Quick Answer

Yes, you can accept a signing bonus for freelance contractor work if it is documented as service compensation tied to a specific business event. Define the trigger, approval proof, amount, and invoicing path in your contract stack, then remove loyalty or discretionary wording that reads like employee pay. Once paid, handle it as contractor income and reconcile records against the applicable form path, including 1099-NEC, 1099-K, or 1042-S when relevant.

Moving Beyond the Payday to Strategic Incentive Engineering#

A signing bonus for freelance contractor work is not automatically a problem, but it gets riskier when it is structured like employee pay rather than service compensation. Before you accept it, define what the payment actually is:

- Employee-style signing bonus: a payment treated like employee supplemental wages. IRS employee supplemental wage rules include 22% withholding and 37% above the stated high-income threshold.

- Contractor incentive payment: nonemployee compensation for services, generally reported on Form 1099-NEC when reporting thresholds are met, including $600 ($2,000 for payments made after December 31, 2025).

That distinction matters because status turns on the real working relationship, including control and independence, not just the label in the contract. Use this three-part filter before you say yes:

- Trigger: Is the payment tied to a defined service outcome, such as a milestone, deliverable, or completion, or is it just for joining or being available?

- Documentation: Is it written into your contract stack, such as the MSA, SOW, or an amendment, and invoiced as service compensation rather than handled with payroll-style language?

- Control: Does the arrangement preserve your independence in how you do the work, or does it give the client employee-style control over what and how you do it?

| Issue | Employee-style bonus | Contract-linked incentive |

|---|---|---|

| Trigger | Joining or start-date style payment | Defined milestone, deliverable, or completion |

| Documentation | Offer or payroll-style language | Contract, SOW, or amendment plus invoice line item |

| Risk signal | Looks like supplemental wage treatment | Better aligned with nonemployee service pay |

The practical move is to stop negotiating around the word "bonus" and start negotiating around the business event that earns the payment. For related freelancer compliance context, see A Guide to the German 'Künstlersozialkasse' (KSK) for Freelance Artists.

The Mindset Shift: From "Bonus" to "Incentive Engineering"#

If you want to reduce classification risk, treat this as incentive compensation for defined results, not as an employee-style bonus. When a client offers this kind of payment, the safer move is to tie it to measurable outcomes and document it in project terms.

Use outcome language, not payroll language#

Words matter here. IRS payroll guidance treats bonuses as supplemental wages, so the term "bonus" naturally pulls the conversation toward employee-pay framing. That does not make every contractor deal using that word invalid, but it does create avoidable risk.

For contractor status, the core issue is control. The client can specify the result, but not your day-to-day method. Your language should point to scope, deliverables, and acceptance criteria.

| Weak term | Defensible term | Why it improves posture |

|---|---|---|

| Signing bonus | Completion incentive tied to final deliverable acceptance | Ties payment to a defined result, not hiring language |

| Retention bonus | Milestone incentive for Phase 2 delivery in the SOW | Anchors payment to contracted scope |

| Start-date bonus | Kickoff payment triggered by agreed onboarding deliverables | Connects money to work output, not mere start date |

| Discretionary bonus | Performance fee tied to stated acceptance criteria | Makes the trigger objective and documentable |

Script it like a vendor conversation#

Do not argue about terminology in the abstract. State the business mechanism clearly and move the client toward a clean payment trigger.

What to say: "I do not structure compensation as an employee-style bonus. If you want an additional payment, let's tie it to a defined milestone, acceptance criteria, and an invoice trigger in the SOW."

Avoid phrases like these:

- Reward for loyalty

- Pay for availability

- "Joining the team" framing

- Employee-style commitment language

Those phrases push the relationship toward employment framing instead of an independent vendor delivering outcomes.

Make sure the wording matches real practice#

Good wording helps, but it is only part of the evidence. Worker-status analysis looks at behavioral control, financial control, and relationship factors, and DOL's current proposal also puts weight on actual practice over theoretical wording.

Before you accept the payment, verify that:

- It is documented in an MSA, SOW, amendment, or other written agreement.

- The trigger is measurable, such as delivery, completion, or acceptance of listed work.

- It is invoiced as nonemployee service compensation and may need Form 1099-NEC reporting.

- The client is buying a result, not managing your daily process.

If the label says "incentive" but actual practice still looks employee-style, relabeling did not solve the risk. Redesign the payment terms or decline the structure.

Need the full breakdown? Read Conflict Resolution for Freelance Partnerships.

The Risk-Mitigation Playbook: Proposing the Right Incentive Structure#

Once the language is right, choose a structure. Pick the one that makes the payment trigger easiest for you to verify in writing. Usually, the safest option is the one where "done" is observable, the payout is pre-agreed, and the evidence is easy to produce.

That matters because classification is not decided by one label or one clause. IRS analysis evaluates behavioral control, financial control, and the relationship of the parties under common-law principles. DOL analysis uses a totality-of-the-circumstances approach where no single factor is dispositive. Your payment structure should reinforce an outcomes-based vendor relationship.

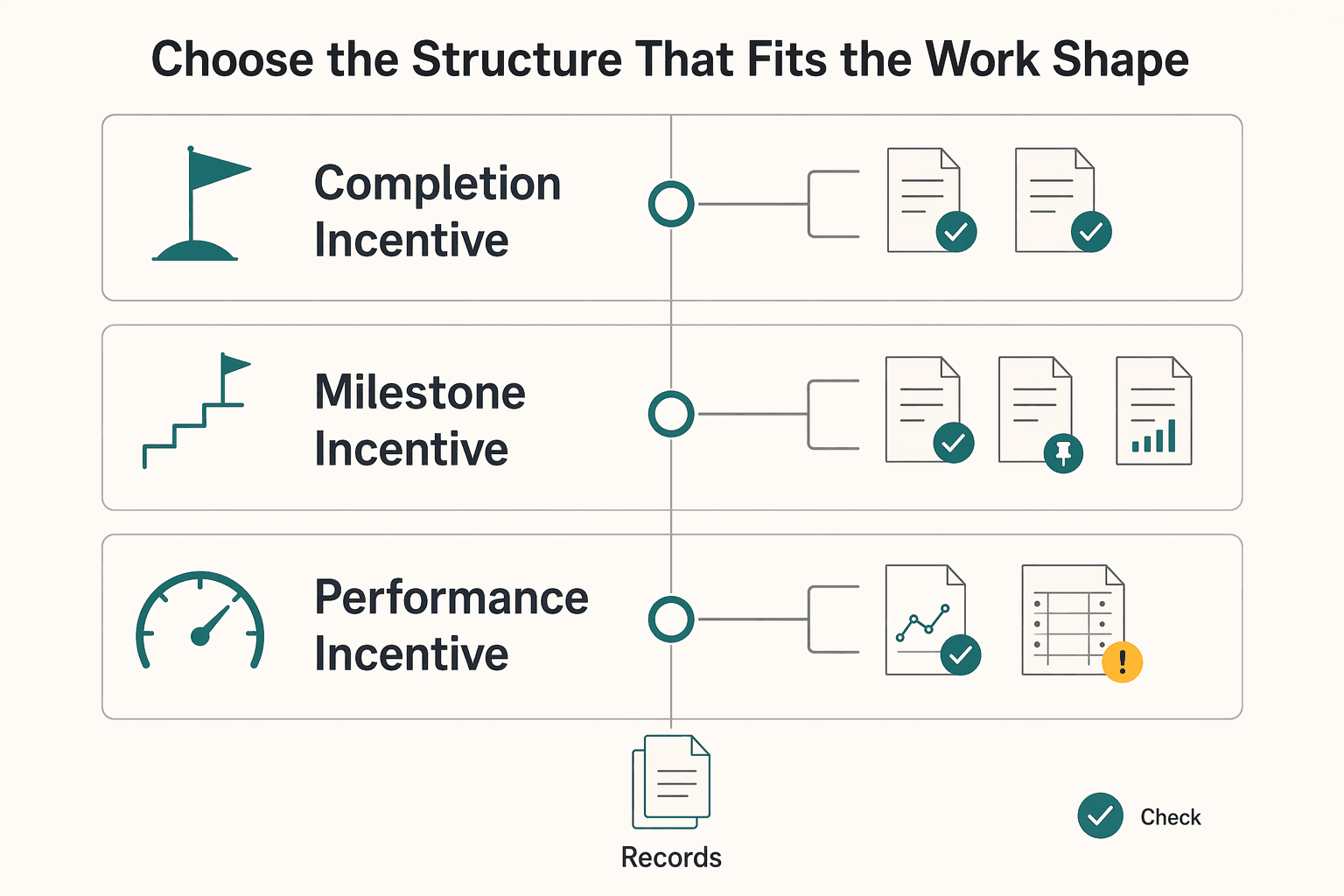

Choose the structure that fits the work shape#

Match the trigger to how value is delivered, not to how long you are available.

| Structure | Choose it when | Trigger | Payout logic | Evidence of completion | Do not use when |

|---|---|---|---|---|---|

| Completion incentive | You are delivering one final package and value is concentrated at the end | Final acceptance event for the defined deliverable after verification | One lump-sum payment at final acceptance | Signed acceptance, delivery record, versioned final files, acceptance email or ticket | Dependencies outside your control are high, or final approval is likely to be subjective |

| Milestone incentive | The work naturally breaks into phases and you need steadier cashflow | Acceptance of each named work segment after verification | Separate payment per milestone | Approved phase deliverable, milestone submission record, invoice mapped to that phase | Phase boundaries cannot be defined, or the client will not predefine acceptance events |

| Performance incentive | Success can be measured with an objective metric or defined event | Objective metric hit or defined event achieved using a named data source | Payment when the threshold or event is met | KPI report, analytics export, client system record, dated measurement window | Metric inputs are outside your control, KPI ownership is disputed, or success is subjective |

Define "done" so payment is enforceable#

For each incentive, define three things in the contract: trigger, amount, and evidence. If one is vague, you have a dispute gap.

Use this contract-ready pattern:

- Completion incentive: Use this only after the signed contract verifies the payment amount, final deliverable, and acceptance event.

- Milestone incentive: Use this only after the signed contract verifies the milestone name, acceptance criteria, payment amount, and acceptance process.

- Performance incentive: Use this only after the signed contract verifies the payment amount, KPI target, data source, and measurement window.

Avoid time-only or admin-only triggers such as "paid after 30 days" or "paid on signature."

Run a quick selection check before proposing terms#

Before you propose terms, run the structure through these five checks:

| Decision factor | If this is true | Prefer | Why |

|---|---|---|---|

| Project shape | One bundled final output | Completion | Single acceptance event matches delivery model |

| Cashflow pressure | You need payment across execution | Milestone | Splits risk across defined work chunks |

| Outcome measurability | Result can be measured objectively | Performance | Trigger can be tied to quantifiable evidence |

| Client approval risk | Reviews are slow or subjective | Milestone | Limits end-loaded approval exposure |

| Dispute risk | Responsibility or data ownership may be contested | Milestone or completion | Reduces ambiguity versus KPI-dependent payout |

If outcome measurement depends heavily on the client's internal operations, use performance incentives only when the data source, ownership, and trigger event are fully specified.

Verify the payment path before work starts#

A clear trigger is not enough if the payment mechanics are fuzzy. Before work starts, confirm your signed contract or amendment, invoice terms, acceptance record, and delivered output all map to the trigger.

If you are using Upwork fixed-price, confirm each milestone is funded before starting work. The client has a 14-day review window. Approved or auto-released funds then move to a 5-day security hold, and refund requests have a 7-day response or dispute window. Those timings are platform-specific, but the practical rule is the same: verify funding, the acceptance path, and your evidence before you begin.

For related prep work, see Build a Pitch Deck for a High-Value Freelance Proposal.

The Compliance Shield: Structuring Incentives Without Triggering Misclassification Alarms#

After you choose the structure, make the contract carry the same logic. Treat this kind of arrangement as an outcome-based contract incentive, not pay for loyalty, availability, or effort.

Define key terms before you draft#

Use these terms consistently in the SOW or MSA:

- Deliverable: the product or service you submit for acceptance against contract requirements.

- Acceptance criteria: the stated specs, goals, measures, tests, or other checks used to accept or reject that deliverable.

- Discretionary payment: a payment where the payer keeps sole discretion over both whether to pay and how much to pay.

If the trigger depends on subjective approval or open-ended discretion, treat it as uncertain upside, not committed compensation.

Build the clause around observable acceptance#

Before you sign, make sure the clause covers each of these points:

| Clause part | What to specify | Article example |

|---|---|---|

| Trigger event | Named deliverable or milestone meets the acceptance criteria in the SOW section or exhibit | Payment amount, deliverable or milestone, and SOW reference pending signed agreement verification. |

| Measurable outcome | Current threshold, named data source, and measurement window | Performance threshold, data source, and measurement window pending signed agreement verification. |

| Acceptance method | Acceptance certificate, written approval from named role, or approval in named system after review against the acceptance criteria | Acceptance evidence method pending signed agreement verification. |

| Invoice timing | Invoice within the signed contract's stated business-day window after acceptance and reference the deliverable ID, milestone, or reporting period | Invoice window, reference field, and payment term pending signed agreement verification. |

| Dispute path | Written reasons tied to unmet criteria within the signed contract's stated response window, then review named evidence records and resubmit or close disputed items | Rejection response window and evidence review process pending signed agreement verification. |

Use those elements together. If any part of the clause is vague, you still have both payment risk and classification risk.

Replace risky wording with contract-ready language#

| Risky wording | Why it is risky | Defensible wording |

|---|---|---|

| "Bonus after 30 days if manager is satisfied with performance" | Subjective manager approval reads like employee-style supervision | "Completion incentive payable after the signed contract verifies the named deliverable and written acceptance criteria." |

| "Extra pay for attending daily standups and being available during client hours" | Ties compensation to schedule and process control | "Milestone payment due after the signed contract verifies the named milestone and validation evidence." |

| "Discretionary bonus for hard work" | Unilateral judgment over payment and amount | "Performance fee payable only after the signed contract verifies the threshold, data source, and measurement window." |

Just as important, keep practice aligned with the paper. If the contract says you control how the work is done, but the day-to-day setup looks like employee management, the clause alone may not protect you on its own.

Run a pre-signing validation flow#

Use this short check before you sign:

- Confirm outcome link: the incentive is tied to a defined deliverable, milestone, or measured result.

- Confirm autonomy: the terms define what you deliver, not how you must execute each step.

- Confirm signed placement: the final SOW or MSA includes the incentive clause, acceptance criteria, invoice path, and rejection procedure before work starts.

For a step-by-step walkthrough, see The Pros and Cons of a C-Corp for a Freelance Business.

The Negotiation Toolkit: Proposing a Win-Win Incentive Structure#

Good drafting only matters if you can get the client to agree to it in the room. In negotiation, position the incentive as a contract payment mechanic tied to outcomes, not as a personal perk or loyalty reward.

Reframe the ask around outcomes, not loyalty#

Treat a payment as an incentive only when it is earned by a defined deliverable, milestone, or measurable result with clear acceptance criteria. If a client says "signing bonus," translate it into outcome language right away.

You can say: "I'm open to an incentive if it is tied to a defined deliverable or milestone with written acceptance criteria, so we both know exactly when it is earned."

| Say this | Not that | Why this is safer |

|---|---|---|

| "Add a completion incentive only after the payment amount, deliverable, and SOW acceptance reference are verified in the signed contract." | "Give me a signing bonus for taking the project." | Ties payment to contract performance, not joining the engagement |

| "Use a milestone payment only after the phase, scope, and approval method are verified in the signed contract." | "Pay extra if I stay through launch week." | Focuses on a business result, not retention |

| "Set a performance fee only after the payment amount, threshold, data source, and measurement window are verified in the signed contract." | "Bonus me if the team is happy with my work." | Replaces subjective judgment with an objective trigger |

| "Release payment after written acceptance and invoice under the payment term verified in the signed contract." | "Pay extra if I attend standups and stay online during client hours." | Avoids schedule and process-control terms |

A quick test helps. If the trigger depends on attitude, attendance, hours, or manager satisfaction, it is not a strong contractor incentive term.

Bring a call-ready checklist and fill it live#

Do not leave the important details for later. On the call, lock down these four items:

- Trigger event: the exact deliverable, milestone, or threshold that earns payment

- Acceptance method: how acceptance is evidenced, such as a named approver, acceptance record, or named system

- Payment term: the amount plus when payment is due after acceptance or invoice

- Written documentation: the final SOW, MSA, or addendum includes this term in writing, ideally before work starts

If any item is vague, ask for the specific record: section number, deliverable ID, approver role, and payment mechanism.

If New York Article 44-A applies to the engagement, keep this in mind during negotiation. Covered freelance contracts must be in writing and must include services, compensation, and the payment date or mechanism. If timing is not specified, payment is due no later than 30 days after completion. The $800 threshold can aggregate with the same hiring party over the prior 120 days.

Run a go or no-go screen when terms drift#

Use this screen before you price the incentive into your economics:

| Signal | Status | Article action |

|---|---|---|

| We'll decide later if we want to pay it | Fix now | Convert it to a defined trigger plus payment term, or remove it from your compensation assumptions. |

| Payment tied to required hours, attendance, or continuous availability | Fix now | Convert it to milestone-based or acceptance-based payment tied to outcomes. |

| Refusal to document the term in written contract language | No-go if unresolved | Treat it as non-contractual and do not price it as committed compensation. |

| The contract says independent, but the day-to-day plan is staff-style control | No-go warning | Paper terms alone do not resolve classification risk. |

If a term still fails this screen, do not price the incentive as committed compensation.

Close with a repeatable four-step flow#

Keep the close simple and repeatable:

- Propose the incentive in client-value terms tied to a business outcome.

- Validate the trigger, acceptance method, amount, and payment term.

- Document those terms in the written contract set, ideally before work starts.

- Confirm who updates the draft, when you review it, and what evidence will prove acceptance.

If you cannot complete all four steps clearly, pause the deal and renegotiate before you proceed.

Related: How to Structure an LLC for a Freelance Writing Business.

Before you send terms, draft your incentive clause and acceptance language in the Freelance Contract Generator.

The Financials: Tax Implications for Your 1099 Incentive#

Once the term is negotiated, handle the money like business income from day one. In contractor arrangements, this kind of payment can be 1099 incentive income: nonemployee compensation for services, not employee wages, and generally paid without federal withholding (though backup withholding can apply in specific cases).

Classify it correctly before you spend it#

Start with a plain working classification:

| Scenario | Form path | Article note |

|---|---|---|

| Direct client payments for contractor services | Form 1099-NEC | Typically tracked toward Form 1099-NEC reporting under current IRS instructions. |

| Payment card and third-party network transactions | Form 1099-K | May be reported on Form 1099-K instead of 1099-NEC. |

| Cross-border payments to nonresident contractors | Form 1042-S | Can fall under Form 1042-S rules, and withholding may apply. |

| Missing form | No form received | Do not treat a missing form as no-tax income. You still report income you earned. |

- 1099 incentive income: contractor compensation for services

- Self-employment tax: Social Security and Medicare tax for people who work for themselves

- Estimated payments: pay-as-you-go tax payments on income that is not subject to withholding

Verify the payment path and form path together. A missing form does not change the fact that you still report income you earned.

Take immediate control of cash and records#

The first operational mistake is spending the deposit before you have accounted for tax, reporting, and any platform fee effects.

| If this incentive is paid now | What you should do immediately |

|---|---|

| U.S. client pays by ACH or check | Set aside part of the payment in a separate tax bucket. Record gross income by payer, invoice, and milestone or deliverable. Review your estimated-payment plan and update the next payment if needed. |

| Paid through card or platform | Set aside the tax portion even if the net deposit is reduced by fees. Reconcile the gross amount, fees, and net deposit so 1099-K reporting matches your ledger. Recheck estimated payments based on total gross inflow, not just deposits. |

| Foreign payer or cross-border work | Hold a larger buffer until withholding and reporting treatment are clear. Tag payer location and any withholding shown in your records. Get tax advice before filing when 1042-S or foreign withholding is involved. |

Use this rule set:

- Increase your set-aside when the payment is unusually large for your year, arrives late in the year, or you have limited withholding elsewhere.

- Use a separate tax bucket if cash in your operating account is easy to spend.

- Bring in a tax professional when foreign payers or cross-border withholding enter the picture.

Reconcile forms first, then file from your books#

When forms arrive, reconcile each one against your ledger and deposits: 1099-NEC, 1099-K, or 1042-S. If an expected form is missing, contact the payer and document that outreach. If a form is wrong and it is not corrected in time, attach an explanation to your tax return and report your income correctly from your own books.

You might also find this useful: How to use 'escrow' for a large freelance project payment.

Your Incentive Isn't Just a Payday - It's a Strategic Advantage#

The common thread is simple: the payment is usually easier to defend when you can explain it as a real business event rather than goodwill. Frame it as startup work, risk-sharing, or a defined result so the client can approve it, you can invoice it, and the contract matches how the work actually runs.

Pick the position that matches reality#

Start by being honest about what the relationship actually looks like.

| If the relationship looks like this | Position yourself as | Incentive structure that usually fits |

|---|---|---|

| Client directs tasks closely and focuses on process, meetings, and day-to-day execution | Execution support | Project initiation fee or milestone payments tied to kickoff, discovery, onboarding, or named deliverables |

| You control how work is done and the client mainly cares about results | Outcome partner | Completion incentive or outcome-based incentive tied to a defined event, metric, data source, and measurement period |

| Control is mixed or unclear | Higher-risk case | Simplify terms, avoid vague "bonus" wording, and pause for review before signing |

Use this as a decision check, not a shortcut. Worker status turns on the full working relationship, and no single clause decides classification by itself. Different laws can apply different classification standards, so avoid treating one framework as final certainty.

Lock four controls before sending terms#

Before you send terms, lock these four controls:

- Define the event: Name the startup obligation, deliverable, or measurable outcome in one sentence.

- Define the trigger: State the amount or formula, payment date, and proof required to release payment, such as milestone sign-off or a metric report.

- Plan cash flow and tax: Contractor payments are generally not payroll-withheld, so map timing to estimated-tax planning. If net self-employment earnings reach $400, self-employment tax usually applies.

- Use compliance-safe wording: Draft to the result, not control of your method. If the payment can only be explained as "you joined fast" or "we liked your attitude," it is still too vague. Check current IRS instructions and forms before relying on a fixed 1099-NEC threshold because IRS pages conflict on $600 vs $2,000 after Dec. 31, 2025.

Apply this on your next proposal#

On your next proposal, pair one client risk with one incentive structure. In the contract or SOW, use the same label, trigger, amount, payment date, and required proof. In invoicing, use that same label and confirm taxpayer information early, since avoidable paperwork issues can trigger 24% backup withholding in some cases. If the client insists on employee-style bonus wording or status is disputed, pause and assess whether Form SS-8 is the right next step.

If you want a deeper dive, read How to Calculate Your Billable Rate as a Freelancer.

Before you finalize the deal, sanity-check classification and tax planning with the W-2 vs 1099 Calculator.

Frequently Asked Questions

How do you ask for signing-bonus-style pay without making the deal look employee-like?

Lead with the business event, not just the word “bonus.” If the client needs a fast kickoff, propose a project initiation fee tied to startup work such as kickoff, discovery, onboarding, or reserved capacity. If the value lands later, use a completion incentive or outcome-based incentive tied to a defined event or measurable result, and put the trigger, amount or formula, and invoice timing in one place.

Which incentive type should you choose?

Choose the term that matches the commercial event you can actually prove. A project initiation fee fits startup work or reserved capacity, a completion incentive fits fixed scope or a final milestone, and an outcome-based incentive fits a measurable business result with a clear data source and time window. A discretionary bonus is usually the weakest option for enforceability because payment and amount are not promised in advance.

How do you reduce misclassification risk when negotiating these payments?

Do not rely on labels alone. IRS classification is multi-factor, and DOL FLSA analysis focuses on economic dependence, with recent rulemaking signals reinforcing that real-world practice matters more than wording by itself. Keep incentive triggers tied to objective events, quantifiable results, or defined deliverables, not open-ended manager discretion.

What should be in the contract so the incentive is enforceable?

Put the incentive in the signed agreement, SOW, or amendment with the exact trigger, amount or formula, payment date, and required proof. Electronic signatures generally cannot be denied legal effect solely because they are electronic, so an e-signed record can support enforceability. Keep a simple evidence file with signed terms, approval messages, the scope version, delivery proof, and any metric report used to trigger payment.

Are there location-specific contract rules you need to check?

Yes. Treat federal tax treatment and local worker-classification and contract rules as separate checks. For example, NYC requires a written contract for covered freelance work totaling $800 in any 120-day period, including scope, pay, and payment date, and California may apply AB 5 tests in some cases. Assume rules can differ by city and state.

How should you invoice and report the incentive after approval?

Invoice using the same term as the contract clause, such as “Project initiation fee” or “Completion incentive,” and send Form W-9 early with your correct TIN. Missing or incorrect certification can trigger 24% backup withholding on reportable nonemployee compensation. Reconcile your books to 1099-NEC or 1099-K as applicable, report income even if no form arrives, and verify the current 1099-NEC reporting threshold in current-year IRS instructions before relying on a fixed number.

What if you or the client is outside the U.S., or the work spans multiple states?

Treat that as a higher-risk setup, not a minor variation. U.S. persons abroad still report worldwide income, and cross-border or multi-state facts can affect withholding, reporting, and sourcing outcomes. FEIE analysis can also depend on tests such as 330 full days in 12 months. For state-side triage, start with Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?, then escalate to tax or legal review for a final position.

When should you pause and get tax or legal review before signing?

Pause when the client insists on employee-style “bonus” wording, refuses to define an objective trigger, omits a payment date, or keeps payment fully discretionary after delivery. Also pause for foreign payers, foreign withholding, multi-state allocation, or any deal where contract language and actual workflow do not match. At that point, better drafting alone is not enough risk control.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?

Living abroad does not end `state income tax` exposure by itself. The first decision is practical: choose a filing position your facts can support, then build records that support the same story all year.

How to Calculate a Freelance Rate You Can Actually Get Paid On

A workable rate is not the neat number a calculator produces. It is the number that still works after you account for real billable capacity, non-client time, scope drift, and the gap between sending an invoice and receiving cleared cash. Start with hourly math even if you do not plan to bill hourly, then turn that number into a quote with clear `payment terms`.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.