Quick Answer

Start by locking one operating model before vendor evaluation: HQ-Led Accounts for tighter central governance or Chapter-Level Payouts for local speed. In events ticketing platform payments refunds payouts, expansion decisions should then be based on country-level proof of refund handling, settlement behavior, payout authority, and reconciliable records. Keep deletion separate from monetary reversal, and approve launch only when finance can trace each case from request through processor reference to accounting output.

Start with refund and payout authority#

Start with the money movement model, not the demo. In event ticketing, payment, refund, and payout failures often show up after launch. They usually come from unclear refund authority, settlement landing in one account that finance has to reallocate manually, or currency mismatches between checkout, settlement, and reporting.

That is why this guide starts with HQ-Led Accounts versus Chapter-Level Payouts before comparing Bevy, Eventbrite, Ticketing.events, or any other vendor. UI matters, but it does not determine refund authority, settlement ownership, payout controls, or reconciliation accountability. Those are operating-model decisions first.

Teams often start with ticketing features and integrations, then find out that refunds, payouts, and settlement depend on gateway setup, currency design, and account structure. A single settlement account can look simpler early on and create manual cross-entity reallocation later, especially during peak launches or frequent cancellations.

Decide who controls money before you decide who sells tickets#

If finance needs tighter centralized governance, HQ-Led Accounts may align better with that goal. If local teams need faster local action, Chapter-Level Payouts may align better with that goal, with tradeoffs in control consistency and reconciliation workload.

Before you shortlist vendors, align on three answers. If those answers are still fuzzy, product demos can create false confidence.

- Who can authorize refunds, and at what level?

- Who can pause or release payouts?

- Who owns reconciliation when platform, gateway, and ledger records differ?

Treat refunds and settlement as finance design, not support tasks#

Refund policy is not just a support setting. It affects accounting entries and payout expectations, and it needs explicit authorization and delegation controls. Each refund path should leave a clear record sequence that finance can review, especially for exceptions.

Settlement needs the same discipline. Event-ticketing flows may include high-ticket sales with higher dispute exposure, or frequent low-value transactions where fees add up quickly. In both cases, the core question is the same: when money comes in, when it goes out, and what evidence proves it moved correctly?

Keep currency and reporting separate in your head#

Multi-currency checkout is easy to oversimplify. The attendee display currency can differ from gateway settlement currency, and both can differ from finance reporting currency. If you blur those together, you increase the chance of FX surprises and dispute risk.

This guide stays focused on operations: payment collection, refund paths, settlement timing, payout controls, and reconciliation requirements across platforms like Bevy, Eventbrite, and Ticketing.events. Choose your control model first, then test each vendor against it. If ownership, evidence, and currency design do not fit, feature depth is secondary.

Refund operations across travel and events share timing and evidence issues; Airline Delay Compensation Payments gives a parallel refund-disbursement model.

Step 1 Choose your payout control model before vendor demos#

Decide where payout control lives before you evaluate vendors. Choose a centralized or local ownership model, then map who owns payout timing, refund approvals, and reconciliation.

Use a centralized model when finance needs one control point and tighter governance. Use a local model when local teams need more autonomy and you can accept more variation in controls.

Make this decision in writing now, not in demo follow-ups. Start with a simple scenario map, then turn it into an ownership matrix so product, payments ops, finance ops, and support have clear boundaries. At minimum, confirm ownership for:

- Product: account structure, permissions, and in-product control paths

- Payments ops: processor-side exception handling and escalation paths

- Finance ops: payout-release rules and reconciliation

- Support: customer communication and escalation routing within approved authority

Before you shortlist any vendor, run one checkpoint. Every role should give the same answer to:

- Who can pause payouts?

- Who can authorize refunds?

- Who reconciles discrepancies?

If those answers differ, fix ownership first. Fragmented setups often force manual monthly reconciliation across separate ticketing and processor records, and that is slow, error-prone, and hard to scale.

Related: How Platforms Should Prepare for CBDC Payments: What Digital Currency Means for Contractor Payouts.

Step 2 Build a country and gateway coverage matrix#

A market is only ready when refunds, payouts, action location, and open unknowns are documented with owners and proof. Build that view country by country so launch decisions rest on validated operations, not demo impressions. This step turns the control model from Step 1 into something you can test market by market.

Create one matrix per launch market#

Use one row per gateway candidate in each country sheet, for example: Stripe, Square, Worldpay, 2Checkout, AliPay, PayU, Instamojo. Fill cells from documented evidence, not memory or verbal confirmation. Keep Action location strict: In-product, External dashboard, or Undocumented. Track Apple Pay and Google Pay separately, not as a single wallets note, and default to Unknown until validated.

| Gateway | Refunds supported | Payouts supported | Action location | Apple Pay | Google Pay | Key unknowns | Validation owner |

|---|---|---|---|---|---|---|---|

| [Gateway name] | Yes / No / Unknown | Yes / No / Unknown | In-product / External dashboard / Undocumented | Yes / No / Unknown | Yes / No / Unknown | Refund timeline; settlement window; chargeback handling depth | [Owner] |

Record unknowns as explicit blockers#

Do not bury uncertainty in comments. Put Unknown in the matrix and attach a validation task. At minimum, track:

- documented refund timeline

- payout settlement window

- chargeback handling depth, including evidence, status, and export detail

- whether payment events expose a shared identifier for internal matching

- whether export data includes payment-attached information needed for receivables and invoice reconciliation

Treat missing reference fields as reporting risk, not a minor gap.

Validate with evidence, not verbal confirmation#

Every filled cell should map to proof: document link, screenshot, or recorded demo. For high-risk rows, run one end-to-end test path, including approval, denial, and refund handling, before marking the market ready.

If a vendor says payouts, refunds, and attendee changes can all be handled from one operator flow, keep the exact workflow article in your evidence pack. Bevy's Managing Paid Events guidance is the kind of source support and finance should validate together before a market is marked ready.

No country is Ready until every unknown has an owner-assigned validation task and launch-critical fields have attached proof.

Step 3 Define refund paths and reconciliation-safe actions#

Define refund paths before live issues start. Treat attendee removal and money reversal as separate actions unless your own test evidence shows the same financial outcome.

Separate money reversal from attendee removal#

Deleting an attendee may change access or operational records, but on its own it does not confirm that cash was returned or revenue was reversed. Document each action in plain terms:

- attendee record impact

- payment-processor impact

- accounting artifact created, if any

- export or ledger impact

Run two test cases in the same setup: delete only and refund. If only the refund flow creates a financial artifact, for example when a Customer Return Authorization created with a Credit Form generates a Credit Memo, the actions are not interchangeable.

Split refunds into two execution lanes#

Use two lanes: automated in-product refunds, but only where validated, and manual processor-handled refunds when the in-product flow is unavailable or unverified.

If documentation is incomplete or access fails verification, keep that path out of automated handling until someone validates it end to end.

For both lanes, do not close the case until your internal record includes the order identifier, the processor refund reference used by your team, the amount and reason, and the approver or executor. It should also include the resulting accounting record.

Set refund authority in writing#

Write down who can execute standard refunds and who must approve exceptions before volume increases. Keep the control simple: owner, escalation path, and exception handling should be clear and shared across support and finance.

Tie every refund to reconciliation evidence#

A refund path is only reconciliation-safe when finance can trace request -> processor event -> accounting impact. Add a standing control to compare expected versus actual fees on refunded transactions. Treat fee overruns or missing accounting artifacts as investigation triggers, not admin noise.

For service-provider payouts, Accounting and Bookkeeping Platform Payments shows how payee controls and scale change the payment design.

Step 4 Set settlement and payout policy with reserves and cutoffs#

Once refund handling is defined, lock down cash movement policy. Do not release funds unless each market and account has verified settlement evidence, a written post-payout refund path, and a clearly owned reserve decision process where applicable.

Build the settlement table before you approve any market#

Use one settlement table to force every market and account into verified or blocked status. Keep it operational, not aspirational.

| Field | What to record | Why it matters |

|---|---|---|

| Country / legal entity / account owner | Who operates the flow | Clarifies control and accountability |

| Payout configuration evidence date | When settings were last verified | Prevents stale assumptions |

| Payout cadence status | Verified or blocked (until tested and evidenced) | Avoids launching on unproven timing |

| Required evidence | Settings capture, payout report, bank-arrival trace | Gives finance audit-ready proof |

| Unknowns and escalation owner | Open gaps and who resolves them | Stops silent risk carryover |

If payout configuration or evidence is missing, keep that row blocked.

Define a reserve that protects refund capacity#

Treat reserve decisions as release controls, not preferences. Keep funds available for full or partial refunds and disputes before discretionary payouts. Do not assume a universal percentage unless your own history supports it.

Ground the policy in your money-flow authority. In GetYourGuide Supplier Terms (Version: 12 January 2026), the operator is described as collecting customer payments, transferring applicable payouts, and making full or partial refunds. Your policy should mirror that sequence and define who can act at each step.

Also treat supplier payment account details as a release gate. Incomplete account data is a payout-readiness risk, not a back-office cleanup item.

Add hard cutoff rules for refunds that arrive after payout#

These sources do not define a universal cutoff rule for post-payout refunds. Document decision points by money-movement stage and keep them visible to support and finance:

- Before payout release: process through your documented refund path and record the adjustment trail.

- During payout processing: treat intervention controls as account-specific until they are tested and evidenced.

- After payout completion: route to finance approval, link payout and refund records, and only apply offset recovery when your contract and process evidence explicitly support it.

Do not assume automatic future netting without evidence.

Plan for chargebacks without pretending you know the numbers#

Do not treat external dispute-automation claims as validated performance data for your policy.

Build the contingency around timing uncertainty across payouts, refunds, and order changes.

Your evidence pack should include traceable order-level history. Eventim's Summer 2025 update highlights audit-report visibility for delivery-method reissues and ticket swaps. That is the kind of audit trail you want linked to payout and refund records.

Include a late-exception path for fraud and compliance interruptions as well, since GetYourGuide terms explicitly allow contract conclusion rejection for those concerns.

For a broader platform-payment reference, Gruv Platform Payments maps global B2B payout and compliance requirements.

Step 5 Apply compliance and tax gates before money moves#

Use compliance and tax readiness as payout-release controls, but keep unsupported specifics explicit. Market-level KYC/KYB/AML triggers and W-8/W-9 requirements should stay marked as unknown until your compliance and tax owners confirm them for each market and entity.

Map the gates by market, not just by platform#

Build a market-by-entity gate matrix next to your settlement table so each control has an owner, timing, and current status. Do not assume one global trigger model for KYC, KYB, or AML. Keep unverified triggers and thresholds as open dependencies rather than guessed rules.

| Control point | Decide now | Record before release |

|---|---|---|

| Onboarding | Which compliance and tax checks are required for this market/entity | Current status, owner, and missing items |

| Payout-time check | Whether any completed checks must be revalidated before payout | Recheck result and unresolved holds |

| Threshold/change event | Which changes force re-review | Escalation owner and block/unblock state |

Separate tax setup from payout approval#

Treat tax setup as pre-release operational work, not month-end cleanup. A VAT report is a tax return on taxable transactions, and filing cadence can be monthly or quarterly depending on turnover and applicable regulatory requirements.

Before launch, confirm your transaction tax treatment and reporting configuration:

output taxtreatment on salesinput taxtreatment on purchased goods/services- tax-grid, or equivalent, mappings used to generate returns

- reminder and deadline setup for return submission

If tax mapping is wrong, payout flow may continue while reporting breaks later.

Use onboarding to set initial eligibility, then define re-check triggers#

Set onboarding as the point where base eligibility is established, then define when files must be reviewed again. For W-8/W-9, keep applicability explicitly unknown in this scope until your tax owner confirms whether they apply to the payee type, entity structure, and jurisdiction.

Also account for legal-availability risk. In regulated markets, operations can be blocked until a licensing regime exists or goes live. Treat that as a hard launch dependency, not a documentation follow-up.

If marketplace payout coverage is part of the shortlist, Payoneer Deep Dive gives a vendor-specific comparison point.

Step 6 Design the evidence pack finance needs at month-end#

Treat the month-end pack as a close gate. If a required record cannot be traced from source evidence, mark it unresolved and carry it forward. Build every record around one chain: request -> source record -> internal update -> export. If any link is missing, the action is not reconciled.

Standardize the pack before close#

Use one pack structure across entities and reporting scopes. At minimum, retain:

- internal request or case ID

- source record showing the state change

- internal posting/reference created from that record

- export row or report file finance reconciles

- exception log for unmatched, retried, reversed, or manually corrected items

Do not treat summary-level agreement as enough. If line-level records or links are missing or ambiguous, keep the item open in the exception log until the full chain is complete.

Add tax and reporting artifacts only where confirmed#

Include reporting artifacts only where your tax owner has confirmed they apply for that entity and scope.

For confirmed refund or payout scope, retain the operator-facing source your team actually validated. A vendor article such as the Ticketing.events refund guidance should sit next to the case evidence, not in someone's memory:

- order, registration, or attendee record tied to the action

- refund or payout path used in product, including whether it was automated or manual

- platform or processor reference captured after the action completes

- payout, balance, or ledger-facing impact visible to finance

- report row, audit log, or export file used for reconciliation

- exception note for partial refunds, retries, or manual corrections

Keep the approval trigger explicit in your controls. If the platform policy is non-refundable by default or only allows exceptions for cancellation or reschedule cases, record that rule next to the approval path before support acts.

If a refund, payout, or attendee record is corrected after close, retain the original reference and the replacement evidence so finance can follow the full change trail.

Before signoff, validate required fields in your submission artifacts and exports. If finance cannot pull the full chain for any sampled item from the report, keep it unresolved.

Related reading: AgriTech Platform Payments: How to Pay Farmers and Agricultural Workers in Emerging Markets.

Before launch, map your evidence flow to concrete API events and exports in one implementation pass: Read the Gruv docs.

Step 7 Implement integration controls that prevent duplicate or lost money movement#

Record each refund or payout intent once. Then make every retry resolve back to that same intent instead of creating a new money movement.

Persist the intent before you call out#

Keep providers behind one controlled gateway layer on your side, and store one record per refund or payout intent before any external call. Include the request key, internal case ID, payee or order ID, amount, currency, and status.

On retries, look up that same key first. Return the existing result, or a pending state, rather than sending a fresh movement.

This matters because blind retries can create duplicates. Reported timeout-retry failures have produced 15,000 duplicate orders, with customer and accounting impact.

Make asynchronous processing replay-safe#

Treat asynchronous gateway events as replayable inputs, not one-time commands. Track processed events by external event ID, and apply the ledger update once.

If the same event arrives again, acknowledge it and log it as a duplicate. If an event arrives before the related order, refund case, or payout batch exists, route it to an exception queue instead of auto-posting.

Monitor failure states that hide lost money#

Monitor these states continuously:

- repeated requests for the same order or seat that signal anomalous behavior

- delayed or missing gateway events that leave internal status stuck in pending

- payout or refund status drift where your ledger and provider final states do not match

Verification checkpoint: simulate retry and replay scenarios, then confirm one external movement, one ledger posting, and a clear audit trail that links duplicate attempts to the original intent.

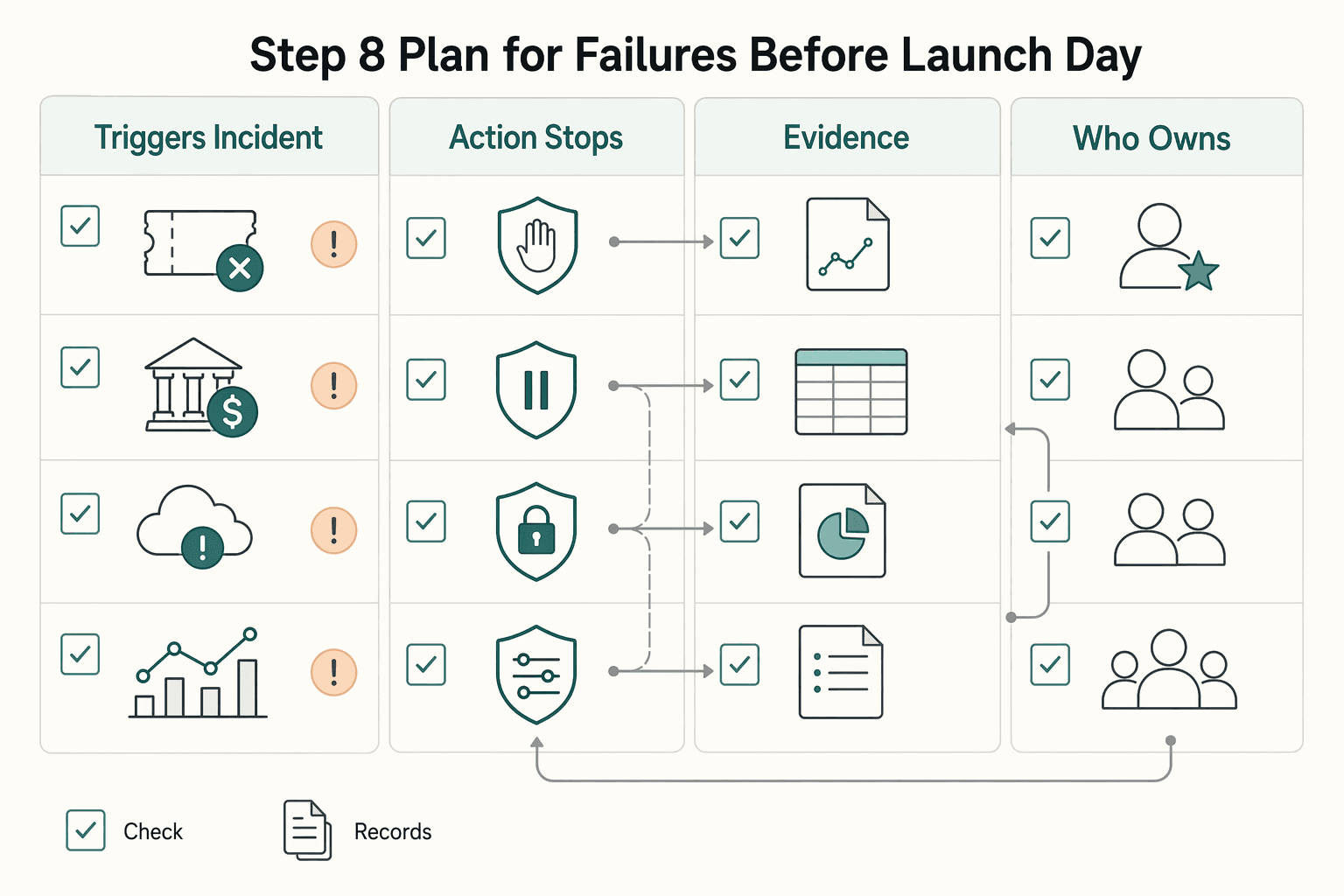

Step 8 Plan for failures before launch day#

Before go-live, write a short failure plan for refunds, payouts, and service interruptions so launch incidents do not turn into trust failures.

Keep each incident note operational. It should answer, in order:

- what triggers the incident label

- what action stops immediately

- what evidence is required first

- who owns the next business decision

- what confirms closure in your records

Treat evidence as a launch gate. If support, finance, and engineering cannot quickly assemble the same case record, for example order ID, action log, provider reference when available, and internal case ID, recovery can slow down when pressure is highest.

Set escalation expectations before launch, and keep the provider System status link and your internal dashboard where support starts triage. This matters even more when payout speed is short, including same-day payout setups, because the window to intervene can be smaller.

Maintain a known-issues register by market and payment provider. Log only observed behavior and open questions, not assumptions.

Run a cancellation drill under burst conditions, not just a happy path. Confirm the refund policy is published on the event page and that cancellations map to a traceable money outcome in finance review.

For a step-by-step walkthrough, see Gaming Platform Payments for Market Entry and Developer Payouts.

Step 9 Score vendors with operational criteria, not feature claims#

Use a weighted evidence scorecard, not a feature demo, to choose between Bevy, Eventbrite, and Ticketing.events. If a vendor cannot show how money moves, reverses, and appears in your records, treat that as operational risk.

Weight evidence quality as heavily as product capability. A polished UI should not outrank contract terms, reporting clarity, or proof that a refund can be traced to ledger-facing output.

Weight what breaks operations#

Score the controls that fail hardest under pressure:

| Criterion | What you need to see | Penalty trigger |

|---|---|---|

| Refund controllability | Exact refund path, actor permissions, and sample audit record | "Handled manually" with no record example |

| Payout governance | Who can release, pause, or redirect funds, and where that control lives | No documented approval path |

| Settlement transparency | Report or statement showing transaction-to-payout linkage | Undocumented timing or missing payout detail |

| Reconciliation traceability | One example from order to refund to ledger-facing export | No provider reference or export proof |

Penalize missing detail aggressively. If payout timing is undocumented, chargeback handling is only high-level, or support answers are vague, score down until the vendor provides concrete proof.

Ask for artifacts, not assurances#

In demos, ask for artifacts: a log export, a payout or settlement report, current terms, and one refund-to-ledger trace for a sample order. You should also confirm that support, finance, and implementation all label the same case with the same identifiers.

Include contract terms directly in the score. Clauses such as final-sale language, no-prior-notice policy changes, downstream-partner outage liability disclaimers, mandatory arbitration or class-action waiver terms, and termination terms are operating constraints, not legal footnotes. That includes a 10 business day without-cause notice where it applies, and some terms may allow immediate termination for breach. If terms are part of your control check, verify where the current version lives and whether update recency is visible.

Apply a hard go or no-go rule#

For your first expansion cohort, reject any vendor that cannot show required controls in writing or in product. "We support that market" is not enough without a demonstrable refund path, payout control point, and reporting evidence.

Conclusion and copy-paste launch checklist#

Do not mark a market launch-ready until you can prove how money is collected, refunded, held, and reported. In this workflow, evidence is the control point, not vendor confidence.

-

Choose one payout control model and assign owners. Pick

HQ-Led AccountsorChapter-Level Payouts, then assign accountable owners for payout release, refund approval, reserve decisions, and reconciliation signoff. Every team should be able to name who can pause payouts, who can authorize refunds, and who clears discrepancies. -

Build a country-gateway matrix and keep unknowns explicit. Use one row per launch market with

Stripe,Square,Worldpay,2Checkout,AliPay,PayU, andInstamojoas columns or options. Do not infer country coverage, refund behavior, or payout behavior from marketing copy. If proof is missing, leave it blank and assign an owner, validation method, and target date. -

Lock refund rules in writing, including cancellation-versus-refund handling. Define when support can act, when finance approval is required, and what evidence must be attached. Use governing terms: Eventbrite's Merchant Agreement (last updated March 10, 2025) includes Section 9 Fees, Deductions, and Reserves, Section 10 Payouts Before Your Event, and Section 11 Refunds, and says it controls over conflicting Terms of Service.

-

Finalize settlement exception handling before launch. Even if exact timing is still being validated, define what happens when a refund request comes after payout release or queueing. Document who can hold funds, who approves exceptions, and how support explains timing gaps between attendee status and cash movement.

-

Validate compliance dependencies per market. The evidence does not provide universal trigger thresholds (for example,

KYC/KYB/AML/VAT), so confirm requirements market by market with the vendor and your compliance owner. Do not release payouts without visible status for these gates. -

Run reconciliation tests with full evidence and one failure simulation per market. Require a trace from customer request to provider reference, internal record change, and month-end finance export. Include event-level identity, not just customer identity: in Auctria, all purchases require a Participant Record, missing records can be auto-created at checkout, and registration is event-specific.

-

Hold a go/no-go review based on proof, then launch the lowest-risk market first. Request agreement terms, report extracts, and one end-to-end trace. Eventbrite's footprint in nearly 180 countries shows reach, but not that your first market meets your refund, payout, and reconciliation requirements.

For legal-services style marketplaces, How to Launch a Legal Compliance Platform shows a different regulated payout launch path.

If your go/no-go scorecard is complete and you need country-specific payout and compliance confirmation for rollout, talk to Gruv.

Frequently Asked Questions

What is the real difference between refunding and deleting an attendee, and why does it change finance reporting?

Do not assume those actions are interchangeable. Require one report extract that shows both actions, the attached provider reference, and any payout-reporting impact. If a vendor cannot show that, treat attendee deletion as a reporting-risk action until finance signs off.

When should we use automated self-serve refunds versus manual gateway refunds?

Use self-serve refunds only when the platform can prove they produce the same audit trail and payout or settlement visibility as operator-handled refunds. If that proof is missing, keep refunds manual until you validate the path in a live or sandbox trace. Also confirm policy first. The Ticketing Co says tickets are non-refundable unless the event is cancelled or rescheduled.

How do `HQ-Led Accounts` and `Chapter-Level Payouts` change control, speed, and risk?

The sources do not establish a universal answer by vendor, so require each vendor to show exactly where funds land and who controls release and refunds. TixFox, for example, says ticket revenue goes directly to the organizer’s Stripe account and the organizer controls transfer timing. That is a different control model from a platform that holds funds first. Before you build around either model, confirm account owner, payout owner, and refund authority for the specific vendor setup.

Which criteria matter most when comparing event payment platforms for expansion markets?

Prioritize the criteria that change cash and support outcomes: refund policy, fund custody, and payout availability. A non-refundable-by-default policy, a direct-to-organizer Stripe flow, and a seven-day post-event availability model create materially different operating constraints. The practical comparison questions are who holds funds, when funds become available, and what payout reporting the platform provides.

What should we verify about settlement timing before committing engineering resources?

Verify the full sequence, not just a payout-frequency label. evvnt distinguishes these steps: funds become available seven (7) days after the event, frequency only controls disbursement cadence, and bank arrival is typically 2-5 business days after disbursement. Also verify weekend and bank-holiday handling, early-payout reserve behavior (up to 20% with release 7 days after the event), and whether the dashboard shows past and upcoming payouts.

Which unknowns are acceptable at pilot stage, and which are launch blockers?

At pilot stage, acceptable unknowns are tuning choices inside known rules, such as whether to use Nightly, Weekly, Fortnightly, or Monthly disbursement once funds are available. Launch blockers are unknowns that change customer promises or cash timing, including refundability, who holds funds, reserve withholding, and weekend or bank-holiday payout behavior. Another blocker is support ambiguity around duplicate charges versus temporary authorizations that may clear in a few business days.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 5 external sources outside the trusted-domain allowlist.

- congress.gov/crs-product/R48179trusted

- federalregister.gov/documents/2024/04/26/2024-07177/refunds-and-...trusted

- oabcc.delaware.gov/faqtrusted

- academy.auctria.com/participantsexternal

- clients.seetickets.us/hc/en-us/articles/6823260774683-Product-Upda...external

- eventbrite.com/help/en-us/articles/346993/eventbrite-mercha...external

- getyourguide.com/c/supplier-terms-and-conditionsexternal

- help.bevy.com/hc/en-us/articles/35197223216151-Managing-Pa...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: