Quick Answer

Platforms should choose payout methods by recipient fit, failure recovery, compliance alignment, operational burden, and future flexibility, not just by which rail is easiest to integrate. In practice, bank payouts, wallet payouts, cash pickup, stablecoin payouts where allowed, and Employer of Record routing fit different cases, so most teams need a layered setup, clear evidence and reconciliation, and a phased launch.

Why this guide exists and who should use it#

If your team needs to send money to contractors, creators, freelancers, marketplace sellers, or other non-payroll recipients across borders, the payout decision can look deceptively simple at first. On paper, you are choosing a payment rail. In practice, you are choosing an operating model that affects onboarding, compliance, support load, engineering effort, treasury visibility, failure recovery, and the degree of legal risk your company is willing to carry.

This guide is for platform teams that need practical platform strategies for paying unbanked contractors in developing markets before they hard-code the wrong assumptions into product and operations. It is especially useful if you are in one of these situations:

- You are launching payouts for the first time and want to avoid rebuilding your stack after the first few markets.

- You already support one payout method but are seeing failed transfers, support tickets, or delays that point to deeper design issues.

- You are expanding into new jurisdictions and need a clearer way to separate payment mechanics from worker-classification risk and compliance risk.

- You are deciding whether one provider is enough or whether you need a broader architecture.

- You need a decision framework that product, finance, legal, operations, and engineering can all use without talking past each other.

A common mistake is treating payout choice as a narrow vendor selection exercise. That tends to push teams toward whichever option is easiest to demo, easiest to explain internally, or fastest to integrate in a single market. The result is often a system that works for a small subset of users and becomes fragile as soon as payment preferences, regulatory requirements, or business models vary by country.

A better approach is to start from the real-world job the payout system has to do. That job usually includes more than moving funds. It may also include:

- collecting recipient details in a usable format

- validating those details before money is sent

- handling corrections and retries

- producing records that finance and compliance teams can rely on

- giving recipients clarity on status, timing, and fees

- preserving options when a direct contractor payout model becomes risky

This guide is written for decision-makers who need to keep that broader picture in view. It does not assume that every recipient should be paid the same way. It also does not assume that the technically simplest path is the safest one for the company.

The core idea is straightforward: choose payout options based on the work they need to do in your operating model, not just on the existence of an API. That means understanding where each method fits, what it demands from recipients, how it fails, what evidence it produces, and when it should not be your default.

The sections that follow move from framework to options to execution. First, we cover the criteria that separate workable choices from expensive mistakes. Then we compare the main payout types. After that, we look at architecture, compliance, and phased launch planning. The last sections answer common questions and pull the decision into a practical takeaway for teams making the call now. Related reading: How Platforms Build Multi-Currency Sub-Wallets for Contractors.

Selection criteria for paying unbanked contractors in developing markets#

Before you compare payout methods, decide which criteria actually matter. Otherwise, teams tend to optimize for whichever feature is easiest to measure early, such as raw delivery speed or implementation effort, while underweighting the factors that drive cost and risk later. The most useful criteria fall into a few groups.

| Criterion | What to assess | Why it matters |

|---|---|---|

| Recipient fit | What details the recipient needs to provide; how familiar the method is; whether it is available where the recipient lives | A payout option is only viable if recipients can actually use it with minimal friction |

| Geographic coverage and local usability | Whether the payout route is local-feeling and practical for that recipient population | Coverage is not the same as real usability |

| Cost structure and who absorbs it | Provider fees; currency conversion effects; failed payout handling; support time; reconciliation effort; engineering maintenance; exception management; compliance operations | Direct transfer cost can differ sharply from operational cost once failures and manual review are considered |

| Speed and predictability | When funds will arrive; settlement, cash movement, and issue resolution | Predictable is often more useful than simply being fastest |

| Failure modes and recoverability | What usually causes failure; whether errors can be caught before funds are sent; whether the payout can be reversed or amended | Teams should compare what happens when data is wrong, the account is inactive, or more evidence is required |

| Compliance alignment | Required recipient checks; status and event history; additional review or escalation work; whether the payment model matches the legal reality of the relationship | Payout design shapes what information you collect, what you can verify, and what records you retain |

| Product and engineering complexity | Onboarding UI requirements; validation logic; country-level branching; webhook and event handling; reconciliation inputs; payout retry logic; reporting needs; support tooling | Early simplicity can hide later branching logic |

| Treasury, controls, and reporting | What was funded, sent, returned, pending, or adjusted | If the payout method makes these tasks harder, the burden shows up later as close delays, exception queues, and manual spreadsheet work |

| Strategic flexibility | Whether it will be hard to add methods, reroute by jurisdiction, or split contractor flows from higher-risk engagements later | Avoid design decisions that make future options harder |

Recipient fit#

A payout option is only viable if recipients can actually use it with minimal friction in the markets and channels where you plan to offer it. Ask:

- What details does the recipient need to provide?

- How familiar is the method to the recipient?

- Is the method available where the recipient lives?

- Does the recipient need a bank account, wallet account, or local pickup access?

- How easy is it for the recipient to correct mistakes?

Teams often overestimate recipient willingness to complete extra steps. A payout method can look efficient internally and still fail in practice if recipients struggle to register, verify, or maintain the destination account.

Geographic coverage and local usability#

Coverage is not the same as real usability. A provider may list a country, but the relevant question is whether the payout method works in the way your recipients expect. You need to know whether the payout route feels local and practical for that recipient population, or whether it technically exists but creates confusion and support issues.

This matters because a payout method that works cleanly in one region may be weak in another. Some methods depend on banking access and standardized account information. Others depend on established wallet behavior. Others are useful mostly where cash access remains important.

Cost structure and who absorbs it#

Do not evaluate cost only at the transaction layer or only by provider pricing. The meaningful cost picture includes:

- provider fees

- currency conversion effects

- failed payout handling

- support time

- reconciliation effort

- engineering maintenance

- exception management

- compliance operations

Two options with similar direct transfer cost can have very different operational cost once failures and manual review are considered. Likewise, an option that appears cheap can become expensive if it shifts too much confusion or uncertainty onto recipients.

Speed and predictability#

Fast is useful. Predictable is often more useful. Recipients usually care about knowing when funds will arrive and what they need to do if something goes wrong. Internal teams care about being able to forecast settlement, cash movement, and issue resolution.

A payout option that is not always the fastest can still be the better operational choice if it is more consistent, easier to trace, and easier to support.

Failure modes and recoverability#

Every payout method fails differently, so that should be part of your selection criteria from the start. Ask:

- What usually causes failure?

- Can errors be caught before funds are sent?

- Can the payout be reversed or amended?

- How visible is the payout status to your team?

- What does recipient support need to know to resolve issues?

This is where many expensive mistakes begin. Teams compare methods based on successful payouts, but not on what happens when the data is wrong, the account is inactive, the recipient cannot access funds, or the provider requires more evidence.

Compliance alignment#

Payout design is not separate from compliance. It shapes what information you collect, what you can verify, what records you retain, and how easily you can demonstrate control. Even when the payout itself is operationally smooth, the surrounding compliance burden may make it a poor fit if it leaves gaps in onboarding, monitoring, or audit evidence. Assess whether:

- the payout flow supports your required recipient checks

- status and event history are available in a way your teams can use

- the method creates additional review or escalation work

- the payment model matches the legal reality of the relationship

That last point becomes especially important when contractor payouts begin to look risky and an Employer of Record route needs to be considered instead.

Product and engineering complexity#

A method that looks attractive on a spreadsheet may still be expensive to maintain. Consider:

- onboarding UI requirements

- validation logic

- country-level branching

- webhook and event handling

- reconciliation inputs

- payout retry logic

- reporting needs

- support tooling

This is one reason you should avoid letting a single successful pilot determine the long-term architecture. Early simplicity can hide later branching logic.

Treasury, controls, and reporting#

Finance teams need more than a transfer confirmation. They need clarity on what was funded, sent, returned, pending, or adjusted. They need enough detail to reconcile balances and explain differences. If the payout method makes those tasks harder, the burden shows up later as close delays, exception queues, and manual spreadsheet work.

Strategic flexibility#

A payout choice should preserve future options where possible. That does not mean overbuilding on day one. It means avoiding design decisions that make it hard to add methods, reroute by jurisdiction, or split contractor flows from higher-risk engagements later.

When you use these criteria together, a more disciplined picture emerges. The right payout option is usually not the one that wins every category. It is the one that fits the recipient, supports the business model, can be controlled operationally, and does not force hidden risk onto legal, finance, or support teams.

Compare the main payout options for paying unbanked contractors#

Before building a full integration, compare the main payout categories side by side using the criteria above. This is the stage where teams should challenge assumptions and decide what each method is for. The practical question is which method should be primary, which should be secondary, and which should be reserved for edge cases or risk transitions.

| Method | Where it fits | Key note |

|---|---|---|

| Bank payout | Strong default where recipients already expect bank settlement and can provide reliable account details | In some programs, bank payouts should be primary |

| Wallet payout | Better where mobile financial behavior is common and recipients want simpler access to funds | In others, wallets should be primary and bank payouts should be available for users who prefer them |

| Cash pickup | Useful when digital account access is limited or inconsistent | Often strongest as a fallback or targeted method rather than a universal default |

| Stablecoin wallet payout | Specific situations where it is allowed and operationally suitable | Changes the support and compliance profile and should not be treated as a simple substitute for conventional methods |

| Employer of Record route | Certain engagements when direct contractor payouts are no longer the prudent path | Not just another rail; it changes the engagement structure |

Use case fit matters more than abstract preference. Bank payouts can be a strong default where recipients already expect bank settlement and can provide reliable account details. Wallet payouts may be better where mobile financial behavior is common and recipients want simpler access to funds. Cash pickup can be useful when digital account access is limited or inconsistent. Stablecoin may appeal in specific situations where it is allowed and operationally suitable, but it also changes the support and compliance profile. An Employer of Record route is not just another rail. It changes the engagement structure when direct contractor payouts are no longer the prudent path.

Think in layers, not winners. For most platforms, the practical design is layered:

- a primary method for the majority of recipients

- one or more fallback methods for specific regions or user groups

- a separate route for engagements that should not stay in direct contractor payout flows

This layered approach prevents the common failure of trying to force one payout type to solve every case.

Compare methods by what they ask of the recipient. One of the cleanest ways to compare methods early is to focus on the recipient experience:

- How much information must the recipient provide?

- How easy is it to understand the destination details?

- How much trust does the method require from the recipient?

- How much effort does it take to access funds?

- How likely is the recipient to contact support?

This helps teams avoid designing from the provider's perspective alone.

Compare methods by operational burden. You should also compare each option by what it demands from your internal teams. For example:

- Does onboarding require country-specific forms?

- Is validation straightforward or highly variable?

- Do failures create recoverable workflows?

- Can support diagnose issues without escalating every case?

- Can finance reconcile the data without building custom workarounds?

A method that is slightly harder to integrate initially may still be the better choice if it reduces manual operations over time.

Compare methods by risk boundaries. Some payout options are mainly a question of payment execution. Others affect the relationship model itself. That is why it is important not to treat an Employer of Record route as equivalent to a wallet or bank rail. It belongs in the comparison because it may be the correct answer for certain engagements, but it solves a different problem.

A practical way to decide. Before engineering starts, align on these questions:

- Which payout method is the default for your lowest-friction, lowest-risk cases?

- Which recipient groups need alternatives from the beginning?

- Which jurisdictions or engagement types should trigger additional review?

- What evidence must each method generate for operations, finance, and compliance?

- What would make you reroute a recipient from one method to another?

If you cannot answer those questions yet, you are probably not ready to commit to a full build. The cost of waiting a bit longer at this stage is usually lower than the cost of redesigning payout logic after launch. For a step-by-step walkthrough, see How to Build a Currency Reserve Strategy for Marketplace Platforms Operating in Volatile Markets. Before you shortlist rails, run your expected corridors, payout methods, and failure-retry assumptions through this payment fee comparison tool to pressure-test total cost and recoverability.

Direct bank account payouts and wallet routes for unbanked contractors#

Direct bank account payouts and mobile or digital wallet payouts are often the first methods platform teams evaluate. Each can serve as a mainstream path for large recipient groups. They are not interchangeable, and the difference matters.

Direct bank account payouts#

Direct bank account payouts are often attractive because they feel familiar, formal, and well-suited to recurring payments. They can align well with recipients who already manage income through a bank account and expect settlement there.

They also tend to appeal internally because they seem orderly: recipient details are collected, funds are routed, and payment records can fit cleanly into finance workflows. In the right context, that can be true. But bank payouts work well only when the underlying assumptions hold.

A strong bank payout setup usually depends on a few things:

- recipients can provide accurate account details

- those details can be validated before funds move

- the destination account is usable for the intended transfer

- recipients understand how the payment will appear and when

- support can trace failures or returns clearly

Where those assumptions break down, bank payouts become operationally heavy. The common pain points are not just transfer failures. They also include onboarding confusion, recipient mistrust when details feel formal or unfamiliar, and long issue resolution cycles when a payment is delayed or returned.

Bank payouts are often a sensible default when you need:

- a standard method for business-like recurring payouts

- strong alignment with finance and reconciliation processes

- a payout destination recipients are already accustomed to using

- a method that does not require recipients to adopt a new wallet environment

They are less attractive when your audience has inconsistent banking access, struggles to provide the right account information, or prefers a more mobile-first experience.

To make bank payouts workable, you need to design for data quality from the beginning. That means not only collecting destination details, but also giving recipients enough context to enter them correctly, edit them safely, and understand what happens if something changes. Operationally, bank payouts benefit from strong pre-send validation, clear status reporting, and well-defined exception handling. If you rely on manual support to fix most issues after the payment is already in motion, you will likely feel the cost quickly.

Mobile and digital wallet payouts#

Mobile and digital wallet payouts can reduce friction where recipients are already comfortable receiving and using funds through wallet systems. They may feel more accessible than bank transfers, especially for recipients who manage more of their financial activity through a phone than through a traditional bank account interface.

The appeal of wallet payouts often comes from user experience:

- the destination may be easier for recipients to recognize

- onboarding may feel lighter or more familiar

- recipients may access funds more directly

- the method may match local payment behavior more closely

That does not automatically make wallets easier for your platform. Wallet payouts can simplify recipient experience while creating different operational dependencies. You still need to manage destination accuracy, account readiness, provider status visibility, and support playbooks for cases where the wallet is limited, inaccessible, or not properly configured for the payout.

Wallet payouts are often useful when you need:

- a recipient-friendly alternative to bank detail collection

- a mobile-first payout experience

- a method better aligned with how recipients already receive and use funds

- broader practical usability in places where bank access is not the best assumption

But wallet payouts also require discipline. Teams sometimes treat them as a lighter-weight shortcut and underbuild controls around them. That can lead to preventable confusion around recipient identity, destination changes, failed deliveries, or missing status detail.

Choosing between the two#

The right comparison is not bank versus wallet in the abstract. It is this:

- Which method is more natural for your recipient base?

- Which method creates fewer avoidable errors in onboarding?

- Which method gives your operations team more control over failures?

- Which method produces the records your finance and compliance teams need?

- Which method can scale without a large support burden?

In some programs, bank payouts should be primary and wallets should be optional. In others, wallets should be primary and bank payouts should be available for users who prefer them. In still others, both should exist from the start, with eligibility or preference determined by jurisdiction, recipient type, or product segment.

The mistake to avoid is choosing one purely because it seems more universal. Universal in theory is not the same as effective in your actual payout population. Related: Global Payouts and Emerging Markets: 5 Regions Every Platform Should Prioritize.

Cash pickup and stablecoin routes for unbanked contractors in developing markets#

Cash pickup partner payouts and stablecoin wallet payouts sit further from the default choices many teams begin with, but both can matter in the right context. They solve very different problems and should be assessed with care.

Cash pickup partner payouts#

Cash pickup partner payouts can be useful when recipients need physical access to funds or when digital destination coverage is not sufficient for the user group you are serving. They are especially relevant when a platform cannot assume that every recipient has reliable access to a usable bank or wallet destination.

The biggest advantage of cash pickup is straightforward: it can extend reach where account-based methods are not practical for everyone. That makes it a valuable option in some programs, especially as a fallback or targeted method rather than a universal default.

But the operational tradeoffs are substantial. Cash pickup adds complexity around:

- recipient expectations and instructions

- pickup readiness and identity matching

- support for missed or disputed pickups

- country- and partner-specific operational rules

- exception handling when a payout is not collected as expected

This is why cash pickup is usually strongest when used intentionally, not casually. It should exist because you have a clear recipient need for it, not because you want to say you cover every edge case.

From a product perspective, cash pickup requires very clear communication. Recipients need to know what to do, what details matter, and how to resolve problems. If your support team cannot confidently guide users through the process, cash pickup can become one of the more labor-intensive methods in your stack.

Cash pickup can be a strong fit when:

- digital destinations are not consistently practical

- recipients clearly value physical access to funds

- the business case justifies the extra support and operational work

- you can maintain reliable partner coordination and recipient communications

It is a weaker fit when your recipients already expect direct digital access to funds and would see pickup as slower, less convenient, or harder to trust.

Stablecoin wallet payouts where allowed#

Stablecoin wallet payouts attract interest because they can appear to offer a distinct model for moving value to recipients. For some platforms and recipients, they may be worth evaluating. But they should never be treated as a simple substitute for more conventional payout methods without careful review.

Even before you consider recipient demand, the first gating question is embedded in the section title itself: where allowed. If the method is not permitted or is not operationally appropriate in a given context, it should not be part of the payout design there. This is one reason teams need a jurisdiction-aware framework rather than a single global answer.

Where stablecoin payouts are allowed and under consideration, the practical questions become:

- Do recipients actually want to be paid this way?

- Can recipients securely receive and use funds through a wallet?

- Can your support team help with errors, access issues, and destination mistakes?

- Can your compliance and finance teams handle the evidence, controls, and reporting implications?

- Does the method fit your business model, or are you using it to work around a deeper problem?

That last question matters. Stablecoin should not be used as an escape hatch from recipient verification, payout controls, or engagement risk. If the underlying contractor model is itself under strain, changing the rail does not solve the structural issue.

Stablecoin payouts may be worth considering when:

- there is a clear recipient use case

- the jurisdictions involved support the approach

- your teams can manage the operational and compliance consequences

- the method is part of a deliberate payout policy, not an improvised workaround

They are a weaker choice when recipient understanding is low, support readiness is weak, or internal teams do not have confidence in how the method will be monitored and documented.

Choosing between cash pickup and stablecoin#

Although both can look like alternatives to bank and wallet payouts, they serve different recipient realities. Cash pickup is about physical access and reach. Stablecoin is about wallet-based receipt under a different operational model. They should not be grouped together as niche methods and left at that. Each needs its own acceptance criteria, support design, and escalation policy.

For many platforms, the practical answer is not to make either one a default. Instead, evaluate whether either one solves a clearly defined problem that your primary methods cannot handle well. If you want a deeper dive, read Cash Pickup Payouts: How to Reach Unbanked Contractors in Cash-Preferred Markets.

Employer of Record routing when paying unbanked contractors becomes risky#

At some point, the payout conversation stops being only about payout mechanics. This happens when the issue is no longer how to pay someone, but whether the company should continue paying them through a direct contractor model at all. That is where Employer of Record routing comes in.

An Employer of Record route should not be viewed as just another payout option beside bank transfer or wallet disbursement. It is a different operating path for engagements that create enough risk that direct contractor payouts are no longer the prudent choice. It is about who should sit in the employment or engagement structure, not just about where funds land.

This distinction matters because teams sometimes try to solve a structural risk problem with a payment solution. For example, they may keep adjusting the payout rail while ignoring signals that the relationship itself deserves re-evaluation. That usually leads to a false sense of progress. The payments may move, but the underlying exposure remains.

When this route becomes relevant#

Employer of Record routing becomes relevant when your review of a contractor engagement raises concerns that make direct payout less comfortable from a risk perspective. Those concerns might emerge through onboarding, legal review, ongoing operations, or expansion into new jurisdictions.

The guide's key point is not to guess at a universal trigger. It is to recognize that a platform needs a clean escalation path when direct contractor payouts become risky. Without that path, teams are left improvising case by case, and decisions become inconsistent.

Why routing matters operationally#

Even if legal or compliance teams identify the need for a different engagement structure, the operational handoff often breaks down unless the payout architecture has already accounted for it. Product teams may still treat the worker as if they belong in the same contractor flow. If you are paying unbanked contractors in developing markets, your platform strategy has to account for that routing before the handoff breaks.

A well-designed routing model separates two questions:

- Can this person be paid as a direct contractor through the payout methods in our standard stack?

- If not, what is the alternate route, and how does the system reflect that change?

This separation helps avoid a common failure mode: leaving a risky engagement in the ordinary contractor pipeline because there is no clean operational alternative.

What platform teams need to design for#

If your program may require Employer of Record routing, plan for that early. That means thinking through:

- how cases are flagged

- who decides that direct contractor payout is no longer appropriate

- how the recipient experience changes

- how records are maintained across the transition

- how finance, operations, legal, and support stay aligned

The goal is not to route people unnecessarily. The goal is to avoid a system in which the only available action is to keep paying through a model the company no longer feels comfortable defending.

Why this belongs in the payout guide#

Some teams resist including Employer of Record routing in payout planning because it does not look like a conventional payment method. But it belongs here because the payout system is where many structural issues surface first. If a platform only designs for direct contractor disbursement, then every problem gets forced back into that frame.

By acknowledging Employer of Record routing as part of the decision set, teams create room for a more responsible operating model. Not every engagement belongs in the same lane, and the payout architecture should reflect that reality.

One platform or multi-provider architecture for paying unbanked contractors#

Once you understand the payout methods you may need, the next decision is architectural: should you rely on one platform or assemble a multi-provider setup? There is no universal answer, but there is a disciplined way to think about the tradeoff.

Why one platform is attractive#

A single-platform approach is appealing for obvious reasons, especially early on:

- one integration path

- a simpler product surface

- fewer operational relationships

- less vendor management

- a cleaner story for internal stakeholders

For early-stage programs or narrower geographic footprints, this can be the right decision. Simplicity is not a flaw. If one platform truly supports your recipient needs, reporting requirements, and control expectations, staying focused can help you move faster and operate more consistently.

A single-platform setup also makes it easier to standardize:

- onboarding flows

- support scripts

- payout status handling

- reconciliation processes

- internal ownership

That consistency has real value because it reduces variation across teams as volume grows.

Where one platform becomes limiting#

The challenge appears when the platform's strengths are uneven across payout methods, jurisdictions, or recipient types. A provider may be strong for bank payouts, weaker for wallets, limited for cash access, or unsuitable for a route you need as your risk model evolves.

At that point, insisting on one platform can create hidden costs:

- forcing recipients into suboptimal methods

- building complex workarounds around provider gaps

- accepting weaker operational visibility in certain regions

- delaying expansion because the current stack cannot support it well

- carrying more concentration risk than your team is comfortable with

The danger is not only capability mismatch. It is also organizational inertia. Once one provider is embedded deeply, teams can become reluctant to add alternatives even when the business case is clear.

Why multi-provider architecture is attractive#

A multi-provider approach can give you:

- better fit across different payout methods

- more flexibility by jurisdiction

- stronger fallback options

- leverage when one route underperforms

- clearer separation between ordinary payouts and higher-risk routing decisions

This is often the more resilient model for platforms serving diverse recipient populations across multiple markets. But resilience comes with complexity. Multi-provider setups increase demands on:

- routing logic

- monitoring

- reconciliation

- support tooling

- reporting normalization

- vendor oversight

- internal governance

You do not want to add that complexity unless it solves a real problem.

A practical decision rule#

A good way to frame the choice is simple.

Use one platform if it can serve your priority payout methods and recipient groups without forcing major compromises in usability, control, or compliance.

Use a multi-provider architecture when those compromises become material enough that the added complexity is justified.

The key word is material. Do not split your stack just because alternatives exist. Split it when the difference affects recipient success, operational burden, risk posture, or business expansion in a meaningful way.

Build for optionality even if you start simple#

Even if you begin with one provider, it is wise to avoid product and engineering choices that make future expansion unnecessarily painful. That includes:

- keeping payout method abstractions clear

- separating recipient preference from provider implementation

- storing destination and status data in a structured way

- designing support tooling that can accommodate more than one route

- avoiding provider-specific assumptions in core product language where possible

This does not mean overengineering for a future that may not come. It means preserving enough flexibility that you are not trapped by early convenience. We covered this in detail in Crypto Payouts for Contractors: USDC vs. USDT - What Platforms Must Know.

Compliance and evidence you need before scaling#

Scaling payouts without scaling evidence is one of the fastest ways to create expensive internal friction. A system can appear operationally successful while still leaving legal, finance, compliance, and audit stakeholders without the records they need.

The question is not only whether payments go out. It is whether your organization can show what happened, why it happened, and how it was controlled.

Evidence starts with recipient onboarding#

Before payouts are sent, your system should collect and maintain the information required for the payout method and the engagement model. The exact details depend on your program, but the broader principle is constant: if onboarding quality is weak, downstream evidence quality will also be weak.

You should be able to show, in a usable way:

- what recipient details were collected

- when those details were provided or changed

- what payout method the recipient selected or was assigned

- whether any review or validation occurred

- how routing decisions were made for exceptions

This is not just for audits. It matters for support, finance, and dispute resolution too.

Keep a clear payout event trail#

As you scale, you need a reliable event history for each payout. That means being able to follow the payment through its lifecycle, including status changes, failures, returns, retries, and resolution steps.

A strong event trail helps different teams answer different questions:

- support can explain what happened to the recipient

- finance can reconcile and investigate differences

- compliance can review patterns and escalation decisions

- operations can improve failure handling over time

If your payout data is fragmented across provider dashboards, inboxes, and manual notes, you may still be able to operate at small scale. Under growth, though, that model tends to break.

Evidence is also about decision-making, not only transactions#

Teams often focus on proof that money moved. That is necessary but incomplete. You also need evidence around decisions, especially when cases do not follow the standard contractor path.

For example, if an engagement is routed away from direct contractor payout, your system should make that transition understandable internally. Not every detail belongs in the product layer, but the organization should not have to guess why a route changed.

The same principle applies to method selection. If certain payout methods are restricted, conditional, or secondary, those rules should exist in a durable form and be reflected in operations.

Design compliance into support workflows#

Support is often where compliance gaps become visible first. A recipient says funds did not arrive. Another says the destination account changed. Another wants to switch methods. Another disputes whether a payout was made correctly. If support teams do not have controlled workflows and reliable evidence, they may start resolving issues informally. That creates inconsistency and record gaps.

A scalable payout program gives support enough visibility to help, without relying on ad hoc fixes that bypass controls.

Reconciliation is part of control#

Compliance evidence and finance evidence overlap more than teams sometimes expect. If finance cannot consistently tie funding, disbursement, pending items, returns, and adjustments together, that is not merely a reporting inconvenience. It can also indicate weak control over the payout system.

This is why platform teams should involve finance early. The best time to define what records are needed is before you launch, not after exception volume grows.

What "ready to scale" should mean#

Before you scale a payout program meaningfully, you should be confident that you can answer these kinds of questions:

- Who was paid, through which method, and based on what destination details?

- What happened when payouts failed or were delayed?

- What changes were made to recipient payout information, and when?

- Which cases stayed in direct contractor flows, and which did not?

- Can finance reconcile activity without depending on fragile manual work?

- Can support and compliance review issues using the same underlying record?

If the answer to those questions depends on stitching together multiple tools and institutional memory, the program is not as scalable as it looks.

Launch in three phases without losing control#

A phased launch is not just a safer way to ship. It is the best way to learn which parts of the payout design are actually durable before volume and jurisdictional complexity make changes harder.

| Phase | Usually includes | What to confirm |

|---|---|---|

| Phase one | A limited set of recipient types; a limited set of jurisdictions; one primary payout method; tightly defined internal ownership; clear exception handling | Whether recipients can complete onboarding without confusion; whether destination data quality is strong enough; whether status updates are usable; whether finance can reconcile the flow; whether support can resolve common issues |

| Phase two | Another payout method; another region; another recipient segment; more automation in routing and status handling | Comparing failure patterns across methods; refining routing logic; improving recipient communications; tightening support escalation paths; confirming that internal reporting still holds together |

| Phase three | Clear ownership across product, operations, legal, finance, and support; documented routing rules; repeatable evidence collection; stable reconciliation and reporting; escalation paths for higher-risk engagements; a defined approach to adding or changing providers | Whether the program can keep expanding without becoming dependent on tribal knowledge, heroics, or inconsistent exceptions |

The point of phasing is not to move slowly for its own sake. It is to sequence risk so that you can improve the system before each new layer of complexity arrives.

Phase one proves the core path#

Start with the narrowest version of the payout program that still reflects the real business need. That usually means:

- a limited set of recipient types

- a limited set of jurisdictions

- one primary payout method

- tightly defined internal ownership

- clear exception handling

The purpose of this phase is to test the end-to-end operating model, not merely the API connection. You want to learn:

- whether recipients can complete onboarding without confusion

- whether destination data quality is strong enough

- whether status updates are usable

- whether finance can reconcile the flow

- whether support can resolve common issues

This phase should produce operational truth, not just launch metrics. If the system only works because a few internal people are manually rescuing every exception, that is valuable information. It means the process is not yet stable.

Phase two adds controlled breadth#

Once the core path works, expand deliberately. This usually means adding one kind of complexity at a time, such as:

- another payout method

- another region

- another recipient segment

- more automation in routing and status handling

The mistake to avoid here is broad expansion without updated controls. Each added method changes onboarding, support, reconciliation, and communication. Each added region may introduce new operational variation. Expansion is where the original design assumptions are most likely to break.

At this stage, focus on:

- comparing failure patterns across methods

- refining routing logic

- improving recipient communications

- tightening support escalation paths

- confirming that internal reporting still holds together

This is also the phase where teams often discover whether a one-platform strategy is still sufficient.

Phase three scales with governance, not improvisation#

The third phase is about durable scale. By this point, the question is no longer whether payouts can be sent. The question is whether the program can keep expanding without becoming dependent on tribal knowledge, heroics, or inconsistent exceptions.

A mature phase-three posture usually includes:

- clear ownership across product, operations, legal, finance, and support

- documented routing rules

- repeatable evidence collection

- stable reconciliation and reporting

- escalation paths for higher-risk engagements

- a defined approach to adding or changing providers

At this phase, control matters as much as capability. You do not want every new market or payout request to become a custom project. The operating model should be flexible enough to adapt, but structured enough to remain understandable.

What not to do#

Across all three phases, avoid these patterns:

- launching too many payout methods before the first one is truly operational

- expanding coverage based on provider marketing rather than real recipient fit

- assuming support can absorb ambiguity

- treating compliance as a post-launch cleanup task

- ignoring the need for an alternate route when direct contractor payouts become risky

A phased launch works when each phase answers a real question and creates usable evidence for the next decision.

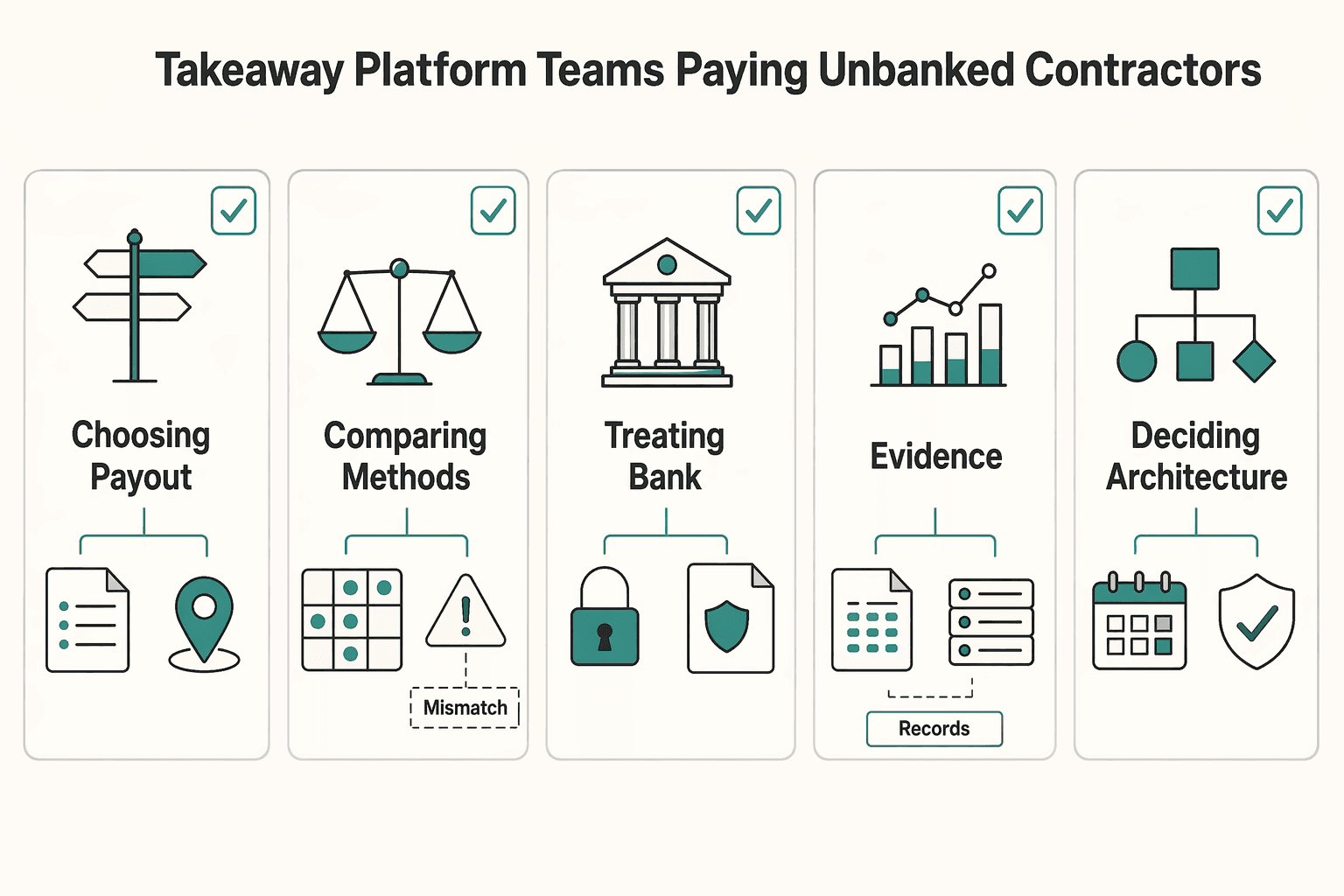

The takeaway for platform teams paying unbanked contractors now#

If your team is making this decision now, the most useful mindset is to stop looking for a single payout method that solves everything. That framing usually leads to overconfidence early and rework later.

A better framing is to build a payout strategy that matches recipient reality, preserves operational control, and gives the company a clear path when direct contractor payouts are no longer the right answer.

According to Federal Reserve guidance and FFIEC materials in the source set, third-party payout routes still need active oversight, even when the rail itself looks familiar. In a 2025 or 2026 rollout, use data from your first 30 days of live payouts and an analysis by corridor, payout method, and failure code before you widen coverage. We covered the jurisdiction layer in Cross-Border Compliance Checklist for Platform Payouts.

Model the recipient path with concrete scenarios before launch. For example, compare a wallet payout that costs $2, a bank transfer at $4, a local-wallet cash-out at 3 EUR, a cash-pickup fallback at $7, and an exception-driven resend that adds another $10 in operational drag. If ownership is still fuzzy at that point, align the rollout with payment approval workflow thresholds before engineering scope hardens.

In practice, that means:

- choosing payout methods based on recipient fit and operational durability

- comparing methods before engineering locks in assumptions

- treating bank, wallet, cash pickup, and stablecoin options as distinct tools with distinct tradeoffs

- recognizing that Employer of Record routing is a structural route, not just another rail

- deciding architecture based on real compromise, not convenience or fear

- requiring evidence and reconciliation discipline before calling the system scalable

- launching in phases so that complexity is earned, not guessed at

The best decision is rarely the most expansive or the most minimal one. It is the one that your teams can explain, operate, defend, and adapt as the business grows.

If you keep that standard in view, you are far less likely to end up with a payout stack that looks fine in a product diagram but falls apart under real-world recipients, real-world exceptions, and real-world risk.

Frequently Asked Questions

Should we start with bank payouts because they seem the most standard?

Not necessarily. Bank payouts are a sensible starting point only if recipients can easily provide bank details, expect to receive funds that way, and your teams can support the process well. If your audience is more mobile-first or less well served by bank-based flows, a wallet option may be more practical.

Is it a mistake to offer more than one payout method at launch?

Not always. More than one method can make sense when recipient needs are clearly different and one method would leave too many users behind. The key is to avoid adding methods that support, finance, and compliance are not ready to operate well.

When should cash pickup be part of the stack?

Cash pickup should be part of the stack when recipients need physical access to funds and account-based options do not serve enough of the intended population. It is usually strongest as a targeted method rather than a blanket default because it adds distinct support and operational demands.

How should we think about stablecoin payouts?

Treat stablecoin payouts as a specific option for specific cases where allowed, not as a universal shortcut. Evaluate recipient demand, operational readiness, supportability, and how the method fits your control framework. It should not be used to paper over deeper issues in onboarding, compliance, or contractor risk.

Can a payout rail solve contractor classification or engagement-structure concerns?

No. A payout rail changes how funds move, but it does not resolve structural issues in the relationship. If direct contractor payouts become risky, an alternate route such as an Employer of Record model may need to be considered.

Is one provider usually enough?

Sometimes. One provider can be enough if it truly supports the payout methods, geographies, controls, and records your program needs. If it forces too many compromises, a multi-provider architecture may be the better long-term choice.

What is the most common planning mistake?

A common mistake is committing engineering time before the operating model is clear. Teams often start building around a payment method before aligning on recipient fit, failure handling, compliance evidence, or what happens when a direct contractor model is no longer appropriate.

What should support teams have before launch?

Support should have clear payout-status visibility and a structured way to identify common failure modes. They also need approved steps for destination changes or corrections, plus an escalation path for cases that do not fit the standard flow. Without that, simple launches can become difficult once real exceptions appear.

What does “scalable” really mean here?

Scalable means more than sending more payouts. It means product, operations, finance, compliance, and support can all handle growing volume and complexity without relying on manual heroics or inconsistent decisions.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- dol.gov/agencies/whd/flsa/misclassificationtrusted

- dol.gov/agencies/whd/flsa/misclassification/rulemakingtrusted

- fdic.gov/sites/default/files/2024-03/fil18026a.pdftrusted

- federalreserve.gov/frrs/regulations/appendix-cpss-iosco-princip...trusted

- federalreserve.gov/frrs/guidance/interagency-guidance-on-third-...trusted

- ffiec.gov/sites/default/files/media/press-releases/201...trusted

- irs.gov/forms-pubs/about-form-8233trusted

- irs.gov/businesses/small-businesses-self-employed/in...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: