Quick Answer

The German Blue Card is a strong option if you want stable, employment-based residence in Germany and can accept an employer-linked first phase. You need a job that matches your qualification, a German or comparable foreign academic qualification, a binding contract or offer for at least six months, and salary that meets the current threshold. It is usually a weaker fit if you need full client and work-model flexibility from day one.

Is the German Blue Card the Right Strategic Move for Your 'Business-of-One'?#

Choose the Blue Card if your priority is stable, employment-based residence in Germany and you can accept an employer-linked first phase. If your priority is full client and work-model flexibility from day one, it is usually not the best first route.

The central tradeoff is control versus stability. The permit starts as residence for qualified employment tied to a specific job, so early job changes require process discipline.

Step 1. Decide what you are optimizing for#

For the next 12 to 24 months, decide what matters most: a faster settlement path and household stability, or maximum business autonomy.

| Blue Card benefit | Operational trade-off | Best-fit profile |

|---|---|---|

| Settlement path can be faster: 27 months, or 21 months with B1 German | Status is employer-linked at the start, so early changes need care | You want long-term residence and can commit to one role now |

| Family reunification terms are relaxed; spouse can work immediately without restriction | Relocation planning still needs coordination across family logistics | You are moving with a partner or family and want faster household income continuity |

| Defined EU mobility pathways and short travel options | Mobility is not unrestricted work rights across Europe | You need short cross-border travel, not open labor-market access everywhere |

| Clear qualification-and-contract route | Role, qualifications, contract, and salary must align cleanly | You already have a strong qualifying offer |

Step 2. Pre-check the hard requirements#

Before you invest more time, run this checklist:

| Requirement | What the article says |

|---|---|

| Role fit | The job must match your academic qualification. |

| Qualification path | You need a German academic qualification or a foreign qualification comparable to a German one. |

| Contract readiness | You need a binding employment contract or offer for at least 6 months. |

| Salary fit | As of 2026, the federal portal lists €50,700 for the general route and €45,934.20 for certain shortage occupations. These thresholds are updated annually, so re-check the current figures before you file. |

| Current legal detail | Verify the live eligibility rule before you rely on any summary. |

| Relocation tolerance | Be realistic about whether you can operate as an employee in Germany during the initial phase. |

Step 3. Price the dependency risk early#

For solo operators, early dependence on one employer is the real risk. The permit is issued for a specific job, and in the first twelve months job changes can be reviewed and controlled. The foreign office can suspend a change for up to 30 days.

| Point in process | What the article says |

|---|---|

| First twelve months | Job changes can be reviewed and controlled. |

| Foreign-office review | The foreign office can suspend a change for up to 30 days. |

| Before changing roles | Confirm the local process and be ready to document permit details, the new signed contract, role scope, salary details, and qualification match based on local office requirements. |

| After one year in that job | Berlin service guidance states that broader employment flexibility applies without notifying immigration authorities. If you are outside Berlin, verify local practice directly. |

Treat that as a real operating limit, not a footnote. Before you change roles, confirm the local process and be ready to document permit details, the new signed contract, role scope, salary details, and qualification match based on local office requirements. If your model depends on rapid switching, this first-year window is a meaningful limitation.

After one year in that job, Berlin service guidance states that broader employment flexibility applies without notifying immigration authorities. If you are outside Berlin, verify local practice directly.

Step 4. Make the call for this year#

This route is strongest when your near-term goal is residence stability, family setup support, and a shorter route to settlement. It is weaker when your near-term goal is unrestricted work-model autonomy.

If you already have a qualifying offer and can accept the employer-linked start, this route is often a good fit. If that tradeoff is too expensive for the way you work, pause and compare other residence routes before you sign.

Once you know the route fits on paper, the next question is not immigration alone. It is the compliance picture your move triggers.

The Compliance Landmine: Your New Tax Reality#

If you move to Germany on this route, treat your move date as a compliance checkpoint, not just an immigration milestone. Your visa process is one track, and your tax and filing position may change at the same time depending on your facts.

For relocation guidance, start with official channels. The EU EURES Germany page on europa.eu points to the Federal Government's Make it in Germany portal. EURES advisers can guide you on living conditions, and you can register for official web tutorials on topics like recognition procedures and living conditions. That does not replace tax advice, but it is a better starting point than forum posts.

Step 1. Treat your move date like a compliance deadline#

Before you relocate, build a complete first-year file. Tax-residency and filing rules are fact-specific, so verify current triggers and any exceptions with current-law guidance, not older blog summaries.

| What to verify | Why it matters to you | What to prepare before move date |

|---|---|---|

| Whether your main tax residence may shift to Germany | Your filing center can change even if you keep home-country ties | A dated timeline: arrival, housing start, employment start, and time spent outside Germany |

| Which income categories are in scope for review | You may need to assess more than payroll alone | A year-to-date income inventory by source, country, and payment date |

| Whether you may face overlapping filing tracks | A move year can create obligations in more than one country | Your latest home-country return, employer tax documents, and adviser contacts |

| Whether your year-one records are complete | Missing statements and unclear dates create preventable rework | Download statements for bank, broker, rental, and payment-platform accounts before access changes |

A useful readiness test is simple: can you hand over one organized folder with your contract, pay records, move timeline, and non-salary income records?

Step 2. Inventory every income stream, not just salary#

Salary is often only part of the file. List every income category that could matter in a cross-border review: employment pay, investments, rental income, and ongoing business or side income.

Use one spreadsheet for evidence, not assumptions: payer, country, account, gross amount, withholding if any, and payment date. That becomes your adviser handoff pack and lowers the chance that something gets missed.

Step 3. If you may have two-country filing exposure, run a coordinated plan#

If you may file in more than one country, run a coordinated plan until qualified advice says otherwise. Work from one shared data set.

Use four tracks:

- Prepare the Germany filing package from complete income and account records.

- Prepare the home-country filing package from the same underlying records.

- Confirm any treaty or relief method based on your actual facts.

- Review whether foreign-account reporting and related asset-reporting obligations apply.

Verify current filing thresholds, deadlines, and reporting labels before you act.

Step 4. Build a first-year compliance checklist#

Use this minimum checklist for a move tied to an employment-based permit:

| Checklist area | What to include |

|---|---|

| Gather records | passport ID page, employment contract, first and last payslips of the year, move and travel timeline, housing documents, prior-year return, and account statements |

| Track accounts | every foreign and German account opened, closed, or used for salary, investments, rent, or side income |

| Prepare adviser handoff | one summary of countries involved, income types, dependents if relevant, and open questions on relief or reporting |

| Set filing calendar controls | monthly document downloads, payroll checks, adviser review dates, and verified filing deadlines |

| Use official support channels | Make it in Germany and EURES for living-conditions guidance; confirm fees in advance if you use private placement agencies |

If you do one pre-move task, make it this: build your year-one evidence pack before departure. It lowers the chance of missed obligations and expensive cleanup later. Once the filing exposure is clear, you can model whether the offer still works in actual cash terms.

Financial Modeling: What Is Your Actual Net Income in Germany?#

Use net pay as your decision number, not the gross salary on your contract. For a Blue Card move, the 2026 salary floors of €50,700 for the standard route and €45,934.20 for certain shortage-occupation cases are eligibility thresholds, not spendable income.

Before you model anything, collect your draft contract, expected family status at the move date, and payroll-relevant details such as children, church membership, and any second employer.

Step 1. Model from Netto, not Brutto#

Your monthly budget should start with what actually reaches your account after payroll deductions. In Germany, payroll deducts taxes and social security contributions from gross salary before net pay is paid out.

Use two deduction buckets:

- Taxes: including wage tax, which your employer transfers monthly to the tax office.

- Social security: statutory coverage for key life risks, with contributions generally shared by employee and employer.

Treat your payslip as the source of truth. Your first payslip is the first hard check that wage tax, church tax, if applicable, and social security deductions match your assumptions.

Step 2. Test the household profile that matches your real situation#

Tax class affects withholding, so model the setup that fits your life now, not a generic example. Germany has six tax classes, and withholding can change with marriage, children, and multiple employers.

| Household scenario | Tax setup to test first | What can change your net | Modeling note |

|---|---|---|---|

| Single employee, one job | Usually Tax Class I | Church membership, social-security deductions | Verify exact tax and social-security deduction assumptions against official guidance and payroll records before using a net-pay estimate. |

| Married couple, both employed | Usually start with married-couple payroll setups, often Class IV scenarios | Children, church membership, payroll/tax-office records | Confirm the payroll setup and deduction assumptions with payroll, official guidance, or adviser records before using the estimate. |

| Household with child or children | Model actual marital and employment status, then include child-related payroll facts | Whether payroll records reflect current family status | Verify family-status payroll records and deduction assumptions with payroll, official guidance, or adviser records before planning from the model. |

| Two jobs or two employers | Model main-job withholding plus second-job withholding | A second employer can trigger Tax Class VI on one payroll stream | Verify second-job payroll treatment and deduction assumptions with payroll, official guidance, or adviser records before using the estimate. |

If your life situation is changing around the move, confirm the current classification with payroll, an income tax assistance association, or a tax adviser.

Step 3. Verify contract and payroll inputs before you accept#

A reliable net-pay model depends on clean input data. For planning, confirm the employment period is at least six months and that the gross annual salary in your offer matches the route you are using.

Then verify the payroll-critical details before signing:

- Marital status

- Children

- Church membership status

- Whether you will have a second employer

Use a simple evidence pack: employment contract, passport, qualification proof for the residence process, and a one-page payroll fact sheet. Do not negotiate from one guessed monthly figure. Negotiate from a tested range instead.

Step 4. Negotiate to a tested net-pay range#

- Run a German gross-net calculator with your real household inputs.

- Test multiple contract scenarios, especially near €50,700 and €45,934.20.

- Set a target monthly net range for your actual budget.

- Use that range in salary and start-date discussions.

This keeps the decision tied to take-home pay and gives you a clear first-payslip checklist for validation. If the net number works, turn it into contract terms that support your application and first year on the ground.

Before you accept an offer, map your move date and paperwork timeline early with the Tax Residency Tracker.

Securing Your Offer: How to Negotiate a Blue Card-Ready Contract#

Negotiate for a contract that is both eligible and workable in real life. It should clear the legal floor, match your qualifications, and support your net-income plan.

Step 1. Verify eligibility before you negotiate numbers#

Start here: compensation talks do not help if eligibility is weak. For a Blue Card-ready file, confirm three basics first: a concrete job offer or contract, a qualified role, and a salary at or above the legal minimum threshold.

Use this pre-negotiation checklist:

- Recognition status: Confirm whether your foreign qualification is already recognized or whether you still need additional proof.

- Role alignment evidence: Make sure the written job title and core duties clearly align with your qualifications.

- Employer document readiness: Confirm HR can provide a signed contract and required employer documentation if requested.

If the role description reads vague or disconnected from your qualifications, fix that language before you negotiate package terms.

Step 2. Negotiate the package, not just minimum compliance#

Use the current threshold as a pass-fail checkpoint, not your target. Anchor negotiations on your compensation goals, and ask for the gross annual salary to be stated clearly in the contract.

Focus on the full package: base pay, relocation support, onboarding timing, and clear written terms so your application file stays consistent.

| Clause | Why it matters in practice | What to confirm in writing |

|---|---|---|

| Salary definition | Blue Card eligibility depends on a clear pay figure | Gross annual salary |

| Role scope | Helps show qualified-role fit and keeps your file consistent | Job title and key duties |

| Probation | Sets expectations for the first phase of employment | Probation length and terms |

| Notice | Sets expectations if employment terms change | Notice period |

| Working hours | Clarifies compensation structure | Weekly working hours |

| Paid leave | Clarifies total package terms | Annual leave entitlement |

| Start date | Aligns onboarding expectations | Exact employment start date |

Step 3. Run a final compliance check before signing#

Review the final contract as an evidence file, not just an offer letter. Confirm that salary and role scope are consistent across your contract and application materials. Then keep your contract and qualification or recognition documents together.

If the salary meets the threshold but the wording is unclear, pause and request corrected written terms before signing.

With a usable contract in hand, compare it against your other options one more time before you commit.

The Blue Card vs. The Freelance Visa: A Strategic Comparison#

Choose the route that matches how you actually earn. If you already have a secured employee offer, the Blue Card path is often simpler to structure. If you run an independent client business, a freelancer or self-employed path may fit better, but you should verify current route-specific requirements before filing.

Step 1. Choose by your real work model#

Start with one question: do you already have a secured job offer, or are you operating through clients? The Blue Card route is tied to secured employment conditions, including a job offer and a minimum salary, so treat the current salary requirement as a checkpoint to verify before you apply.

If you already have secured employment, structure your file around that. If you are staying independent, build a file that reflects genuine self-employment.

One risk is especially worth avoiding: bogus self-employment is a recognized risk pattern. If your setup could be interpreted as employment presented as freelance work, pause and get route-specific advice before you file.

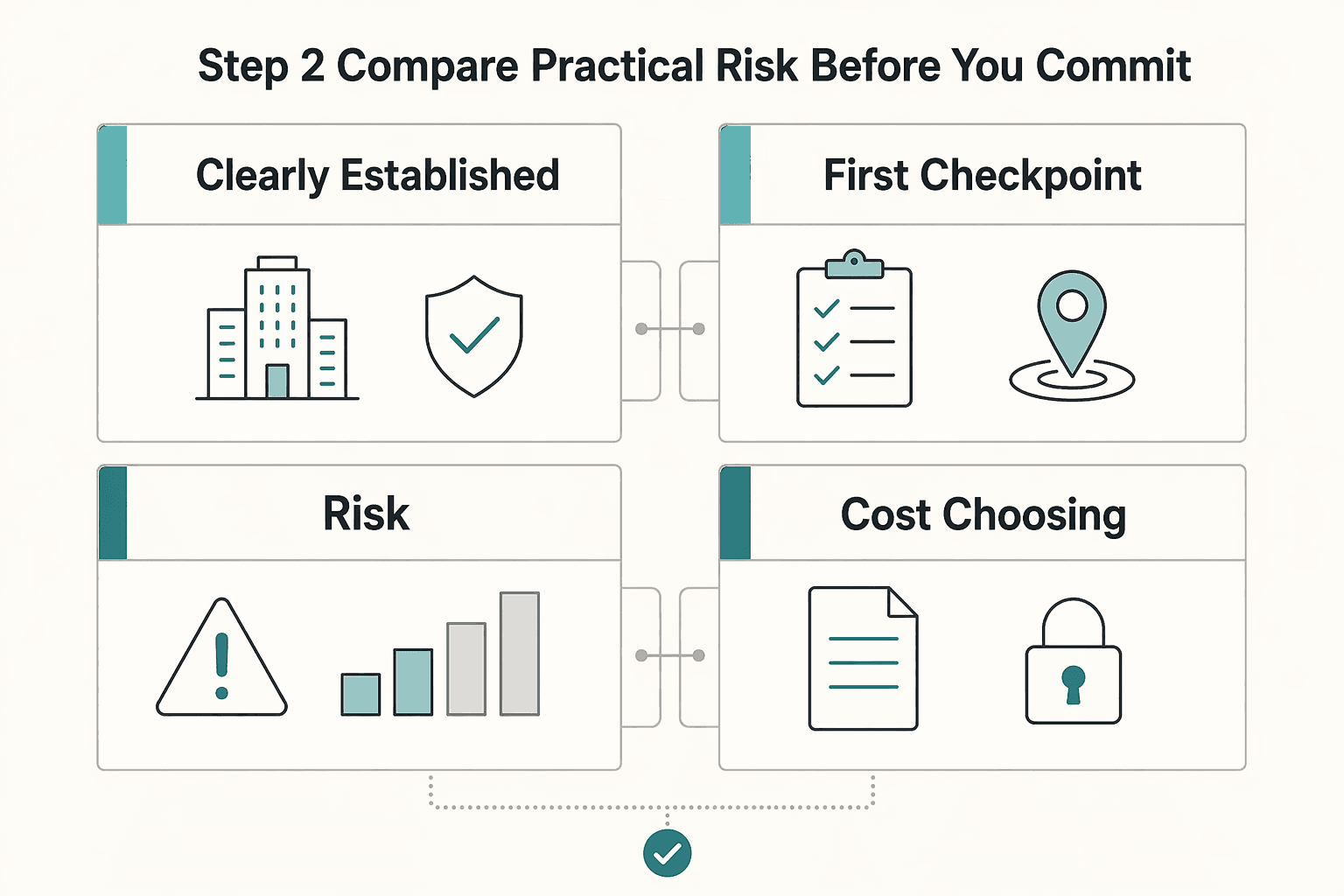

Step 2. Compare practical risk before you commit#

| Decision factor | Employer-backed route | Freelance route |

|---|---|---|

| What is clearly established | Blue Card is tied to secured employment conditions, including a job offer and minimum salary | A freelancer or self-employed pathway exists, but criteria details are not established in this excerpt |

| First checkpoint | Confirm you already have secured employment and meet the current Blue Card salary requirement | Verify current freelance or self-employed requirements before filing |

| Misclassification risk | Keep the work setup clearly aligned with employment status | Bogus self-employment is a recognized risk pattern to avoid |

| Cost of choosing the wrong route | A poor route match can increase delay, refusal, and avoidable fee risk | A poor route match can increase delay, refusal, and avoidable fee risk |

The core tradeoff is employer-backed stability versus independent-path autonomy. Making that call early helps reduce delays, refusals, and avoidable application costs.

Step 3. Use a hybrid path only if the sequence is realistic#

A hybrid path may be possible when you want stability first and independence later, but this grounding set does not establish switch timelines or automatic conversion rules.

Before any switch, verify in writing what your current status allows and what documents a change requires.

If you plan to stay independent, use this next: How to Get a Residence Permit in Germany as a Freelancer.

Your Next Move: From Compliant Resident to Thriving Professional#

Approval is the starting line, not the finish. In your first phase, run a simple sequence: confirm compliance, stabilize cash flow, and build integration habits that support your next career move.

Step 1. Revalidate your compliance baseline#

Before you optimize anything else, recheck the live rules tied to your permit. The EU Blue Card in Germany is established under Section 18g, salary thresholds are updated, and regulated professions can require a German practice license.

Use this checkpoint:

- Confirm the current salary threshold for your category before you rely on it

- Confirm your role still matches your qualifications

- Confirm your contract still meets the minimum duration of 6 months

- Store your contract, qualification evidence where relevant, and licensing proof where relevant in one folder

Step 2. Lock your real monthly cash flow#

Treat your offer as a draft until onboarding records confirm how pay and deductions are handled in your case. If tax, health-insurance, or pension setup applies to your onboarding, verify those details through official employer records and the relevant provider or authority.

Use this checkpoint:

- Compare expected net pay against your first payslips

- Confirm insurance status and contribution handling from official onboarding documents

- Hold a buffer until payroll and coverage are consistent month to month, based on a target you have verified for your case

Step 3. Build your residence evidence file early#

Residence administration is document-led, with supporting-document requests and processing-time checkpoints, so keep your records ready. Keep clean digital and paper records tied to your permit and employment, plus official correspondence.

Use this checkpoint:

- Keep one indexed file so you can answer document requests quickly

- Track request and response dates where processing-time checkpoints apply

Step 4. Plan integration as a career lever#

Use the early months to widen your options, not just settle in. Set one networking target, one role-progression target with your manager, and one work-relevant language target you can measure.

Use this checkpoint:

- Networking: pick one recurring industry event or community

- Role progression: define the skills and results needed for your next step

- Language: set a practical work outcome, for example meetings or internal docs

Use this next-step checklist:

- Reconfirm current Section 18g and salary requirements before acting on timing assumptions

- Validate tax, insurance, and pension setup from final onboarding records

- Keep a complete evidence file for future residence or status checks

- Revisit your priority each quarter: stability, savings capacity, or role progression

If you want one place to pressure-test your relocation numbers and paperwork assumptions, run through the Gruv tools hub.

Frequently Asked Questions

Does the German Blue Card automatically make me a tax resident?

No. Tax residency depends on your exact facts. If you establish a domicile or habitual residence in Germany, you can become fully taxable there, and habitual residence can arise after a continuous stay of more than six months. Check your move date, expected stay pattern, and living setup before filing.

What is the realistic net salary after tax with a Blue Card?

There is no single net-salary number from Blue Card rules alone. Eligibility is based on gross salary thresholds that are updated annually, while your net outcome depends on your personal tax setup. Use a current payroll and tax calculation for your exact situation before deciding on an offer.

Which is better: the Blue Card or the Freelance Visa?

Neither is universally better because they are different legal pathways. The Blue Card depends on employed work with a specific job offer, and the period of employment must be at least six months. The freelance route is a separate self-employment pathway. If you choose the Blue Card route, early job changes can be reviewed in the first twelve months and may be suspended for up to 30 days.

How does the Blue Card affect my U.S. tax filing, including FEIE or FBAR-type reporting?

It does not cancel your home-country filing framework. Germany and the U.S. should be analyzed separately: Germany can tax residents on worldwide income, while U.S. citizens and resident aliens generally still file on worldwide income and may still have foreign-account reporting duties. Run a Germany checklist and a U.S. checklist in parallel, then get treaty-specific advice for your country pair.

How quickly can I get permanent residency with a Blue Card?

Do not plan around stale numbers. Verify the current timeline and language requirement before using this as a planning anchor. Right before submission, check the live settlement-permit criteria on an official page.

Can my family join me on this status?

Yes. Family reunification is possible, and family members entering through family reunification are allowed to work in Germany. The exact document set and conditions can still vary by route, nationality, and filing location. Pull the current checklist from the relevant mission or immigration office before you book appointments.

What are the most recent changes I should care about?

Focus on changes phased in since November 2023 that affect eligibility, and verify each one right before filing. The main checkpoints are the current salary threshold or thresholds, expanded shortage-occupation coverage, IT-specialist access without a degree with the current experience requirement, and mobility rules for people who already hold an EU Blue Card from another member state. Confirm current criteria on live official pages, because some pages still show historical figures that should not drive a 2026 application.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bidenwhitehouse.archives.gov/wp-content/uploads/2025/01/ERP-2025.pdftrusted

- circabc.europa.eu/sd/a/e8c15a00-e75e-4741-bda5-884470a44de1/10...trusted

- cs.wheatoncollege.edu/mgousie/comp218/CPlusPlusProgramming.pdftrusted

- eures.europa.eu/living-and-working/living-and-working-condit...trusted

- faa.gov/newsroom/statements/general-statementstrusted

- irs.gov/individuals/international-taxpayers/us-citiz...trusted

- oecd.org/content/dam/oecd/en/publications/reports/202...trusted

- sec.gov/Archives/edgar/data/2035832/0001193125253267...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The 2026 Global Digital Nomad Visa Index for 50+ Countries

Start with legal fit, not lifestyle filters. The practical order is simple: choose a route you can actually document, then decide where you want to live. That single change cuts a lot of wasted comparison work and stops you from falling in love with places that were never a real filing option.

Can Digital Nomads Claim the Home Office Deduction?

Claim the deduction only when your facts and records can carry it. With the home office deduction for digital nomads, the real decision is usually a three-way call: claim it, do not claim it, or pause and get help because your file is not ready.

How to Get a Residence Permit in Germany as a Freelancer

**Treat your German freelance residence permit like an operations project, and you will cut avoidable delays before they start.** The hardest part is often not the forms but the uncertainty around procedure, especially if you are working from Berlin-based experience while local office workflows shift as you prepare paperwork. Confusion costs time, money, and momentum.