Quick Answer

Freelancers should treat FATF blacklist or greylist status as a payment-risk signal, not an automatic ban. Before accepting work, verify the legal payer, confirm which FATF label and provider rules apply to the route, and check whether your cash runway can absorb delays. If the route is workable but slower, tighten milestones and upfront coverage. If payer identity or route support is unclear, pause or decline.

Start Here With the One Outcome That Matters#

Protect payout predictability and cash runway before you accept scope. If you searched fatf blacklist freelancer, start with one operating question: can this client, on these terms, through this payment route, keep next month's cash position safe? FATF is a standards setter, so treat list status as a risk signal, not an automatic verdict on your deal.

A risk signal is a public warning about jurisdiction-level AML/CFT risk, not proof that your specific transaction is improper. Payment friction is the delay caused by holds, pauses, extra checks, or blocked transfers before funds are usable. Cash runway is how long your business can operate before reserves run out if no new cash comes in.

Use this order every time#

Run these checks in sequence before you send a proposal or commit to delivery dates:

| Step | Check | Grounded note |

|---|---|---|

| 1 | Legal payer identity | Verify the entity that will actually pay you, not just the brand name or email contact. |

| 2 | Jurisdiction signal your provider will apply | FATF publishes two public list documents three times a year; record which document applied when you checked. |

| 3 | Terms before work starts | If the route or jurisdiction suggests more review, use more upfront coverage, shorter billing intervals, and less unsecured delivery. |

| 4 | Runway against likely friction | "Invoice paid" is not always "cash available"; provider examples include holds up to 21 days and paused payouts that should unpause within two business days after required tax form submission if nothing else is outstanding. |

| 5 | Evidence log | Keep a short record of what you checked, when you checked it, and what terms changed. |

-

Confirm the legal payer identity. Verify the entity that will actually pay you, not just the brand name or email contact. If the contract names one entity but payment comes from another, treat that as a real risk issue.

-

Check the jurisdiction signal your provider will apply. FATF publishes two public list documents three times a year. As of 13 February 2026, both the high-risk and increased-monitoring statements were current on that date. Record which document applied when you checked. For high-risk jurisdictions, FATF calls for enhanced due diligence and, in serious cases, counter-measures. For increased-monitoring jurisdictions, FATF does not call for blanket enhanced due diligence.

-

Adjust terms before work starts. If the route or jurisdiction suggests more review, tighten terms early: more upfront coverage, shorter billing intervals, and less unsecured delivery.

-

Check runway against likely friction. "Invoice paid" is not always "cash available." PayPal notes funds are usually held for up to 21 days in some cases. Stripe says paused payouts should unpause within two business days after required tax form submission if nothing else is outstanding. These are provider examples, not universal timelines.

-

Log evidence before proceeding. Keep a short record of what you checked, when you checked it, and what terms changed.

Make the go or no-go call early#

| Decision | Use it when | What you do now |

|---|---|---|

| Proceed | Legal payer is clear, details are consistent, and runway can absorb normal processing delays | Send proposal on standard terms and set a recheck at signing |

| Tighten terms | Payer is identifiable, but route, jurisdiction signal, or provider behavior suggests slower access to funds | Increase upfront coverage, shorten billing intervals, limit unsecured delivery |

| Decline or pause | Legal payer is unclear, documents conflict, account details keep changing, or delay risk exceeds your runway tolerance | Stop before scope expands; request clarification or walk away |

This is a risk-based process, not blanket de-risking. FATF explicitly says standards do not envisage automatic cutoffs by customer class. The real red flag is operational: you cannot verify who pays you, cannot confirm which jurisdiction signal your provider will use, or cannot absorb likely delay on current terms.

Keep an evidence log you can actually use#

Once you know the deal is workable, keep a record you can use later if the route is reviewed. For each client or invoice path, capture:

- client trading name and legal payer name

- expected payment route and receiving account or provider profile

- FATF document checked, jurisdiction signal, and check date

- identity-verification documents or data reviewed

- term changes made because of the signal or route

- reviewer name and next recheck trigger

Recheck at the points where friction can appear: before proposal, at contract signature, before major invoices, when payer entity or bank details change, when your provider requests more verification, and whenever FATF issues list updates. Wise notes verification can expand over time, for example identity first and address later. A clean intake does not guarantee a smooth payout path later.

If inconsistencies repeat, pause scope expansion until payer, route, and terms align again. If delays are already showing up as margin drag, read The Silent Profit Killer: How to Stop Margin Erosion in Your Freelance Business.

For a step-by-step walkthrough, see How Global Inflation Changes Freelancer Rates and Real Earnings.

Understand the FATF Terms Before You Change Your Process#

Use precise terms before you tighten payment terms, pause work, or change invoice flow. In practice, FATF labels, provider labels, and legal conclusions are different signals. Mixing them creates avoidable payment friction.

FATF is a standards-setting and assessment body for money laundering, terrorist financing, and proliferation financing. AML/CFT means Anti-Money Laundering / Countering the Financing of Terrorism. Keep this distinction explicit in your file. A FATF listing is a risk signal about a jurisdiction, not a legal determination about your client or invoice. FATF does not handle individual cases or seize funds.

Use one terminology map per client file#

Map each shorthand term to the exact label you checked, then timestamp it. FATF's two public listing documents are issued three times a year, and the February 2026 updates were published on 13 February 2026. Provider wording also changes, so check the current label before you use it.

| Label you may see | What it means operationally | Default action |

|---|---|---|

| FATF High-Risk Jurisdictions subject to a Call for Action | FATF calls for enhanced due diligence and, in the most serious cases, counter-measures | Tighten terms and verify payer and route before work expands |

| FATF Jurisdictions under Increased Monitoring | Jurisdiction is under monitoring; FATF does not call for enhanced due diligence for this category | No automatic change, but check provider behavior and runway |

| Provider restricted or prohibited | Provider-specific operational restriction, not FATF wording | Review provider terms and payment route before invoicing |

| Provider unsupported country or region | Service may be unavailable; transfers may be cancelled or refunded | Pause pending verification or use a different route |

Keep one term end to end#

Use the same label wording across the proposal, contract, invoice notes, and support messages. If one document says "increased monitoring," another says "high-risk list," and a support ticket says "unsupported region," you create unnecessary escalation risk.

Practical rule: name the exact FATF or provider label once, then reuse that exact phrase in every client-facing and internal record for that file.

Let wording trigger action, not emotion#

Use this decision rule:

- No change when the label is only a signal and payer, route, and provider support are clear.

- Tighten terms when the label points to higher review risk or possible slower payout access.

- Pause pending verification when provider wording indicates restriction, unsupported geography, or payer details do not align.

Keep client updates neutral and process-first. Reusable lines:

- "We're adjusting payment terms to match current verification requirements for this payment route."

- "Before we proceed, we need to confirm the legal payer entity and receiving details."

- "This is a payment-process check, not a judgment about your business."

Compare Blacklist and Greylist by Payment Risk and Friction#

Do not price or accept a deal based on the label alone. Before you assume payment behavior, verify three layers: the current FATF label, the local legal rules for your route, and your payment provider's program rules.

Each layer answers a different question. FATF publishes risk signals and standards. Local law determines legal obligations. Provider rules determine whether your route is supported, restricted, or subject to extra review. A FATF label is a risk signal, not a legal conclusion about a specific client or invoice.

| Situation | What to check first | What it changes in your terms | What to do if unclear |

|---|---|---|---|

| FATF high-risk jurisdiction subject to a Call for Action | Current FATF status, exact payer legal entity, and whether your provider supports the route without special approval | Tighten cash-protection terms before scope expands: higher upfront coverage, smaller milestones, and no large unsecured delivery | Pause before proposal or signature until provider support and payer details are confirmed in writing |

| FATF jurisdiction under increased monitoring | Current FATF status, provider support for country and payout method, and whether beneficiary details match the contract | Standard terms can still work when payer identity and route are clear; otherwise tighten milestones | Proceed only after contract, invoice, and receiving details match cleanly |

| Provider restricted, prohibited, or unsupported geography | Provider terms and product eligibility, not FATF wording | Do not rely on normal payout timing or usability | Treat this as a route problem first and switch provider or rail before work starts |

| Status unclear, recently changed, or support answer is vague | Latest FATF page, latest provider policy date, and a written support answer | Do not promise standard billing cadence yet | Plan for the highest-friction path until verified |

Know which layer is driving the decision#

FATF uses stronger language for high-risk jurisdictions: enhanced due diligence and, in the most serious cases, counter-measures. As of 13 February 2026, the high-risk list names DPRK, Iran, and Myanmar. That does not automatically decide your payment outcome, but it is a clear signal to tighten controls before you extend unsecured work.

For increased monitoring, FATF's framing is different. Jurisdictions have committed to address deficiencies within agreed timeframes and are under monitoring. That is not an automatic prohibition. The practical question is narrower: can this payer, on this route, pay with predictable settlement and usable funds?

Recheck at the moments that change your exposure#

Country treatment is not static. FATF listing documents are issued three times a year, and FATF Recommendations are updated over time. Use a recheck cadence that matches your exposure: at proposal, contract signing, and before major invoices.

Log a compact record each time: check date, exact FATF label, provider rule or support reply, payer legal name, and payout method. If payer entity or bank details change after initial checks, rerun the same checks before continuing.

Use a simple commercial decision path#

If the route is supported, the payer is clear, and no live issue appears in local law or provider rules, proceed with standard terms. If support exists but payout predictability is weaker, proceed with tighter upfront protections and shorter billing intervals. If you cannot confirm route support or legal payer identity, decline or redesign the payment path before more work.

This is a commercial tradeoff. Stricter upfront controls may slow kickoff, but they can protect the margin you already won. For the margin logic, see The Silent Profit Killer: How to Stop Margin Erosion in Your Freelance Business.

Related: Best Way for a German Agency to Pay a US-Based Freelancer.

Run a Client Acceptance Check Before You Send a Proposal#

Decide one thing before you quote: proceed, proceed with tighter protections, or pause. If payer identity, route fit, or your delay tolerance is unclear, pause before you send a proposal that assumes normal payment behavior.

Verify in this order#

- Legal payer identity

Confirm the exact legal entity that will sign and pay, using reliable, independent documents or data where possible. If one entity signs but another sends funds, treat the file as unresolved until the legal details and bank details align.

- Current jurisdiction risk signal

Check the latest FATF status for the payer jurisdiction on the live FATF page. FATF issues these documents three times a year. As of 13 February 2026, the Call-for-Action list names DPRK, Iran, and Myanmar.

- Provider program eligibility

Confirm your specific provider path, not just country-level support. Eligibility can vary by product, country, currency, and account setup, including connected-account differences.

- Transaction-path fit

Confirm rail, presentment currency, settlement currency, and beneficiary details before pricing. A supported country can still fail on a specific currency path, and missing originator or beneficiary information can trigger additional checks or review.

Use that sequence every time. FATF is a standards and assessment body, not a case investigator, so your intake decision is operational: can this payer pay you predictably on this route under your terms?

Tie acceptance terms to explicit conditions#

| Signal clarity | Cashflow tolerance | Outcome | Next action | Stop condition |

|---|---|---|---|---|

| High: identity verified, FATF status checked, provider path supported, currency/beneficiary fit confirmed | You can absorb normal admin friction | Green: proceed | Send proposal on standard terms; recheck at contract and before each major invoice | Stop if payer entity, route, or bank details change |

| Mixed: one item pending or route is usable with weaker predictability | Delay risk is near your comfort limit, or exposure could exceed your current internal threshold | Yellow: proceed with tighter protections | Narrow phase-one scope, increase upfront coverage, shorten milestones, avoid large unsecured delivery | Stop if verification stays unresolved or the client pushes weaker terms before route clarity improves |

| Low: identity unclear, provider support vague, or the path does not cleanly fit | Delay would strain cashflow or exposure exceeds your current internal threshold | Red: pause | Do not issue a final proposal or start date; request corrected legal details, an alternate rail, or written provider confirmation | Stop kickoff until missing items are resolved in writing |

Keep negotiation simple: less upfront protection means narrower scope. Broader scope requires stronger payment protection. For the margin impact, see The Silent Profit Killer: How to Stop Margin Erosion in Your Freelance Business.

Keep an evidence log someone else can run with#

For continuity, log fields such as: check date, verifier, payer legal name, payer jurisdiction, FATF label at check time, provider or product reviewed, rail, presentment currency, settlement currency, beneficiary details, source page or support-reply date, outcome color, term changes, and next recheck trigger. Refresh this log at two handoff points: contract signing and before each major invoice.

If you use an internal unsecured-exposure or invoice-size limit, record the verified threshold you used for this file. Do not let a yellow file drift into kickoff. If entities switch, beneficiary details do not match, provider guidance is vague, or required originator or beneficiary information is incomplete, move back to pause, tighten scope, or redesign the payment path before unsecured work starts.

Write Contract Terms That Price in Compliance Friction#

If your intake result is anything other than clean green, price payment uncertainty into the contract from the start. The goal is to reduce unsecured exposure, define clear pause rights, and treat cash as usable only when it is actually available.

Define the terms before you set timing#

Compliance friction: operational drag in cross-border payments when AML/CFT rules or implementation differ across the payment path. Review delay: time when payment is submitted or marked paid but still under provider, bank, or intermediary review. Settled cash: funds that are available for payout, not funds still pending or on hold.

Use FATF status as a risk signal for contract design, not a legal determination about a specific client or invoice. FATF is a standards and assessment body, does not decide individual payment cases, and cannot release held funds. Its two public jurisdiction statements are issued three times a year. As of 13 February 2026, high-risk and increased-monitoring are separate categories: FATF calls for enhanced due diligence for high-risk jurisdictions, while it does not call for automatic enhanced due diligence for increased-monitoring jurisdictions.

Clause patterns with clear "use this when" triggers#

| Clause | Use when | Example wording |

|---|---|---|

| Milestones + upfront coverage | The route is workable but delay would strain cashflow. | You receive delivery in paid phases. I start each next phase only after the prior invoice is paid and funds are available for payout. |

| Verification-linked timing | Review timing is uncertain. | Any timeline tied to payment starts only when payer details are verified and funds are available, not when a transfer is initiated or pending. |

| Payer accuracy | One entity signs and another may pay. | The legal payer details must match the contract, invoice, and payment route before work starts. |

| Screening cooperation | Your provider may request support documents. | If payment review is triggered, you will provide requested records promptly, including contract, invoice, scope, and payer details. |

| Status-shift protection | Route treatment may change mid-project. | If payer identity, route treatment, or payment details change, I may pause new work, adjust milestones, or switch rails before more scope begins. |

- Milestones + upfront coverage

Use this when the route is workable but delay would strain cashflow. Write: You receive delivery in paid phases. I start each next phase only after the prior invoice is paid and funds are available for payout.

- Verification-linked timing

Use this when review timing is uncertain. Write: Any timeline tied to payment starts only when payer details are verified and funds are available, not when a transfer is initiated or pending.

- Payer accuracy

Use this when one entity signs and another may pay. Write: The legal payer details must match the contract, invoice, and payment route before work starts.

- Screening cooperation

Use this when your provider may request support documents. Write: If payment review is triggered, you will provide requested records promptly, including contract, invoice, scope, and payer details.

- Status-shift protection

Use this when route treatment may change mid-project. Write: If payer identity, route treatment, or payment details change, I may pause new work, adjust milestones, or switch rails before more scope begins.

This is margin protection, not admin overhead. Friction and delay add follow-up cost and reduce profit. See The Silent Profit Killer: How to Stop Margin Erosion in Your Freelance Business.

| Risk scenario | Contract move | Tradeoff |

|---|---|---|

| High-risk jurisdiction signal or enhanced review likely | Narrow phase one, stronger prepayment, explicit pause rights | Slower start, smaller initial scope |

| Increased-monitoring signal but route remains supported | Keep the project moving with shorter milestones and stricter payer-data checks | More admin, more frequent invoicing |

| Signing entity, invoice entity, and sending account do not match | Pause kickoff until documents align | Start date may slip |

| Invoice shows paid but funds remain pending or held | Block the next phase until funds are available for payout | Tighter cash timing for the client |

Decision criteria at signing and before new scope#

Tighten terms if payer identity changes after proposal, if signer and payer split without clear documentation, or if bank or beneficiary details arrive late or conflict with prior records. Pause delivery if required records are incomplete, provider guidance is still unresolved, or payment is not yet usable. Decline expansion if earlier invoices are unresolved or the client asks for broader unsecured scope without stronger payment protection.

Mini playbook for phased commitment#

Start small when the route is workable but not fully proven, then expand only after the payment behavior matches the paperwork.

- Phase 1 (commit small): limited scope, paid phase, complete document set (signed contract, scope, invoice, legal payer details, beneficiary details).

- Phase 2 (expand): only after Phase 1 payment behavior is normal and records stay consistent.

- If status shifts: reopen terms before accepting additional unsecured work.

Use this negotiation script: We can start quickly with a smaller paid phase now, or start broader once payer details and payment availability are confirmed. I can do either, but I do not begin broader scope while payment risk is unresolved.

Related reading: A Canadian Freelancer's Guide to Setting Up a US Stripe Account.

Before kickoff, draft terms that match your risk tier so milestone timing, verification dependencies, and scope limits are explicit in writing. Use the Freelance Contract Generator.

Set Up Invoicing and Collection to Prevent Avoidable Holds#

Use one stable payment path per client and count cash as usable only when it is settled in your business bank account. Avoidable holds and returns can happen when identity or destination records drift mid-cycle, or when you act on a paid invoice before payout settlement is complete.

Lock the payment path before the first invoice#

Keep rails, payer details, and payout destination stable through each invoice cycle unless you are correcting a verified error. Late changes can increase return and hold risk, especially on routes already likely to get extra review.

Use this order every time:

- Confirm legal payer name, payer contact, collection route, and your beneficiary details.

- Issue the invoice with matching legal names, a consistent invoice ID format, and a service description aligned to scope.

- Collect on the agreed route only.

- Confirm payment success before moving to payout.

- Initiate payout only to prechecked destination details tied to that client record.

- Count funds as available only when they are settled cash in your business bank account.

Because FATF public jurisdiction statements are updated on a recurring cycle, recheck route risk at signing and again before major invoices, especially if client, sender, or path details changed since intake.

Use payment states that mean one thing#

Use four labels in your tracker, and keep each one exclusive:

| State | Meaning | Handling rule |

|---|---|---|

| Paid invoice | The invoice has transitioned to paid after full payment. | Do not treat as settled cash. |

| Payment confirmed | The payment flow is complete, for example a succeeded payment state. | Keep it exclusive from the other labels. |

| Payout initiated | Funds are allocated to payout but still pending movement or completion. | Do not treat as final availability. |

| Settled cash | Funds are available in your business bank account after settlement. | Count funds as available only at this state. |

Paid invoice means the invoice has transitioned to paid after full payment. Payment confirmed means the payment flow is complete, for example a succeeded payment state. Payout initiated means funds are allocated to payout but still pending movement or completion. Settled cash means funds are available in your business bank account after settlement.

Do not treat these states as interchangeable. Paid invoice is not settled cash, and payout initiated is not final availability. Even a posted payout does not guarantee bank-available cash. At each state change, log the timestamp, owner, pass or fail result, action taken, and next review time.

Run checkpoints and contain failures fast#

Check the same fields before invoice issue, after payment confirmation, and before you treat funds as available for the next unsecured milestone. Review the legal payer name, sender identity if visible, invoice amount and ID, service description, and payout destination details.

| Mismatch type | Immediate containment step | Owner | Resume condition |

|---|---|---|---|

| Contract payer name, invoice payer name, and expected legal payer do not match | Stop invoice issue or the next unsecured milestone; request corrected legal payer details plus a supporting record | You and client | Resume only when contract, invoice, and payer record align exactly |

| Sender identity differs from expected payer or signer | Hold applying funds to the project record; request explanation and supporting documentation | Client first, then you | Resume after sender verification and a check of the relevant provider rule for split-entity or third-party payment |

| Beneficiary name or bank details changed after invoice issue | Freeze payout-detail changes for that invoice cycle; re-verify destination details before any payout attempt | You | Resume after destination details are rechecked against the stored beneficiary record |

| Invoice is paid or payment is confirmed, but payout is initiated, pending, or posted | Do not treat funds as available cash; do not start the next unsecured phase | You | Resume only when funds are settled in your business bank account |

Make pause triggers binary#

Use hard if/then rules, not judgment calls:

- If legal payer identity is unresolved, then do not issue the invoice or start the next unsecured phase.

- If contract, invoice, sender, or beneficiary records drift after invoicing, then pause nonessential work until records match again.

- If the invoice is paid or payment is confirmed but payout is still unsettled, then do not count funds as available and do not expand scope.

- If a payment is pending on a rail where cancellation is unavailable, then contain exposure immediately and wait for a final state before more unsecured delivery.

This is stricter, but cheaper than resolving mismatches after more unsecured work has shipped.

Send a process-first client update#

When a checkpoint fails, send one short update with the required fields:

Invoice ID: Amount: Current invoice state: Current payment state: Current payout state: Pending verification item: Action underway now: Who owns the next step: Next review time: Effect on the next unsecured milestone:

Keep the message factual and state-based. If this friction repeats across clients or rails, tighten billing intervals and review margin impact. See The Silent Profit Killer: How to Stop Margin Erosion in Your Freelance Business.

If crypto is part of your fallback plan for cross-border payments, How to Get Paid in Crypto as a Freelancer (and Manage the Risks) covers the operational and compliance tradeoffs.

Build a Small Evidence Pack for Enhanced Due Diligence Events#

Build a small, invoice-linked evidence pack now so you can answer an enhanced due diligence request quickly instead of reconstructing records under pressure. Treat this as an operational response tool, not legal advice.

An enhanced due diligence event is a higher-risk situation where extra checks are applied. FATF's 13 February 2026 call for action urges enhanced due diligence for high-risk jurisdictions. FATF's 13 February 2026 increased-monitoring statement says it does not call for blanket EDD measures for grey-list jurisdictions. Counterparty identity means verifying the customer with reliable, independent documents or data. Legitimate business purpose means documenting the purpose and intended nature of the business relationship.

Keep one trail per invoice cycle: the legal payer, scope, invoice, payment trail, and delivery proof should all point to the same real business activity.

| Common review question | Document examples to keep ready | Store in | Owner of updates |

|---|---|---|---|

| Who is the counterparty? | Signed contract with legal payer name, onboarding record, and legal-entity document where required (verify the provider and country requirements involved) | Client folder > EDD > Identity | You; update at signing and when payer details change |

| Why is this payment legitimate? | Statement of work or scope summary plus invoice with unique invoice ID, service period, and billed payer name | Project folder > Invoice cycle | You; update before invoice issue |

| Can you link funds to normal business activity? | Recent invoices and matching business bank statements; in some reviews, Wise may request invoices from the last 6 months plus bank statements | Finance folder > Restricted > Source of funds | You or bookkeeper; update monthly |

| Did you deliver the work? | Acceptance email, submitted files, portal export, call summary, or fulfilled purchase order; for PayPal intangible goods, keep compelling evidence of delivery | Project folder > Delivery proof | You; update at each milestone |

Use these binary pause triggers as an internal risk-control policy before each new invoice cycle:

- If counterparty identity is incomplete, pause new billing until completed.

- If invoice linkage to contract and payment records is incomplete, pause new billing until records align.

- If delivery proof is incomplete, pause new billing until proof is filed.

Run this maintenance checklist at the end of each billing cycle:

- Add the final invoice, payment confirmation, and delivery proof to the invoice-cycle folder.

- Confirm legal names, invoice ID, and project reference match across files.

- Version superseded files clearly, for example

v2026-03-26, and archive older copies instead of overwriting. - Check access controls so only current staff or advisers can access full-detail documents.

- Log the last review date and next review date.

If you want this upkeep to stay lightweight, fold it into your recurring finance process using How to Automate Your Freelance Tax Preparation.

If your issue is a specific payment corridor rather than a FATF listing, The Best Way for a UK Freelancer to Get Paid by an Australian Client compares practical options.

Handle Mid-Project List Changes Without Blowing Up Cashflow#

When a mid-project list alert appears, verify it first, then adjust delivery and billing in a fixed order. Do not treat rumors as facts, and do not keep expanding unpaid scope while status is unclear.

A risk signal is a public FATF warning that a jurisdiction may present AML/CFT-related risk. An unverified signal is any claim not yet matched to a dated FATF statement or plenary outcome. A verified change is a jurisdiction-status update explicitly stated in a dated FATF publication, for example the 13 February 2026 statements or the 11-13 February 2026 plenary outcomes. A cashflow-control event is a provider restriction on fund movement, such as paused payouts, account limitation, or a transfer pause.

| Trigger | Temporary operating condition | Client message | Required evidence to resume or scoped exit |

|---|---|---|---|

| News post, chat message, or secondary alert about list movement | Keep work to paid scope or already accepted items only. Do not expand scope. | "We are verifying a jurisdiction-related update against the latest FATF publication before changing project timing." | Latest dated FATF statement or plenary output confirming or disproving the change |

| Verified move to increased monitoring | Recheck payer identity, invoice route, and provider, program, and country requirements. Continue only on terms you can fund if payment timing slips. | "We have confirmed a status update and are rechecking payment-route requirements before the next milestone." | Updated payer record, invoice linkage, and provider-specific requirements verified for the provider, program, and country involved |

| Verified high-risk jurisdiction update | Pause new unsecured work. Tighten milestone release until the payment route is confirmed. | "Because the payment route now requires additional review, the next unpaid milestone starts after required checks are completed." | Confirmed payment channel acceptance, complete counterparty documents, and written agreement on revised timing if needed |

| Provider payout pause, limitation, or transfer hold | Treat funds as not usable cash until restrictions clear, even if receipts continue. Stop work that increases unsecured exposure. | "Payments may still be receivable, but withdrawals are currently restricted, so we are holding the next unpaid deliverable until the account review clears." | Provider notice resolved, payouts restored or transfer released, and requested documents submitted |

Use these checkpoint rules before each major milestone or near-term invoice:

- If your contract includes a compliance or payment-risk pause right, invoke it when a signal is unverified or a cashflow-control event is active.

- If the next invoice is not yet issued, hold it until payer details and route checks match.

- If the invoice is issued but withdrawals are paused, plan delivery as if that invoice is still unpaid.

- If unsecured exposure would increase, pause additional unsecured work until the resume evidence is complete.

That controlled pause can be cheaper than hidden margin erosion.

Use this factual client update template: "We are verifying a dated FATF or provider status change. Until that check is complete, project work is limited to current paid scope. To resume the next milestone, we need the specific document or provider confirmation requested for this route. If that cannot be completed by the agreed date, we will close out delivered scope and reissue timing for remaining work."

Anchor checks to official FATF publications, which are issued three times a year, usually in February, June, and October, instead of relying on social chatter.

Recover Faster From Holds Returns and Rejections#

Treat this as a sorting problem first. If you label the case correctly on day one, your recovery actions get faster and cleaner.

In this workflow, a hold is a temporary restriction where funds are not fully available during review or dispute checks. A return means funds were sent back after the payment did not complete under that rail or program. A rejection means the payment could not be processed and was tagged with a failure reason or code. A prolonged pending review means the provider is still reviewing the transaction. It is not the same as a failed payment.

| Case type | First check | Evidence to gather | Owner | Client update | Resume or escalate condition |

|---|---|---|---|---|---|

| Hold | Open the provider notice or email and confirm whether the hold is on funds, withdrawal, or account review | Transfer ID, status screenshot, invoice, payer legal name, requested documents | Usually you with provider support | "Payment is initiated/received but temporarily unavailable during review. We will resume the next unpaid milestone after release or alternate route confirmation." | Resume when the hold is lifted or an alternate route is confirmed. Escalate when requested documents were submitted and the provider window is exceeded, for example some PayPal withdrawal reviews may run up to 72 hours. |

| Return | Confirm funds were returned and capture the reason | Return reason or code, corrected recipient or bank details, refund confirmation | You and client, based on which record is wrong | "This payment was returned. We are correcting records before reissue." | Retry only after corrections are complete or the refund is confirmed. If the same route returns again, reassess that route and switch paths if needed. |

| Rejection | Capture the exact rejection or failure code before taking action | Failure code, recipient details, account identifiers, provider message | Depends on rail and error source | "The payment was rejected before completion. We are validating the exact failed field or control check." | Correct records first; do not blind-retry. If policy requires cancel or refund instead of resend, follow that path. |

| Prolonged pending review | Check whether more information was requested and when | Case number, request email, submitted documents, timestamps | You first, then client if counterparty documents are needed | "Payment is still under review, not completed. We have submitted/requested the documents needed for release." | Pause new unsecured work if exposure would increase. Escalate when the stated review window or follow-up trigger is exceeded. Verify the exact program window, because examples in Wise docs vary by context, including 2-3 and 5-14 working days. |

Use these decision criteria every time:

- Retry only after you know the exact failure reason.

- Correct names, account details, and invoice linkage before any resend.

- Pause new unsecured work when funds are pending but not usable.

- Reassess a payment path after repeated returns or rejections on the same route.

- If repeats start consuming time, fees, and delivery capacity, treat it as margin erosion, not a one-off issue.

Keep the policy caveat clear. FATF high-risk and increased-monitoring statements, including the 24 October 2025 publications, are risk signals, not a universal recovery playbook. FATF calls for enhanced due diligence for high-risk jurisdictions (and can call for countermeasures in serious cases), while increased-monitoring status does not automatically trigger enhanced due diligence. Apply a risk-based approach rather than blanket cutoffs. Use universal controls first: verify current status, capture the exact reason, preserve evidence, and prevent unsecured exposure from growing. Then hand off to provider, program, country, and rail specifics before you commit timing.

Confirm What Varies by Country and Program Before You Commit#

Treat this as a pre-commit control: a risk signal is not a legal verdict, and not proof that your payment route will clear.

Keep these three checks separate every time:

- Your country legal position: the current local requirement that applies to your transaction type in the relevant jurisdiction.

- Your provider program rules: the current terms and compliance criteria for the exact payment product you plan to use.

- Your transaction path: the actual money route, including payer country, beneficiary country, currency pair, payout method, and intermediary or bank steps.

If any point is not verified, do not guess. Mark the item as unresolved and hold commitment until you confirm the requirement.

| What to verify | Evidence to save | Who confirms it | If signals conflict |

|---|---|---|---|

| Country legal position for this transaction type | Dated note, official page screenshot, adviser email, or internal memo with verification date | You, local counsel, or qualified local adviser | Keep scope narrow and paid while legal interpretation is unresolved; pause expansion until confirmed |

| Provider program rules for the exact payment product | Current terms page PDF or screenshot, support ticket ID, account notice, eligibility page | You and provider support or compliance | If the legal position appears workable but product terms are unclear, switch routes or reduce unsecured work |

| Transaction path acceptance | Test payment result, bank detail check, corridor confirmation, rejection or return messages if any | You, client finance contact, provider, receiving bank where possible | If the path is unstable, change route before adding deliverables |

Run this check at signature and again before any major invoice. Save dated evidence each time.

Use a written commitment policy, adapted to your legal advice and risk tolerance:

- When all three checks are current and consistent, you may consider broader scope.

- When uncertainty remains, consider narrower scope with shorter paid intervals.

- When uncertainty is still material, consider pausing or declining until verification is complete.

That discipline can reduce the chance that uncertainty turns into delays, fees, and rework that compound into margin erosion.

If screening raises a PEP flag alongside country-risk checks, What Is a Politically Exposed Person and How to Decide Next Steps explains what that means and how to handle it.

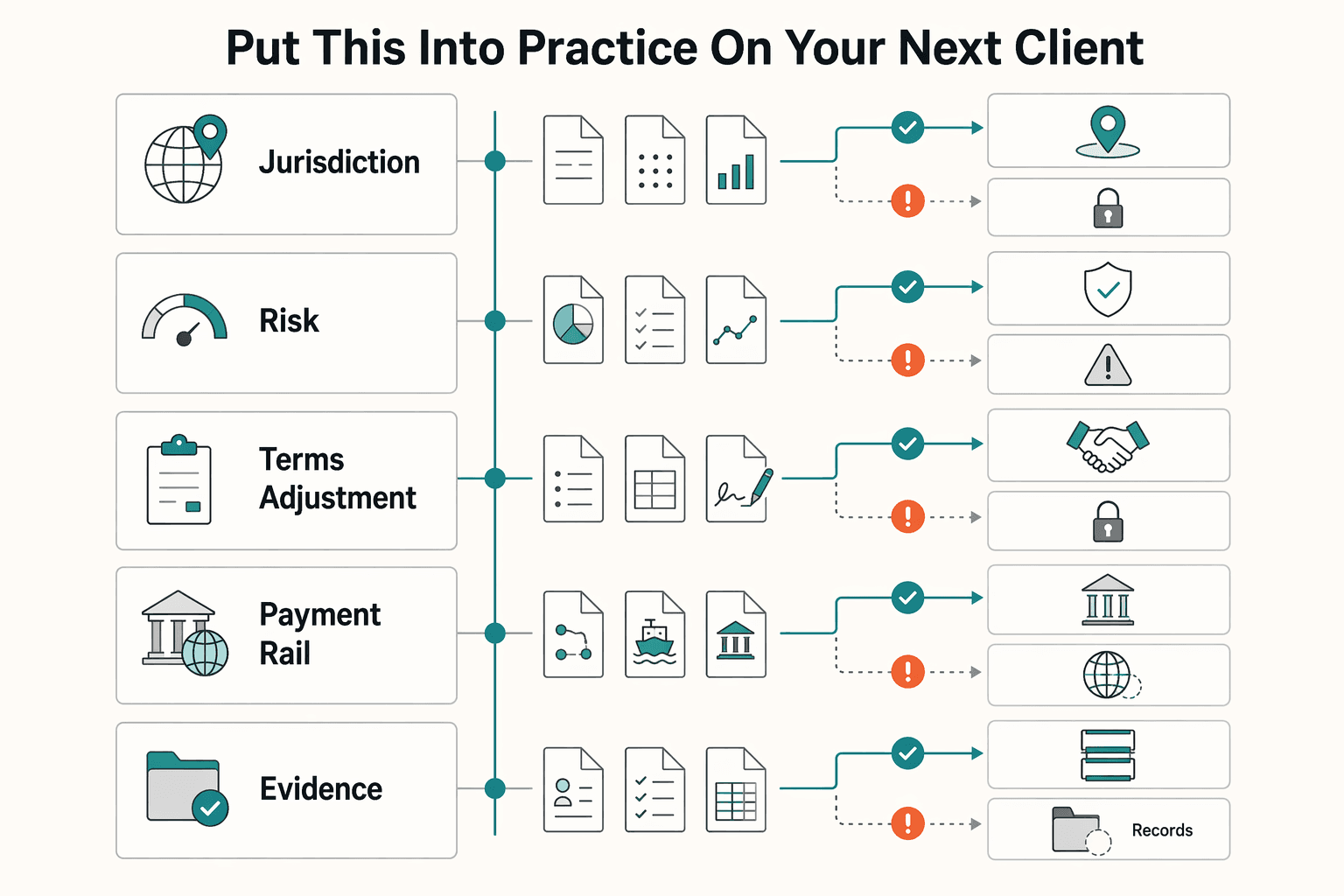

Put This Into Practice on Your Next Client#

Use one repeatable checkpoint before you send a proposal or invoice, and force a branch decision before you commit more unsecured work. Do not rely on static country lists. FATF updates these public documents three times a year, and status can change between cycles.

Run this checklist pre-proposal, at signature, before major invoices, and any time the payer, route, country, or provider program changes.

| Step | What to verify | Why it matters | Decision if unclear | Ownership |

|---|---|---|---|---|

| Jurisdiction check | Confirm client legal country, payer country, beneficiary country, currency, and the FATF statement date you checked. As of 13 February 2026, the call-for-action statement names DPRK, Iran, and Myanmar, and increased monitoring updates also identify Kuwait and Papua New Guinea. | Your risk sits in the full payment route, not a marketing location. FATF status can change, including removals between updates. | Proceed when route and party details are clear and current. Pause unsecured work when party country or payer identity is unclear. Decline until verified when you cannot establish who is paying from where. | Verification |

| Risk tier | Classify the deal by friction risk using list status, inconsistent party details, unusual payer structure, or unclear commercial purpose. | FATF supports a risk-based approach, not blanket de-risking, so your control level should match the actual risk. | Proceed for consistent, low-friction facts. Tighten terms for increased monitoring or unresolved friction. Decline until verified where risk cannot be mitigated case by case. | Verification |

| Terms adjustment | Check that contract protection matches the risk tier: upfront share, billing interval, milestone size, approval language, and stop-work rights. | Unsecured delivery can increase cashflow risk. | Proceed if terms cover exposure. Tighten terms when the route is workable but review risk is higher. Pause unsecured work if the client will not accept protective terms. | Document consistency |

| Payment-rail choice | Confirm the exact provider and program for collection and payout. Stripe features vary by country or region, Wise says unsupported-location use can trigger restrictions, cancellations or refunds, and transfer holds pending review, and PayPal's broad coverage still requires route or program confirmation. | "Available somewhere" does not confirm your exact corridor. | Proceed when corridor and program are confirmed. Tighten terms when only fallback rails are available. Decline until verified when the route is unconfirmed. | Verification |

| Evidence-pack readiness | Confirm proposal, contract, invoice, payer name, bank or wallet details, scope, and delivery records all match; log check date, result, and follow-up point. | Enhanced due diligence is easier when you submit one consistent file set. | Proceed when records match. Pause unsecured work until mismatches are fixed. Decline until verified if basic payer or contracting details are missing. | Document consistency + status log/follow-up |

If you work solo, still keep the ownership split as separate passes: verification, document consistency, then status log or follow-up. If you work with a teammate, assign those three owners explicitly.

Save the FATF statement date, provider program, and fallback route in the client file so you can rerun decisions cleanly when timing or risk signals change. For execution detail, use Set Up Invoicing and Collection to Prevent Avoidable Holds. If review friction is already hurting profitability, read The Silent Profit Killer: How to Stop Margin Erosion in Your Freelance Business.

Final reminder: confirm current country and program support before you rely on any payment route. If a client route still looks uncertain after your checklist, confirm market and program fit before you rely on that payment path. Talk to Gruv.

Frequently Asked Questions

What is the FATF blacklist for freelancers and why does it affect getting paid?

For freelancers, the FATF blacklist refers to High-Risk Jurisdictions subject to a Call for Action. It is a risk signal, not an automatic ban, but it can lead to more bank or provider review before funds are released. If a client, provider, or payout route touches one of these jurisdictions, verify the exact route and save a dated record before proceeding.

What is the practical difference between the FATF blacklist and FATF greylist for invoices and withdrawals?

The practical difference is payment friction. Call-for-action status can mean heavier review, and FATF urges enhanced due diligence and, in serious cases, countermeasures. Increased-monitoring status is different because FATF does not call for blanket enhanced due diligence for that category, so standard terms may still work if payer identity and route are clear.

How often should I recheck High Risk Jurisdictions subject to a Call for Action and Jurisdictions under Increased Monitoring?

Recheck at decision points, not on a vague calendar. FATF issues the two public status documents three times a year, but you should also recheck before proposal, at contract signature, before major invoices, and after payer, route, or provider changes. Save the statement date you used in the client file.

Does FATF listing automatically ban all freelancer payments?

No. FATF listing alone does not decide legality or guarantee a payment outcome. Your real outcome depends on local legal rules, provider program rules, and the exact transaction path.

What should I do before invoicing a client in a greylist jurisdiction?

Only invoice after the route and records fully match. Confirm the exact product and corridor are accepted, then align payer legal identity, country, currency, bank details, and scope across the proposal, contract, and invoice. Build an evidence pack in advance so the agreement, invoice, delivery details, and recent business documents are ready if review is triggered.

What should I do immediately if a payment is held or returned after delivery?

Stop new unsecured work and get the exact hold, return, or rejection reason first. Check for preventable errors such as recipient name or account-detail mismatches, then submit one consistent file set with the contract, invoice, delivery proof, and any requested identity, tax, or source-of-funds documents. Do not treat funds as available until the hold is lifted, the return is resolved, or an alternate route is confirmed.

Watch

How Freelancers Can Handle FATF Risk

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

Educational content only. Not legal, tax, or financial advice.

Related Posts

Stop Freelance Profit Margin Erosion Before It Hits Cashflow

Revenue can hold steady while the business underneath it gets weaker. What comes in matters, but what you keep after the work is delivered is the clearer signal of health.

How to Automate Your Freelance Tax Preparation

**To automate freelance taxes safely, automate the boring mechanics and keep human approval for the decisions that create real compliance risk.** You are the CEO of a business-of-one. Your job is to run a system that stays resilient while your clients, tools, and countries change.

The Best Antivirus and Malware Protection for Freelancers

If you want the best antivirus for freelancers, do not start with feature lists. Start with your work context, choose the right lane, and keep your shortlist small. That is the simplest way to avoid paying for extra admin while still protecting client files and keeping billable work moving.