Quick Answer

Start with model choice, then validate one market before funding acquisition. For marketplace economy platform business models buyers sellers operators, the decision hinges on operational proof: onboarding controls, clear responsibility between sides, and a traceable path from payment receipt to payout batches. If those checks are incomplete, keep scope tight and postpone expansion until the core transaction loop is dependable.

How the Marketplace Economy Works#

Choosing between a Marketplace business model and a Platform business model should be an operating decision, not a branding exercise. This guide is built to help you make that call with go or no-go checks that reflect how the business will actually run once buyers, sellers, and expansion pressure show up.

At a basic level, a marketplace connects buyers and sellers on a centralized platform. It usually acts as the middleman rather than owning inventory, which contrasts with a traditional retail model with stock and storefront overhead. A platform is broader. It can include a marketplace, but it also pushes you to think harder about partnerships and growth strategy because the upside can be large and the failure risk is real.

That risk is not abstract. One analysis reviewed more than 100 failed digital ecosystems and found recurring signs of failure across different growth phases. That matters because marketplace and platform ideas often look cleaner in slides than they do in operations.

Early traction can hide harder questions: how onboarding works, which checks or approvals sit between signup and first transaction, whether the core transaction flow is reliable enough for both sides, and how much the model changes as you expand. A model can look scalable because it avoids inventory, but that does not make it easy to run.

The hard part is not the label. The hard part is deciding what obligations you take on between the two sides of the transaction, what partners you depend on, and what breaks first as volume grows. If you pick the wrong model, you can spend heavily on acquisition before the core transaction path is under control.

Use the guide in sequence. First, define the terms clearly so you do not confuse a transaction-matching marketplace with a broader platform play. Next, compare the economics, especially where take rate, listing fee, or hybrid pricing fits. Then validate launch conditions before you spend on growth.

A practical checkpoint is whether you can explain, in plain language, who is onboarded, who gets paid, what checks or documents sit between signup and first transaction, and which segments are explicitly in scope for phase one. If you cannot answer those questions yet, that is not a reason to quit. It is a reason to narrow the plan before you scale it.

The sections that follow are built to help you do exactly that: choose the model, pressure-test the economics, and sequence expansion in a way your operations can actually support.

Define the marketplace economy in operator terms#

Start with operations: if you match third-party buyers and sellers and provide the transaction rails, you are running a Marketplace business model. In this model, the operator is an intermediary that provides the infrastructure and tools for transactions, and revenue is typically fees or commissions.

The core difference from a Traditional retail model is inventory and sales control. Retail usually buys or owns stock and sells directly. A marketplace is typically inventory-light: sellers carry inventory costs, while the operator focuses on technology, user experience, and customer acquisition.

Use Platform business model as the broader label. A marketplace can be one type of platform, but not every platform is only a marketplace transaction layer.

For Peer-to-Peer (P2P) marketplace and Business-to-Business (B2B) marketplace, treat the labels as operating context and map the flow clearly: who supplies, who buys, who sets price, who fulfills, and where the operator intervenes. If that path is still unclear, the model is not ready to price or scale.

If you want a deeper dive, read eCommerce Reseller Payouts: How Marketplace Platforms Pay Third-Party Sellers Compliantly.

Compare model structures and monetization levers#

Choose pricing based on the value you actually control in the transaction flow. If you mainly reduce search and transaction costs between buyers and sellers, transaction-linked pricing is usually easier to justify; if your value is access or tooling before any sale, listing or access pricing is often easier to defend.

| Monetization lever | When it fits | Why teams pick it | Common break point |

|---|---|---|---|

| Take rate | You meaningfully shape discovery, trust, checkout, and transaction completion | Revenue tracks completed transactions and value capture at the point of exchange | Fragile if supplier margins are tight or if buyers and sellers can move repeat deals off-platform |

| Listing fee | Sellers get clear value from presence, visibility, or access even before conversion | More predictable top-line than fully transaction-linked revenue | Churn risk if listing value is weak or conversion stays low |

| Hybrid pricing | You provide both ongoing access and transaction rails | Balances access revenue with performance-linked revenue | Can feel like double charging unless each fee maps to a distinct service |

Use a simple decision rule: if supplier margins are thin, avoid an aggressive early take rate unless you are providing demand they cannot reliably get elsewhere. If your demand aggregation is genuinely unique, transaction-linked pricing is easier to sustain.

Why reference patterns differ#

Airbnb and Amazon's marketplace are established transaction-platform examples: they connect buyers and sellers and reduce search and transaction costs. That pattern often supports transaction-linked monetization.

Use Shopify and DoorDash as comparison prompts, not copy-paste templates. The practical test is always operator scope: what you control, what each side can do without you, and where your work creates measurable value.

The broader platform evidence points the same way: outcomes come from coherent business model design across sides, not from copying one fee label in isolation.

What to verify before you pick a model#

Trace one successful order and one failed order end to end, then confirm:

| Check | What to confirm |

|---|---|

| Generated demand | Who generated demand |

| Trust and transaction risk | Who handled trust and transaction risk |

| Support and exception handling | Who absorbed support and exception handling work |

| Next deal off-platform | Whether the next deal can happen off-platform after first contact |

| Contribution margin | After incentives, not before them |

Failure checks that can erase headline margin#

Watch three failure modes that can wipe out headline margin:

- Disintermediation: repeat transactions bypass your rails after initial matching.

- Subsidy dependency: growth depends on continuing incentives rather than durable unit economics.

- Quality-control load: refunds, disputes, and support work consume more margin than headline pricing suggests.

For a step-by-step walkthrough, see MoR vs. PayFac vs. Marketplace Model for Platform Teams.

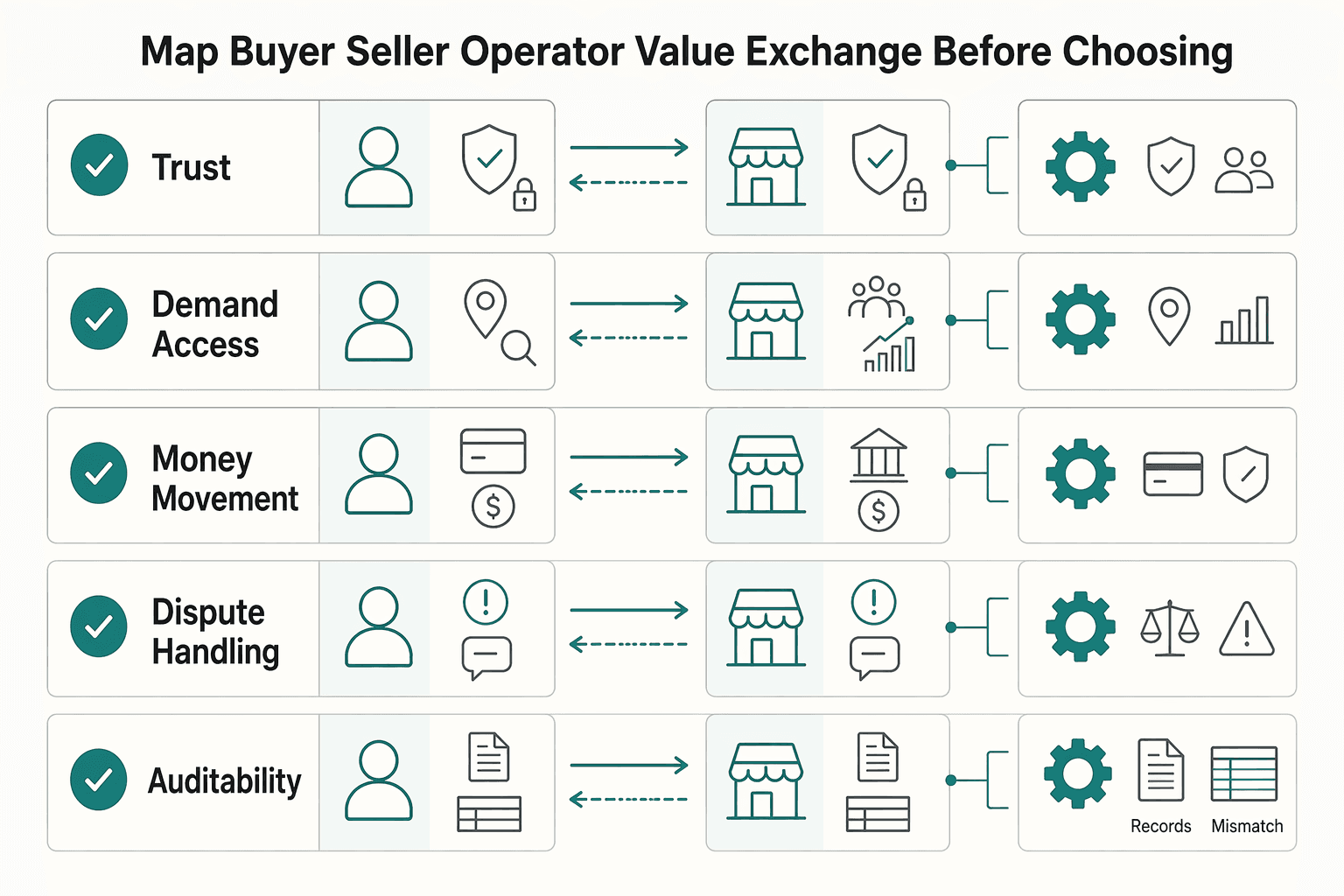

Map buyer seller operator value exchange before choosing a model#

Map the transaction as a three-sided value exchange before you choose a model: buyer to seller, seller to buyer, and both sides to the operator. If the operator's value is unclear for any side, liquidity and retention are likely to stay fragile even with strong acquisition.

Define the exchange in testable value units, not slogans. The operator's core job is to make third-party transactions more valuable, so each row should show what buyers and sellers get and what the operator must run reliably.

| Value unit | Buyer receives | Seller receives | Operator responsibility |

|---|---|---|---|

| Trust | Confidence in who they are transacting with | Confidence the counterparty is legitimate | Set and run onboarding controls (including KYB/KYC decisions where relevant) |

| Demand access | Faster access to relevant supply | Access to relevant demand, including buyers they may not reach directly | Build and maintain matching and discovery quality |

| Money movement | Clear payment experience and status | Clear payout path and status | Operate payment acceptance, reconciliation, and payout batches |

| Dispute handling | A defined path when a transaction fails | A defined path to respond and resolve | Own exception handling and resolution workflow |

| Auditability | A usable record of what happened | A usable record for finance, support, and review | Maintain transaction and decision history |

Use one checkpoint before committing: for each row, can you clearly state why buyers stay, why sellers stay, and what only the operator provides? If one answer is vague, treat that as a model risk.

You may see different expectation patterns by market segment, for example consumer flows that emphasize speed versus business flows that emphasize records, but the test is the same: the operator value must be explicit and operational. Related: Choosing Creator Platform Monetization Models for Real-World Operations.

Decide if a market is launchable before go-to-market spend#

A market is launchable only when your operating evidence is stronger than your growth assumptions. If you cannot clearly show how you will protect users, collect seller information, and handle complaints in that country, hold the launch until you can.

In 2021, OECD survey work across 28 countries and 15 online marketplace businesses found fraud and scams were significant concerns in online marketplaces. It also highlighted practical mitigation patterns: targeted surveillance, education for sellers and consumers, and stronger seller/product information requirements. Use that as your baseline filter before you spend on demand.

| Launch check | What to verify before launch | Launch signal | Hold signal |

|---|---|---|---|

| Consumer-protection readiness | The country/category expectations you will follow and who owns them | Clear policy owner, documented process, user-facing handling path | Rules are still abstract or ownership is unclear |

| Seller-information readiness | What third-party seller and product information you require | Required fields and review steps are defined and usable | Information standards are incomplete or inconsistent |

| Complaint-data readiness | How complaints will be tagged, routed, and reviewed | Marketplace-specific complaint categories and escalation ownership are set | Complaint handling is ad hoc or defined "after launch" |

| Fraud/scam response readiness | How you will detect and respond to abuse early | Surveillance and seller/consumer education actions are in place | Controls are deferred until after growth |

| Evidence quality | Whether teams can review one end-to-end case without guesswork | Support, risk, and operations can trace and explain the case | Teams depend on tribal knowledge to explain outcomes |

Build the evidence pack before spending#

Before approval, compile the operational evidence you will actually run: policy owners, required seller/product information, complaint categories, escalation path, and abuse-response actions. The goal is not perfection. The goal is a defensible core path that is documented, owned, and reviewable.

Use one checkpoint that is hard to fake#

Run one realistic pre-launch walkthrough and test whether support, risk, and operations can independently explain what happened. If they cannot, you do not have a launch-ready market plan yet.

OECD also called out the value of more specific consumer complaint data for marketplaces, so define those tags before launch rather than after the first spike.

Sequence cold start and liquidity by vertical and country#

Start narrow: seed constrained supply first, validate transaction quality, then scale demand only in the vertical-country corridors where both sides are transacting more efficiently over time.

A market can be launchable and still be the wrong place to spread thin. In a platform model, value comes from making third-party transactions work, so supply, demand, and transaction trust need enough concentration to create liquidity density rather than headline activity.

Start with the narrowest supply that can fulfill real demand#

Choose the smallest credible seller or provider cohort for one category in one geography, then test whether buyers can complete a first transaction without manual rescue. If first transactions close only through heavy operator intervention, you do not have early liquidity yet.

The shape of demand changes how this plays out. Uber-style models depend on local density in a tight area, while B2B marketplaces often run through longer, fit-sensitive procurement paths where supplier quality and transaction reliability matter more than catalog breadth.

Validate quality before buying more demand#

Track these leading indicators by cohort:

| Indicator | What the article says |

|---|---|

| First successful match rate | Track by cohort and read together with repeat transaction rate and dispute incidence |

| Repeat transaction rate | Strong first matches with weak repeat demand usually signal weak underlying fit |

| Dispute incidence (with reason codes) | Rising matches with rising disputes usually signal low-trust volume |

Read them together, not in isolation. Strong first matches with weak repeat demand usually signal weak underlying fit, and rising matches with rising disputes usually signal low-trust volume.

Use one hard checkpoint before expansion: review failed first matches, tag root causes, and keep the linked evidence trail: request, outcome, dispute artifact if any, and operator action. If repeat demand is weak, narrow category scope before expanding geography.

Design payments and payout operations that survive scale#

Money movement has to be reliable before you broaden launch. In practice, that means you can trace each transaction from invoice or checkout through payment receipt, internal balance update, and Payout batches completion, with retries that do not create duplicate payouts or duplicate balances.

Build the money trail first#

Your transaction backbone should do four things clearly: collect funds, post to the correct internal balance, determine payout eligibility, and execute payouts with exception handling. The key test is state visibility and repeatability, not architectural elegance: even if events arrive late or more than once, your records still need to resolve into one coherent status.

| Failure mode | What it looks like |

|---|---|

| Webhook timing drift | Product shows "paid" while finance still has an unposted balance |

| Duplicate payout attempts | Retries fire after slow success responses and guardrails are weak |

| Unmatched deposits | Incoming transfers cannot be tied to the right payer |

| Stale FX quote usage | Promised payout amounts do not match settlement assumptions |

Use an operator checkpoint before wider rollout: sample pilot transactions and prove end-to-end visibility for source document, payment status, balance impact, payout instruction, and final batch result. If your team cannot quickly answer "where is this seller's money right now?", treat that as a launch blocker.

Choose intake and payout tooling with eyes open#

For bank-transfer-heavy flows, teams often evaluate Virtual Accounts as part of intake design; for embedded payments and payouts, teams often evaluate Stripe Connect models. The core decision is not just implementation speed, but whether your unit economics still work once fees and payout behavior scale.

Stripe's published pricing highlights why fee modeling must happen early:

| Component | Published pricing signal |

|---|---|

| Standard domestic card processing | 2.9% + 30¢ per successful transaction |

| International cards | +1.5% |

| Manually entered cards | +0.5% |

| Connect (platform-managed) monthly active account | $2 per monthly active account |

| Connect (platform-managed) payout fee | 0.25% + 25¢ per payout sent |

| Managed Payments fee | 3.5% per successful transaction, in addition to standard processing fees |

Connect pricing is not one universal model. In platform-managed pricing, Stripe states you are responsible for processing fees, and a monthly active account is any month payouts are sent to that account's bank account or debit card. Also, country pricing pages can supersede listed method fees, so treat headline fees as directional until you validate your exact country and method mix.

Build compliance and governance gates before volume#

Before you scale, make payout and withdrawal eligibility explicit so every hold, approval, and release is traceable. Your baseline should be simple: no money-out action clears without a defined review state, a recorded hold reason when restricted, and documented release criteria.

Gate money out with explicit review states#

If you use KYC, KYB, or AML controls, apply them at payout and withdrawal decisions, not only at signup. The key test is operational: can you show the account review state at release time, who approved exceptions, and what evidence supported that decision?

A workable queue usually includes:

- visible states such as pending review, restricted, eligible for payout, or under investigation

- hold reasons tied to the account or transaction

- release criteria documented before funds are unlocked

Keep market overlays as separate launch blockers#

Treat market-specific governance as its own go/no-go track, separate from payments readiness. If the UK is in scope, run a dedicated legal and policy review for Online Safety Act implications rather than bundling it into later work. For a deeper legal-focused walkthrough, use Online Safety Act UK: What Marketplace and Platform Operators Must Do to Comply.

Keep tax operations narrow, factual, and evidence-based#

For U.S. persons abroad, IRS guidance states they are taxed on worldwide income. The foreign earned income exclusion applies only to a qualifying individual with foreign earned income who files a U.S. return reporting that income. One qualification path is the physical presence test: 330 full days in a 12-month period, and those days do not need to be consecutive.

Treat FEIE as a planning signal, not a blanket seller promise. Qualification also requires a tax home in a foreign country, and part-year qualification requires adjusting the maximum exclusion by qualifying days. The published maximum exclusion is $132,900 per person for tax year 2026, and IRS amounts can change by year.

For FBAR tracking and 1099 workflows, set ownership and process scope before launch, including what data is stored and how sensitive fields are handled in internal tooling.

What to decide in the next 30 days#

Use the next month to lock three decisions in order: choose the model, prove one country is launchable, and run one controlled pilot before scaling. That sequence keeps you from funding demand before money movement and operator workflows are ready.

Pick the model and price it on purpose#

Decide now whether you are building a Marketplace business model or a broader Platform business model, then tie pricing to that choice. A marketplace connects buyers and sellers on a centralized platform and typically does not own inventory, so sellers usually carry inventory cost while the platform focuses on technology, user experience, and customer acquisition.

Write a one-sentence monetization rationale your team can repeat: what value you create, for which side, and when that value is clear enough to charge for it. Also assume your first setup is a starting point, not a forever decision. Once scaled, platforms often reconfigure value to stay competitive, so the goal now is a clear starting logic, not perfect final design.

Finish one country launchability review#

Complete one launchability review for one country with evidence, not assumptions. The output should cover compliance scope, payout path readiness, and reconciliation visibility.

At minimum, verify:

- a dry onboarding flow for the seller or payee profile you plan to support

- the first payout path, including approval or hold points

- traceability from transaction record to payout status and finance reporting

If the compliant payout path is still uncertain, pause demand efforts in that market.

Pilot narrowly, then confirm fit before expanding#

Run one controlled pilot cohort and scale only if liquidity quality and operational reliability meet your predefined thresholds. Keep the pilot narrow enough to test real matching and repeat usage, not just signups.

Use a clear go or no-go rule before launch, then confirm country or program fit, payout coverage, and implementation constraints against your actual rollout plan. If you need to pressure-test model choice, use this archetypes guide. For coverage and implementation fit before expansion commitments, Talk to Gruv.

Frequently Asked Questions

What is the difference between a marketplace and a platform in one sentence?

In this context, a marketplace is a transaction-focused platform model where multiple buyers and sellers connect to transact, while “platform” is the broader label.

How does a marketplace create value differently for buyers, sellers, and operators?

Buyers get access, choice, and a simpler way to transact in one place. Sellers get demand plus infrastructure the operator may provide, such as payments, shipping, and customer service. The operator creates value by reducing transaction friction and trust gaps, then usually earns through fees or commissions while typically not owning the inventory itself.

When should an operator use a take rate, a listing fee, or a hybrid pricing model?

Marketplace revenue is commonly fee- or commission-based, with six primary models: commission, subscription, listing fees, lead fees, freemium, and featured listings. Commission is the most common model, with 51% using it as primary and 17% combining it with subscriptions.

What is the chicken-and-egg problem, and what is the practical first move?

It is the cold-start dynamic where buyers wait for supply and sellers wait for demand. The grounding here does not validate a universal first-move playbook, so practical sequencing should be treated as context-specific.

What usually breaks marketplace economics after early growth?

A common pressure point is the operator’s infrastructure burden: supporting transactions through capabilities like payments, shipping, and customer service can be expensive to run well. Another pressure point is pricing: one academic model describes situations where operators price low to induce seller competition, which can help activity but compress operator economics.

What must be validated before launching a new country or vertical?

Validate that the marketplace can reliably run its core transaction loop in that market: buyers and third-party sellers can transact, operator infrastructure is in place, and the fee/commission model can support operations. If those fundamentals are still uncertain, delay launch.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- cftc.gov/sites/default/files/idc/groups/public/@other...trusted

- cmr.berkeley.edu/assets/documents/promo/best-article-award/sa...trusted

- hbs.edu/ris/Publication%20Files/The%20Platform%20Org...trusted

- humanecology.ucdavis.edu/sites/g/files/dgvnsk161/files/media/document...trusted

- irs.gov/individuals/international-taxpayers/figuring...trusted

- irs.gov/individuals/international-taxpayers/foreign-...trusted

- oecd.org/content/dam/oecd/en/publications/reports/202...trusted

- oecd.org/content/dam/oecd/en/publications/reports/201...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Which of the 5 Marketplace Archetypes Fits Your Platform

If you need to choose a marketplace model without getting stuck in taxonomy debates, this guide is meant to help you get to a decision in one pass. It is written for founders, product leaders, finance ops, and engineering owners who need to choose a model that fits the business, then carry that choice into execution without avoidable surprises.

UK Online Safety Act Compliance for Marketplace and Platform Operators

Treat the UK Online Safety Act as operating work now, not a policy debate. The most practical way to reduce uncertainty is to run an auditable implementation plan: make an initial scope call, stand up baseline controls, assign owners, and keep records you can defend if Ofcom asks questions.

How Marketplace Platforms Pay Third-Party Sellers Compliantly

Generic marketplace payout advice usually skips the part that breaks in production. Paying many sellers is not just moving money out. It is deciding who gets paid, when they become eligible, what happens when a buyer disputes a payment, and how finance proves every release later. If you are working on **ecommerce reseller payouts marketplace platforms pay third-party sellers**, this guide is for the marketplace operator, not for solo freelancer banking tips.