Quick Answer

A marketplace AR cycle should track buyer collection and seller disbursement as separate timelines, with the ledger as the source of truth. Define provable states from obligation created through funds cleared, hold, release, payout initiated, and payout settled. Do not treat buyer payment as payout-ready. Require provider references, timestamps, journal entries, and reconciliation at transaction, batch, and close levels.

How the accounts receivable cycle works in a marketplace#

Treat this as an operating problem, not a theory lesson. This guide covers the marketplace AR cycle from buyer payment collection through seller disbursement: money owed, collected, cleared, held when required, and released under your payout rules.

Step 1. Set scope before mapping the flow. Accounts receivable is money owed for goods or services already provided, but marketplace AR runs on two clocks. Buyer collection and seller transfer are often separate events. A buyer charge can be decoupled from seller transfers, and one payment can be split across multiple recipients. So this guide stays focused on post-sale money movement and accounting evidence, not generic invoicing theory or broad revenue-recognition topics.

The main operating rule is simple: do not treat "paid by buyer" as "ready to disburse." Some programs disburse only after customer funds are collected, and payout availability can still be delayed by holds or reserves. If your reporting collapses those into one status, separate them first so you do not waste time on false "missing payout" investigations.

Step 2. Build controls operators can use daily. The target is clear checkpoints, explicit failure branches, and reconciliation controls that keep working at scale. Finance, Ops, and Product need the same underlying truth in different forms: a reliable close, an explainable payout timeline, and state logic that can actually be implemented.

A checkpoint needs evidence, not just a dashboard label. At minimum, each material state change should tie to a provider reference, a timestamp, and the journal entry posted to the ledger. Journal entries are the building blocks of the accounting record, and the general ledger is the master record that summarizes transactions across the entity. If the dashboard and the ledger disagree, explain the dashboard against ledger evidence.

A practical test is to start from one seller payout and trace it to the payout batch, then to the included payments, refunds, and chargebacks, and then back to the posted journal entries. If you cannot do that, you do not yet have end-to-end traceability.

Step 3. Keep the ledger authoritative and make policy gates explicit. Throughout the rest of this article, keep one stance: treat the ledger as the accounting source of truth, keep flow states traceable end to end, and make release gates explicit wherever the program supports them. Payout reconciliation and settlement reconciliation views help match bank payouts to underlying batches and break out payments, refunds, and chargebacks at payout level.

That keeps timing assumptions honest. Automatic payout setups can preserve the link between transactions and payouts, which makes reconciliation and failure handling cleaner. You can then distinguish funds cleared, funds held, payout initiated, and bank arrival as separate states.

In some programs, funds become available about 1-2 days after buyer payment confirmation. In other programs, bank arrival after disbursement can take about 1-2 business days. One timestamp is not enough to explain payout status.

From here, define each state precisely and make each one provable.

Related: What is 'Working Capital Management'?.

Define the marketplace AR cycle before you change any process#

Define your cycle first, or your process changes will optimize the wrong thing. In a marketplace, buyer collection and seller disbursement often run on different clocks, so classic AR definitions explain only part of what your ledger needs to show.

Step 1 Separate classic AR from marketplace settlement#

Use classic AR definitions as a boundary, not your full operating model. Taulia defines AR from credit order to full payment receipt, and Tipalti frames completion at invoice settlement. That works for buyer-side collection, but it does not fully describe marketplace payout flow.

Marketplace settlement can be multi-stage: funds are processed, split between platform and users, then held until payout. So "buyer paid" can be true while seller disbursement is still pending.

Step 2 Name the minimum states your team will enforce#

Keep the state list short and make every state provable across Finance, Ops, and Product. The goal is shared operational meaning, not a universal taxonomy.

| State | What it means in practice | Verify with |

|---|---|---|

| Obligation created | Sale or charge creates a buyer receivable or payment claim | order ID, invoice/payment reference, ledger posting |

| Collection initiated | You attempted or requested collection | processor reference, initiation timestamp |

| Funds cleared | Money is no longer just authorized or pending | settlement event, balance update, cleared timestamp |

| Liability recognized | Seller amount is owed under your rules | journal entry to seller payable or similar liability account |

| Payout eligible | Hold window and policy gates are satisfied | reserve check, cutoff date, eligibility flag |

| Disbursed | Payout instruction has been sent | payout batch ID, provider payout reference |

| Exception | Normal release path broke | failure code, reason, owner |

Operational check: trace one seller payout through every state with a timestamp and source record. If you cannot prove why it became payout-eligible, your state model is incomplete.

Step 3 Test liquidity impact before changing cadence#

Do not use AR timing alone as your liquidity view. CCC tracks how long cash is tied up before it becomes available again, while seller cash-out timing is also shaped by payout cadence and hold rules.

Platform rules make that tradeoff visible. Shopify supports daily, weekly, or monthly payout schedules, and Amazon documents a standard DD+7 reserve period to help cover refunds, claims, or chargebacks. So faster buyer collection can coexist with slower seller cash-out if hold policy stays unchanged. Treat that as a deliberate design choice, not a reporting anomaly.

If billing cadence is part of your receivables process, Recurring Billing for Marketplaces: How to Charge Buyers and Pay Sellers on the Same Cycle shows how to align buyer charges and seller payouts on the same schedule.

Gather prerequisites and assign owners before rollout#

Before rollout, make every state provable. Use the ledger and journal entry stream as your source of truth, and use dashboards for projection and monitoring.

Step 1 Anchor truth in ledger-backed records#

Reconciliation should close from ledger-backed records, not dashboard-only totals. The general ledger underpins your accounting record, so buyer collection and seller disbursement reporting should tie back to ledger balances and journal entries.

Use a three-way match by default: internal order data, PSP or provider transaction data, and bank data. If you have a collections and disbursement dashboard, use it to spot timing gaps and exceptions, but do not treat it as the book of record. A practical control is to sample one completed payout batch and trace it to transaction IDs, related journal entries, and the bank movement that confirms settlement.

Choose payout controls with your eyes open. Automatic payouts preserve transaction-to-payout linkage and usually make tracing easier. Manual payout timing and amounts increase reconciliation effort because the linkage is less explicit.

Step 2 Publish the operating artifacts before the first live cycle#

Do not launch until payout timing and exception handling are documented in operating artifacts the team can execute. At minimum, publish:

- a payout calendar with cadence and bank-holiday handling

- versioned settlement cutoff rules, including whether timing is business-day based

- clear exception-queue ownership and escalation paths

Document cutoff logic with examples, not assumptions. Business-day rules change real payout timing when weekends or holidays intervene, and weekly or monthly schedules need explicit initiation-day and clearing expectations. If reserve or hold policy affects availability, include it in the same packet so your "payout eligible" state stays defensible.

Step 3 Split duties and handoffs before incidents force the issue#

Set ownership boundaries before go-live, then test them with incident scenarios. The baseline control is segregation of duties: initiation, authorization, recording, and reconciliation should not all sit with one person.

| Team | Responsibilities |

|---|---|

| Finance Ops | ledger impact; reconciliation review; payout approval policy |

| Payments Ops | payment operations; payout execution; exception handling |

| Product | state definitions; event generation; incident tooling and visibility |

Capture this in a simple responsibility matrix. For each activity, name who initiates, approves, reviews, and reconciles, then run a tabletop for a failed disbursement and confirm the handoffs are unambiguous. Handoff ambiguity can cascade into cash-flow problems during rollout.

For a collection-efficiency view of the same flow, see Accounts Receivable Turnover for Platforms to Measure Collection Efficiency.

Map statuses from buyer payment to seller disbursement#

Build the status map so anyone can answer two questions quickly: why funds are not yet payable, and why a payout amount changed. If a status cannot be traced to provider evidence, ledger evidence, and time, investigations drag.

Step 1 Define one internal state table with clear entry and exit rules#

Use one internal table across Finance Ops, Payments Ops, and Product, then map provider events into it.

| State | Enter when | Exit when | What to watch |

|---|---|---|---|

| Authorization | Provider confirms funds are reserved on the buyer payment method | Capture succeeds, or authorization expires/cancels | In manual-capture flows, monitor expiry; Stripe notes expired authorizations release funds and can move payment to canceled |

| Capture | Provider confirms the charge was captured | Funds move into settlement/clearing or fail/reverse | Captured is stronger than authorized, but not yet the same as payable cash |

| Clearing | Funds are included in provider settlement processing | Funds post to the balance you treat as clear enough for hold/release logic | Adyen's sales day is a 24-hour period, so clearing should follow settlement timing, not order time |

| Hold | Funds are restricted under your reserve hold policy | Hold expires, risk clears, or funds are consumed by refund/dispute handling | Keep hold separate from payment failure states |

| Release | Funds become payout-eligible after hold and cutoff rules pass | Payout is created or funds are re-restricted by a later adjustment | Do not treat release as paid out |

| Payout initiated | A payout instruction is created with the provider | Payout is credited/paid, returned, failed, or canceled | Stripe payouts start as pending; Adyen exposes Payout initiated and related payout webhooks |

| Payout settled | Provider marks payout as paid/credited and, if tracked, bank movement confirms settlement | Final state unless return/reversal handling applies | eBay notes banks may take an additional 1-3 days after initiation to make funds available |

| Failed payout | Provider reports failed, returned, or canceled payout | Recreated payout succeeds or case closes with funds re-credited internally | Keep this explicit; AWS Marketplace reporting includes failed disbursement paths |

Step 2 Require trace evidence for each status transition#

For each transition in your internal model, capture the provider reference and timestamp, plus internal evidence such as a ledger link or actor or system source when available. Keep status history append-only, and store both the raw provider state and your normalized internal state so outcomes stay explainable across providers.

Step 3 Keep timing windows separate#

Track three windows separately because they answer different operating questions:

- payment processing window: authorization, capture, clearing

- hold window: reserve hold policy

- payout execution window: platform payout schedule

Do not collapse them into one "available on" date. Shopify's payout cadence can be daily, weekly, or monthly, and weekends and holidays do not count toward settlement timing. Its Friday day-0 to Wednesday day-3 example shows why business-day logic needs to be explicit. Use separate fields such as captured_at, cleared_at, hold_started_at, hold_released_at, payout_initiated_at, and payout_settled_at.

Step 4 Add explicit branches for refunds and tax adjustments#

Build refund and tax adjustment branches into the model so disbursement math is auditable, not just gross-payment based. AWS Marketplace notes disbursements can include customer payments, settled subscription refunds, and some taxes collected or refunded to customers. Model those as separate adjustment events linked to the original commercial record so payout deltas are explainable without manual reconstruction.

Set payout cadence and cutoff rules with explicit tradeoffs#

Set payout cadence as a policy layered on top of release logic, not a substitute for it. Faster schedules work best when eligibility rules are strict enough to block unsettled, reserved, or adjustment-prone funds.

Step 1 Anchor cadence to release rules, not order time#

Define one hard payout-eligibility checkpoint. A balance should be payable only after it clears your processing window, passes settlement cutoff, and is outside reserve and active adjustment paths. In practice, check cleared status, reserve release status, and adjustment flags, not just capture time.

If refund or dispute volatility is high, keep a longer processing window and a stricter cutoff before release. That does not guarantee lower losses, but it can reduce the chance of paying out funds that are about to be reduced. Amazon's mechanics show the pattern: scheduled payout follows settlement-group close, and standard delivery-date reserve can hold funds to DD+7.

Before go-live, sample one payout batch and confirm every line has provider evidence, ledger evidence, and a valid eligibility reason.

Step 2 Choose cadence by failure cost, not preference alone#

Choose cadence based on failure cost: reconciliation effort, exception handling, and recovery work after adjustments.

| Cadence option | Usually fits when | Main upside | Main tradeoff | Grounding pattern |

|---|---|---|---|---|

| Daily | Lower volatility and strong eligibility checks | Faster access to released funds | More payout events to reconcile | Shopify supports daily payouts; eBay supports daily and on-demand requests |

| Weekly | Moderate volatility or leaner ops capacity | Fewer payout runs and cleaner review windows | Longer interval between payout runs | eBay supports weekly scheduling; Amazon scheduled disbursement follows settlement-group closure |

| Custom or longer window | Higher adjustment volatility or reserve-heavy flows | More time for refunds, claims, and settlement timing to resolve | Longer gap between earned and payable funds | Amazon DD+7 and account-level reserves show why longer release logic may be required |

If you shorten cadence for commercial reasons, document post-payout adjustment handling up front so recovery and support work is planned instead of reactive.

Step 3 Ground seller expectations in real payout timing behavior#

Frequency labels are not enough. Define payout promises with cutoff and bank-lag detail.

| Platform | Payout pattern | Timing notes | Adjustment or limit |

|---|---|---|---|

| Shopify | daily, weekly, and monthly schedules | schedule changes can delay pending payouts to the next eligible date; Friday-Sunday captures are grouped into one payout batch | refunds and chargebacks can settle faster than charges and reduce payout totals |

| eBay | daily, weekly, biweekly, and monthly schedules; on-demand payout requests | funds generally become available within 2 days after buyer payment confirmation; banks generally add another 1-3 days after payout initiation | selling costs and fees are deducted before payout; refunds can be funded from available or processing balances or linked accounts when balances are insufficient |

| Amazon | scheduled disbursement follows settlement-group closure; Disburse on Demand is limited to once every 24 hours | funds can remain in settlement groups, DD+7 delivery-date reserve, or account-level reserve | if disbursement fails, funds carry into the next settlement period |

Shopify supports daily, weekly, and monthly schedules, but schedule changes can delay pending payouts to the next eligible date. It groups Friday-Sunday captures into one payout batch and notes that refunds and chargebacks can settle faster than charges, reducing payout totals.

eBay generally makes funds available within 2 days after buyer payment confirmation. It supports daily, weekly, biweekly, and monthly schedules, and allows on-demand payout requests. After payout initiation, banks generally add another 1-3 days. eBay also deducts selling costs and fees before payout, and can fund refunds from available or processing balances or linked accounts when balances are insufficient.

Amazon shows why "paid" is not the same as "disbursable": funds can remain in settlement groups, DD+7 delivery-date reserve, or account-level reserve for refunds, claims, and chargebacks. If disbursement fails, funds carry into the next settlement period, and Disburse on Demand is limited to once every 24 hours.

For the ledger side of this process, see Accounts Payable vs. Accounts Receivable for Platforms and the Two-Sided Ledger.

Handle holds, refunds, and tax adjustments without breaking trust#

You preserve trust when payout changes follow a clear internal sequence and every delta is explainable from the ledger. Define one internal order of operations, keep buyer and seller timelines separate, and map each change to a reporting category before close.

Step 1 Define your internal adjustment order#

Set one stable internal sequence: apply the reserve hold policy, process refunds that are no longer pending, then recalculate net seller disbursement and next payout eligibility. If you use settled subscription refund, treat it as an internal label, not a provider-standard status term.

Providers expose different states, so your internal mapping needs to stay consistent. For Stripe connected accounts, refunds and disputes tied to a transaction are taken first from reserved amounts for that transaction, and refunds can stay pending when available balance is insufficient. eBay shows a similar operating reality: a buyer can pay, funds can still be on hold, and those held funds may be used to refund that buyer on the same transaction.

Verification checkpoint: each adjustment should tie to the original order or charge reference, journal entry ID, reserve or hold entry, and affected payout batch.

Step 2 Separate buyer and seller clocks#

Treat buyer payment completion, payout availability, and bank receipt as different clocks. A paid order is not automatically payout-ready, and payout-ready is not the same as money in the bank.

Track at least three timestamps: payment captured, funds available or hold released, and payout initiated under your payout schedule. eBay explicitly notes funds can be paid by the buyer but still unavailable for payout. When no hold applies, proceeds typically appear as available in 1-2 days, with daily scheduled payout initiation typically around 2 days after payment confirmation. Shopify defines settlement time as capture-to-availability and notes an additional 1-3 day bank delay after payout is sent.

That gives Support a factual script instead of guesswork: paid date, release or hold status, payout initiation, then bank lag.

Step 3 Add guardrails for partial and staged release#

If your system supports partial release, make it rule-based, not ad hoc. Release only the amount no longer needed for active reserve coverage, and keep the remainder blocked until documented risk or processing conditions clear.

If recovery is needed after payout, Stripe supports full and partial transfer reversals, and those reversals are real balance movements on both sides of the ledger. For Stripe connected-account reserves, add an age-control check so reserve holds do not exceed the 180-day limit.

For each release event, checkpoint the pre-release held balance, released amount, remaining reserve, reason code, and rule or approver ID.

Step 4 Align reporting categories before period close#

Close is cleaner when reporting categories match payout mechanics. Classify movements as gross sales, refunds, disputes or chargebacks, transfer reversals, seller-collected tax, and tax adjustments.

eBay reporting separates gross from expenses and refunds and includes a distinct seller-collected tax field at order level. Shopify shows why tax needs its own lane: a negative sales tax figure in a payout can move tax back to the main balance account.

Final test: every payout delta should map to one reporting category and one journal path, with no manual reclassification.

If your team reconciles incoming funds by client or merchant, How Platforms Use Virtual Accounts to Reconcile Incoming Payments Per Client goes deeper on that setup.

Build reconciliation checkpoints that catch drift early#

Drift is easiest to fix before period close, so run checkpoints at three layers: transaction tie-out, daily batch netting, and period-close certification. Make each reconciliation checkpoint explicitly pass or fail against written criteria.

Step 1 Tie out each transaction before it disappears into a payout batch#

Start at transaction level so batching does not hide errors. For each settled payment, refund, dispute, fee event, or reversal, confirm a direct path from provider record to ledger entry, then to payout treatment when relevant.

Adyen supports transaction-level settlement reconciliation, and PayPal's Balance Report provides daily transaction-level data for reconciling sales, refunds, fees, disputes, and related activity. Use that granularity to catch misclassified items early.

Keep a stable minimum field set across providers:

- provider transaction reference

- internal order or charge reference

- journal entry ID

- event type: payment, refund, chargeback, fee, reversal

- amount and currency

- payout ID or

not yet assigned

Verification checkpoint: sample yesterday's settled activity and trace both directions, ledger to provider and provider to ledger, without manual guesswork.

If you use Stripe, payout method choice affects traceability. Stripe states automatic payouts keep transaction-to-payout association and can be queried with the payout parameter, while manual payouts do not provide transaction-level reporting for payout composition.

Step 2 Net daily at the payout-batch layer#

Use daily batch netting to confirm your payout-eligible ledger set matches provider payout batches. This is an aggregate control and should include payments, refunds, and chargebacks in the batch composition check.

Adyen documents batch-level settlement reconciliation for this use case. Stripe also provides payout reconciliation status against bank deposits, which helps separate "payout created" from "bank deposit received." For PayPal disbursement reporting, keep the Transfer ID as the payout trace key into bank-transfer reconciliation.

Define pass or fail using policy thresholds you publish internally:

- variance tolerance

- max age for unresolved stale items

- max unresolved exception queue count

Daily netting catches aggregate drift early, but it does not replace transaction-level tie-out.

Step 3 Certify period close with a fixed evidence pack#

Period close should certify controls, not trigger a data hunt. The baseline standard is that reconciliations are timely, documented, and verifiable.

Use one fixed evidence pack for close and incident review:

- ledger extract for the close period

- payout batch log with payout IDs and statuses

- refund register

- unresolved variance log with owner and aging

Include a payout trace key used to connect provider payout records to bank movement, for example Transfer ID where available.

If you depend on PayPal reporting, account for operational limits. A Balance Report file can contain a maximum of a million records, and the disbursement reconciliation report has historical boundaries: account activity after July 2025 and successful payouts initiated on or after October 2025.

Step 4 Escalate repeated failures before they become payout risk#

Set a hard escalation trigger so repeated failures do not become payout risk. Define in policy when recurring failures of the same checkpoint pause non-critical payout batches and route the issue through incident handling with named owners.

The point is not the exact threshold but forcing action when normal queue handling is no longer resolving variance. Repeated failures usually point to a mapping break, a missing feed, or a retry defect that needs coordinated response.

Your incident packet should include:

- failed checkpoint result

- affected payout IDs or batch IDs

- oldest unresolved item age

- current exception queue count

- evidence-pack snapshot used to declare failure

If you cannot show what changed between failures, keep non-critical batches paused.

If you want a concrete reference for payout status tracking, batch visibility, and retry-safe operations, review Gruv's Payouts workflow.

Engineer retry-safe execution for scale#

At scale, retries should be routine. A retried action should return the same result and avoid creating a second disbursement.

Step 1 Make every write path idempotent#

Use idempotency on every retriable write that can change money state: collection confirmation, payout creation, webhook ingestion, and replay jobs in the AR cycle.

| Provider | Mechanism | Noted behavior |

|---|---|---|

| Stripe | idempotency key | reusing the same key returns the same outcome, including 500 responses |

| PayPal | PayPal-Request-Id header on REST POST calls | omitting it can duplicate a request |

| Adyen | API idempotency | keys are valid for a minimum of 7 days after first submission |

Stripe documents that reusing the same idempotency key returns the same outcome, including 500 responses. PayPal uses the PayPal-Request-Id header on REST POST calls and warns that omitting it can duplicate a request. Adyen supports API idempotency, with keys valid for a minimum of 7 days after first submission.

Set one internal rule: one business action gets one key, and every retry reuses that key until you have a terminal outcome.

Step 2 Store replay evidence next to the journal entry link#

Treat replay evidence as a control, not optional logging. Store the idempotency key, request fingerprint, provider response status, provider reference, replay count, and final outcome with the related journal entry link. That gives Finance and Payments Ops a clear answer on whether a retry created a second liability or only replayed the first result.

Verification checkpoint: take one timed-out payout creation from yesterday and confirm you can retrieve the original key, provider outcome, and linked journal entry without reading app logs.

Do not prune internal replay evidence down to provider minimums alone. Stripe notes keys can be removed after they are at least 24 hours old, but your internal buyer-to-disbursement audit trail may require longer retention.

Step 3 Design for async failure states before they happen#

Assume webhook delivery can be duplicated, delayed, or arrive out of order, and design for that behavior. Stripe warns webhook endpoints can receive the same event more than once and advises ignoring already processed events while returning success to stop retries. PayPal retries non-2xx deliveries up to 25 times over 3 days. Adyen recommends acknowledging webhook receipt before business logic, can mark delivery as failing if acknowledgment is not returned within 10 seconds, and advises checking timestamps for chronological processing.

Your handler needs two decisions on every event:

- Can I acknowledge receipt now?

- Should this event apply a state change, be ignored as already processed, or wait because an earlier event is missing?

Step 4 Publish provider-specific recovery actions before launch#

Launch with a short, provider-specific recovery playbook that on-call can execute quickly. Include:

- expected event states relevant to that provider (for example, payment, refund, reversal, payout, and failed disbursement where exposed)

- duplicate-event handling rule

- late-event and out-of-order handling rule

- acknowledgment requirement and timeout threshold where published

- retry window and manual replay method where supported

- escalation trigger when your payout monitoring shows failed disbursements

If an incident note says "replayed manually" but does not include the original key, event ID, and journal entry, your retry process is not yet provably safe.

Run an exception queue that actually closes issues#

Treat the exception queue as a financial-risk control, not a generic support inbox. Prioritize by exposure first, then by age.

Step 1 Rank by money risk first#

Handle exceptions that can block or materially distort seller disbursement first: payout failures, returned payouts, hold states, and dispute- or refund-linked items. That keeps focus on items where funds can be pulled back, held funds can be consumed by refunds, or reserves and payout limits are acting as risk controls.

Keep low-value timing mismatches lower priority only while they remain inside the platform's published payout schedule or settlement window. A payout still within normal bank posting delay is different from one that is failed, returned, or blocked by a reserve hold. Once it moves outside your published window or fully blocks a seller, promote it.

Step 2 Set SLA buckets by payout impact and seller exposure#

Use impact and urgency to assign response targets, not ticket age alone. A fully blocked payout, a short-paid seller, and a harmless date mismatch should not sit in the same SLA bucket.

At intake, require at least: current payout state, monetary exposure, affected seller count, and whether the next payout run is at risk. Verification checkpoint: sample open items and confirm those fields are populated with a clear owner. If items repeatedly return to unassigned, queue control is breaking down.

Step 3 Tag root cause so repeats drive system changes#

Close each item with a structured cause tag, not only free text. Prefer machine-readable signals such as provider errorCode, payout states like pending, failed, or returned, refund-linked status, dispute hold, or reserve block.

Review repeated tags and use them to prioritize upstream validations or payout-control checks. If the same returned-payout reason or hold condition keeps recurring, fix that upstream instead of resolving the same exception one ticket at a time.

Avoid the common failure patterns and recover fast#

Many repeat payout issues come from three avoidable gaps: mixed definitions, uncontrolled cutoff changes, and non-idempotent incident retries. The fix is tighter terms and better evidence, not just another dashboard.

Step 1 Publish one glossary for AR and payout states#

Keep Accounts Receivable (AR) cycle states separate from seller disbursement states. In marketplaces, AR can refer to buyer amounts owed to the platform, while seller disbursement reflects amounts the platform owes sellers after fees or holds.

Use a hard rule in reporting: "buyer paid" is not "seller settled." A completed sale can remain in a processing state before seller funds are available. After payout initiation, bank availability can still take 1 to 3 business days. Verification checkpoint: sample recent transactions and confirm one item is not labeled both collected AR and completed disbursement without a payout reference and timestamp.

Step 2 Control settlement cutoff changes like financial policy#

Treat settlement cutoff changes as controlled internal policy updates, not quick Ops edits. Payout timing depends on cutoffs and business-day calendars, so weekends and holidays change outcomes even when transaction timestamps look similar.

Document each cutoff change with effective date, timezone, calendar basis, and management authorization details. Example: with a three-business-day settlement rule, a Friday sale can process on Wednesday.

Step 3 Close periods from the ledger, not from dashboards#

Use dashboards for monitoring, but close periods from ledger and journal entry evidence. Books and records should reflect transactions in reasonable detail, and journal entries are what post into the general ledger.

Before close, require a payout-batch evidence pack: transaction-level extract, batch total, linked journal entry IDs, and unresolved variance notes. Dashboard totals can look right while the underlying transaction classification is wrong.

Step 4 Recover incidents through idempotent replay#

Recover payment incidents through an idempotent replay path, not ad hoc reruns. Retries should not perform the same payment action twice.

Track each replay with the request, affected payout batch, and final accounting or exception outcome. Verification checkpoint: for any replayed item, records should show whether the original request was accepted, treated as a duplicate, or failed cleanly.

Related reading: Accounts Payable vs Accounts Receivable for Freelancers.

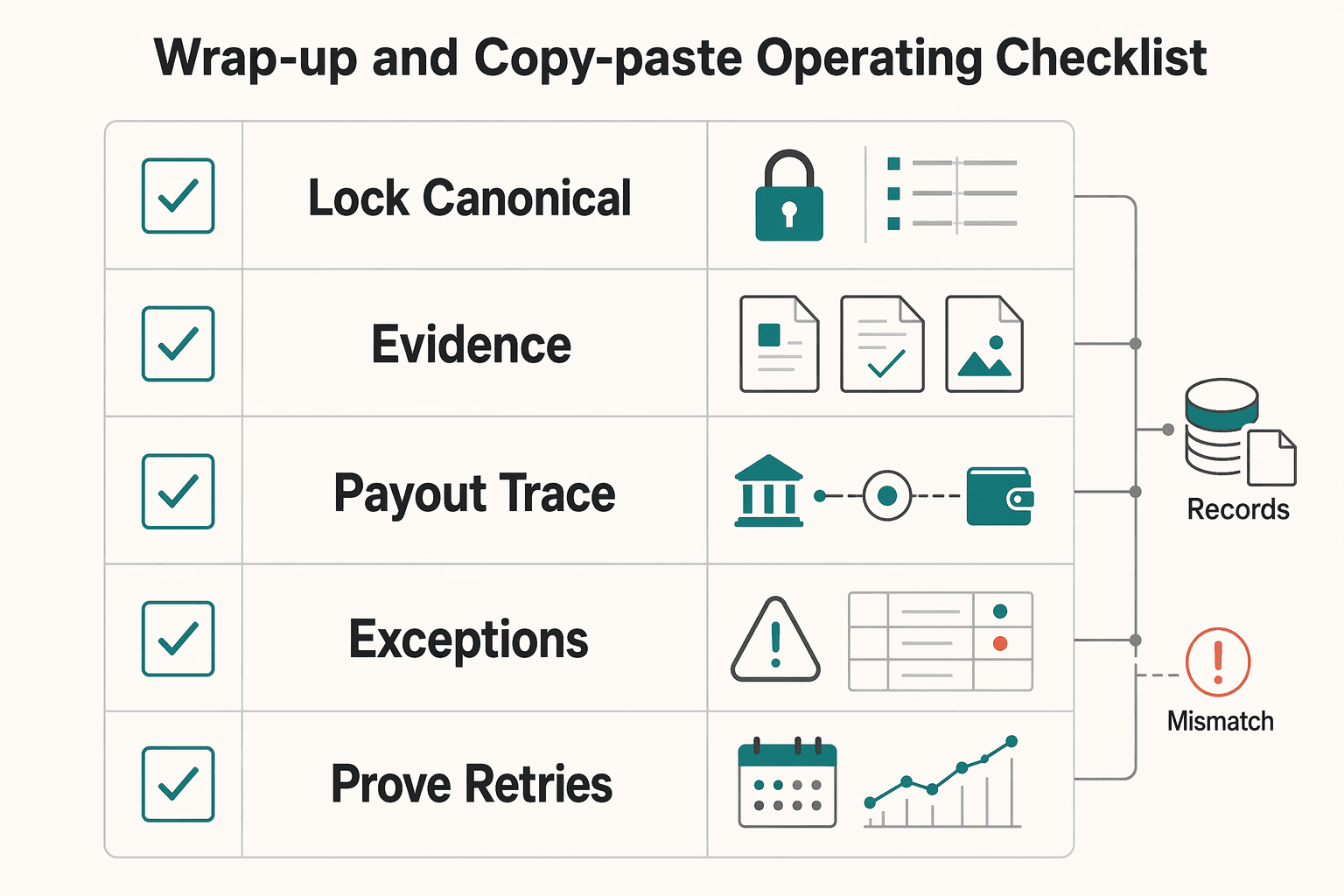

Wrap-up and copy-paste operating checklist#

Use one release standard: do not disburse seller funds until the status path, evidence trail, and retry behavior are all provable.

- Step 1: Lock your canonical state model.

Define the states you actually run from buyer collection through seller disbursement, and keep buyer-side and seller-side timelines separate. Charges and transfers can be decoupled, and some flows settle to an internal balance before external payout. If different teams cannot derive the same current state from the same records, your model is still too vague.

- Step 2: Require evidence for every state change.

Treat each transition as incomplete unless it links to source evidence. Keep the processor reference, payment date, and linked journal entry for accounting impact. For any payout line, you should be able to trace collection to disbursement without guesswork.

- Step 3: Publish and control settlement cutoff and payout eligibility logic.

Put release rules in writing and version them. For scheduled payouts, cutoff logic must align with when funds are credited and with provider cut-off timing. Keep eligibility rules explicit for cleared versus pending funds and for adjustments like refunds, chargebacks, reserves, or fees that can still change net payout.

- Step 4: Run reconciliation checkpoints on a defined cadence and triage exceptions by age.

Make checkpoint review routine, not reactive. Confirm transaction-level records tie to net movements and that each payout batch maps back to included transactions. Keep items blocked when evidence is missing or when unresolved refunds, reserves, or settlement-to-payout mismatches can still change outcomes. For a fuller operating model, use the same discipline in Accounts Receivable Management for Platforms: How to Collect from Buyers While Paying Sellers Fast.

- Step 5: Prove retries are safe before scaling payout volume.

Verify idempotent processing anywhere retries could duplicate effects: collection confirmation, webhook ingestion, payout creation, and replay jobs. Use replay tests, not design assumptions, to confirm the same keyed request returns the same result instead of creating a second disbursement. Store the idempotency key or replay token with the same records that hold the provider reference and journal link.

- Step 6: Run a monthly rule review.

Review reserve handling, refund handling, and payout cadence together each month. Cadence changes shift when payouts are initiated, and bank-display delays can still apply after funds are paid out. Adjust rules deliberately, document the reason, and keep eligibility logic in sync with operations and ledger behavior.

For a step-by-step walkthrough, see Accounts Receivable Automation for Platforms to Collect from Enterprise Buyers at Scale.

When you're ready to turn this checklist into implementation specs, use the API and webhook patterns in the Gruv docs.

Frequently Asked Questions

What is the difference between a marketplace AR cycle and a standard AR cycle?

A standard AR cycle ends when the supplier receives customer payment in full. A marketplace AR cycle adds the seller disbursement layer, so buyer collection and seller transfer should be tracked as two linked but separate timelines.

Why can a sale be completed while seller payout is still delayed?

A completed sale does not mean the funds are payout-eligible. Money can still be pending, in reserve, or subject to hold, refund, dispute, or other risk controls before seller disbursement.

What should we track between buyer collection and seller disbursement every day?

Track each daily balance movement that enters or leaves your processor balance. For each payout item, keep a trace from source collection through holds, refunds, or other adjustments to final payout-batch inclusion, and use payout reconciliation when automatic payouts are enabled.

How should refunds and taxes be reflected in disbursement totals?

Show refunds and taxes as separate lines in disbursement math rather than folding them into gross payment totals. Refunded amounts can be deducted from the next available payout, and tax treatment should stay in its own reporting category so payout deltas remain explainable.

How do AR cycle timing and Cash Conversion Cycle differ for marketplace operators?

They measure different things. AR-cycle timing follows the path from buyer obligation and collection to seller disbursement readiness, while Cash Conversion Cycle is a working-capital metric defined as DIO + DSO - DPO. Changing payout cadence changes when payouts are sent, not when pending funds become available.

Which checkpoints should block payout release when data is incomplete?

Block payout release when required transaction evidence for reconciliation is missing. Also block when funds are still pending or when unresolved refunds, disputes, holds, or other adjustments can still change the net amount. At batch level, do not release if totals cannot be reconciled to the included transactions.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- department.va.gov/financial-policy-documents/financial-documen...trusted

- docs.stripe.com/reports/payout-reconciliationtrusted

- docs.stripe.com/plan-integration/get-started/reporting-recon...trusted

- finance.columbia.edu/sites/www.finance.columbia.edu/files/content...trusted

- finance.cornell.edu/controller/internalcontrols/unitlevelactivit...trusted

- sec.gov/spotlight/fcpa/fcpa-recordkeeping.pdftrusted

- uscode.house.gov/view.xhtmltrusted

- docs.adyen.com/platforms/quickstart-guide/payoutsexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: