Quick Answer

Set payment terms before kickoff, then run collections and payables from one weekly control loop. Use explicit terms such as Net 30, Net 60, Net 90, or 2/10 Net 30, issue invoices at milestone triggers, and escalate overdue items at a preset point. Recalculate current assets minus current liabilities from the same snapshot, and tighten follow-up when DSO rises in consecutive periods. Use financing only for a defined timing gap, not as cover for repeat billing or approval delays.

How to use working capital as a cash-timing check before bills come due#

Protect your working capital before cash gets tight. In practice, that means balancing short-term assets and obligations so you have enough cash to cover near-term bills and keep operations steady.

For freelancers and small teams, the common risk is timing. Revenue can look fine while usable cash is delayed. Working capital is the gap between what is available or collectible soon, like cash and receivables, and what you need to pay soon, like payables.

This guide focuses on the operating choices that move cash faster and reduce surprises:

- payment terms and invoice timing

- receivables follow-up and collections discipline

- payable timing and cash planning

- risk controls when payments are delayed

Treat this as a risk-control guide, not a borrowing guide. Short-term financing can help as a bridge when used carefully. But receivables, payables, inventory where relevant, and cash management are the core levers. They can free cash trapped on the balance sheet and reduce reliance on outside borrowing.

At the start of each client engagement, use a simple decision lens. Decide when invoices go out, how receivables follow-up will run, and how payment terms are documented. Those basics affect how quickly cash lands and how often delays turn into bigger cash-flow problems.

The examples here focus on invoice-led service businesses, where receivables and payables discipline often drives outcomes. If payment delays show up, treat the examples as patterns, not fixed rules.

For a step-by-step walkthrough, see A Guide to Dunning Management for Failed Payments.

Working capital management for freelancers in plain English#

Working capital management means controlling short-term assets and short-term obligations so your day-to-day operations stay stable, not just profitable on paper.

Net working capital is the gap between those two balances: current assets minus current liabilities. For many freelancers, receivables can be a meaningful part of working capital, so net working capital is not the same as cash in your bank account.

That is why strong revenue can still feel tight. You can book a good month and still run short on usable cash if invoices are paid late. Receivables may look healthy on paper, but overdue invoices do not pay bills due now. In general, positive working capital supports short-term stability, while negative working capital raises risk.

Use one practical lens throughout this guide: cash timing can matter as much as headline income. Check both sides of liquidity together regularly:

- what is actually collectible soon

- what must be paid soon

For more context, see What is 'Working Capital' in the Context of an M&A Deal?.

Read your balance sheet without overcomplicating it#

Use the balance sheet as a point-in-time liquidity check. Find the sections labeled Current Assets and Current Liabilities, then calculate the gap. That gap is your Net Working Capital.

On a Balance Sheet (statement of financial position), current and non-current items are separated, as IFRS requires. "Current" generally means expected to convert to cash or come due within 12 months (or one year or less). In practice, review items like cash and Accounts Receivable on the asset side, and near-term obligations such as Accounts Payable on the liability side. Working capital is a calculation from those sections, not a standalone cash number.

Be careful with Accounts Receivable. Its value depends on how much is actually collectible. If collectibility is doubtful, that risk needs to be reflected. When present, Allowance for Doubtful Accounts reduces receivables to a more realistic collectible amount.

For many freelancers and service businesses, inventory is minimal or absent, so day-to-day results depend more on billing, collections, and payable discipline than on inventory analysis.

Before you rely on any liquidity number, run one control check. Make sure invoice-level AR detail, or the subsidiary ledger, reconciles to the Accounts Receivable control balance in the general ledger. If those do not match, your liquidity view may be stale or misstated. Need the full breakdown? Read Freelance Financial Management That Protects Cashflow First.

The metrics that actually predict cash stress#

Use four metrics together to spot cash-stress risk: Current Ratio, Quick Ratio, Cash Conversion Cycle (CCC), and Working Capital Turnover Ratio. No single metric is definitive, but this set helps show whether cash is available, tied up, or under pressure.

Start with the two coverage checks:

- Current Ratio = short-term assets ÷ short-term obligations

Use it to check short-term obligation coverage. A value above 1.0 can indicate more near-term resources than near-term obligations, but it is not a universal pass mark.

- Quick Ratio = (Cash + Short-term marketable investments + Receivables) ÷ short-term obligations

Equivalent form: (short-term assets - Inventory) ÷ short-term obligations. This is the stricter liquidity test because it excludes inventory.

Why CCC can catch trouble early#

CCC can serve as an early warning signal because it measures how long cash stays tied up before it comes back as usable cash. Use the formula CCC = DIO + DSO - DPO.

- DSO (Days Sales Outstanding): average days to collect after a sale

- DPO (Days Payables Outstanding): average days to pay suppliers

- DIO (Days Inventory Outstanding): average days inventory is held before sale

If you build these from annual data, use 365 days consistently. Mixing time windows or data sources can hide a real trend.

A shorter CCC is generally linked to lower external financing pressure and more internally available cash.

A practical decision rule#

Use this as an operating trigger: if DSO rises for consecutive periods, tighten collections. Treat it as a decision heuristic, not a universal law.

Check where the DSO rise is concentrated, then fix that bottleneck first: billing timing, approval workflow, follow-up cadence, or invoice contact clarity.

| Metric | What it signals | Common failure mode | First corrective action |

|---|---|---|---|

| Current Ratio | Broad short-term obligation coverage | Looks healthy because broad short-term assets can mask immediate liquidity pressure | Review asset quality inside short-term assets, not just totals |

| Quick Ratio | Immediate liquidity stress without relying on inventory | Cash is thin even though short-term assets look adequate | Prioritize collections and defer nonessential outflows |

| Cash Conversion Cycle | How long cash stays tied up in operations | Rising DSO or DIO quietly lengthens the cycle | Isolate the component that moved and fix that delay first |

| Working Capital Turnover Ratio | How efficiently revenue is generated from net short-term assets | Trend breaks because the formula basis changed | Pick one convention and keep it consistent period to period |

For Working Capital Turnover Ratio, consistency matters more than picking a single "correct" numerator. Sources use both net annual sales and total revenue over average working capital. For a fuller walkthrough, see How to Calculate the Cash Conversion Cycle.

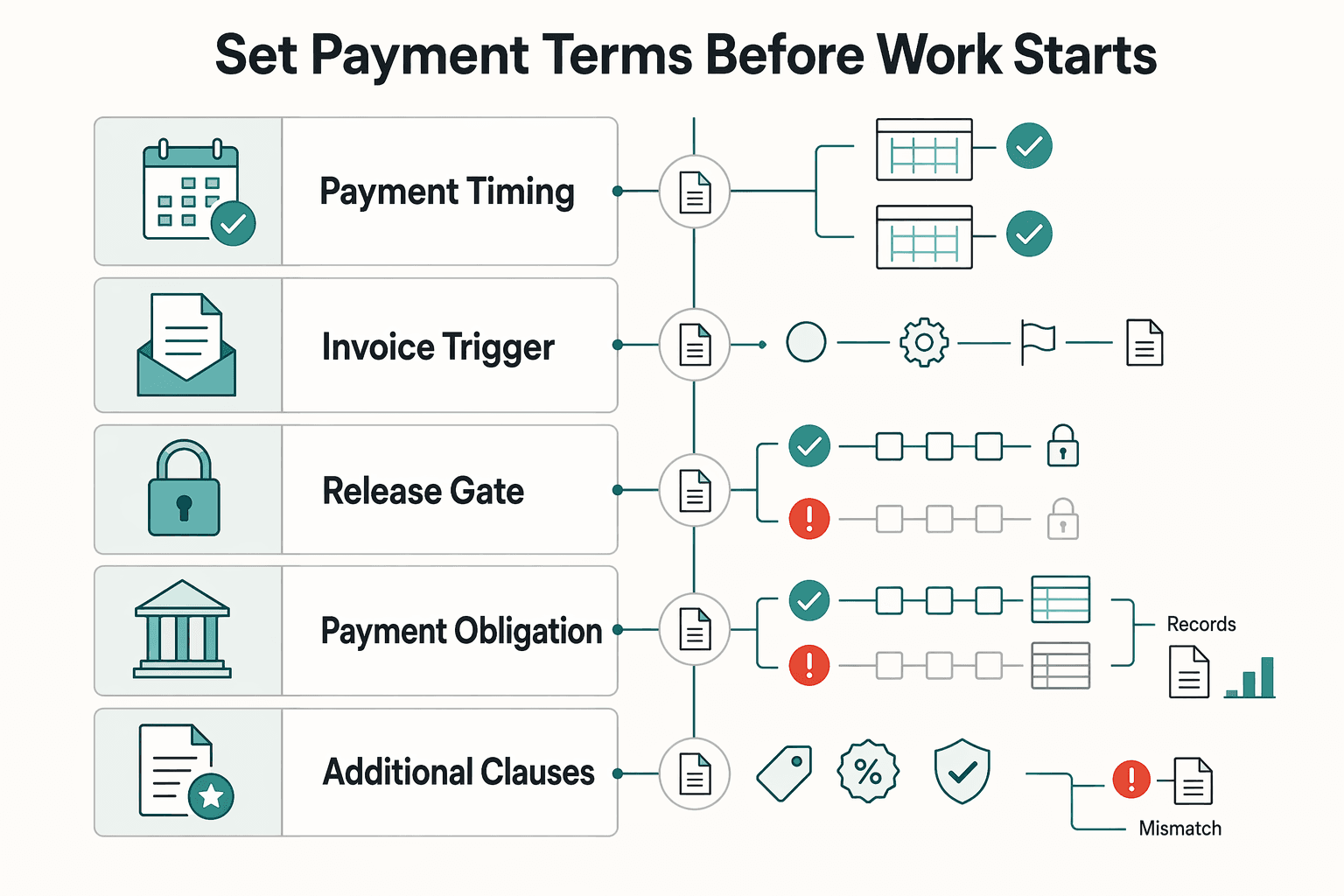

Set payment terms before work starts#

Set Payment Terms before delivery begins, when payment timing is usually agreed in the contract.

| Checklist item | What to specify |

|---|---|

| Payment timing format | Net 30 / Net 60 / Net 90 |

| Invoice trigger points | When invoices are issued |

| Invoice approval | Who approves invoices and where approvals are recorded |

| Payment obligation | What is owed, by whom, and when each payment is due |

| Additional clauses | Written clearly in the agreement |

Terms should state the exact due window for full payment, not a vague expectation. Use clear formats such as Net 30, Net 60, or Net 90 so both sides are aligned on due dates. If you offer an early-payment incentive, write it explicitly, for example 2/10 Net 30.

Build the checklist you send clients. Keep the client-facing checklist short but complete enough to remove ambiguity: payment timing, invoice trigger points, invoice approval, payment obligation, and any additional contract clauses you choose to use, written clearly in the agreement.

Treat term length as a cash-risk tradeoff. Term length is a cash-risk decision, not an admin detail. It can affect cash flow, profitability, sales growth, credit, and supply risk.

If a client asks for longer terms, reassess risk before kickoff instead of accepting the same commercial setup by default. Longer terms can improve the payer's cash timing. They can also bring hidden costs, including price increases from the other side.

Do not start delivery without evidence. Before kickoff, keep documentation that lets you verify payment obligations clearly. The checkpoint is simple: you should be able to verify what is owed, by whom, and when it is due before work starts.

We covered that in more detail in A Guide to Invoice Factoring for Freelancers. Lock your payment-term language in writing before kickoff to reduce ambiguity later. Draft cleaner client terms.

Build an invoice and follow-up cadence that shortens DSO#

If you want Days Sales Outstanding (DSO) to come down, stop relying on ad hoc chasing. Use a fixed invoice-to-collection sequence with clear checkpoints, owners, and status visibility from the moment an invoice is ready to send.

Use the same order every time#

| Step | What you do | What to verify | Why it matters for DSO and AR |

|---|---|---|---|

| Issue invoice at the milestone trigger | Send as soon as the agreed trigger happens | Invoice format is standardized, details match scope, schedule aligns to contract terms, and client data is correct | Late or error-filled invoices can delay payment before follow-up even starts |

| Confirm receipt | Confirm the invoice reached the right approver and entered their process | You can identify who received it and whether anything is missing | Early visibility helps keep AR items from stalling |

| Send reminders on a defined cadence | Follow up based on due date and prior payment behavior | Message includes invoice ID, due date, amount, and payment method/link | Timing matters: too early can strain the relationship, too late raises risk |

| Escalate when it crosses your internal point | Shift from reminder to escalation with clear ownership | You can show prior outreach, current status, and next owner | Defined escalation paths and visibility help disputes move instead of stalling |

| Send final notice | State the immediate next step needed to clear the account | Record includes full outreach history and latest commitment | Creates a clean handoff for dispute handling or leadership review |

Tie follow-up to aging, not mood. Treat DSO as an operating signal. It reflects the average days from invoice issuance to payment. If DSO rises or older items stack up in aging, adjust the process early. Consistency, clarity, and visibility in AR usually improve outcomes more than aggressive tactics. Manual invoicing and spreadsheet-heavy tracking often let invoices drift.

Make escalation a real checkpoint. Set one internal escalation point in advance. When an invoice crosses it, decide the next account action based on your risk policy and contract terms, and route any issue into a defined dispute path.

The key question is not only "Is it paid?" Ask instead, "Do we know why it is unpaid, who owns the next action, and what evidence supports that status?"

Keep proof easy to audit. Use standardized invoices, include a payment method or link where appropriate, and track status so invoice history is visible. That audit trail helps disputes move forward and reduces reconstruction work later.

For most small teams, the payoff is simple: fewer preventable delays, faster resolution, and tighter control over accounts receivable.

Manage payables and expenses without harming supplier trust#

Once collections are moving with discipline, manage the other side of the cycle just as deliberately. The goal is to protect critical commitments first, then control timing on noncritical expenses without surprising vendors.

Prioritize payables by business impact#

Treat Accounts Payable as a ranked queue. Pay first what can disrupt delivery, trigger penalties, or damage relationships you depend on, including suppliers, contractors, and services tied to core operations.

Then manage the rest actively. Before you change timing, run a balance-sheet check so you are solving a real working-capital issue: short-term assets minus short-term obligations. Example: $300,000 in short-term assets and $200,000 in short-term obligations leaves $100,000 in working capital. If needed, align your payment plan with what your balance sheet shows before acting, using How to Read a Balance Sheet.

For each payable, confirm the amount, due date, and delivery criticality so payment order follows business impact, not urgency noise.

Use DPO carefully, not as a habit#

Using payment delays as a default can strain supplier relationships and limit flexibility. It can also cost you early-pay or volume discounts when those would help.

The bigger risk is silent delay. Paying on time supports both penalty avoidance and stakeholder relationships, so if cash is tight, renegotiate noncritical terms before delaying without notice. Ask for a revised due date, split payment, or adjusted billing rhythm. Even with limited bargaining power, explicit negotiation is usually safer than silence.

Small-team caveat#

If you carry little Inventory, stock optimization may not be your main lever. Receivable speed and expense timing can matter more, so connect your payable plan to your collections cadence and keep both sides of cash flow moving intentionally. If you want a deeper dive, read Hiring Your First Subcontractor: Legal and Financial Steps.

Decide when short-term financing helps and when it hides a broken process#

Short-term financing can help as a bridge for a defined timing gap, but it should not become the default fix for recurring cash-management issues. The tradeoff is simple: you get cash now, and commit part of future cash flow later.

A practical rule: if financing keeps covering the same shortfall, treat that as a process signal first and review your invoicing and collections workflow before adding more financing.

There is no universal financing rule that fits every business, so compare options by fit, cash-flow pressure, and admin load in your context. In working-capital terms, you need enough cash to cover immediate costs without tying up too much cash.

| Option type | Best fit | Future cash-flow pressure | Operational complexity |

|---|---|---|---|

| Broad short-term facility | Repeated small timing gaps across operations | Can build if used frequently | Moderate |

| Receivable-tied financing | A specific issued receivable expected to convert soon | Concentrated on that receivable cycle | Moderate to high |

| Fixed-term short borrowing | A one-off near-term obligation with a defined repayment plan | Compressed into upcoming periods | Low to moderate |

Before you accept financing, run a liquidity checkpoint against expected cash-in dates and near-term obligations like supplier invoices and payroll. Then test whether repayment timing is realistic within your 12-month working-capital window. If repayment is likely due before cash-in, you are not closing one gap. You are creating another.

This pairs well with our guide on A guide to Stripe's 'Capital' for business financing.

Handle holds, chargebacks, and payment failures with clear escalation#

Treat chargebacks, payout holds, and payment failures as active working-capital risk, not routine support tickets. In card-network dispute flows, funds can be reversed immediately, and missed response deadlines can turn a dispute into a loss.

Separate the failure modes early#

Do not label everything as a "delay." Identify the event first, because ownership, evidence, and timing are different.

| Event type | What it means | Timing or cash note |

|---|---|---|

| Client dispute or chargeback | A cardholder challenges a payment through their issuer | The payment can be reversed right away |

| Payout hold or paused payout | Funds can be restricted or transfers out can be blocked | Payouts may be paused when required account information is unresolved |

| Delayed credit | A release, reversal, or refund is expected | It has not posted yet |

| Unmatched return | Funds moved back | You cannot tie them to a specific invoice or ledger entry |

Make the first response fast and controlled#

When one of these events hits, use a simple control sequence: protect cash, isolate exposure in Accounts Receivable, and preserve evidence.

- Confirm the event type in the provider dashboard.

- Mark affected invoice(s) in Accounts Receivable for internal tracking as disputed, held, or pending reconciliation.

- Collect the evidence set immediately (scope, terms, invoice, delivery or acceptance proof, payment confirmation, and message history).

- Confirm the case deadline in the provider tool and assign one owner.

The key checkpoint is the response deadline. Some tools show a case-specific reply-by date, and missed evidence deadlines can trigger automatic loss. Dispute handling is also not identical across card networks.

Do not promise release timing before verification#

Release behavior varies by provider, country, and program, so confirm current account conditions before giving a date.

| Scenario | Documented timing example |

|---|---|

| Stripe initial payout | Typically 7-14 days after first successful live payment |

| Stripe Connect paused payout | In-flight payouts can remain pending up to 10 days |

| PayPal hold (supported physical-goods flow) | Funds released 1 day after confirmed delivery |

| PayPal hold (service/digital status update flow) | Funds could release after 7 days |

| PayPal hold (merchant hold guidance) | Holds may last up to 21 days |

| Dispute lifecycle (issuer decision path) | Can take 2-3 months |

If someone asks when funds will clear, verify the live provider rule first instead of committing to an unverified timeline.

Keep one event from forcing bad financing#

Maintain a minimum operating cushion so one hold, reversal, or paused payout does not force emergency borrowing. Size that cushion against near-term must-pay obligations and realistic resolution time for disputes, holds, and reconciliation. If one processor event can block critical obligations, your cash buffer is too thin for your current risk exposure.

Keep an audit-ready evidence pack for disputes and reconciliation#

Once a hold or dispute is live, documentation quality often affects how quickly questions can be resolved. Keep one evidence pack per client engagement that is complete enough for disputes and structured enough for reconciliation.

What belongs in your records#

Treat this as a lightweight PBC pack: prepared support that is easy to trace. Build it early, not reactively, so you are not hunting through inboxes, chats, and scattered folders when a case is live.

| Artifact | What to keep |

|---|---|

| Signed contract or statement of work | Keep it tied to the same client file and invoice reference |

| Invoice trail | Invoice number, issue date, revisions, and credit notes if any |

| Approvals or acceptance records | Link them to the related invoice or work |

| Payment records and confirmations | Tie them to the same invoice reference |

| Variance notes | Show what is open, who owns it, and what was resolved |

At minimum, keep those artifacts tied to the same client file and invoice reference.

Cross-reference everything. If invoice INV-1048 is disputed, that same ID should appear in the contract schedule, approval record, and ledger note.

Tie it to the books, not just the inbox#

Do not keep your records only as support evidence. Use them to explain the accounting impact of each event in your books.

Your reconciliation view should show a clear chain: invoice issued, payment received, dispute opened, and dispute resolved. Raw exports alone are not enough. Add a short summary that explains the event, ties it to the related entry, and notes any open variance.

Reconcile while the trail is still easy to retrieve#

Run reconciliation at regular checkpoints so support records, approvals, and payment confirmations are still accessible. Use each review to confirm:

- every new invoice has matching support and a clear status in your records

- every payment event ties to the expected book entry

- every break has an owner, a note, and a documented resolution history

That last point is core exception management: assign, resolve, and document breaks with an audit trail. Scattered evidence across email, chat, personal devices, and multiple folders creates avoidable delay risk. Unresolved breaks can leave key balances unclear longer than they should be.

Run a weekly 15-minute working capital control routine#

Keep this routine decision-first. Check cash, receivables, near-term obligations, and updated Working Capital, then decide whether optional spend is go or no-go until the next review.

Keep the review narrow#

Start with actual bank cash, not expected collections. Then update Working Capital and do a quick liquidity check with the Current Ratio.

Use the same checklist each cycle:

- Confirm actual bank cash and flag unusual spend or transactions above your review threshold.

- Review Accounts Receivable aging by bucket (for example 0-15, 16-30, 31-60) and isolate older or disputed items.

- Review near-term obligations due before the next review and mark must-pay items.

- Recalculate Working Capital and Current Ratio from the same snapshot.

- Record the next action for each exception before you close the review.

Do not treat aging as fully reliable when invoice disputes are building. If invoices look collectible in the ledger but are stalled by disputes, your liquidity view can be overstated.

Use signals to trigger action#

Your routine only helps if signals force action.

For Current Ratio, treat ranges as directional:

- Below 1.0: short-term debts are not covered.

- 1.0 to 1.2: cushion is thin.

- 1.2 to 2.0: often a workable range for many small businesses.

- Above 2.0: may indicate idle cash or other underused short-term assets.

For receivables, use trend direction instead of fixed targets. If more balances move into older aging buckets, tighten follow-up before approving extra spend.

Also treat recurring invoice disputes as a root-cause signal. If reminders increase but invoices still stall, fix invoicing quality at the source.

Assign owners so action is explicit#

Even in a solo operation, responsibilities still need to be explicit: cash check, collections follow-up, and final spend decision. In a small team, assign those responsibilities before the review ends.

Use this as a default matrix and adapt it to your setup:

| Signal | Next action |

|---|---|

| Current Ratio weakens toward thin coverage | Freeze optional spend, confirm must-pay items, refresh cash view from bank balances |

| More receivables move into older aging buckets | Confirm invoice status, clear dispute blockers, and prioritize oldest open balances |

| Older or disputed receivable appears in aging | Pull invoice trail, confirm status, and fix recurring invoicing issues at the source |

| Unusual spend is detected | Verify transaction, document outcome, and stop repeat leakage if needed |

End with one binary decision: go or no-go on optional spend until the next cycle. Use no-go when liquidity signals are weakening or a major receivable is disputed and unresolved. Related reading: How to Calculate Weighted Average Cost of Capital (WACC).

Common mistakes that drain working capital#

Working-capital problems usually come from avoidable gaps in liquidity checks, documentation, and follow-through.

Treating liquidity risk as implicit. Make Liquidity Risk an explicit review item each cycle. If you cannot state your current liquidity risks clearly, your decisions may be running ahead of your evidence.

Letting documentation lag behind decisions. Do not treat records as optional cleanup work. Keep operating documentation current before decisions are made, so cash and risk calls rest on verifiable facts rather than memory.

Skipping required checkpoint structure. Use a repeatable structure with required sections in your review process. When sections are inconsistent or missing, you lose comparability across periods and make issues easier to miss.

Waiting for escalation before tightening controls. Escalation gets expensive fast, so tighten controls before pressure builds rather than after issues have already escalated.

Overstating confidence from incomplete or inaccessible records. If a source is blocked or inaccessible, do not treat it as support for a concrete claim. Mark uncertainty plainly and make decisions on evidence you can actually review.

Conclusion#

Strong working capital management is a repeatable risk-control habit, not a one-time spreadsheet task. When discipline is consistent, it supports day-to-day operations and growth. When it slips, cash shortfalls and reliance on high-cost credit become more likely.

Start with three moves:

- Tighten Payment Terms before work starts.

- Enforce a consistent collections cadence instead of ad hoc follow-up.

- Run a weekly check so issues surface while options remain.

Use those moves as an operating checklist. Define scope, terms, and invoice-approval steps before delivery. Apply the same reminder and escalation rhythm each cycle. Review what is collectible now versus what is delayed. Keep status explicit with yes or no checkpoints, not implied.

Then adapt the checklist to your client mix and billing model, and confirm any country-specific or program-specific constraints before rollout. If you rely on external guidance, verify that it is still current before you adopt it unchanged.

If your weekly review keeps flagging late invoices and cash-flow risk, move to a flow with clearer payment tracking and control points. See Gruv for freelancers.

Frequently Asked Questions

What is working capital management in a freelancer business?

Working capital management means balancing short-term assets and short-term obligations so you can meet near-term bills and keep operating smoothly. For freelancers, that usually means tracking cash and receivables against upcoming liabilities.

How do you calculate working capital from a basic balance sheet?

Use the core formula: current assets minus current liabilities equals working capital. Pull both numbers directly from your balance sheet, then verify items are correctly classified as current versus non-current so the result is reliable.

What is the difference between working capital and cash flow?

Working capital is a point-in-time view of your short-term financial cushion. Cash flow measures money generated or consumed over a period. You need both views to understand liquidity now and movement over time.

Which metric matters most for service businesses with little inventory?

No single metric is always the most important. Current ratio, quick ratio, and the cash conversion cycle help assess liquidity and operational efficiency, so read them together for a more dependable picture.

How can I improve working capital quickly without hurting client relationships?

Start with the parts you control: closely monitor short-term assets and liabilities so you can spot liquidity pressure early.

When should I use short-term financing versus tightening payment terms?

There is no universal rule that fits every case. Whichever option you use, avoid relying on financing to absorb ongoing losses or high burn, because that reduces your working-capital buffer.

What should I do first if a payment is held or disputed?

Timelines and outcomes vary by provider and client. Treat payment timing as uncertain when planning near-term liquidity.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- academia.edu/20119022/An_Analysis_of_Working_Capital_Mana...trusted

- ag.purdue.edu/commercialag/home/wp-content/uploads/2015/09...trusted

- carlsonschool.umn.edu/sites/carlsonschool.umn.edu/files/2018-10/j....trusted

- federalreserve.gov/frrs/guidance/interagency-policy-statement-o...trusted

- finance.cornell.edu/accounting/topics/revenueclass/baddebttrusted

- fiscal.treasury.gov/files/reports-statements/financial-report/02...trusted

- govinfo.gov/content/pkg/CHRG-115shrg37801/html/CHRG-115s...trusted

- occ.gov/publications-and-resources/publications/comp...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Hiring a Subcontractor for the First Time Without Costly Surprises

**Start with a risk-control sequence, not an ad hoc handoff.** As the Contractor, your goal is simple: deliver cleanly, control scope, and release payment only when the work and file are complete.

Working Capital in M&A for Small Service Businesses

If you are selling a small service business, define working capital early. It is one of the simplest ways to protect your proceeds before the Letter of Intent (LOI), during financial due diligence, and at closing. In many deals, these mechanics can still move what you take home in a meaningful way.

How to Read a Balance Sheet for Freelancers and Small Teams

Use your balance sheet as a dated decision dashboard, not an accounting exercise. It shows what your business owns, what it owes, and what is left on that date. Use it to make better calls on cash safety, client risk, tax readiness, and growth timing.