Quick Answer

To freelance in Italy, you usually need to verify Regime Forfettario fit, register the Partita IVA with the correct AA9/12 flow, keep VAT treatment separate from registration status, and confirm INPS contribution handling before you activate invoices or payouts.

Separate Partita IVA eligibility from payout readiness#

If you cannot separate Regime Forfettario eligibility, VAT treatment, and payout controls, delay launch.

This guide is for operators making product and compliance decisions, not just individuals opening a Partita IVA. A Partita IVA is a tax identification number. It does not, on its own, define the tax regime or VAT handling. That distinction should shape onboarding, invoicing, and exception paths from day one.

Start with the baseline assumption#

For new taxpayers, the cited baseline from FY 2016 onward is Regime Forfettario. The official Agenzia delle Entrate regime forfetario rules frame it as a simplified tax lane for individuals acting as sole traders. Use that as a starting assumption, not as a complete eligibility engine.

Begin with cohort fit. Can your target users clearly qualify for this lane? The official requisiti del regime forfetario page is the right place to verify the €85,000 annual threshold, the ATECO interaction, and the core access tests. Because exclusions and edge cases still require interpretation, treat unclear cases as manual review.

Qualify the scheme before you build downstream flows#

Qualify the scheme before you build downstream flows. For launch design, treat it as relevant to individuals carrying out business, artistic, or professional activity as sole traders, not partnerships or companies.

Capture the activity profile and revenue expectations for each cohort. Then verify uncertain cases with Agenzia delle Entrate before enabling self-serve onboarding. Keep a hard verification checkpoint wherever interpretation depends on guidance, especially where some 2026-related provisions may still need clarification.

Validate VAT treatment separately from Partita IVA status#

Validate VAT treatment separately from Partita IVA status. The Agenzia delle Entrate page on semplificazioni e adempimenti Iva explains why taxpayers in this lane do not charge VAT to clients and cannot recover VAT on purchases.

Do not map "has Partita IVA" to "charge VAT." If revenue exceeds €100,000 during the year, cited guidance indicates immediate exit from the scheme for that year. VAT must then be applied from the transaction that caused the exceedance onward. Your product should have a threshold trigger for that event.

Sequence payments and compliance only after the tax lane is clear#

Map payment and compliance operations only after your regime and VAT logic are defensible. If the simplified lane does not apply, the ordinary regime may apply, and cited guidance describes that option as binding for at least three years.

That sequence matters. First qualify the regime. Then validate VAT obligations. Then map invoices, payouts, and audit checks. For exclusions, residency interactions, or unsettled 2026 points, set explicit pre-launch verification with Agenzia delle Entrate, INPS, and a qualified commercialista.

Related reading: German Blue Card for Highly Skilled Workers: Eligibility, Net Pay, Tax, and Freelance Tradeoffs.

Decide if Italy is the right lane this quarter#

Italy is the right lane this quarter only if your first cohort can be onboarded through one clear regime path with low interpretation risk. If you expect mixed profiles, unclear residency, or users likely to move past the €85,000 limit quickly, either design for Regime Ordinario from day one or defer launch.

Assess cohort fit before feature scope#

Start with your actual first cohort, not the long-term market. The real decision is whether most users can pass one narrow onboarding path without heavy manual intervention. Screen the cohort against these questions:

- Can most users operate with a Partita IVA, which is required to invoice?

- Can most plausibly fit the simplified lane at registration, instead of forcing immediate support for both Forfettario and Ordinario?

- Are expected revenues comfortably below €85,000?

- Can activity be mapped to a clear ATECO code without repeated edge-case review?

- Are residency facts straightforward, or do you already have cross-border cases that may need review against the 183-day reference?

If multiple answers are uncertain, treat that as an onboarding and compliance signal, not just a tax interpretation issue. Registration requires a regime choice, and setup choices can create long-term consequences.

Compare the launch shape you are buying#

In practice, this is usually a choice between a constrained Forfettario launch and a mixed-profile launch.

| Decision area | Simplified-lane launch | Mixed profiles (possible Ordinario) |

|---|---|---|

| Target cohort | Individuals likely to fit the flat-rate lane at registration | Broader freelancer mix with uncertain regime fit |

| Onboarding complexity | Lower with one primary regime path | Higher because regime choice is required at registration |

| Revenue pressure | Better when expected revenue is well below €85,000 | Better when users may outgrow the simplified lane quickly |

| ATECO risk | Narrower activity profiles are easier to standardize | Higher variance; ATECO affects tax and contribution treatment |

| Compliance overhead | More manageable if edge cases stay out of self-serve | Heavier manual review and advisor-dependent operations |

Model two practical cost and risk flags early:

- ATECO choice affects the profitability coefficient and INPS category. Some profiles can face fixed contributions of about €4,200 per year regardless of revenue.

- Advisor dependency is real in this lane. Sources recommend pre-registration consultation, and cited setup fees are in the €800 to €1,500 range.

Set a go or no go rule and verification checkpoint#

Use a simple rule. If your first cohort is likely to breach simplified-lane constraints quickly, build for Ordinario from day one.

Add a hard verification checkpoint before self-serve activation for unresolved regime fit, ATECO selection, residency facts, or contribution assumptions. Use Agenzia delle Entrate registration timing and qualified advisor review for edge cases. Plan operations so issues are resolved before the cited 30 day registration window becomes a user failure point.

Do not automate a single "final" Gestione Separata rate until verified with current guidance. Proceed only when you can clearly define the supported cohort, justify its primary regime path, and document the escalation path for exceptions.

This pairs well with our guide on Italy Digital Nomad Visa Tax Playbook for Remote Professionals.

Gather the minimum evidence pack before setup#

Freeze a single provisional evidence pack before launch, and treat Italy form and document logic as unverified until you confirm it with authoritative primary Italian sources. The current source set does not establish production-ready registration rules.

Define a provisional evidence pack and mark unverified items#

Use a minimum checklist, but label it clearly as draft validation scope. Reserve placeholder fields for core identity, residency, and business context, and mark each as pending confirmation from authoritative Italian guidance. Do not present that list as a final legal requirement.

Keep one shared record set across onboarding, VAT review, and payouts. Each required field should map to one source document or one applicant attestation with a named owner. Remove fields that have no downstream use.

Separate tax ID context from business and VAT registration context#

Keep tax-ID and business/VAT registration logic separate in ops notes, but do not hard-route users unless primary Italian guidance confirms applicability and sequence.

Until validated, use two internal review statuses:

Tax ID context needs confirmationBusiness or VAT registration context needs confirmation

Use one operator-owned checklist across onboarding, VAT, and payouts#

Run one checklist, one document store, and one record owner for the applicant pack so identity acceptance, VAT profile review, and payout setup rely on the same records. If key identity or business fields change, rerun downstream checks before activation.

Add a pre-launch escalation path for residency and cross-border ambiguity#

Assign one escalation owner for unclear residency facts and potential cross-border tax ambiguity, and define when self-serve stops for human review. For residency context, keep a reference available: Tax Residency in Italy: A Guide for Freelancers and Nomads.

Before accepting sensitive uploads, require official government sources and secure connections, and do not treat database inclusion or polished PDFs as proof of procedural authority.

Related: A Guide to the 'Imposta Sostitutiva' for Italy's Regime Forfettario.

Choose the tax lane before building onboarding logic#

Choose a provisional lane first, then design onboarding around that decision record. Treat lane labels as internal operating states, and keep both unverified until primary guidance and local professional advice confirm what you can automate.

Compare lanes as operational states, not legal outcomes#

Treat the lanes as different operating states. Use a side-by-side view to decide review depth and automation risk, not to promise eligibility or reporting outcomes that are not yet validated.

| Decision point | Simplified lane (provisional) | Standard lane (provisional) |

|---|---|---|

| Routing posture | Use only when applicant facts are coherent enough to support a consistent lane decision | Use when simplified-lane fit is unclear or disputed |

| Onboarding messaging | Avoid definitive claims about eligibility, burden, or filing duties | Avoid definitive claims about broader obligations until verified |

| Automation posture | Keep gated behind explicit checks and operator sign-off | Keep manual review available from day one |

| Risk signal | Escalate if facts are incomplete, shifting, or inconsistent | Escalate if lane choice depends on assumptions you cannot evidence |

Keep lane labels tightly scoped#

Keep lane labels narrow and explicitly provisional. Do not reuse a lane-specific label across lanes, and do not publish rate or calculation logic until confirmed by primary sources.

Before adding new lane-specific automation, check whether existing controls already address the risk.

Block automation when activity facts are unstable#

Do not auto-route when the activity description, revenue model, or customer profile is too vague to support a consistent lane decision. If an operator cannot explain the lane choice from documented facts, the profile is not ready for automation.

Escalate ambiguity early#

Escalate as soon as the file starts to drift. Route to manual review when lane evidence conflicts across screens, applicant statements change, or multiple interpretations remain plausible. Risk increases when enforcement capacity is limited or governance safeguards are weak, so keep the outcome explicit in the record: simplified lane pending confirmed fit, standard lane pending confirmed fit, or manual review required.

You might also find this useful: How to Choose a Tax Preparer for Your Freelance Business.

Qualify freelancer eligibility with explicit pass-fail checks#

Treat Regime Forfettario as a qualification gate, not a label. If you cannot connect the lane to registration facts, gross-income evidence, and a reviewed residency or employment picture, keep the profile unverified.

Anchor the check to Partita IVA registration facts#

Start from records you can reconcile, not self-described claims. Use the applicant's codice fiscale, AA9/12 registration data or draft, selected ATECO code, chosen tax regime, and a plain-language description of the services sold.

Run one core pass-fail check first. Does the activity record support a Forfettario posture? The grounded threshold is Euro 85,000 per year, measured on gross income invoiced to clients, not profit after costs. If the applicant answers with net earnings or post-expense margin, the check is not complete. If the ATECO code, service description, and revenue model do not align, stop automation and hold the lane.

Review residency and employment before confirming the lane#

Review residency and employment before you confirm the lane, and avoid claiming rules that are not evidenced in the file. If residency is split across countries, the work location is unclear, or the person is also employed, keep the lane as pending review.

Use a simple operator test. Can someone explain from documented facts why residency and employment do not block the proposed lane? If not, escalate.

Route conflicts to manual review immediately#

Send the case to manual review when any of these appear:

- projected invoiced income is over, or too close to confidently stay below, Euro 85,000

- residency or employment evidence is missing, conflicting, or changes across screens

- AA9/12 data, ATECO code, and business description do not align

- the applicant may be relying on older small-taxpayer rules from an earlier start year

When evidence is conflicting or incomplete, require case-by-case review and record the reason. For uncertain cases, verify with Agenzia delle Entrate and INPS before marking the profile eligible.

Register correctly with the tax authorities in the right order#

After eligibility, treat registration order as a control gate, not an admin task. Keep invoices and production payouts off until identity prerequisites, agency interaction, and issued registration data reconcile in one record.

Confirm the Codice Fiscale before any Partita IVA filing step#

Start with identity. Before applying for a Partita IVA, the freelancer must already have a Codice Fiscale. Verify the identity and residence documents in your file against that tax code before moving forward.

Use one pass-fail checkpoint. Can you tie the applicant to one tax code without spelling or residency ambiguity? If not, stop and resolve the record before any filing handoff.

Record the Agenzia delle Entrate interaction and avoid hardcoding a single deadline#

Document the Agenzia delle Entrate step in your operating record, including who filed, when, and what was returned. If your workflow uses a specific filing form, tie it to the official AA9/12 model and instructions rather than relying on legacy process notes.

Do not hardcode one timing rule into product logic without current confirmation. Some guidance says freelancers should apply before starting activity, while other guidance describes registration within 30 days of starting activity. Because tax and contribution rules can change, confirm current requirements with official bodies and a qualified local advisor before operational go-live.

Reconcile registration outputs before enabling payouts#

Enable payouts only after the registration output reconciles to onboarding data. Confirm the issued Partita IVA is present as an 11-digit code and that the core identity and activity details used operationally match the registered result.

A practical failure mode is a valid number tied to details your invoicing or payout flow no longer reflects. If identity, activity description, or beneficiary records do not reconcile cleanly, hold for manual review before live money movement.

Need the full breakdown? Read A Deep Dive into the US-France Tax Treaty for Freelance Performers.

Map VAT obligations to invoicing and platform controls#

Treat this as a control design problem. Having a Partita IVA and applying the right VAT invoicing treatment are related, but they are not the same decision. Store tax ID, tax lane, and invoice treatment as separate fields, and require them to reconcile before the first invoice is issued. The Agenzia delle Entrate page on fattura elettronica per i forfettari should sit in the control packet for invoice-path decisions.

Separate registration identity from VAT handling#

A Partita IVA confirms registration identity. It does not, by itself, define which invoice path your system should use for each customer case.

Keep lane classification explicit from the start: Regime Forfettario versus Regime Ordinario. If both lanes are collapsed into one generic profile, invoice logic and customer messaging can drift from the registered setup, and compliance risk increases, including potential penalties.

Require a minimum invoicing record before invoice creation#

Before invoice release, require one operational record that an operator can review from start to finish:

- VAT or tax registration number from the reconciled setup record

- tax-lane flag: simplified lane or Regime Ordinario

- activity description captured at registration

- customer country and billing-entity details

- dated reviewer note confirming the lane-to-invoice mapping

If a reviewer cannot explain why this customer is routed through this invoice lane from the record alone, hold issuance.

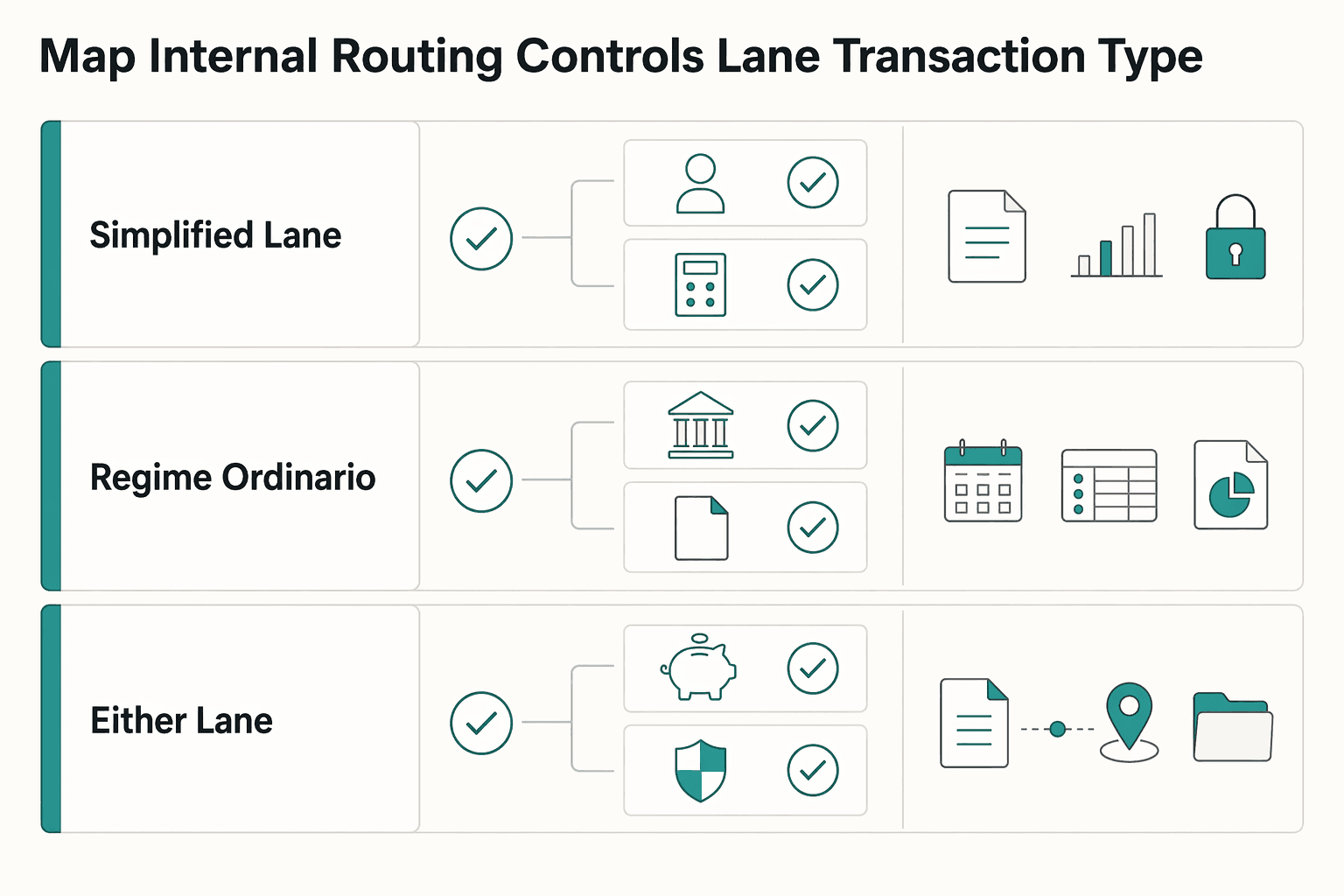

Map internal routing controls by lane and transaction type#

| Lane and transaction type | What should be on file | Platform control |

|---|---|---|

| Simplified lane, domestic customer | Tax or VAT registration number, simplified-lane flag, activity record, customer country = Italy | Route to the simplified invoice path; do not default to Ordinario messaging |

| Regime Ordinario, domestic customer | Same core record set, lane flagged as Ordinario | Route to the Ordinario invoice path; require finance review if VAT handling is not fully configured |

| Either lane, cross-border customer | Core record set plus customer country and a cross-border review note | Block auto-issuance until manual cross-border review is complete |

Add a cross-border verification gate#

Cross-border cases should have a review gate. Require a manual check when customer geography, residency facts, or other tax-treatment uncertainty appears in the file.

That gate should confirm current residency evidence, correct customer location data, and reviewer sign-off before release. If facts are unclear, do not infer treatment from Partita IVA status or generic tax residency guidance. Escalate and document the basis for the decision first.

If you want a deeper dive, read A Guide to Italy's 'Regime Forfettario' for Freelancers.

Before you automate invoice rules, run each VAT ID through the VAT number validator and store the result in your onboarding evidence pack.

Model effective burden instead of headline flat-tax claims#

Model total burden, not just the headline rate. Under Regime Forfettario, treat taxable-base assumptions, income-tax assumptions, and social contributions as separate inputs. Confirm that the declared activity and ATECO Codes support the model before you automate.

Build a three-layer burden model#

Use one operator-owned worksheet per applicant. The goal is not perfect forecasting. It is to stop pricing, payout, or margin assumptions from breaking once the real burden is applied.

Model these three layers separately:

- Revenue assumption

Use expected annual gross revenue from the onboarding record. If the freelancer gives a wide range, model at least a base case and a higher case.

- Taxable-base assumption linked to ATECO activity

Record the declared activity and selected ATECO Codes. ATECO classification is part of how tax is determined, so vague or shifting activity descriptions weaken the model immediately.

- Tax and contribution layers

Apply the assumed income-tax rate for the simplified lane, then model social contributions as a separate burden line. The INPS iscrizione liberi professionisti service page and the latest published Gestione Separata aliquote notice are the right starting points for contribution controls. A flat-tax label does not mean total payments equal the headline tax percentage.

Before automation, require one reviewer note that explains why the chosen ATECO mapping, revenue assumption, and lane are coherent for that freelancer profile.

Treat the 5% and 15% figures as lane markers, not final outputs#

Treat 5% and 15% as branch logic inside the simplified lane, not as a complete burden result. One source frames this as approximately 5% effective income tax in the first five years, then 15% afterward, but that still excludes social contributions.

Store at least four modeling fields:

- selected lane: simplified lane

- assumed income-tax rate used in the model

- separate social-contribution assumption

- model-freshness date and reviewer

Keep freshness visible. The source framing is time-bounded to early 2026, warns that tax and contribution rules change regularly, and notes that some 2026 updates linked to Law No. 199 of 30 December 2025 may still need implementing guidance.

Contrast scenarios by activity, not just by rate#

Compare scenarios by activity, not just by the tax figure. Different ATECO Codes can change taxable-base determination, so equal gross revenue does not guarantee equal effective burden.

| Scenario | What changes | Why headline rate misleads |

|---|---|---|

| Stable single-service activity | Cleaner activity mapping and taxable-base assumption | The 5% or 15% headline still excludes social contributions |

| Mixed-service activity | Classification can be less stable across revenue streams | ATECO uncertainty can distort the taxable-base assumption before tax is applied |

| Evolving offers during the year | Revenue model and activity description may shift | Early assumptions can break as actual activity changes |

The practical comparison is eligibility, real costs, and duration, not headline rate alone. Keep the cross-regime boundary explicit too. If a profile no longer fits simplified assumptions, stop treating it as interchangeable with the ordinary progressive system, where one source notes IRPEF can reach 43% at higher income levels.

Escalate uncertainty instead of hiding it in automation#

If effective-burden uncertainty is still high after modeling, delay automation and require assisted onboarding. Treat these as high-uncertainty triggers:

- ATECO classification is unclear or likely to change

- social-contribution assumptions are not supportable with current facts

- model logic depends on interpretations not refreshed against current guidance

At that point, require verification with Agenzia delle Entrate, INPS, and a qualified commercialista before enabling self-serve estimates or production payout assumptions. Keep an auditable evidence pack: declared activity, selected ATECO record, expected revenue range, modeled tax lane, contribution assumption, review date, and escalation note.

In tooling, always show the tax layer, contribution layer, and model freshness date together. For implementation details, see How to Automate Your Freelance Tax Preparation.

Design payment operations for Italian freelancer cohorts#

Design this lane so unverified Italy-specific assumptions do not trigger automatic payout release. Treat country-specific tax data as records to verify before automation, and keep payout decisions tied to auditable evidence.

The grounding sources support a cautious design posture. They are discussion or study documents, they may contain errors, and they are not presented as official Commission positions. Use them to shape internal controls, then complete primary-source checks before treating country-law assumptions as production rules.

Map the records that drive payout decisions#

Define the records your system relies on through primary legal and provider sources before automating release logic.

Avoid collapsing all checks into one generic "verified" state if that would hide review context needed for investigations.

Release payouts against evidence, not lane labels#

Release payouts against evidence, not labels. Keep Italy-specific KYC/AML gating and tax-entity alignment rules in manual review or separately verified policy until confirmed from primary sources.

Use a hard hold when required evidence is incomplete and a reviewer cannot confirm release conditions.

Define mismatch handling before launch#

Define stop conditions before launch for incomplete, contradictory, or stale records, based on requirements you can verify in primary sources.

When a trigger fires, open an exception case, log the mismatch, capture reviewer action, and require corrected data or explicit approval.

Keep a minimum audit trail finance can use#

As an internal control baseline (not as a legal conclusion), retain and export a minimum evidence pack for each payout decision:

- request

- approval record

- provider or transaction reference

- reconciliation output

If you cannot produce that chain for released payouts, pause automation for this lane until the evidence path is complete.

For a step-by-step walkthrough, see Germany Freelance Tax Decisions for Globally Mobile Consultants.

Build compliance checkpoints and ownership across teams#

Assign separate owners and checkpoint gates before you scale an Italy lane, and treat Italy-specific legal criteria as items to confirm rather than assumptions to automate.

Assign named owners for each decision class#

Use an owner matrix, not a generic compliance bucket. One owner handles tax interpretation, one validates onboarding record integrity, and one controls payout release.

For Italy-tagged files, keep those ownership lines explicit when records reference residency or taxpayer-registration evidence. The source-backed control logic is general: VAT administration depends on registration and taxpayer identification, invoicing and bookkeeping requirements, and penalties when records are wrong. Any Italy-specific form rules or evidence standards should be confirmed separately.

Each approved case should show who signed off on interpretation, who verified records, and who released payout capability.

Gate onboarding on record integrity, not applicant claims#

Gate approval on record integrity, not applicant claims. If your process collects residency or taxpayer-registration evidence, require those records to be complete and internally consistent before approval.

Do not treat a single field like "has a VAT number" as sufficient on its own. Review onboarding identity, taxpayer ID fields, invoicing profile, and payout beneficiary setup together, and hold the case when they conflict.

Escalate ambiguous residency cases early#

Do not let frontline reviewers resolve ambiguous residency claims ad hoc. Route those files to the tax-interpretation owner with a required evidence pack and pause automation until a documented decision is returned.

Use concrete internal triggers such as conflicting residency signals or incomplete location evidence. If treaty treatment or country-specific legal thresholds are in scope, confirm those criteria separately with qualified local guidance.

Constrain PII access and make every touch auditable#

Keep access tight and every touch auditable. Collect only the fields needed for registration, taxpayer identification, invoicing, and payout controls. Mask sensitive values where full display is unnecessary, and log access, edits, and exports.

This keeps controls usable in practice, not just on paper. Test one case from start to finish and confirm you can answer three questions: who accessed the file, what changed, and what evidence supported approval. These controls support process integrity, but they do not by themselves establish country-specific legal compliance.

Common mistakes and how to recover fast#

When a case goes off track, recover in this order. Pause automation. Re-check tax-lane classification and registration records. Resume invoicing or payouts only after the file is internally consistent.

Re-qualify tax lane assumptions#

Treating Regime Forfettario as automatic is a common error. It is a specific flat-rate regime, not a default for every freelancer, so cases should be re-checked against the ordinary lane when facts change.

Use clear triggers: expected or actual gross income near the Euro 85,000 annual threshold, or a freelancer who started under earlier rules that may still apply. The reduced 5% rate for the first five years is a separate issue and does not make eligibility automatic. Record why the case stays in the simplified lane or moves to ordinary taxation, along with the owner and review date.

Reconcile registration records before releasing payouts#

Do not enable payouts while tax registration records are still inconsistent. Setup errors at the VAT or INPS stage can turn into delays, fines, or incorrect tax treatment later.

Use a strict pre-payout gate: Partita IVA/tax ID data, registration details, invoicing profile, and payout beneficiary setup should match before release. If they conflict, hold the account until reconciled. One reviewer should log the reconciliation result, and any mismatch is a stop signal.

Reclassify invoice handling by lane and rerun VAT checks#

Generic invoice templates can be a failure point. For Italy lanes, VAT treatment should be tied to the correct classification and transaction context.

Recovery is operational: reclassify affected invoices, then rerun controls. At minimum, confirm each invoice uses the correct VAT codes and required electronic format. Sample one invoice per active lane and confirm VAT handling matches the stored lane for that freelancer.

Escalate unresolved edge cases and log the interpretation source#

If a file depends on interpretation rather than clear records, escalate early. This matters most when older-rule application, VAT handling, or INPS assumptions are unclear.

For unclear situations, verify with Agenzia delle Entrate or INPS, then log the authority checked, decision owner, and decision date. Keep automation paused until the interpretation is documented. Missed filing deadlines can trigger automatic penalties or interest, and misestimation can cause overpayments, underpayments, or year-end bill shocks.

Conclusion#

For an Italy launch, decide on eligibility certainty, effective burden, and compliance-operational fit first, not a headline flat-tax rate. That matters even more in 2026. Updates tied to Law No. 199 of 30 December 2025 may still need implementing guidance, so a clean summary is not the same as a production-ready policy.

- Confirm cohort and lane before onboarding.

Separate profiles that appear eligible for Regime Forfettario from profiles that may require a different path, and do not rely on user self-selection or marketing copy for that decision. If eligibility is unclear, hold for manual review.

- Validate the document pack before setup.

Confirm the required identity and tax-profile inputs for the chosen lane. Keep one canonical record so onboarding, invoicing, and payouts do not drift.

- Reconcile registration output with invoicing data.

Before enabling invoices or payouts, ensure the recorded tax profile, invoice setup, and beneficiary data align. If finance cannot trace the profile without interpretation, treat it as not ready.

- Model real burden, not just reported headline rates.

Figures like 5% for the first five years, then 15% should be treated as reported examples, not guaranteed outcomes. Include social contributions in your go-live scenarios.

- Enable payouts only after compliance gates pass with an audit trail.

Registration alone is not the finish line. Go live only after lane decision, document checks, registration output, and invoicing profile have all passed review and are documented.

If eligibility is uncertain, burden modeling is headline-only, or records do not reconcile cleanly, do not automate yet. Verify with Agenzia delle Entrate and treat Italy as a controlled rollout.

If your Italy checklist is complete and you want to confirm payout and compliance coverage for your cohort, talk with Gruv.

Frequently Asked Questions

What is Regime Forfettario and who can use it with a Partita IVA?

Regime Forfettario is a special flat-rate tax scheme for self-employed activity run through a Partita IVA, which is Italy's VAT identification number for freelancers and businesses. The practical screen includes gross invoiced income up to the Euro 85,000 annual threshold, with final eligibility confirmed against current Agenzia delle Entrate guidance. For onboarding, verify the freelancer's Codice ATECO and expected gross revenue, because the threshold is based on gross income, not profit after costs.

Is the reduced starter rate automatic, or are there qualification conditions?

It is not automatic. The 5% for the first five years is described for start-ups, but only when qualification conditions are met. One cited condition is that the person has not previously carried out the same job activity in the relevant way.

Does flat tax in Italy mean there are no other contributions to pay?

No. Flat tax here covers income tax treatment, but social contributions still apply. For freelancers registered solely with INPS Gestione Separata, the 2025 contribution rate is approximately 26.07% of taxable income, and enrolment with INPS is required within 30 days after registration.

What is the difference between Regime Forfettario and Regime Ordinario for operators?

The first is the special flat-rate scheme, while Ordinario is the alternative VAT-account regime. In practice, treat them as distinct options and base the choice on verified registration and activity facts.

Do these rules fully define every VAT and exclusion edge case?

No. Not every VAT exclusion, cross-border, treaty, or residency edge case is covered here. What is supported is narrower: freelancers invoicing in Italy need a Partita IVA, and electronic invoicing is mandatory for all Partita IVA holders since 2024. If a case depends on interpretation, confirm it with Agenzia delle Entrate before proceeding.

Which documents are required first: Codice Fiscale, AA4/8 form, or AA9/7 form?

From the evidence here, Codice Fiscale comes first. The cited registration flow then references Form AA9/12 submitted to Agenzia delle Entrate, plus identity documents and activity classification details. Do not hardcode AA4/8 or AA9/7 for this flow from this article alone. Before proceeding, make sure the tax code, identity record, submitted registration form, and selected ATECO activity are aligned.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: