Quick Answer

Separate checkout from payouts first, then lock a single release-control path before any money moves to providers. The article’s decision rule is to keep disbursements blocked when classification, tax routing, or required review evidence is incomplete. It also treats Form 8938 as a reporting branch tied to return filing context, not as a direct approval gate. A defensible launch record names the reviewer, captures source version dates, and states whether Form 8938, FBAR, both, or neither applies.

How Compliance-First Payouts Work for Pet Services Platforms#

If you are building a marketplace for pet care, the hard part is not just taking bookings and collecting customer payments. Your platform connects pet owners with caregivers rather than delivering care directly, so you also have to manage scheduling, messaging, payment processing, and payout release after service completion.

The cleanest way to handle that is to split the problem in two. First, map how owners and providers move through scheduling, messaging, payment processing, and service completion. Then build commission and payout logic around that path so funds are released only after the service is complete.

That sequence matters throughout the rest of this guide. You will start with country and operating assumptions, move into classification and basic compliance checks, then finish with payout rails, reconciliation, and launch checks.

Separate customer checkout from provider payout architecture#

Treat checkout and payouts as two different products from day one. Your checkout stack handles customer collection: scheduling and booking, invoicing, card and digital-wallet payments, payment links, and automated reminders. That matters operationally, but it does not answer the payout question.

Provider payout operations need a separate review. If a demo only shows scheduling, billing, and customer checkout, it does not prove payout readiness. It proves checkout readiness.

Use this checkpoint in every vendor review: if the demo only shows scheduling, billing, and card capture, you are evaluating checkout, not payout architecture.

Define success for that split with explicit payout and reconciliation KPIs so exceptions and handoffs are visible.

For a walkthrough, see How EdTech Platforms Pay Instructors Globally: Compensation Models, Payout Controls, and Reconciliation. Related: How EdTech Platforms Pay Tutors: Tax and Payout Architecture.

Gather prerequisites before choosing countries#

Choose countries only after you lock a written input pack. Otherwise, demand signals can outrun your operating model and push pricing or product decisions ahead of evidence.

Build a minimum country-selection pack#

Build this pack before vendor talks or take-rate modeling. Start with the marketplace shape: pet owners, service providers, and your platform, which makes this a three-sided model. Then define the service categories you plan to support, such as walkers, sitters, groomers, trainers, or veterinarians.

Write it at a level your operations or finance team can challenge quickly. "Europe" is too broad. "Two named markets, dog walking and sitting, launch as a three-sided marketplace" is usable.

Lock trust controls before launch assumptions harden#

Lock trust controls early, before launch assumptions harden into product and support work. For each market, define how provider verification works, what insurance expectations apply, and what profile detail is required.

Include review and reputation mechanics in the same readiness check. Reviews shape future bookings, so they are core operating logic, not a nice-to-have.

Clarify the transaction flow before build work starts#

Do not let country choice turn into build work until the transaction flow is clear. In this model, the platform handles payment processing, scheduling coordination, and messaging, and it may hold funds until service completion.

| Area | Item | Detail |

|---|---|---|

| Feature support | Online scheduling | Confirm minimum feature support across tools and vendors |

| Feature support | Client and pet profiles | Confirm minimum feature support across tools and vendors |

| Feature support | Payment processing | Confirm minimum feature support across tools and vendors |

| Feature support | Automated reminders | Confirm minimum feature support across tools and vendors |

| Fee assumption | Provider commissions | 15-25% range |

| Fee assumption | Booking fee | $2-5, if used |

Confirm those minimums across tools and vendors. Set fee assumptions explicitly, such as provider commissions in the 15-25% range and, if used, a $2-5 booking fee, so market comparisons stay consistent. Once that pack is written, you can move from market interest to operating and pricing decisions without guessing.

Choose worker classification and tax handling before pricing#

Treat pricing as provisional until you define worker classification and tax handling for each launch market. The source material here describes platform participation roles, but it does not provide explicit worker-classification or tax-rule instructions, so unresolved items should not be treated as pricing-ready.

Separate platform labels from legal status#

Separate platform labels from legal status. In the PetBacker terms, users are defined as either a Service Provider or a prospective Service User, but those labels alone do not establish employment or tax treatment.

| Path | What must be decided before pricing | Operational consequence |

|---|---|---|

| Employee path | Legal/tax classification and payroll operating path | Plan a distinct onboarding, approval, and payout-control flow |

| Contractor path | Legal/tax classification and contractor operating path | Plan a distinct onboarding, documentation, and exception-control flow |

| Classification unclear | Legal/tax interpretation still open | Keep payouts disabled until resolved |

If you cannot show this record for a market, keep pricing provisional.

Map tax-document handling early#

Map tax-document handling early, but do not confuse document collection with correct classification. Taxpayer-reporting context and platform controls should stay separate.

The source material does not specify tax forms, withholding rates, filing thresholds, or filing deadlines. Keep those requirements in a separate, market-by-market compliance decision before launch.

Pause payout activation until classification is clear#

Use a hard rule here: if classification is uncertain, pause payout activation in that market. Expanding onboarding first can create rework across forms, payout promises, and support operations.

Require an evidence pack before the first live payout: classification record, tax-handling branch, onboarding checklist, and payout exception controls. If one item is missing, do not launch payouts.

Stress-test margin with compliance workload included#

Stress-test margin with compliance and exception workload included, not just gross commission splits. A model that works only on clean-flow assumptions can break once operational friction shows up.

Model economics across at least a clean path and an exception-heavy path before you lock take rate. Price after classification and tax handling are mapped, not before.

For a related walkthrough, see How Legal Platforms Pay Interpreters and Court Reporters.

Design compliance gates that must pass before any payout#

Once classification and tax handling are set, payout release needs its own control sequence based on your compliance policy. No payout should be released until every required gate in that policy passes, and every retry should inherit the existing case state. If a provider is failed or under review, the next attempt stays blocked until a reviewer changes that status.

Set one gate order in policy and product logic#

Set one non-bypassable gate order in policy and product logic, then route every payout attempt through it. A workable sequence can include identity verification, required screening checks, AML review, then release. The exact order matters less than consistency, ownership, and an auditable record.

| Gate outcome | Action owner | Escalation path | Release decision |

|---|---|---|---|

| Hard fail | Named compliance owner closes under current facts | Escalate to legal or senior compliance when regulatory or suspicious-activity risk is present | Do not release |

| Soft fail | Operations or compliance requests refreshed documents or manual review | Escalate to a second reviewer when evidence conflicts or remains incomplete | Hold until resolved |

| Timed hold | Payments or risk owner applies a temporary hold with a stated reason | Escalate to manual review before hold expiry | Do not auto-release |

Verification point: A blocked payee's second payout attempt should return the same stored outcome, not a fresh pass.

Keep retries in the same case record#

Retries should resume from prior state, not from a new button click. Bank-detail edits, document resubmissions, or transfer retries should not reset unresolved compliance outcomes.

Keep one case record per provider and gate state with timestamps, reference IDs, reviewer actions, and the final hold or release decision. Amend the record when facts change. Do not overwrite history. A timed hold should end in reviewed release or continued hold, never silent release because time passed.

Keep tax reporting separate from payout approval#

Keep tax reporting on a separate track from payout approval. Tax forms affect reporting and documentation duties, but they are not payout-release controls.

For U.S. tax context, the IRS states Form 8938 is used to report specified foreign financial assets when applicable thresholds are exceeded, and those thresholds are not universal. IRS materials also direct filers to review Form 8938 instructions for exceptions. IRS materials also state Form 8938 should be attached to an annual or amended return, and filing Form 8938 does not remove possible FinCEN Form 114 (FBAR) obligations.

Some filers may need both, with separate penalties possible. Keep Form 8938, FBAR, FATCA, W-8, and related reporting items in a tax matrix, not in your payout gate logic. For that mapping, see FATCA and W-8 Tax Compliance for Platforms: How to Avoid Withholding on Foreign Payouts.

Verification point: Your payout approval UI should not treat "Form 8938 filed" as a release condition.

Trigger manual review with a short, current checklist#

Manual review should be triggered by a short, current checklist, and any sensitive post-approval change should be able to force a new hold.

| Review area | What it covers | Article action |

|---|---|---|

| Identity verification | Verification result, response ID, document type, and mismatch reason | Current threshold pending policy verification for amount, geography, or risk triggers |

| Screening checks (where required) | Provider, match result, list/reference version, and reviewer disposition | Rescreen on policy-defined events |

| AML review | Exact trigger facts, reviewer notes, and final disposition | Current AML review threshold pending policy verification for transaction or velocity triggers |

| Post-change safeguards | Beneficiary details, bank details, or key contact details | Reapply hold after sensitive changes; hold duration pending policy verification |

Use current verified policy values wherever the table marks an item pending. For sanctions design, see OFAC Compliance for Payment Platforms: How to Screen Every Payout Against the Sanctions List.

Release only when the full gate sequence and evidence pack are complete. If any required item is missing, keep the payout on hold.

We covered this in detail in How Beauty and Wellness Platforms Pay Stylists and Therapists in Chair Rental and Employee Models.

When you define release states, retries, and evidence capture, use the implementation details in the Gruv docs to keep controls traceable.

Map payout rails timing and exception handling by market#

A market is not launch-ready just because you can charge customers there. It is ready when your payout map shows how funds move, what can fail, who decides the next action, and which record proves that decision.

Build a market matrix from provider evidence, not sales claims#

Create one row per launch country with one primary rail choice per row. Build it from provider contracts, implementation docs, test results, and pilot outcomes. If anything is unknown, mark it pending and block go-live until it is verified.

| Checklist item | What to capture | What the matrix should show |

|---|---|---|

| Rail choice | One primary rail choice per launch country row | Which rail is used |

| Beneficiary data | Beneficiary data required for that rail | Which beneficiary fields are required |

| Cutoff behavior | Current cutoff rule pending provider or policy verification | Documented post-cutoff handling |

| Settlement window | Current settlement window pending provider verification | Verified expected movement window |

| Provider responses | Current return-code set pending provider verification | Likely exception labels |

| Authority | Named retry and escalation authority pending assignment | Who has retry authority |

Use the table as your operator checklist for each row.

Keep checkout and payout on separate launch tracks. A market may support customer charging while payout setup, timing behavior, and exception handling are still incomplete.

If Europe is in scope, tie your SEPA row to the same VAT operating record your payments and finance teams use. Under EU OSS, a business registers in one Member State of identification for declaration and payment of VAT under the relevant scheme. OSS includes non-Union, Union, and import schemes, and participation is optional. If you choose a scheme, all supplies in that scheme must be declared through OSS returns, and OSS returns do not replace domestic VAT returns. Plan VAT operations with scheme cadence in mind: quarterly returns for non-Union and Union schemes, and monthly returns for the import scheme. OSS operations also cover record keeping, audits, and exit handling, and marketplace/platform record-keeping duties can still apply even when the platform is not treated as a deemed supplier. For Europe-specific implementation detail, see VAT and SEPA: How European Platforms Combine Tax Compliance with Automated Euro Payouts.

Verification point: Someone outside implementation should be able to answer, from the matrix alone, which rail is used and which beneficiary fields are required. They should also be able to explain the documented post-cutoff handling, verified expected movement window, likely exception labels, and who has retry authority.

Tighten exception labels before the first live transfer#

Keep the failure-state table, but define a primary retry path, one owner, and one evidence set for each internal label. The goal is operational clarity, not a mirror of provider taxonomy.

| Failure state | Primary retry path to define in policy | One owner to assign in policy | Required evidence set |

|---|---|---|---|

| Rejected beneficiary | Correct beneficiary data, keep same case, resubmit only after review | Named payments or compliance owner pending assignment | request ID, beneficiary version, provider response, reviewer action, final disposition |

| Returned transfer | Review original transfer result first, then decide reissue or hold | Named operations owner pending assignment | original payout reference, return message or code, beneficiary version, reviewer action, final disposition |

| Stale quote if FX applies | Refresh quote under current controls, then resubmit or cancel | Named treasury or payments owner pending assignment | quote timestamp, provider reference, amount, reviewer action, final disposition |

| Duplicate request blocked by idempotency control | Do not resend blindly; confirm whether the original request progressed | Named engineering or payments owner pending assignment | idempotency key, request ID, provider response, reviewer action, final disposition |

Store the beneficiary version that was active at submission time, not just the latest profile state. Also store the provider response exactly as returned, including code or free-text message, even if your UI shows a simplified label.

Prove payout readiness with one success and one controlled exception#

Before launch, run a proof-of-readiness test in at least one real launch market: one successful path and one controlled exception path. Both should end with a complete case record.

For the success path, confirm that required beneficiary data is captured, the payout request is created, the provider reference is stored, status changes are visible to ops, and the final outcome is traceable to the payee. For the exception path, use a controlled, provider-approved test condition so your team sees the exact response, review step, and retry rule without exposing live funds.

If support can see the booking and charge but cannot identify the payout case, beneficiary version, or reviewer decision tied to the provider response, pause launch.

Verification point: Launch only when both paths produce a stored reference, visible case owner, and final disposition that can be explained without inbox archaeology.

Choose singles or batches based on control visibility#

In new markets, start with single payouts when you still need clean traceability and visible approvals. Use batches only when line-level outcomes stay clear after submission. Throughput alone is not enough.

Move to batches when finance and risk can quickly answer who was included, who approved release, which lines succeeded or failed, and whether one failed line can be retried without obscuring the rest. If not, stay on singles or tightly reviewed micro-batches. For a related payout-ops pattern at scale, see How EdTech Platforms Pay Instructors Globally: Compensation Models, Payout Controls, and Reconciliation.

If your EU launch still has unresolved VAT treatment questions about platform role, pause payout rollout until tax provides a documented position. The EU VAT Cross Border Rulings mechanism exists for complex cross-border VAT transactions, and requests are filed in a participating EU country where the taxable person is VAT-registered at the time of filing. It does not define payout cutoff behavior, but it can help you avoid scaling a market with unresolved VAT positioning.

Build reconciliation and audit evidence into daily operations#

Reconciliation has to be designed into daily operations, not patched in at month end. Set one non-negotiable standard: one payout lifecycle, one traceable record chain, and one accountable owner for every unresolved break. If finance, ops, and support cannot all follow that same chain from release to final outcome, you are not close-ready.

Before you start#

Daily reconciliation gets much easier when three basics already exist: an internal ledger record for each payout event, the provider response stored as received, and named ownership for unmatched items. Checkout or booking tools can help centralize charging and scheduling, but they do not automatically create payout-grade reconciliation on their own. For a parallel control pattern, see How EdTech Platforms Pay Instructors Globally: Compensation Models, Payout Controls, and Reconciliation.

Capture each payout event when it happens#

Record each lifecycle event in your internal ledger as it happens, then link external references back to that record. Keep the lifecycle explicit for your team, for example: release created, provider acknowledged or rejected, return or reversal if applicable, then any adjustment linked to the original case.

Verification point: from one internal record, a non-engineer should be able to identify the core case references, current status, and next owner. If that still requires inbox or raw-log digging, the evidence chain is weak.

Match across systems before breaks age into close problems#

Match across systems every day. At a minimum, match internal ledger records against provider outputs and against accounting handoff outputs.

Focus pre-close work on common traceability breakpoints, such as field-mapping drift, adjustments posted without original payout references, and duplicate external provider references across multiple internal records. Work three buckets daily: unmatched internal items, unmatched provider items, and non-unique external references. Each item needs one owner and a dated resolution note before close-readiness signoff.

Triage exceptions and sign off close readiness#

Treat unresolved mismatches as incidents with single-threaded ownership through final disposition. No break should move into close without a complete reference chain and supporting evidence.

Keep tax reporting boundaries clear. Form 8938 is used to report specified foreign financial assets and must be attached to an annual tax return, or an amended return. It is not filed by itself.

Form 8938 and FinCEN Form 114 (FBAR) are separate requirements, and filers may need one or both. The IRS comparison table is the right checkpoint.

Failure to report foreign financial assets on Form 8938 may result in a $10,000 penalty, with additional penalties up to $50,000 for continued failure after IRS notification, plus a 40 percent substantial understatement penalty.

Also avoid using one universal threshold. IRS notes a general $50,000 point in some cases, with higher thresholds possible, and specified domestic entities have separate $50,000 and $75,000 tests. For the related documentation branch, see FATCA and W-8 Tax Compliance for Platforms: How to Avoid Withholding on Foreign Payouts.

Final verification point: every payout event is matched or explicitly queued, every break has one owner, and no manual adjustment hides a missing reference chain.

Avoid the rollout mistakes that sink pet-service expansions#

A common rollout mistake is getting the sequence wrong, even when demand looks strong.

The first miss is choosing markets before operating checks are ready. Demand can look strong while basics like scheduling, client and pet profiles, and reminder coverage are still inconsistent. That pushes avoidable problems into live operations.

The second is treating booking capability as the whole operating model. Pet-sitting tools can centralize bookings, client information, and day-to-day operations, but your team still needs clear processes for service notes and owner communication rather than relying on defaults.

A third mistake is scaling while failure-prevention signals are still unstable. If automated reminders are not reliably reducing no-shows, or GPS and service-note visibility is inconsistent, pause expansion and tighten execution before you add volume.

Finally, do not leave risk monitoring for later. Compare user reviews in current software tables, confirm your shortlist is based on recently updated information, and treat customer-concentration disclosures as an added warning signal where that reporting exists.

Related reading: Pay Translators and Interpreters Globally for Language Services Platforms.

You might also find this useful: How Home Services Platforms Verify, Dispatch, and Pay Contractors.

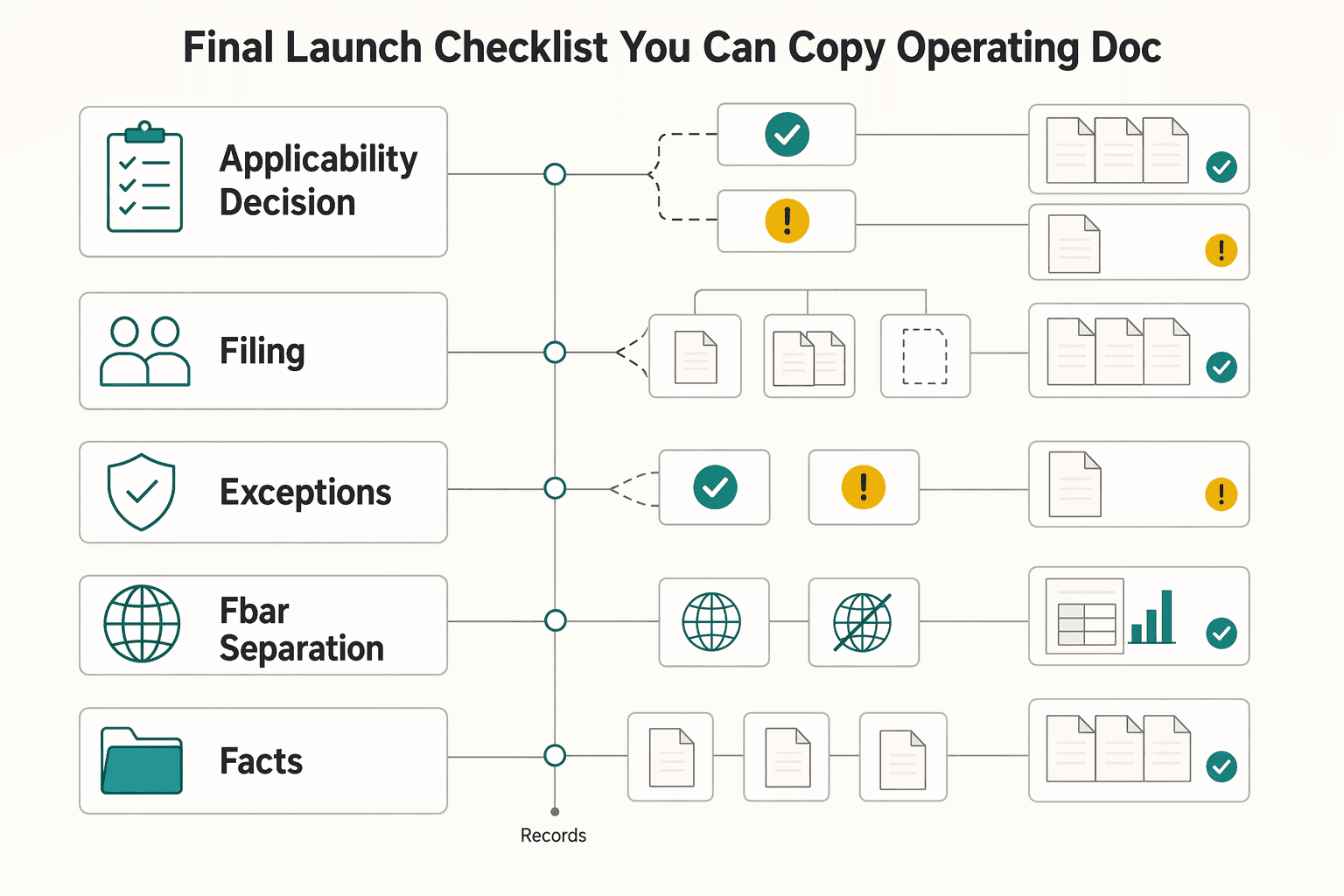

Final launch checklist you can copy into your operating doc#

Use this as a documentation checkpoint only. It confirms your Form 8938 branch decision and evidence, not full payout launch approval. Before go-live, your checklist should capture four things: whether this branch applies, who reviewed it, what evidence they used, and whether the outcome is Form 8938, FBAR, both, or neither.

- Record an explicit applicability decision before any provider payout goes live.

Form 8938 branch applies to this provider population, or *Form 8938 branch does not apply based on reviewed facts.

For that decision, document filer type, whether an income tax return is required for the year, the asset or account inventory reviewed, and whether current Form 8938 instruction exceptions were checked. Also record the source version date used, for example, an IRS Form 8938 page excerpt showing "None at this time" with a page review date of 31-Mar-2026.

- Use this checklist table and require an owner, evidence source, and review status on every row.

| Case | What to verify | Evidence owner | Evidence source | Review status |

|---|---|---|---|---|

| Applicability decision | Does the Form 8938 branch apply to this provider mix before go-live? | Owner pending assignment | Current IRS Form 8938 page and instructions | Not started / In review / Approved / Not applicable |

| Return filing status check | Is the relevant U.S. taxpayer required to file an income tax return for the year? If not, note that Form 8938 is not required for that year. | Owner pending assignment | Reviewed tax filing context and Form 8938 guidance | Not started / In review / Approved / Not applicable |

| Threshold and exception check | Current threshold pending official or advisor verification. Confirm whether any instruction-based exception applies. | Owner pending assignment | Current Form 8938 instructions | Not started / In review / Approved / Not applicable |

| FBAR separation check | Document whether FinCEN Form 114 may also apply. Do not treat Form 8938 as a substitute. | Owner pending assignment | IRS comparison guidance and current instructions | Not started / In review / Approved / Not applicable |

| Filing artifact check | If Form 8938 is required, confirm it is attached to the annual return or amended return, not handled as a standalone filing. | Owner pending assignment | Return preparation evidence or filing confirmation | Not started / In review / Approved / Not applicable |

Keep the threshold row unresolved until the current rule is verified. IRS gives a general reportability reference above $50,000, but thresholds can vary. The instructions also include separate specified domestic entity triggers such as $50,000 on the last day of the tax year or $75,000 at any time during the tax year. Do not hardcode one universal value.

- Keep this branch separate from other tax workflows.

Form 8938 review is not a substitute for your broader tax-routing work. If your FATCA or W-8 path is unresolved, route it separately using FATCA and W-8 Tax Compliance for Platforms: How to Avoid Withholding on Foreign Payouts.

- Mark non-tax controls as out of scope in the same launch document.

This checklist does not validate KYC or KYB, sanctions screening, AML monitoring, payout rail readiness, or reconciliation controls. If sanctions logic is open, route that work to OFAC Compliance for Payment Platforms: How to Screen Every Payout Against the Sanctions List.

- Require a final one-line reviewer decision and store the evidence pack.

The reviewer should record: Form 8938 required, FBAR required, both may apply, or neither applies based on reviewed facts. Store reviewer name, review date, and source version date with the evidence.

Two bright-line checks should stay explicit. If Form 8938 is required, it must be attached to an annual or amended return. If a U.S. taxpayer is not required to file an income tax return for the year, Form 8938 is not required for that year. If your record does not show who made the decision, which threshold version they used, and whether FBAR was reviewed separately, delay go-live until the checkpoint is complete.

Related reading: How Logistics and Freight Platforms Pay Carriers and Owner-Operators at Scale.

If your checklist is complete and you need to confirm market/program payout coverage before go-live, talk to Gruv.

Frequently Asked Questions

Should Form 8938 be a hard gate before any provider payout goes live?

No, not by itself. Form 8938 is attached to an annual tax return, or an amended return. If a taxpayer does not have to file an income tax return, Form 8938 is not filed regardless of foreign asset value. The release gate should be a documented decision on whether Form 8938, FBAR, both, or neither may apply for the account setup.

Can we set one Form 8938 threshold in product logic for every payee?

No. IRS guidance gives a general reportability reference above $50,000, but thresholds can be higher depending on filer context. Keep any live threshold value pending official or advisor verification rather than treating the general reference point as universal. Filer-specific cases can differ, including specified domestic entity thresholds.

Do Form 8938 and FBAR overlap, or does one replace the other?

They can overlap, and one does not replace the other. Filing Form 8938 does not remove a possible FBAR obligation, and separate penalties may apply for failure to file each form. Before release, record who checked the IRS comparison path and what conclusion they reached.

What should we do if worker classification or W-8/W-9 collection is still unresolved?

Treat this as a separate decision track. This section does not define worker-classification tests or exact W-8/W-9 routing rules, so do not infer them from Form 8938 materials alone. Use a dedicated review path for that tax-form branch, along with the companion guide on FATCA and W-8 Tax Compliance for Platforms: How to Avoid Withholding on Foreign Payouts.

What is the minimum evidence pack for a defensible Form 8938 decision?

Record the filer type, the account or asset inventory reviewed, the threshold version used, the review date, and the final decision: Form 8938, FBAR, both, or neither. If Form 8938 is required, note that it must be attached to an annual or amended return and not filed standalone. Keep the source version date you relied on as part of the audit trail.

How much penalty exposure is enough to justify a stricter review?

Treat this as pre-launch control work, not post-launch cleanup. IRS materials note a $10,000 failure-to-report penalty, potential additional penalties up to $50,000 for continued failure after IRS notification, and a 40 percent substantial understatement penalty tied to non-disclosed foreign financial assets. If you cannot show who made the threshold decision and on what facts, treat that as an unresolved compliance risk.

Does Form 8938 guidance answer sanctions screening, OFAC checks, or EU VAT and SEPA design?

No. Form 8938 and FBAR materials do not define sanctions screening logic, AML sequencing, VAT handling, or SEPA operating design. Use the companion articles on OFAC Compliance for Payment Platforms: How to Screen Every Payout Against the Sanctions List. For VAT and payout-rail design, use VAT and SEPA: How European Platforms Combine Tax Compliance with Automated Euro Payouts.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- cumingcountyne.gov/wp-content/uploads/2021/06/2-Zoning-Regulati...trusted

- irs.gov/businesses/corporations/fatca-information-fo...trusted

- irs.gov/forms-pubs/about-form-8938trusted

- sec.gov/Archives/edgar/data/1842356/0001842356250000...trusted

- sec.gov/Archives/edgar/data/1766502/0001193125191633...trusted

- sos.ms.gov/ACProposed/00012691B.pdftrusted

- taxation-customs.ec.europa.eu/archives/taxable-persons/vat-cross-border-ru...trusted

- tile.loc.gov/storage-services/service/gdc/lhbum/08574/085...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

FATCA and W-8 Tax Compliance for Platforms: When to Release, Hold, or Withhold Foreign Payouts

---

OFAC Compliance for Payment Platforms: How to Screen Every Payout Against the Sanctions List

Sanctions control in payouts is a release decision, not a search-box task. If your platform moves funds quickly, you need a defensible way to stop, review, and document risky payouts before money leaves your control.

VAT and SEPA: How European Platforms Combine Tax Compliance with Automated Euro Payouts

The hard part is not VAT on one side and SEPA on the other. It is keeping tax treatment, beneficiary checks, and euro payout execution aligned when your platform pays across multiple European markets at speed.