Quick Answer

Score each corridor first, then approve only markets with verified operating evidence. Treat Wise pricing details as inputs, not assumptions: fees vary by currency, transfer discounts start after 25,000 USD, and discount eligibility resets on the first of the month. Treat PayPal pages scoped to US-resident accounts as out of scope for non-US corridors until local-market artifacts are attached. Keep AML, KYC, KYB, and VAT items marked unknown until mapped, and require pilot payouts that show status, failures, and reconciliation outputs before scale.

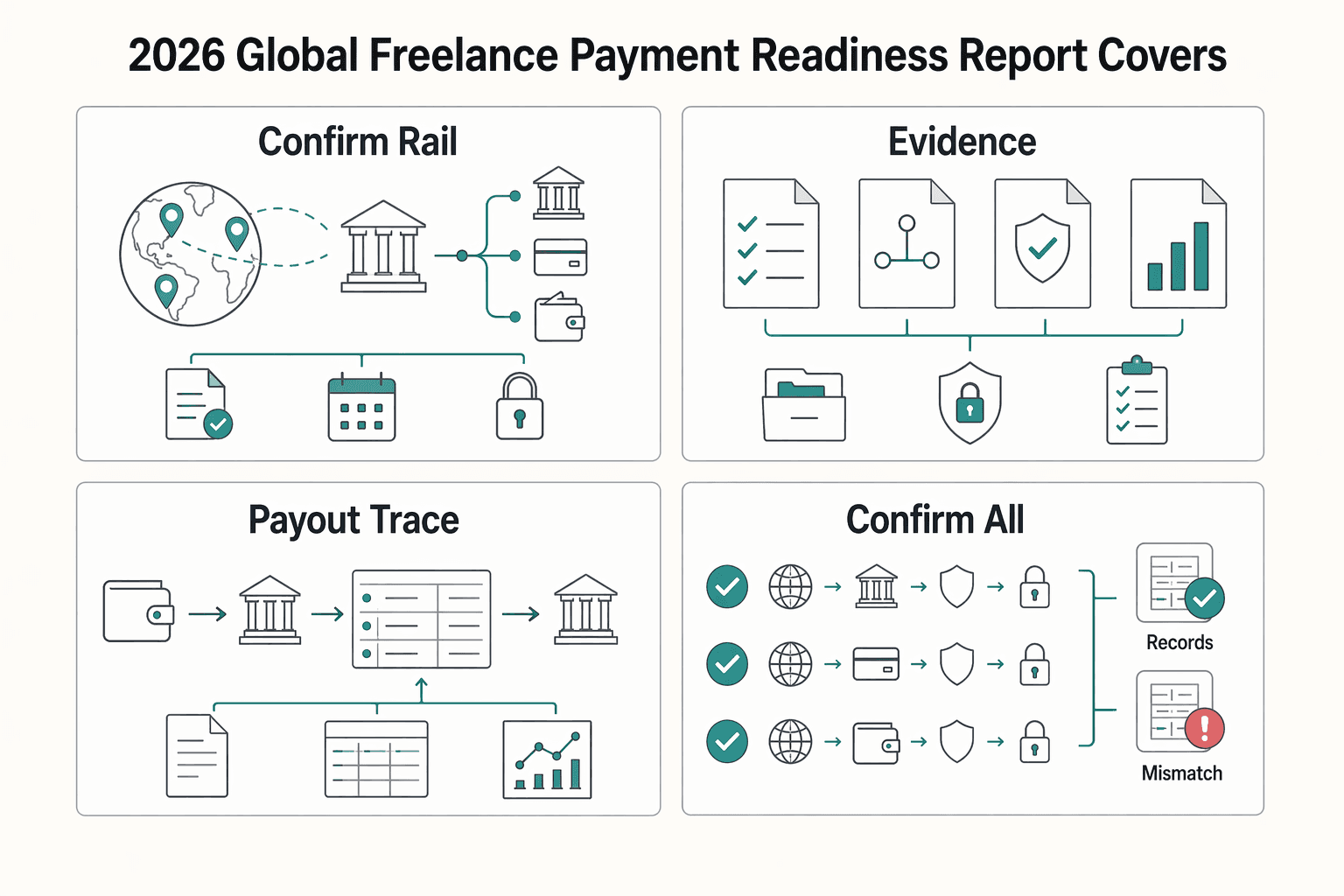

What This 2026 Global Freelance Payment Readiness Report Covers#

Use this report as a launch decision map, not a generic freelancer payment guide. If a country looks attractive on nominal fees but you cannot show how the payout rail, compliance checks, and KYC reviews will work in production, it belongs in a later tier.

Cross-border payout decisions can fail when teams optimize one variable at a time. The cheapest path is not always the fastest to launch, and the fastest path is not always the easiest to defend under transparency, reporting, and tax-compliance requirements. In 2026, workers expect quick access to earnings and have little tolerance for delays, but speed alone is not enough if verification and compliance handling are weak.

Payment method choice changes freelancer net pay after fees and conversion costs. In one 2026 comparison, at a $60,000 annual billing level, the gap between the cheapest and most expensive international methods could exceed $1,500 per year. Treat that as a decision signal, not a fixed market truth, and recheck current provider pricing and country availability before you commit product or go-to-market resources.

This report helps you make that call with clear rollout tiers, readiness signals, and evidence checkpoints. The goal is not a single global ranking. It is a practical view of where rates, rails, and compliance friction support a clean launch, where tighter controls are needed, and where the evidence is still too thin to move quickly.

Use these operational checkpoints before launch:

- Confirm the rail is actually available for your corridor, not just marketed as global.

- Confirm which payer and payee documents and reviews are triggered.

- Confirm finance can trace payout flow from approval to settlement, including holds and failures.

- Confirm all of the above against current provider terms, sample transaction results, and named owners.

Country-specific compliance changes should also affect sequencing. EasyStaff notes that in Spain, from 2026, any payment needs to be reported and the prior €3,000 threshold is abolished. Details like that can turn a market that looks simple on paper into a controls-first rollout.

What this report measures and what it does not#

This report measures launch readiness by corridor, not by country stereotype. Here, a payment rail is the money path in a specific corridor, such as a bank wire, Wise transfer, PayPal route, or another supported method. Readiness means both rail viability and your ability to run the operational work around it.

This report does not directly define AML, KYC, KYB, VAT validation, or local reporting rules, so treat those checks as unknown until you verify them separately.

What we can measure with higher confidence is narrower than many "global" comparisons imply. That includes provider-published pricing rules, thresholds, scoping notes, and disclosure artifacts. One provider states pricing is pay-as-you-use, fees vary by currency, and transfer discounts start from 25,000 USD cumulative volume. It also links pricing in a regulator-standardized format. PayPal's consumer fee page is explicit that listed rates apply to US-resident accounts, with domestic and international classification based on whether the parties are in the same market.

What this report does not claim matters just as much. It does not provide one unified, auditable 50-country dataset. When a source does not provide enough methodology detail for a country-level operational claim, this report marks the answer unknown rather than filling in the gap.

Use these confidence labels as you read:

- Hard data: directly supported by published provider terms, thresholds, or scoped definitions.

- Synthesized estimate: directional synthesis across sources with known gaps.

- Unknown: missing methodology detail, corridor scope, or evidence strong enough for launch decisions.

Keep one red flag in view: listed platform fees are not always the full cost picture. PayPal notes that bank or card-issuer charges may still apply, so fee comparisons without real transaction checks can understate freelancer net-pay loss.

For a step-by-step walkthrough, see Average Freelance Rates by Country and Profession in 2026.

How to score country readiness before you commit budget#

Only score country readiness when you can show a usable rail, a realistic cost profile, and the operating controls to handle compliance and payout failures. Use a 100-point model across five factors, and treat unknowns as a penalty, not a neutral value. For this report, the rule is simple: high demand should not override low evidence quality.

| Factor | Weight | Scoring note |

|---|---|---|

| Rail coverage | 30 | Count only rails you can verify for the target corridor |

| Cost predictability | 20 | Prefer current, scoped pricing artifacts over generic fee claims |

| Settlement reliability | 20 | Base this on real pilot payouts and operational visibility when available; otherwise mark it as unknown |

| Compliance burden | 20 | Score AML, KYC, KYB, VAT validation, and review workload when country-level inputs are available; otherwise mark it as unknown |

| Payout failure recovery | 10 | Confirm your team can detect failures, explain causes, and reroute or refund cleanly; if not evidenced, mark it as unknown |

Standardize each country card before comparing markets#

Use the same fields for every country so your comparisons stay consistent. That makes unknowns visible instead of letting them hide inside narrative notes.

| Country record | Primary rail options | AML KYC KYB burden | VAT validation impact | Evidence note | Confidence level |

|---|---|---|---|---|---|

| Country A with direct provider artifacts | Wise, wire | Not yet mapped | Not yet mapped | Pricing captured from the current pricing page and regulator standardized format; fee varies by currency and volume discounts start at 25,000 USD | Hard data for pricing mechanics, unknown for compliance |

| Country B where PayPal evidence is out of scope | PayPal, wire | Not yet mapped | Not yet mapped | US-resident PayPal fee page is not evidence for a non-US market; use the relevant market page before scoring | Unknown until market-scoped evidence is added |

| Country C with demand signal but thin payout evidence | Wise, PayPal, wire all unverified | Not yet mapped | Not yet mapped | No current provider artifact, no pilot payout results, no documented fallback route | Unknown |

Capture baseline cost mechanics in each card so "cheap" does not hide the real cost structure. At minimum, record the published fee logic, volume conditions, and any setup or receiving charges that affect the corridor.

- Wise states upfront pricing, uses the live mid-market rate, and says the fee varies by currency.

- Volume discounts start at 25,000 USD, so effective cost depends on volume.

- Wise Business includes a 31 USD one-time setup cost.

- It also publishes fixed receiving fees such as 6.11 USD for USD wire/Swift, 2.16 GBP for GBP Swift, and 2.39 EUR for EUR Swift.

- PayPal's cited consumer fee page is explicitly scoped to US resident accounts, and its domestic versus international distinction depends on whether parties are in the same market.

- PayPal also notes fee changes through policy updates, so periodic revalidation is required. The cited page shows Last Updated: February 19, 2026.

Use a controls-first tier for risky readiness profiles#

If a country has high demand but low confidence and unresolved compliance burden, put it in a controls-first tier instead of launching it now.

That means limited pilot volume, named approvers, documented primary and fallback rails, and a written exception path for payout failures before broad rollout. This keeps budget from moving ahead of evidence.

Use one final gate before approval: require each country owner to attach the exact provider artifact used for pricing, confirm the market scope, and explicitly mark unmapped areas as unknown.

With the scoring model in place, the next step is narrower and more practical: which rails can you actually defend today? For related controls, see 8 Resilient Compliance Controls for Payment Platforms in 2026.

Which payment rails are actually viable by market#

Viability should be evidence-led, not preference-led. Only one rail has concrete, market-usable pricing artifacts here, so treat Payoneer, PayPal, and generic bank-wire assumptions as unverified until you attach corridor-specific proof.

What you can defend now#

| Market cluster | Rails you can defend now | Fee structure evidence | Settlement window evidence | Return/failure behavior | Coverage limit note |

|---|---|---|---|---|---|

| Markets with a current Wise artifact for the exact product and corridor | Wise is the only rail with concrete pricing artifacts in this section; bank wire fallback only if separately verified | The provider describes usage-based pricing with no subscription, lists send and conversion pricing starting at From 0.57%, states use of the mid-market rate, and shows send-volume discounts from 25,000 USD with a reset cycle of Resets on the first. It also links fee details in a regulator-standardized format. Wise Business also references a 31 USD one-time setup cost. | Unknown from provided excerpts | Unknown from provided excerpts | Product context differs: receiving details in 25 currencies in personal pricing context versus 24 currencies in business pricing context |

| Markets where Payoneer or PayPal are proposed without market-scoped artifacts | Candidate rails only, not approved rails yet | Unknown in this section | Unknown | Unknown | Unknown until local pricing and terms artifacts are attached and scoped |

| Markets where bank transfer is the likely fallback path | Bank wire fallback can be considered; Wise only where corridor support is proven | No generic bank-wire benchmark is supported here. The concrete wire figure in scope is the provider's 6.11 USD fixed fee for receiving USD wire/Swift on its side. | Unknown | Unknown | Unknown |

Sparse but verified is better than detailed but ungrounded.

Decision logic for rollout#

If reliability and reconciliation are the priority, prefer the rail where you can verify fee mechanics and operational status outputs from pilot payouts. If reach is the priority, keep other rails in candidate status and move them to fallback only after you verify market-scoped coverage and pricing artifacts.

Before you mark any rail viable in a market, require:

- A current pricing page or contract artifact

- A product-scoped coverage statement

- Pilot payout outputs that show status and failure handling

Don't let headline pricing hide operating cost#

Use the non-discounted view as your baseline unless the corridor reliably clears 25,000 USD in monthly volume, because this discount cycle resets monthly.

Also model downstream access costs where relevant. Card pricing notes 2 free withdrawals each month, then 1.5 USD per withdrawal, plus 2% on amounts over 100 USD.

Direct bank transfer vs platform-mediated payout#

Treat these as separate operating paths and validate both with pilot evidence before you scale. If payout delays or dispute handling differ, keep route-specific exception handling so support and finance can reconcile outcomes without guessing.

Where stablecoin may fit#

This section does not provide enough evidence to score stablecoin pricing, coverage, or failure behavior, so do not treat it as an approved default rail here.

Once rail viability is clear, reassess adjacent constraints, including compliance operations, before you scale.

How compliance gates change launch speed and operating cost#

VAT operating design can slow launch and raise operating cost. For EU cross-border activity, the highest-confidence gates here are OSS setup choices, return cadence, recordkeeping duties, and the use of CBR for complex cases.

Map the VAT gate before you call a market launchable#

| VAT control area | Decision to make before launch | Why it affects speed/cost |

|---|---|---|

| OSS eligibility and scope | Whether your activity fits an OSS scheme and which supplies will be reported through it | If you opt into a scheme, you must declare all supplies that fall under that scheme through OSS returns |

| Member State of identification | Which single Member State will own your OSS registration | This choice sets operating ownership, and in some fixed-establishment cases can bind you for the calendar year plus the next two calendar years |

| Filing cadence | Which OSS scheme applies, Union, non-Union, or import | Returns run quarterly for Union and non-Union and monthly for import, creating recurring finance and ops workload |

| Records and audit readiness | How you will manage required records, invoices, and bad debt relief handling | OSS returns are additional and do not replace the regular VAT return, so compliance workload can increase |

Since 1 July 2021, EU cross-border B2C VAT rules shifted to an EU-wide EUR 10 000 threshold for the referenced supplies. OSS is positioned to reduce red tape, up to 95% in the cited EU framing. That helps, but it does not remove ongoing filing and recordkeeping work.

Use CBR when VAT treatment is ambiguous#

For complex cross-border VAT treatment, use VAT Cross-border Rulings, or CBR, to seek an advance ruling. CBR requests are filed in a participating EU country where the requester is VAT-registered, under that country's ruling conditions.

If policy treatment is unclear for a country or corridor, a conservative internal launch-control choice is to keep onboarding in manual review with auditable approvals until the treatment is stable.

Reviewer checkpoint before corridor go-live#

Use an internal go-live checkpoint across finance, legal, and payments ops before you enable a new-country corridor. This is an internal governance choice, not an OSS or CBR requirement. Confirm that the VAT treatment path is documented, including OSS or CBR where relevant, filing ownership is named, and recordkeeping and audit handling are operational.

The practical takeaway is simple: compliance here is not a one-time setup task. OSS and CBR decisions shape launch sequencing and recurring operating cost after go-live.

For a country-heavy operating model, see Translation and Localization Platform Payments: How to Pay Freelance Linguists in 100+ Countries.

Where payment-delay risk breaks marketplace economics#

Payment-delay risk starts breaking marketplace economics when timing variability widens and you still operate as if payouts are predictable. Use Jobbers and Atradius as directional context only, not as audited delay baselines; country-level rates, medians, or provider-level settlement gaps require separate verification.

Use directional signals, but label confidence clearly#

Focus on spread, not just promised timelines. Invoice approval, provider release, local bank receipt, and freelancer availability can drift apart. When that spread grows, you are managing uncertainty, not just payment processing.

Keep source quality explicit in your model:

- At least one Jobbers page is behind a consent wall, which creates a data-collection gap you should account for when using it as a reference.

- No Atradius excerpt text is provided here, so Atradius should not be presented as verified corridor fact in this section.

- Forecast-style narratives should stay labeled as scenario content, not hard operating data.

Variability hurts operations before it shows up cleanly in finance#

As delay volatility rises, operations become harder to manage, but this evidence set does not quantify specific effects on support, churn, advance-funding pressure, or retry volumes. Reliability is a baseline expectation, so repeated inconsistency can damage trust.

There is also a governance risk. Exposure can grow faster than operating controls. A corridor that looked manageable at pilot volume can become unstable at scale if exception handling is still manual.

The operating rule that protects unit economics#

If delay volatility is high, tighten invoice terms and hold back aggressive acquisition targets until payout predictability improves. Before you scale spend, verify promised settlement windows against observed outcomes from live cohorts and separate exceptions by cause so you fix the right failure mode first.

If the observed timing spread is wider than what you promise users, pause growth spend and repair the corridor before scaling. That same discipline matters even more when a rail adds new control requirements instead of removing them.

For a broader view of where payout rails are heading, read Payment Infrastructure Trends 2026: How Marketplace Operators Should Prioritize Real-Time Rails, Stablecoins, BNPL, and Embedded Checkout.

When stablecoin rails help and when they add risk#

Stablecoin rails should be a controlled option, not a launch default. They can reduce friction in some cross-border payout flows because payers can send from a digital wallet. A processor can then either keep the digital asset or convert it into fiat such as USD or EUR. Use that path only when your compliance approach and program controls are already clear.

The usual value proposition is speed and cost, with frequent claims about lower fees and faster cross-border transfers. Treat adoption narratives as demand signals, not proof that your reporting and control model is ready. Even widely cited figures like 962.9 million crypto users by 2026 and 1 in 5 owners expected to use crypto for payments are directional. They are secondary-source numbers, not operating evidence for your program.

What you need to verify first#

Start with conversion design. Confirm whether the processor converts to fiat immediately or whether your flow holds digital assets at any step. That single choice affects downstream treasury and reconciliation handling.

Next, test your recovery path. Confirmed crypto transactions are final. That removes chargeback risk, but it also removes chargeback-based recovery. If your support team cannot execute a clear escalation path for misdirected funds, do not make this a primary rail.

The launch rule#

If fiat off-ramp reliability or reporting treatment is still unclear, keep stablecoin optional and non-primary for launch-tier countries. Use established fiat rails as the default until controlled payouts show the flow is operational. If stablecoin is optional, state that directly and name the fiat fallback rail.

For U.S. exposure, use the Federal Register as a live monitoring checkpoint rather than a one-time lookup. It is an official publication channel for federal regulations and legal notices, and it is updated daily when published.

Whether you use fiat rails only or keep stablecoin as an option, the country owner still needs to prove the launch can be operated end to end.

Related: Handling the FATF Blacklist and Greylist as a Freelancer.

Build the evidence pack each country owner must deliver#

Every country launch needs one auditable pack and one named owner. If that owner cannot show tested rails, executable compliance controls, a clear tax-document path, and a real fallback flow, the country may not be launch-ready.

The pack should answer four operator questions in plain language:

- Which payout rails were actually tested?

- Which compliance checks must pass before first payout?

- How are tax documents collected, validated, and stored?

- What happens when a payout is held, fails, or cannot complete?

What the pack must prove#

For rails, do not accept "provider supports this country" as evidence. Require test records for each proposed route, including returned status signals and documented fallback behavior when the primary rail is unavailable. Finance should be able to trace a sample payout attempt from provider status output to reconciliation export without engineering decoding raw events.

For compliance, map conditions at operator level. Where sanctions exposure exists, capture the exact condition, source, and owner. OFAC guidance around GLs 46B, 51A, and 52 shows the level of precision required: reduced sanctions exposure for non-U.S. persons is conditional, not automatic. One condition references a non-U.S. entity organized under third-country law on or before January 29, 2025. Another references routing into the Foreign Government Deposit Funds. Listed conditions also include screening for blocked-vessel involvement. These are corridor-specific controls, not universal defaults.

For tax documentation, define the workflow, not just the form names. If your program includes W-8, W-9, or Form 1099 handling, document who requests documents, when validation occurs, where records are stored, and who owns reporting decisions in applicable U.S. cases.

Label source quality before people rely on it#

Separate sources into three buckets:

- Institutional primary sources

- Synthesized internal estimates

- Vendor marketing claims

If a source is promotional, label it that way. For example, one payroll source explicitly states its content package is built to compete with other providers. Another vendor positions Contractor Management as lower cost than Contractor of Record while also stating the client retains compliance responsibility. Those inputs can be useful, but they are vendor claims, not neutral benchmarks.

The operational artifacts that prevent fuzzy launches#

Include four working artifacts in every country pack:

- Onboarding checklist with required document states and approval points

- Payout exception taxonomy shared by support, risk, and finance

- Approval matrix for manual release, rail changes, and country activation

- Reconciliation export sample already tested by finance against ledger expectations

Missing any one of these can create conflicting status language across teams and unclear answers for contractors.

The go-live gate#

Make the gate binary: no country launch without documented fallback rail behavior and a named compliance-escalation owner. If you use a vendor, the pack must also state whether you are using Contractor of Record coverage or contractor-management tooling where the client retains compliance responsibility.

The pack is not paperwork for its own sake. It is proof, before launch, that the team can defend the rail choice, explain the document path, and handle the first hard exception without improvising. A strong evidence pack also makes it easier to spot evaluation mistakes that can cause avoidable failures later.

For a related workflow, see Build a Global Contractor Payment Compliance Calendar for Monthly, Quarterly, and Annual Obligations.

If VAT IDs are part of your onboarding controls, run a quick sanity check before approving a country pack: Validate VAT numbers.

Expansion mistakes that create avoidable payout failures#

Avoidable payout failures can start in evaluation, not execution. Teams treat pricing pages and coverage claims as launch evidence when those pages are only one input.

| Mistake | What it misses | Verification |

|---|---|---|

| Headline fee comparisons | Costs can shift with FX treatment, currency pair, sender market, or bank and card-issuer charges | Lock the exact corridor, currency pair, account type, and pricing view used at decision time |

| Uniform provider assumptions | Providers can differ by country, product, corridor, receiving-currency counts, and grouped-market logic | Require corridor-by-corridor verification before rollout decisions |

| No market-specific checkpoints | A launch decision is weak if the team cannot produce the exact fee view used at approval time | Keep a checkpoint record for each in-scope route, including the fee page context and date |

| Posted fees as total cost | Exchange rates or fees charged by a customer's card issuer or bank may still apply | Use a final verification step so lowest posted fee is not treated as lowest all-in cost |

Mistake 1: treating headline fee comparisons as sufficient#

Headline fees are not enough to approve a payout rail. A route can look cheap on paper while costs shift with FX treatment, currency pair, sender market, or bank and card-issuer charges.

One provider, for example, says it uses the live mid-market rate with a separate upfront fee. It also states fees vary by currency, lists pricing from 0.57%, and applies transfer savings only after 25,000 USD for the rest of that month. Eligibility then resets on the first. Your approval record should lock the exact corridor, currency pair, account type, and pricing view used at decision time. If that provider is in scope, save the regulator-standardized fee view. If PayPal is in scope, record the resident market tied to the fee table and the page checkpoint date, which for the US consumer page is February 19, 2026.

Mistake 2: assuming one provider works uniformly across markets#

Do not assume one provider behaves the same across countries, products, and corridors. Even public personal and business pricing pages show different receiving-currency counts, and PayPal defines "international" by different sender and receiver markets while also grouping certain markets for rate calculations.

When you compare providers such as Wise and PayPal, require corridor-by-corridor verification before rollout decisions. "Supported" at a brand level is not the same as "fit" for a specific market pairing.

Mistake 3: launching without market-specific verification checkpoints#

A launch decision is weak if the team cannot produce the exact fee view used for the corridor and resident market at approval time. Keep a checkpoint record for each in-scope route, including the fee page context and date.

For Wise, keep the relevant pricing view, including the regulator-standardized format when used. For PayPal, confirm that the resident market and grouped-market logic match the intended pairing before go-live.

Mistake 4: treating posted platform fees as total payout cost#

Do not assume listed platform fees are the full cost in production. PayPal notes that exchange rates or fees charged by a customer's card issuer or bank may still apply.

Use that as a final verification step so "lowest posted fee" is not treated as "lowest all-in cost." Once those mistakes are out of the way, the rollout plan becomes much easier to manage.

A practical 90-day rollout sequence for the first 10 countries#

Treat this 90-day structure as an internal gating model, not a source-validated launch calendar. For an initial country cohort, the goal is to prove each market is operable before expansion: clear compliance ownership, testable payout behavior, and reconciliation that support and finance can both trust.

| Phase | Focus | Key actions |

|---|---|---|

| Days 1 to 30 | Selection and documentation | Finalize country scoring, assign launch tiers, and set named owners across payments ops, compliance, finance, and legal |

| Days 31 to 60 | Controlled pilot execution | Keep volumes small, validate end-to-end traceability, and test exception paths on primary and fallback rails |

| Days 61 to 90 | Selective expansion | Scale only the countries that passed reliability and compliance checks and move high-friction countries to a controls-first backlog |

Days 1 to 30#

Month one is for selection and documentation. Finalize country scoring, assign launch tiers, and set named owners across payments ops, compliance, finance, and legal.

Baseline mapping should be explicit for each country: expected AML review path, required KYC and KYB data before payout, whether VAT validation affects onboarding or invoicing, and who signs off exceptions. If those fields, owners, and approval paths are not documented, treat that country as not ready for pilot.

Set a recurring compliance checkpoint from day one. KPMG states its indirect-tax update is produced monthly as developments occur. The February 2026 issue tracks digitalized-economy updates, e-invoicing updates, global rate changes, and OECD guidance on Digital Continuous Transactional Reporting, or DCTR, for VAT. Use that as an operating signal to refresh country compliance views monthly, not just at launch.

Days 31 to 60#

Month two is for controlled pilot execution on primary and fallback rails. Keep volumes small enough to inspect every exception path and review every failure record.

Validate end-to-end traceability, not just payout completion. For each pilot payout, confirm you can match the initiation record, provider status updates, internal ledger events, any failure or return code, and the finance export record.

Test exception paths on purpose: missing or mismatched beneficiary details, manual compliance holds, and fallback-rail routing when the primary path fails. If teams cannot answer "where is this payment now?" from aligned records, the country is not ready to scale.

The source material notes US instant rails have expanded through FedNow and RTP. Treat that as rail context, not a readiness shortcut. Faster rails do not reduce launch risk if status visibility and reconciliation are weak.

Days 61 to 90#

Month three is selective expansion. Scale only the countries that passed reliability and compliance checks. Move high-friction countries to a controls-first backlog until the gaps are fixed.

Keep change scope tight. One banking forecast source warns that strategic consolidation and migration need deep consideration. Operationally, do not change countries, rails, and reconciliation formats all at once when you still need clean fault isolation.

Make the stop rule explicit before scaling. If payout failure rate or compliance exception rate breaches your internal threshold for a country, freeze expansion there until the root cause is documented, the fix is implemented, and the fix is retested.

For every country approved after day 60, keep one evidence trail: pilot results, exception log, reconciliation sample, current compliance mapping, and latest policy-review date. The monthly update cadence in the tax/e-invoicing tracker makes that review date a decision control, not an admin detail.

For a broader benchmark on fees, speeds, and rails, read The State of Global Contractor Payments 2026: Fees Speeds Rails and Trends.

Conclusion#

Expansion quality is decided at the country level, not by a single global average for fees or payout speed. A market is launch-ready only when the rail works in practice, the compliance path is clear, and your team can handle payout failures without turning operations into a support queue.

The next step is operational: use a standardized readiness score, require an evidence pack, and launch in tiers with explicit confidence labels. If evidence is hard data, label it as hard data. If it is synthesized, label it as synthesized. If methodology is missing or a benchmark source is unavailable, mark it as unknown.

Keep scoring tied to what actually blocks or unlocks launch:

- Rail coverage and settlement visibility

- Cost predictability

- Compliance handling burden

- Payout failure recovery

Then require a minimum evidence pack per country:

- Exact pricing page and product variant reviewed

- Pull date

- Compliance requirements expected for that market

- Fallback behavior if the primary rail fails

When you compare providers, do not stop at nominal transfer cost. Hidden infrastructure costs can sit in engineering lift, compliance handling, FX overhead, and support burden, especially once error states and reconciliation work begin.

Country specifics will keep breaking global shortcuts. Spain illustrates the point: the 2026 reporting change requires that any payment must be reported, and the prior €3,000 threshold is abolished. Even if that exact rule does not apply elsewhere, it shows why broad regional assumptions can fail when tax and reporting pressure tightens.

The rule is straightforward: when data is weak or compliance is unclear, slow rollout and increase controls. Put that market in a controls-first tier, use tighter review, and scale only after the exception path is proven.

If your first-wave markets are close calls, use a short operator review to pressure-test rail choice, controls, and fallback rules before committing rollout budget: Talk with Gruv.

Frequently Asked Questions

Which payment rails should we evaluate first for global freelancer payouts in 2026?

Start with rails where you can verify corridor-specific pricing and compliance conditions before launch. Wise is the clearest starting point because it publishes detailed pricing and a regulator-standardized pricing document. Confirm comparable data for Payoneer or PayPal directly with each provider before ranking them.

What fee and settlement-time ranges are realistic across wires, Wise, Payoneer, and PayPal?

This section cannot support credible settlement-time ranges across providers. The grounded fee signals here are the published Wise pricing points: sending fees shown from 0.57%, depending on currency, plus fixed receive fees including 6.11 USD for USD wire/Swift, 2.16 GBP for GBP Swift, and 2.39 EUR for EUR Swift. For Payoneer, PayPal, and broader wire fee or settlement-time ranges, use current provider quotes or pilot data.

Which compliance factors most often delay a country launch?

The provided evidence does not support a global ranking of the most common delay factors. It does show a critical sanctions point: OFAC's no-sanctions-risk position for certain non-U.S. person activity is conditional on compliance with GL 46B, 51A, and 52. If transaction terms do not meet those conditions, treat sanctions exposure as unresolved and a potential launch blocker.

How should FATF Blacklist and FATF Greylist status change our market-priority decisions?

There is not enough grounded evidence to set a FATF-based weighting rule for prioritization from public sources alone. Require separate legal and compliance review before committing budget to markets with FATF Blacklist or Greylist status.

Is there one authoritative 50-country benchmark we can trust without normalization?

No. The evidence here does not support a single unified, auditable 50-country benchmark that works without normalization. Even within one provider, product-tier differences matter: one pricing page shows account details to receive in 25 currencies as free, while Wise Business shows account details to receive in 24 currencies with a 31 USD charge.

How do we verify synthesized country payment data before committing go-to-market budget?

Require an evidence pack, not a summary, for each corridor and product tier. Include the exact pricing page, product variant, and regulator-standardized pricing document when available. Also validate volume assumptions against discount mechanics: discounts begin after 25,000 USD in cumulative transfers and reset on the first of the month.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- cncc.edu/documents/25-26/Catalog_2nd_Addendum-Updated...trusted

- congress.gov/event/119th-congress/house-event/LC75335/texttrusted

- congress.gov/event/118th-congress/senate-event/LC73226/texttrusted

- ftc.edu/wp-content/uploads/2025/12/FTC.Catalog.2025-...trusted

- govinfo.gov/content/pkg/FR-2026-03-31/pdf/FR-2026-03-31.pdftrusted

- le.utah.gov/xcode/Title53H/C53H_2025101420251206.pdftrusted

- ofac.treasury.gov/faqs/addedtrusted

- paypal.com/us/digital-wallet/paypal-consumer-feestrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: