Quick Answer

Start with three controls: a written journal posting policy, a compliance-gated payout release rule, and a named-owner exception path. Then run reconciliation and settlement against rail-specific timing windows, and validate each period with traceability from event intake to ledger outcome. The result is more reliable close performance: fewer duplicate postings from retries, clearer ownership when payouts are blocked, and faster recovery when provider updates arrive late.

Build a Controller-Grade Finance Ops System for Payment Platforms#

If your close depends on matching payout activity and provider reports to the General Ledger, controller-grade ops comes down to one standard: you can trace each posting, explain each exception, and show reliable evidence for why the books are right. This is for operators who own that outcome across payment events and ledger results, not just generic bookkeeping cleanup.

- Who this is for

This article is for teams such as a Financial Controller, Finance Ops lead, or product owner accountable for ledger accuracy as money moves through APIs, event deliveries, provider reports, and payout rails. The standard is operational ownership. When a Ledger Journal entry cannot be tied to the originating payment event, or a Payout Batch closes with unexplained variance, you own the fix.

- What this is not

This is not broad advice like "reconcile often" or "document your process." The focus is General Ledger integrity, clear approval and exception ownership, and evidence quality that is relevant and reliable, consistent with PCAOB AS 1105. In practice, you should be able to pull a sample journal, show the source event or provider record, show exception review where applicable, and explain why the posting logic was valid.

- How the list is ranked

The recommendations are selected using four filters: month-end close impact, repeat-failure risk, implementation burden, and traceability from API or event activity to Ledger Journal entries. A webhook is an HTTP endpoint that receives payment-related events, and webhooks can help process large volumes of business-critical events. Idempotency keys support safe retries without duplicate operations. If you cannot show how duplicate requests, delayed events, and replayed deliveries are prevented from creating duplicate postings, the control design is incomplete.

- What you should expect to get

You will get a practical order of operations, known failure points, and decision checkpoints that help growth without weakening ledger control. The guidance is specific, but it does not assume one universal sequence for every platform. A practical rule applies throughout: if a transaction cannot be traced from source event to tie-out result to final ledger impact, treat that as a design gap before adding more automation.

For teams subject to formal internal-control requirements, the underlying ICFR standard is mandatory. SEC Item 308 assigns management responsibility for internal control over financial reporting, requires disclosure of material weaknesses, and does not allow an effective-control conclusion when material weaknesses exist. Even if you are not under that requirement today, this is still a useful pressure test.

Your close evidence pack should be easy to retrieve and hard to dispute. Include the source event ID, idempotency key if used, provider reference, journal reference, and approval or exception record.

If you want a deeper dive, read Lean Accounting for Payment Platforms: How to Run Efficient Finance Ops Without a Big Team.

Set ownership boundaries before you automate anything#

If Finance Ops, engineering, and risk all touch the same matching and payout chain, settle ownership before you add automation. Clear ownership keeps exceptions from stalling, evidence from going missing, and close accountability from getting blurry.

This is a control design step, not a documentation exercise. Payment operations span onboarding, money movement, tracking, and matching, so ownership should cover more than the General Ledger. Internal-control guidance also puts responsibility on management and supports separating authority, custody, and accounting activities. In practice, avoid letting one person default into all three roles: Ledger Journal policy, exception clearance, and close approval.

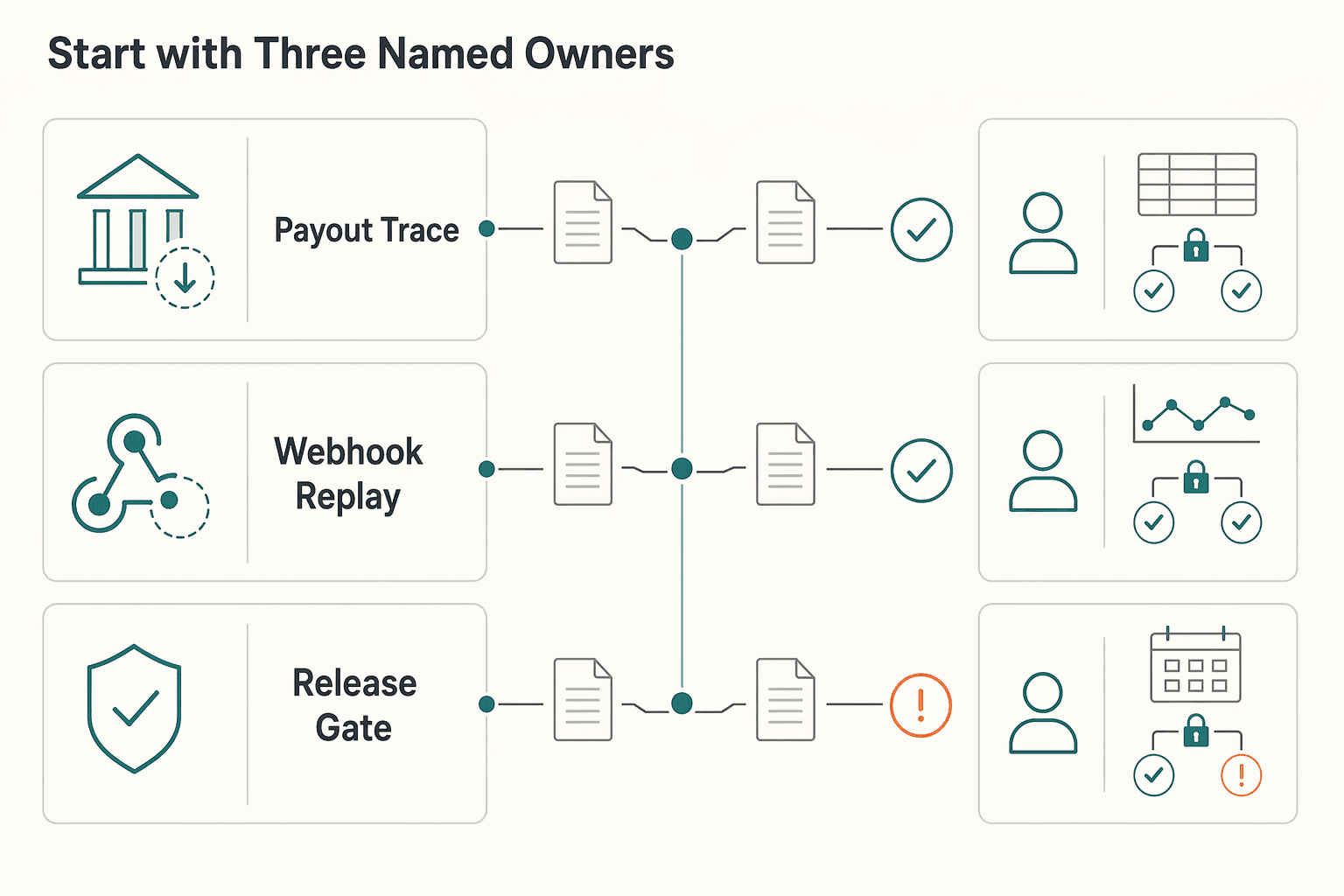

Start with three named owners#

Before any new matching bot, posting rule, or payout automation goes live, assign one accountable owner for each area below. One owner does not mean one person does all the work. It means one person is answerable when evidence is missing or an exception is unresolved.

| Area | Accountable owner | What good evidence looks like |

|---|---|---|

| Ledger Journal policy | Financial Controller or designated accounting owner | Posting rules, approval record for logic changes, sample trace from source event to journal |

| Webhook exception triage | Engineering or Finance Ops owner, named explicitly | Exception Queue status, retry history, event ID, resolution note |

| Close sign-off | Finance lead with month-end authority | Summary tie-out, unresolved-item log, sign-off record tied to the close cycle |

Checkpoint before go-live: confirm each owner has decision rights in the Approval Workflow, not just role labels. Early bottlenecks can happen when duties are separated, so plan for that tradeoff before close pressure hits.

Pay special attention to event-delivery exception ownership. These flows are asynchronous, and undelivered events can be retried for up to three days, so an unowned queue can create delayed postings and weaker traceability back to the source event. If you send ACH, review whether the March 2024 Nacha responsibility updates apply to your organization and whether legal, compliance, fraud, or cybersecurity should be included in your ownership map before go-live.

Related: Accounting for Tech Companies: How to Structure Finance Ops for a Payment Infrastructure Business.

Choose your source of truth and map every posting path#

Once ownership is clear, make one decision before anything else: what is allowed to create a Ledger Journal entry. If final provider states are asynchronous, use a ledger-first path for those flows. Post from validated API or event inputs, then use bank activity and provider reports to verify completeness.

Bank tie-out still matters, but it serves a different control objective. It checks internal records against bank statements for completeness. As a primary posting trigger, it can be weaker for event-level traceability because bank-side outputs may not preserve the same payment-message detail end to end. If you want defensible matching, separate posting evidence from cash-verification evidence.

1. Ledger-first posting#

In a ledger-first model, transaction-level events create or update the journal, not the bank line. That can give you a direct chain from source event to journal entry to later provider evidence.

Adyen guidance matches this design: track transaction activity through API responses and webhooks, update ledgers from those events, then use the daily Balance Platform Accounting Report to reconcile funds. Stripe follows a similar split in practice: balance transactions represent funds moving through your Stripe account, and payout reconciliation reporting ties transactions into payout batches.

| Decision area | Ledger-first model | Bank-first model |

|---|---|---|

| Traceability | Links source event, provider transaction record, and Ledger Journal directly | Often starts from amount/date matching and may have less event-level detail |

| Close handling | Can support daily or higher-frequency matching when journals are posted before full bank visibility | Can require waiting for bank lines or statement detail before full tie-out |

| Error recovery | Can be easier to isolate missing or duplicate postings by event ID or provider transaction ID | Can be harder to isolate whether the break is bank output, message transformation, or posting logic |

2. Bank feeds and payout reports as verification#

Use bank feeds, payout reports, and daily accounting reports as verification layers. Their job is to confirm completeness, not define transaction meaning. Bank-first is not automatically wrong, but you should choose it deliberately and document the tradeoff.

Stripe shows why this matters. Automatic payouts maintain transaction-to-payout association for matching, while with manual payouts Stripe says it cannot identify which transactions are included in each payout. That product setting directly affects how defensible your posting path will be later.

The same issue shows up with asynchronous lifecycle updates. Stripe webhooks handle asynchronous events, and Stripe retries undelivered events for up to three days. If you post from bank activity during that gap and then post again when delayed events are processed, you can create duplicate or conflicting entries. The control is straightforward: post from validated journal-triggering events, then tie bank movement back to those entries.

3. A written posting-path map for every money movement#

Do not leave posting logic in people's heads. Write the model down so close and exception handling do not depend on ad hoc judgment.

For each posting path, define the items below:

- the source event allowed to create or update the Ledger Journal

- the validation checkpoint required before posting

- the verification artifact used after posting

- the owner responsible for exception clearance

Name concrete artifacts, not generic labels. Typical evidence includes provider event ID, balance transaction ID, payout ID or payout-batch reference, Ledger Journal ID, and the matching line in a payout report or bank statement. For Adyen, verification may rely on the Balance Platform Accounting Report. For Stripe, it may rely on balance transactions plus payout reporting.

Use a go-live checkpoint that traces real transactions end to end across multiple outcomes. If any path still depends on manual spreadsheet judgment because event-to-journal rules are unclear, the source-of-truth policy is not complete.

If final statuses can arrive asynchronously, the practical rule is simple: post from validated ledger events, then use bank tie-out afterward to prove completeness.

Standardize a settlement calendar that survives growth#

After you decide what can post, decide when it belongs in a close cycle. If Ops and Accounting keep arguing about timing, use a rail-specific calendar with explicit cutoff, posting, and review windows. Assign each window to a named owner in Finance or Ops. Operating-day boundaries and batch-close patterns differ by rail and provider.

| Rail or batch type | Boundary to calendar against | What it changes in close |

|---|---|---|

| Same Day ACH | Example FedACH window shows 10:30 a.m. ET transmission with 1:00 p.m. ET settlement on the current day | Cutoffs should follow the ACH schedule in use, not a generic midnight boundary |

| Fedwire | Business day begins at 9:00 p.m. ET on the preceding calendar day and ends at 7:00 p.m. ET | Posting and review need to follow Fedwire day boundaries, not office-calendar assumptions |

| FedNow | Cycle day is generally 7 p.m. to 7 p.m. ET the next day | Instant payments still need a defined accounting boundary and report schedule |

| Provider payout batch | Adyen says payable batches close according to the payout frequency defined for a merchant account | Merchant or account payout configuration can set timing |

1. Cutoff window#

Define the exact in and out boundary first. For Fedwire, use the 9:00 p.m. ET to 7:00 p.m. ET business day. For FedNow, use the cycle day, generally 7 p.m. to 7 p.m. ET the next day. For Same Day ACH, use the transmission and settlement schedule that applies to your file, such as the published 10:30 a.m. ET transmission and 1:00 p.m. ET current-day settlement example.

Avoid cutoff language like "end of day" without a rail reference. Keep evidence for each closed window: report timestamp, provider or payout-batch identifier, and the policy line that defines the applied cutoff.

2. Posting window#

Set a separate posting window for when validated activity can hit the General Ledger. Provider cutoff and GL posting are different control points. Oracle payables close guidance follows that sequence: complete and approve transactions and payment files, then transfer approved invoices and payments to the general ledger.

Assign this posting window to one named owner, not a shared mailbox. The principle is simple: assign responsibility and delegate authority. If approvals are incomplete at posting time, keep the item in a documented exception state with an owner and reason code.

3. Review window#

Use the review window to compare provider reports, matching evidence, and GL support, and document any breaks. Stripe payout reconciliation treats transactions in each payout as a batch, and Stripe bank reconciliation tracks payout status against bank deposits. Oracle receivables-to-GL reporting adds a balance-level check with beginning balances, ending balances, and period activity.

Run one verification checkpoint each cycle: compare provider report totals, GL balances, and reconciliation logs, then log residual differences as open recon items with owner and aging. If payout-batch totals align but bank deposit timing differs, classify it as a timing item. If bank deposits align but the GL is off, classify it as a posting or mapping issue.

For a step-by-step walkthrough, see Microsoft Dynamics 365 for Payment Platforms: Finance Module Setup and Payout Integration Guide.

Treat payout execution as a controlled production process#

Payout release should behave like a controlled production step, not a background task. In high-volume batches, explicit gates and exception states help keep retry noise, event lag, and provider failures from turning into accounting breaks. The tradeoff is real: tighter controls can delay payouts when account data is incomplete.

Gate release before money moves#

Put the eligibility gate at release time. If required verification is still outstanding for your program, block release and route the item to your Exception Queue instead of forcing a manual override.

This lines up with provider behavior: payouts can remain disabled until verification requirements are fulfilled, and outstanding requirements can restrict capabilities. Where bank-program CIP minimum data applies, use your actual required identity fields and documented status as the release condition.

Use exception states you can operate and close#

Your labels are internal, but every blocked or failed payout should have one clear state, one owner, one next action, and one evidence set.

| Internal exception state | What it means operationally | Release or retry rule | Evidence to retain |

|---|---|---|---|

| Verification outstanding | Account requirements are still due, so payout eligibility is restricted | Do not release until required verification fields are resolved | Account requirement status, owner, decision timestamp |

| Duplicate idempotency key | Retry reused the same key and returned the same prior result | Treat as correlation to the original attempt. Confirm original outcome before new action | Idempotency key, original request ID, returned response |

| Webhook status not final | Depending on provider behavior, events can arrive out of order or be resent later | Use event timestamps and confirm current provider object state before final status changes | Event IDs, timestamps, replay or resend evidence, current status check |

| Payout failed or returned | Provider reported non-success outcome, failed or returned | Route to exception handling with correction or follow-up action before release | Failure code or reason, payout ID, remediation record |

Two controls matter most in practice. A reused idempotency key is not a new payout attempt by itself. Webhook delivery can arrive out of sequence, so timestamp checks plus current-state validation should drive final status decisions.

Close each batch with evidence, not memory#

Close each Payout Batch with a standard evidence packet so Finance Ops can revalidate outcomes later without rework. The packet should let someone else reproduce the result without relying on memory. At minimum, include:

- batch totals, count and amount, versus submission totals

- exception outcomes, including failed, returned, and blocked items, with reasons

- retry history showing same-key retries versus new attempts

- if your internal closeout includes ledger journals, tie posted accounting outcomes to validated payout states

If you run PayPal Payouts, a batch can include up to 15,000 payments per API call, so check both batch-level totals and item-level exceptions. Also account for delayed outcomes: unclaimed PayPal payouts can be returned after 30 days, so day-one status is not always final.

We covered this in detail in SaaS Accounting Software Evaluation: What Payment Platforms Need Beyond Standard GL Features.

If you are defining batch close controls and exception handling, review Gruv Payouts workflows to align statuses, retries, and audit evidence.

Design idempotent retries and webhook replays from day one#

Duplicate inputs will create matching noise unless retries and event handling are replay-safe by design. If an API call can trigger money movement or an internal posting entry, route it through one idempotent write path. Treat every provider event as replayable input, not a new instruction.

Idempotent request path#

Use one client-generated key from the first POST through your internal posting decision. The HTTP Idempotency-Key pattern is meant to make non-idempotent methods retry-safe, and provider variants like PayPal-Request-Id can follow the same operating model on APIs that explicitly support it. If a caller times out, retry with the same key where the API supports that behavior.

Persist enough data on that key to make safe decisions: request payload hash, provider request ID, provider object ID, posting decision, and final response body. Stripe returns the same result for reused keys, including 500 errors. Repeated failure on the same key is a signal to verify the original outcome before allowing any second posting or manual reissue. If you support Adyen, enforce the key-length limit at implementation time: maximum 64 characters.

Webhook deduplication#

Log provider event IDs before any accounting side effect runs. Stripe explicitly warns that endpoints can receive the same event more than once, and its guidance is to store processed event IDs and skip anything already logged.

Use immutable receipt records with event ID, event type, provider object ID, receive timestamp, processing status, and internal record touched. This matters even more for PayPal, where any non-2xx response can trigger redelivery up to 25 times over 3 days.

A practical control check is to sample replayed events and confirm they resolve to "already processed" with no new internal posting entry.

Out-of-order event control#

Do not post deltas based on arrival order. Stripe does not guarantee in-order delivery, and its guidance is to retrieve missing objects through the API when event sequence is incomplete or unexpected.

Apply transitions from verified current state, not from event order. If an internal record is already in a terminal state, a late intermediate event should be logged and ignored. If the sequence looks incomplete, fetch current provider object state first, then apply only allowed transitions from your state model.

For auditability, keep evidence of the processed event ID, prior internal status, fetched provider status when used, and the transition rule that allowed or blocked the change.

Need the full breakdown? Read Accounting Automation for Platforms That Removes Manual Journals and Speeds Close.

Put compliance gates in the transaction path, not in side docs#

If compliance status can stop a payout, your release logic should enforce that directly. Treat KYC, business verification, and AML decisions as transaction-path controls, not notes in onboarding files or spreadsheets.

Gate on live eligibility#

Use the live eligibility signal your processor exposes and make payout release depend on it. In Stripe Connect, payouts_enabled indicates whether a connected account can pay out to an external account. If it is false, block release before any release file, provider instruction, or downstream Ledger Journal is created.

This keeps decisions tied to current provider state, not stale onboarding assumptions. Stripe also notes unresolved requirements can disable charges or payouts after a grace period (documented as 14 days in that flow), so a one-time onboarding check is not enough.

Store reason codes, not generic holds#

A gate works best operationally when block reasons are machine-readable. Stripe provides requirements.disabled_reason, and Adyen also notes payouts can be blocked for compliance reasons at merchant or company level. Keep those provider reasons intact in your exception queue instead of collapsing them into a generic "compliance issue."

For each blocked payout, keep a record with:

- provider account ID

- payout ID or internal transaction ID

- block reason

- first blocked timestamp

- current age

- required follow-up

- reviewer

- final release or rejection outcome

Treat KYC and AML as ongoing controls#

Do not model compliance as a one-time pass or fail at signup. CDD includes ongoing monitoring to identify and report suspicious transactions and, on a risk basis, maintain and update customer information. FinCEN also describes beneficial ownership identification and verification as one of four core CDD elements.

If you operate a U.S. money services business, AML programs must be reasonably designed to prevent misuse for money laundering and terrorist financing. That is why the control belongs in the payout path itself.

Review aging and release outcomes on a recurring cadence#

Use a recurring checkpoint, for example monthly, on blocked payouts by reason code, aging, and release outcome. Track what cleared, what is still aging, which reasons dominate, and which items are approaching provider deadlines.

If blocked volume rises while reason coding degrades into free text, the gate is weak in practice. The control is working when Finance Ops can open any blocked payout and immediately see why it is stopped, what must change, and what event restores eligibility.

Improve AP hygiene without overloading your close process#

Keep vendor AP and customer payout liabilities on separate control paths. As a default, route an AP issue into the payout Exception Queue only when it could change a provider or payout release decision.

1. Keep liabilities separate in the ledger#

This is a core control boundary. IAS 1 paragraph 54 supports presenting trade and other payables separately from other financial liabilities, which aligns with keeping vendor invoices distinct from payout obligations. In safeguarding regimes where relevant-funds rules apply, relevant funds must be kept separate from other funds.

In practice, keep vendor invoices in the vendor payment cycle and payout obligations in the provider and payout chain. Avoid merging their matching paths unless the issue directly affects payout liability.

2. Standardize intake, but do not build an approval maze#

Use a paperless AP intake and a documented approval workflow with clear owners so controls are established, documented, and maintained. Avoid layering approvals that slow routine invoices with no customer-fund impact. Segregation of duties should separate authority, custody, and accounting, but escalation should still be risk-based. For genuinely payout-critical invoices, define a narrow expedited path with clear approver authority instead of bypassing controls informally.

3. Route exceptions by operational impact#

Use this routing default: if the AP exception does not affect payout liability, keep it in AP review rather than the payout queue. Send it to AP review with its own evidence pack:

- vendor name and invoice number

- PO, contract, or service confirmation

- approver and approval timestamp

- GL account and liability classification

- payment status and exception reason

Your close checkpoint should stay simple: AP aging, payout liability aging, and provider matching should each be reviewable without cross-contamination. If one mixed queue makes it unclear what blocks vendor payment versus customer payout, your routing is likely too broad. Related reading: Best Accounting Firms for Startups if You Run on Client Cashflow.

Build tax-document operations that are auditable and low-friction#

After separating AP and payout liabilities, apply the same discipline to tax records. Collect the required tax form before payout activity, keep one authoritative timestamped record, and link tax status to the Ledger Journal entries it supports.

| Form | Use for | Note |

|---|---|---|

| W-9 | U.S. payees | Lets the payee provide the correct TIN to the requester |

| W-8BEN | Foreign individuals | Used when requested by the withholding agent or payer |

| W-8BEN-E | Foreign entities | Documents foreign entity status for chapters 3 and 4 |

- Collect the correct form during payee setup

For U.S. payees, use Form W-9 so the payee can provide the correct TIN to the requester. For foreign individuals, use Form W-8BEN when requested by the withholding agent or payer. For foreign entities, use Form W-8BEN-E to document foreign entity status for chapters 3 and 4. These forms are provided to the requester, payer, or withholding agent as applicable and retained in your process.

Do not let payout go live with a blank or unverified tax profile. If a required TIN is missing or incorrect, backup withholding can apply at 24%.

- Use one evidence pack per tax profile

Keep tax support in one operating record instead of scattered email attachments or ticket notes. For each payee, store form type, status, collection timestamp, the latest validation status or date, and the reference that links that profile to payout eligibility and related Ledger Journal postings.

A practical pack includes:

- form type (

W-9,W-8BEN, orW-8BEN-E) - received timestamp and current status

- payee legal name and tax classification used in the profile

- TIN or foreign-status validation result where applicable

- Ledger Journal link or posting reference

- reviewer and timestamp for manual overrides or status changes

For close, sample reportable payees and confirm tax-profile status matches the posting population in the ledger.

- Keep platform reporting records separate from personal tax artifacts

Form 1099-K is a payer-side reporting obligation: a payment settlement entity files it for reportable payment transactions, including payment card and third party network transactions. Treat that as a payer-side recordkeeping workflow, not a year-end scramble.

Keep personal taxpayer items scoped. FEIE is an individual taxpayer claim and requires Form 2555 attached to Form 1040/1040X. FBAR is separate, tied to foreign financial accounts that exceed an aggregate $10,000 during the year, due April 15 with an automatic extension to October 15. If these appear in support workflows, do not mix them into withholding or 1099 evidence unless there is a clear operational reason.

Use one control rule: no tax-status-dependent payout or reporting classification without a timestamped document record and a direct link to the posting trail.

This pairs well with our guide on Vendor Relationship Management for Platforms That Finance and Ops Can Run.

Decide when to use Virtual Accounts and Merchant of Record#

Use Virtual Accounts when inbound collection attribution is the bottleneck. Evaluate Merchant of Record (MoR) first when the bigger constraint is centralized transaction compliance ownership across markets.

A Virtual Account helps organize receivables and payables with unique identifiers, but it is not a separate physical cash-holding account. An MoR is the entity legally responsible for processing customer payments, and that scope can include financial, legal, and compliance responsibilities, including refunds and chargebacks.

| Decision area | Virtual Accounts | Merchant of Record (MoR) |

|---|---|---|

| Control ownership | You typically keep more direct control of collection flows, with cleaner receipt attribution through unique account identifiers. | Legal and operational payment responsibility sits with the MoR. |

| Settlement visibility | Typically stronger line of sight into direct inbound collection and attribution in your own structure. | Settlement and reporting may be shaped by the MoR outputs and contract scope. Validate report-to-ledger mapping before commit. |

| Reconciliation burden | Improves inbound attribution, but does not remove asynchronous state risk. Some outcomes, including refunds, can finalize later via webhooks. | Can reduce some operational burden, but you still need clear status mapping into your ledger and matching controls. |

| Compliance dependencies | Does not by itself transfer transaction compliance ownership. | Better fit when you want one party to absorb more tax and compliance operations, but eligibility and scope must be confirmed in writing. |

Two guardrails matter in either model. First, asynchronous events must be replay-safe and idempotent in your matching design, including delayed refund outcomes, because some providers may retry undelivered events for up to three days. Second, do not turn coverage marketing into policy. If materials show different scope figures, such as 75+ versus 80+ countries plus product-category qualifiers, validate current country and product eligibility in contract artifacts before relying on them.

Final checkpoint: require one written mapping from collection or provider events to ledger postings, because neither model makes up for weak matching.

Run a weekly and monthly checkpoint scorecard#

Once the posting path, timing, and gating logic are in place, use a short scorecard to catch drift before it turns into close pain. A practical cadence is weekly for early warning and monthly for control review. It only works if threshold breaches have clear ownership and escalation. Otherwise, it becomes dashboard noise.

| Metric | What to review | Follow-up |

|---|---|---|

| Reconciliation break rate | Current-period breaks and trend direction | Assign an owner and document the cause and corrective action |

| Settlement aging | Whether cash movement and ledger recognition are staying aligned | Support with transaction-level provider detail and batch-to-bank-statement matching |

| Exception Queue volume | Open volume split into new, aging, and reopened cases | Tie each unresolved case to a named owner and reporting-line escalation path |

| Payout Batch retry outcomes | Results by batch, outcome, and final posting status | Treat a retry as incomplete until the ledger outcome is confirmed |

- Reconciliation break rate

Track both current-period breaks and trend direction, not just totals. Your controller view should show recent period-over-period movement, plus month, quarter, and year trend views where volume justifies it. If the rate rises, assign an owner and document the cause and corrective action.

- Settlement aging

Use aging to test whether cash movement and ledger recognition are staying aligned. Support the checkpoint with transaction-level provider detail and batch-to-bank-statement matching. A monthly aging number without underlying evidence is weak for close review.

- Exception Queue volume

Monitor open volume, but split it into new, aging, and reopened cases so response quality is visible. Keep each unresolved case tied to a named owner and reporting-line escalation path. If ACH exceptions are in scope, historical windows such as a 13-month archive and a two-year repository can help confirm whether a case is truly new or recurring.

- Payout Batch retry outcomes

Treat retry outcomes as a control metric, not just an operations metric, because many failed payments are recoverable. Review results by batch, outcome, and final posting status. For control purposes, treat a retry as incomplete until the ledger outcome is confirmed.

Your verification checkpoint should be strict: every metric has a named owner, a defined threshold, an escalation path through established reporting lines, and an attached evidence artifact for Finance Ops review. If breaches repeat and are not prevented or detected on a timely basis, treat them as potential control deficiencies and document corrective actions.

Turn this into your next 90-day operating plan#

The first 90 days should lock down a small set of controls that can materially reduce close and payout risk: source of truth, payout exception handling, and compliance gating. If those three are clear, automation has something solid to build on. If they are not, more tooling usually just makes errors harder to unwind.

| Days | Focus | Key actions |

|---|---|---|

| 1 to 30 | Ownership and definitions | Assign clear ownership for ICFR-related controls and daily exception operations; document a source-of-truth policy, a payout exception taxonomy, and a compliance eligibility policy |

| 31 to 60 | Automate stable paths, then shadow them | Automate repeatable flows with idempotent write behavior and replay-safe event handling; run a phased rollout with shadow-mode comparison before full cutover |

| 61 to 90 | KPI checkpoints and escalation discipline | Add recurring monitoring tied to owners and actions; track exception backlog aging, blocked payouts by reason, replayed event volume, and unreconciled close items |

- Days 1 to 30. Set ownership and definitions.

Start by assigning clear ownership for ICFR-related controls and daily exception operations, then document the rules each team follows. For SEC issuers, management is responsible for establishing and maintaining ICFR, reporting on its effectiveness at year end, and evaluating ICFR changes during the year. Keep the documentation tight: a source-of-truth policy, a payout exception taxonomy, and a compliance eligibility policy. Define which record can post to the ledger, which failures enter the exception queue, and which compliance states block release. If teams give different answers to "what posts to the ledger," stop there and resolve that first.

- Days 31 to 60. Automate stable paths, then shadow them.

After definitions are stable, automate repeatable flows with idempotent write behavior and replay-safe event handling. Idempotency keys support safe retries by reusing the first outcome for the same key, and Stripe allows keys up to 255 characters. For webhooks, design for delays and retries: in Stripe, undelivered events are automatically retried for up to three days, and the related event-listing recovery flow is limited to the last 30 days. Run a phased rollout with shadow-mode comparison before full cutover, and compare exceptions, duplicate suppression, and posting deltas before you trust the new path.

- Days 61 to 90. Add KPI checkpoints and escalation discipline.

Once flows are defined and partly automated, add recurring monitoring tied to owners and actions. For MSBs, AML programs must be written, risk-based, and include policies, procedures, and internal controls, so compliance gating should be explicit in release logic, not informal. Track a short monthly scorecard: exception backlog aging, blocked payouts by reason, replayed event volume, and unreconciled close items. Monitor control quality over time, and require escalation when a metric deteriorates in consecutive reviews.

If you run this on Gruv, use supported capabilities to keep transaction records, compliance decisions, and payout outcomes traceable end to end, and confirm market and program coverage before rollout. When you are ready to confirm market coverage and control ownership for rollout, talk with Gruv.

Frequently Asked Questions

What accounting best practices matter most first for a payment platform at scale?

A practical starting point is controls that make transaction recording defensible and reviewable. For SEC issuers, that includes books and records that accurately reflect transactions, supported by internal accounting controls. A useful test is whether you can trace a payout or provider event from API or event intake to the final general ledger entry without guesswork.

Should a controller standardize Reconciliation, close process, or payout controls first?

There is no universal sequence, and a fixed order is usually the wrong approach. Control design should match the payment channels, products, and complexity you actually run. Prioritize the area creating current risk, whether that is matching and posting reliability or payout failure and duplication risk.

How do we reduce payout and settlement errors without slowing growth?

Use structured exception handling with clear retry logic and ownership instead of forcing broad manual review. Keep standard flows moving, and escalate only cases that require intervention. If ACH is in scope, track ACH return-rate signals by rail: 0.5% unauthorized returns, and 3.0% administrative or 15.0% overall return rates, are key ACH monitoring levels.

What proof shows Finance Ops is truly scalable and not just automated?

Scalable operations are explainable, not just fast. Your team should be able to show what posted, why it posted, and who handled exceptions. Reliable proof is consistent evidence linking transaction detail, provider or batch outcomes, and general ledger posting decisions to accountable owners and review checkpoints.

How do Idempotency Key and Webhook controls affect month-end accuracy?

They directly affect duplicate and late-posting risk. Idempotency keys reduce duplicate actions during retries, but they do not by themselves guarantee exactly-once outcomes across every internal step. Because event deliveries can arrive out of order and may retry for up to three days in live mode, month-end controls should use current state or event timestamps and include delayed-event handling.

When should we use Virtual Accounts versus Merchant of Record (MoR)?

Use virtual accounts when your problem is routing and reconciliation detail within a broader settlement account structure. Evaluate MoR when the core decision is legal and compliance responsibility for processing customer payments. These are not interchangeable choices, and in some platform models the platform user, not the platform, is the merchant of record.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- ecfr.gov/current/title-17/chapter-II/part-229/subpart...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- guides.gaoinnovations.gov/greenbook/2025/principle-10-design-control-a...trusted

- guides.gaoinnovations.gov/greenbook/2025/principle-3-establish-structu...trusted

- irs.gov/businesses/small-businesses-self-employed/re...trusted

- irs.gov/individuals/international-taxpayers/foreign-...trusted

- occ.gov/publications-and-resources/publications/comp...trusted

- occ.gov/publications-and-resources/publications/comp...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Lean Accounting for Payment Platforms: How to Run Efficient Finance Ops Without a Big Team

Run finance ops from the **General ledger** first. When transaction records, settlement matching, and **Payout execution** do not share clear control points, small breaks turn into manual cleanup, duplicate actions, and weak close evidence.

Accounting for a Payment Infrastructure Business: How to Structure Finance Ops

Treat payment infrastructure accounting as an operating-control problem first and a reporting problem second. Money movement can clear, settle, or trigger payout activity before month-end. That means finance operations need ledger integrity, reconciliation, settlement tracking, and payout controls, not just clean journal entries after the fact.

Supplier Portal Best Practices for a Self-Service Contractor Payment Hub

If you are building a **supplier portal self-service contractor payment hub**, the real issue is not terminology. It is whether the portal cuts payment-support load without weakening control or reconciliation.