Quick Answer

Map marketplace payment flow as one chain from checkout to seller receipt, with explicit pay-in, payout, refund, and release states. Define the transaction boundary, anchor the design to the core transaction, assign one owner per checkpoint, and separate support-visible statuses from finance-visible records. Before launch, test ledger rules, reconciliation, retries, holds, and failure handling.

How money moves from buyer to seller#

Treat your payment design as one continuous chain, not three disconnected diagrams. The job is to map transaction states across payment collection, payout, and refunds, then test cost, controls, and recovery before launch.

Step 1 Define the transaction boundary you actually own#

A marketplace is a dual-user platform, so your design is not just checkout. It also has to cover payment collection, payout, refunds, and confirming whether the order actually closed.

Start with one plain question: where does your responsibility begin, and what counts as done? Pick one finish line for the map first, or the rest of the design will drift.

Step 2 Anchor the design in the core value unit first#

Start with the clearest unit of value, then expand into adjacent monetization layers. That keeps payment design tied to the real transaction instead of turning into disconnected fee rules and exception handling.

Marketplace monetization can grow into a stack, but adding revenue mechanics too early creates clutter and trust risk. If your team is debating commission rules, split logic, payout timing, and buyer protection all at once, pause. Define the core transaction first: what is the order, when is it complete, and what event justifies releasing funds?

Step 3 Map handoffs as explicit states#

Payment collection, payout, and refund handling are connected but distinct, so map the handoffs as explicit states. Use one verification rule from the start: every material state should have both a support-visible status and a finance-visible record.

A practical checkpoint is simple: can you prove whether the order actually closed? If not, your release decision is still ambiguous.

Step 4 Gather the evidence pack before promising speed#

Do not promise faster disbursement until you know which records are required to support it. That can include seller payment account details, identity documentation artifacts, and commercial register details where applicable.

Run this review with product, engineering, finance, and ops in the same session. If any team cannot explain how refunds, disputes, or payout readiness change transaction state, the design is not ready yet.

Set your design objective before touching a flowchart#

Pick a phase-one objective before you draw the flow. Payment processing spans authorization, clearing, and settlement across multiple parties, so trying to optimize speed, cost, control, and support simplicity at the same time usually creates conflicting logic.

Step 1 Pick one primary outcome#

Choose a single primary goal for version one: lower unit cost, faster seller disbursement, stronger control posture, or fewer support tickets. Keep the other goals visible, but do not let them outrank the primary one.

Use one decision test: if a transaction has passed Capture but still looks ambiguous, what wins first? If you release funds, you are optimizing payout speed. If you wait for records and checks to align, you are optimizing control. Write that choice as one sentence product, finance, and ops all agree to.

Step 2 Write the tradeoff rule in plain language#

Make the tradeoff rule explicit. If trust and risk are the constraint, prioritize stronger verification and matching controls even when payout speed drops.

This matters because authorization, clearing, and settlement are separate steps in a multi-party system, so delays and async state changes can happen. A good test is whether support and finance see the same transaction state when deciding whether funds are ready.

Step 3 Define non-negotiables as internal bounds#

Set internal bounds before design starts: what conditions trigger manual review, what evidence is required before payout release, and who owns each decision. Assign an owner and a measurement method to each bound.

Also make verification standards explicit. If release logic depends on legal or regulatory interpretation, verify against an official edition rather than relying on a prototype display alone, and use the linked official govinfo PDF when available.

For a step-by-step walkthrough, see Net-30 Payment Terms for Platforms: How to Set Vendor Payment Terms Without Killing Contractor Cash Flow.

Prepare the prerequisites and ownership map#

Do not map money movement from memory. Start with the live artifacts, then assign clear ownership to each checkpoint where funds can pause, fail, or be released.

| Artifact | Use in design |

|---|---|

Current Settlement flow | Use the document that reflects production behavior today |

| Active provider or rail operating terms | Use where they apply to reflect current behavior |

| Current buyer and seller state labels | Include if product or support already maintain them |

| Current buyer and seller personas (or equivalent user personas) | Include before deeper flow decisions |

Step 1 Pull the live artifacts#

Use the documents that reflect production behavior today: your current Settlement flow, active provider or rail operating terms where they apply, and current buyer and seller state labels if product or support already maintain them. Include your current buyer and seller personas (or equivalent user personas) before deeper flow decisions.

Treat this as a consistency check before design. Everyone should be working from the same current artifacts, not assumptions.

Step 2 Assign one owner per checkpoint#

Unclear ownership creates delays when a transaction is stuck between states. Assign one decision owner to each checkpoint and document who can make the release call.

Run one quick test: if payout looks ready in one view but blocked in another, who makes the release call? If that answer is unclear, ownership is still incomplete.

Step 3 List policy gates before release logic#

Define policy gates before you design release logic, especially where jurisdiction or provider rules apply. The legal or regulatory framework and safeguards for customer funds should be explicit in your map, not implied.

Depending on your setup, gates can reflect legal obligations, customer-fund safeguards, and risks such as limited transaction-account access or fee pressure. Mark each gate with a reason code so product, support, engineering, and finance can all see the same block reason.

Map the pay-in states from checkout to available funds#

Once ownership is clear, make pay-in states explicit so support, engineering, and finance are reading the same event the same way. A single "paid" label is often too coarse once statuses can change after checkout.

| State | Order | Note |

|---|---|---|

Authorization | 1 | Not usable cash |

Clearing | 2 | Keep distinct from authorization and settlement |

Settlement | 3 | Keep distinct as its own pay-in handoff |

| available funds | 4 | Separate state after settlement |

Step 1 Name the pay-in states in business order#

Name the pay-in chain in operational order, for example: Authorization -> Clearing -> Settlement -> available funds. If your provider uses different labels, keep equivalent boundaries so you still separate buyer intent, provider processing, and settlement availability.

Keep the meanings strict. Authorization is not usable cash. Payment processing is multi-step and includes authorization, clearing, and settlement, so your state map should reflect those handoffs.

Step 2 Mark where status can change after checkout#

Treat checkout success as one event in a longer flow, not final truth by itself. Downstream processing steps can still change the outcome later.

Mark each transition as sync or async, and assign one source-of-truth event to each transition. One failure mode to plan for is an early success event in-product that later changes to failure or pending downstream. Your map should make that boundary obvious so support messaging and finance status stay aligned.

Step 3 Decide what hits the ledger and what stays projected#

Use your Ledger model to separate confirmed movement from projected movement. Set one team rule for which transitions create finance journal entries and which remain operational-only until later confirmation.

In practice, authorization comes before settlement and should be treated as non-final. Post finance-grade entries at the provider-confirmed transition your team trusts, then reflect availability-for-settlement as its own movement state.

Step 4 Verify dual visibility before you move on#

Before you design payout logic, verify that each pay-in state maps to a support-visible status and a documented finance handling rule.

For each state, record the state name, trigger event, request or event ID, provider reference, support label, finance handling note, and owner. Review that map with engineering, finance, and compliance together before you change payout logic.

Map the pay-out states from release decision to seller receipt#

Do not collapse release approval and money movement into one label. Your payout map should separate release approval, transfer initiation, and confirmed Seller disbursement so support and finance are less likely to mark a seller as paid before provider confirmation.

| State | Meaning |

|---|---|

held | Internal balance state until release is clearly logged |

| eligible for release | Keep distinct from release approved |

| release approved | Your platform decided to release funds |

Pay-out flow initiated | Distinct from approval and seller receipt |

| provider confirmation | Separate state before Seller disbursement confirmed |

Seller disbursement confirmed | Do not collapse this with approval or initiation |

Step 1 Separate approval from transfer execution#

Build the pay-out chain in business order, not portal-screen order. Keep labels distinct, for example: eligible for release, release approved, Pay-out flow initiated, provider confirmation, and Seller disbursement confirmed.

Approval means your platform decided to release funds. It does not mean a transfer has started or reached the seller. If those states are collapsed into one label, support, finance, and ops can read the same payout differently.

For each state, record one clear trigger and one owner. At minimum, keep seller ID, payout or batch reference, request or event ID, provider reference, and support-facing status.

Step 2 Define hold logic like a policy, not a feeling#

Make hold logic explicit so payout handling stays consistent across teams. Without that, payout timing can become inconsistent and hard to plan around.

Keep held, ready for payout, and payout initiated as separate states. Treat funds on hold as an internal balance state until release is clearly logged.

Step 3 Model single and batched payouts through the Marketplace payout API#

Map one-off and bulk payout paths before launch, using consistent state meanings. A [Marketplace payout API](https://tipalti.com/blog/marketplace-payouts-api) is a secure, automated connection between your marketplace and bank systems, and payout software can submit bulk payout requests to a provider as volume grows.

As volume rises, manual CSV uploads can become time-consuming and error-prone, and manual payout processes can make cash-flow forecasting less reliable. Automated API submission replaces manual portal uploads with provider-processed bulk transfer requests.

If you are choosing an API style, REST API is the common option, while SOAP API is the older, more structured option.

Step 4 Review hold windows with cross-functional controls#

If seller experience is the bottleneck, review hold policy first, not just messaging. Any hold-policy changes should be coordinated across engineering, finance, and compliance.

Before moving on, verify that every payout state has both a seller-visible status and a finance-visible entry or pending rule. That is what turns a payout diagram into something your team can operate.

Related reading: Payment Volume Forecasting for Platforms: How to Predict Cash Flow.

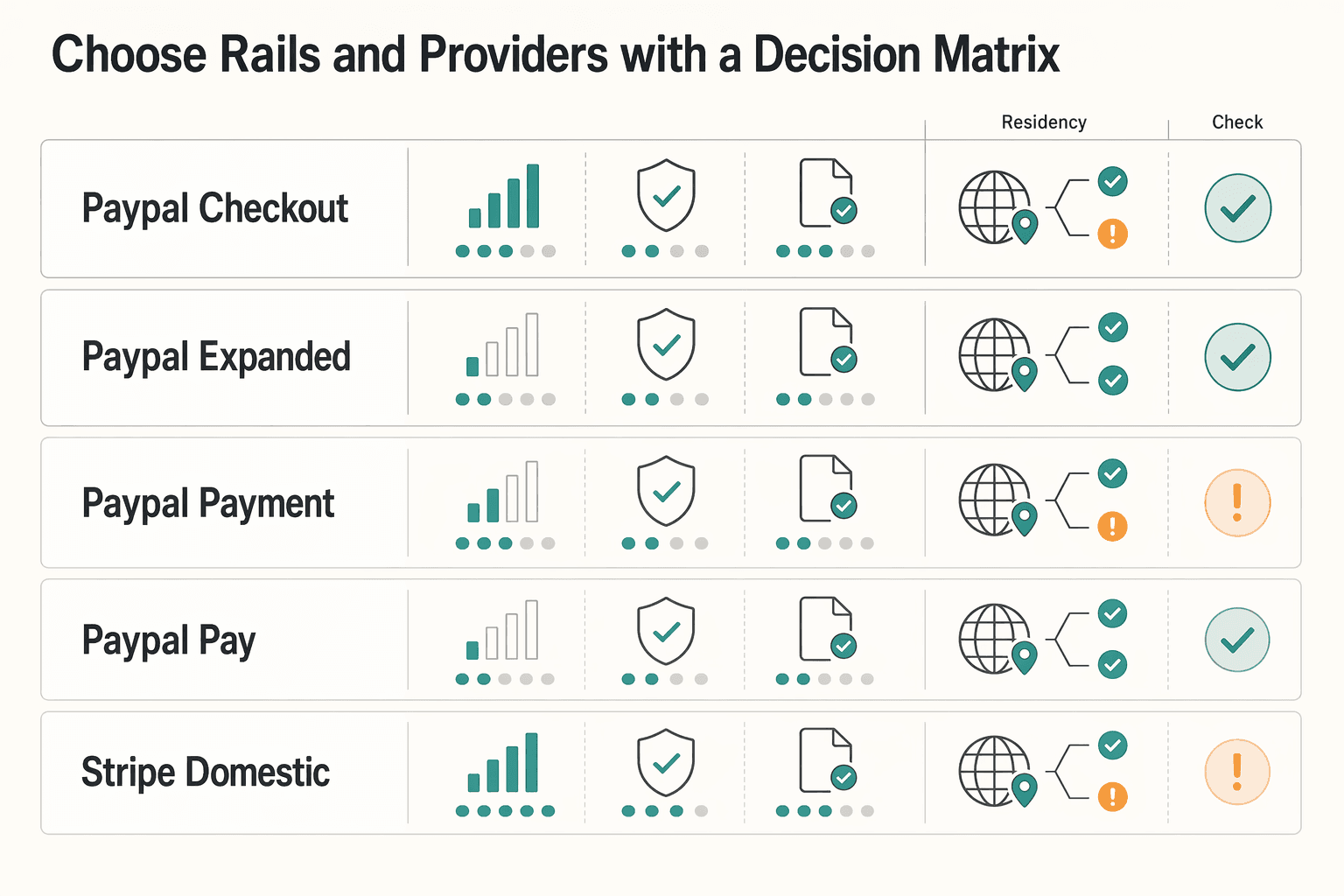

Choose rails and providers with a decision matrix#

Use a weighted decision matrix, not a headline-fee comparison, and lock market scope first so you do not model the wrong economics.

Start with two controls before scoring anything:

- Define

domesticvsinternationalas market residency of sender and receiver, then price each flow separately. - Treat PayPal pricing as market- and product-specific, not universal, and checkpoint the current fee artifact used in your review.

| Path or product view | Price signals currently visible | What this means for your matrix |

|---|---|---|

| PayPal Checkout (credit/debit cards) | 2.99% + $0.49 per transaction | Card path economics depend on the checkout product you choose. |

| PayPal Expanded Checkout (credit/debit cards) | 2.89% + $0.29 per transaction | Keep product-path rows separate. Do not blend into one PayPal rate. |

| PayPal payment option | 3.49% + $0.49 per transaction | Product choice changes margin assumptions. |

| PayPal Pay Later | 4.99% + $0.49 per transaction | Model this as a distinct buyer or payment path. |

| Stripe domestic cards | 2.9% + 30¢ | Baseline card comparator for domestic card transactions. |

| Stripe Instant Bank Payments | 2.6% + 30¢ | Bank-linked paths can price differently from cards. |

| Stripe ACH Direct Debit | 0.8% with $5.00 cap | Include capped-fee behavior in larger-ticket scenarios. |

Then score provider fit against your operating model using the same weights for each provider:

- Onboarding friction: score from your own KYC/KYB workflow tests.

- Payout control depth: mark as

verifyfrom your required controls and release-state needs. - Technical fit (

REST API,SOAP API,Webhookcoverage): mark asverifyuntil confirmed in your own docs review. - Finance fit: settlement assumptions, reversal handling, and close artifacts.

- Reversal-cost handling: for PayPal, explicitly account for

Chargeback Fees,Dispute Fees, and where eligible, Seller Protection impact.

For buyer protection and guarantee design, see Payment Guarantees and Buyer Protection for Platform Operators.

Before finalizing rail mix, run a quick margin sensitivity check with the payment fee comparison calculator so cost tradeoffs are explicit.

Make the ledger and reconciliation layer non-negotiable#

Treat this as an internal control choice, not an external rule. The supplied evidence does not establish a universal ledger doctrine; even adjacent BCT-integrated procurement research shows under-represented theory coverage and limited empirical evidence.

Step 1 Pick the internal record finance will trust#

Decide which internal record is authoritative when processor views, internal balances, and bank activity do not line up. Call it your Ledger model, subledger, or journal store, but make the precedence explicit so product, engineering, and finance resolve state from the same place.

Use a simple test: take one transaction from initiation to disbursement and ask each team to explain its current state from that record alone. If the answer depends on multiple screens, exports, or ad hoc log reading, your control layer is still ambiguous.

Step 2 Define journal granularity before you ship#

Define posting granularity from your own flow map before launch. Decide which events in your lifecycle should be posted separately and which can be summarized, based on the level of review operations and finance require.

Keep this framed as internal policy, not a universal doctrine. The key is that your chosen granularity preserves the economic meaning you need for operations and finance review.

Step 3 Build a traceability chain you can test#

Choose a traceability chain and make it testable end to end. Define the identifiers and records that must link together so operators can follow one event without guesswork.

Validate the chain with sample transactions and confirm that a non-implementing teammate can trace them quickly. If tracing depends on tribal knowledge, your audit path is incomplete.

Step 4 Make reconciliation a defined close control#

Define reconciliation in your own policy, with clear owners, timing, and exception handling. Decide how unmatched events are labeled and handled until the supporting records are in place.

The supplied sources do not provide numeric tolerances or mandated timelines, so set those internally and document them before scale increases.

Engineer retries and event handling so duplicates cannot happen#

Set this as a control objective: retries, redeliveries, and incident replays should resolve one economic intent, not create a second money movement. Apply that standard across both Pay-in flow and Pay-out flow, and align it to your payment model (gateway, PSP, PayFac, wallet, or orchestration), because how deeply you sit in money movement changes technical and compliance scope.

Step 1 Define idempotency policy on money-moving requests#

For money-moving actions, define a consistent [Idempotency](https://newsletter.pragmaticengineer.com/p/designing-a-payment-system) policy instead of handling duplicate prevention only at buyer-facing checkout. Treat key design as an internal intent-mapping choice for your flow.

Keep implementation details such as key format or retention as internal policy, and verify behavior in one narrow corridor first before scaling capabilities. A practical checkpoint is one end-to-end use case from Buyer authorization to Seller disbursement with repeated submissions.

Step 2 Design event handling for safe redelivery and replay#

For Webhook-driven flows, define controls so repeated or delayed events can be handled without unintended extra financial impact. The source material does not establish provider delivery guarantees, so replay and redelivery behavior should be explicitly specified and tested in your own system.

Do not rely on a single check as universal correctness. Where sequence matters to business meaning, preserve that sequence in your own control logic and replay tests.

Step 3 Add stale-state guardrails before funds move#

Before funds move, reject operations when required prerequisites are no longer current instead of trying to recover after movement has started. Define these prerequisite checks in your own control policy.

In pay-in paths, keep required protections in force, including tokenization and explicit user consent where they apply.

Step 4 Make incident replay follow the same controlled path#

Manual replay should follow the same control path as automated processing, with the same intent checks and posting rules. Avoid separate force paths that bypass normal controls.

Record the replay decision trail so teams can confirm whether the action should return an existing outcome, progress a blocked state, or require explicit approval for a new economic event.

Model real margin after every fee and reversal#

Do not model margin from headline take rate. Model it by money state, or you may overstate what the platform keeps after fees, failed transfers, Refund, and Dispute activity.

The same control mindset applies here. One buyer payment moves through multiple states before it becomes real platform margin.

Step 1 Break economics into observable buckets#

Start at gross payment, then split deductions into separate lines. Keep processor charges, Payment gateway costs, payout costs, refund or chargeback leakage, and ops overhead separate from Platform commission.

Two items matter early. Actual commission retention depends on commission deduction logic, split payment behavior, and vendor-specific commission structures. Payout cost also includes failed-transfer handling, because fallback or retry work can create manual review and support overhead.

Step 2 Show margin by state, not headline rate#

Use a shared state view that finance, product, and engineering all interpret the same way:

| Margin state | Include | Common modeling error |

|---|---|---|

| Gross payment | Buyer payment amount in scope | Treating an early money state as final margin |

Net after Platform commission mechanics | Commission retained after split logic and payment costs | Using headline commission and ignoring deduction logic |

| Net after payout | Payout costs plus failed-transfer handling | Assuming seller transfers always succeed on the first try |

Net after Refund and Dispute | Reversals plus related ops overhead | Treating reversals as one-off noise |

This is where the map becomes economically useful. Architecture choices such as who holds funds and who carries failure liability change where the margin impact lands.

Step 3 Check payout-timing sensitivity before fee renegotiation#

If margin changes sharply when payout timing changes, review settlement and hold policy before renegotiating headline fees.

Test holding periods for escrow, payout cadence, and release rules against reversal exposure. Faster release can increase Refund or Dispute exposure for the platform after funds are out. If timing sensitivity is high, release policy is a practical lever to test early.

Also treat failed transfers and reversals as unit-economics signals when they trigger manual correction work. Those choices can show up in seller NPS, support queues, and roadmap speed.

Step 4 Verify monthly with Reconciliation outputs#

Run a monthly modeled-versus-actual take-rate check using close outputs and exception logs.

Focus on two drift patterns: structural drift, where modeled retention differs from actual split and commission outcomes, and leakage drift, where modeled reversal or retry cost is below what exception logs show. When drift appears, fix the state model first, then decide whether changes belong in pricing, hold policy, gateway configuration, or payout operations.

For cash flow timing and reconciliation tradeoffs, see How Payment Platforms Use DPO to Improve Cash Flow Without Reconciliation Risk.

Design failure handling before launch day#

Decide ownership before launch. When payouts rely on manual weekly uploads, operations can become time-consuming and error-prone as volume grows.

A Marketplace payout API can reduce manual effort and improve payment consistency, but successful implementation still depends on clear planning across developers, finance, and compliance.

Step 1 Name the payout incident labels you will operate#

Define your internal incident labels up front so everyone uses the same language and next-action logic. For each label, assign a primary owner before launch, document what must be captured for review, and write the next action and escalation path.

Step 2 Pair each label with owner, evidence, and handoff#

For each label, document three things: first responder, required evidence, and the event that marks the case resolved. Build this record jointly across developers, finance, and compliance.

Use a standard incident evidence pack in your payout stack, including payout request details, amount, batch context for bulk payouts, and current provider processing status. If you cannot trace a request through processing and internal records, fix that gap before launch.

Step 3 Define recovery paths in the payout stack#

Write recovery paths so teams can execute them without interpretation. In bulk payout workflows, define how exceptions are reviewed and handed off when outcomes are inconsistent.

Design this process to scale with volume, not just launch-day volume.

Step 4 Run a cross-functional launch check#

Before launch, run a joint check with developers, finance, and compliance to confirm ownership, evidence requirements, and handoffs are clear for each incident label.

If the same incident would still be handled differently across teams, tighten the plan before launch.

Related: How to Calculate LTV for a Two-Sided Marketplace: Buyer LTV Seller LTV and Platform LTV.

Run launch checks and first-scale checkpoints#

Start with design scope before go-live, then validate that the same payment event maps to one intended ledger outcome, including replayed or duplicate delivery paths. This helps surface gaps before they spill into support and finance.

Step 1 Validate state coverage before launch#

Check both the Pay-in flow and Pay-out flow state by state. Confirm, for each state, the owner, trigger, ledger posting, buyer- or seller-visible status, and terminal condition.

Then run replay and Idempotency checks on repeated pay-in requests, repeated payout requests, and repeated Webhook events. Aim for one intended money result, one journal sequence, and no duplicate payout or duplicate status transition.

Step 2 Watch early operations for operational cracks#

In the first phase after launch, track failed Webhook deliveries, manual payout interventions, and close breaks. These can signal timing gaps, missing references, and stale-state handling.

For each exception, keep the same evidence pack: internal request ID, provider reference, seller ID, amount, current internal state, and latest provider event or status. If those fields are fragmented across tools, you are taking on integration debt and data silos. Move toward a single system, contract, and support relationship where possible.

Step 3 Re-tune after launch using real operating data#

After launch, re-evaluate rail mix, Pay by Bank vs card, hold policy, and payout cadence using your own dispute, support, and exception data. Make changes where your actual case patterns justify them, not where launch assumptions suggested them.

Also verify the full chain from buyer payment to seller payout in your AR view, and tighten gaps with finance using tracking buyer payments through to seller disbursement. For recurring billing models, confirm buyer charge cycles and seller payout cycles still align after these adjustments.

For recurring payment cycles, see Recurring Billing for Marketplaces: How to Charge Buyers and Pay Sellers on the Same Cycle.

Conclusion#

Launch only when your transaction flow, controls, and failure handling are testable and traceable at close. The design that wins is not the prettiest diagram. It is the one product, engineering, finance, and ops can all read the same way under normal volume and under stress.

- Freeze the version you are actually launching. Treat phase one like a marketplace MVP, not a scale exercise. Keep scope on essential buyer-seller flows and secure payment integration, with transaction security, user data protection, and compliance handled from the start. If edge features are still in debate while core transaction states are unsettled, cut scope and stabilize the flow first.

- Validate each transaction state with evidence, not assumptions. Review your launch flow line by line. For every state, confirm who owns it, what proves it happened, and where it appears in your records. A practical check: support can explain the customer status, finance can trace the matching transaction record, and engineering can safely re-run handling when needed.

- Break the flow before users do. Run replay and failure-path tests across the core transaction flow, including payment failures and exception cases. A visible fix is not enough if finance is left with an unreconciled break. If escalation paths and exception-closing evidence are not written down, your team will rely on memory under pressure.

- Document the launch tradeoffs you chose. Do not leave payment and workflow decisions as informal preferences. Record the risk, speed, and operational tradeoffs you accepted for launch and tie them to the constraint you are solving. Transaction-flow design affects how well your marketplace matches supply and demand, and weak flow choices can surface as buyer drop-off.

Use the checklist only after you freeze the launch version, because a checklist without a frozen flow still leaves ambiguity in the handoff.

- Core transaction states are explicitly mapped with owners.

- Every money movement is traceable in records used by support, finance, and ops.

- Replay and failure-path tests are passing for core payment events.

- Launch tradeoffs are documented with clear risk-speed-operational rationale.

- Failure handling includes clear escalation paths and exception-closing evidence.

If you want to move this design into production with controlled disbursements and retry-safe execution, review Gruv Payouts for compliance-gated payout workflows and batch operations where enabled.

Frequently Asked Questions

What is the exact sequence of a marketplace payment flow from buyer payment to seller payout?

There is no universal sequence you can copy as-is. Define your scope early, anchor the map to the core transaction, and document the full path from payment collection through payout, refunds, and confirmed order close for your own marketplace. Pressure-test that sequence against failure points such as checkout drop-off.

What is the practical difference between `Pay-in flow` and `Pay-out flow` ownership?

The article does not give one canonical ownership split. It recommends making the split explicit, assigning one owner per checkpoint, and documenting who can make the release call. If ownership is vague, handoffs can fail even when the flowchart looks complete.

Which costs sit outside headline processor fees in a real `Settlement flow`?

Do not assume the headline processor fee is the whole picture. The article says marketplace monetization can include multiple streams and that margin should also reflect payout costs, failed-transfer handling, refund or chargeback leakage, and ops overhead. Build the full cost and revenue view explicitly for your own marketplace.

When should a platform hold funds before `Seller disbursement`?

There is no universal hold rule or timing threshold in the article. It recommends setting hold and release policy inside your design scope and keeping held, ready for payout, and payout initiated as separate states. Document the rule clearly so product, operations, and finance use the same standard.

How do `Refund` and `Dispute` events change platform margin and reconciliation?

The article does not give quantified effects for refunds and disputes. It advises modeling margin by money state, not headline take rate, and tracking reversals plus related ops overhead as a separate state. Then verify modeled versus actual results monthly with reconciliation outputs and exception logs.

What minimum controls should exist before payout release for compliance and audit readiness?

The article does not provide a legal or universal minimum checklist. It recommends defining payout-release controls explicitly, assigning clear ownership, and setting evidence requirements before funds are released. If those controls are not written down, readiness is uncertain.

How should teams implement `Idempotency` and `Webhook` retries to prevent duplicate payouts?

The article does not prescribe key design, retry counts, or ordering policy. It says teams should define these as implementation choices, apply them to money-moving requests, and test replay and redelivery so one economic intent cannot create a second movement. Manual replay should follow the same controlled path as automated processing.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bis.org/cpmi/publ/d144.pdftrusted

- bisbeeaz.gov/DocumentCenter/View/8472/City-Code-Updated-M...trusted

- columbia.edu/~ak472/papers/coursepack.6386.s06.pdftrusted

- farmingdale.edu/courses/index.shtmltrusted

- federalregister.gov/documents/2024/11/15/2024-25534/negative-opt...trusted

- hbs.edu/ris/Publication%20Files/22-050_ec28aaca-2b94...trusted

- hks.harvard.edu/sites/default/files/centers/mrcbg/Final_AWP_...trusted

- housing.nv.gov/uploadedfiles/housingnvgov/Content/Public/20...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: