Quick Answer

To choose a tax preparer for freelancers, use a compliance-first framework instead of picking on price alone. Start by classifying your case, run baseline screening questions, and compare candidates with a scorecard focused on scope, documentation, and risk controls. If your facts include cross-border movement or foreign accounts, escalate to specialist support and require written handling for FBAR and Form 8938.

Choose Your Tax Preparer With a 10 Minute Compliance First Framework#

Choose a tax preparer for freelancers by ranking compliance controls ahead of speed and price, then shortlist only candidates who can show strong documentation habits.

| Check | Pass | Reject |

|---|---|---|

| Will you sign the return and include your PTIN? | Yes | No |

| Are you available year-round after filing season? | Yes | No |

| Can you share how I should review complaint or disciplinary history? | Yes | No |

| Do you ever charge fees based on a percentage of refund? | No | Yes |

| Will you refuse to ask me to sign a blank return? | Yes | No |

If you're a globally mobile consultant, the tension is simple: you want fast filing, reasonable cost, and low compliance risk at the same time. As a business-of-one, you need a tax preparer who runs on controls, not vibes. Most hiring advice stays generic and stops helping the moment your facts get messy across locations, clients, and filing obligations. This guide gives you a practical shortlist decision and a hiring script you can use right away.

This playbook helps you choose the right tax preparer or tax professional for your case, but it does not provide legal advice. Use this compliance-first framework:

- Step 1. Define the decision boundary.

Write your goal in one line: compliant filing with documented assumptions. Then set your shortlist rule: only interview candidates whose scope matches your risk profile, because preparers can have different levels of skill and qualifications. Verification point: you can explain why each shortlisted candidate fits your complexity, not just your budget.

- Step 2. Run a non-negotiable compliance screen.

Ask each candidate direct yes or no questions before discussing fees.

- Will you sign the return and include your PTIN?

- Are you available year-round after filing season?

- Can you share how I should review complaint or disciplinary history?

- Do you ever charge fees based on a percentage of refund?

- Will you refuse to ask me to sign a blank return?

Reject any candidate who fails these checks. Keep one rule front and center: you stay responsible for what gets filed, even when someone else prepares it. Verification point: your list now contains only candidates who pass baseline compliance safeguards.

- Step 3. Apply the safe default when facts are unclear.

Prioritize documentation quality and specialist scope over aggressive assumptions. In a hypothetical case where you split time across countries and client locations, choose the preparer who documents uncertainty, states escalation triggers, and narrows claims to supportable facts. If your case looks basic and you qualify, community options like VITA can still be a valid route for free basic prep. Verification point: you can name one safe-default candidate and one backup, each with clear scope boundaries.

If your work pattern stays highly mobile, pair this framework with The Ultimate Digital Nomad Tax Survival Guide for 2026 before final selection.

What You Need Before You Start#

Assemble one complete, compliance-ready prep packet before you interview anyone, so your tax preparer can evaluate risk without guessing.

| Checkpoint | Rule or condition | Review note |

|---|---|---|

| Schedule SE | Generally triggered when net self-employment earnings are $400 or more | Organize documents for annual filing and quarterly estimates |

| New York statutory residency | Both conditions apply: a permanent place of abode and 184 days or more in-state | Map personal and client locations before interviews |

| FBAR review | Uses a foreign account aggregate threshold and follows its own filing flow, separate from the IRS return | Collect prior FBAR records if they apply |

| Form 8938 review | Thresholds vary by filing status and residence | Review separately from FBAR |

To run clean interviews, you need clean inputs. A CPA, Enrolled Agent, or other tax professional can only move fast when your records are structured and your assumptions are visible.

Before You Start

Create one working folder for this tax year and keep every filing document in that single place.

| Packet item | Why it matters | Verification point |

|---|---|---|

| Prior-year return | Supports current estimated tax planning | You can reference it for current-year estimates |

| Income and expense logs | Supports accurate business reporting | Every deposit maps to an income category and every expense has support |

| Location footprint notes | Flags jurisdiction and residency complexity | You can show where you lived and where clients operated |

| Cross-border compliance notes | Surfaces FBAR and Form 8938 review needs | You can show prior filings or a clear "not applicable yet" note |

- Step 1. Assemble your IRS workflow file.

Gather your prior-year return, current income logs, expense categories, and current-year estimates. Self-employed filers generally file an annual return and pay estimated taxes quarterly, so organize your documents around that cadence. Include a Schedule SE checkpoint because Schedule SE is used to calculate self-employment tax, and filing is generally triggered when net self-employment earnings are $400 or more. Verification point: your packet supports both annual filing and quarterly estimate planning.

- Step 2. Map your location footprint before interviews.

List your personal locations and client locations in one timeline, then mark jurisdictions that can change filing complexity, including New York. New York can treat someone as a statutory resident when both conditions apply: a permanent place of abode and 184 days or more in-state. If you split work between two countries and keep a regular New York base, this map prevents unsafe residency assumptions. Verification point: you can explain your location pattern in two minutes.

- Step 3. Pull cross-border compliance history early.

Collect prior FBAR and Form 8938 records if they apply to you. FBAR uses a foreign account aggregate threshold and follows its own filing flow, separate from the IRS return. Form 8938 review does not replace FBAR review, and Form 8938 thresholds vary by filing status and residence, so your process should test both when relevant. Verification point: your file shows what you filed before and what needs review now.

- Step 4. Export operating records for handoff.

Prepare invoice trails, payout trails, and reconciliation exports from your accounting and payment tools. Add supporting documents like invoices, receipts, deposit records, and paid bills so your tax professional can trace each material number quickly. Verification point: a reviewer can trace income and expenses without asking for scattered screenshots.

Should You Use Free Tax Prep a Marketplace Preparer or a Specialist Firm?#

Use a triage matrix to match your case complexity to a service model, then default to specialist support when foreign reporting or residency uncertainty appears.

Your packet is your leverage. Use it to choose the right service lane without trading compliance safety for short-term speed.

| Option | Best fit | Risk limits | Verification point |

|---|---|---|---|

| NYC Free Tax Prep or local SETP support | Basic, mostly local returns with straightforward records | Eligibility and scope rules apply. NYC self-employed support includes income and business-expense limits. | Staff confirms your case fits program scope before intake. |

| Marketplace tax preparer (for example, Upwork) | Moderate complexity when you can vet process quality yourself | Quality varies by provider. You must screen credentials, scope, and documentation standards. | Candidate gives a clear scope, response cadence, and post-filing support terms. |

| Specialist tax professional or firm | Cross-border facts, residency uncertainty, or foreign asset reporting risk | More involved engagement, but often a better fit when complexity rises. | Team explains assumptions, escalation triggers, and evidence requirements in writing. |

- Step 1. Classify your case before you shop.

Label your case as basic, moderate, or specialist based on jurisdiction spread, account structure, and reporting exposure. If your work and life stay mostly local, start with community options. If your facts cross borders, move up a lane right away. Verification point: you can defend your classification in two sentences.

- Step 2. Route to the lowest-risk lane, not the cheapest lane.

Use free programs when your facts are simple and the program confirms fit. Use marketplace hiring only when you can run strict vetting. Move to a specialist tax professional when complexity grows, then compare candidates on scope quality, not brand claims. Verification point: your shortlist includes only providers whose scope matches your risk level.

- Step 3. Apply a foreign-reporting risk gate before filing.

If your foreign accounts exceed $10,000 in aggregate at any point in the year, treat that as a specialist trigger. Review Form 8938 separately because thresholds can vary by filing status and residence context, and not every taxpayer files both forms. In a hypothetical case where you live abroad, serve US clients, and hold multiple foreign accounts, skip generic filing-only help and start with specialist support. Verification point: your selected provider states how they handle FBAR (FinCEN Form 114), Form 8938, and escalation paths.

If you need a deeper specialist shortlist for mobile cases, start here: The Best Accounting and Tax Advisors for US Expats.

Do You Need a CPA or an Enrolled Agent for Your Case?#

Pick the professional whose scope matches your risk, then lock ownership in writing before you hire.

Once you know your lane, pick the credential that matches how you operate. Multiple professionals can prepare returns, but only a clear scope prevents gaps during quarterly planning and post-filing support.

Use a simple standard in your interviews: secure compliance coverage first, then pursue optimization.

| Role | Best fit | What to verify before hire |

|---|---|---|

| CPA | Planning-heavy work, business complexity, and forward-looking strategy (especially when the CPA specializes in tax) | Confirm they will own tax planning cadence, not just return prep |

| Enrolled Agent | Tax procedure execution and direct IRS representation support | Confirm they will handle notices, audits, collections, and appeals support scope |

| Any PTIN tax preparer | Basic federal return preparation | Confirm limits of representation rights and escalation path |

- Step 1. Match credential to workload complexity.

Start with your workload, not job titles. If you need heavier planning around changing business decisions, a CPA often fits better. If you need strong tax procedure execution and representation depth, an Enrolled Agent may fit better. Both CPAs and Enrolled Agents can represent clients on audits, collections, and appeals. Verification point: you can explain why this credential fit reduces your highest compliance risk.

- Step 2. Force explicit ownership in writing.

Require each candidate to list exactly what they own before you sign:

- Year-end return preparation and review

- Quarterly planning workflow and deadlines

- Residency guardrails and assumption tracking

- Post-filing support, including notice handling

Verification point: each candidate sends a scope statement that names owner, timeline, and deliverables.

- Step 3. Stress test technical depth with trigger questions.

Ask for concrete answers on freelancer issues. A strong candidate should explain when Schedule SE applies, including the self-employment earnings trigger. They should also separate Form 8938 analysis from FBAR (FinCEN Form 114), because these obligations run under separate rules and can both apply.

- Step 4. Run one realistic scenario before selection.

Use a short hypothetical: you work across borders, receive payments in multiple accounts, and need clean quarterly decisions. Ask each tax professional to walk through forms, assumptions, and escalation triggers in order. Verification point: the candidate gives a clear, sequential plan without vague handoffs.

This helps you choose based on execution quality, not credential labels.

What Questions Should You Ask Before You Hire?#

Ask every candidate the same compliance-first interview script, then hire the one who proves scope, documentation discipline, and secure operations.

| Proof request | What to confirm | Verification point |

|---|---|---|

| Scope template | Same scope template from every candidate | Clear owners and dates |

| Notice support clause | What they handle, what they escalate, and what costs extra | Written clause defines notice support |

| FBAR/Form 8938 decision memo | How they decide if FBAR, Form 8938, or both apply | Clear decision memo, not a verbal shortcut |

| Workflow and security process | Secure intake, document tracking, and organized records | Documented process map before kickoff and a maintained WISP |

Credentials get you to the table. Process is what keeps you safe. Use one script, demand written proof, then compare answers side by side.

| Interview block | Ask this question | Strong answer includes |

|---|---|---|

| Communication cadence | How often will we review estimates, deadlines, and open risks? | Fixed cadence, response window, named owner |

| Filing sign-off | Who prepares, who reviews, and who signs final filings? | Clear workflow, PTIN confirmation, final review before you sign |

| Support boundaries | What happens if the IRS follows up after filing? | Defined notice support scope and fees |

| Foreign reporting | How do you separate FBAR from Form 8938 analysis? | FinCEN filing flow, IRS filing flow, written assumptions |

| Data security | How do you protect my records end to end? | Secure intake process and a maintained WISP |

- Step 1. Standardize your interview script.

Ask every tax professional the same core questions on cadence, turnaround, and sign-off ownership. Confirm that they are available year-round for follow-up questions after filing season. Verification point: each candidate returns the same scope template with clear owners and dates.

- Step 2. Lock notice and post-filing support terms.

Ask, "If an IRS notice arrives, what do you handle, what do you escalate, and what costs extra?" Get boundaries in writing before engagement. Verification point: you can point to a written clause that defines notice support.

- Step 3. Probe documentation standards for FBAR and Form 8938.

Ask what records and receipts they require, how they document assumptions, and how they decide if FBAR, Form 8938, or both apply. Require them to explain that FBAR runs through FinCEN and does not replace Form 8938 analysis. In a hypothetical cross-border case, ask them to walk from facts to filing decision step by step. Verification point: they produce a clear decision memo, not a verbal shortcut.

- Step 4. Validate secure workflow and status visibility.

Ask which secure channel they use for intake, how they track document completion, and how they keep records organized. Request confirmation that they maintain a Written Information Security Plan. Verification point: you receive a documented process map before kickoff.

Run a Vetting Scorecard and Pick a Safe Default#

Score candidates with a compliance-first scorecard, run hard fail gates first, and break close calls with documentation quality.

Interviews create impressions. A scorecard turns them into a decision you can defend. Use one scorecard for every candidate so community programs, marketplace talent, and specialist providers are evaluated on the same standards.

| Score area | What to measure | Priority to set upfront | Hard fail trigger |

|---|---|---|---|

| Capability | Technical depth for freelance and cross-border issues | High / Medium / Low (set before interviews) | Cannot explain Schedule SE and when the $400 self-employment trigger matters |

| Responsiveness | Turnaround time, clarity, and ownership | High / Medium / Low (set before interviews) | Gives vague answers on who owns filing sign-off and follow-up |

| Process quality | Checklist rigor, assumption logs, audit-ready records | High / Medium / Low (set before interviews) | Cannot show a documented workflow for intake, review, and approval |

| Risk controls | FATCA, Form 8938, FBAR, and FinCEN handling | High / Medium / Low (set before interviews) | Treats Form 8938 and FBAR as interchangeable, or gives vague FBAR/FinCEN filing handling |

- Step 1. Set your priorities before scoring.

Set your score priorities to match your risk profile, then keep them fixed across all candidates. If your case includes foreign accounts or residency uncertainty, raise the risk-controls priority and keep your logic consistent. Verification point: you can explain your priority logic in one sentence.

- Step 2. Run hard fail gates first.

Disqualify candidates before comparing total scores if they miss core compliance checks.

- Weak Schedule SE explanation

- Weak FATCA or Form 8938 reasoning

- Vague FBAR and FinCEN process ownership

- Unclear escalation path for edge cases

Verification point: only candidates who pass every gate stay on your shortlist.

- Step 3. Compare service-model fit side by side.

Use community support like NYC Free Tax Prep only when your case fits local eligibility and scope. That route uses IRS-certified VITA/TCE volunteer preparers and advertises year-round assistance in NYC. Use marketplace sourcing like Upwork as a sourcing channel, then verify credentials and process quality yourself. Move to specialist support when complexity rises, especially when cross-border issues are in scope.

- Step 4. Pick the safe-default winner.

When two finalists score close, choose the one with clearer documentation discipline and a stronger escalation policy. That choice usually gives you better long-term freelance tax help than a slightly cheaper quote with weaker controls. Verification point: your chosen tax preparer gives you a written scope, a filing timeline, and explicit post-filing support boundaries.

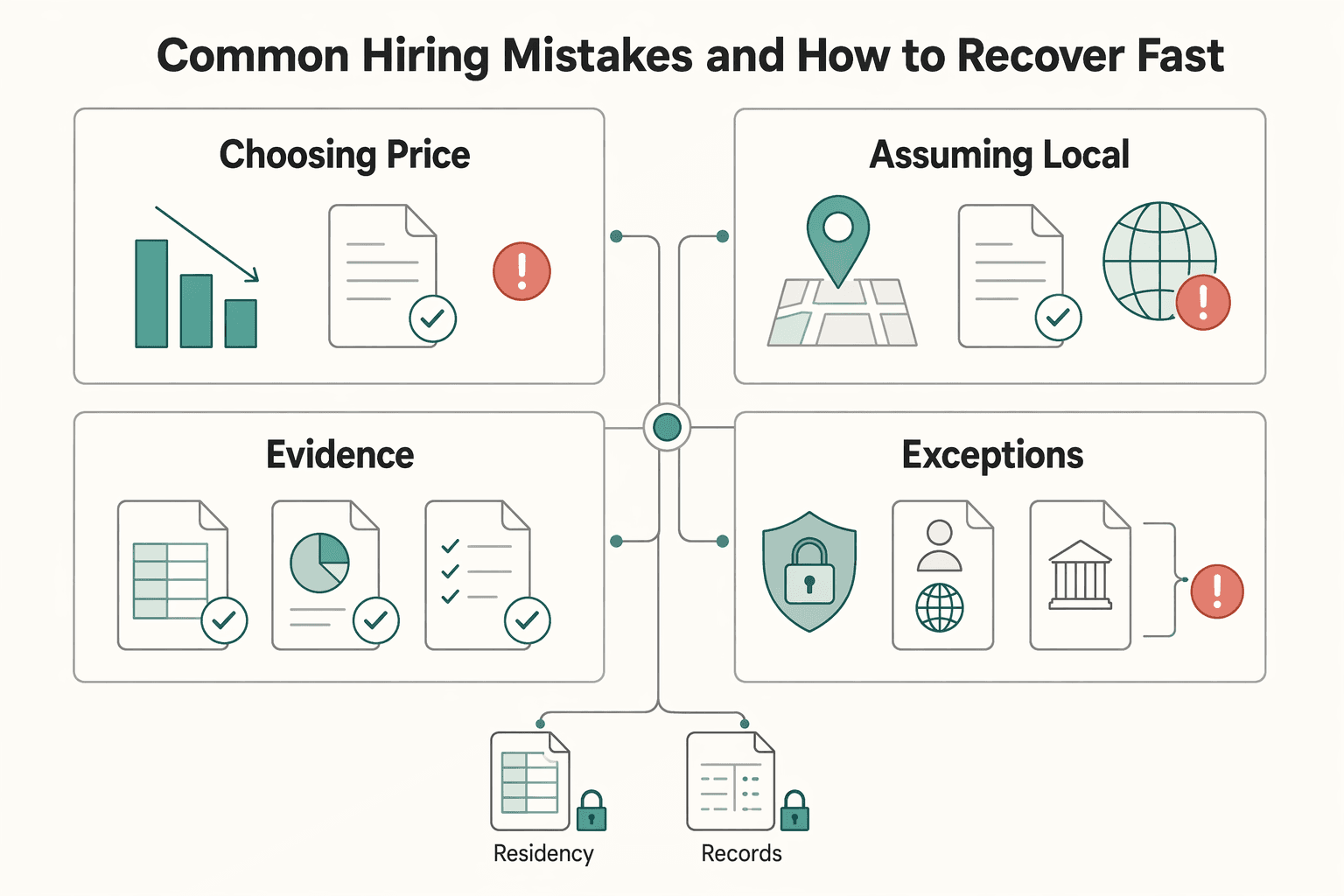

Common Hiring Mistakes and How to Recover Fast#

Fix hiring mistakes by pausing quickly, re-screening with compliance gates, and restarting only after scope, records, and escalation rules are written.

Before filing work starts, stress test your decision. This is where you prevent a rushed hire from turning into rushed assumptions.

| Mistake | Why it hurts | Fast recovery |

|---|---|---|

| Choosing on price alone | Low fees can hide weak scope and weak controls | Re-screen promptly with your scorecard and include a CPA and an Enrolled Agent option |

| Assuming local-only rules while mobile | You can miss separate cross-border reporting duties | Add a checkpoint for FBAR and Form 8938 before submission |

| Starting with incomplete records | Gaps create bad assumptions and rework | Pause filing, rebuild logs, then restart with explicit milestones |

| Skipping escalation rules | Edge cases stall and errors compound | Add written triggers for specialist referral on FinCEN or multi-jurisdiction conflicts |

- Step 1. Re-screen price-first choices promptly.

Use your weighted scorecard again and add at least one CPA and one Enrolled Agent alternative. Reject any tax preparer who prices on a percentage of your refund, and verify that the paid preparer has a PTIN. Verification point: you hold a written scope, fixed fee logic, and named owner for filing sign-off.

- Step 2. Add a cross-border compliance gate before submission.

Treat FBAR and Form 8938 as separate determinations. FBAR (FinCEN Form 114) is not filed with the IRS, and one form does not replace the other. Check the thresholds directly: FBAR uses aggregate foreign account value above $10,000 at any time in the year, while Form 8938 has its own threshold tests. Verification point: your checklist shows a yes or no decision for each form and who documented it.

- Step 3. Pause filing when records are incomplete.

Rebuild source logs, receipts, and reconciliation exports first, then restart. Good tax help starts with complete records, not quick assumptions. If you move countries midyear and open a foreign payout account, halt submission and rebuild the account and residency logs before review. Verification point: your workflow shows intake complete, assumption review complete, and final approval pending.

- Step 4. Write escalation triggers into the engagement.

Define when your preparer must refer to a specialist, including FinCEN issues, conflicting multi-jurisdiction facts, or representation needs. Only attorneys, CPAs, and enrolled agents can represent taxpayers in all IRS matters. Verification point: your engagement notes include referral triggers, response times, and handoff ownership.

Use this recovery loop whenever you need to hire under time pressure without giving up compliance control.

Use This Final Checklist and Make the Decision Today#

Choose the tax professional who passes compliance gates, documents scope clearly, and commits to written execution dates, then onboard immediately.

Skip another round of research and run the checklist. Pick the safest operator, then move.

| Checklist area | What to confirm before you decide | Pass signal |

|---|---|---|

| Credentials | PTIN status, plus whether your lead is a CPA, Enrolled Agent, or attorney when representation depth matters | Paid preparer has a PTIN and can explain representation scope clearly |

| Scope and fees | Exact deliverables, deadlines, and fee model | Clear pricing and support boundaries in writing |

| Records readiness | Income, expense, and supporting documents organized for review | Preparer asks for records and receipts before drafting |

| Cross-border screening | Separate review for FBAR and Form 8938 decisions, including thresholds and due dates | Written yes or no decision for each filing track |

- Step 1. Define case complexity and build a focused shortlist.

Classify your case as local or cross-border, then shortlist candidates who match that complexity. If you can, compare multiple options so you can see differences in process quality and ownership. Prioritize documentation standards over the lowest quote. Verification point: each candidate gives you a written scope and confirms who signs and files.

- Step 2. Run interviews and enforce hard decision gates.

Ask every tax preparer about fee structure, post-season availability, and notice support. Confirm they stay available after filing season. You stay responsible for what gets filed, so choose the operator who documents assumptions, asks for supporting records, and challenges weak inputs. Always review the return before signing, ask questions if anything is unclear, and never sign a blank or incomplete return. Verification point: you can name one safe-default winner and one backup.

- Step 3. Confirm the handoff packet against filing workflow.

Require a written workflow checklist that includes Schedule SE handling when the filing trigger applies ($400 on line 4c). If foreign accounts or assets apply, confirm separate handling for FBAR and Form 8938 because one does not replace the other. FBAR is filed electronically through FinCEN, is not filed with your federal tax return, and follows its own deadline cycle (due April 15 with an automatic extension to October 15). Form 8938 attaches to the annual return when applicable; thresholds vary by filing situation (with a commonly cited base threshold of $50,000 and higher thresholds for joint filers and taxpayers abroad). Verification point: your packet shows complete records, filing owners, and due-date accountability.

- Step 4. Lock cadence, escalation, and onboarding rules in writing.

Set kickoff date, document deadlines, communication channel, and response times before work starts. Add explicit escalation triggers for FinCEN issues, multi-jurisdiction conflicts, or scope changes that require specialist review. In a hypothetical case, your preparer discovers a new foreign account mid-process and activates the written escalation path instead of improvising. Verification point: you have one signed operating plan, a defined onboarding start date, and audit-ready documentation.

Frequently Asked Questions

How do I choose a tax preparer as a freelancer if I work across multiple countries?

Start by filtering for candidates who define cross-border scope in writing. Require a clear process for separate FBAR and Form 8938 checks, since those are distinct filings and may both apply. If you want a deeper operating checklist for mobile work, review The Ultimate Digital Nomad Tax Survival Guide for 2025.

Do I need a CPA or can an Enrolled Agent handle my freelance taxes?

A CPA and an Enrolled Agent can both help with freelance taxes, and both have unlimited representation rights before the IRS. Choose based on service scope and support needs, not title alone. Ask each tax professional what support they provide after filing season.

What should I ask a Tax Preparer before I sign an engagement?

Ask for their PTIN, exact fee structure, and whether they are available after filing season for follow-up questions. Avoid any tax preparer who charges based on a percentage of your refund. Confirm the engagement scope in writing so responsibilities are clear.

When should I use NYC Free Tax Prep or SETP instead of a paid specialist?

Use NYC Free Tax Prep or SETP when you qualify and your return fits program scope. IRS VITA and TCE programs offer free basic preparation for qualifying taxpayers, and people who generally make $69,000 or less may qualify. TCE focuses on taxpayers age 60 and older, and NYC SETP includes help with federal and New York State quarterly estimated filings. If your facts involve multi-country complexity, confirm scope first, since program services can vary.

What records should I prepare before meeting a Tax Professional?

Bring core tax forms and records, including W-2, 1098, 1099, plus your self-employment income and expense records. Add organized receipts and payout records so your tax professional can verify assumptions quickly. A clean document packet usually reduces back-and-forth.

When do FBAR, FATCA, or Form 8938 become part of preparer selection?

Treat this as a hiring screen as soon as you hold foreign accounts or other specified foreign financial assets, because rules can overlap. FBAR and Form 8938 are separate obligations, and Form 8938 does not replace FinCEN Form 114. FBAR uses a $10,000 aggregate account-value trigger at any point in the calendar year, while Form 8938 uses its own threshold tests, including the $50,000 and $75,000 example thresholds for certain U.S.-living unmarried filers. FBAR is due April 15, with an automatic extension to October 15.

What should be included in the fee and support scope so there are no surprises?

Lock the full scope in writing, including return types, quarterly work, who signs, and what post-filing support the fee covers. Add response-time expectations, escalation triggers, and a rule for handling out-of-scope work before extra fees apply. This protects you and your tax preparer from ambiguity when deadlines tighten.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Best Accounting and Tax Advisors for U.S. Expats: Pick the Right Support Level

**Pick the support level that matches your compliance surface area, then evaluate providers on written scope and form coverage.** The common failure mode for most U.S. expats is not "forgetting to file." It is hiring the wrong help model, under-scoping what you actually need, and finding the gap when IRS filings and related reporting obligations hit the critical path. You run a business-of-one, and your tax workflow is part of the system.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.