Quick Answer

Yes, freelance vs contractor vs employee classification should be handled as a two-lens decision, not a contract label choice. Use Internal Revenue Service factors (behavioral control, financial control, relationship of the parties) and then validate with the U.S. Department of Labor employment analysis under the Fair Labor Standards Act. If those reads conflict, escalate before payouts go live and keep a timestamped approval record with the governing facts.

Classify the work before trusting the contract label#

If your team needs a defensible answer on whether a worker should be treated as an independent contractor or an employee, do not start with the label in the contract or onboarding form. Start with the actual working relationship, then test it through both the Internal Revenue Service and U.S. Department of Labor lenses before payouts scale.

Most articles stop at definitions. That is rarely enough for compliance, finance, or legal owners who may later need to explain the decision to an auditor, a worker in dispute, or a regulator. The real question is not what the worker is called in sales, recruiting, or product copy. It is whether the facts support employee status or independent contractor status, and whether you kept enough evidence to show how you reached that conclusion.

The IRS directs businesses to assess worker status through three categories: behavioral control, financial control, and the relationship of the parties. The DOL, through the Fair Labor Standards Act, analyzes whether the worker is an employee or an independent contractor for wage and hour purposes, and employees receive the protections of the FLSA. If your internal review only checks tax onboarding fields and skips the labor side, you can end up with a classification that looks tidy in accounts payable but is weak when challenged.

A useful operating rule: facts beat labels, and documentation beats memory. If a signed agreement says "freelancer" but managers set the schedule, direct the work in detail, and treat the person like part of normal operations, route that case to employee review instead of auto-approving contractor status. At minimum, keep the agreement, the business owner's rationale, the approver's name, and a timestamped record of the facts reviewed before the first production payout.

One early checkpoint matters. The DOL's current regulations discussed in Fact Sheet 13 were effective March 11, 2024, and the agency notes litigation around the rule while also stating it remains in effect for private litigation. So if your policy deck or vendor intake form still relies on stale definitions, update it now.

A repeatable classification process is not just a legal exercise. It is a payout control, an audit trail, and an escalation path you will want in place before volume makes rework expensive. This pairs well with our guide on How to Calculate a Freelance Rate You Can Actually Get Paid On.

At a glance comparison for freelance contractor and employee#

Treat "freelance" as a label, not a legal status. Classify based on relationship facts you can document under both IRS and DOL/FLSA lenses.

| Worker category | Label used in contracts | Legal status signal | Primary test | Tax handling | Labor protections | Escalation trigger | Required internal evidence |

|---|---|---|---|---|---|---|---|

| Freelance | Often written as "freelancer," "consultant," or similar | Terminology only; not a standalone federal status test in the cited IRS/DOL materials | The label alone does not decide status; review IRS factors and DOL/FLSA implications | Not determined by the word "freelance" | Not determined by the word "freelance" | Contract label says freelance, but relationship facts suggest employee-like control or continuity | Signed agreement, scope notes, classification rationale, approver name, timestamp before first payout |

| Independent contractor / self employed individual | Usually "independent contractor" in a services agreement | Possible legal status when facts support that the person is in business for themselves; IRS says such a person is generally self-employed | IRS: behavioral control, financial control, relationship of the parties; DOL/FLSA review may still be needed | IRS says businesses generally do not have to withhold or pay taxes on payments to independent contractors | DOL Fact Sheet 13 says independent contractors are in business for themselves and are not covered by the FLSA | Facts begin to show company control of work, control of business aspects, employee-type benefits, or continuity | Executed services agreement, work scope, payment terms/invoices, evidence of business independence, control analysis notes, approval record |

| Employee | Offer letter, employment agreement, payroll onboarding documents | Employee status is more likely where business control and relationship facts support employment | IRS: behavioral control, financial control, relationship of the parties; DOL/FLSA employment analysis also applies | IRS says employers must withhold and deposit income, Social Security, and Medicare taxes, and pay matching Social Security/Medicare plus unemployment tax | DOL says employees receive FLSA protections | Any uncertainty after review, or a worker set up as contractor but managed like staff | Employment terms, payroll setup record, reporting/control notes, benefits/continuity indicators, written determination with approver and date |

The IRS and DOL ask related but different questions, so keep evidence that works for both. A practical control is to keep at least one concrete fact for each IRS category: who controls how work is done, who controls business and financial aspects, and what the contract, benefits, and continuity facts show.

The common failure pattern is stopping at the contract label. If "freelance" is on paper but the relationship facts point another way, escalate before payout activation.

If you want a deeper dive, read How to Classify a Worker as an Employee vs. an Independent Contractor in the US.

Why freelance language creates classification mistakes#

Treat "freelance" as a business label, not a legal determination. Neither the IRS nor the U.S. Department of Labor presents "freelance" as a standalone classification test, so status decisions based on label alone create avoidable risk.

The mismatch is operational: forms collect labels, but agencies evaluate the working relationship. IRS guidance says status depends on the relationship between the worker and the business, including whether the business has the right to control how services are performed. Under the FLSA, DOL guidance distinguishes workers who are in business for themselves from employees, and warns that misclassified employees may lose minimum wage and overtime protections.

| What your form says | What it helps with | What it does not prove |

|---|---|---|

| "Freelancer" | Intake language and commercial routing | Legal status under IRS or DOL standards |

| "Independent contractor" | Contract and payout workflow setup | That the relationship facts support contractor treatment |

| "Employee" | HR/payroll routing | That mixed facts were reviewed and documented correctly |

The decision rule is straightforward: if the contract says "freelancer" but the facts show employer-like control, do not auto-approve contractor status. Route the case to employee review.

The fix is procedural, not semantic. Keep commercial labels if they are useful, but base approval on documented relationship facts and a distinct IRS and DOL review. You might also find this useful: Contractor vs Employee Classification Tool for Platform Operators.

How to apply IRS and DOL tests in one decision path#

Use one fact set and run two reviews in sequence: IRS first, then a DOL/FLSA pass. If those signals diverge, mark the case as legal review required and do not activate payouts.

| Step | Key question | Action |

|---|---|---|

| IRS review | What is the relationship between the worker and the business? | Score each IRS bucket as contractor-leaning, employee-leaning, or mixed |

| DOL / FLSA pass | Is the worker in business for themselves, or economically dependent on the company? | Run a separate labor review because IRS and DOL are not answering the same legal question |

| Signals diverge | Do the IRS and DOL reads point in different directions? | Mark the case as legal review required and do not activate payouts |

Start with the IRS review#

The IRS is the first screen because status depends on the relationship between the worker and the business. Start with facts, not labels: who has the right to control how work is done, who controls financial and business aspects, and what the relationship looks like in practice over time.

| IRS bucket | What to review |

|---|---|

| Behavioral control | Who controls or has the right to control how the job is done |

| Financial control | Who directs the financial and business aspects of the job |

| Relationship of the parties | Contract terms, employee-type benefits, continuity, and whether the work is key to the business |

- Capture current work facts from the manager, worker, and contract record.

- Score each IRS bucket as contractor-leaning, employee-leaning, or mixed:

- Behavioral control: who controls or has the right to control how the job is done. * Financial control: who directs the financial and business aspects of the job. * Relationship of the parties: contract terms, employee-type benefits, continuity, and whether the work is key to the business.

- Run a second pass under the DOL economic realities lens for FLSA purposes: does the worker appear to be in business for themselves, or economically dependent on the company?

- If the IRS and DOL reads point in different directions, pause and escalate.

That second pass matters because IRS and DOL are not applying identical tests or answering the same legal question. IRS focuses on tax classification and the business's right to control service details; DOL analyzes employee versus independent contractor status under the FLSA, where employees receive FLSA protections and independent contractors are treated as in business for themselves.

When the signals conflict#

Escalation should be trigger-based, not ad hoc. Use mixed patterns like these to route cases before payout activation:

| Facts on the ground | IRS read | DOL / FLSA read | What to do |

|---|---|---|---|

| Worker chooses methods and timing, but works almost only for your company on a continuing basis | Low behavioral control can look contractor-leaning | Economic dependence concern | Legal review required before payout activation |

| Contract says independent contractor and offers no benefits, but managers direct day-to-day methods and approve how work is performed | Employee-leaning because the business has the right to control details | Employee concern under FLSA | Route to employee review |

| Project-based engagement, worker controls methods, negotiates business terms, and serves multiple clients | Contractor-leaning across behavioral, financial, and relationship factors | In-business-for-themselves signal | Contractor status can proceed if evidence is complete |

| Little day-to-day supervision, but the relationship is indefinite and includes employee-type benefits or other long-term ties | Mixed IRS result, especially on relationship of the parties | Employee concern under FLSA | Legal review required |

Two common errors drive bad outcomes: treating one clean signal as decisive, and treating contract labels as proof. Low behavioral control alone does not close the case if economic dependence is high, and a contractor label does not overcome employer-like control in practice.

For close calls, document the DOL pass carefully. Fact Sheet 13 references regulations effective March 11, 2024, notes ongoing litigation, and also references the Department's February 26, 2026 NPRM. Treat borderline outcomes as reviewable legal judgments, not automated approvals.

Verification before status goes live#

Before status goes live, require a verification record with:

| Required item | What it must show | If missing |

|---|---|---|

| Written rationale | A rationale tied to each IRS bucket and the separate DOL pass | The classification is not production-ready |

| Approver identity | Approver identity and role | The classification is not production-ready |

| Timestamped evidence | Signed agreement, current scope, and manager statements on how work is directed | The classification is not production-ready |

If any item is missing, the classification is not production-ready.

We covered related payout handling in How to Handle a Signing Bonus for Freelance Contractor Work.

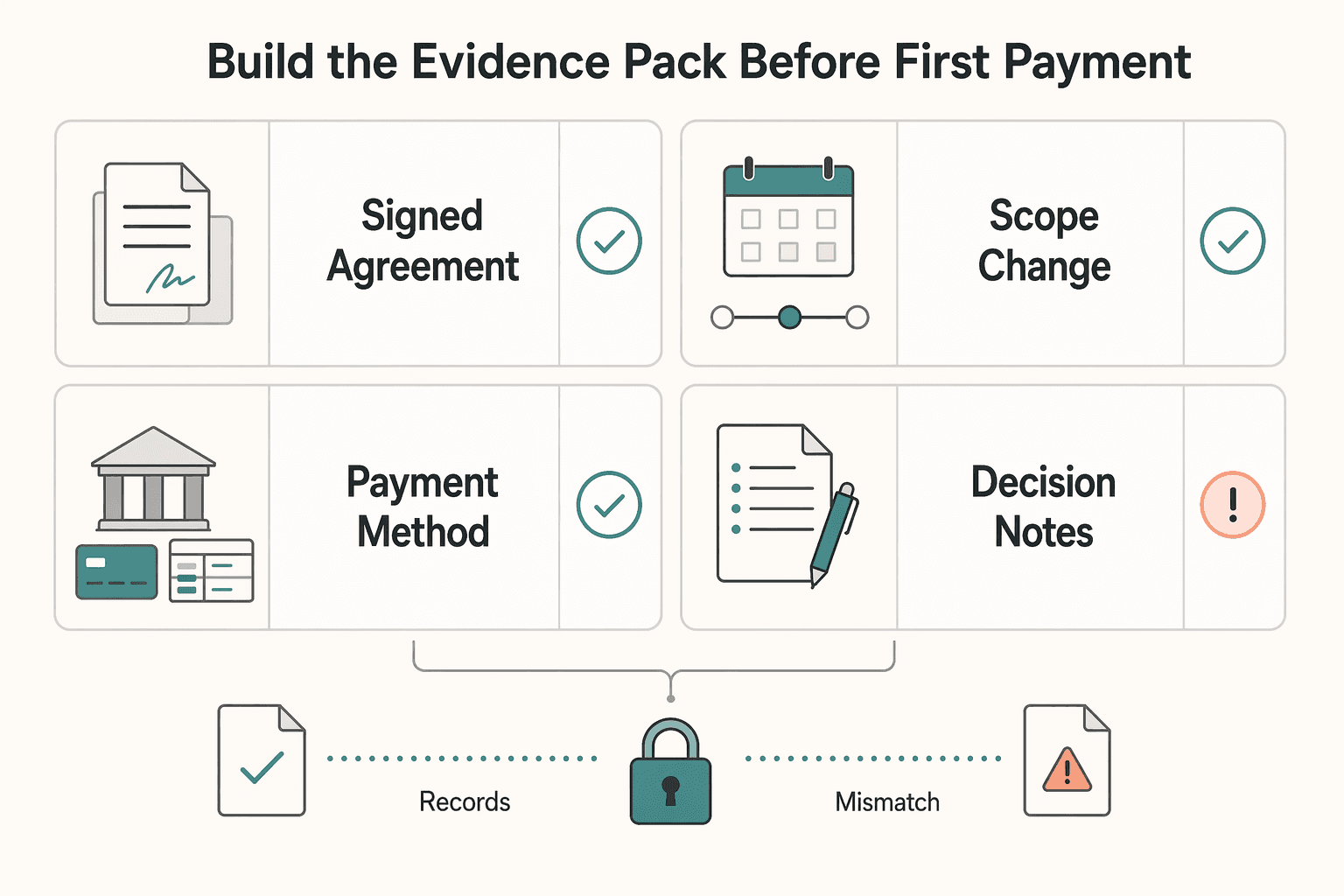

Build the evidence pack before first payment#

No complete evidence pack, no production payout activation. After you reach a classification outcome, keep a single file that explains the decision and ties it to how money is actually paid.

Use a minimum internal pack with four parts: the signed agreement terms in force at approval, scope or responsibility change history, payment method and payout account details, and written notes supporting the final status decision. These are not federal form requirements; they are the minimum record needed to defend the decision later.

| Evidence item | Employee classification | Independent contractor outcome | Red flag if missing |

|---|---|---|---|

| Signed agreement terms | Terms consistent with employment treatment and tax handling | Terms describing a contractor relationship, without relying on label alone | Team can only point to a label like "freelancer" |

| Scope change history | Changes that increase ongoing duties or supervision | Project scope, deliverables, and approved changes | Current work no longer matches approved facts |

| Payment method details | Routing into the channel where employee tax handling is performed | Routing into contractor payout handling | Payment path conflicts with approved status |

| Decision notes | Why facts support employee treatment | Why facts support contractor treatment | Reasoning cannot be reconstructed |

This payment link is a core control. The IRS says employee treatment generally requires withholding and depositing income, Social Security, and Medicare taxes, plus paying matching Social Security/Medicare and unemployment tax. For independent contractors, the IRS says businesses generally do not withhold or pay taxes on those payments. If your case file does not connect classification to payout setup and ledger records, your audit trail is weak.

Two operator steps make this defensible: keep linkable records across classification approval, payout account, and ledger entries, and stamp the case with the rule set and decision date used at approval. That date context matters: the current FLSA classification rule was published on 01/10/2024, and a proposed rule was posted on Feb 27, 2026 with comments open through Apr 28, 2026 at 11:59 PM EDT.

If status is disputed, keep all artifacts in the same case file so tax or legal can decide whether Form SS-8 or Form 8919 is relevant. The common failure mode is fragmented storage: contract in one system, approval note in another, payout data elsewhere, and ledger records somewhere else. Related: A Guide to California's 'AB5' Law for Independent Contractors.

What changes operationally when status changes#

When status changes, operations have to change with it, not just the contract label. In practice, employee routing generally requires withholding, deposits, and employer tax handling, while contractor routing generally does not.

| Operational area | Employee treatment | Independent contractor treatment | What to verify before first payment |

|---|---|---|---|

| Social Security tax and Medicare tax | IRS says the business generally must withhold and deposit these taxes from wages, and also pay the matching employer portion | IRS says businesses generally do not have to withhold or pay taxes on payments to independent contractors | Tax setup is active in the correct pay channel, not just noted in the contract file |

| Federal unemployment tax | IRS says the business generally pays unemployment tax on employee wages | IRS guidance here says contractor payments are generally not handled with that same employer unemployment tax path | Ledger mapping and worker record show the person is routed through the intended path |

| Cross-border Social Security handling | If U.S. coverage applies under a Totalization agreement, SSA says a Certificate of Coverage is proof of exemption from Social Security taxes to the foreign country | Do not assume the same employee proof path applies to a contractor arrangement | For cross-border cases, check whether a Totalization agreement applies and store the Certificate of Coverage if issued |

| Labor handling | Employee status should trigger labor-law review in your workflow | Contractor treatment does not remove review risk if underlying facts later support employee treatment | Status memo and approver note should show tax routing and labor handling were reviewed together |

The cross-border branch is easy to miss. SSA says Totalization agreements assign Social Security coverage to one country and exempt the employer and employee from Social Security taxes in the other, with the Certificate of Coverage as the proof document. If the worker record says "employee" but no one checks this, payroll can still be wrong even when the status call was otherwise documented.

The tradeoff is operational, not theoretical. Under-classifying can leave you correcting tax handling after payments are already out, while over-classifying can add withholding and deposit process the IRS generally does not require for contractor payments. If status changes, recheck tax routing, confirm who carries Social Security and Medicare obligations, and update the decision file before the next payout. Related reading: How to Create a Freelance Client Welcome Packet That Actually Protects You.

Escalation triggers and failure modes teams miss#

The main escalation rule is simple: if the engagement facts drift, treat the classification as potentially stale before more money moves. Misclassification carries legal and financial risk, so escalation should be triggered by operating changes, not only by complaints or audits.

These are practical warning signs, not standalone legal tests:

| Trigger event | Why it matters | What to do now |

|---|---|---|

| Scope shifts into ongoing core work | The live relationship may no longer match the original contract file | Reopen the classification review and compare current duties to signed scope |

| Schedule or process control tightens | Increased direction can change how the relationship is characterized | Recheck who sets priorities, methods, and approvals |

| Repeated exclusivity or near full-time dependency | Dependence may be increasing in practice | Reassess whether the current classification still fits |

| Manager-level direction replaces vendor-style coordination | Day-to-day supervision may now look different from the original setup | Preserve current operating evidence and escalate review |

A federal-only review may be incomplete in some cases. If the engagement has a California connection, add a California AB5 law check for applicable work instead of relying only on a federal file.

Disputes need a controlled path. Preserve the evidence pack, centralize handling, and decide whether Form SS-8 is appropriate; do not assume payouts must always pause, but consider pausing unsettled future payouts when the disagreement directly affects tax treatment or withholding expectations while a determination is pending.

The failure mode teams miss most is reusing an old decision after material contract changes. Early classification reviews and clear contracts are the safer default, and if the file does not show current facts, current approver, and current contract version, treat it as stale and re-review before additional payouts. Need the full breakdown? Read How Freelance Designers Get Hired and Paid on Dribbble.

Multi market controls and known unknowns#

Treat this section as U.S.-only guidance: non-U.S. worker-classification tests are out of scope here and should go to local counsel, not be inferred from U.S. guidance.

Your key control is to separate classification from adjacent tax-reporting workflows. A Form 8938 decision does not answer employee-versus-contractor status, even when both issues appear in the same engagement file.

For example, Form 8938 is used to report specified foreign financial assets, and it is attached to the tax return. For certain specified domestic entities, the stated trigger is $50,000 on the last day of the tax year or $75,000 at any time during the year. Keep that workflow separate from classification, and do the same for FATCA, FBAR, FinCEN, and Schedule SE so controls do not get mixed.

| Policy outcome | When to use it | Required record |

|---|---|---|

| Supported | U.S. engagement your team can support with current evidence | Classification memo, approver, timestamped evidence pack |

| Legal review required | Any non-U.S. work location, entity, or governing law not covered by this U.S.-centric material | Jurisdiction flag, local counsel request, hold note before payout expansion |

| Not supported | Market or structure your team has decided not to classify or pay without custom review | Written prohibition, escalation owner, exception log |

Use a country-by-country policy matrix with explicit supported, legal review required, and not supported outcomes before first payment and when scope changes. If a rule set is unknown, say that plainly in the file, route it, and avoid claiming the U.S. analysis applies abroad.

Conclusion#

If you want a classification decision that survives audits, worker disputes, and internal turnover, make it a two-part review every time: run the Internal Revenue Service control analysis and the U.S. Department of Labor employment relationship analysis, then save the reasoning. Labels like "freelancer" are not the answer. The answer is in the facts about control, continuity, and whether the person is truly in business for themself.

The IRS asks whether the business controls, or has the right to control, what the worker does and how the worker does the job. The DOL asks whether there is an employment relationship under the Fair Labor Standards Act, which matters because employees receive FLSA protections and independent contractors do not. If either lens points strongly toward employee status, treat that as a real escalation point, not something a contract title can smooth over.

For compliance and finance owners, the gain is not academic precision. It is more predictable operations. When status is decided with evidence and routed correctly, payroll and tax handling are easier to defend, and you are less likely to discover a reclassification problem after money has already moved. The verification detail that matters most is simple: before status goes live, keep a timestamped rationale, the approver's identity, the governing facts, and links to the agreement and payment record in the same file. If that packet is missing, you do not really have a completed decision.

A common failure mode is reusing an old contractor call after the relationship has changed. A manager starts directing hours, setting methods, or folding the worker into a core team, but the record still reflects the original onboarding label. That mismatch can trigger tax withholding issues and wage-and-hour exposure. The IRS is explicit that correct employee-versus-independent-contractor determination is critical, and employee wages generally require withholding and deposit of income, Social Security, and Medicare taxes.

One final caution for operators working at scale: improve evidence quality and jurisdiction routing before you improve speed. The DOL fact sheet itself notes the current framework remains in effect for private litigation while rulemaking activity continues, including the NPRM announced on February 26, 2026 with a comment period through April 28, 2026 at 11:59 ET. If your payout stack spans more than the U.S., do not infer foreign rules from U.S. guidance. Route those cases separately.

For a step-by-step walkthrough, see Are You an Employee or a Contractor? A Self-Assessment Checklist.

Frequently Asked Questions

Is freelancer a legal worker classification in U.S. federal law?

In the IRS and U.S. Department of Labor materials used here, the core federal distinction is employee versus independent contractor. In that sense, "freelancer" is common market language, not a separate classification in these materials.

Who decides employee versus contractor status, the IRS or the DOL?

Both matter, and they look at different consequences. The Internal Revenue Service focuses on the relationship between the worker and the business for tax treatment, including control over what is done and how it is done. The U.S. Department of Labor looks at whether the worker falls within an employment relationship covered by the Fair Labor Standards Act.

Can two people doing similar work be classified differently?

Yes. The IRS says a business might pay an independent contractor and an employee for the same or similar work, but the legal result depends on the underlying relationship facts, not the job title or service category. Before reusing a prior decision, verify whether control and the overall relationship with the business are still the same.

What is the economic realities test in plain terms?

In plain English, the DOL is asking whether the person is really in business for themself or is working in an employment relationship that should receive FLSA protections. If the facts point to employee status, FLSA protections can apply. If the person is truly operating their own business, the FLSA generally does not apply to them as an independent contractor.

What changes first when someone is treated as an employee?

Tax handling changes. The IRS states that employee pay generally requires withholding and deposits for income tax, Social Security, and Medicare taxes, while payments to independent contractors generally do not require withholding or tax payment by the business. Under DOL guidance, employees receive FLSA protections and independent contractors do not.

What should a company do if a worker disputes contractor status?

Reassess the worker-business relationship facts rather than relying on labels alone, since IRS classification depends on that relationship. If facts have changed or are unclear, get a fresh legal, tax, and payroll review before continuing with the prior classification assumption.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- dol.gov/agencies/whd/fact-sheets/13-flsa-employment-...trusted

- dol.gov/agencies/whd/flsa/misclassificationtrusted

- federalregister.gov/documents/2024/01/10/2024-00067/employee-or-...trusted

- federalregister.gov/documents/2021/01/07/2020-29274/independent-...trusted

- hks.harvard.edu/sites/default/files/centers/mrcbg/files/97_f...trusted

- irs.gov/newsroom/worker-classification-101-employee-...trusted

- irs.gov/businesses/small-businesses-self-employed/in...trusted

- oui.doleta.gov/dmstree/op/op2k/op_05-00.pdftrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Classify a Worker as an Employee vs. an Independent Contractor in the US

Start with the real working relationship, because that drives the classification outcome. If the day-to-day setup looks like a **common-law employee** relationship, calling the worker a contractor in the agreement does not by itself remove the underlying **worker misclassification** risk.

California AB5 Law for Independent Contractors

If you sell services to California clients, the real issue is often whether the client's legal and procurement teams can evaluate and document the classification decision before they send your contract for signature. Under AB5, that review happens inside a framework that has been in place since January 1, 2020. Misclassification exposure can include [civil penalties of $5,000 to $25,000 per violation](https://www.dir.ca.gov/Fraud_Prevention/Misclassification.htm).

Contractor vs Employee Classification Tool for Platform Operators

Treat a contractor classification tool as a payment control, not a one-time legal checkbox. If your team cannot show why a worker was treated as an independent contractor or employee before the first payout batch runs, you do not just have a policy gap. You have a release-control problem that can create downstream tax reporting, reconciliation, and audit-defense risk.