Quick Answer

Start with market-by-market proof, not feature demos. For subscription revenue platform marketplace billing, the reliable order is: define charge mix, document country constraints, validate FTC Negative Option Rule evidence, and test finance outputs under ASC 606 or IFRS 15 before procurement. Then run a constrained pilot that traces signup, retry, refund, and cancellation into GL handoff. If any country still depends on manual spreadsheet repair or unclear partner ownership, mark that launch path no-go and defer.

Why marketplace subscription revenue fails after a strong launch deck#

Recurring billing usually breaks after the pitch stage for a simple reason. Teams buy a feature story when they really need an operating decision. If you are evaluating a subscription revenue platform for marketplace billing, the real question is not which vendor demo looks strongest. It is where you can launch first, which recurring-charge rules apply, and what your finance team can prove after go live.

Step 1#

Narrow the scope before you compare tools. This article is for platform founders and operators deciding how to launch recurring billing by market, with marketplace realities in view. Rollout order, payment and payout constraints, finance handoff, and integration depth matter more than any generic "best billing platform" list.

Launch decks make subscriptions look clean because vendor pages usually lead with catalog features: plans, invoicing, dunning, analytics, self serve portals. A vendor may belong on your shortlist, but feature claims alone will not tell you whether your launch survives real market conditions. The risk sits in the parts that are harder to show in a demo: applicable recurring-charge rules, cancellation handling, reconciliation evidence, ERP handoff, and who owns the failure path when payments or lifecycle events go wrong.

Step 2#

Anchor your evaluation in enforceable rules, not product promises. One concrete example is the FTC Negative Option Rule, published in the Federal Register on 11/15/2024 with citation 89 FR 90476. The final rule applies broadly to negative option programs in any media. It requires key disclosures before obtaining billing information and charging, unambiguously affirmative consent before charging for the negative option feature, and simple cancellation mechanisms that immediately halt recurring charges.

That matters because "subscription launched" is not the same as "subscription is operationally viable." A common failure mode is a product that can start a recurring charge but cannot prove the disclosure shown, the consent captured, and the cancellation path used. If you cannot retrieve those records quickly, collections may look fine while your compliance posture is weak. Ask each vendor or implementation partner to show where those artifacts live, how they are timestamped, and how they can be exported for finance or legal review. Also verify against official legal editions, not just informational XML pages on FederalRegister.gov.

Step 3#

Once the rules and evidence requirements are clear, define success in operating terms before you commit product and GTM resources. Here, success means predictable collection, low reconciliation drag, compliant payout paths, and audit-ready evidence for finance. If a platform can bill but your team still reconciles by spreadsheet, manually traces failed payments, or cannot tie subscriber events to ledger outputs, you have not solved recurring revenue.

By the end of this guide, you should be able to decide three things: what to validate first, what to phase later, and which vendor claims need proof before procurement. That is the standard worth using for any marketplace billing decision.

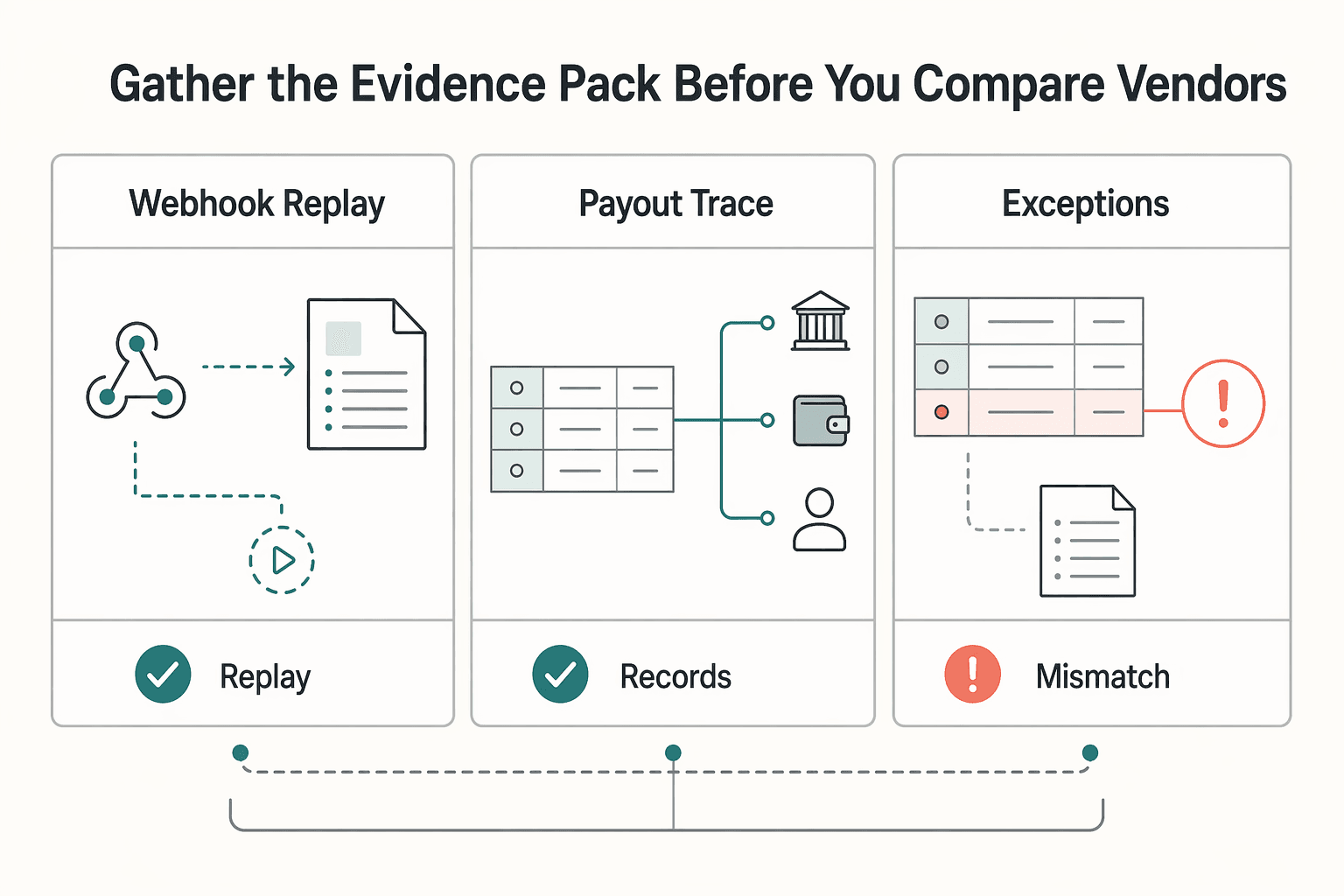

Gather the evidence pack before you compare vendors#

Do not start demos until every vendor gets the same evidence pack. That is how you avoid feature theater and compare delivery risk instead of slide quality.

Step 1 Define your charge mix in plain categories. Write a one-page brief that separates one-time charges, recurring subscription charges, and usage-based charges so finance, product, and payments ops are using the same language.

Step 2 Gather market facts by country before asking about coverage. Stripe's marketplace guidance highlights payment-processing challenges, so document required payment methods, tax handling expectations, and onboarding or payout compliance gates for each target market before you score vendors.

Step 3 Lock your system anchors and system of record. If NetSuite or another ERP owns key transaction objects, state that early and list the integration depth you require across self-serve UX, APIs, webhooks, and downstream systems such as CRM/CPQ, portals, banking/payments, or WMS/3PL where invoicing is affected.

Step 4 Require evidence for every claim. Ask for the supporting docs, implementation notes, and named partner dependencies (for example, Implementation Partners or Tax Partners), and treat any capability that depends on external firms or opaque connectors as delivery risk. For a step-by-step walkthrough, see The Best Tools for Managing Subscription Billing.

Lock non-negotiables before discussing nice-to-have features#

Use finance and payment-control evidence as the first filter. If a vendor cannot show revenue recognition readiness and failed-payment handling before pricing discussions, remove it.

| Filter | What to ask for | Use |

|---|---|---|

| Revenue recognition readiness | One concrete annual-prepay example billed today and recognized over the service period; outputs finance can review directly | Screening requirement |

| Fixed control set | Invoicing, dunning, payment recovery, revenue recognition outputs, and GL handoff with reconciliation artifacts; sample billing outputs, retry/dunning records, recognition schedules, and ledger handoff files | Require end-to-end traceability from charge to accounting output |

| Claim quality | Product-level documentation and implementation evidence; partner-dependent delivery logged as risk | Treat marketing claims and listicle summaries as prompts for questions, not proof |

| Failed-payment and lifecycle handling | Clean, connected handling of payment failure, recovery flow, and related accounting records in one demonstrable path | Apply a reject rule |

Step 1 Make ASC 606 (and IFRS 15 if that is your reporting basis) a screening requirement, not a phase-two item. Ask for one concrete annual-prepay example billed today and recognized over the service period, since subscription revenue is treated over the contract term rather than all at once. ASC 606 is commonly framed as a 5-step model, so require outputs your finance team can review directly instead of rebuilding them in spreadsheets.

Step 2 Require proof for a fixed control set: invoicing, dunning, payment recovery, revenue recognition outputs, and GL handoff with reconciliation artifacts. For each control, collect product evidence (for example sample billing outputs, retry/dunning records, recognition schedules, and ledger handoff files) and confirm end-to-end traceability from charge to accounting output.

Step 3 Set a claim-quality policy before vendor comparison. Treat marketing claims from Recurly or listicle summaries from Zone & Co as prompts for questions, not proof. For material capabilities, require product-level documentation and implementation evidence, and log partner-dependent delivery as risk rather than native capability.

Step 4 Apply a reject rule on failed-payment and lifecycle handling. Vendors should show clean, connected handling of payment failure, recovery flow, and related accounting records in one demonstrable path. Some recurring-billing sources report meaningful recovery from smart retries and link payment failures to involuntary churn in certain contexts, but those figures are not universal benchmarks, so validate mechanics directly in the product.

Compare market fit with a country-by-country decision table#

Make the country-level decision early: if a market needs custom payout, pricing, or local payment work you cannot prove from current docs within your launch window, mark it no-go and defer.

Step 1 Build one row per country and charging route#

Use one row per country and route, not one row per vendor. The same country can have different economics and delivery risk across standard processing, a connected-account model, and a managed-payments layer.

Use Gartner only for billing-pattern framing (for example recurring subscription, one-time, or usage-based). Treat pricing pages, support docs, implementation notes, and partner dependencies as the proof for each country/route decision.

| Market | Candidate path | Billing model fit | Payment coverage | Tax or compliance constraints | Integration burden | Proof source |

|---|---|---|---|---|---|---|

| Home market | Stripe Standard | Direct subscriptions billed to end customers | Domestic cards listed at 2.9% + 30¢ per successful transaction; manual entry adds 0.5% | Pricing page is not tax proof; validate invoicing and tax handling separately | Lower fee-model complexity | Vendor pricing page |

| Cross-border card market | Stripe Standard | Card-based recurring billing into another country | International cards add 1.5%; currency conversion adds 1% where required | Country treatment still needs local review before launch | Medium, because margin and reconciliation change by country and currency | Vendor pricing page |

| Marketplace country where you set user pricing | Stripe Connect, platform handles pricing | Connected-account marketplace billing where you own the commercial model | Connect lists $2 per monthly active account and 0.25% + 25¢ per payout sent | Confirm who owns pricing, settlement, and payout records | Higher, because per-account and payout economics must reconcile cleanly | Vendor pricing page |

| Marketplace country where Stripe sets user pricing | Stripe Connect, Stripe handles pricing for your users | Faster test path when you accept Stripe-set processing economics for connected users | Stripe says it sets and collects processing fees from your users and may show "No fees for your platform" in this model | Confirm country availability and whether that model is acceptable to your users | Medium, with less pricing control for you | Vendor pricing page |

| Country needing managed payments or local methods | Stripe Managed Payments | Use only when the country and method are explicitly supported | Managed Payments charges 3.5% per successful transaction in addition to standard Stripe processing fees; some local method tables can be superseded by country pricing pages | Highest document-check burden, because country pages may override generic fee tables | Higher, because fees and methods need country-by-country validation | Vendor support doc plus country pricing page |

This split prevents a common margin error: treating Managed Payments as an all-in 3.5% fee. The support doc states that the fee is additive, not a replacement for standard processing fees.

Step 2 Label every row by proof quality#

Label each row by proof type, then keep the label strict:

- Analyst framing: category language only (for example, Gartner)

- Vendor claim: pricing page, product doc, or support article

- Partner marketplace claim: listing or network page (for example, BillingPlatform Marketplace Apps)

If a row for Chargebee, Zuora, Mekari, or OneBill is supported only by a partner listing or sales response, treat it as a dependency, not native coverage. Raise the integration burden until runtime ownership, implementation path, and failure handling are documented.

Checkpoint: finance and payments ops should be able to point to one source per row and explain why it is sufficient. "The vendor said they support it" is not enough.

Step 3 Apply a hard go/no-go rule per market#

Make the tradeoff explicit. A speed-first launch usually means narrower coverage with clearer economics. Finance-grade expansion usually takes longer because connected-account pricing, payout mechanics, or managed-payments overrides add reconciliation work and more country checks.

Use one rule consistently: if local constraints force custom work beyond your timeline, defer launch instead of forcing scope.

Decide partner-ecosystem depth versus native billing depth#

After you mark countries go or no-go, decide whether your billing model is stable on its own or only stable because connectors and partners hold it together. If core billing depends on partner connectors, prioritize native billing depth over partner-network breadth. Marketplace apps can accelerate an early release, but they should not obscure unclear ownership of core billing flows.

Step 1 Separate implementation support from runtime dependencies#

Classify each dependency as either implementation support or runtime dependency. Implementation partners can help with setup, migration, and configuration; runtime dependencies sit in the live path across CRM, self-serve commerce, CPQ, and backend billing.

Use a simple test: if your team can still run billing operations without that partner in the loop, treat it as implementation support. If production behavior depends on that connector or managed service, treat it as product scope and delivery risk.

Checkpoint: for each dependency, document the owner, trigger event, data handoff, and failure behavior. If you cannot describe what happens when data is delayed or mismatched, the risk is not yet controlled.

Step 2 Check whether the ecosystem is covering a native-platform gap#

Connector depth is most likely to become fragile when you run both sales-assisted and self-serve motions. The pattern is clear: that model requires integration across CRM, commerce/self-serve, CPQ, and backend billing, and those systems can rely on different catalogs.

So ask for proof at the catalog and event level, not just partner logos. Trace one SKU or pricing change from quote to checkout to invoice. If that path depends on multiple connectors plus manual reconciliation, treat it as a native-depth gap rather than a temporary integration detail.

Step 3 Set a clear break point before expansion#

Partner ecosystems usually help when the missing capability is narrow and speed matters. They become harder to manage when expansion adds more cross-system change points and more failure handoffs.

Use one rule: if a partner dependency touches essential runtime billing flows or revenue outputs, treat it as a first-class delivery cost, not a minor integration task. Because subscription revenue recognition already carries regulatory and reporting challenges, a slower launch with fewer moving parts is often the safer operating choice.

Sequence the build in phases that reduce irreversible mistakes#

Use phase gates, not feature momentum: keep the core recurring system stable first, then layer country complexity, then expand retention and self-serve. This order reduces hard-to-undo mistakes when billing logic is still fragile.

Step 1 Launch core recurring flows and prove clean financial traceability#

Start with one complete recurring slice: plans, invoices, payment attempts, retries, and subscriber lifecycle events. Treat strict idempotency and ledger-first reconciliation as release conditions so replayed events do not create duplicate or conflicting outcomes.

Do not move on until you can explain month-end without manual cleanup. If teams are still piecing together records across fragmented or delayed systems, stabilize this phase before adding more logic.

Step 2 Add country-specific payment and tax paths only after the baseline closes cleanly#

Add one market-specific path at a time, and treat each as an operational change, not just a checkout option. If the baseline is not stable, adding pricing, settlement, and tax variation tends to become brittle and risky.

Use a 30-day triage for each path with a clear success metric and minimum sample size. Run at least two test cycles before committing roadmap scope so you can validate retries, settlement timing, exports, and exception handling under real conditions.

Step 3 Expand retention and self-serve only after finance controls are stable#

Only expand into retention, self-serve changes, promos, or dynamic pricing after the accounting trail is dependable. Otherwise, added experiments can increase noise instead of improving decisions.

Promote this phase only when these gates hold:

- Failed-payment recovery rate trend is stable or improving across at least two test cycles.

- Reconciliation exception volume does not spike as new paths are added.

- Settlement-to-ledger traceability remains intact for payouts, fees, refunds, and adjustments.

If those signals deteriorate, pause expansion and fix control gaps first.

Related reading: How Solo SaaS Operators Use RevOps to Stabilize Revenue.

Avoid the mistakes competitors gloss over and recover fast#

The fastest way to avoid expensive rework is to raise your proof standard before you scale.

- Mistake: using top-list roundups or sponsored case studies as implementation proof.

Recovery: Use them to build a longlist, then require market-level proof before procurement. For each shortlisted option, ask for evidence tied to one target market and one billing motion, including how invoices, retries, and refunds behave in practice.

- Mistake: assuming category fit means implementation fit.

Recovery: Run a constrained pilot with failure criteria defined upfront. Make sure the pilot can clearly fail on replay duplicates, broken dunning/retry logic, manual correction paths, or mismatched histories between support and finance.

- Mistake: underweighting finance handoff details until late.

Recovery: Test revenue recognition outputs and GL export flows before public rollout. Require clean traceability for invoice, payment, refund, fee, and adjustment records; otherwise core metrics like churn, ARPU, take rate, and payback period become noisy, and churn is a viability signal, not just a dashboard metric.

- Mistake: overcommitting to partner layers too early.

Recovery: Simplify dependencies and re-baseline ownership per integration. Define who creates events, who owns retries, who receives settlement data, who owns GL mapping, and who responds to incidents, with SLA visibility across the chain.

Copy and use this launch-readiness checklist#

Treat launch readiness as four pass/fail gates. If any gate still depends on spreadsheet fixes, undocumented dependencies, or verbal sign-off, hold launch.

| Gate | Verify | Hold launch if |

|---|---|---|

| Market fit by country | Billing model, payment path, completed compliance checks, planned invoice flow, payment method, and open dependencies | Required custom work is still unscoped |

| Finance controls with sample periods | IFRS 15 and ASC 606, dunning behavior, GL handoff, and traceability for invoice, payment, refund, and adjustment | Export traceability requires manual spreadsheet repair |

| Integration risk and named owners | Payment Partners and Tax Partners, one accountable owner, one fallback path, and failure handling for late settlement files, failed tax calls, and missing retry events | Ownership is split with no single responder |

| Go-live gate with shared approval | Pilot metrics reviewed, rollback conditions, launch approvals from product, payments ops, and finance, and a status log for open items | Responsibilities or rollback triggers are not explicit |

- Step 1: Verify market fit by country.

For each target country, document the billing model, payment path, and completed compliance checks. Keep one market sheet with the planned invoice flow, payment method, and open dependencies. If required custom work is still unscoped, mark that market not ready for the first wave.

- Step 2: Verify finance controls with sample periods.

Validate finance-close outputs, including revenue recognition under IFRS 15 and ASC 606, dunning behavior, and GL handoff. Use a representative sample period and fail the gate if export traceability requires manual spreadsheet repair. Finance should be able to trace invoice, payment, refund, and adjustment cleanly.

- Step 3: Verify integration risk and named owners.

List required Payment Partners and Tax Partners, then assign one accountable owner and one fallback path for each dependency. Document failure handling for late settlement files, failed tax calls, and missing retry events. If ownership is split with no single responder, keep the gate open.

- Step 4: Verify the go-live gate with shared approval.

Record the pilot metrics reviewed, rollback conditions, and launch approvals from product, payments ops, and finance. Track open items in a simple status log so issues stay visible. Launch only when responsibilities and rollback triggers are explicit.

Related: How to Use Coupons and Discounts in a Subscription Billing Platform Without Cannibalizing Revenue.

Build for market reality, not feature demos#

The decision that holds up is sequencing: confirm market constraints and finance-proofed operations first, then expand features. If coverage, controls, or ownership are still unclear, delay launch before committing product and GTM spend.

Step 1#

Start with market economics, not feature catalogs. For each country, decide whether your model is recurring access, commission-based, or hybrid (fixed fees plus transaction-linked charges). Subscription models can deliver predictable income and a stable base, but they are not automatically the right fit in every market.

A polished demo does not prove customer fit. You still need to test whether sellers will accept recurring fees (monthly, quarterly, or annually) or prefer pay-on-success. Marketplacer also flags churn risk when seller outcomes disappoint, so if value realization is uneven, a narrower rollout or hybrid structure is often safer.

Step 2#

Require proof that survives finance review. Feature depth and partner logos are weak evidence if your operating path is still unclear.

Use one sample period per target market as the checkpoint: signup, renewal, failed-payment retry, refund, and cancellation, traced through invoice output, revenue treatment, and GL handoff. If finance still has to rebuild the story in spreadsheets, you do not have launch-ready proof.

Step 3#

Document the decision market by market and get joint sign-off from product, payments ops, and finance. Salesforce's 6-step rollout framing (including technology choice and post-launch measurement) is useful here because it forces proof before scope expansion.

Keep the memo explicit: country, monetization model, required dependencies, finance controls, proof source, owner, go/no-go, and unblock conditions. Treat language like "supported through partners" or "available with custom work later" as a stop signal until ownership and controls are clear.

This pairs well with our guide on Deferred Revenue Accounting for Client Prepayments.

Frequently Asked Questions

What is a subscription revenue platform for marketplaces?

It is the layer that manages recurring charges, invoicing, payment events, and revenue outputs for a platform business that sells ongoing access or repeat services. In practice, it should sit inside your quote-to-revenue lifecycle, not just at checkout. If it cannot show how subscription events become finance outputs, it is billing software, not a reliable revenue platform.

How is marketplace billing different from standard SaaS subscription billing?

Standard SaaS billing is often framed as a more linear subscription flow. Marketplace-style billing can introduce more stakeholders and handoffs across the quote-to-revenue lifecycle, especially when teams are adapting revenue processes to mixed go-to-market motions. That is why a feature match on a vendor page is weaker evidence than tested workflows and verified outputs.

Which capabilities are non-negotiable before launching recurring billing in a new country?

Start with invoicing, failed-payment recovery, subscriber lifecycle handling, and clean outputs for revenue reporting. Before launch, verify one sample period that includes signup, renewal, failed payment recovery, refund, and cancellation. If finance still repairs the output in spreadsheets, do not expand yet.

When do connector ecosystems help, and when do they become operational risk?

Connectors help when they speed up non-core setup, such as an ERP connection or a reporting add-on you could replace later. They become risk when core recurring flows depend on multiple third-party dependencies to stay running. A simple check is ownership: if no single person can explain what happens when a critical handoff is late or fails, the stack is too fragile.

How should we evaluate recurring billing vendors in order, step by step?

First, write down your billing model mix and launch scope. Second, test finance controls and evidence requirements. Third, map every required external dependency with an owner and fallback, and only then compare commercials. That order stops you from paying for broad claims before proving operational fit and close readiness.

What does finance-grade billing look like in day-to-day operations?

Your team can trace an invoice, payment, refund, retry, and adjustment into the ledger without manual reconstruction. Month-end closes with reconciliation artifacts, not Slack threads and spreadsheet patches. Claims such as automated revenue recognition only matter if you can verify the exported data against real sample periods.

How can we pressure-test vendor claims when pricing and implementation details are unclear?

Ask for product-level proof tied to your evidence pack: screenshots, docs, implementation notes, and named dependencies for each must-have flow. Then run a constrained pilot with explicit fail conditions, especially around failed payments, lifecycle changes, and GL handoff. A red flag is any capability described as available, but only through unnamed partners, custom services, or pricing that appears after procurement starts.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- cms.gov/files/document/cms-9884-f-2025-pi-rule-maste...trusted

- congress.gov/104/crec/1995/10/12/141/158/CREC-1995-10-12.pdftrusted

- federalregister.gov/documents/2024/11/15/2024-25534/negative-opt...trusted

- ftc.gov/system/files/ftc_gov/pdf/p064202_negative_op...trusted

- people.clas.ufl.edu/dellam/files/2.6-Tubaramure-PM2A-Program.pdftrusted

- stripe.com/pricingtrusted

- stripe.com/connect/pricingtrusted

- support.stripe.com/questions/managed-payments-pricingtrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Migrate Your Subscription Billing to a New Platform Without Losing Revenue

If you need to **migrate subscription billing platform without losing revenue**, treat it as a revenue operations change, not a simple software swap. Billing migrations sit close to renewals, revenue reporting, and payment credentials, so mistakes rarely stay technical. They can show up as duplicate records, inaccurate revenue reporting, failed renewals, or customer-facing downtime.

Use Coupons and Discounts in Subscription Billing Without Cannibalizing Revenue

Coupons can influence acquisition quickly, but in a subscription business they do more than change conversion. They also affect how revenue shows up in your operating metrics, especially Monthly Recurring Revenue (MRR). Many teams use MRR to track predictable income and plan growth, even though it is not a GAAP or IFRS accounting metric.

Choosing a Fintech Platform for Consumer Subscription Billing and Recurring Revenue

Choosing a consumer financial services subscription billing fintech platform is first an operations decision, not a feature-list exercise. Recurring revenue can improve forecasting, but it also creates a continuous billing and engagement cycle your team has to run cleanly.