Quick Answer

Use a finance-owned Go/Delay/No-Go table before locking launch dates. In practice, lean finance modern cfo payment platform leader strategic driver means requiring proof for compliance readiness, payout reliability, reconciliation completeness, and incident ownership. Mark No-Go when customer due diligence cannot be met, and keep a market in Delay when exception handling still depends on inboxes or spreadsheets. Move forward only when test logs, payout failure taxonomy, and matched transaction samples hold up in live operation.

Why Payment Platform Expansion Belongs on the CFO Agenda#

A payment platform should choose its next market based on operational readiness, not volume forecasts alone. The real question is whether you can run that market safely and clearly without creating finance debt that later shows up as payment, reconciliation, or compliance failures. If you cannot explain that operating path cleanly, your forecast should not carry the decision.

This article takes a CFO-grade view of expansion: finance as a launch-readiness function, not a budget checkpoint after strategy is set. That fits the broader shift in CFO expectations from pure gatekeeping to growth responsibility. It also puts ideas like Lean Financial Operations™ in the right place: useful only when they translate into operating choices you can test.

For payment businesses, that translation is critical. Cross-border outcomes are shaped by more than technology. National payment systems combine infrastructure with legal and regulatory conditions, and jurisdictions still supervise bank and non-bank payment providers differently. The FSB final report dated 12 December 2024 reflects that reality. A plan that looks clean in a deck can fail when local regulatory requirements and operating controls are unclear.

So the lens here is practical. In this context, lean finance is less about team size than about reducing unmanaged handoffs across approvals, payment movement, reconciliation, and reporting so decisions reflect operating reality.

That standard matters for a reason. Cross-border payments have been a global policy priority since the Roadmap for Enhancing Cross-Border Payments launched in 2020, with goals aimed at end-2027. Even so, performance still varies materially across countries and segments in speed, cost, access, and transparency, so "cross-border" is not one operating condition.

The goal of this article is straightforward: help you decide where to expand, in what order, and with what finance-owned proof before launch. The standard is not market attractiveness in theory. It is whether your team can validate payment and regulatory assumptions, assign ownership when failures occur, and retain evidence that holds up under pressure. We recommend using that proof standard before your team commits launch dates, not after.

If finance is still mostly retrospective reporting, this is the shift from cost center to strategic driver. The modern CFO earns that role by making expansion decisions more testable, not more abstract.

Need the full breakdown? Read Revenue Leakage from Payment Failures: How Much Are Failed Transactions Really Costing Your Platform?.

What lean finance means for a payment platform leader#

Lean finance is not a headcount exercise. For a payment platform leader, it is process design: reducing unmanaged handoffs across Accounts Payable (AP), payouts, and reconciliation so decisions can move faster without weakening control evidence.

Yooz's Lean Financial Operations framing is useful context because it treats lean as continuous improvement, not a one-time cost cut. But execution is the real test. Can you trace a payment or invoice from source documentation, through approval, into the ledger, and into the accounting output or audit file that shows what happened?

That is where the modern CFO role becomes operational. Deloitte's 2026 finance research describes finance leaders as central to cost optimization, innovation, and strategic agenda-setting. In practice, traceability speeds decisions because ownership and evidence are clearer when something breaks. Two checkpoints matter most:

- Confirm the audit trail links source documentation to accounting output. In AP, you should be able to see invoice intake, approval, payment release, and the resulting book entry.

- Confirm reconciliation ties transaction records to accounting records, with unresolved items tracked in a reviewable finance record.

AI-powered automation does not guarantee control quality. If exports cannot be tied back to ledger entries, or exceptions sit outside the main record, that is a control gap. That matters even more under fraud pressure: AFP reports that 79% of organizations were victims of payments fraud attacks or attempts in 2024, and 63% identified business email compromise as the top avenue for fraud attempts.

Use vendor narratives as prompts, not proof. For expansion decisions, the standard is simple: fast and traceable, with enough detail to stand up under review. We would rather slow one market decision than let your team approve expansion on vendor shorthand.

How the modern CFO changes expansion decisions#

Expansion should be treated as an operating-readiness decision, not just a budget decision. The finance question is whether you can run a market safely at scale with that market's payment infrastructure, compliance requirements, and exception paths.

| Launch-readiness item | What it should cover |

|---|---|

| Jurisdiction note | Legal and regulatory conditions, available payment rails, and local dependencies |

| Test pack | A payment or payout traced from initiation through status updates, exception handling, and ledger reconciliation |

| Named owners | Failed payouts, returns, and manual reviews, with a clear system of record for each |

Finance leaders are increasingly expected to shape strategy, but the practical test is still operational: does your market plan reflect jurisdiction-specific payment constraints, local compliance design, and credible post-launch exception handling?

A familiar regional scheme does not remove this work. SEPA is harmonized across participating countries, but ECB guidance is explicit that those rules do not apply outside the EU/EEA. Likewise, FATF sets international AML/CFT standards, while countries implement them through local legal, administrative, and operational frameworks.

If compliance handling or payout recovery is still vague, avoid firm commitments until those assumptions are explicit. The FSB's 12 December 2024 report notes that inconsistent jurisdictional approaches can increase compliance complexity, raise costs, and reduce processing speed. It also keeps operational, fraud, cyber, third-party, resilience, and financial-crime risks in scope.

Before product or sales lock dates, make those three go gates explicit and evidence-backed. If exceptions still live in inboxes, provider portals, or spreadsheets outside the finance record, launch readiness is likely incomplete.

You might also find this useful: How to Measure AP Automation ROI: A CFO's Framework for Payment Platform Finance Teams.

Where to own, outsource, or partner before launch#

Use control criticality as your rule. Keep decision rights close to finance when failures could create compliance exposure or operational disruption. Partner where market access is the constraint.

Before rollout, classify each activity by whether it is a critical or important function. For critical outsourced functions, senior-management responsibility is not delegable, so provider involvement does not remove internal accountability for compliance and safe operations. A practical split looks like this:

| Area | Primary operator | Finance should retain |

|---|---|---|

| Policy decisions, approval thresholds, ledger posting rules | Typically internal | Decision rights, change control, audit trail |

| Local payment rail or payout access | Partner/provider | Market-level capability confirmation, fallback plan |

| High-volume execution (routing, file transfer, status polling) | External provider can run | Reconciliation expectations, exception handling ownership, escalation owner |

Partnering is most useful where coverage is market-specific. Payment capability can vary by country or region, processing and settlement currency, feature set, and integration type. Payout support may also be tiered rather than uniform, for example, 4 levels in PayPal's country feature model. Treat generic "supported" claims as insufficient until you have market-level capability confirmation.

Outsource execution, not accountability. Third-party use can reduce direct control and add risk, and it does not remove your responsibility for compliant, safe operations. In practice, a third-party relationship can exist even without a formal contract or remuneration, so informal dependencies should be governed accordingly. A workable pattern is to use partners for scale or access while keeping final accountability for customer-impact, compliance, and financial outcomes internal.

Related reading: Supply Chain Finance for Marketplaces: How Early Payment Programs Can Attract and Retain Sellers.

Which markets to enter first using a country and vertical screen#

Start with markets where you can test controls end to end before launch, rather than relying only on forecast volume. A strong first-country rollout is one where rail access, compliance gating, settlement behavior, and finance evidence are verifiable in practice.

That follows directly from the ownership split above. Once finance-owned controls are defined, rank markets by whether those controls will hold in production.

Screen the country and vertical together#

Score each country and vertical market as a pair. Payment patterns, payout profiles, and evidence burden can change by use case even within the same geography.

Also split by payment segment. The G20 framework uses separate targets for wholesale, retail, and remittances, so "cross-border payments" should not be treated as one operating condition. For remittance-sensitive models, include corridor economics in the screen. The World Bank reports a 6.49% global average sending cost, while the policy target is 1% average with no corridor above 3% by end-2027.

What to compare in each market row#

Use one row per country-vertical pair, with separate checks for collection, conversion, and payout. The goal is not a universal formula. It is a consistent evidence standard across candidates.

| Use case | What to verify on payment rails | What raises gating complexity | What finance should test |

|---|---|---|---|

| Collection | Is the rail available in that jurisdiction and for your provider type, or only described as broadly supported? | AML/CFT implementation differs by country under a risk-based approach | Can funds be matched from provider reference to bank movement to ledger entry without manual reconstruction? |

| Conversion | Are settlement timing and corridor economics predictable for pricing and reconciliation? | Legal and operational differences by country create real launch constraints | Can treasury, AP, and ledger teams see the same value date and fees on sample flows? |

| Payout | Is payout live for the exact corridor and beneficiary pattern you need? | Conditional support and provider-dependent access can increase exception risk | Can rejects, retries, returns, and reversals be classified cleanly enough to close without suspense buildup? |

Confirm market-level and provider-level support in writing for the exact flow you plan to launch. "Available in Europe" is not enough if your rollout depends on euro instant credit transfers. Under the EU Instant Payments Regulation, implementation is staggered. That includes key receiving deadlines on 9 January 2025 and 9 January 2027.

Add a separate finance readiness score#

After market screening, add a separate internal finance-operations score for each row. Keep it simple and repeatable. There is no universal industry formula. Score these four areas separately:

| Score area | What to assess |

|---|---|

| AP flow maturity | Whether invoices, FX charges, rail fees, and adjustments can be routed and booked consistently |

| Payout exception load | Whether expected manual interventions fit team capacity |

| Reconciliation complexity | Whether request, provider status, bank movement, and ledger posting can be tied together on sample transactions |

| Audit artifact quality | Whether approvals, timestamps, policy references, and exception records are review-ready |

Do not let a strong average hide a weak control. If reconciliation or audit evidence is weak, treat that market as later-stage even when demand is strong. Also avoid assuming payment-system legal maturity is uniform: World Bank reporting indicates payment system laws in 81% of participating countries, which still implies meaningful variation.

Produce a ranked market stack with why now and why later#

Output a ranked market stack, not a heat map. Each row should include an explicit decision note.

A defensible why now usually means exact rail fit is confirmed, the compliance path is understood for that jurisdiction, settlement behavior is predictable enough for pricing and close, expected exceptions are manageable, and evidence is testable end to end.

A defensible why later is just as specific. Support may be conditional, implementation timing may still be staggered, corridor costs may be misaligned with target economics, or finance may not yet be able to prove provider-to-ledger traceability on sample flows.

This keeps expansion sequencing tied to operating proof instead of optimism.

How to use a Go or Delay or No-Go table that finance owns#

Use a finance-owned Go/Delay/No-Go table to block launch dates when any hard gate lacks evidence. If a hard gate is unresolved, treat the market as not launch-ready. A practical setup is four hard gates: compliance readiness, payout reliability, reconciliation completeness, and incident response ownership.

| Gate | Mark Go when | Mark Delay when | Mark No-Go when | Evidence to attach |

|---|---|---|---|---|

| Compliance readiness | KYC/AML controls are documented for the market, tested, and usable for the planned customer type and flow | Policy exists, but onboarding reviews, ongoing monitoring, or escalation handling are still manual or unproven | Customer due diligence cannot be met for the planned launch model | CIP/KYC test logs, approval records, monitoring rules, unresolved issue list |

| Payout reliability | The rail works for the planned corridor and beneficiary pattern, with tested failure handling | Rails exist, but returns, retries, rejects, or reversals still depend on ad hoc handling | Reliability cannot be demonstrated, or critical operational/security control gaps remain | Test payouts, failure logs, payout failure taxonomy, partner confirmations |

| Reconciliation completeness | Request, provider reference, bank movement, fee, FX, and ledger entry can be tied end to end | Matching works for normal cases but breaks on timing differences, fees, or reversals | Finance cannot reconstruct money movement without manual guesswork | Reconciliation reports, sample matched transactions, unmatched aging, close notes |

| Incident response ownership | Named owners, escalation path, and provider boundary are documented and leadership-approved | Response path exists, but ownership splits or after-hours escalation are unclear | No approved incident plan or no accountable owner for live failures | Incident response plan, contact tree, severity matrix, provider responsibility map |

Keep the compliance rule strict: if CDD cannot be met, treat it as No-Go, not Delay. FATF standards support blocking account opening, business relationships, or transactions when due diligence cannot be completed.

Tie every gate to testable proof, not confidence. For identity controls, confirm your CIP can support a reasonable belief in true customer identity. For payout and security controls, require testing artifacts and clear handling paths for exceptions. For reconciliation, require evidence that flows can be traced end to end, including non-happy paths.

Make approval explicit before GTM dates are finalized. Set an internal sign-off rule, for example CFO and operations, and ensure incident readiness includes named ownership, escalation boundaries, and leadership-approved response planning.

Re-score at checkpoints you define, especially when launch conditions change. Ongoing monitoring and customer-information updates are expected, so a prior Go can become Delay if evidence no longer holds.

Related: How Finance Leaders Are Using AI in 2026: A Platform CFO's Guide to Practical Applications.

Before you finalize a Go decision, map each gate to concrete events, payout statuses, and reconciliation evidence in your stack using the Gruv docs.

What a 30-60-90 rollout looks like in finance operations#

Treat a 30-60-90 rollout plan as staged proof, not a calendar ritual. Validate control surfaces first, expand only when exception handling is stable, then scale volume and geographies only where gates keep passing.

| Phase | What finance needs to prove | Checkpoint evidence | Rollback trigger |

|---|---|---|---|

| Days 1 to 30 | AP Automation flow integrity, payout status visibility, and reconciliation procedures work in live conditions | AP request-to-ledger traces, payout lifecycle mapping for paid/failed/canceled states, reconciliation logs with corrective follow-up | Missing status states, duplicate effects after retries, or unresolved reconciliation breaks |

| Days 31 to 60 | Chosen payment rails handle normal traffic and exceptions without close-quality slippage | Exception aging by rail, retry results, month-end close review, rail-specific cutoff and settlement checks | Exception backlog grows, close quality deteriorates, or rail timing assumptions prove wrong |

| Days 61 to 90 | Volume and market expansion can increase without repeating earlier control failures | Repeated gate passes, stable exception metrics, clean periodic control reviews, approved expansion decision memo | A major process change is introduced without timely control review, or delayed markets still fail hard gates |

Days 1 to 30#

In the first month, focus on control visibility, not throughput. For AP Automation, confirm invoice, approval, payment instruction, ledger posting, and export are traceable end to end without manual reconstruction. If you cannot show where a transaction failed or who approved a correction, the launch surface is not stable.

For payouts, require explicit lifecycle states and actions for paid, failed, or canceled outcomes. Test retry behavior at the same time so idempotency prevents duplicate transaction effects. Without idempotency safeguards, retry logic can create duplicate payouts or duplicate ledger events.

For reconciliation, the checkpoint is simple: do your procedures define timing, ownership, and corrective follow-up when deficiencies appear? Documented control activities need that level of specificity.

Days 31 to 60#

Expand only if exception handling is stable on the rails you actually use. Rail behavior changes your staffing and monitoring expectations. FedNow runs 24x7x365, settlement is final, and missing expected acknowledgments should trigger escalation through defined FedNow procedures.

For ACH, validate local timing assumptions. Same Day ACH schedules publish ODFI deadlines (10:30 a.m. ET, 2:45 p.m. ET, 4:45 p.m. ET), but precise processing timing is not fixed identically across operators. If you run ACH debits, monitor unauthorized returns against the 0.5% threshold over the preceding 60 days or two calendar months. If returns or exception queues drift up, hold expansion.

Days 61 to 90#

At 90 days, scale only on repeated passes, not one clean cycle. Increase volume and add geographies where gates continue to pass through periodic and ongoing review. If you introduce a major process change, run a timely post-change control review before further expansion.

Keep the rollout artifact operational: list the business-process objective, owner by organizational unit, checkpoint date, required evidence, and exact rollback trigger for each phase. That lets you revisit delayed markets using evidence, not opinion.

If you want a deeper dive, read Why CFOs Need to Modernize Financial Operations: A Payment Platform Leader's Roadmap.

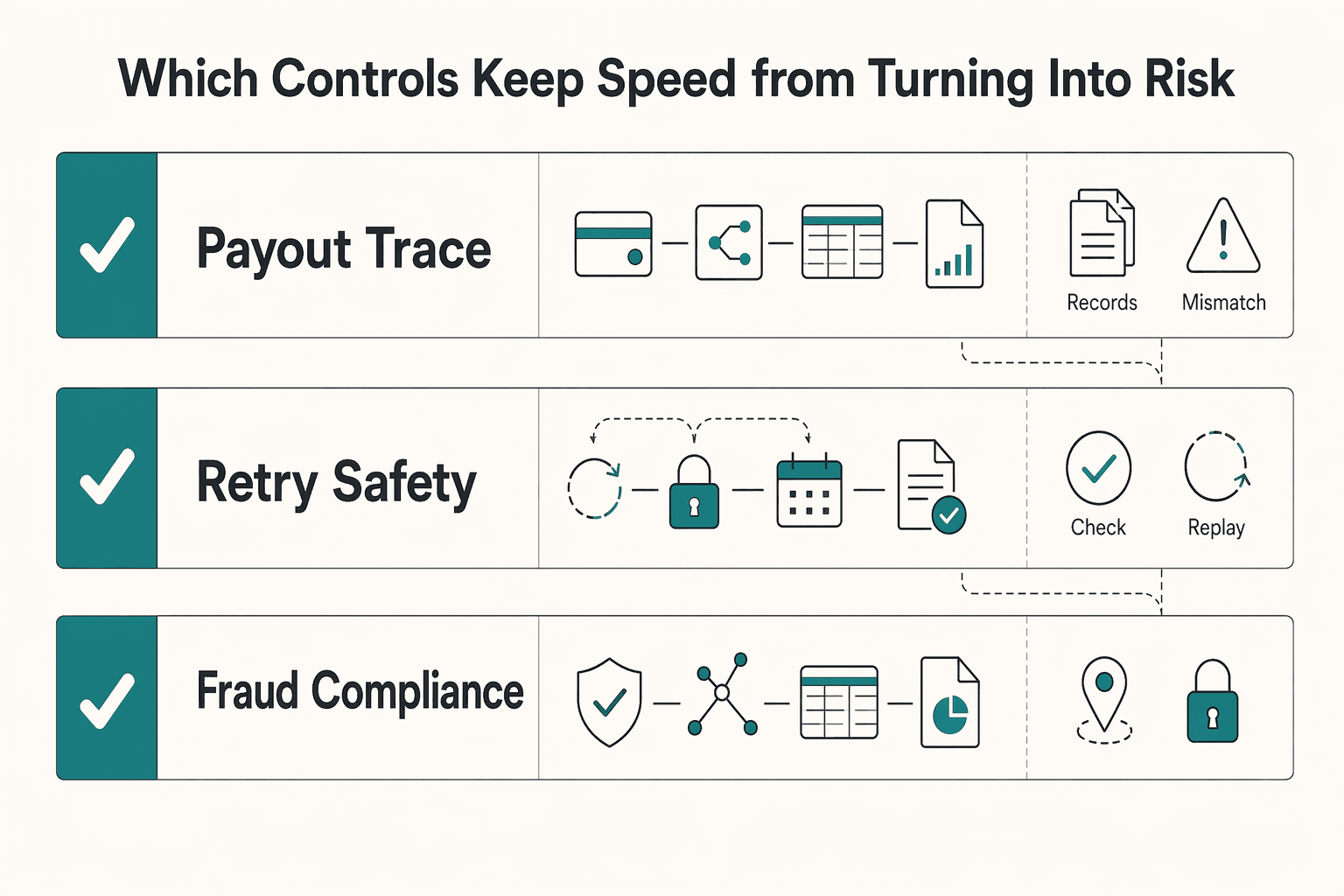

Which controls keep speed from turning into risk#

If you cannot reconstruct a payment decision end to end, you are moving too fast. For a payment platform, speed is only real when policy gates, provider events, ledger postings, and exports stay linked so finance can explain a transaction without manual guesswork.

| Control area | What to confirm | Evidence or rule |

|---|---|---|

| Traceability | Approval record, payment instruction, provider reference, ledger entry, and downstream export stay linkable through stable identifiers | Sample normal, failed, and corrected cases can be traced from request to export without engineering intervention |

| Retry safety | Payout requests and webhook handling replay safely and do not create new financial side effects | Use a durable idempotency key for payout creation, and store processed webhook event identifiers |

| Fraud and compliance | Webhook signatures are verified on every event, and launches that touch card data are checked against PCI DSS before go-live | Do not launch while fraud checks or compliance evidence are still in progress |

Traceability is the first release gate#

Traceability should be a release gate, not a cleanup task. A usable audit trail captures who performed the action, what changed, when it happened, and the affected object so a reviewer can rebuild the sequence later. In practice, your approval record, payment instruction, provider reference, ledger entry, and downstream export should stay linkable through stable identifiers.

If your team needs multiple tools and manual reconstruction to explain a failed payout or a redrafted payment, your launch surface is still fragile. Payment lifecycle events like create, approve, deny, and update are control points, so keep them visible and exportable from day one.

Use a simple checkpoint: sample transactions across normal, failed, and corrected cases, then trace each one from request to export without engineering intervention. If you cannot do that, hold the release. As one CFO put it, "We're not gonna differentiate on billing. But we can screw it up."

Retries must be safe by design#

Retries must replay safely, not create new financial side effects. That applies to payout requests and webhook handling, because providers can redeliver events.

Stripe may retry webhook delivery in live mode for up to 3 days with exponential backoff. Adyen uses at-least-once delivery, expects an acknowledgment within 10 seconds, and if that acknowledgment does not arrive, notifications are queued and retried, then every 8 hours for the following 7 days. If your consumer treats each delivery attempt as a new business event, duplicate payouts or duplicate ledger movements can follow.

Make verification explicit with two checks:

- Use a durable idempotency key for payout creation, and keep retry handling tied to that key through provider submission, internal status updates, and ledger posting.

- Store processed webhook event identifiers and return a fast acknowledgment after signature verification so retries do not create new financial effects.

One failure mode is partial success: the provider accepted the payment, an internal update timed out, and a retry posted again because state checks were weak. Treat that as a core control risk, not transport noise.

Fraud and compliance belong in release criteria#

Fraud and compliance controls should be part of go-live criteria, not post-launch remediation. Verify webhook signatures on every event to confirm the event was not sent or modified by a third party. PCI DSS is a baseline of technical and operational requirements to protect payment account data, so launches that touch card data should be checked against that baseline before go-live.

Set a hard operating rule: do not launch while fraud checks or compliance evidence are still in progress. Release criteria should include production signature verification, documented ownership for suspicious-payment escalation, and exportable audit evidence for investigation.

Keep the evidence pack tight: audit exports, retry test results, signature-verification logs, and proof that finance can reconcile corrected cases without rebuilding history by hand. If those artifacts are weak, delay. Resource-intensive reporting, audit prep, and reconciliation often become major pain points when controls are treated as optional.

What breaks first in cross-border launches and how to catch it early#

What often breaks first is not the payment rail itself. It is the recovery layer around it: exceptions, investigations, and reconciliation. As launch volume rises, weak handoffs in data, message mapping, provider responses, and internal posting show up quickly.

Cross-border payments already face known friction in speed, transparency, access, and cost, and fragmented messaging standards can add strain. So early monitoring should focus on whether your team can classify and resolve cases quickly, not just whether payments are moving. If you cannot explain root cause in aged or unresolved cases, the queue can outgrow your capacity.

Exception handling and investigations are still manual and resource-intensive in many environments, so low-volume stability can hide scaling risk. Watch for internal warning signs each cycle:

- more aged payment cases

- unresolved cases carrying into the next cycle

- close timelines slipping because prior-period exceptions are still open

In regulated payment environments, reconciliation obligations can make delay tolerance tighter, including expectations for regular internal and external safeguarding reconciliation. When clearing lags persist, that can signal a control-quality issue, not just an operations inconvenience.

A second failure point is automation speed without evidence quality. AI-assisted AP and finance workflows can increase throughput, but financial reporting still depends on governance and internal controls. Keep a hard check that automated actions leave exportable evidence for who approved, what rule fired, what source document applied, and what ledger impact followed.

Use a clear internal discipline. For example, if exception recovery misses your agreed SLA for two consecutive cycles, you may pause new market activation until recovery stabilizes. That is not a universal rule, but it can be a practical way to keep growth from masking control drift.

How to prove finance moved from cost center to strategic driver#

Finance is acting as a strategic driver when its metrics inform expansion decisions, not just processing cost. The proof is a decision trail: what finance recommended, what evidence supported it, and what the business changed as a result.

Measure outcomes that can change market decisions#

Use a compact metric pack tied to decision memos and board updates:

| Metric | Why it matters | Decision check |

|---|---|---|

| Forecast reliability | Shows whether planning inputs are decision-useful | Did finance recommend delay, narrower rollout, or reallocation? |

| AP cost per $1,000 revenue | Normalizes AP efficiency across growth stages | Were savings achieved without weakening controls? |

| First-time error-free disbursements | Tracks payment accuracy without rework | Did payment quality hold as costs improved? |

| ICFR effectiveness (where applicable) | Confirms control quality at the reporting level | Were any material weaknesses identified? |

Keep efficiency in context. APQC shows a wide AP cost spread ($0.38 vs $0.92 per $1,000 revenue), and at $1 billion in revenue that gap can exceed $500,000 annually. That matters, but cost improvement alone does not prove strategic impact.

Count AP automation ROI only when quality and controls hold#

Treat AP automation ROI as valid only if process quality and control evidence stay intact. APQC frames first-time error-free disbursements as a process-efficiency KPI, and its indexed benchmark page shows 95.0% with a 2,480-company sample.

Use a hard check. If AP cost per $1,000 revenue improves while first-time error-free disbursements decline, do not treat that as strategic progress. Keep auditable traceability for approvals, source documents, ledger impact, and rework resolution.

Where ICFR applies, this is non-negotiable: management cannot conclude ICFR is effective if one or more material weaknesses exist. Lower unit cost with control breakdowns is risk transfer, not strategy.

Give the board cause-and-effect evidence#

Board-level proof should show finance shaped decisions, not just reported outcomes. IFAC positions finance-function evaluation as a board-and-management tool for assessing progression and value contribution, and PwC describes modernization as finance helping shape strategy through better insights, forecasting, and decisions.

Show these three items together in each review cycle:

- the market recommendation finance made

- the evidence behind it (forecast assumptions, control checks, and payment-quality performance)

- the action taken (for example, delaying launch or limiting initial volume)

If that chain is clear and repeatable, finance has moved beyond overhead into strategic execution.

For a step-by-step walkthrough, see How to Build the Ultimate Finance Tech Stack for a Payment Platform: Tools for AP Billing Treasury and Reporting.

The evidence pack every expansion decision should include#

If the documentation cannot pass pre-launch review, the market is not ready for Go. Treat this evidence pack as a finance gate before GTM dates are committed, not a cleanup step after sales, product, and legal lock plans.

Expansion support is often conditional beyond headline market lists. A provider can be available in a country while still limiting payment-method support by presentment currency, integration type, connected-account eligibility, or local payout availability. Your pack should surface those conditions before the CFO approves launch timing.

What the minimum pack should contain#

Keep the pack compact, but complete enough that a platform CFO can trace each decision to evidence.

| Artifact | What it should show | Common red flag |

|---|---|---|

| Market screen table | Country, currency, rail fit, settlement behavior, ops burden, and support caveats | Market marked "supported" with no country/currency limits noted |

Decision table (for example, Go/Delay/No-Go) | Hard gates for compliance readiness, payout reliability, reconciliation completeness, and ownership | Status based on opinion instead of test evidence |

| Control test results | Passed/failed checks, dates, scope, owner, and open remediation items | Screenshots only, with no clear result or owner |

| Reconciliation proof set | Sample transaction path from source to settlement to ledger, including unmatched-item handling | Summary looks clean but cannot be reproduced |

| Concise decision memo (often one page) | Assumptions, constraints, caveats, and reversal triggers for that market | No stated condition that would move Go back to Delay |

Use explicit caveat language: "where enabled," "where supported," and "coverage varies by market/program." This is operationally accurate. Payment-method support can vary by country and presentment currency, connected accounts can have different eligibility requirements than the platform account, and when local payout is unavailable, settlement may shift to a cross-border transfer.

What a concise decision memo needs to say#

The memo is the judgment layer. It explains why the same facts lead to Go, Delay, or No-Go in one market versus another. If you use a one-page format, include at least these fields:

- assumptions that must remain true

- known constraints

- evidence that is still conditional or provider-dependent

- reversal triggers that would change the decision

If you have U.S. money services business exposure, 31 CFR 1022.210 is a key control line. The AML program must be in writing, available for inspection, and include policies, procedures, and internal controls commensurate with risk by location, size, and service profile. If that written support is incomplete for a target market, state that directly and mark the decision accordingly.

A strong memo also reflects a risk-based approach. You do not need identical control depth in every market, but you do need documented reasoning that control depth matches the market's actual risk.

Check the pack before GTM commitments#

Final checkpoint: verify document quality, not just document existence. Before GTM dates are approved, confirm each artifact is current, market-specific, inspectable, and owner-assigned, with a clear link across provider behavior, control testing, and reconciliation evidence.

Do not wait until contracts are signed or launch planning is fixed. Third-party risk guidance treats planning, due diligence, third-party selection, contract negotiation, ongoing monitoring, and termination as one lifecycle. One risk is a Go built on broad provider coverage pages when the actual market depends on unsupported currencies, different connected-account rules, or a cross-border payout path finance did not model.

Conclusion#

What matters is not sounding strategic. It is requiring finance-owned gate decisions before expansion turns into committed spend. If you skip that gate, your team can turn ambition into finance debt quickly.

A platform CFO can create leverage by making each country or vertical clear an explicit Go/Delay/No-Go checkpoint with evidence. In gated programs, work should not advance without a formal go/no-go decision, and proceeding decisions can be tied to funding release. Expansion should run the same way: no launch date, budget release, or external commitment until operating proof is in place.

That proof has to be market-specific. Payment-method support depends on country, currency, and product setup, and payout availability varies by industry and country. So a market can look strong in a forecast and still fail readiness. A provider's headline coverage, including claims of reaching more than 50 countries, is not the same as proving your collection flow, payout route, settlement behavior, and exception handling are ready for your use case.

Start with a practical checkpoint: can finance trace the flow end to end and reproduce the evidence pack without heroics? If the answer depends on spreadsheet stitching, tribal knowledge, or one person fixing issues at month end, it is not a Go case. We recommend asking that question before your GTM plan hardens. Cash timing is another hard gate: if your model assumes near-immediate access to funds but initial payouts can take 7-14 days after first payment, the launch plan is misaligned with cash reality.

Keep these gates finance-led for governance as well as execution. Firms are expected to maintain systems and controls appropriate to the business, and risk-based CDD is foundational in BSA/AML programs. If CDD ownership is unclear, escalation paths are undefined, or payout exceptions lack named owners, mark the market Delay or No-Go even when demand looks strong.

If you do only three things next, do them in this order:

- Build the country screen around operability variables: payment-method fit, payout constraints, settlement timing assumptions, compliance gating, and reconciliation burden.

- Convert that screen into a finance-and-operations-owned Go/Delay/No-Go table with evidence at each gate.

- Release rollout resources only where evidence is current, reproducible, and signed off.

Finance becomes a strategic driver here through operating discipline, not title. Build the screen first, force the gate decision second, and let evidence determine where you expand. We recommend treating that order as the baseline so your team does not confuse motion with readiness.

If you want a market-by-market read on coverage, compliance gating, and rollout risk before committing launch dates, talk to Gruv.

Frequently Asked Questions

What does lean finance actually change for a payment platform leader day to day?

It changes where finance time goes: less manual rework, more control-ready execution. Lean Financial Operations keeps controls in place while removing manual, redundant, and error-prone steps, so approvals, payouts, and reconciliation can run with less friction and clearer traceability. If your team still has to stitch spreadsheets together to trace a payment end to end, you likely still have avoidable operating risk.

How is a Modern CFO decision process different from a traditional CFO process during expansion?

A modern CFO process starts with operability, not just affordability. Traditional models were built for control and after-the-fact reporting, while current expectations are for finance to support real-time decisions during expansion. In practice, that means pressure-testing execution and control readiness before launch momentum sets the pace.

What should founders evaluate first before entering a new country or vertical market?

Start with local payment fit and control readiness before demand projections. Payment localization matters because local methods, currencies, and market constraints can directly affect conversion, and customers may abandon checkout when familiar options are missing. Then confirm the finance path is workable, including due diligence obligations and reproducible reconciliation evidence.

When should a team mark a market as Delay instead of Go?

Use Delay when demand is promising but operating proof is incomplete. Typical cases include unresolved compliance gating, unclear exception ownership, or reconciliation evidence that cannot be reproduced cleanly. If customer due diligence readiness is not established, the market is not ready for Go.

What should stay in-house versus be outsourced in the operating model?

Keep key decision rights in-house: policy, approvals, ledger logic, reconciliation standards, and escalation authority. Outsource execution where it helps coverage or speed, but do not treat outsourcing as a transfer of accountability, because management responsibility remains with the institution. A practical default is to outsource commodity execution, not core decision control.

Which failure modes most often invalidate a fast GTM expansion plan?

Recurring invalidators include outdated money-movement workflows, weak real-time visibility, and rising reconciliation burden. False declines are another risk because they can quietly leak revenue. Fast plans also fail when teams assume broad market readiness without confirming local payment fit and control execution in practice.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bsaaml.ffiec.gov/manual/AssessingTheBSAAMLComplianceProgram/04trusted

- cisa.gov/sites/default/files/publications/Incident-Re...trusted

- csrc.nist.gov/glossary/term/audit_trailtrusted

- ecb.europa.eu/paym/retail/instant_payments/html/instant_pa...trusted

- ecfr.gov/current/title-17/chapter-II/part-229/subpart...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- executiveeducation.wharton.upenn.edu/thought-leadership/wharton-at-work/2024/04/c...trusted

- fdic.gov/news/financial-institution-letters/2023/fil2...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Why CFOs Modernize Financial Operations in Payment Platforms

For a platform CFO, modernization is not a finance rebrand or a software shopping exercise. It is a decision discipline for a payment platform: which markets are worth entering, which constraints are real, what to launch first, and when to pause until the facts improve.

How Finance Leaders Are Using AI in 2026: A Platform CFO's Guide to Practical Applications

AI is a priority for finance in 2026, but most teams are still in early-stage adoption rather than finance-wide deployment. The gap is straightforward. Interest is high, pilots are common, and production discipline is often limited, especially in multi-country operations with sensitive data and money movement.

Measure AP Automation ROI for Payment Platform Finance Teams

AP automation ROI is credible only if the gains still hold at month-end close. A CFO can defend the investment in budget and audit review when the value is tied to evidence that the books stay complete and accurate, reconciliation closes cleanly, payouts execute reliably, and the audit trail is easy to retrieve.