Quick Answer

Yes - use a pooled omnibus setup only when you can prove contractor-level ownership from intake to payout. In practice, that means named control owners across the Intermediary chain, replay-safe ledger journals, and clear evidence for every hold or release. If duplicate provider events, unmatched VBA deposits, or return handling cannot be explained from exported records, delay launch and use a more separated structure.

How Omnibus Account Architecture Works for Contractor Funds#

Step 1#

Start with the real choice: do you want one pooled Omnibus account operated through an Intermediary, or a more externally separated account structure for contractor funds? If you choose a pooled route, your internal records need to show, consistently, which contractor a balance belongs to, why it is held, and when it can be released.

That is the basic go or no-go rule for this guide. If your team cannot maintain reliable attribution from inbound funds to contractor balance to payout, do not launch a pooled model yet. Shared balances become hard to untangle when a return, investigation, or hold arrives.

Step 2#

Treat this as a product, ops, and engineering decision, not a bank-account naming exercise. Product needs clear user states for pending, held, and paid funds. Ops needs named owners for onboarding checks, release decisions, exceptions, and reconciliations. Engineering needs a ledger that can prove what happened when provider events arrive late, twice, or out of order.

Before you build, check whether you can answer four questions on one page:

- Who legally or contractually controls the master funds account

- Who performs or relies on compliance checks before release

- What record is the source of truth when provider data conflicts with your app balance

- What evidence you can export when a contractor, partner, or regulator asks why funds were held or paid

If any of those answers are still "shared," "TBD," or "handled by the provider," you do not have launch readiness. You have an ownership gap.

Step 3#

Keep the scope narrow. This is an operational design guide for contractor wallets and payouts, not legal advice, and program-specific requirements still apply. A useful compliance principle comes from outside fintech. FTA Circular 4220.1G, applicable January 17, 2025, states that when guidance conflicts with a governing statute or regulation, "the statute or regulation will supersede this circular," and that recipients remain responsible for compliance. The same mindset applies here. General design guidance helps, but your actual program rules, contracts, and governing regulations decide what is allowed.

Success is not just faster disbursement. It is faster movement without losing control of review processes, auditability, and ownership inside your own records. The real tradeoff is where separation lives: outside your platform in account structure, or inside your platform in ledger discipline and control ownership.

One practical note before you go deeper: the omnibus model for custody is not new. Fidelity Digital Assets describes it as having origins in traditional finance and explains why custodians use it to secure customer assets. That history is useful, but it should not make you casual. Pooled funds can be efficient. They are not forgiving.

If you are comparing pooled accounts with dedicated account identifiers, see Virtual IBANs for Platforms: How to Give Every Seller Their Own Dedicated Bank Account Number.

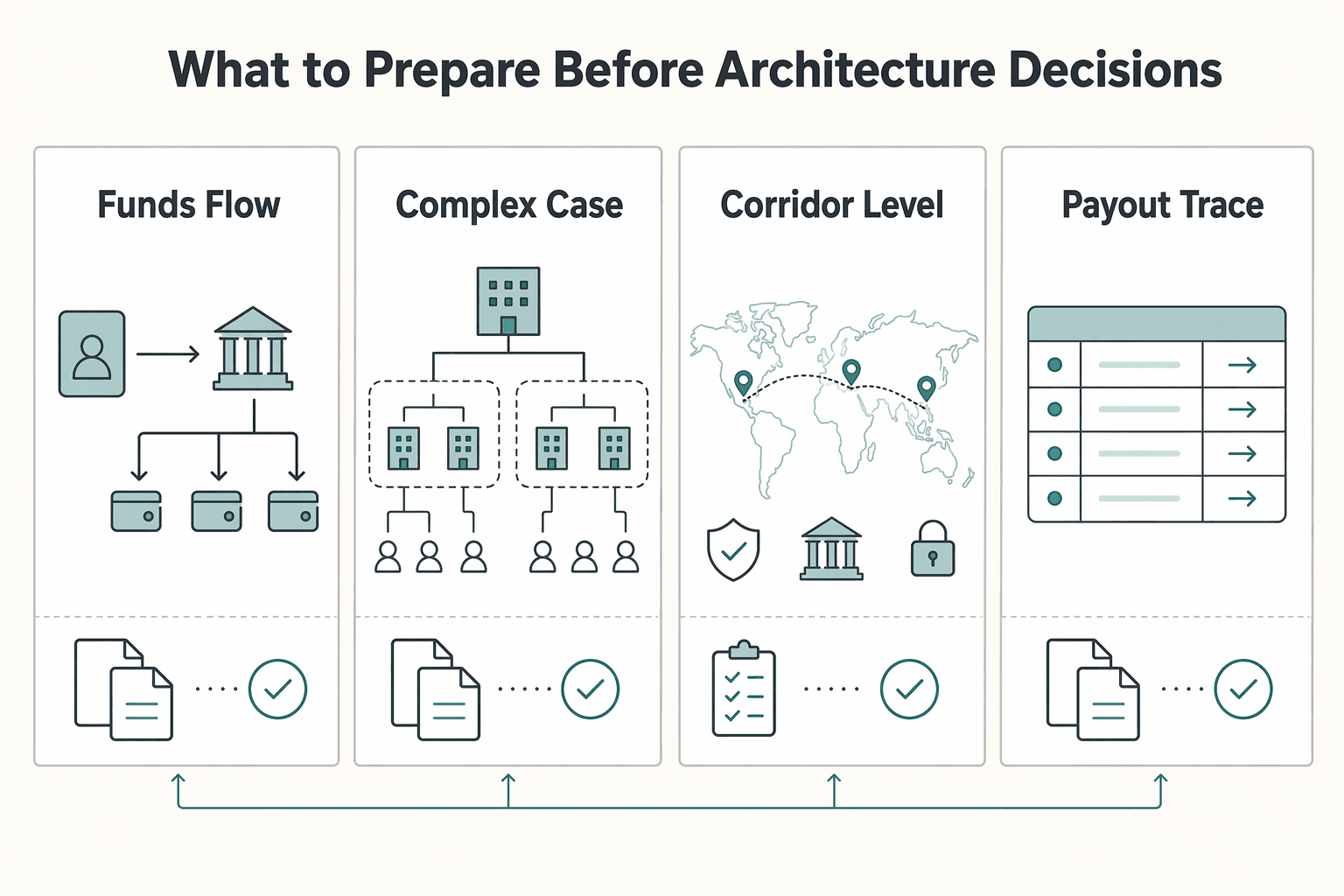

What to prepare before architecture decisions#

Prepare four things before choosing pooled or externally separated funds: a full funds-flow map, an entity-and-contract map, corridor-level compliance assumptions, and a ledger-first source-of-truth model. If you cannot tie each balance to a specific contractor with exportable records, pause the architecture decision.

| Preparation | What to document | Grounded check |

|---|---|---|

| Funds-flow map | From first receipt to final payout, including where a VBA credit is recorded, where holds or returns are handled, and which path releases funds | Ops can trace one inbound payment to one contractor balance and one payout or return without jumping across multiple tools |

| Entity-and-contract map | Your platform, the Intermediary, any Sub-custodian, the payout provider, and any Merchant of Record (MoR) role | Use segregation of duties as a control prompt when you review this map |

| Corridor-level compliance assumptions | Where KYC, KYB, and AML gates apply before release, where manual review is expected, and what evidence must be retained for held or cleared payments | Define the gate, the owner, and the record |

| Ledger-first source of truth | Ledger journal schema, a webhook event model, reconciliation exports, and beneficial-owner attribution fields | For any contractor, export journal entries, provider events, and reconciliation line items that explain the current balance |

Step 1#

Map the full funds flow from first receipt to final payout. Document where a Virtual Bank Account (VBA) credit is recorded, where holds or returns are handled, and which path releases funds. If you use an FBO-style master account, mark it clearly and include the contractor-level balance record, not just the bank account. Program ledgers still need to track individual end-user balances.

Use a practical check: can ops trace one inbound payment to one contractor balance and one payout or return without jumping across multiple tools?

Step 2#

List every entity and contract in the chain: your platform, the Intermediary, any Sub-custodian, the payout provider, and any Merchant of Record (MoR) role. This is less about reaching final legal conclusions and more about exposing handoff risk early.

A common breakdown is split ownership across funds holding, screening, and payout execution without a clean exception path. Use segregation of duties as a control prompt when you review this map.

Step 3#

Set compliance assumptions by corridor, not as a single global policy. For each corridor, note where KYC, KYB, and Anti-Money Laundering (AML) gates apply before release, where manual review is expected, and what evidence must be retained for held or cleared payments.

Do not invent thresholds at this stage. Define the gate, the owner, and the record.

Step 4. Define your source of truth before engineering starts#

Keep the build sequence ledger-first: create the ledger, provision user-level ledger accounts, connect external accounts, then enable money movement. Minimum artifacts are a ledger journal schema, a webhook event model, reconciliation exports, and beneficial-owner attribution fields.

Final verification is simple: for any contractor, you should be able to export journal entries, provider events, and reconciliation line items that explain the current balance. If you cannot, the architecture choice is still premature.

For the accounting treatment of held funds, reserves, and liabilities, see What Is a Balance Sheet? How Payment Platforms Account for Held Funds Reserves and Liabilities.

Compare omnibus and segregated models before you build#

If you cannot prove beneficial owner attribution on demand and keep ledger postings replay-safe, do not launch an omnibus model. Pooled custody can reduce account sprawl, but it also puts more investigation and compliance pressure on your internal ledger controls.

Step 1#

Start with custody mechanics, not naming.

An omnibus account pools multiple customers under one named account. In the FBO-style version, one custodial account is opened in the institution's name for members, assets are commingled, and your institution tracks who owns what on its own ledger.

A segregated (1:1) model keeps each customer in their own custodian account. Assets are not commingled, and beneficial ownership is established at the custodian level.

Use that distinction to decide where you want control evidence to live: mostly inside your platform ledger (pooled) or more explicitly at the custodian layer (1:1).

Step 2#

Compare the models on the decisions that create downstream operational pain.

| Decision point | Omnibus / FBO pooled model | Segregated / 1:1 model |

|---|---|---|

| Setup complexity | Fewer external accounts, more internal ledger responsibility | More external account setup per customer |

| Reconciliation burden | Internal mapping from pooled funds to contractor balances is critical | Ownership separation is clearer at custodian level, but platform/provider reconciliation still matters |

| Control surface | Holds and releases can be routed through one pooled balance | More externally separated balances and handoffs |

| Payout path | Centralized release flow is possible if internal controls are strong | Flow depends more on per-account custodian handling |

| Exception handling | Investigations often start with decomposing pooled ownership | Contractor-level separation is clearer, but external coordination can increase |

| Jurisdiction friction | Weak records can increase AML/regulatory scrutiny | External separation can be easier to evidence, but treatment still varies by jurisdiction |

One tradeoff is consistent: omnibus structures are often operationally efficient, but they also carry fraud, regulatory, money-laundering, and market-manipulation risk when controls are weak.

Step 3#

Apply one go/no-go test before build: if your team cannot maintain reliable beneficial owner attribution and replay-safe ledger postings, do not use pooled custody for contractor balances.

Test it with real evidence. For one contractor, produce the inbound credit record, ledger entries, current balance explanation, hold or release decision record, and payout or return outcome. Then replay a duplicate provider event and confirm the balance does not post twice.

Choose segregated handling when your strongest control sits at the custodian layer. Choose pooling only when your ledger, reconciliation, and evidence exports are already dependable.

If you need a deeper primer on structure mechanics, see Omnibus Accounts Explained: How Platforms Hold and Segregate Client Funds. We covered adjacent operating patterns in How Staffing Platforms Automate Healthcare AP for Clinical Contractors.

Assign accountability across the chain#

Do not launch until every control has a named owner, evidence artifact, and escalation SLA. In omnibus programs, accountability gaps, not account structure alone, are what turn routine exceptions into compliance risk.

Step 1 Name the accountable entity for each control#

List each actor separately: your platform, the Intermediary, the Sub-custodian, and, where relevant, a Broker-dealer or Registered Investment Advisor (RIA). For each control, record who performs it, who is accountable, and who only provides data or tooling.

If your platform makes hold or release decisions using another party's screening output, document who can approve, who can override, and who retains evidence. For U.S.-scoped programs, define who owns any BSA reporting or recordkeeping path tied to FinCEN (the Financial Crimes Enforcement Network within Treasury), since BSA administration authority is delegated to FinCEN.

Step 2 Build a responsibility matrix you can test#

Keep ownership, evidence, and timing in one place.

| Activity | Named owner | Evidence artifact | Escalation SLA |

|---|---|---|---|

| Onboarding and customer due diligence | Platform / Intermediary / other named entity | Approved onboarding record, review notes, decision timestamp | Written clock for unresolved cases |

| Sanctions and AML screening | Named screening owner | Screening result, match disposition, reviewer identity | Written clock for true-match escalation |

| Transaction monitoring and suspicious activity review | Named monitoring owner | Alert ID, case file, disposition log | Written clock for escalation to the defined authority or compliance lead |

| Hold and release decisions | Named decision owner | Hold reason, release approval, linked ledger event | Written clock for release or continued hold review |

| Disputes and regulator inquiries | Named response owner | Case file, response packet, audit trail export | Written clock for first response and final handoff |

Run one end-to-end scenario through this matrix: onboarding, inbound credit, hold, alert, payout release or block, then dispute. If you cannot identify owner plus evidence at each step quickly, the matrix is incomplete.

Step 3 Assign reporting mechanics before go-live#

When reporting or valuation rules may apply, assign execution mechanics, not just legal ownership. For FBAR (FinCEN Form 114) workflows, FinCEN guidance says each account must be valued separately, amounts are recorded in U.S. dollars rounded up to the next whole dollar (for example, $15,265.25 becomes $15,266), and negative calculated value is entered as 0 in item 15.

The recurring failure pattern is split responsibility with no final decider. Before go-live, confirm every control has one accountable owner, one stored evidence artifact, and one written escalation SLA with backup coverage.

Related reading: Account Reconciliation for Payment Platforms: How to Automate the Match Between Payouts and GL Entries.

Design the ledger and wallet projection layer#

Set the rule first: your ledger journal is the source of truth, and wallet balances are derived projections that can be briefly out of sync without changing the legal or operational record.

Step 1 Anchor truth in journal entries#

Record every money movement as a journal event first, not a direct balance update. When funds hit a Custodial account, write an immutable journal entry tied to that external event, then let the wallet layer project contractor balances from journals.

This separation is what keeps the system recoverable during retries, delayed webhooks, and backfills. Projections can be rebuilt; journals are your evidence trail. A quick check is to replay one contractor's journals in a lower environment and confirm available, held, and total balances match the current projection.

Step 2 Define the posting model before coding#

Avoid a generic balance updated event. Define explicit posting states, and require each state to carry an immutable reference to the external trigger (provider event, statement line, or payout outcome).

| Posting state | What it means in your ledger | Required reference |

|---|---|---|

| pending | Funds signaled but not yet recognized as usable | Provider event ID or intake record |

| credited | Funds recognized to the contractor ledger | Custodial account credit event or statement line |

| held | Funds restricted from release | Hold reason code and decision record |

| released | Funds approved out of held or available status | Release approval and payout instruction ID |

| returned | Funds sent back or failed before final contractor use | Return event ID or bank/provider return code |

| reversed | Prior posting economically undone | Linked original journal ID and reversal reason |

Keep entries immutable. Do not overwrite credited into returned; post a linked returned or reversed entry instead.

Step 3 Make ingestion idempotent and replay-safe#

Assume provider events arrive duplicated, out of order, and late. Your webhook path should let you process the same provider event repeatedly without creating duplicate contractor value.

Store core fields for each inbound event (event ID, type, amount, currency, timestamp, raw payload hash, and resulting journal IDs), then enforce one outcome rule: many processing attempts, one economic effect. Replays should no-op cleanly or reproduce the same journal linkage.

Step 4 Reconcile in three hops#

Reconcile in the same order money moves:

| Hop | Compare | Catches |

|---|---|---|

| 1 | Provider statements or confirmed Custodial account events to your internal ledger | Intake mismatches |

| 2 | Ledger totals to wallet projections | Projection defects |

| 3 | Payout outcomes back to the ledger so released funds settle, return, or reverse visibly | Payout-state drift |

Each hop catches a different failure class: intake mismatches, projection defects, and payout-state drift. For mismatches, keep a compact evidence pack with provider event or statement line, journal IDs, projection snapshot, payout instruction ID, and operator notes.

Step 5 Build in implementation order#

Use this order: event schema first, posting engine second, balance projection third, reconciliation jobs fourth. Reversing it usually forces wallet behavior around incomplete event semantics and creates long-term exception debt.

Build the contractor funds lifecycle in production order#

Once your journal model is stable, enforce one production order end to end: collect, post, evaluate release controls, route payout, confirm settlement, then close exceptions. Keep one rule visible across the flow: credited is not the same as releasable.

Step 1. Collect into intake, then post to the ledger#

For Virtual Bank Account (VBA) intake, treat credited and returned events as separate lifecycle signals. Create an intake record first, then post only what is actually matched; if a deposit is unmatched, route it to investigation instead of assigning ownership from arrival alone. Keep investigation context attached to the record (event reference, amount, currency, VBA identifier, and match notes) so ops can resolve it without rework.

Step 2. Separate fund recognition from release eligibility#

Keep recognition and release as different decisions. Funds can be credited while release stays blocked under your control rules, including compliance holds, stale profile checks, or unresolved beneficiary mismatches. Require each release or unblock action to carry the decision reference so the reason is explainable later.

Step 3. Route payout from releasable funds, then wait for settlement truth#

Only instruct payout from releasable funds, and keep the original credit history intact. After instruction, post the final outcome explicitly: settled, returned, or reversed. If funds come back, move them out of releasable state until the exception is reviewed.

Step 4. Use the same status language in ops and user views#

Use richer internal states, but map them to a small contractor-facing set that does not contradict what ops sees.

| Internal condition | Ops meaning | Contractor-facing status |

|---|---|---|

| pending intake | money received but not fully matched | Payment received |

| credited with release block | funds recognized, payout not allowed yet | On hold |

| payout instructed, no final result | money is in transit | Processing payout |

| settled | payout confirmed | Paid |

| returned or reversed | payout failed or funds moved back | Action needed |

For the liquidity side of funds that are ready to pay out, see Liquidity Management for Payment Platforms With Funds Ready to Pay.

Add compliance and tax controls before scale#

Treat compliance and tax controls as launch requirements, not back-office cleanup. Keep identity eligibility, tax profile readiness, and hold or release evidence as separate control lanes so each payout decision is explainable.

Step 1. Split identity checks from tax profile collection#

Use KYC/KYB to determine account and payout eligibility, and run tax profile collection on a separate track for W-8, W-9, and reporting readiness. Keep separate statuses, timestamps, and remediation queues so ops can see exactly what is blocking release.

Before launch, test edge cases like identity approved with a missing tax profile, and a tax profile present with payout still blocked for AML review. In both cases, funds can remain correctly credited while release stays blocked for a specific, recoverable reason.

Step 2. Capture reporting signals early, not after the first tax season#

Store reporting-critical facts early, even if your platform is not the filer for every form. From the IRS materials, Form 8938 is a core signal point and should shape what you retain and export.

| Form 8938 point | Grounded requirement to reflect in design |

|---|---|

| What it is | Used to report specified foreign financial assets. |

| Filing placement | Attached to the taxpayer's annual income tax return. |

| Baseline threshold context | IRS cites aggregate value exceeding $50,000 for certain U.S. taxpayers, with higher thresholds for some filers (including joint filers and taxpayers residing abroad). |

| Applicability timing | Reporting applies to taxable years starting after March 18, 2010. |

| Return-required condition | If no income tax return is required for the year, Form 8938 is not required. |

| Entity scope expansion | IRS notes applicability for certain specified domestic entities for tax years beginning after December 31, 2015. |

For architecture, retain holder or entity classification, jurisdiction context, account relationship facts, and balance history in exportable form. Treat FATCA, Intergovernmental Agreement (IGA) context, FBAR, and Form 1099 as downstream review signal points that need traceable data from day one.

Step 3. Produce an evidence pack for every decision#

Require an evidence pack for each hold and release: masked tax profile artifacts, policy decision logs, AML review records, and an exportable audit trail tied to the decision event. Each record should include timestamp, actor or service, rule version, linked case ID, and affected ledger entries.

Run a blocked-payout drill and ask ops to produce the full packet without engineering help. If they cannot, the architecture is not production-ready.

Related: FATCA Compliance for Marketplace Platforms: Identifying and Reporting Foreign Account Holders.

Common failure modes and how to recover fast#

Recovering fast starts with containment: stop expanding uncertainty, document what is known, and assign owners before you change flows.

| Failure mode | Grounded response |

|---|---|

| Balance drift between internal views and recorded obligations | Treat the mismatch as an incident, establish a single reconciled baseline, and avoid widening the affected flow until that baseline is clear |

| Unclear ownership between a platform and an Intermediary | Keep a written chain of responsibility with named control owners and evidence artifacts |

| Tax-profile gaps hidden inside broad compliance statuses | Make status visibility and remediation ownership explicit so operators can distinguish tax issues from other compliance issues |

| Launch decisions relying on unsettled interpretations or non-binding materials | Narrow operational scope and document assumptions before broadening exposure |

Step 1 Contain balance mismatches before scaling activity#

A common failure mode is balance drift between internal views and recorded obligations. Treat any mismatch as an incident, establish a single reconciled baseline, and avoid widening the affected flow until that baseline is clear. Fixing only a surface view without resolving underlying records usually creates repeat reconciliation work.

Step 2 Remove AML responsibility ambiguity across entities#

Another frequent break is unclear ownership between a platform and an Intermediary. The 2026 National Money Laundering Risk Assessment reinforces that AML risk spans multiple categories of financial institutions and related entities, including Money Services Businesses (MSBs) and broker-dealers or investment advisers, so ownership cannot stay implicit. Keep a written chain of responsibility with named control owners and evidence artifacts.

Step 3 Surface tax-readiness gaps as explicit operational blocks#

Tax-profile gaps often hide inside broad compliance statuses and then appear late in payout operations. If your flow uses W-8/W-9 data, make status visibility and remediation ownership explicit so operators can distinguish tax issues from other compliance issues. Ambiguous "verified" states are the pattern to remove.

Step 4 Tighten scope when legal posture is unsettled#

Overexpansion risk rises when launch decisions rely on unsettled interpretations or non-binding materials. SEC submissions and comment letters can inform analysis, but they are not substitutes for existing law; for example, the January 12, 2026 POLARIS 3.0 submission states it is not an alternative to U.S. securities laws. When posture is unclear, narrow operational scope and document assumptions before you broaden exposure.

For a step-by-step walkthrough, see How Platforms Use Pooled Wallets vs. Individual Wallets for Contractors.

Conclusion#

Use an omnibus model only if your controls are stronger than your launch pressure. If attribution, reconciliation, or role ownership is still fuzzy, stop. Choose the simpler path or delay release.

Step 1. Confirm the model choice in writing#

Do not let "Omnibus account" or "Segregated account" stay as a verbal preference. Write the decision criteria you actually used: who holds funds, how contractor entitlements are attributed, what external statements you will reconcile against, and what breaks if a provider event arrives twice. A good verification point is simple: someone outside the build team should be able to read the memo and explain the ownership boundary without guessing.

Step 2. Assign named owners for controls that cannot float#

You need one owner each for AML, KYC or KYB review, hold and release decisions, and escalations across the platform, any Intermediary, and any Sub-custodian in the chain. The failure mode here is familiar. Everyone assumes screening or monitoring is "handled elsewhere," then no one can show the contract clause, policy, or queue that proves it. If a control has no named owner and no evidence artifact, treat that as a no-go item.

Step 3. Make the ledger the truth before you expose balances#

Your ledger postings should be replay-safe and idempotent before wallet balances go live. Verify three links in order: provider statement to internal ledger, ledger to wallet projection, and payout outcome back to ledger. If duplicate webhook delivery can create duplicate contractor value, or if returns and reversals cannot be traced to the original event reference, pooling funds will hide errors until they become payout disputes.

Step 4. Gate release on compliance and tax evidence, not intent#

Keep an artifact list for tax and compliance context where applicable, but do not assume one universal rule covers every filer or corridor.

One concrete checkpoint from the IRS side is Form 8938. It is used to report specified foreign financial assets when value is more than the applicable threshold, and it is attached to the taxpayer's return. If your review touches U.S. reporting signals, capture whether Form 8938 is relevant and whether the filer is a specified person (a specified individual or a specified domestic entity).

Do not flatten the thresholds into one number. IRS materials note a $50,000 trigger for certain U.S. taxpayers, but they also say higher thresholds can apply. Certain specified domestic entities have instruction-level tests such as more than $50,000 on the last day of the tax year or more than $75,000 at any time during the year. Just as important, if no income tax return is required for that year, Form 8938 is not required. Required Form 8938 filers also do not report certain accounts maintained by listed U.S. or branch institutions.

Step 5. Test recovery before launch#

Run a live-fire drill for returns, reversals, and unmatched deposits. The test passes only if ops can freeze release, identify the affected contractors, replay journals cleanly, and produce the decision record that explains what happened. If you cannot do that on demand, your design is not ready for scale.

Frequently Asked Questions

What is omnibus account architecture for contractor platforms in plain terms?

The ICI intermediary guide includes a section titled "11 Omnibus Accounts", and that same publication says it should not be construed as legal advice. For a full plain-language architecture definition, consult the relevant authority or a qualified adviser.

Is an omnibus account the same thing as a segregated account?

The provided materials do not supply an explicit omnibus-versus-segregated definition, so this section cannot reliably treat them as equivalent or non-equivalent based on label alone.

Who is responsible for AML obligations when multiple parties are in the chain?

AML responsibility across platform, intermediary, or sub-custodian roles should be taken from governing contracts, policies, and applicable law.

When should a platform avoid an omnibus model entirely?

This section does not provide a bright-line rule for when omnibus should be avoided entirely. It does support one guardrail: do not rely on unofficial or secondary materials as if they were binding authority. For example, the FederalRegister.gov XML rendition of the SEC item dated 03/09/2023 says it "does not provide legal notice to the public or judicial notice to the courts."

What controls must exist before launching omnibus-based contractor balances?

The excerpts here do not specify a definitive required-control checklist. They do support using official publications and signed program documents as the decision basis, and they also make clear that the ICI paper is not legal advice.

How do VBA credits, returns, and holds affect omnibus ledger design?

For VBA credit, return, and hold mechanics, confirm the applicable operational rules with the relevant authority or your payment processor.

Which tax and reporting artifacts should be ready before payout scale-up?

For jurisdiction-specific tax or reporting artifact requirements, confirm with the relevant authority. For date-checking sanctions or license assumptions: OFAC states GL 128B expires on April 29, 2026, and GL 131D extends an existing authorization until May 1, 2026.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bsaefiling.fincen.gov/docs/XMLUserGuide_FinCENFBAR.pdftrusted

- comptroller.war.gov/portals/45/documents/fmr/volume_02b.pdftrusted

- ecfr.gov/current/title-38/chapter-I/part-1trusted

- federalreserve.gov/econres/notes/feds-notes/money-market-fund-r...trusted

- fincen.gov/reporting-maximum-account-valuetrusted

- fincen.gov/report-foreign-bank-and-financial-accountstrusted

- home.treasury.gov/system/files/246/2026-NMLRA.pdftrusted

- irs.gov/businesses/corporations/do-i-need-to-file-fo...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How Platforms Hold and Segregate Client Funds with Omnibus Accounts

Most platform teams should start with the lightest structure they can prove. Choosing between an omnibus structure and deeper segregation is not just a naming exercise. For most platform teams, **omnibus account platform fund segregation** is really a decision about ownership visibility, the control work your team can sustain, and how much launch friction you can absorb.

Paying Unbanked Contractors in Developing Markets: Best Payout Routes for Platforms

If your team needs to send money to contractors, creators, freelancers, marketplace sellers, or other non-payroll recipients across borders, the payout decision can look deceptively simple at first. On paper, you are choosing a payment rail. In practice, you are choosing an operating model that affects onboarding, compliance, support load, engineering effort, treasury visibility, failure recovery, and the degree of legal risk your company is willing to carry.

FATCA Compliance for Marketplace Platforms: Identifying and Reporting Foreign Account Holders

For marketplace teams handling cross-border payouts, FATCA work is mostly a control-design problem. You need to decide what to implement first, what evidence to keep, and what to escalate before a payout creates avoidable reporting or withholding risk. The practical question is not whether FATCA exists, but which controls actually reduce reporting errors and potential 30% withholding outcomes.