Quick Answer

Split Buyer LTV and Seller LTV first, then roll up to Platform LTV only after side-level checks pass. Tie each side to gross profit and its own CAC path, and count value only at defined lifecycle states such as confirmation, classification, and final close. Keep unresolved fees, credits, or attribution gaps in an explicit unknowns-and-interim-assumptions log with an owner and review date before using the model for spend decisions.

Define LTV for Buyers, Sellers, and the Platform#

In a two-sided marketplace, many teams look at buyer-side and seller-side value separately, then compare each view to the relevant Customer Acquisition Cost instead of forcing everything into one blended ratio. Treat Lifetime Value as an operating number, not a spreadsheet guess.

Before you start#

Step 1. Anchor LTV in gross profit. For this guide, LTV means the gross profit a user brings to the business over the full relationship. That matters because it keeps the model tied to unit economics instead of vanity revenue. It also sets the right expectation early. This is a planning metric, but not a simple one. Different customers create value in different ways, and the two sides of a marketplace can behave differently.

Step 2. Set an evidence standard before you touch formulas. The goal is not a neat spreadsheet. The goal is a number that finance and ops owners can defend. By the end of this guide, you should be able to connect your LTV:CAC view to operating checkpoints your team can verify, so the number is not floating above the business.

A simple rule helps. If a fee, refund, credit, or cost line cannot be traced back to a source record you trust, do not quietly absorb it into an average. Mark it as unverified. That discipline will save you from building a confident model on top of missing revenue adjustments or costs captured late.

Step 3. Make assumptions explicit when the data is incomplete. Marketplace teams often disagree because they are trying to answer different questions with one metric. Some use a fully loaded CAC view that includes both buyer and seller acquisition. Others want side-specific CAC for buyer and seller acquisition. Neither approach works if the model hides where the data is weak.

So this guide uses a stricter rule. When you know something, label the source. When you do not, flag it as unknown. If attribution is partial or a cost line is unresolved, the model should say that plainly. Add the assumption, add an owner, and add a date for review.

That is the tone for the rest of the article. The point is not to make LTV look objective. The point is to make it usable for decisions, auditable, and specific enough that you can tell whether buyer-side value is healthy, seller-side value is weak, or the overall view only looks strong because the missing pieces were never forced into the open. Related reading: Building Subscription Revenue on a Marketplace Without Billing Gaps.

Define the three LTVs before touching any formula#

Start by separating the decision views: use Buyer LTV, Seller LTV, and Platform LTV for different decisions, not one blended number.

| LTV view | Primary use | Definition note |

|---|---|---|

| Buyer LTV | Demand-side acquisition choices | Use lifetime gross profit contribution, not raw revenue |

| Seller LTV | Supply retention, activation, and incentive choices | Use lifetime gross profit contribution, not raw revenue |

| Platform LTV | Overall budget and health decisions | Roll up after Buyer LTV and Seller LTV are settled |

- Name the decision owner for each view.

Buyer LTV supports demand-side acquisition choices. Seller LTV supports supply retention, activation, and incentive choices. Platform LTV is the combined unit-economics view for overall budget and health decisions.

- Use one baseline definition across teams.

Define LTV as lifetime gross profit contribution, not raw revenue. This keeps finance, ops, and growth aligned on value after direct costs. Before you model, agree on what is included and excluded so teams are not comparing different definitions.

- Keep side-level views separate before LTV:CAC comparisons.

CAC context can vary sharply, so a single blended LTV:CAC view can hide weak performance on one side. Review buyer-side and seller-side economics first, then compare them to the right acquisition lens.

- Reconcile upward only after side-level agreement.

If there is debate about one "true" LTV, settle Buyer LTV and Seller LTV first, then roll them into Platform LTV. Because LTV is hard to pin down exactly, favor a transparent, decision-useful estimate over false precision.

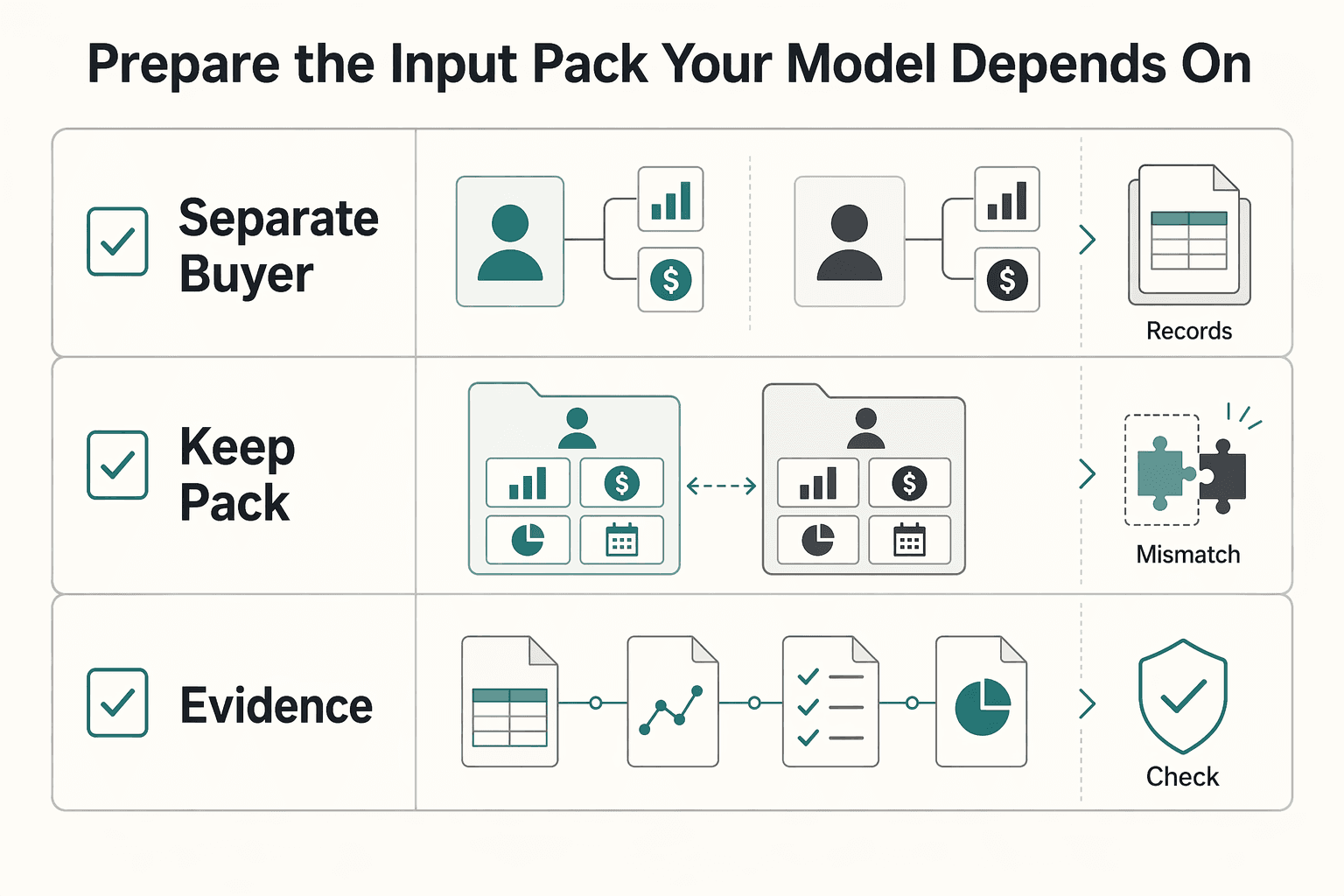

Prepare the input pack your model depends on#

Do not model until your input pack is explicit and traceable.

| Input pack rule | What to record | Review/control |

|---|---|---|

| Separate buyer and seller inputs | Distinct buyer and seller metrics, CAC paths, value earned, direct costs applied, and acquisition cost source | Track both sides separately from day one |

| Keep the pack minimal | Only the fields the model actually consumes, plus an owner and as-of date for each input | Use a monthly review cadence until the baseline is stable |

| Document unknowns | Missing attribution, unsettled items, and other gaps in an unknowns and interim assumptions tab | Add an interim rule, owner, and review date |

Step 1. Separate buyer and seller inputs from day one. Track buyer and seller metrics separately, including distinct CAC paths, instead of blending both sides into one average. Your pack should let you answer, for each side: what value was earned, what direct costs applied, and where acquisition cost came from.

Step 2. Keep the pack minimal and decision-ready. Use only the fields the model actually consumes, and record an owner plus an as-of date for each input so assumptions can be reviewed quickly. If definitions are still settling, use a monthly review cadence until the baseline is stable.

Step 3. Document unknowns before debating outputs. Keep missing attribution, unsettled items, and other gaps in an explicit unknowns and interim assumptions tab with an interim rule, owner, and review date. Hidden unknowns create false precision.

This pairs well with our guide on MoR vs. PayFac vs. Marketplace Model for Platform Teams.

Map the money lifecycle to measurable events#

Only count value after it reaches a defined, auditable checkpoint. If an amount cannot be tied to a clear state and a stable record, keep it in a pending bucket rather than treating it as earned.

Build one event chain and keep the order fixed#

Use one fixed lifecycle sequence for every transaction, and apply it the same way to buyer-side value, seller-side value, and platform value. The goal is consistency: teams should not read different moments in the lifecycle and call them the same outcome.

Name the first measurable event at each stage and avoid collapsing stages into one label. For example, "initiated," "confirmed," and "final" should not be treated as interchangeable when they represent different levels of certainty.

Run a quick trace test: pick one recent transaction and confirm you can follow it end to end with stable identifiers. If the trail breaks, your LTV window is relying on assumptions, not records.

Assign a source of truth to every checkpoint#

Set one authoritative record per checkpoint and mark other records as supporting only. This keeps lifecycle decisions defensible when numbers are reviewed.

| Lifecycle checkpoint | Source of truth | What to verify | Distortion if skipped |

|---|---|---|---|

| Initial state | Canonical transaction record | Stable ID and current state | Early activity counted as realized value |

| Confirmation state | External/internal matched reference | One-to-one match across systems | Duplicates or orphaned activity |

| Classification state | Authoritative accounting classification | Correct direction and category | Revenue/cost mix-ups in LTV |

| Final state | Closed status in your process | Included vs pending is explicit | Timing gaps hidden in cohort results |

Because CLV can be defined in revenue-only or margin-aware ways, lock your definition before modeling and apply it consistently across checkpoints.

Set failure rules before exceptions pile up#

Define failure and delay handling before reporting pressure shows up. If an item is unmatched, delayed, or unresolved, decide whether you defer it, reserve it, or exclude it, and document that rule.

Keep timing risk explicit in the model instead of assuming every transaction closes cleanly on the same schedule. Transaction outcomes can include both failure risk and longer completion times, so your LTV window should reflect that operational reality.

Watch exception aging. A growing unresolved bucket usually signals that lifecycle assumptions are masking process debt.

Enforce replay-safe handling in retry paths#

When a record is reprocessed, it should replay the same event state rather than create new economic value. Use durable keys so repeated ingestion does not inflate value or cost lines.

Test this directly by reprocessing the same record and checking that totals do not change. If they do, your LTV output is sensitive to operational noise instead of underlying economics.

Calculate Buyer LTV and Seller LTV with asymmetric CAC#

Calculate Buyer LTV and Seller LTV separately first, then attach CAC by side. A blended CAC can hide which side is actually sustaining the model.

Split lifetime value by side and by cohort#

Use side-specific gross profit contribution that has already passed your lifecycle checkpoints. Buyer LTV should tie to buyer-side journaled and reconciled contribution, and Seller LTV should do the same for seller-side contribution.

Do not stop at one average per side. Segment cohorts by attributes that change churn or growth, such as price point, payment period, and sales channel. Keep churn-based lifetime assumptions attached to the cohort that produced them, rather than applying one lifetime across all buyers or sellers.

Before you trust the output, confirm each cohort's value ties back to the same ledger population and date window. If cohort counts come from one system and value comes from another, verify that entity IDs match exactly.

Pair each side with its actual CAC path#

Attach Customer Acquisition Cost by side, not as one blended figure. Buyer and seller acquisition often follow different motions, so they need separate CAC treatment in LTV:CAC decisions.

Asymmetry should be explicit in the model. For example, one KPI reference uses side-specific CAC inputs of $5,000 for sellers and $2,000 for buyers in 2026; treat values like this as scenario inputs, not universal benchmarks.

If supply and demand are acquired differently, add a documented marketplace ratio assumption before you use LTV:CAC as a scaling signal. Assign an owner and review date, and keep it as a planning assumption rather than a fixed formula.

Use the asymmetry to make a spending decision#

Use this split to decide spend order. If Buyer LTV is healthy but Seller LTV is weak, focus first on seller activation or retention before you increase demand spend.

| Buyer cohort pattern | Buyer-side signal | Seller-side check |

|---|---|---|

| Low volume, high margin buyers | Higher Buyer LTV can support higher buyer CAC | Confirm seller quality and availability can retain this cohort |

| High volume, low margin buyers | Thin contribution requires tighter buyer CAC | Monitor seller utilization and servicing cost so Seller LTV does not erode |

| Mixed buyer base | Averages can hide true payback | Keep cohort-level CAC ceilings instead of one blended threshold |

If network effects dominate your marketplace, keep a note for advanced Customer Lifetime Value extensions such as CLV2. Use them only when cross-side effects are observable in your cohort data. Until then, a clean side-specific model with documented asymmetry is the safer operating baseline.

For a step-by-step walkthrough, see How to Use a Community to Reduce Churn and Increase LTV.

Derive Platform LTV that leadership can operate#

Platform LTV should be a transparent roll-up of Buyer LTV and Seller LTV, not a blended number that hides where value is created or lost. Since CAC and LTV calculations can vary, leadership should only use a platform view with explicit assumptions, side-level outputs, and sensitivity.

Roll up side-level value with named assumptions#

Build Platform LTV from the same buyer and seller cohort outputs, then apply only the platform cost lines you explicitly include in that view. Keep a short assumptions note next to the model with an owner and review date.

If payout timing, incentive treatment, or shared servicing cost allocation changes, document the change directly instead of burying it in a multiplier. Platform LTV should reconcile to the same cohort populations and date windows used for Buyer LTV and Seller LTV. If the roll-up improves while one side worsens, treat it as a warning that the blend may be masking weakness.

Connect Platform LTV to the three decisions leadership actually makes#

Use Platform LTV to make operating decisions, not just to report a headline metric.

- Set acquisition budget ceilings. This ratio is decision-useful only when both sides remain visible. If Buyer LTV is strong but Seller LTV is weak, cap buyer spend before service levels or incentive costs erode gains.

- Design payout incentives carefully. Model seller bonuses, reduced payout fees, or activation credits as explicit Seller LTV inputs, then test the effect on Platform LTV sensitivity.

- Sequence marketplace expansion. Do not justify new categories or geographies with a healthy average alone. Expand only when the roll-up still works after weaker-side acquisition paths and support costs are modeled.

As customer acquisition costs rise, this side-level discipline becomes more important.

Require a side-by-side leadership view every time#

Set one governance rule: no leadership review without Buyer LTV, Seller LTV, and Platform LTV shown side by side, plus sensitivity. Keep that view front and center on the reporting dashboard so leaders can approve, pause, or redirect spend based on the side creating value and the assumptions carrying risk.

If you cannot produce that three-part view from one evidence pack, the platform number is not decision-ready.

Related: Two-Sided Marketplace Dynamics: How Platform Supply and Demand Affect Payout Strategy.

Stress-test assumptions before using numbers in planning#

Before you use Buyer LTV, Seller LTV, or Platform LTV for budget decisions, test how fragile those numbers are. This matters because there is no single agreed LTV definition, and LTV:CAC is often misread in practice.

| Test area | Scenario change | What to watch |

|---|---|---|

| Retention | Lower repeat behavior | Measure Buyer LTV and Seller LTV compression |

| Margin | Pressure take-rate realization or increase servicing, refunds, or incentives | Check whether platform contribution remains positive |

| Demand dynamics | Test softer buyer demand at flat acquisition volume, and higher seller activation with lower quality | Watch whether side changes propagate across conversion, repeat behavior, and seller retention |

| Operating trigger | Cohort variance breaches pre-set bounds | Pause CAC scaling and rerun with updated cohort data |

Step 1: Lock the definition before testing outcomes. Use one LTV scope per test set. If one model uses revenue-only inputs and another uses gross profit or margin, treat that as a definition change, not sensitivity. Keep cohort window, inclusion rules, and profit basis constant within each scenario set.

Step 2: Run operator-readable sensitivity cases. Test each side separately before combining results.

- Retention: Lower repeat behavior and measure Buyer LTV and Seller LTV compression.

- Margin: Pressure take-rate realization or increase servicing, refunds, or incentives, and check whether platform contribution remains positive.

- Demand dynamics: Test softer buyer demand at flat acquisition volume, and higher seller activation with lower quality.

Step 3: Test cross-side feedback before scaling CAC. In two-sided marketplaces, side changes propagate. Lower seller quality or availability can weaken buyer conversion and repeat behavior; weaker buyer demand can reduce seller retention. Use a clear operating trigger: if cohort variance breaches pre-set bounds, pause CAC scaling and rerun with updated cohort data.

Step 4: Keep modeling complexity tied to observable inputs. When data quality is uneven, prefer simpler operational formulas. Move to more dynamic CLV-style modeling only after key assumptions are observable and documented over time. Otherwise, complexity can create false precision.

If you want a deeper dive, read Accrued Revenue for Platforms: How to Recognize Revenue Before Buyers Pay in a Two-Sided Marketplace.

Common mistakes and how to recover quickly#

Once you have stress-tested the model, the next failures are usually reporting discipline and assumption hygiene, not the formula itself. Fix them quickly, because rising CAC makes small LTV errors expensive.

- Mistake: treating LTV as a side metric.

Recovery: keep LTV front and center on your dashboard, and lock the definition and reporting window before you use it for planning decisions.

- Mistake: hiding uncertainty inside blended metrics.

Recovery: publish a short known vs unknown appendix with an owner and remediation date for each gap, and hold high-impact spend calls until material unknowns are resolved or clearly bounded.

- Mistake: monitoring marketplace balance too slowly.

Recovery: track marketplace liquidity daily and run a weekly KPI review cadence so buyer-side and seller-side shifts are visible before they distort planning.

- Mistake: treating retention as a vanity signal.

Recovery: use retention and LTV as profitability and sustainability indicators, and escalate quickly when trend changes could alter your LTV:CAC decisions.

You might also find this useful: Marketplace Economy 101: How Platform Business Models Create Value for Buyers Sellers and Operators.

Conclusion#

The useful answer is not a prettier spreadsheet. It is an auditable chain from how value enters your records to how you approve or pause spend for buyers, sellers, and the platform.

If you want to close out this LTV work cleanly, use this checklist and do not skip the verification points. LTV is only decision-ready when the definitions, evidence pack, and uncertainty are all visible in the same review.

- Lock the definitions before anyone debates the number.

Confirm that Buyer LTV, Seller LTV, and Platform LTV are each defined in writing as lifetime gross profit over the relationship period you chose, and state what sits inside LTV:CAC for each view. Verification point: one written definition set that finance, ops, and product are all using in the same planning deck. Red flag: two teams use the same acronym but apply different start points or time windows.

- Validate the evidence pack, not just the model output.

Check that your data pack includes coordinated cost, revenue, profit, and ROI inputs, plus side-level CAC attribution logic. The expected outcome is that you can trace a sample cohort from source inputs to computed economic value without filling gaps from memory. If acquisition attribution is missing, or key inputs are incomplete, publish those as explicit unknowns with an owner and date instead of blending them away.

- Verify duplicate handling and record consistency.

You do not need a perfect architecture diagram here, but you do need proof that duplicate records are not creating extra revenue or cost lines in the model. Verification point: for a test sample, one transaction/reference maps to one economic event in your calculations. A common failure mode is counting the same event twice during data joins or periodic refreshes before anyone notices.

- Publish sensitivity side by side before budget decisions.

CLV has more than one valid calculation approach, so document the method you chose and show how the result changes when retention, margin, or timing assumptions move. Expected outcome: leadership sees Buyer LTV, Seller LTV, Platform LTV, and the related LTV:CAC views together rather than one blended number. If one side stays underwater across reasonable cases, pause scaling on that side and fix the operating issue first.

- Review on a fixed cadence and update when behavior changes.

A weekly review cadence is a reasonable starting point for fast-moving marketplaces because capital efficiency can move quickly, but treat it as a review habit, not a universal benchmark. Recheck assumptions whenever retention behavior, margin structure, channel mix, or timing shifts materially. That is the point where yesterday's model becomes today's planning error.

Used this way, the model stays practical, defined, evidenced, stress-tested, and honest about what it still does not know.

Frequently Asked Questions

What is the practical difference between Buyer LTV, Seller LTV, and Platform LTV in a two-sided marketplace?

Buyer LTV estimates value from buyers over time. Seller LTV estimates value from sellers over time. A platform-level LTV view is a blended rollup. They are not interchangeable in practice: in two-sided marketplaces, supply-demand balance is an ongoing challenge, so keeping side-level views helps you see where imbalance is coming from.

How should we handle LTV:CAC when buyer acquisition and seller acquisition happen through different channels?

Keep buyer and seller acquisition paths separate first, then roll up only as a secondary view. Because CAC and LTV calculations can be ambiguous, make assumptions explicit for each side. That makes it easier to see whether performance issues are coming from buyer economics, seller economics, or both.

Which minimum inputs must exist before we can trust an LTV model for planning?

At minimum, define CAC and LTV clearly for each side, document the assumptions, and apply those rules consistently over time. If those basics are missing, treat the output as directional and publish the unknowns explicitly.

Why does two-sided LTV feel subjective, and how do we make it decision-usable anyway?

It feels subjective because there is real ambiguity in both CAC and LTV calculations, and marketplace supply-demand balance is always moving. Make it usable by locking definitions, stating assumptions in plain English, and showing sensitivity ranges instead of presenting one number as objective truth.

When should we keep a simple marketplace model versus moving to CLV2-style dynamic modeling?

Keep the simple version when definitions and assumptions are still being stabilized. Move toward CLV2-style modeling when you can consistently observe how changes on one side affect outcomes on the other. If demand outpaces supply, you can create disappointed buyers. If supply outpaces demand, sellers sit idle. That is where a static model starts to miss important behavior.

How do compliance checks like KYC, AML, or tax documentation affect realized lifetime value?

Treat KYC, AML, and tax-documentation requirements as potential constraints on realized lifetime value, state uncertainty plainly, and avoid hard numeric adjustments unless you have separate validated evidence.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 3 external sources outside the trusted-domain allowlist.

- dspace.mit.edu/bitstream/handle/1721.1/152447/kondo-kochiro...trusted

- fdic.gov/media/168951trusted

- pages.stern.nyu.edu/~jstroebe/PDF/JF_Stroebel.pdftrusted

- sec.gov/files/cft-written-sifma-digital-assets-12-16...trusted

- sec.gov/Archives/edgar/data/1370637/0001370637250000...trusted

- cs-cart.com/blog/unit-economics-how-to-calculate-ltv-for...external

- cs-cart.com/blog/how-to-balance-sellers-and-buyers-in-an...external

- financialmodelslab.com/blogs/kpi-metrics/local-business-directoryexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Accrued Revenue for Platforms Recognizing Revenue Before Buyers Pay

You can recognize revenue in a two-sided marketplace before buyer cash arrives, but only if you separate the earning event from billing and make the reclass path explicit. The practical job is to design the accounting so your finance, ops, and product teams can record revenue early without losing control of reconciliation. If you cannot explain that path clearly, your close team will feel it at month end.

How Supply and Demand Dynamics Should Set Your Marketplace Payout Strategy

In a two-sided marketplace, payout strategy is not back-office plumbing. It can shape whether sellers stay active, whether transactions complete reliably, and whether buyers can find supply that is ready to transact.

Marketplace Economy 101 for Buyers, Sellers, and Operators

Choosing between a **Marketplace business model** and a **Platform business model** should be an operating decision, not a branding exercise. This guide is built to help you make that call with go or no-go checks that reflect how the business will actually run once buyers, sellers, and expansion pressure show up.