payment-specific case review. Ask the candidate to walk through a broken payment-to-recording flow, define ownership, and show what evidence they would review first and escalate. Judge written reasoning and control depth, not presentation quality.

2. Put an end date on Fractional CFO coverage#

Use a Fractional CFO as scoped support, not indefinite default ownership. These engagements are commonly limited, for example a few hours per week or project-based, and are often positioned as complementing day-to-day finance operations.

Set written transition criteria now, before fractional coverage turns into default ownership:

- name the accountable owner for Treasury Management, Accounting, and FP&A

- set the trigger or date to decide between full-time CFO and VP Finance leadership

- define decisions a fractional leader should not hold alone, including launch sign-off and unresolved cash-exposure escalation

3. Separate Controller and FP&A decisions#

When Controller and FP&A both "support" the same decision, accountability can disappear. Publish an ownership matrix and enforce one owner per decision.

Apply this to forecast assumptions, close sign-off, reconciliation escalation, and variance commentary. Each material decision should map to one accountable owner and one evidence pack.

4. Move treasury into launch governance#

Treat treasury as a risk function, not back-office administration. Payment, clearing, settlement, and recording activities carry operational and settlement risk, and governance is expected to reduce and control that risk.

Make treasury review a required launch checkpoint. If settlement timing or funding-path evidence is incomplete, finance should be able to pause rollout.

If your checklist shows ownership gaps across treasury, controllership, and launch governance, use a scoped conversation to pressure-test fit and market coverage with Gruv.

Conclusion and copy-paste hiring checklist#

Use this practical sequence to reduce hiring risk: define the role first, then choose the employment model, then test evidence, then run references, then onboard with governance check-ins.

In payment platforms, unclear finance ownership can increase operational risk, not just org-chart noise. The practical question is whether you need stronger book-close execution, clearer controllership and FP&A boundaries, or broader finance leadership.

Step 1 Choose the role first#

Start by naming the bottleneck. If books-and-close execution is the issue, that points to a Controller. If budgeting, forecasting, and decision support are the gap, that is FP&A scope and may fit VP Finance. If both accounting operations and broader finance leadership needs are active, you are likely in CFO scope.

Step 2 Pick the model after the role is clear#

Choose full-time when continuity and immediate access are critical. A Fractional CFO is part-time or project-based, which can fit bounded transition or cleanup work. An Outsourced CFO can also provide strategic support on a part-time or project basis, but limited availability can slow decisions when timing is tight.

Step 3 Write the mandate before interviews#

Define the mandate before candidate conversations so scope is explicit. Spell out ownership for accounting operations, controllership vs FP&A responsibilities, and expectations for budgeting, forecasting, and analysis.

Step 4 Use structured evaluation#

Use the same predetermined questions, in the same order, for each finalist. Structured interviews are more reliable than unstructured conversations and make it easier to separate strong storytelling from real controllership and FP&A depth.

Step 5 Run references near the final decision#

Do reference checks after narrowing to top candidates. Verify evidence, not impressions: ask what the candidate owned, how they worked with accounting and FP&A teams, and which decisions improved outcomes.

Step 6 Onboard with scheduled governance reviews

Set 30/60/90-day reviews before the new leader starts. Use those checkpoints to confirm ownership clarity, better coordination across accounting and FP&A, and clear escalation paths.

- Defined payment-specific finance risks for the Payment Platform

- Chosen role with explicit Controllership, FP&A, and Accounting boundaries

- Compared full-time, Fractional CFO, and Outsourced CFO with written tradeoffs

- Finalized a time-bound mandate with accounting operations and FP&A checkpoints

- Completed structured case interviews and evidence-based references

- Set 30/60/90 governance reviews for the incoming Finance Team leader

Frequently Asked Questions

When should a payment platform hire a CFO instead of a VP Finance?

Hire a CFO when finance needs to cover both FP&A and books-and-controls execution during expansion decisions, not just planning cadence. A VP Finance can be enough when the main gap is forecast discipline and business partnering. If unresolved reconciliation, payout timing, or market-entry obligations can block launches, the role is usually bigger than FP&A leadership alone.

What should a new CFO own first in a payment company?

First, set clear ownership for treasury, the books, close discipline, and FP&A, plus escalation paths when payment-to-recording evidence is incomplete. Early in payments, review whether MSB registration applies, whether registration obligations and filing timing are being tracked, and whether a written AML program is in place when the business is in MSB scope. This is foundation work before broader transformation promises.

How do we choose between a full-time CFO and a Fractional CFO?

Use a Fractional CFO when the need is bounded, such as cleanup, transition support, or short-term senior coverage. The model is part-time or contract senior finance leadership, which works when day-to-day ownership is already covered. If you are entering new markets while redesigning controls, a full-time CFO can be safer because continuity and decision speed matter more.

Which interview questions reveal real payment-platform CFO readiness?

Use a structured interview with identical predetermined questions in the same order for every candidate. Higher-structure interviews are associated with stronger validity and reliability than low-structure interviews. No interview question set can guarantee payment-platform CFO success, but useful prompts ask candidates to diagnose a broken reconciliation flow, separate FP&A from the close-and-controls function, identify the first evidence to review, and state when finance should pause a launch.

What are realistic first 90-day deliverables for a CFO in payments?

The first 90 days should focus on learning, assessment, and direction-setting. Realistic outputs are named ownership across treasury, the books, close discipline, and FP&A; a written list of material control gaps; launch-gate criteria for new flows or markets; and a communication cadence with founders. Ask for evidence packs on close quality, unresolved reconciliations, liquidity exposure, and forecast reliability.

What red flags show a candidate is SaaS-strong but payments-weak?

A common red flag is polished planning language with weak detail on books-and-controls execution. FP&A and controllership are different, and many leaders are stronger in one than the other. Watch for vague answers on AML ownership, PCI DSS scope when cardholder data is stored, processed, or transmitted, suspicious transaction review thresholds, and ACH unauthorized return-rate pressure.

Which expansion decisions should always require CFO sign-off?

No cited rule requires title-specific CFO sign-off, but internal governance can require finance approval before expansions that change money movement, settlement timing, or regulated obligations. This includes changes that may trigger MSB registration duties, written AML program requirements, remittance-transfer disclosures in writing and retainable form, or broader PCI DSS scope. If funding path, reconciliation design, or control ownership is unclear, finance should be able to pause launch.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bsaaml.ffiec.gov/docs/manual/04_AssessingTheBSAAMLComplianceP...trusted

- bsaaml.ffiec.gov/docs/resources/new_5_2007/OCC/BL_2006_39.pdftrusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-17/chapter-II/part-229/subpart...trusted

- fdic.gov/sites/default/files/2024-03/fil12003.pdftrusted

- federalregister.gov/documents/2011/07/21/2011-18309/bank-secrecy...trusted

- federalreserve.gov/paymentsystems/files/psr_2020_policy.pdftrusted

- federalreserve.gov/paymentsystems/psr_about.htmtrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How Modern CFOs Make Payment Platform Expansion a Strategic Driver

A payment platform should choose its next market based on operational readiness, not volume forecasts alone. The real question is whether you can run that market safely and clearly without creating finance debt that later shows up as payment, reconciliation, or compliance failures. If you cannot explain that operating path cleanly, your forecast should not carry the decision.

Measure AP Automation ROI for Payment Platform Finance Teams

AP automation ROI is credible only if the gains still hold at month-end close. A CFO can defend the investment in budget and audit review when the value is tied to evidence that the books stay complete and accurate, reconciliation closes cleanly, payouts execute reliably, and the audit trail is easy to retrieve.

End-to-End Payments Visibility: How CFOs at Platform Companies Track Every Dollar in Real Time

For a Chief Financial Officer, real-time visibility is an operating decision before it is a reporting feature. If teams are not aligned on ownership and proof for each money event, a live dashboard exposes that gap faster. That is broader than a simple payment-status view. Risk can appear at handoffs, especially when a payment event cannot be tied cleanly to bank data and back to ledger records.