Quick Answer

Use spending controls for ai agents as an end-to-end release system, not a budget alert. Set policy and approval rules first, enforce limits before execution, and require Human-in-the-loop review for first-time payees, exceptions, and override requests. Then verify each payout through provider status, Ledger posting, and Reconciliation before treating it as complete. For cross-border flows, keep KYC, KYB, AML, VAT, and W-8 or W-9 checks as explicit gates where required by program and jurisdiction.

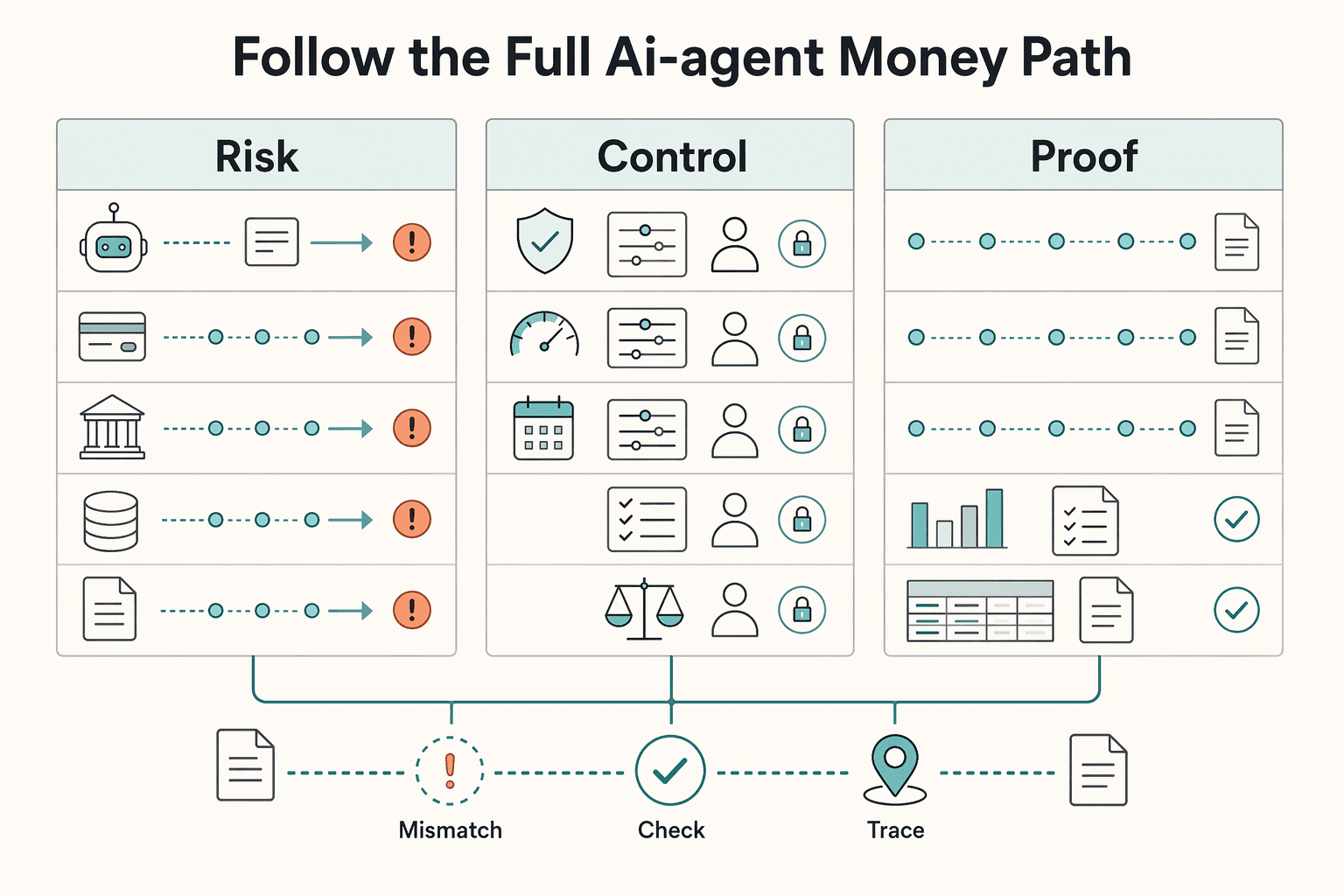

Follow the full AI-agent money path#

Spending controls for AI agents are only credible when they follow the full money path, not just the moment an agent asks to spend. For platform finance, ops, and product owners, the job is to set approvals, hard limits, and human-in-the-loop checkpoints that can actually be enforced from authorization through execution, settlement, posting to the books, and final record matching.

That end-to-end view matters because payment activity is staged. In common card-network processing, authorization, clearing, and settlement are distinct steps, so an approved transaction is not the same thing as completed settlement. If you design controls as if approval alone proves money movement is finished, you can miss late failures, timing gaps, and posting mismatches that show up after the agent has already moved on.

Treat the agent as a requester and initiator, not as the final authority on whether money should leave your platform. The authority comes from policy gates, approval rules, and accounting checks that stay visible after execution. A simple rule is worth adopting early: if your team cannot trace one payment from the agent decision to the execution event and then to the resulting journal entry, the control is not ready for production.

For higher-risk AI uses, human oversight should scale to risk, autonomy level, and context of use. That does not mean a person needs to click every payment. It means you should define clear intervention points for the cases most likely to cause harm or cost, such as new counterparties, policy exceptions, unusual spend patterns, or time-sensitive manual overrides. For higher-risk activity, people need a real chance to review and intervene, not just receive an alert after funds have moved.

Reconciliation is where weak designs usually get exposed. In accounting terms, it is the comparison of two sets of records to confirm they match and to identify discrepancies when they do not. In practice, that means your controls need to survive contact with provider statuses, settlement timing, and posting rules. If an execution record says paid but your books or downstream records disagree, you need an exception path, not a quiet assumption that the data will sort itself out later.

One scope warning upfront: payout availability and timing are not uniform across industries, countries, or programs. Some programs use context-dependent initial payout schedules, such as 7 to 14 days after a first successful payment. So do not hard-code one approval or release pattern and expect it to travel unchanged. Configure explicit policy gates by market and program context where supported, then expand agent autonomy only where your controls remain observable and enforceable.

Related reading: FBAR for a Foreign-Owned US LLC and the Filing Path That Works.

Define spending controls before you configure tools#

Set policy first, then configure tools to enforce it. Spending controls for AI agents should define what an agent can spend, when it can spend, and when an approval chain must intervene.

| Control family | What it covers |

|---|---|

| Per-agent limits | What an agent is allowed to spend |

| Purpose or category constraints | Prevent drift into unrelated payment types |

| Counterparty allow/deny rules | Who can receive funds |

| Variance alerts with escalation | Unusual activity that should route to blocking, freezing, or manual review |

Treat the agent wallet as an execution surface, not the authority layer. Use policy rules to gate signing actions before funds move, keep the general ledger as the accounting source of truth, and use the audit trail to preserve who did what and when. This separation is what lets you investigate cases where execution and downstream records do not match.

Before choosing vendors or wiring automation, define at least four control families:

- Per-agent limits for what an agent is allowed to spend

- Purpose or category constraints to prevent drift into unrelated payment types

- Counterparty allow/deny rules for who can receive funds

- Variance alerts with escalation so unusual activity routes to blocking, freezing, or manual review instead of passive notification

Your operator check should be explicit: for any executed transaction, you can trace the policy decision, execution event, ledger record, and reconciliation status. If one link is missing, the control is not production-ready in practice.

Do not treat approval as completion. Reconciliation is where you compare records and resolve discrepancies, so controls should be measurable at that checkpoint, especially for new counterparties and alerts that require human-in-the-loop review.

You might also find this useful: Internal Controls for Accounts Payable on Platforms: How to Prevent Fraud and Ensure Accurate Disbursements.

Place controls at the right layer of the payment stack#

Place controls by function: policy decides, execution moves funds, and accounting confirms truth. Keeping those layers separate makes decisions easier to defend when settlement, posting, or final record checks do not line up.

A clean split is also easier to verify. The policy layer should allow or block requests, route approvals when needed, and record approval evidence. That mirrors document-approval flows where purchase orders are routed to approvers and approval actions are recorded. Execution should follow that decision through payout rails or batch release. In procure-to-pay integrations, approved or canceled purchase orders can be published by batch; payout batches should likewise release approved instructions, not create approval at release time.

Use movement tools for movement, not authority#

Use virtual accounts for visibility, not authority. They provide sub-ledger reporting while settlement cash concentrates in a physical account, which helps operations track activity by agent, customer, or use case without treating the virtual view as the accounting record.

Set the control gate before release to the rail. A practical pre-release check is whether the request has a policy decision ID, approved counterparty data, and the expected payment purpose or category. If any are missing, hold the instruction for review.

Feed upstream business signals into payment permission#

Build payment permission from upstream source-to-pay signals, not from payout-time guesses. Accounts payable invoice matching connects vendor invoice, purchase order, and product receipt information; procure-to-pay runs from purchase order through shipment, receipt, invoice, and payment; and e-invoicing flows can add business rules and audit-ready tracking without breaking source-to-pay operations.

| Signal | Related workflow | Section note |

|---|---|---|

| Matched invoice and PO status | Accounts payable invoice matching | Connects vendor invoice, purchase order, and product receipt information |

| Receipt or delivery confirmation when required | Procure-to-pay | Runs from purchase order through shipment, receipt, invoice, and payment |

| Supplier identity and approval state | Upstream source-to-pay signals | Carry forward into payment permission |

| E-invoicing rule outcomes | E-invoicing flows | Can add business rules and audit-ready tracking without breaking source-to-pay operations |

Carry forward signals such as:

- matched invoice and PO status

- receipt or delivery confirmation when required

- supplier identity and approval state

- e-invoicing rule outcomes

If wallet balance and ledger journal disagree, treat the ledger as authoritative for investigation and open an exception case with the wallet event, payout reference, journal entry, and current status. Reconciliation exists to confirm the completeness and accuracy of cash in the general ledger, so this check is where disputes should be resolved.

Related: A Real Estate Agent's Guide to the Home Office Deduction.

Build an approval matrix that scales with risk#

Your approval matrix should answer one question first: can this payment go straight through, or does a named person need to review it? Use a simple default rule: if the request is policy-compliant and the counterparty is pre-approved, allow straight-through processing. If not, route it to a specific approval-chain owner with a review SLA set to your risk tolerance and staffing capacity.

Keep this routing in an approval rules engine, not in inbox habits. Route to identified approvers, record approval actions, and treat urgency as a routing factor, not as a source of new spending authority.

Use risk triggers that map to one owner#

Define a small set of triggers and map each one to a single owner role so exceptions do not drift between teams.

| Trigger | Required approver role | Max autonomy allowed | Required audit trail evidence |

|---|---|---|---|

| Policy-compliant request to a pre-approved counterparty | No manual approver, auto-approved by rules engine | Straight-through processing | Policy decision ID, approved counterparty record, purpose or category, release timestamp |

| First-time payee | AP or procurement owner | Request can be created, but not released until reviewed | Counterparty approval record, request details, approver identity, approval action and time |

| Policy exception, missing data, or mismatch | Finance approver or exception owner | Hold funds release pending review | Exception reason, supporting documents, policy rule hit, reviewer decision, remediation notes |

| Repeated variance alerts or manual override request | Risk, finance, or delegated control owner | Temporary hold or one-time exception only | Prior alert history, override reason, named approver, linked payout reference, post-event review note |

| Settlement marked urgent | Named business owner plus finance owner if it breaks the normal path | Limited escalation only; urgency does not create new spending rights | Urgency reason, original due date, approval actions, final release reference |

Make Human-in-the-loop explicit#

Put human-in-the-loop triggers directly in policy for first-time payees, repeated variance alerts, and manual overrides. This keeps exception handling explicit instead of reactive.

Set oversight to the autonomy and risk of the workflow. Control design should match your risk tolerance and resources, and human oversight should be effective for the system's risk, autonomy, and context of use. Before release, verify the request has a policy decision ID, counterparty status, and either an approval action or a valid auto-approval result. If a manual override was used, require the override reason and approver identity in the same audit trail path as the payout reference.

Use timed SLAs for each review tier, but set durations to your actual volume and reviewer capacity. If the SLA expires without action, keep the request blocked rather than releasing it by age.

For a step-by-step walkthrough, see A Deep Dive into the UAE's Corporate Tax for Freelancers and LLCs.

Set limit hierarchies to stop runaway spend early#

Do not rely on one global cap; layer limits across action, agent, counterparty, and cycle so concentrated risk is blocked before money moves.

Pre-authorization controls support this approach because they can decline disallowed spend before authorization handling. In card-based flows, controls can be applied at both the card and cardholder level. Also, do not treat platform defaults as policy: for example, Stripe Issuing notes a default 500 USD per day limit on newly created cards if limits are not set, plus an unconfigurable 10000 USD per-authorization limit.

| Limit type | What it protects | Where to route review |

|---|---|---|

| Per action or authorization | Prevents a single oversized or out-of-policy payment | Your approval-chain owner for payment exceptions |

| Per agent or cardholder | Limits cumulative spend from one actor | Your owner for agent/cardholder controls |

| Per counterparty | Reduces concentration to one supplier or payee | Your procurement/AP counterparty owner |

| Per cycle or time window | Caps exposure across a day, month, or settlement window | Your risk/treasury exposure owner |

Set thresholds by use case, not as one shared band. In AP Automation, tolerance should track whether invoice, purchase order, and receipt evidence align (three-way matching). In e-Procurement, controls should reflect lifecycle stage, from planning through contract management. In Supply Chain Finance, avoid inheriting AP thresholds directly, because payables finance is buyer-led and exposure/concentration controls matter differently.

When the same limit is breached repeatedly, auto-pause instead of letting alerts stack. One practical pattern is setting a cardholder to inactive status, which forces declines on attached cards. Reactivation should require a documented review decision and a clear remediation step in your own approval workflow.

Before reactivation, confirm which limit was hit, the time window involved, counterparty status, and what changed to reduce repeat risk, especially where exposure is monitored across multiple settlement dates or entry types.

We covered this in detail in Best Corporate Debit Cards for Global Spending in Small Teams.

Run the authorization to reconciliation sequence in fixed order#

Define one canonical money path and run it in the same order every time: request intake, policy checks, compliance checks, execution, provider status ingest, ledger posting, then final reconciliation. The point is not that this is a universal standard, but that a fixed internal order prevents retries from creating accounting drift.

Approval is not completion. A payment can pass policy and execute, then still break close if status ingest, posting, or matching runs from stale or duplicate events.

Keep one canonical money path#

Treat each stage as gated by explicit evidence before the next step runs.

| Stage | Evidence to advance | Replay risk to block |

|---|---|---|

| Request intake | Stable operation ID and request snapshot | Same request submitted twice |

| Policy + compliance | Recorded decision and pass/hold outcome | Conflicting outcomes from re-runs |

| Execution | Provider reference for the attempt | Duplicate payout or authorization |

| Status ingest + posting + reconciliation | Current provider state, one journal post, and matched/exception state | Duplicate entries or premature close |

If you use real-time card authorization, keep the synchronous step narrow. In Stripe Issuing, you must approve or decline within 2 seconds before timeout behavior applies, so heavy lookups and manual review should stay out of that path.

Make retries boring#

Retries are normal, so idempotency should apply to every write step that changes money movement or accounting state. Use a stable operation key and persist the first result so connection failures can be retried safely without duplicate payouts or duplicate journal entries.

Webhook/event pipelines should also assume at-least-once delivery and out-of-order arrival. When payloads look stale or partial, fetch current state before posting or matching.

Do not close until reconciliation criteria are met#

Late and reordered updates are expected in async systems, and some event infrastructure waits 30 seconds for an endpoint response before retrying. Hold settlement closure until your internal reconciliation criteria are met and any differences are either resolved or explicitly opened for follow-up.

As an operating checkpoint, keep one audit-trail view that ties together the decision record, provider reference, posting result, and current reconciliation state for each executed payout. That makes exceptions visible before period close instead of after it.

Prepare exception handling before launch day#

Before launch, define exception queues, default operator actions, and a minimum evidence pack so unresolved payments do not become ad hoc decisions.

Exception queues are the investigation stage in payment processing, so treat them as first-class controls. A practical setup for this workflow is blocked compliance checks, unmatched deposits, request-context mismatches, and posting mismatches between the agent wallet and the ledger.

| Queue | What belongs there | Default action | Minimum evidence before closure |

|---|---|---|---|

| Blocked compliance check | Payment held or rejected by compliance screening | Manual review, reject, or escalate to approval chain | Operation ID, counterparty details, screening result, request snapshot, provider reference |

| Unmatched deposit | Funds visible on a virtual account or statement with no matched open item | Manual review, then retry posting if a match is confirmed | Virtual account identifier, master account reference, amount, payer reference, statement line |

| Request-context mismatch | Execution or status event that does not align with the approved request context | Retry fetch of current state, then escalate if still inconsistent | Decision ID, request snapshot, current request version, event timestamp |

| Agent wallet vs ledger mismatch | Wallet movement without matching journal entry, or journal entry without matching wallet movement | One idempotent retry, then manual review | Wallet event ID, journal reference, provider reference, reconciliation status |

Keep action rules explicit. Retry only when the issue appears transport-related and the write is idempotent. Use manual review where rails can still produce later returns through manual handling. Reject when evidence shows the transaction should not proceed, and escalate when an operator cannot validate it from the current record.

Require a consistent evidence pack: operation ID, policy decision, provider reference, journal reference, and relevant external bank signals. For return handling, include camt.053 details when present. If a transaction is rejected for sanctions reasons, capture the identifying details needed for rejected-transaction reporting, to the extent available.

Use virtual accounts as an investigation path, not the settlement source of truth. They help track transactions by unique identifier, while funds settle in the linked master account. For items your program labels as credited, held, or returned, investigate against both the virtual account identifier and the master-account settlement record, and document your own reopening criteria for suspended agents.

Set a clear internal decision rule: if an exception cannot be resolved with existing evidence, pause new spend with that counterparty until the case is closed or a human approver accepts the risk.

Add cross-border compliance and tax gates to spending decisions#

Use cross-border compliance and tax controls as payout release gates: if required checks are missing, the payout stays queued.

| Gate or artifact | When noted in the section | Operational note |

|---|---|---|

| KYC | For individuals | Decision record should show which requirement cleared for that flow |

| KYB plus beneficial ownership checks | For legal entities | Decision record should show which requirement cleared for that flow |

| AML screening | When required by your program | If required checks are missing, the payout stays queued |

| VAT identification numbers | For EU businesses | Where supported, use VIES as the operational checkpoint |

| Form W-8BEN | If a payer or withholding agent requests it | Require it before release |

| Form W-9 | If you need a correct TIN for information returns | Require it before release |

| Form 1099-NEC reporting | Payments to independent contractors may require it | Gate on downstream tax artifacts |

| FBAR / FinCEN Form 114 | Cross-border account and income facts may affect obligations | Tied to the cited $10,000 aggregate foreign-account threshold |

Start with identity and AML scope. Your decision record should show which requirement cleared for that flow: KYC for individuals, KYB plus beneficial ownership checks for legal entities, and any AML screening your program requires. In U.S. regulated contexts, CIP requires identifying information before account opening, and beneficial ownership rules require covered institutions to identify and verify beneficial owners of legal-entity customers. Do not assume one checklist works globally; confirm scope by jurisdiction, rail, and rollout with legal and compliance teams.

Then gate on tax status and reporting readiness. Validate VAT identification numbers for EU businesses, and where supported use VIES as the operational checkpoint. If a payer or withholding agent requests Form W-8BEN, require it before release. If you need a correct TIN for information returns, require Form W-9.

Finally, gate on downstream tax artifacts. Payments to independent contractors may require Form 1099-NEC reporting. Cross-border account and income facts may also affect FEIE eligibility and FBAR obligations, with FBAR filed on FinCEN Form 114 and tied to the cited $10,000 aggregate foreign-account threshold.

Keep operations PII-safe throughout. Show masked identifiers in review tools instead of raw tax forms or full account data; for payment data, displaying only the first six and last four digits is an established masking control. Store W-8, W-9, TIN, and related tax artifacts in encrypted systems of record, and let operators work from status flags, document presence, and expiry dates.

Conclusion#

Teams that get spending controls for AI agents right do not treat them as nicer budget alerts. They treat them as a governance model for money movement: operating model, policies, controls, traceability, and review steps that stay connected from request to final outcome.

That matters because durable cost control is a lifecycle job, not a one-time budget setting. The stronger pattern is to start with explicit governance controls, then widen autonomy only after behavior is stable over time. In practice, that means checking more than approval success. You want visibility into exceptions, retries, and whether records remain traceable end to end without manual reconstruction.

A practical expansion rule is simple: if you cannot trace an executed action back to its policy decision and final status in one audit trail view, do not grant the agent more authority. That checkpoint keeps autonomy honest. It also lines up with the traceability principle behind Article 12 of the EU AI Act for high-risk AI systems, where automatic event logging over the system lifetime is part of the design, not an afterthought.

For rollout, prove the model on one use-case profile first. NIST AI RMF 1.0 (2023) frames profiles as specific to a setting, risk tolerance, and available resources, which is the right way to scope agent spend. A pilot should test the strengths and weaknesses of the approach before scaling. If your first candidate is too noisy to evaluate clearly, start with a cleaner repeatable flow and use that to validate controls.

The failure mode to avoid is broad autonomy backed by weak evidence. Teams can see straight-through approvals working and assume the design is mature before the underlying control evidence is strong enough. Before you extend the model to new programs, keep a short evidence pack: sampled exception cases, override reasons, linked policy decisions, event logs, and final outcomes. If that pack shows outcomes are understandable and attributable over time, then expand. If not, hold scope, tighten controls, and fix the visibility gap first.

Frequently Asked Questions

What are spending controls for AI agents in payment operations?

They are rules that determine whether an agent can authorize or release money, under what limits, and when a person must step in. In practice, these controls span approval, execution, and record checks so each payout can be traced to a policy decision and a financial record.

What controls are mandatory before allowing any autonomous spend?

There is no single global checklist that is mandatory in every country and program. A practical baseline is to run policy checks before release, apply the jurisdiction-specific compliance checks that apply, use idempotency keys so retries do not create duplicate payouts, and keep logs detailed enough to review who approved what.

When should Human-in-the-loop approval be required instead of auto-approval?

Use human-in-the-loop when risk is not routine or when a case falls outside normal policy. The decision rule should be risk-proportional, and in the EU AI Act context, Article 14 makes human oversight a design requirement for high-risk AI systems.

How do you prevent runaway spend across multiple agents and payout rails?

Do not rely on a single cap alone. Combine limits with monitoring of aggregate exposure across agents and rails, and treat repeated failed or retried execution attempts as escalation signals. A common failure mode is retry logic that resubmits the same payout, so use an idempotency key on execution requests to prevent duplicate execution.

What must be logged in the Audit trail for finance and compliance review?

Log the initiator and tie each event to a specific user or agent identity, because review only works when activity is attributable. Keep enough context to reconstruct the decision and execution path, including approvals, key transaction identifiers, and any overrides.

How should teams handle Ledger and wallet balance mismatches?

Treat mismatches as exceptions that require reconciliation. Reconciliation is used to compare records and resolve differences, so compare payment records and accounting records directly and resolve discrepancies before proceeding.

What parts of approval and compliance policy vary by country or program?

A lot can vary by jurisdiction, program design, and use context. Do not hard-code one autonomy or compliance rule set and assume it applies the same way in every market.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- ec.europa.eu/taxation_customs/viestrusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- federalreserve.gov/frrs/regulations/payment-clearing-and-settle...trusted

- irs.gov/businesses/small-businesses-self-employed/re...trusted

- irs.gov/individuals/international-taxpayers/foreign-...trusted

- taxation-customs.ec.europa.eu/taxation/vat/vat-directive/vat-identificatio...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Best CRM for a Real Estate Agent

If you start with "what is the **best crm for real estate agents**," you will probably compare demos, feature grids, and pricing pages before you define what your business actually needs. That is backwards. A CRM is not just a contact database. It is where your leads, follow-ups, campaigns, client communication, and day-to-day visibility either stay organized or start slipping.

Home Office Deduction for Real Estate Agents: Qualify, Choose a Method, and Keep Records

If you file Schedule C, the key question is not whether this deduction looks aggressive. It is whether you can prove you qualify, choose the right method for that tax year, and support the claim with clean records.

Internal Controls for AP Platforms to Prevent Fraudulent Disbursements

Start here: your AP control design should reduce fraudulent disbursements and payment errors without turning every payout into a bureaucratic exercise. In practice, that means clear escalation points at the moments where money can move incorrectly, not extra approvals added just to look controlled.