Quick Answer

Start with a country-plus-vertical scorecard and fund only markets that clear documented launch, pilot, or pause gates. For each corridor, verify KYC/KYB/AML requirements, payout route availability, FX behavior through returns, and the records needed for activation versus reporting. Then run one end-to-end trace from API request and webhook updates to General Ledger posting and bank deposit reference. If that chain breaks, or retries can create duplicate financial effects, pause expansion until controls are fixed.

Why CFOs modernize payment operations#

For a platform CFO, modernization is not a finance rebrand or a software shopping exercise. It is a decision discipline for a payment platform: which markets are worth entering, which constraints are real, what to launch first, and when to pause until the facts improve.

That matters because the role itself has changed. The remit now reaches beyond reporting and stewardship, even as compliance and reporting obligations remain. Leadership teams now expect finance to turn operating data into strategic decisions. In payments, both pressures stay visible: in one survey, 44% of finance leaders named cost cutting and efficiency as a top-three priority, and 33% named risk management.

The pressure is sharper in cross-border operations. Since 2020, the G20 Roadmap for cross-border payments has aimed to make payments faster, cheaper, more transparent, and more inclusive. In 2021, the G20 endorsed quantitative targets, most set for end-2027, to create accountability. Yet the core frictions remain familiar: high costs, low speed, limited access, and insufficient transparency. Recent progress reporting makes the point clearly: activity alone does not matter if end users do not see better outcomes.

That is why modernization should be treated as an operating decision process, not a broad transformation slogan. Cross-border oversight remains fragmented, with jurisdictions taking different approaches to supervising banks and non-banks. Operating conditions also vary by country in speed, cost, access, and transparency. Add the growing role of non-bank PSPs in cross-border markets, and assumptions from one corridor often fail in another.

So the practical question is not whether modernization sounds important. It is whether you can show that a target market is executable before product and go-to-market spend outruns control reality. An early checkpoint is simple: can you document, country by country, the regulatory approach, likely user operating conditions, and the evidence required before launch? If that packet is still mostly narrative, the market is not ready to turn green.

This article stays at that operator level. It focuses on the choices platform CFO teams face in a payments context: market selection, compliance gates, rollout sequence, and control design. The goal is not to force a universal order of operations, because none applies across all platforms and jurisdictions. The goal is to replace optimism with documented conditions, explicit pause points, and clearer tradeoffs.

If there is one recommendation to carry into this roadmap, it is this: do not confuse momentum with readiness. When cross-border conditions vary by market and regulation is applied differently across jurisdictions, finance needs evidence thresholds before expansion, not after a failed launch. Finance is not only reporting what happened. It is deciding what should happen next, and what should not happen yet. For a fuller breakdown, read How to Handle Payment Disputes as a Platform Operator.

What CFO modernization means in payment operations#

In payment operations, modernization is not broad finance transformation. It is the narrower shift in how a payment platform initiates, approves, moves, reports, and reconciles money without losing trust in the numbers. Finance transformation is enterprise-wide change across finance processes, systems, and organization. Payment-operations modernization is execution discipline inside that larger frame.

For a platform CFO, the real test is whether growth speed and control quality stay aligned. The mandate combines cost and growth pressure with control requirements, so faster launches cannot come at the expense of accounting integrity. If a new flow goes live but your team cannot explain how balances, fees, reserves, or payouts reached the General Ledger, operations changed on the surface, not in substance.

The core check is whether operational events and accounting entries resolve to the same auditable record. APIs and webhooks help systems communicate and pass event data, but they are not enough on their own. Modernization is real only when events feed finance controls, records can be matched through reconciliation, and the books close cleanly.

A practical test is to trace one payment end to end: initiation request, provider response, webhook updates, internal status changes, and final posting in the books. Then verify that reconciliation works without manual guesswork. If the trace breaks, the usual causes are missing event handling, posting logic that does not mirror money movement, or duplicate side effects on retries where idempotency controls are weak. Related: Finance Operations Priorities for Payment Platform CFOs.

Why CFOs are modernizing now and what actually changed#

What changed is not only the push for growth. Risk now lives in execution details that finance can no longer treat as cleanup work. For a payment platform, modernization becomes urgent when cross-border launches, FX handling, and payment exceptions determine whether revenue is usable, explainable, and repeatable.

Cross-border risk got more local#

Cross-border KYC, KYB, and AML controls do not operate uniformly across markets. FATF sets an international standard, but countries implement measures through their own legal and operational frameworks. As a result, onboarding and monitoring controls can behave differently by corridor.

The failure mode is usually operational, not just a compliance miss. Activation stalls. Manual-review queues grow. Beneficial-owner data is incomplete for legal-entity onboarding. Or approved customers still cannot use the payout path that was modeled. Before you fund a launch, verify that finance can name the exact customer data, verification result, and approval state required to move from onboarding to first live transaction.

Economics moved below the revenue line#

Unit economics now depend on operating precision, not just payment volume. Cross-border payments still face persistent friction in cost, speed, access, and transparency, and remittance economics are shaped directly by transaction fees, exchange rate and FX margin, and service speed.

That means gross payment volume can rise while contribution worsens if exception handling absorbs margin. Review a corridor across quote, conversion, payout initiation, settlement, and returns before you approve spend. If the economics change materially after exceptions, treat that as a market signal, not an accounting footnote.

The CFO role is broader than stewardship now#

Finance is now expected to co-own growth decisions, not only report outcomes. Gartner's survey of 251 CFOs in October 2024 reflects that broader decision mandate. For platform teams, that translates into explicit launch gates, pause gates, and evidence requirements.

The control test is still traceability and retry safety under real volume. If you cannot walk one transaction from API request through provider response and webhook updates to final posting in the books, expansion will surface control gaps quickly. That risk rises when duplicate webhook events and weak idempotent retry handling affect finance outcomes.

Score countries and verticals before committing GTM spend#

Score countries and verticals before you commit GTM spend, because demand alone does not make a market operationally launch-ready. Use one scorecard across markets and use cases so strong demand cannot hide weak compliance, payout, FX, or documentation readiness.

Treat this as a pre-commit operating screen, not a presentation artifact. FATF provides a common AML/CFT framework, but countries do not implement identical measures, and payment infrastructure maturity still varies by region. Keep one scoring structure, then require local evidence for every field.

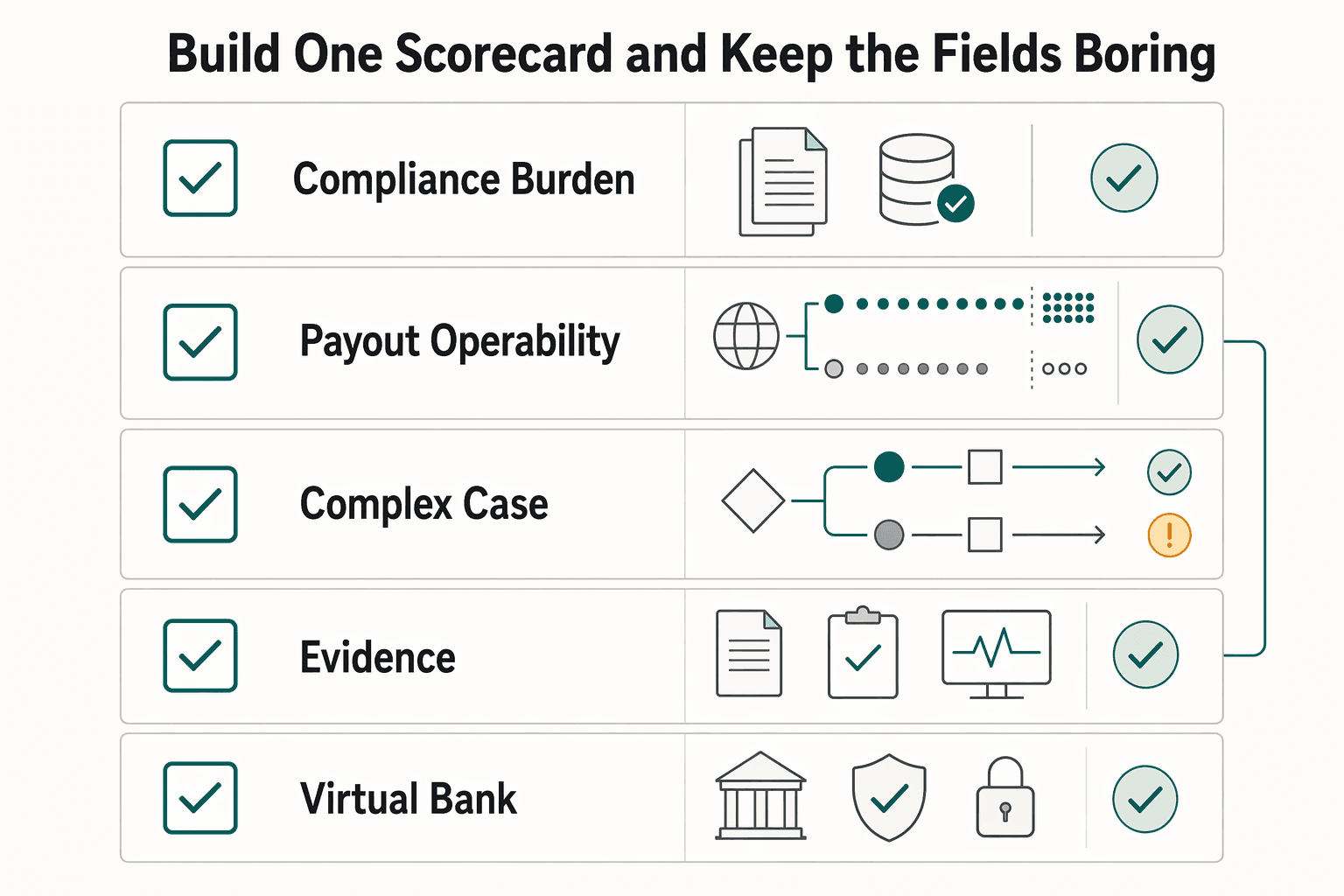

Build one scorecard and keep the fields boring#

If a field cannot be supported by documentation, provider confirmation, or a live test result, it should not be green.

| Score field | What you are checking | Evidence to collect | Common failure mode |

|---|---|---|---|

| Compliance burden | Expected KYC, KYB, and AML friction in onboarding and monitoring | Required entity data, beneficial-owner requirements, approval states, compliance signoff | Sales commits before finance knows what must be verified to activate |

| Payout operability | Whether pay-ins or payouts can actually run in-market | Provider country coverage, licensing or partner permission, payout method confirmation | Commercial demand exists, but the payment path is not legally or operationally available |

| FX complexity | Where conversion happens, what it costs, and what remains opaque after exceptions | Quote source, conversion step, settlement currency, exception path for reversals and returns | Margin looks healthy on quotes, then breaks after failed payouts, retries, or returns |

| Local document expectations | Which finance or tax records must be ready before activation or reporting | W-9 needs for US TIN collection, VIES VAT validation for EU VAT checks where relevant, document retention plan | Onboarding is approved, but reporting or tax handling blocks scale |

| Virtual Bank Accounts viability | Whether Virtual Accounts or a Virtual IBAN improve collections in that market | Product availability, account format, settlement mapping to primary account, reconciliation design | Team assumes local collection behavior the available account structure cannot support |

| Payout Batches fit | Whether the use case needs high-volume disbursement and provider support | Batch API availability, batch-size limits, country reach, retry rules | Manual payouts survive pilot volume, then fail under scale |

| Merchant of Record relevance | Whether a third party should be the legal entity responsible for payment processing | Commercial model, liability allocation, settlement ownership, reporting ownership | Platform launches with the wrong merchant-responsibility assumption |

Two fields need extra precision. First, do not mark payouts as a simple yes or no. One documented product supports Standard Payouts to 96 countries and up to 15,000 payments per call, but those limits are product-specific, not universal. Record the exact product variant, country scope, and throughput you plan to rely on.

Second, score Virtual Bank Accounts carefully. A Virtual IBAN is a unique digital account number linked to a primary bank account. That can improve receipt flow design, but it does not by itself prove local collection fit or reconciliation readiness.

Match the market to the vertical, not just the country#

Score country-plus-use-case pairs, not countries in isolation. A high-volume marketplace or creator model may depend on mature payout batches, while a collections-heavy B2B model may depend more on Virtual Account behavior and reconciliation speed. For direct-to-customer entry, Merchant of Record design can become decisive because the MoR is the legally responsible payment-processing entity.

If one market supports inbound flows well but outbound payouts poorly, that can still justify a limited launch for one vertical and a pause for another.

Use evidence-based decision labels#

Use explicit labels tied to evidence completeness, not optimism:

| Label | Criteria |

|---|---|

| Launch | Compliance requirements are documented, payout routes are confirmed, FX handling is modeled through settlement and exception states, and required documents have clear owners |

| Pilot only | The market is promising but one key assumption still needs proof, such as batch payout behavior, VBA reconciliation, or MoR necessity |

| Pause | A binary blocker remains, such as unclear regulatory permission, missing provider coverage, unknown document expectations, or no credible economics view after FX and payout exceptions |

As a control, ask finance, ops, and commercial leads to produce the same market packet independently. If they disagree on onboarding, payout execution, or mandatory documents, the market is not launch-ready.

How to Build a Deterministic Ledger for a Payment Platform goes deeper on the ledger design choices that make reconciliation and reporting more reliable.

Choose your module sequence based on risk and time-to-value#

Choose the first module by the blocker you need to remove, not by what sounds most strategic. If onboarding friction is the blocker, start with Virtual Bank Accounts plus controlled payout rails. If tax scope and merchant liability are blocking launch, start with a Merchant of Record model.

Use the country-plus-vertical scorecard from the previous section to make that call. A market can show demand and still require a different first module depending on whether your constraint is collections, disbursements, or who is legally responsible for processing customer payments.

| First module | Start here when | Early value | Main tradeoff to price in | Phase exit criteria before next module |

|---|---|---|---|---|

| Virtual Accounts first | Inbound bank-transfer onboarding is the bottleneck and you need cleaner receipt attribution | A virtual bank account number can improve collections routing, and some flows can auto-reconcile transfers to the closest matching invoices | Auto-matching is not full reconciliation; unmatched transfers can remain unreconciled until manual action, and some bank-reconciliation tooling has a US-based availability limit | Prove transfer-to-invoice matching rates, manual handling for unmatched receipts, country and account eligibility, and accounting posting logic for partial, unmatched, and corrected transfers |

| Payout Batches first | Your use case is payout-heavy and manual disbursement operations are the immediate scaling constraint | You reduce one-off payout handling and prepare for higher-volume disbursements | More merchant accounts can mean more payout batches, which can increase report volume and reconciliation effort if account structure is not designed intentionally | Document batch ownership, failure classification, control totals, retry behavior, and reporting volume that finance can close |

| Merchant of Record first | Merchant liability, tax handling, and compliance ownership are delaying launch | The MoR becomes the entity legally authorized and responsible for processing customer payments, and assumes core financial, legal, and compliance liability for those transactions | You may launch faster in some markets, but you are also changing settlement, reporting, and customer payment ownership; scope is product- and market-specific | Document which markets and products are in scope, what the MoR covers, what stays with you or the seller, and how settlement and reporting data land in your books |

Start with the narrowest move that removes a real blocker#

Start with the smallest move that clears a real operating constraint. A VBA-first sequence fits when your first problem is getting money in cleanly. In Stripe's bank-transfer flow, Stripe creates a virtual bank account number customers can transfer to, and Stripe says it attempts to reconcile those transfers to the closest matching invoices. The question is whether that flow reduces manual matching in your target market and entity setup.

Do not assume documented bank-reconciliation tooling applies everywhere. Stripe notes one bank-reconciliation feature is only available for direct US-based Stripe accounts using an automated payout schedule. If your plan depends on that behavior, verify country, account type, and payout setup before you count on a lighter close.

MoR first is a liability decision, not just a launch tactic#

If launch is stalled by merchant-responsibility questions, move MoR to the front. The definition is straightforward: the Merchant of Record is legally authorized and responsible for processing customer payments, and is liable for the financial, legal, and compliance aspects of transactions.

Treat MoR scope as configurable, not universal. Stripe says its managed-payments setup can be applied selectively for specific markets and products, and it positions that offering across more than 75 countries and 35 product categories. Your checkpoint is a written scope map: market, product, reporting owner, settlement owner, and obligations that remain with your entity.

Rollout speed fails when controls lag the module#

Across all three paths, risk rises when a module goes live before posting and retry controls are ready for exceptions. Launch speed can increase reconciliation load when events are retried, delayed, or missing posting rules. Idempotency matters here, but only for the behavior it actually guarantees.

Stripe idempotent requests support safe retries without duplicating the same operation. Repeated requests with the same idempotency key return the same result, including 500 errors. That helps with payout creation and similar operations, but it does not prove downstream accounting correctness. Stripe also notes keys can be removed after they are at least 24 hours old.

Payout-heavy paths need one more design check early. Adyen states that more merchant accounts produce more payout batches, while fewer merchant accounts simplify operations and reduce reconciliation reporting. If you start with Payout Batches, lock merchant-account structure before volume ramps.

Define the next-phase gate before shipping phase one#

Do not add the next module because a pilot feels stable. Add it only when the current phase has closed its known exception class. For VBAs, that usually means unmatched transfers are aged, owned, and posted consistently. For Payout Batches, retries, reversals, and batch control totals reconcile to the books. For MoR, scope, liability boundaries, and settlement reporting are explicit enough that close does not depend on interpretation.

If you cannot write those exit criteria on one page, do not stack the next module yet. If your sequencing decision is stuck on integration and control tradeoffs, review the implementation surfaces in Gruv Docs.

Build the compliance and tax evidence pack before launch#

Build two separate tracks before launch: one for activation, meaning can this account process payments and payouts now, and one for tax reporting, meaning do you have the records needed later. If you mix them, you either block valid accounts for the wrong reason or launch without reporting evidence.

Split activation from reporting#

Treat payout activation as a verification gate, and tax forms as reporting artifacts. Connected accounts must satisfy KYC requirements before they can accept payments and send payouts, and verification is described as a prerequisite for payouts. Keep that activation evidence separate from W-8, W-9, and 1099 workflows.

| Artifact | Primary purpose | Pre-launch checkpoint |

|---|---|---|

| Payout eligibility record | Shows the user or entity passed the provider verification gate for payments/payouts | Confirm verified status and payout enablement in the target market |

| Form W-9 | Collects a U.S. payee TIN for IRS information-return reporting | Define which U.S. personas require collection and where TIN access is restricted |

| Form W-8BEN | Documents foreign beneficial owner status for payer/withholding workflows | Confirm routing and retention, since the payee gives it to the payer or withholding agent, not the IRS |

| VAT Validation via VIES | Checks whether an EU VAT number is registered in the relevant national database | Store result plus check date, and define follow-up when status is invalid or unavailable |

| Form 1099 output | Supports U.S. information-return reporting where enabled | Confirm required output fields are captured before volume accumulates |

Define market and persona rules before the first payout#

Do not use one generic checklist. Build a market-and-persona matrix for required activation evidence versus required reporting evidence, collection owner, and system of record.

VIES is a lookup tool, not a full tax-compliance certificate. Keep both the submitted VAT number and the validation result, with a follow-up path for mismatches.

Add cross-border visibility before it becomes a support problem#

Do not treat FEIE, FBAR, and Form 1099 as universal launch gates. Use them as visibility checkpoints for qualifying U.S. taxpayers or U.S. reporting obligations in scope.

| Item | When relevant | Key detail |

|---|---|---|

| FBAR (FinCEN Form 114) | For qualifying U.S. persons when aggregate foreign financial accounts exceed $10,000 at any point in the year | Due April 15, with an automatic extension to October 15 |

| FEIE | When eligibility conditions are met | Figured on Form 2555; the 2025 maximum exclusion amount listed in IRS instructions is $130,000 |

| Form 1099 output | For U.S. information-return reporting where enabled | Confirm required output fields are captured before volume accumulates |

Keep these items visible if they apply, but do not let them blur into a universal activation checklist.

Mask sensitive fields from day one#

Apply masked-data handling from sandbox onward. Sensitive fields should not be logged directly and should be removed, masked, sanitized, hashed, or encrypted.

Verify this with one full onboarding test: inspect app logs, payload captures, support tickets, and CSV exports. A common miss is masking the UI while raw payloads remain unmasked in logs or attachments.

Teams modernizing ahead of a raise, audit, or IPO can use IPO Readiness for Payment Platforms: The Financial Operations Checklist to pressure-test controls and reporting gaps.

Design reconciliation and audit controls before volume ramps#

Before volume ramps, make reconciliation a scale gate. You should be able to trace money flow from collection through payout to deposited cash without manual reconstruction.

For a payment platform, treat your Ledger as the internal source of truth, and use provider reconciliation outputs as external evidence. Define a reconciliation cadence that fits your payout schedule and close process, then verify that you can join wallet projections, provider payout references, and settlement status back to the same posting records. In Stripe, bank reconciliation and payout reconciliation reports are designed to connect payout activity to bank deposits and reconcile transactions within automatic payout batches.

Make the Ledger the control point#

Do not treat "settled in the provider dashboard" as the final control result. Automatic payouts can include funds from multiple transactions, so you need payout-level traceability.

At minimum, posting records should carry the IDs needed to trace the full path:

- invoice or receivable ID

- collection or charge event ID

- provider transaction and payout reference

- payout status and status timestamp

- bank deposit reference when funds land

Test this with a sample trace before expansion: start from a deposited payout, then walk back through the payout batch and underlying transactions to the originating invoice. If that trace depends on ad hoc exports or memory, controls are not ready for scale.

Use Webhooks for traceability, not just notifications#

Webhooks should update posting state, but they are not guaranteed single-delivery signals. Providers may deliver the same event more than once, so log event IDs and deduplicate before you post financial effects.

Apply the same replay-safe design to API retries. Idempotency exists to prevent duplicate operations during retries. The control objective is simple: one business event, one financial effect, even with retry and redelivery behavior.

Classify exceptions before they pile up#

Classify exceptions early so finance, ops, and engineering work from one queue:

- unmatched deposits

- stale FX quote usage

- return or failed payout flows

- held transactions, including reserve hold and reserve release activity

For FX controls, retain quote ID and expiry context (lock_expires_at) so you can prove whether a conversion used a valid quote window. Lock durations can be short, for example five minutes, or longer, such as an hour or a day, so freshness checks need to be explicit.

For payout aging, avoid false alarms from normal latency. Some payout trace states can remain pending for up to 10 days, so aging rules should separate "within expected window" from "needs intervention."

Set a pause rule before expansion pressure hits#

Set the rollout rule in advance: if reconciliation cannot close within your internal target window, pause new market rollout until you reduce control debt. This is an operating discipline decision, not a legal mandate.

Use concrete evidence for that go or no-go call: latest bank reconciliation report, payout reconciliation output, exception aging by class, and a tested trace from invoice to payout completion.

For a step-by-step walkthrough, see Spending Controls for AI Agents in Platform Payment Operations.

Set API and webhook reliability gates that prevent financial duplication#

Set one non-negotiable rule: one business instruction, one financial effect in the Ledger. Apply that rule to API timeouts, Webhook redeliveries, and queue retries so a retry never becomes a second version of the truth.

Make idempotency a posting control, not just an API feature#

Require Idempotency on every payout-creating POST call and every retry path that could reissue the same instruction. Stripe supports idempotency keys on POST requests and returns the same result for the same key, including 500 responses, so retry handling should assume response replay unless the key changes.

Persist the idempotency key with the payout intent before you send the provider request, then carry that key into posting records and status handling. On Stripe, idempotency keys can be up to 255 characters and can be removed after they are at least 24 hours old. On PayPal REST POST calls, PayPal-Request-Id is the idempotency control, and PayPal warns that omitting it can duplicate the request.

Two failure patterns are common:

- Generic retry code generates a new key and turns a network retry into a second business request.

- Two concurrent requests reuse the same

PayPal-Request-Idand are treated as if both should succeed, even though PayPal notes the first may process and the second might fail.

If your service cannot show which idempotency key maps to which business instruction, treat that as a scale blocker.

Separate retry policy by operation type#

Do not apply one retry policy to every operation. The risk profile changes by operation, so your timeout and retry behavior should too.

| Operation | Primary risk to control | Retry posture | Ledger checkpoint |

|---|---|---|---|

| Quote | Stale pricing | Retry only while quote context is still valid | Store quote ID and expiry context before use |

| Conversion | Duplicate execution | Retry only with the same business identifier plus explicit status checks | Post pending state first; finalize after confirmed result |

| Payout initiation | Duplicate disbursement | Retry only with the same idempotency key | Persist payout intent, request ID, and provider reference |

| Status callback processing | Double-posting on redelivery | Accept redelivery and dedupe by event ID | Log event ID, processing result, and posting reference |

Use webhook dedupe and dead-letter recovery as auditable controls#

Assume webhook duplicates will happen. Stripe notes the same event can be delivered more than once and recommends using event IDs to prevent double-processing. Stripe also retries failed webhook deliveries for up to three days in live mode with exponential backoff, so replay-safe handling is mandatory.

| Record | What it should show |

|---|---|

| Original request record | Idempotency key or PayPal-Request-Id |

| Webhook log | Provider event ID |

| DLQ record | Failure reason and receive count |

| Redrive record | Who replayed it, when, and whether a posting was created or skipped |

Route failed events to a DLQ instead of dropping them. AWS SQS supports dead-letter queues for unprocessed messages, recommends tuning maxReceiveCount to allow sufficient retries, and documents explicit redrive operations to replay failed messages. For finance controls, every redrive should leave an audit-visible recovery record in the posting path.

A minimal evidence pack for this gate:

- Original request record with idempotency key or

PayPal-Request-Id - Webhook log keyed by provider event ID

- DLQ record with failure reason and receive count

- Redrive record showing who replayed it, when, and whether a posting was created or skipped

If replay can post money movement without checking whether that event ID or business request already produced a financial effect, the control is incomplete.

Red flags that should trigger a rollout pause#

Pause the rollout when exceptions are growing faster than your team can explain and remediate. More volume at that point only compounds unresolved control debt.

Compliance exceptions that no one can remediate#

Treat rising AML manual overrides or recurring KYC/KYB failures without a documented remediation path as a stop signal. FATF guidance requires identity verification using reliable, independent sources. U.S. CIP procedures must support a reasonable belief that you know the customer's true identity. Beneficial-owner verification is also required for legal entities under risk-based procedures.

Use a simple readiness test: for each failed or overridden case, can you show the missing evidence, the decision taken, and why it was acceptable? If not, you are scaling judgment without a defensible record.

Reconciliation breaks that survive a reporting cycle#

If provider status and internal balances do not reconcile within a reporting cycle, pause expansion. FCA CASS guidance is clear that discrepancies require a determined cause and records that accurately correspond to client money.

For each break, maintain the provider reference, internal posting reference, exception age, root-cause note, and correction entry where applicable. If you cannot trace one payout from initiation through status updates to final financial effect, the market is not ready for more volume.

Corridor failure concentration and tax-policy ambiguity#

When failures concentrate in one corridor, especially in Payout Batches, treat that concentration as rollout risk even if global success rates look stable. Where ACH applies, monitor unauthorized returns over the preceding 60 days or two calendar months against the Nacha 0.5% threshold. Review concentration by corridor, batch ID, and originator before you add demand.

Pause for tax-policy ambiguity as well. Form W-9 provides the correct TIN, and Form W-8 BEN is provided by a foreign beneficial owner when requested by a payer or withholding agent. Missing tax-status information can pause payouts, and some platforms state payouts should unpause within two business days after successful W-8/W-9 submission if no other requirements remain. If your team cannot clearly define who needs W-8, W-9, or Form 1099 handling, and when backup withholding at 24% may apply, do not scale first and interpret later.

Assign ownership so finance, ops, and engineering do not drift#

Assign clear decision rights up front, or pause signals get debated instead of acted on. In this operating model, the Chief Financial Officer (CFO) should be accountable for launch and pause criteria within executive governance. Payments ops should own day-to-day operational health. Engineering should own API, Webhooks, and Idempotency reliability.

This is not just org hygiene. Payment governance expectations emphasize a clear organizational structure with transparent lines of responsibility, so control decisions and reliability decisions do not blur across teams.

Put one review in charge of go or no go#

Use a weekly control review as the forum where these owners make explicit go or no-go decisions. That cadence is a management choice, not a regulatory mandate, but it keeps one shared view of the items that usually drift apart:

- compliance gates still open or blocked

- exception backlog and exception age

- market-readiness status by corridor or product module

Keep one decision log for that review. For each item, record the evidence reviewed, the decision taken, the owner, and the next checkpoint date.

Tie the RACI to checkpoints, not initiative names#

A RACI chart works when it is tied to specific tasks, milestones, or deliverables, not broad labels like "Finance Transformation." Assign ownership to concrete checkpoints. Examples include approving launch criteria for a defined rollout, clearing a webhook replay gap, or resolving reconciliation exceptions tied to a release gate.

Include a checkpoint for undelivered webhook recovery. If your provider can automatically resend failed events for up to three days, someone must verify replay handling inside that window and confirm no duplicate posting impact. This is where idempotency ownership becomes operational: the same idempotency key should return the same prior result on retries, rather than creating duplicate financial side effects.

90-day execution checklist for a CFO-led modernization#

Use the next 90 days to prove controls, traceability, and market assumptions before you scale volume. This timeline is a management framework, not a regulatory standard.

Days 1 to 30#

Start by baselining failure modes. Expansion planning is not credible until you can explain the current transaction path.

- Trace a representative sample of real transactions from initiating API call to webhook events to final posting in the books across collections, conversions, and payouts.

- If that chain is not clean and reproducible, pause expansion planning.

- Finalize market scorecard inputs by country or corridor: KYC/KYB/AML burden, FX exposure, and payout constraints.

- Treat money-laundering and terrorist-financing exposure as an early planning input, and include cross-border frictions.

- When your scorecard is ready, validate market and module coverage assumptions with the Gruv team via Contact.

Frequently Asked Questions

What should a CFO prove before scaling payment volume?

Before volume scales, the team should be able to trace one transaction end to end, explain the approval path, and show how failures, reversals, and retries are handled. If those controls are not observable in a live workflow, expansion assumptions are still theoretical.

Which controls belong in the first modernization wave?

Start with the controls that protect ledger accuracy and release discipline: approval ownership, tax and compliance evidence, reconciliation checkpoints, and a documented exception path. Those controls create the operating base that later automation and corridor growth depend on.

How should finance, ops, and engineering divide ownership?

Own checkpoints rather than broad initiative labels. Finance should own policy and release evidence, ops should own runbook execution and exception handling, and engineering should own the event, ledger, and integration behaviors that make those controls observable.

What should trigger a rollout pause?

Pause when the team cannot explain a failure path, cannot reproduce approval evidence, or sees reconciliation drift between system states and settlement outcomes. A pause is also justified when webhook recovery, provider status handling, or tax/compliance evidence is still incomplete.

Why does webhook recovery belong in a CFO modernization plan?

Because finance operations depend on complete event evidence, not just successful API calls. If failed or delayed events cannot be recovered and replayed safely, the organization loses confidence in status changes, exception handling, and period-close reporting.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- advocacy.sba.gov/2026/02/18/fincen-issues-exceptive-relief-to...trusted

- ec.europa.eu/taxation_customs/vies/index.htmltrusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- europa.eu/youreurope/business/taxation/vat/check-vat-n...trusted

- federalreserve.gov/publications/2022-ar-payment-system-and-rese...trusted

- federalreserve.gov/supervisionreg/srletters/SR9551a2.pdftrusted

- irs.gov/forms-pubs/about-form-w-9trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

IPO Readiness for Payment Platforms Starts in Financial Operations

Use this checklist to separate **expansion readiness** from **filing readiness** before you commit to new markets. A payment platform can be ready to launch in a new country or vertical yet still be unready for IPO scrutiny. Filing readiness brings its own requirements: SEC effectiveness before securities can be sold, ongoing Exchange Act reporting, and CEO/CFO certification tied to Form 10-K and Form 10-Q.

Finance Operations Priorities for Payment Platform CFOs

When a payment platform expands, the finance question that shapes execution is often not broad strategy alone. It is country-level operability. Can your team move funds, verify counterparties, manage exceptions, tie activity back to the ledger, and handle tax and reporting work without building a fragile manual operation?

How Modern CFOs Make Payment Platform Expansion a Strategic Driver

A payment platform should choose its next market based on operational readiness, not volume forecasts alone. The real question is whether you can run that market safely and clearly without creating finance debt that later shows up as payment, reconciliation, or compliance failures. If you cannot explain that operating path cleanly, your forecast should not carry the decision.