Quick Answer

Use an operations-first sequence: launch only where your team can audit OFAC and PEP decisions, trace payout status end to end, and reconcile returns without vendor-ticket dependence. Start with Peru as a controlled pilot to test reject reasons and exception handling, keep Southeast Asia in wallet-first cohorts with bank fallback until status mapping is stable, and raise South Asia batch volume only after idempotency keys and ledger links are consistently reliable.

Global payouts in emerging markets are won in operations, not slide decks#

If you are choosing where to launch cross-border payouts in 2026, start with what your team can actually run. Too many "top" lists lean on hype or market-cap tables. That may work for headlines, but it does not help with execution.

In emerging-market regions, demand is usually easier to present than operations. The harder question is whether your product, ops, finance, and engineering teams can support the compliance and execution load without constant manual cleanup.

- Who this list is for

This is for platform founders, product leaders, finance and ops teams, and engineering owners running contractor, creator, or marketplace payouts. If your team owns recipient onboarding, compliance workflows, payout routing, or reconciliation outputs, you are the audience. The working assumption is simple: someone on your team will eventually have to explain a held payment or an unreconciled batch to both support and finance.

- How regions should be judged

We are not picking regions on addressable-market slides alone. Judge them on operational fit and regulatory execution demands, because those often decide whether an early launch stays contained or turns into a support and finance problem. A good first-wave region is not just a place with demand. It is a place where your team can run the required checks, handle exceptions, and keep reconciliation usable.

- What is in scope for 2026 execution

The scope here is region choice and launch checkpoints. Treat each option as an operating choice, not a branding choice. Stablecoin adoption may have upside, but it also comes with explicit risks and limitations, so it should not be your default first move unless you already have a clear compliance and support model. If a provider cannot clearly show status visibility, return handling, and reconciliation outputs before launch, that is a red flag no matter how strong the growth story looks.

One practical rule runs through the rest of this article: choose the regions your team can prove, not the ones you can pitch. In payments, structure matters because it shapes the regulatory workflows you will need to handle. Related: How to Pay Creators Globally: Payout Options for YouTube Twitch Substack-Style Platforms. If you need a quick next step, try the free invoice generator.

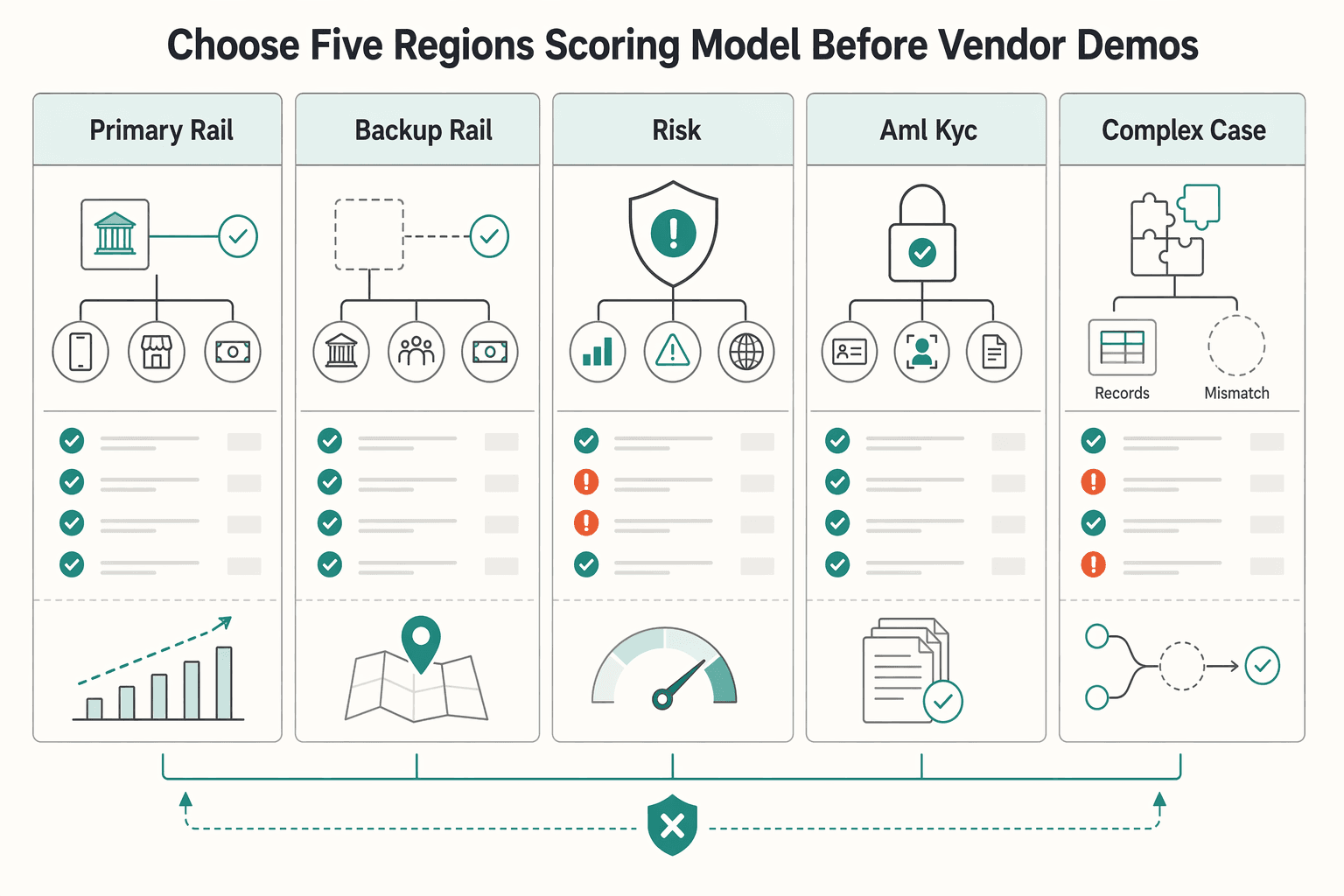

Choose your five regions with a scoring model before vendor demos#

Build the scorecard before you book demos. If sanctions controls or payout-status visibility are not auditable, treat the region as no-go regardless of growth forecasts.

| Scorecard field | What to record for each region | Wave 1 standard |

|---|---|---|

| Primary rail | Your main payout route and who can receive it | Must work for your core recipient type |

| Backup rail | Usable fallback when the primary rail fails | Must be live and operational, not roadmap-only |

| Data risk | Required beneficiary fields, validation flow, and common reject patterns | Pre-submit checks and usable return reasons |

| AML/KYC/KYB load | Which checks run, where manual review happens, and who owns the queue | Documented ownership and review steps |

| FX complexity | Where conversion happens and how rate/fee disputes are handled | Finance signoff before launch |

| Support burden | Likely hold/failure scenarios and what support can explain from system data | Visible status events and exception paths |

| Wave | First-wave or second-wave candidate | First wave only if every gate below is met |

-

Build rails first. Capture the primary rail, the real backup rail, and the data-risk handling for each region. The key test is recoverability: can you validate before submit, and can you get return reasons your team can act on when payouts fail?

-

Make compliance a hard gate. Record whether OFAC screening is performed, what logs are retained, and how held payouts are reviewed and released. OFAC sanctions programs can require blocking property and prohibiting dealings in blocked property, so your audit trail must show what happened and why. If your policy also includes PEP screening, W-8/W-9 collection, or VAT documents, document who owns those checks and whether your flow can collect, store, and retrieve the required artifacts.

-

Define the finance evidence pack before launch. Finance should be able to trace each payout from request through completion, return, fee, FX, and reversal states without opening a vendor ticket. If U.S. tax reporting or foreign-account analysis could apply, map that path with your tax team early. Where FBAR handling is relevant, store maximum account values in U.S. dollars rounded up to whole dollars and convert non-U.S. currency with the Treasury Financial Management Service rate.

-

Use one no-go rule and enforce it. If you cannot audit sanctions decisions or prove payout status end to end, stop. "Processing" is not enough when you cannot tell whether funds were blocked, returned, or still in flight.

-

Treat wave planning as an operating decision. First-wave regions should pass stricter readiness gates than second-wave regions because they set your support load and close quality. Second-wave regions can carry more manual work only after the first wave closes cleanly with defensible evidence.

You might also find this useful: Cash Pickup Payouts for Unbanked Contractors in Cash-Preferred Markets.

Region 1 Peru as a controlled Latin America learning market#

Peru is a practical first-wave learning market in Latin America if you want to test local-clearing operations before broader rollout. The World Bank's LAC fast-payments analysis (published 2025-11-01) surveyed 11 central banks in countries with operational fast payment systems and includes Peru, which supports using Peru as an infrastructure-relevant test market.

Peru also appears in the MILA market-integration context with Chile and Colombia. That makes Peru a reasonable early regional learning wave, with strict controls before scale.

Why Peru is useful early#

Use Peru to test recoverability, not just reach. A SWIFT fallback can extend coverage when the primary route cannot handle a case, but weak beneficiary IBAN/SWIFT data quality and unclear return messages can still create avoidable failures and support load.

In vendor demos, ask for proof of pre-submit field validation, clear return reasons, and timestamped reject/hold events. If those controls are missing, keep Peru at pilot scope.

What to prove before you scale Peru#

Do not move past pilot volume until AML/KYC handling and exception operations are stable and visible:

- AML/KYC visibility: Track submitted, approved, held, and rejected recipients, including manual-review volume.

- Exception queue quality: For each held or returned payout, capture reason, reviewer action, release or rejection timestamp, and payout reference ID for reconciliation.

- Recoverability evidence: Confirm your team can diagnose and resolve returned payouts without relying on vendor-ticket back-and-forth.

Treat Peru as a measured first launch, and scale only if completion quality and exception handling stay controlled.

Need the full breakdown? Read When Platforms Should Use Wires vs Local Rails for Cross-Border Payouts.

Region 2 Southeast Asia for wallet-first scale with bank fallback#

Southeast Asia is a strong next region for creator and gig platforms when last-mile wallet access matters. Scale it with wallet-first routing and a bank fallback only if your controls and status visibility are audit-ready. The operating risk is not just reach. It is whether your team can trust and reconcile payout outcomes across providers.

One regional commerce source reports that 73% of e-commerce transactions are mobile, with Android at 82% mobile browser share across ASEAN-6 in Q1 2024. That is checkout evidence, not payout evidence, so treat it as directional. It still supports a practical design choice: make enrollment and payout UX work cleanly on mobile instead of assuming bank-first flows will convert.

Why this region earns a wallet-first design#

PayNow-UPI linkage and Project Nexus both indicate movement toward linking domestic instant payment systems across jurisdictions and away from traditional SWIFT-only paths. That supports wallet-first routing when recipient access and payout speed matter.

The tradeoff is operational: progress remains uneven in wholesale settlement and end-to-end visibility. In practice, you can gain reach while losing status clarity, which drives support load and slows finance reconciliation.

What you need to prove before widening the cohort#

Do not move past pilot volume until failure taxonomy is stable across wallet providers and AML holds are resolved predictably. Focus on three controls:

| Control | Required detail | Scale note |

|---|---|---|

| Normalized status mapping | Store provider status, internal status, timestamp, and payout reference ID for every transaction | Keep this region in pilot mode if teams are still manually translating statuses in tickets or spreadsheets |

| AML hold traceability | Capture hold reason, review/case reference, reviewer decision, and release or rejection timestamp for held payouts | Do not move past pilot volume until AML holds are resolved predictably |

| Bank fallback discipline | Validate beneficiary bank data before fallback | Use bank fallback as a backup path, not a substitute for clean status truth |

Keep this region in pilot mode if your team is still manually translating statuses in tickets or spreadsheets. Use bank fallback as a backup path, not a substitute for clean status truth.

Only connect this regional choice to USDC when stablecoin payout rails are already enabled and compliant for your use case. If relevant, apply the same control standard before rollout: Stablecoin Payouts for Platforms: How to Disburse USDC to Contractors Globally.

For adjacent infrastructure context, see ISO 20022 Migration for Payment Platforms: What the Global Standard Means for Your Payouts.

Region 3 South Asia for recurring high-volume contractor batches#

South Asia is worth prioritizing for recurring contractor batches when control maturity leads volume, not the other way around. Batch throughput helps only if you can prevent duplicates and trace each payout from request creation to ledger export.

The economic case should stay disciplined. Platform growth is not the same as platform scaling: you are only scaling if volume rises without matching cost growth in exception handling, compliance review, and reconciliation. If reconciliation is still partly manual, put stronger controls in place before faster rollout.

Cross-border payout operations already face delays, unexpected fees, and compliance requirements, so provider selection is a control decision, not a coverage slide. Require transparent FX charges, real-time tracking, multi-currency wallet support where needed, and built-in compliance checks.

Controls to lock before raising batch size#

| Control | What to do | Checkpoint |

|---|---|---|

| KYC/KYB gating | Complete recipient and business verification | Before payouts enter live batch populations |

| Tax-form readiness where applicable | Pre-collect W-8 or W-9 during onboarding | When your tax workflow requires it |

| End-to-end traceability | Retain payout request ID, idempotency key, provider reference, timestamps, amount and currency, FX/fee details when applicable, and ledger export reference | Sample a batch and confirm engineering, ops, and finance can independently trace payouts end to end without ad hoc interpretation |

Use one hard checkpoint before you increase batch size: sample a batch and confirm engineering, ops, and finance can independently trace payouts end to end without ad hoc interpretation. If that chain is not reliable yet, keep volume capped and close control gaps first.

We covered this in detail in How to Build a Currency Reserve Strategy for Marketplace Platforms Operating in Volatile Markets.

Region 4 Sub-Saharan Africa where mobile money determines reach#

Prioritize Sub-Saharan Africa when expanding recipient reach matters more than keeping one uniform payout path. As of the World Bank's April 17, 2024 overview, 49 percent of adults in the region had an account, and account ownership had more than doubled since 2011, with much of that growth linked to mobile money adoption.

Why this region earns a slot#

Mobile money can materially expand who you can pay, especially where bank-account access is uneven. At the same time, digital payments are increasing while cash is still common, so treat mobile money as a reach enabler, not a guarantee of a fully digital payout journey.

A June 2026 Scientific African study using the latest Global Findex data for Sub-Saharan Africa also notes there is no full consensus on mobile money's effect on financial inclusion. The practical takeaway: demand signal and inclusion outcome are related, but not identical.

The operating rule to keep expansion healthy#

Scale this region only as fast as your exception process can close held and returned payouts. If investigations are not clearly owned, traceable, and time-bounded in your own operating policy, pause expansion until they are. Reach gains are real, but they stop compounding when unresolved cases grow faster than your team can clear them.

Related reading: Crypto Payouts for Contractors: USDC vs. USDT - What Platforms Must Know.

Region 5 Central and Eastern Europe for control-heavy bank rail execution#

Pick Central and Eastern Europe when you want tighter control design before you scale. The practical anchor here is not "easy payouts." It is using EU VAT mechanisms to make cross-border operating decisions explicit, documented, and reviewable.

The finance control layer that actually matters#

For EU-facing activity, start with what is concrete. From 1 July 2021, EU cross-border B2C e-commerce VAT rules changed. Under One Stop Shop (OSS), sellers and platforms can register in one Member State of identification for covered VAT declaration and payment, and the OSS page says this can reduce red tape by up to 95%.

If more than one fixed-establishment Member State could apply under the Union scheme, your choice of Member State of identification is binding for the current calendar year plus the two following calendar years.

What to verify before calling it your control market#

If your model includes complex cross-border VAT treatment, use a VAT Cross-border Ruling (CBR) where available. Check the participating-country list first, since CBR does not cover every EU country, and submit under that country's national VAT-ruling conditions.

Before treating this region as your control benchmark, require an evidence pack with:

- reconciliation records that tie payout request to final ledger outcome

- an exception log that shows how rejected or returned cases are resolved and closed

If finance can explain OSS choices but operations cannot close returned payouts cleanly, you have administrative structure, not operational control.

For a step-by-step walkthrough, see Global Treasury Management for Platforms Across 50+ Countries.

Launch sequencing and ownership rules that prevent payout chaos#

Sequence before speed: roll out in gated phases, because distribution can scale globally faster than payment operations can stay reliable.

| Phase | Gate | Ownership / checkpoint |

|---|---|---|

| Sandbox first | Start with one region and one primary payout rail, and lock the required recipient data for that rail from day one | Engineering should own retry safety and webhook status handling; prove you can reconcile payout request, provider outcome, and ledger movement before you go live |

| Limited live cohort next | Move to a small production cohort only when ops can explain failures by rail and close exceptions consistently | Ops owns routing and exception handling, and finance owns tax and policy artifacts for the live flow |

| Controlled scale last | Scale in small increments with a recurring go/no-go review across finance, ops, and engineering | Update provider mappings before expansion if message formats change; pause if reconciliation cannot cleanly tie request, fees, FX, and final posting |

- Sandbox first

Start with one region and one primary payout rail, and lock the required recipient data for that rail from day one. Engineering should own retry safety and webhook status handling here. Treat this phase as a proof phase: show that you can reconcile payout request, provider outcome, and ledger movement before you go live.

- Limited live cohort next

Move to a small production cohort only when ops can explain failures by rail and close exceptions consistently. Payments are local, so do not assume one method will perform the same way across markets or providers. Keep ownership explicit in this phase: ops owns routing and exception handling, and finance owns tax and policy artifacts for the live flow.

- Controlled scale last

Scale in small increments with a recurring go/no-go review across finance, ops, and engineering. Keep the same ownership boundaries as volume grows, and update provider mappings before expansion if message formats change. If payout completion looks healthy but reconciliation still cannot cleanly tie request, fees, FX, and final posting, pause expansion until controls catch up.

This pairs well with our guide on Mass Payouts for Gig Platforms That Teams Can Actually Operate.

Pick regions by payout certainty and scale only with proof#

Sequence regions by measurable payout certainty, not momentum: start where completion, compliance controls, and reconciliation evidence are already strong enough to audit, then expand only when results hold.

- Start with proof, not pipeline

Choose the first region where you can measure cost, speed, transparency, and access from live operating data, not provider positioning. This matches the G20 direction since 2020 toward measurable outcomes, with most global quantitative targets set for end-2027. If payout outcomes and reconciliation evidence are not clear, you do not have a scale-ready launch.

- Treat each region as a corridor decision, not a map color

Region-level coverage claims are not enough. Conditions vary by corridor, and the World Bank dataset spans 367 corridors across 48 sending countries and 105 receiving countries. Validate coverage and constraints corridor by corridor, including intermediary hops, because extra hops can increase fees and delay fund availability. Also account for first-mile and last-mile dependence on domestic rails.

- Use a balanced first trio as a practical sequencing choice

A useful first wave is one learning market, one growth market, and one control market. It is not a universal formula, but it gives you a practical spread for testing reliability and operability. Keep one evidence standard across all three, and pause expansion if one market cannot meet it.

- Pilot only after provider terms and success criteria are explicit

Before increasing volume, review provider agreements and confirm service expectations are defined in ways you can monitor. Run a limited production pilot with auditable exit gates: corridor coverage confirmed, status reporting stable, and reconciliation evidence strong enough to support scale decisions over time. If you want to confirm country- and program-level coverage, Talk to Gruv.

Frequently Asked Questions

What are the top criteria for choosing emerging market payout regions first?

Start with payout certainty, not market buzz. The first-wave region should have rail performance you can verify on speed, cost, and transparency, plus compliance checks you can audit. If sanctions controls or payout-status visibility are weak, treat that region as a no-go even when demand looks strong.

Which rail should we choose first for contractors and creators: SWIFT, local bank transfer, or wallet/mobile money?

There is no universal winner, so choose based on recipient behavior and corridor evidence. For some creator or gig corridors, wallet/mobile-money rails can be materially cheaper; in other cases, bank or SWIFT rails may still be the practical fit for coverage. Keep a primary rail and fallback, but validate real cost, speed, and transparency before standardizing.

What usually breaks first when a platform expands payouts into a new region?

Usually it is not nominal send speed. It is weak control and operating visibility: cost assumptions that do not hold, limited status transparency, and compliance gates that are not fully operationalized. A good checkpoint is one export that ties screening, payout routing, cost outcomes, and final ledger posting before you add volume.

How should finance, ops, and engineering split ownership of global payouts?

Use a clear practical split even though no regulator mandates one. Assign explicit owners for compliance-policy controls, day-to-day routing and exceptions, and system reliability/data integrity. If one team informally owns all three, problems usually surface at month end instead of during launch.

When should we delay a region launch even if demand is strong?

Delay when your evidence pack is thin. That means no auditable OFAC and PEP control process, stale beneficial ownership information for business recipients, or weak corridor evidence on cost, speed, and transparency. Strong demand does not offset control gaps you cannot audit.

How do KYC, KYB, AML, OFAC, and PEP watchlists change prioritization?

They change it a lot because they determine whether a region is operable at scale. FATF Recommendations remain the baseline for AML and counter-terrorist financing controls, and PEP scrutiny extends beyond the individual to family members and close associates. Also, OFAC name-list search is a tool, not a substitute for due diligence, so if your team cannot maintain current true-owner data and review logic, move that region out of wave one.

Where does USDC fit in a payout strategy, and when is it the wrong first move?

USDC fits when intermediaries are a proven bottleneck in a specific corridor. It can reduce intermediary dependence in some cross-border flows, but it also brings specific financial-crime risk controls and U.S.-dollar exposure risk for foreign recipients. If your KYC, KYB, AML, and control operations are still immature, it is the wrong first move. If you are exploring it seriously, see this deeper USDC guide.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bsaefiling.fincen.gov/docs/XMLUserGuide_FinCENFBAR.pdftrusted

- federalreserve.gov/econres/notes/feds-notes/payment-stablecoins...trusted

- federalreserve.gov/econres/notes/feds-notes/payment-stablecoins...trusted

- fincen.gov/reporting-maximum-account-valuetrusted

- fincen.gov/report-foreign-bank-and-financial-accountstrusted

- ie.edu/uncover-ie/top-fintech-companies-master-in-f...trusted

- imf.org/-/media/files/publications/gfsr/2025/october...trusted

- lincolninst.edu/app/uploads/legacy-files/pubfiles/financing-...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Stablecoin Payouts for Platforms Disbursing USDC to Global Contractors

**Step 1. Set the operating model before you talk about speed.** This guide is for platform operators shipping stablecoin contractor payouts in production, not for freelancers choosing a wallet. The core stance is simple: approve compensation in USD, use a stablecoin as the settlement rail, and treat controls as product requirements from day one. Stablecoins are built to behave like money, and businesses already use them for supplier payments, cross-border invoicing, and treasury movement. That makes stablecoin payouts worth a look, but only if your payout process is as disciplined as your fiat process.

ISO 20022 Migration for Payment Platforms: Payout Cutover Guide

ISO 20022 is already the production standard for cross-border payouts, so this is now an implementation-sequencing problem, not a watch-and-wait exercise. [Swift CBPR+](https://www.swift.com/news-events/news/iso-20022-new-era-global-payments) went live in March 2023, and Swift marks the cross-border coexistence period as ending on 22 November 2025. For CTOs and solution architects, the core question is what to migrate first without hard-coding avoidable debt into your platform.

How Platform Operators Pay Creators Globally Across YouTube, Twitch, and Substack

Global creator payouts can break when you treat them like a single integration. For YouTube, Twitch, and Substack-style products, payout behavior changes by country, destination type, threshold, and provider program. The launch decision is really a series of smaller operating decisions. If you want creator trust, optimize for predictable delivery and clear exception handling first, not for the broadest coverage claim.