Quick Answer

Start by setting up your own operating foundation, then add outside help in layers. For most readers searching best accounting firms for startups, the practical order is: run bookkeeping and reconciliations in your core system, maintain logs for residency and foreign accounts, and bring in a CPA for filing and interpretation. Keep contractor onboarding tight with required forms and verified payee details. Upgrade to fuller firm support only when complexity creates repeated exceptions across countries, payments, or reporting.

Stop Asking "Which Accounting Firm?" Start Asking "What's My Stack?"#

If you searched for the best accounting firms for startups, the goal makes sense: you want clean books, timely filings, and fewer surprises. The catch is the assumption that one firm should own the whole job. For a solo operator, creator, or small global team, the better move is to build a risk-first financial operations stack around how money actually moves through your business.

| Risk bucket | What to track | Key evidence/action |

|---|---|---|

| Foreign account reporting | Balance tracking against the current filing trigger | Ongoing monitoring task, not just a year-end tax task |

| Residency tracking | Travel days against the current rule | Travel records and dates |

| Cross-border invoicing controls | Entity details and required payment documents | Collect W-9 or W-8BEN before paying contractors |

Most firm roundups are built around a venture-backed profile. Your exposure is usually more practical: cash flow interruptions, missing payment documents, and compliance tasks that sit outside generic startup accounting. A stack keeps ownership with you and outsources only the parts that truly need specialist help.

| Decision lens | Single-firm model | Stack model |

|---|---|---|

| Ownership | One provider holds most context | You keep the records, tools, and handoff points |

| Issue resolution | Depends on firm scope and process | You route each issue to the right tool or specialist |

| Cost control | Simpler billing, but scope can be broad | More moving parts, with spend tied to the tools and support you choose |

In practice, three risk buckets usually drive the choice:

- Foreign account reporting: If you hold money across countries, you need balance tracking against the current filing trigger. This is an ongoing monitoring task, not just a year-end tax task.

- Residency tracking: If tax treatment depends on physical presence, count travel days against the current rule. Your evidence pack matters here, including travel records and dates, not just what you remember later.

- Cross-border invoicing controls: If clients pay from another country, small invoice mistakes can create delays, disputes, and legal headaches. Verify entity details and required payment documents upfront, and collect W-9 or W-8BEN before paying contractors.

A good stack is simple: one core recordkeeping layer, plus specialist support where the risk is real. The next section turns that into a staged model so you can build only what your business needs now. If you want a step-by-step walkthrough, see Best Accounting Software for Small Agencies That Protects Cashflow. For a practical next step, try the free invoice generator.

Why Your "Startup" Isn't a Startup (And Why That's Your Superpower)#

If you invoice clients and fund growth from cash flow, you are operating a different model than a venture-backed startup. That is why many startup accounting-firm lists can feel misaligned, even when the firms are credible.

The gap is operational. Venture-oriented guidance is built for investor readiness: clean books, familiar software, and financials that stand up during diligence. Your baseline is usually different: payments arriving on time, monthly reconciliations, a consistent month-end close, and clear ownership of compliance tasks.

| Decision dimension | Venture-backed company | Cashflow-funded solo founder or small remote team |

|---|---|---|

| Payment reliability | Important, but funding can buffer short gaps | Core constraint because client payments fund operations |

| Compliance ownership | Split across finance staff and advisors | Usually sits with you unless explicitly assigned |

| Reporting needs | Investor-facing reporting and diligence readiness | Internal cash visibility, tax prep support, and clean monthly records |

| Advisor fit | Startup specialists, controller support, fractional CFO discussions | Lean bookkeeping plus targeted specialist help when specific risk appears |

When Kruze Consulting or Pilot come up, they are usually discussed in that venture-focused context. In practice, that can mean service expectations shaped around fundraising and investor-facing reporting. Useful if you are raising capital; less useful if your immediate needs are dependable bookkeeping, payment visibility, and targeted help when a tax or compliance issue appears.

Use this self-check: if no one is asking for investor-ready reporting, do not buy an investor-ready finance function by default. Keep the core controls first: reconcile accounts monthly and close the books consistently.

Three signs you are in a different category#

- Cashflow-first business

If delayed invoices or held payments affect your month, prioritize collections, reconciliations, and margin visibility.

- Founder-owned compliance

If you do not have an in-house finance team, unassigned tasks become your responsibility, and scope gaps can create blind spots.

- Selective senior finance needs

Bring in controller, CPA, or fractional CFO support for specific decisions. Revenue-based trigger points appear in some commentary, but they are not universal rules.

The practical consequence is straightforward: the wrong label leads to unnecessary spend and missed operational risks. Your advantage is control. You can choose systems and specialists by risk profile, margin protection, and cash flow stability. That is why the next section shifts from firm-first thinking to a staged stack. Related: The Best Accounting and Tax Advisors for US Expats.

Stage 1: The Foundation - Bulletproof Your Business-of-One#

At Stage 1, your goal is a simple risk-control stack: you run daily bookkeeping controls, and a specialist handles periodic tax and threshold-sensitive review. That gives you cleaner invoicing, fewer avoidable payment disputes, and less compliance stress when deadlines arrive.

Keep the boundary clear. You own the repeatable transaction work: invoices, payment matching, expense logging, monthly reconciliations, and document storage. Your specialist owns periodic filing positions, jurisdiction-specific interpretation, and any rule tied to a legal trigger or verified threshold. When these roles blur, cleanup work usually replaces strategy work.

| Stage 1 risk | Control in your stack | Protection outcome |

|---|---|---|

| Client challenges an invoice as incomplete or incorrect | Standard invoice packet: signed scope, approved changes, invoice, and proof of delivery stored together | Faster dispute handling and fewer avoidable payment delays |

| Cash appears healthy but records are inaccurate | Reconcile every bank, card, and payment account monthly, then run a simple month-end close | Cleaner books and earlier detection of missing income, duplicate expenses, or unreconciled transfers |

| A filing/reporting trigger is missed | Maintain a running tracker for travel days, account activity, and cross-border exposure; review against the verified threshold or rule before filing decisions | Lower risk of discovering filing issues at year-end |

| Tax prep stalls because records are incomplete | Keep a monthly evidence pack: invoices, receipts, statements, contracts, and owner draws/distributions log | Faster tax prep with less deadline back-and-forth |

Use this checklist to implement Stage 1 without overbuying services:

- Name your top three failure scenarios.

Focus on the operational risks you actually face, such as unpaid invoices, unreconciled accounts, or uncertainty around a filing trigger.

- Map each risk to one control.

Define one owner and one document trail per risk so the control is testable, not aspirational.

- Assign owners now.

You own weekly controls; your specialist owns periodic review and threshold-sensitive interpretation.

- Set the review cadence.

Close monthly, and run specialist review at least annually, then tighten cadence when complexity changes (new country, new accounts, or approaching a verified filing trigger or legal threshold).

Once this foundation is steady, Stage 2 adds people, payroll, and contractor controls on top of it. For a deeper operating playbook, see How to Manage Bookkeeping for Your Freelance Business.

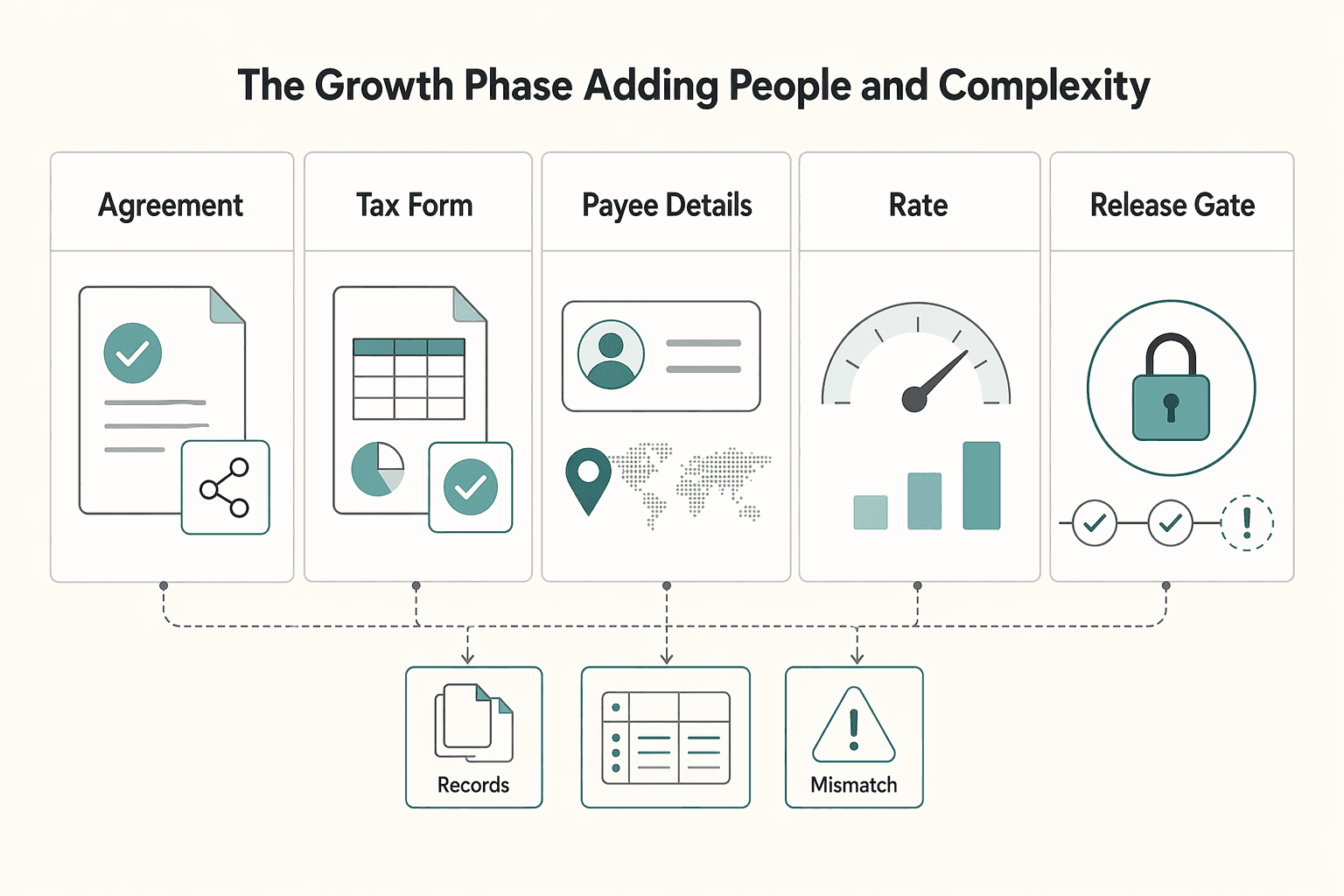

Stage 2: The Growth Phase - Adding People and Complexity#

Once your month-end close is stable, the main risk shifts to team operations: payment errors, onboarding gaps, and margin drift. Use a three-part stack to keep cashflow reliable: your Core OS as source of truth, the right payment platform for your team geography, and advisor time focused on planning instead of cleanup.

| Checklist item | Requirement | Timing |

|---|---|---|

| Agreement | Signed agreement | Before first payment |

| Tax form | Correct tax form (W-9 or W-8BEN) | Before first payment |

| Payee details | Verified payee details | Before first payment |

| Rate | Agreed rate | Before first payment |

| Approval | Approval record | Before first payment |

| Area | Manual ops | Systemized ops |

|---|---|---|

| Payment errors | Ad hoc transfers, late exception discovery, inconsistent records | Separate payout flow, platform records, and routine reconciliation to catch exceptions early |

| Contractor onboarding quality | Agreements or tax forms collected after work starts or after first payment | Standard onboarding checklist completed before first payment, with documents stored together |

| Reporting clarity | Revenue, cards, payouts, and spreadsheets do not align | Accounts synced in one workflow, including payroll and spending cards, with recurring monthly statements |

| Profitability forecast | Cash-balance guesswork | Repeatable project-margin review and cleaner inputs for budgets and forecasts |

Keep your Core OS (Gruv or your equivalent) as the source of truth for invoices, incoming funds, project costs, and reconciled payouts. Then run this sequence each cycle:

- Separate operating cash from payout cash.

- Review project margin on a fixed cadence (revenue minus contractor cost and direct delivery expense).

- Enforce a contractor onboarding checklist before first payment: signed agreement, correct tax form (W-9 or W-8BEN), verified payee details, agreed rate, and approval record.

Choose payment tooling based on worker geography, not familiarity. For mostly domestic teams, a local payroll/contractor tool like Gusto may be enough. For distributed teams, use a global payroll and HR platform like Deel, which states support for worker types in 120+ countries.

Use advisor time for decisions, not reconstruction. Bring reconciled books, monthly statements, and your margin review so conversations stay on budgets, forecasts, and higher-leverage tax planning, including whether to evaluate an S-Corp election. If any filing, election, or reporting duty depends on a legal threshold, document the verified trigger before making the decision.

If this system is running but you still need dedicated ownership of reporting quality and forward planning, that is your signal you are nearing Stage 3.

Stage 3: The Agency - When a Full-Service Firm Makes Sense#

Move to a full-service firm when decisions are moving faster than your visibility and controls, not as a status upgrade. If pricing, hiring, or service changes are happening without reliable cash, margin, and close data, this is usually the point where outside support helps.

Your Stage 2 stack stays in place. Your core platform remains the operating data source, and the firm takes on formal accounting execution and strategic finance support on top of that.

Readiness is about complexity, not status#

The trigger is rising complexity: more transaction volume, more exceptions, and heavier reporting/compliance work. Do not force this on a fixed timeline. Use readiness criteria instead:

| Readiness criterion | What should be true |

|---|---|

| Clean data handoff | You can hand over a clean reconciled-data window that your firm has confirmed is sufficient |

| Records current | Bank, card, payroll, and payout records are organized and current |

| Support traceable | Payment approvals and contractor-cost support are traceable |

| Exceptions limited | Open exceptions are limited and clearly documented |

If records are still unstable, outsourcing can turn into cleanup-heavy work before you get much strategic value.

Keep ownership explicit to prevent scope creep#

Define ownership before kickoff so work is not duplicated.

| Workstream | Primary owner | Handoff inputs | Expected outputs |

|---|---|---|---|

| Operating data capture | You (core platform) | Invoices, revenue detail, project costs, payout activity | Current source data and usable cash/margin visibility |

| Formal bookkeeping and close | Firm | Synced financial activity, statements, chart of accounts, prior reports | Reconciliations, closed books, reporting package |

| Payment operations execution | You (payment tools) | Approved rates, signed onboarding docs, verified payee details, approval records | Completed payments and exception logs |

| Planning and finance review | Firm (with your input) | Clean books plus pricing/hiring assumptions | Forecasts, budgets, and decision support |

If both sides are categorizing transactions or both assume the other owns cross-border workflow checks, costs rise and answers arrive late.

Select and onboard in a narrow sequence#

- Define required services

Decide whether you need outsourced bookkeeping, broader finance/accounting outsourcing, or recurring fractional CFO support.

- Pre-package clean records

Prepare reconciled statements, prior reports, core ledgers, and approval records before onboarding.

- Confirm tool and workflow fit

Validate support for your payment stack, cross-border workflows, and reconciliation cadence (weekly vs monthly) before signing.

- Set diligence, pricing, and review cadence

Use directories to filter by budget, services, industry, and location; verify credibility checks and reviews; then lock reporting dates and strategic review cadence in writing. Treat example price points as examples only, and plan for scope-based cost expansion.

Proceed now if you can hand off clean data and need ongoing finance decision support. Stay in Stage 2 longer if reconciliation is still late, onboarding documents are inconsistent, or exceptions dominate your monthly close.

You might also find this useful: The Best Venture Capital Firms for SaaS Startups in India.

Your First Step: Build Your Foundation, Not Hire a Firm#

Start by building a reliable finance foundation, then hire a specialized CPA when complexity starts creating repeat exceptions you cannot resolve quickly.

| Choice | Control | Risk visibility | Response speed | Cost predictability |

|---|---|---|---|---|

| Foundation stack now | Higher, because you own the records and checks | Better day-to-day visibility when tracking is consistent | Faster, because you can resolve issues in the same cycle | Usually clearer, because routine work and advisory work stay separated |

| Hire firm now | Lower at first, because the firm depends on your inputs | Weaker if records and evidence are incomplete | Slower when questions require missing documents | Less predictable if cleanup and catch-up work appears |

Use this model: technology for daily execution, expert support for strategy and filing.

- Own daily recordkeeping first

Start with bookkeeping, since accurate bookkeeping and reporting are the foundation for informed decisions. If your setup is still simple, cash basis accounting can be a practical starting method because it records income and expenses as they occur.

- Track risk signals continuously

Keep your own logs for residency days, foreign accounts, and invoice compliance checks. When a legal limit applies, record the verified threshold beside the relevant log before relying on it.

- Keep documents audit-ready

Maintain one evidence pack with statements, invoices, receipts, approved payments, and tax forms collected before payment (including W-9 or W-8BEN where relevant). This keeps handoffs clean when you need outside help.

- Add a specialized CPA at a complexity trigger

Bring in specialized support when you move into multi-country operations, contractor expansion, or recurring compliance exceptions. Evaluate firms on industry expertise, technology integration, communication style, and pricing structure, not price alone.

This week, run this sequence: pick your bookkeeping method, start your residency-day log, create a foreign-account review list with a field for the verified threshold, and set up a shared evidence folder. After two clean cycles, start CPA conversations.

We covered this in detail in Best Banking for US Startups Without Payroll Surprises.

Frequently Asked Questions

Do you need a platform, a CPA, or both?

Many teams need both over time, just not at the same time or in the same scope. A platform handles ongoing record capture and visibility, while a CPA handles filing, interpretation, and advice. If you have more complex operations, keep the platform as your source of truth and bring the CPA clean exports, statements, and account records.

What does bookkeeping handle, and when is that enough?

Bookkeeping records what happened: bank activity, card charges, payroll entries, contractor payments, and reconciliations. It is enough when your main problem is late books or an unclear cash position, not tax strategy or forecasting. Your input is the raw evidence pack, including statements, invoices, receipts, approved payments, and required tax documents.

What does accounting or a CPA handle that a bookkeeper does not?

Accounting turns records into financial statements, tax-ready reports, and compliance decisions. You need this when you are filing returns, dealing with entity questions, or preparing for more formal diligence. If you plan to raise Series A or B, GAAP compliance becomes a real checkpoint, not a nice extra. Your input is a closed set of books plus notes on unusual items and owner-level transactions.

When do you actually need a fractional CFO?

You need one when historical reports stop being enough and you need forward-looking decisions, such as burn rate and runway, hiring timing, pricing changes, or expansion planning. That shift can happen faster than you expect, sometimes within months. Your input is not just clean books, but current assumptions about revenue, staffing, margins, and cash commitments.

Should you limit your search to a local CPA?

Usually no. Most CPA services can be performed remotely today, and limiting yourself to local firms can narrow your options for no real gain. The main exception to check for is an audit or other attest service, where local CPA presence may still matter.

How much should you expect to pay?

Do not anchor on old list prices or roundup articles. Ask for current pricing on bookkeeping, annual tax work, cleanup, and advisory hours, and get any upcharges spelled out in writing before you sign. A practical red flag is hidden fees outside advertised monthly pricing, so ask what is included, what triggers extra billing, and who approves it.

How do you check whether an advisor can handle a remote or cross-border business?

Run three checks before hiring: confirm which services they can deliver remotely, verify they have experience with your specific needs, and ask how data will move from your core systems each month. During onboarding, verify whether they can connect to your payroll, expense, and cap table tools, with examples like Gusto or Rippling for payroll, Ramp or Brex for expenses, and Carta for cap table data. If the answer is manual, ask what the monthly evidence pack must include so nothing slips.

What is the biggest onboarding failure mode?

Role confusion. Finance titles are often used interchangeably, so write down who owns transaction coding, month-end close, tax filing, and planning before kickoff. If you and the advisor both think the other side is checking a key compliance task, you have a real risk, not just an admin issue.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 3 external sources outside the trusted-domain allowlist.

- acquisition.gov/sites/default/files/page_file_uploads/far-co...trusted

- dlcp.dc.gov/sites/default/files/dc/sites/DLCP/publicatio...trusted

- ics.uci.edu/~dmdb/chandra/Enron2.1/words.txttrusted

- sec.gov/rules-regulations/2000/11/revision-commissio...trusted

- snap.berkeley.edu/project/12247973trusted

- alajiangroup.com/5-essential-accounting-tips-for-startup-foun...external

- clutch.co/accountingexternal

- cpaccounting.io/best-accounting-firms-startupsexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Hiring a Subcontractor for the First Time Without Costly Surprises

**Start with a risk-control sequence, not an ad hoc handoff.** As the Contractor, your goal is simple: deliver cleanly, control scope, and release payment only when the work and file are complete.

Freelance Bookkeeping for Faster, Safer Client Payments

Control over cash starts with records you trust. When entries are current, categorized, and easy to trace, you spot risk earlier and make calmer decisions about follow-up, spending, and month close.

Best Accounting and Tax Advisors for U.S. Expats: Pick the Right Support Level

**Pick the support level that matches your compliance surface area, then evaluate providers on written scope and form coverage.** The common failure mode for most U.S. expats is not "forgetting to file." It is hiring the wrong help model, under-scoping what you actually need, and finding the gap when IRS filings and related reporting obligations hit the critical path. You run a business-of-one, and your tax workflow is part of the system.