Quick Answer

Small finance teams can run payment operations efficiently by using the general ledger as financial truth, assigning one owner to each money lane, and treating exceptions as evidence-based workflows. Automate only where rules are stable, retries are replay-safe, and each checkpoint can be traced through timestamps, actor history, reference IDs, and ledger outcomes. Daily, weekly, and month-end reconciliation keeps control intact.

What Lean Accounting Looks Like in a Payment Platform#

Run finance ops from the General ledger first. When transaction records, settlement matching, and Payout execution do not share clear control points, small breaks turn into manual cleanup, duplicate actions, and weak close evidence.

This guide uses a simple operating model: treat the ledger as financial truth, make Exception handling explicit, and verify every state change with an Audit trail. A general ledger is the master set of accounts that summarizes entity transactions. Payment reconciliation is matching and comparing transaction records against accounting records. An audit trail records who accessed a system, what operations they performed, and when. Those definitions support everything that follows.

Before you start#

This guide is for finance, operations, and product owners working between transaction intake and payout release. The scope is intentionally narrow: transaction to settlement to payout. Billing, revenue recognition, and treasury may still matter in your environment, but they sit outside this lane.

The goal is not zero manual work. It is fewer manual touches with reliable books, clear ownership, and evidence you can trust at review or month end. Internal control supports efficient operations, reliable reporting, and compliance. The practical question is simple: which touches can you remove without losing control?

Step 1. Anchor financial truth in the ledger#

Use the General ledger as the source of truth for money movement, and treat provider dashboards as operational views. A dashboard may show an attempted or completed payout. The ledger should show the financial event, recognition timing, and any adjustment posted.

Your first checkpoint is straightforward. Every material payment-flow status should resolve to a ledger outcome, not just a provider label. If settlement arrives and you cannot map it to a ledger posting, the loop is not closed.

Step 2. Assign ownership where money can break#

Shared ownership only works when handoffs are explicit. You can split owners across transaction ingest, settlement matching, and payout release, but adjustment authority should stay controlled. Segregating authority, custody, and accounting is a core way to reduce fraud and error risk.

Keep one practical rule in place. If your platform creates manual payouts, your team still owns tying those payouts back to transaction history. If a payout fails, is delayed, or is reissued, assign one owner for the break and one place where the accounting outcome is resolved.

Step 3. Make exceptions and retries evidence based#

Avoid "manual resend" habits when you can. Retry safety should be deliberate. Where your provider supports idempotency, use it to retry safely without duplicating the same operation. Stripe documents idempotency keys up to 255 characters and notes that keys can be removed automatically after they are at least 24 hours old. Provider mechanics vary, but the control principle is the same: retry with safeguards against duplicate operations. Tie retries to stable reference IDs and retain the evidence.

These are the checkpoints used throughout this guide: posted to ledger, settlement matched, payout released, and exception resolved with evidence. If each transition is provable through timestamps, actor history, and related reference IDs, you can reduce manual work while preserving the Audit trail.

Set your operating target and ownership map#

Before you automate anything, decide two things: which record resolves the accounting outcome, and who owns each money lane. That keeps handoffs clean and exceptions visible, so faster tooling does not create slower cleanup in the books.

Step 1. Choose the ledger as the accounting record#

Use the General ledger as the place where financial outcomes are resolved. That fits the ledger's role as the master accounting record across assets, liabilities, expenses, income, and equity. Keep provider dashboards for operational status, but resolve settlement, payout, and adjustment conflicts in the books.

The test is simple. For any material payment status, you can point to the related ledger posting or a documented pending reason. If a payout shows completed in a provider console but has no ledger outcome, the handoff is not controlled.

Step 2. Assign one owner to each money lane#

Give each lane one primary owner with delegated authority, even when multiple teams touch the process. Clear ownership is what keeps transaction-to-payout work from aging into shared ambiguity.

| Lane | Named owner is accountable for | Verification detail | Escalation trigger |

|---|---|---|---|

| Transaction ingest | Intake completeness and reference IDs | Event lands with a recorded transaction ID | Missing or duplicate intake record |

| Settlement workflow | Batch close and settlement file review | Settlement matched after batch close | Batch closes but amount cannot be explained |

| Matching and tie-out | Match ledger, settlement, and payout records | Open-items aging is reviewed on a defined cadence | Unmatched item remains unresolved past your set window |

| Payout execution | Release status and payout break handling | Payout ties to underlying transaction batch | Failed or delayed payout with no owner action |

Step 3. Define escalation rules by lane#

For each lane, write an escalation trigger, a next owner, and an evidence requirement. A practical minimum is timestamp, actor, reference ID, current financial impact, and next action due.

The failure mode to avoid is silent aging. Stripe payout reconciliation includes visibility into failed automatic payouts. If no one owns that queue, breaks can drift into month end and increase manual cleanup.

Step 4. Tighten adjustment authority as you expand automation#

If multiple teams can post adjustments, tighten that control as you expand AP automation. This is a control-first decision. Unauthorized or inappropriate journal entries are a known reporting and fraud-risk area.

Use one checkpoint before you go further: review last month's adjustments and confirm who posted each entry, who approved it, and what source evidence supported it. If that cannot be verified quickly, more automation will scale noise faster than control.

Prepare prerequisites and the evidence pack before you automate#

Do not automate around weak evidence. Lock the evidence pack first so each status is explainable in the books, each retry is safe, and each payout gate is visible.

Step 1. Lock the accounting artifacts#

Start with four aligned artifacts: chart of accounts mapping, provider status taxonomy, month-end close checklist, and a current KPI scorecard baseline. Your chart of accounts is the account list used to record activity in the general ledger. Every provider status that affects cash, fees, reserves, or liabilities should map to a ledger outcome or a documented pending state.

Make the taxonomy explicit, not tribal. Provider event names often use a resource.event pattern, but your internal statuses should carry clear business meaning. Sample recent transactions and confirm each one traces from provider status to ledger treatment to a close-checklist step. If that trace breaks, pause automation.

Step 2. Test event delivery and retry safety#

Document each webhook endpoint, subscribed event types, retry behavior, and duplicate-prevention controls. If Stripe is in your stack, undelivered webhook events are resent for up to three days. That recovery flow only returns events from the last 30 days.

| Stripe behavior | Section detail |

|---|---|

| Undelivered webhook events | Resent for up to three days |

| Recovery flow | Only returns events from the last 30 days |

| Idempotency keys | Reusing the same idempotency key returns the original result instead of re-executing the operation; keys may be pruned once they are at least 24 hours old |

Also define where you use idempotent retries. Reusing the same idempotency key returns the original result instead of re-executing the operation, and Stripe may prune keys once they are at least 24 hours old. Your retry window and key-retention assumptions need to line up.

Step 3. Gather payout gating and close evidence#

Collect the dependencies that can block payout release for your jurisdictions and account models. KYC and KYB requirements can gate payment acceptance and payouts, and outstanding requirements such as requirements.current_due should be tracked as exceptions. In U.S. MSB contexts, AML program duties and customer-identification recordkeeping are mandatory.

Keep approval logs where your process requires human release or override to support audit-trail continuity. Baseline your KPI scorecard before automation, especially monthly close cycle time from trial balance to consolidated statements. If your checklist is still informal, tighten it first with a usable Month-End Close record.

If you are building the core close, controls, and reporting cadence, see Accounting Best Practices for Payment Platforms: A Controller's Guide to Scalable Finance Ops.

Map money movement end to end and mark every control checkpoint#

An end-to-end money map only works if it follows actual funds movement, not app status alone. With a small team, keep one money map anchored to the funds-movement record. In this operating model, gate progress at four checkpoints: posted to ledger, settlement matched, payout released, and exception resolved with evidence.

Step 1. Anchor the map on actual funds movement#

Use one ordered sequence across teams. Your internal trigger can be payment confirmation or another business event, but the accounting anchor should be the record that proves money moved.

If Stripe is in your stack, use BalanceTransaction as that anchor: every funds movement in or out creates one, and those rows do not change after creation. That keeps you from advancing on app status alone when settlement matching or payout inclusion is still incomplete.

| Step | Input | System action | Named owner | Expected status | Failure signal from provider events/data |

|---|---|---|---|---|---|

| 1 | Internal payment confirmation or provider-side payment success event | Create internal transaction record and capture provider reference IDs | Transaction ingest owner | Received and linked | Missing event, duplicate delivery, reference mismatch |

| 2 | Balance transaction or equivalent funds-movement record | Post or queue General ledger entry using account mapping | Finance posting owner | Posted to ledger | No funds record, duplicate post risk, unmapped status |

| 3 | Payout object and payout lifecycle signal | Match settled transactions into payout batch | Matching owner | Settlement matched | Payout missing transactions, amount variance, stale payout status |

| 4 | Release condition met or exception ticket raised | Execute or confirm payout release, or hold and document | Payout owner | Payout released or exception opened | Failed payout, unmet release condition, unresolved prior break |

Step 2. Define handoff fields before automation#

Before you automate, define five fields for each step in this workflow: input, system action, owner, expected status, and failure signal. That is what keeps stops and escalations consistent when the happy path breaks.

In Stripe flows, retrieve payout data when payout.paid or payout.reconciliation_completed arrives so matching runs on fresh lifecycle state. Also choose payout mode deliberately: automatic payouts preserve transaction-to-payout association, while manual payouts leave reconciliation attribution to your team.

Step 3. Treat checkpoints as hard gates#

Treat the four checkpoints as hard gates:

posted to ledger: the transaction has a General ledger outcome, or a documented pending treatment, tied to the source recordsettlement matched: the payout or settlement batch is matched against included transactions, using a payout reconciliation report where availablepayout released: release conditions are met and the payout object reference is capturedexception resolved with evidence: the break is closed with event IDs, reference IDs, and the adjustment or retry record

Run one quick control test. Start from a recent payout and trace back to included transactions, then to balance-style records, then to ledger postings. If the chain breaks, the checkpoint is not reliable.

Step 4. Verify audit-trail traceability and replay safety#

Every status transition should be reconstructable in your audit trail: who changed it, which source event triggered it, what financial record it touched, and whether a retry occurred.

Use idempotent retries so repeated operations do not create duplicate side effects. In Stripe, undelivered webhook events can be resent for up to 3 days. Event retrieval in that recovery flow is limited to the last 30 days, and idempotency keys may be pruned once they are at least 24 hours old. Handlers should ignore already processed events and still return success to stop retry churn.

The rule is simple. If you cannot show the source event, the funds-movement record, and the ledger effect for a transition, do not advance the next checkpoint.

Related reading: Supply Chain Finance for Marketplaces: How Early Payment Programs Can Attract and Retain Sellers.

Decide what to automate first with a decision matrix#

Once the control checkpoints are defined, pick your first automation target with a weighted decision matrix, not the smoothest demo. Prioritize work that is repetitive and rule-consistent, and watch open exceptions so lower touch volume does not hide more unresolved breaks.

Step 1. Score the work, not the tool#

Use a simple scoring model with weighted criteria so every candidate is judged on the same scale before vendor evaluation. Keep the criteria explicit, because vague criteria weaken prioritization. Score each candidate process across four factors:

| Factor | What to score |

|---|---|

| Manual touch volume | How often someone must key, review, chase, or re-enter data |

| Error cost | How costly mistakes are in rework, delay, or correction |

| Compliance risk | How much the process depends on standardized approvals, documentation, and auditable steps |

| Customer impact | Whether failures stay internal or affect payout timing, visibility, or support load |

Compare several lanes in your first pass, such as repetitive Accounts Payable (AP) work, deterministic matching, and payout orchestration. If a top-ranked lane still depends on frequent judgment calls or inconsistent source data, it may not be ready yet.

Step 2. Start where rules are stable#

Start with the lane where rules, inputs, and exception handling are already controlled. Repetitive AP tasks are a strong candidate because AP automation is built to digitize workflow steps, reduce manual workload, and standardize auditable processes.

Deterministic matching is another strong candidate, where rules are configurable and consistent. This works best when status mapping is stable and exceptions are visible and actively resolved.

For payout orchestration, only automate flows where release logic is already tightly controlled. If automation reduces manual touches but open exceptions increase, pause rollout and fix Exception handling before you expand.

A useful pilot check is pre- and post-automation comparison on manual touches per item, open exception count, and time to close addressed exceptions.

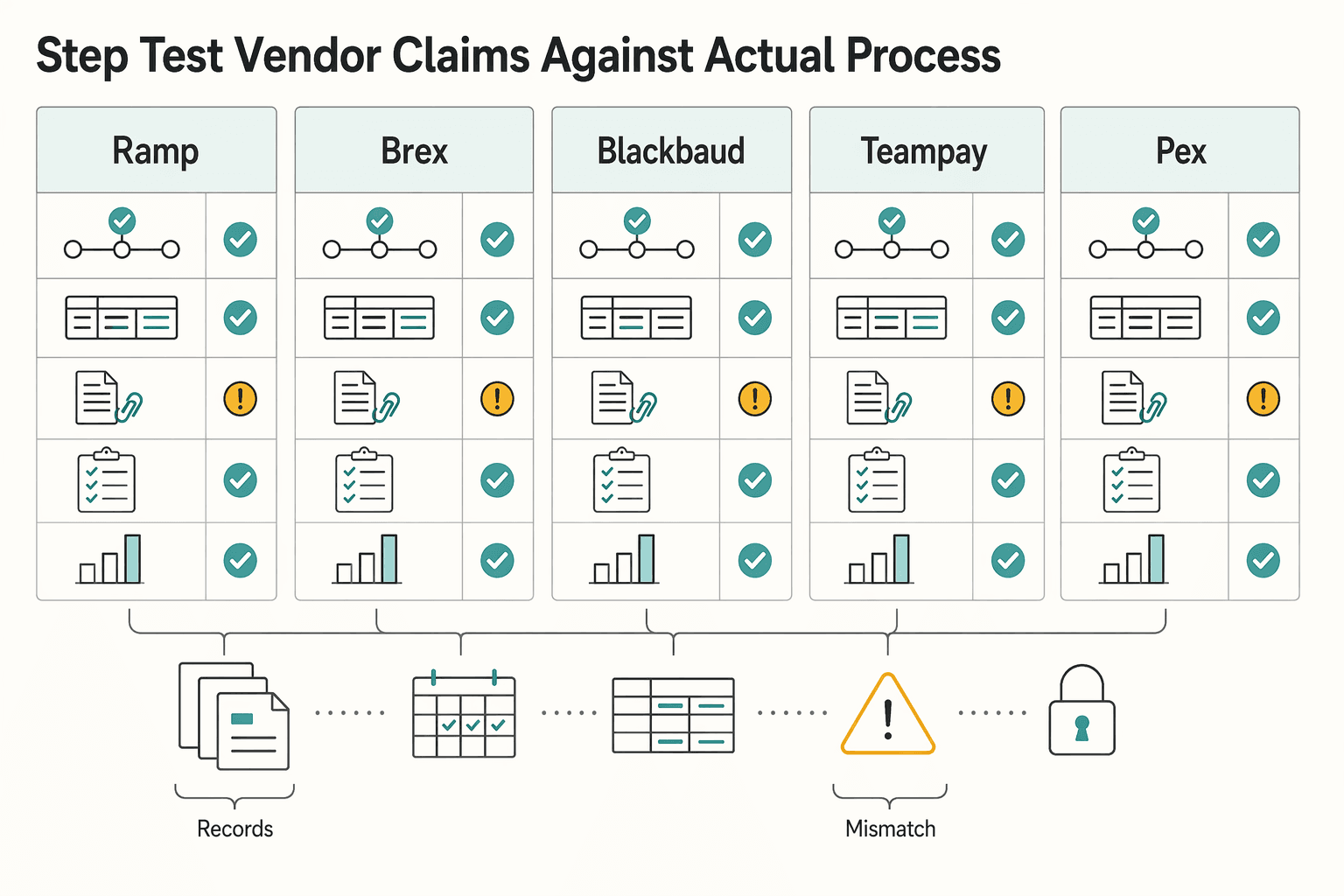

Step 3. Test vendor claims against your actual process#

Use vendor messaging as input, not proof. Treat spend and AP tooling as an infrastructure choice, then test claims against your approval flow, ledger rules, and matching evidence requirements.

| Vendor | Claimed strength | What to verify in a pilot |

|---|---|---|

| Ramp | AP processing 2.4x faster than legacy software; OCR capture with 99% accuracy | Can it preserve approval evidence, coding rules, and exportable records for audit review? |

| Brex | Expense automation that reduces errors and speeds approvals | Does it fit your approval chain without creating off-ledger adjustments or cleanup work? |

| Blackbaud | Payment protection and simpler reconciliation | What output is produced, and can your team trace exceptions to closure? |

| Teampay | Invoice processing, PO matching, and approvals automation | If PO matching is weak today, does this reduce effort or mainly expose upstream control gaps? |

| PEX | Centralized spend tracking and reconciliation | Can finance tie out spend activity without side spreadsheets or duplicate review steps? |

Do not treat headline claims as normalized benchmarks. Use a small pilot evidence pack instead: sample invoices or expenses, expected approval logs, ledger mappings, a short exception list, and the output your close process requires.

For a step-by-step walkthrough, see SaaS Accounting Software Evaluation: What Payment Platforms Need Beyond Standard GL Features.

Before expanding automation scope, map your matrix criteria to actual event states and retry behavior so your ops playbook is testable in implementation. Start with the Gruv docs.

Build daily, weekly, and month-end reconciliation discipline#

Reconciliation discipline works best on a fixed cadence: clear fresh breaks daily, review aging weekly, and run Month-end close as strict tie-out work, not cleanup.

Step 1. Close daily provider-event breaks before they become ledger drift#

Start each day with open Provider events, then confirm what posted to the General ledger. That helps keep unresolved delivery and posting issues from turning into manual fixes that can create duplicate activity.

Work the queue in timestamp order so older items are resolved first. Adyen's webhook troubleshooting records include error messages and timestamps, and Adyen instructs timestamp checks when processing events. For Stripe timing, report data is computed daily for activity between 12:00 am and 11:59 pm, and a day's report is normally available by 12:00 pm on the following day.

Use a simple closure check for each cleared item: provider event ID, event timestamp, action taken, and resulting GL posting, or confirmed non-posting. If that chain is incomplete, the break is still open.

Before booking manual corrections, check retry status. Stripe automatically resends undelivered webhook events for up to 3 days. Adyen retries failed webhooks from queue for up to 30 days, with intervals that progress through 2m, 5m, 10m, 15m, 30m, 1h, 2h, 4h, 8h.

Step 2. Review weekly aging and force owner action into the audit trail#

Run a weekly aging review to force action on unresolved exceptions before close pressure spikes. This cadence is an operating decision, not a universal rule.

The goal is evidence, not status discussion. For each aged matching exception, confirm the named owner, the last action timestamp, and the next action or escalation date. Support that review with Audit trail evidence such as a failed-event record, payout report, or journal reference. Use aging buckets that fit your provider behavior. Items that outlive a provider retry window should move from watch to investigate.

Step 3. Run month-end as a strict tie-out across settlement, payouts, and adjustments#

At least monthly, tie out every account and prove that daily and weekly controls held. Start with settlement and payout tie-outs, then confirm ledger impact.

For Stripe, use the payout reconciliation report to match bank payouts to settled transaction batches. For Adyen, perform settlement reconciliation at payout-batch level against the bank statement, and use the Monthly finance report or Daily finance report based on your fiscal-period close method. Adyen also supports end-balance matching across period boundaries. Use this sequence:

- Tie bank payouts to provider payout batches.

- Tie payout batches to underlying settled transactions and fees.

- Confirm net settled movement in the General ledger.

- Review adjustment logs separately so corrections, reserves, and fee true-ups stay visible.

Your month-end evidence pack should include the payout report, settlement output, bank support, adjustment log, and final GL tie-out. For a deeper checklist, see Month-End Close for Payment Platforms.

If exception aging keeps rising, prioritize data quality recovery before expanding automation scope.

Design exception handling that prevents payout chaos#

Payout chaos usually starts when different break types get worked the same way. Keep exception handling stable by classifying failures up front and recovering through replay-safe retries tied to immutable IDs.

Step 1. Classify failures before anyone starts fixing them#

Do not send every break into one generic "payment issue" queue. Use four failure classes so triage, evidence, and escalation stay consistent.

| Failure class | Triage owner | First action | Verification detail | Escalation cue | Customer-facing update expectation |

|---|---|---|---|---|---|

| Unmatched settlement | Matching owner | Compare provider settlement output to expected settled items and bank payout batch | For Adyen, use the Settlement details report to confirm transaction-level costs and reconciliation details | Escalate when bank payout and provider settlement cannot be tied after initial report review | Tell support whether funds are settled, pending payout, or still under investigation |

| Failed Payout execution | Payout ops owner | Check current payout status and whether the status changed after release | Stripe payout objects can move through pending, in_transit, paid, canceled, or failed, and some payouts can first appear paid and later change to failed or canceled within 5 business days | Escalate when status is failed, canceled, or missing beyond your internal monitoring window | Give a status update tied to payout state, not an assumption of success |

| Duplicate event risk | Integrations or payments engineering owner | Check whether the event or request ID was already processed | Stripe recommends logging processed webhook event IDs and skipping already logged events | Escalate when the same business action appears more than once in the ledger or payout queue | Tell support whether a duplicate was blocked or whether review is still open |

| Stale status from Provider events | Integrations owner with finance visibility | Confirm event timestamp order and delivery state before reprocessing | Adyen says to check timestamps for chronological order and treats non-2xx acknowledgment as delivery failure | Escalate when an event is older than your provider-aware retry window or later events arrived first | Avoid promising payout timing until event order and final state are confirmed |

Make the owner explicit. That person decides whether the record moves, waits, or escalates.

Step 2. Document the response fields that stop handoff gaps#

Each exception record should include five fields: owner, first action, timeout, escalation path, and customer update expectation. Set timeout rules by provider behavior.

Stripe retries undelivered webhook events for up to three days in live mode. Adyen expects webhook acknowledgment within 10 seconds, retries failed deliveries three times immediately, then continues retries for up to 30 days. For Adyen stale-status cases, check webhook acknowledgment first before touching payouts or journals.

Your checkpoint is immutable evidence: provider event ID, payout ID, request ID, bank reference, and resulting GL effect. If one is missing, you have a symptom, not a recovery case.

Step 3. Recover with idempotent retries, not guesswork#

Recover through idempotent retries or immutable reference IDs, then verify ledger impact before any resend.

Stripe idempotency keys return the same recorded result for the same request, including 500 errors. PayPal uses PayPal-Request-Id to return the latest status of a previous request, and PayPal warns that omitting it can duplicate the request. For batch payouts, PayPal large-batch validation also rejects DUPLICATE_REF_ID values within an input file.

When a payout is missing rather than failed, investigate before retrying. On Stripe, use the Trace ID with banking partners to track delayed or missing payouts. Keep the escalation evidence pack tight: payout ID, trace ID if available, original request ID, bank reference, and the GL entry or confirmed non-posting.

Keep non-negotiable controls without adding headcount#

Lean teams do not need more reviewers everywhere. They need a few hard controls that reduce bad money movement and keep close risk from growing with volume.

Step 1. Preserve separation where it matters most#

Keep segregation of duties at the adjustment and payout boundary. In a lean team, one rule does most of the work: the same person should not originate a transaction, process it, and tie it back to the general ledger. If headcount is tight, split by action instead of department, so one person prepares an adjustment and another approves it or clears it during matching.

For each manual adjustment or payout release, verify that you can identify the preparer, approver, timestamp, affected record ID, and resulting GL effect. If any of these are missing, control evidence is weak.

Step 2. Make payout gates explicit before release#

Payout release should stay blocked until required verification checks are complete, and that rule should be explicit in both policy and product logic. In some provider setups, this is a documented constraint: Adyen requires account-holder verification before payout, and Stripe Connect requires KYC before connected accounts can accept payments and send payouts.

If overrides are allowed, make them traceable. Record who approved the override, why, what evidence was reviewed, and which payout IDs were affected. Otherwise, payouts may complete operationally while finance cannot show why release was allowed.

Step 3. Require an audit trail that can reconstruct history#

Your audit trail should preserve enough history to recreate original financial records after changes, not just show the latest state. For financial-state changes, evidence quality matters more than interface polish.

The tradeoff is direct. Faster throughput without these controls can hide timing issues and increase the risk that misstatements are not prevented or detected promptly. Controlled throughput adds friction, but it helps protect month-end close reliability because approvals, exceptions, and overrides remain provable.

Choose your finance tech stack boundaries with integration rules#

Set the boundary so financial truth, control decisions, and evidence stay in systems you can reconcile and export. Keep platform logic for deterministic, replayable orchestration.

Step 1. Assign native duties before you buy or build#

Decide what your finance tech stack must own natively before adding tools. In practice, the native layer should hold what you need to prove later: final outcomes, approval history, and an exportable audit trail.

Use platform logic for event transformation, enrichment, and routing only if the final financial state still lands in source-of-truth records with timestamps, actor history, and record IDs. If you cannot clearly show where final evidence lives, the boundary is wrong.

Use one checkpoint: trace one settled payment and one payout from provider event to GL effect to matching evidence. If the path spans multiple tools and you still cannot export full history, you likely have tool sprawl.

Step 2. Require four integration rules for every connected tool#

Every connected tool should meet four rules:

| Integration rule | Section detail |

|---|---|

| Deterministic status mapping | Map provider states to one internal meaning every time. In event-driven systems (including Stripe), delivery can be out of order, and some actions can emit multiple events, so sequence-dependent logic creates matching noise. |

| Event replay support | Do not rely only on live webhooks. Require a documented retrieval path for historical events. For Stripe specifically, undelivered events are retried for up to three days, and events are retrievable by API for 30 days. |

| Idempotent retries | The same keyed retry should return the same result, not create duplicate effects. |

| Exportable audit trail | Require a chronological, exportable record of who did what and when. UI-only history is weak when finance needs evidence. |

Step 3. Screen vendors against your real reconciliation path#

Use one practical filter: does this improve your actual settlement and matching flow, or just add another tool? Evaluate each addition for cost, complexity, and scalability.

Ask two fit questions:

- Will it reduce unresolved exceptions by making status handling clearer and more provable?

- Will it shorten time from settlement receipt to matched ledger state without adding manual exports or adjustments?

If both answers are no, skip it.

Step 4. Use AI as a speed layer, not a control owner#

Use AI tools to speed repetitive finance work, not to own control decisions. Management remains responsible for internal control over financial reporting, and AI governance expectations still point back to human oversight.

Set one hard rule: AI can recommend or summarize, but a named person approves financial actions, exception outcomes, and control overrides. If people cannot monitor, interpret, and override outputs, control ownership is unclear.

Related: Accounting for Tech Companies: How to Structure Finance Ops for a Payment Infrastructure Business.

Track the KPI scorecard that proves lean ops are working#

A scorecard should show two things at once: whether lean ops are reducing effort and whether control quality is holding. Use both leading indicators, which warn early, and lagging indicators, which confirm outcomes.

Step 1. Build one scorecard from a real baseline#

Start from a baseline in your current operation, then measure change against that reference. Keep the scorecard short, reproducible from exported records, and owned metric by metric.

| KPI | Indicator type | What to measure | Why it matters |

|---|---|---|---|

| Manual touches | Leading | Count of human interventions per payment, settlement, or payout batch | Rising touches can signal process strain before close slips |

| Exception aging | Leading | Open exceptions by age bucket and failure class | Unresolved, older exceptions can increase close risk |

| Reconciliation lag | Leading and lagging | Time from settlement receipt or provider event to matched ledger state | Shows whether source-of-truth records are keeping up with operations |

| Payout status visibility | Leading | Count and age of payouts in in-flight states versus terminal outcomes | If you cannot see movement to paid, failed, or canceled, payout risk is harder to control |

| Close cycle time | Lagging | Calendar days from trial balance run to completion of consolidated financial statements | Shows whether finance capacity is being freed for decision support or consumed by cleanup |

Each KPI should trace back to exported event IDs, ledger references, or matching logs, not just dashboard views.

Step 2. Attach every KPI to an action window#

A KPI without a response window is just a chart. Define each alert as threshold plus time window: what level counts as a breach, and how long it can remain before intervention.

For Exception handling, define three things per KPI: who intervenes, by when, and what "recovered" means. Recovery should be a resolved state or a documented exception with a clear next action and owner.

Set those windows with provider limits in mind. Stripe retries undelivered webhooks for up to three days, and event retrieval in this flow is limited to the last 30 days. If exceptions can age past that evidence window, trigger earlier.

Step 3. Read the scorecard with month-end close context#

Review the scorecard monthly alongside Month-end close findings so leaders can separate growth pressure from control failure. Use close cycle time consistently as calendar days from trial balance run to completion of consolidated financial statements.

Use benchmarks as context, not as your target. In one APQC benchmark cited across 2,300 organizations, median close was 6.4 calendar days, top quartile was 4.8 days or less, and bottom quartile was 10 or more. Pair that context with your own risk profile and operating model. This Month-End Close guide is the companion reference.

A practical readout helps: if close time worsens while exception aging and matching lag stay stable, volume or capacity pressure may be a factor. If close time worsens alongside aged exceptions, stale payout states, or rising manual touches, treat it as a likely control issue.

Step 4. Tie headcount decisions to process-stability evidence#

Queue pressure alone is weak evidence for adding headcount. A practical trigger is a stable process that still misses internal service-level or control thresholds after automation, ownership, and escalation rules are in place.

In practice, confirm that control ownership and monitoring are stable, and that teams can produce an exportable audit trail. If those are not stable, added capacity can hide process debt instead of fixing it.

Common mistakes and how to recover fast#

When manual touches rise, exceptions age, or payout states go stale, fix control sequencing before you add more automation.

Step 1. Lock ledger posting rules before expanding AP automation#

Before scaling AP automation, confirm invoice coding and General ledger posting rules are stable. If coding is incomplete, invoices can move operationally but fail accounting control. In Oracle's flow, invoices in Initiated account coding status are not validated and cannot be paid.

Recovery is straightforward: pause new AP automation, route invoices needing distribution details to coding before validation, and keep payment approval as a control after coding quality is confirmed. Approval helps control disbursement, but it does not replace complete account mapping.

Use one verification point: sample recent invoices and confirm the chain from coding completion to validation status to final ledger account outcome before payment release.

Step 2. Tie payout execution to reconciliation before release#

Treat payout execution and matching as one control lane, not two. Releasing payouts without transaction-to-payout tie-out increases reconciliation risk.

Recovery: enforce a pre-release tie-out check, especially for manual payouts. Stripe states that for manual payouts, you are responsible for reconciling against transaction history, and it notes that automatic payouts simplify reconciliation by preserving transaction-to-payout association.

Hold any payout batch that lacks a reference list mapping included transactions or balance movements to payout records and expected General ledger treatment.

Step 3. Pilot vendor claims against your decision matrix#

Use vendor ROI claims as hypotheses, not decisions. Ramp markets average savings of 5% while noting results are estimates, not guarantees. Brex markets outcomes such as up to 250 hours per year saved. PEX emphasizes real-time spend control.

Recovery: run each tool through the same Decision matrix you use for automation priorities and score process fit against your own manual-touch volume, error cost, compliance risk, and customer impact. Keep FTC substantiation discipline in mind: objective claims need a reasonable basis before dissemination.

Step 4. Assign an owner and replay rules for stale provider events#

Stale provider events need explicit ownership so unresolved deliveries do not become reconciliation gaps. Stripe shows Delivered, Pending, and Failed webhook deliveries, retries for up to 3 days in live mode, and supports querying missed events over any time period.

Recovery: assign one owner, define escalation windows inside the 3-day retry period, and document when to wait, investigate endpoint failure, or replay from missed-event queries. If recovery uses idempotent requests, tie keys to immutable reference IDs, keep within Stripe's 255-character limit, and follow key-retention guidance, since keys can be removed after at least 24 hours. Review Pending and Failed deliveries weekly with owner, age, and replay outcome.

If your team is standardizing systems next, see How to Build the Ultimate Finance Tech Stack for a Payment Platform: Tools for AP Billing Treasury and Reporting.

Put this into action this quarter#

Do not change AP, payouts, and close all at once. Pick one lane, make the control points visible, and use a short review cycle to confirm you improved operations instead of just moving work around.

Step 1. Pick one lane and map handoffs#

Start with your Settlement workflow and matching path, where breaks can be hard to unwind later. Map the flow from transaction or invoice confirmation through ledger posting, settlement match, payout release or hold, and exception resolution. For each step, record the input, system action, owner, expected status, and failure signal.

Keep the map concrete. If a provider event changes status, note where it lands and who reviews it. If adjustments can be posted in more than one place, centralize that authority before further automation.

Then verify with real items. Trace a few recent cases end to end and confirm you can find the ledger entry, settlement match result, payout decision, and exception evidence without relying on memory or side spreadsheets.

Step 2. Build the first decision matrix and select one change#

Use a first-pass Decision matrix on actual lane pain points and choose one change. The goal is to stop debating many ideas and select one meaningful, controllable pilot.

Prioritize deterministic steps over judgment-heavy ones. Strong candidates include matching rules, stale-status exception routing, or approval gating before payout release. Avoid changes that hide unresolved breaks or depend on manual resend behavior.

If a change lowers touches but makes exceptions harder to explain, pause it. That tradeoff can show up at month-end close.

Step 3. Baseline the KPI scorecard before production changes#

Capture your baseline KPI scorecard before the pilot starts. At minimum, track manual touches, exception aging, payout status visibility, General ledger matching cycle time, and Month-end close timing. Assign an owner and corrective action for each KPI.

Use an early checkpoint as a first review, not proof that the process is fully solved. At that checkpoint, compare against baseline and ask: did exception aging improve, and did close reliability improve? If not, tighten exception handling before expanding scope. If close sequencing is still weak, this Month-End Close for Payment Platforms: A Step-by-Step Checklist for Finance Teams can help.

Step 4. Pilot one automation change and inspect evidence#

Launch one automation change, then inspect traceability evidence before declaring success. In practice, check whether an operator can trace a sample item across reference ID, approval history, status changes, retry behavior, and final ledger outcome. If retries occurred, confirm they stayed tied to the same immutable reference and did not create duplicate financial state changes.

Watch for common failure modes: manual resends outside the tracked path, spreadsheet adjustments that never return to the ledger, or exception queues without escalation timers. Those patterns can lower visible effort while raising hidden control risk.

Copy and paste checklist#

- Define the General ledger source of truth and ownership map.

- Document exception classes, escalation timers, and retry rules.

- Baseline KPI scorecard and Month-end close metrics.

- Pilot one automation change, then verify traceability evidence.

- Expand only after exception aging and close reliability improve.

If AP is a bottleneck, see How to Make the Case for AP Automation to Your CFO: A Platform Finance Team Playbook.

When your ownership map and exception rules are stable, validate the payout lane against your control checkpoints and escalation SLAs with Gruv Payouts.

Frequently Asked Questions

How can a small finance team run payment operations at scale without losing control?

Use a consistent general-ledger-first process and assign clear owners for ingest, matching, and payout release. Keep separation of duties and documented approval and recordkeeping steps so one person does not carry a transaction all the way through without a second control point.

What should be automated first in a payment platform: AP tasks, reconciliation, or payouts?

There is no universal order. Start with the lane that has the highest manual touch and stable rules, then expand iteratively. If automation cuts work but increases unresolved discrepancies, pause and fix exception handling first.

Which controls are non-negotiable for lean finance ops?

Keep separation of duties, documented control activities, and traceable approval evidence for financial state changes. These controls should be explicit policies and procedures, not informal team habits. Depending on your environment, PCI DSS and annual internal-control effectiveness reviews for U.S. issuers may also matter.

How do we reduce manual work while keeping an audit-ready trail?

Automate only where inputs, system actions, owners, and expected statuses are explicit and logged. Use reference IDs, approval history, and exception records so a payout or invoice can be traced end to end. If the trail breaks at manual workarounds or missing approvals, control quality has dropped even if effort falls.

What KPI scorecard proves lean accounting is improving operations?

Use a scorecard that combines speed and control, including monthly close cycle time, general ledger reconciliation cycle time, manual touches, and exception aging. Keep each metric concrete, assign an owner, and define a corrective action path. Otherwise, the scorecard will not change behavior.

How do idempotent retries change payout reliability and incident recovery?

Idempotent retries let you repeat failed requests without creating duplicate objects. In Stripe's guidance, the first response for a key is stored, including failures, so the same key returns the same result. Tie each key to an immutable reference, keep it within the 255-character limit, and align retention and replay rules with the guidance that keys can be removed after at least 24 hours.

When should we add people instead of adding more automation?

Add headcount when process design and controls are already stable but service or close outcomes still miss expectations. Automation works best when the process is clear and goals are explicit. When delays are driven by judgment-heavy exceptions or approval bottlenecks, another operator or reviewer may help more than another automation pass.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- csrc.nist.gov/glossary/term/audit_trailtrusted

- csrc.nist.gov/glossary/term/audit_logtrusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-17/chapter-II/part-229/subpart...trusted

- gao.gov/assets/670/665714.txttrusted

- gao.gov/pdf/product/665712trusted

- guides.gaoinnovations.gov/greenbook/2025/principle-3-establish-structu...trusted

- guides.gaoinnovations.gov/greenbook/2025/principle-16-perform-monitori...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: