Quick Answer

To pay CPAs and bookkeepers at scale, separate bookkeeping, CPA, and payroll work first, then build payout operations around clear records, compliance checkpoints, reconciliation, and exception ownership. Prepare a market evidence pack before coding, centralize approval policy and ledger controls, stage onboarding and tax collection, keep payout statuses traceable, and add batching when manual handling starts creating reconciliation risk.

Why paying CPAs and bookkeepers at scale is a different problem than picking accounting software#

Most guidance in this area focuses on bookkeeper-vs-CPA roles and when to hire each. Designing how you pay those roles repeatedly as volume grows is a different operations decision, not just a software choice.

Bookkeepers and CPAs do different work. A bookkeeper handles day-to-day records such as recording transactions, reconciling bank statements, and managing payables and receivables. A CPA is a licensed professional with broader tax and advisory scope. Payroll providers are different again, focused on paying employees and filing taxes. This guide covers the next layer: how your platform pays those roles repeatedly as volume grows.

When those decisions get mixed, the tradeoffs can get expensive. Paying a CPA $200/hour for routine transaction entry is one clear example of using the wrong role for the work.

The goal here is to help you make rollout decisions with clear checkpoints instead of shopping features in the abstract. Define success before you scale:

- clear role boundaries between bookkeeping, CPA, and payroll work

- routine transaction work assigned to bookkeeping, not CPA-level advisory capacity

- a repeatable way to pay each role as volume grows

Before you expand, pressure-test one question: are you consistently matching each task to the right role before you scale payment operations?

If you want a deeper dive, read Accounting Platform Payments: How Bookkeeping and Tax Platforms Pay Their Expert Network.

Where listicle advice stops being useful#

Use listicles as background, not as decision evidence. Most of the sampled results are built around visibility, hiring fit, or software shopping. That context is useful, but it is not direct evidence of payout-operations readiness.

Check what problem the source is actually solving#

Start by checking what problem the source is actually solving. In the sampled results, one source defines success as showing up on page one of Google. Another is a hiring guide about role choice and cost. Another leans on referral-driven local marketing. Useful context, but not evidence that your payout operations are ready.

A simple triage rule works well here: if you cannot quickly find operational detail tied to payout execution and controls, demote the source.

Separate table stakes from launch blockers#

Do not confuse table stakes with launch blockers. Feature coverage can support software selection, but on its own it does not prove operational readiness.

The sampled comparison content also spends most of its time on pricing bands and automation claims. That includes ranges from free (Wave) to $20/month for SMB tools and $20,000-100,000+/year for enterprise ERP. That helps with software budgeting. It does not tell you whether your payout operation is actually ready to run.

Move from listicles to operator evidence#

Move from listicles to operator evidence early. Use comparisons to map the surrounding finance stack, then make rollout decisions from direct operational evidence.

If a source does not help you verify operational readiness, keep it in research notes and out of the final rollout decision. Related reading: Mass Payments for Research Panels: How to Pay Survey Participants and Clinical Trial Subjects at Scale.

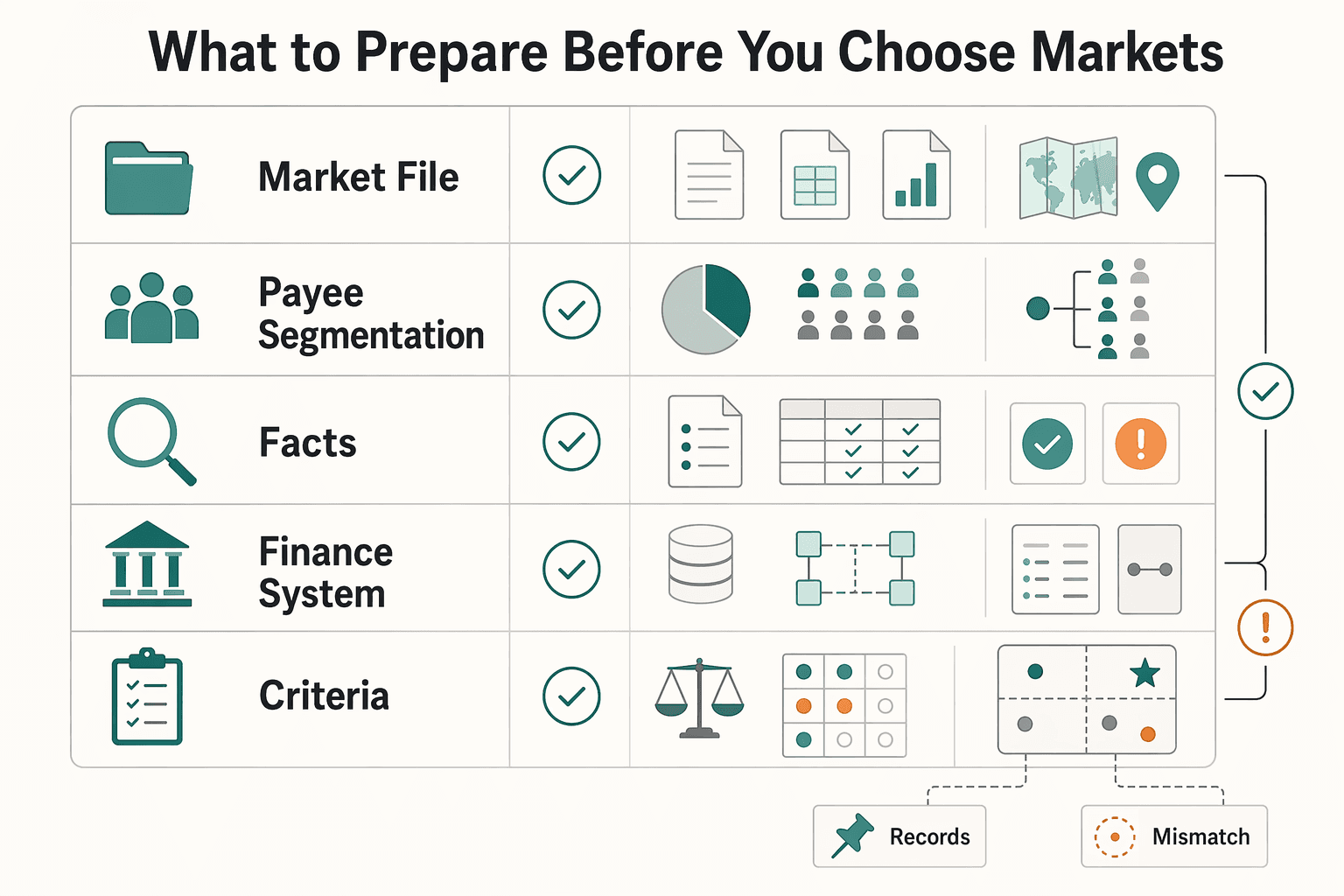

What to prepare before you choose markets#

Prepare a pre-build evidence pack for each target market before anyone starts coding. If a market does not have clear artifacts, open questions, and owners, treat it as not ready. Include a competitor map of at least five potential competitors before locking positioning or pricing.

| Prep area | What to capture | Launch note |

|---|---|---|

| Market file per target country | Current understanding of payout and compliance workflows; unresolved items labeled explicitly; owner assigned | If a market does not have clear artifacts, open questions, and owners, treat it as not ready |

| Payee segmentation | Payout size, payout frequency, expected split between invoice collection and disbursement; monthly payee count, payment cadence, individual-versus-entity mix | If these cannot be estimated, the market plan is too vague for a build decision |

| Tax artifacts | Request W-9s, track submissions, store signed forms by client; flag W-8 and VAT-related questions for tax or legal review | Manual threshold tracking gets harder as volume grows, and feature depth varies |

| Finance-system touchpoints | Source records, imports and exports, sync direction, data ownership; note whether a system creates payout instruction, creates ledger event, or stores tax and compliance evidence | This exposes gaps before rollout planning starts |

| Go or no-go criteria | Compliance checkpoints, reconciliation expectations, exception ownership | If ownership is unclear or critical artifacts are unresolved, keep that market out of the first launch wave |

Create one market file per target country#

Create one market file per target country, including unknowns. Track your current understanding of payout and compliance workflows, label unresolved items explicitly, and assign an owner.

Use a simple readiness view for each market: source of truth, open questions, and approver. Do not mark a market as launch-ready while key compliance or payout-handling decisions are still unresolved.

Segment payees before you segment markets#

Segment payees before you segment markets. Separate cohorts, then estimate payout size, payout frequency, and the expected split between invoice collection and disbursement.

Keep this operational, not just persona-based. If you cannot estimate monthly payee count, payment cadence, and the individual-versus-entity mix, the market plan is still too vague for a build decision.

Define tax artifacts early#

Define tax artifacts early. For US 1099 workflows, treat W-9 collection and tracking as a core capability: request W-9s, track submissions, and store signed forms by client.

As volume grows, manually tracking who crosses the $600 threshold gets harder in this context. For W-8 and VAT-related questions, flag them for tax or legal review and document what your current tooling actually covers, since feature depth varies.

Map current finance-system touchpoints#

Map current finance-system touchpoints so the handoff scope is explicit. If accounting, AP, or payout systems are already in your flow, document what each system does now: source records, imports and exports, sync direction, and data ownership.

A practical label set helps here: creates payout instruction, creates ledger event, or stores tax and compliance evidence. That will expose gaps before rollout planning starts.

Set go or no-go criteria before build starts#

Set go or no-go criteria before build starts. Define compliance checkpoints, reconciliation expectations, and exception ownership up front. If ownership is unclear or critical artifacts are unresolved, keep that market out of the first launch wave until those gaps are closed.

How to score market readiness before committing engineering#

Score readiness with an operations-first market scorecard, not a demand-first ranking. If compliance, payout handling, or reconciliation is still unclear, mark readiness as uncertain until those evidence gaps are closed.

Build one scorecard per market#

Build one scorecard per market from your evidence pack, and use fields that can delay launch. Start with explicit checkpoints such as compliance alignment, integration depth, implementation complexity, and exception handling and edge cases. Add a confidence column for each so unknowns stay visible.

Keep the scoring simple. A low/medium/high scale or a small point range is enough if each score has an owner and a short rationale.

Add operational load signals early#

Add operational load signals early, even if the estimates are directional. Track investigation workload and reconciliation effort where you have evidence, and mark payout-rate assumptions as unknown when evidence is missing.

Require evidence behind each assumption. If a value is based on an open question rather than test results, prior patterns, or a named finance estimate, mark it as unknown instead of scoring it optimistically.

Do not mistake market interest for readiness. Documented finance failure modes show that misreading operating signals can lead to overspending and cash flow crises, so keep exception data and reconciliation effort central in the decision.

Evaluate each market by launch shape#

Evaluate each market with a launch-shape dependency map, not just a country label. If you are considering payouts-only, VBAs plus payouts, or Merchant of Record, list what each option depends on in that market before you rank it.

For each option, confirm ownership and process coverage for onboarding and screening, payment execution, reconciliation, and evidence handling. Keep integration depth visible as a first-order cost. More side tools, manual exports, or disconnected records can increase implementation complexity and operating drag.

Produce a prioritized launch sequence#

Produce a prioritized launch sequence with explicit internal statuses. Status should follow score, confidence, and dependency closure, not revenue ambition alone.

If key risks remain unknown, consider a narrow pilot before broad rollout. Keep the pilot small enough for support, compliance, and finance to review real outcomes and close evidence gaps.

For any high-priority launch decision, require a named approver, a chosen launch shape, clear investigation and reconciliation owners, and no unresolved blockers on compliance alignment or core integrations. If those are missing, lower the launch priority. Related: Airline Delay Compensation Payments: How Aviation Platforms Disburse Refunds at Scale.

Choose the payout operating model for each market cluster#

For launchable markets, centralize approval policy and ledger controls first, then localize payout routing only where payment-method mix or market process requires it. This can help you avoid familiar AP and AR failure patterns such as inbox approvals, portal hopping, and disconnected spreadsheets.

Decide where control lives before execution#

Decide where control lives before execution. Set that first, then decide where execution lives.

| Decision area | Centralize first | Localize only when needed |

|---|---|---|

| Approval policy | Keep one policy owner so approvals stay consistent | Adapt handling only for market-specific exceptions |

| Ledger controls | Keep one accounting logic and reconciliation standard | Avoid splitting ledger logic by region unless a market constraint requires it |

| Payout routing | Start with shared routing rules | Localize when payment-method mix or market process requires it |

Capacity is often the real constraint. If the core team cannot clear holds, returns, and exceptions quickly, approvals can stall. Keep local ownership narrow to routing and market-specific exception handling, not separate approval rules or separate ledger outcomes.

Pick the simpler launch shape when evidence is thin#

Use MoR when it helps reduce operating complexity early. Use direct payout orchestration when you can reliably own the full execution and exception path. Neither model is universally better.

If your evidence still shows unclear failure handling, evidence ownership, or month-end close process, bias toward the simpler launch shape for that cluster. If you need tighter control of routing and provider behavior, direct orchestration can be the right choice, but only with clear finance and ops ownership.

Set a hard system boundary#

Set a hard system boundary: AP and AR plus core accounting own the payable or receivable record, approval state, and ledger outcome. The payout layer owns execution, provider references, status updates, and return or retry handling.

A practical checkpoint is AP or AR software linked to QBO or Xero so close operations do not turn into a fire drill. If both systems can independently define approval state or payout completion, finance and product may end up reconciling against different records.

Standardize operating artifacts before local exceptions#

Standardize operating artifacts before local exceptions. That reduces training friction and cuts down on misunderstandings as you scale across clusters. Use one shared artifact set across markets:

- approval matrix and escalation path

- reason codes for held, returned, and rejected payouts

- payout-method map by cluster

- reconciliation handoff fields across product, finance, and support

- evidence requirements for exception closure

Roll out changes in phases, not all at once. Start with one or two high-impact tools and expand only after the boundary between accounting and payout execution is working cleanly.

Design onboarding and compliance gates that do not break conversion#

Onboarding should gate payout activation behind clear internal checks and traceable records. That reduces risk without creating avoidable drop-off.

Collect only the data needed for the next decision#

Use staged progression: basic profile and entity data first, then internal verification checks, then payout method activation. This keeps you from collecting sensitive payout details before a payee is ready to move forward.

Treat state management as a control, not a UI detail. Distinguish states like profile created, verification in review, and payout-ready so partially screened payees do not leak into payout setup.

Collect tax profiles early and track them separately#

Start tax-profile collection during onboarding and track it separately from identity and compliance review. For W-9 workflows, keep the basics tight: request forms, track submission status, and store signed forms by client.

Define in policy and product when your 1099 workflow starts. If your process uses threshold tracking, the commonly tracked $600 example shows why manual tracking breaks down as payee volume grows.

Route risk signals into review queues#

Send higher-risk patterns into an enhanced review queue with a named owner. Avoid opaque holds that support and finance cannot explain.

Use explicit status states so users know what is happening, for example pending, approved, held, and action required.

Enforce payout readiness with complete compliance state and audit trace#

Set an internal payout-readiness rule that depends on a complete compliance state plus audit history. Keep source-linked import records, and log what changed over time rather than silently overwriting data.

For reconciliation readiness, capture posted timestamps on imported transactions so categorization and close workflows are defensible. Where onboarding depends on external connectors, account for reliability differences between API-aggregator and SFTP methods before marking a payee payout-ready.

Execute payouts with idempotent controls and observable status states#

The practical goal at execution time is simple: keep the payout process traceable from payment action to bank reconciliation, so operations and finance can explain what happened without guesswork.

The source-backed signal here is narrow but useful: keep payments, reconciliation, and reporting connected in the same accounting workflow. When records fragment across tools, payout handling and reconciliation can drift apart.

Use clear workflow labels and notes so teams can explain payment outcomes without manual detective work.

If key execution details are incomplete, treat the payout record as needing review before final reporting. Keep payout records reconciliation-ready so cleanup work does not compound, especially when pressure is highest near year-end.

Add payout batches when manual operations start creating risk#

Move from one-by-one payout handling to controlled batches when manual work starts creating reconciliation risk, not just when the team feels busy. The clearest trigger is repeated evidence that volume and tool complexity are outpacing your ability to explain transaction status and close cleanly. Use a short risk check from recent cycles:

| Risk signal | Grounded example | What it suggests |

|---|---|---|

| Status blind spots | Payout or transaction status is unclear without checking multiple systems | Volume and tool complexity are outpacing your ability to explain transaction status and close cleanly |

| Close impact | Unreconciled items are carrying into close, especially after migration or tooling changes | Set an internal switch point tied to your reconciliation process |

| Volume step-up | Work that was manageable at around 200 transactions/month no longer keeps up near 800 | Batching may be worth adopting if missed items, status blind spots, and close delays keep recurring |

| Long-lived unresolved items | Unresolved items are persisting for months, not days | Stop a temporary lag from turning into an entrenched backlog |

Set an internal switch point tied to your reconciliation process, then apply it consistently. The point is to stop a temporary lag from turning into an entrenched backlog, including months of unreconciled transactions.

If the recurring risk is missed items, status blind spots, and close delays, batching may be worth adopting. If your payout set is mostly one-off exceptions, keep case-by-case handling where needed.

Before you scale batch volume, make reconciliation ownership and records clear so finance can still trace and close with confidence:

- assign clear reconciliation ownership when multiple tools feed the books

- track and resolve migration-related data gaps instead of carrying them forward

- keep one traceable record per batch and attach exceptions to it

If payout data, provider updates, and ledger records live in different tools, anchor reconciliation to one record so period-close explanations stay defensible.

Reconcile fast with an audit trail finance can defend#

In batch operations, treat reconciliation as a traceability job. Finance should be able to move from a payout outcome back to the original request without guesswork.

Step 1. Map the chain from request to settlement. Start with a current-state workflow map before you add more tooling. For each payout, keep core identifiers linked end to end, for example request ID, batch ID, provider reference, payout status, settlement record, and ledger journal reference. If a payment cannot be traced clearly, period close gets harder at scale.

Test this on one settled payout and one failed or held payout. You should be able to explain the full path and final financial outcome without relying on inbox searches or memory.

Step 2. Define one retrieval-ready evidence pack. Set the evidence pack before audit pressure starts. Keep it tied to the payout or batch anchor record, with the provider reference, status history, and any internal review artifacts your program uses.

The goal is one lookup, not reconstruction across chat, email, and screenshots. A complete pack makes the reconciliation story easier to defend under deadline.

Step 3. Give each tool one clear role and integrate deliberately. If you use multiple systems, define exactly which record each system owns and what passes downstream. Each tool should serve a specific purpose and integrate cleanly. Otherwise, you can end up with conflicting statuses and duplicate edits.

Roll out in phases, not all at once. Application sprawl can become a control risk. Add one or two high-impact integrations, then verify results before expanding.

Step 4. Use an internal exception-close checkpoint. Before period close, set an internal checkpoint so each exception has a reason, a clear owner, and a closure note in your process. This helps keep temporary exceptions from turning into a permanent reconciling bucket. Use close metrics to confirm it is working: closing speed, time savings, and error reduction.

Common failure modes and how to recover without a full rollback#

A full rollback is not always necessary when one control fails. Isolate the failure mode, narrow the impact, and resume only when your records are consistent.

Separate document defects from verification issues#

When a payee is blocked, first distinguish a document-quality defect from missing or unresolved verification details. Keep corrected documents in the same client record, and log the original mismatch, what was replaced, and the final review decision.

Your checkpoint is one record that clearly shows request status, submission status, and outcome. If fixes live across email and screenshots, tracking can drift.

Treat clustered issues as a local signal#

If issues cluster in one segment, investigate that cluster first instead of treating it as a platform-wide failure. Review cases from the same tracking record so each one is traceable and comparable.

Focus on patterns you can verify from recorded outcomes and document-status details. Resume broader volume only after the pattern stops repeating in reviewed cases.

Close tax-document gaps before volume gets ahead#

Late tax-document gaps are an operational risk as volume grows. In 1099 workflows, scale gets harder once teams are managing many vendors, W-9 collection, and who crosses the $600 threshold.

Use per-client tracking that shows requested W-9s, who submitted them, and stored signed forms. At that volume, software-based workflow tracking is the practical way to reduce manual work and keep compliance processes organized.

Validate workflow records before raising throughput#

When records drift, treat it as a control-check issue before increasing throughput. Confirm one case end to end and make sure request history, document status, and outcome tell one consistent story.

If one case cannot be explained cleanly from system records, keep throughput changes on hold while you resolve the inconsistency. For a step-by-step walkthrough, see Gaming Platform Payments: How to Pay Game Developers Studios and Tournament Players at Scale.

Copy and use this launch checklist for the first rollout wave#

For the first wave, launch only what you can verify from records with clear history, not from setup notes alone.

Sequence the wave with a dated checklist#

Use a checklist cadence to stage readiness and evidence collection: 6-8 weeks before, 3-4 weeks before, Week 1 after, and Week 2 after. This keeps launch work scoped and reviewable instead of ad hoc.

Document connector choices and expected behavior#

If you import financial data, document whether each flow uses API aggregators or SFTP. Treat that as an explicit tradeoff decision, then verify outcomes from actual records before scaling volume.

Require audit-ready history on imported data#

Confirm imported records retain source details and logged changes. If changes are not traceable in-system, treat the control as not ready for rollout.

Reconcile balance-sheet accounts first#

Run reconciliation as a distinct checklist activity and prioritize balance-sheet accounts first. Confirm outputs map cleanly to your chart of accounts so finance can review and export consistently.

Close the wave with review, corrections, and a final reporting package#

End the first wave with a formal review-and-corrections pass, then produce a final reporting package. That gives you a consistent, repeatable baseline for the next rollout wave.

Before your first rollout wave, pressure-test your controls checklist against Gruv Payouts for idempotent retries, status visibility, and batch workflows where enabled.

Make expansion decisions from operations, not feature lists#

Launch based on operating control, not software comparisons. A feature list can help with tool selection, but it is not proof that a market is ready to run.

Set the go or no-go bar around predictable records#

Accounting software replaces manual spreadsheets and paper ledgers with automated recording, categorization, and reporting. That is necessary infrastructure, but software choice alone is not an expansion decision.

Use a stricter bar: records stay current, data stays trustworthy, and bank reconciliation works in normal operations. If your team cannot consistently match internal records to bank statements to catch errors, expansion is likely premature. Poor tool and process choices can lead to rework, wasted spend, and data people stop trusting.

Roll out in phases with explicit checkpoints#

Use phased rollout with explicit checkpoints, rather than a broad launch driven by generic comparisons of top platforms:

- Require current sync. Prefer real-time or daily syncing; avoid delayed batch uploads that leave record gaps.

- Verify reconciliation behavior. Confirm internal records can be matched to bank statements consistently enough to catch errors.

- Check for workaround load. If teams still rely on frequent workarounds to close gaps, do not scale yet.

This tradeoff can mean fewer launches now and less cleanup later. The key question is not which tool has the longest feature list, but whether the market can run with records that stay accurate, current, and reviewable.

Validate one target market before expanding#

Start with one target market and run it through the scorecard and checklist from earlier sections. Expand only after one clean operating cycle shows that records stayed current, reconciliation worked, and the team did not depend on heavy workaround effort.

If any checkpoint fails, pause expansion, fix the gap, and rerun the same market before opening another. Expansion should follow operational proof, not feature-list comparisons.

If you are validating one pilot market before broader expansion, use the docs to map requirements to your operating model.

Frequently Asked Questions

What is the difference between accounting software and a payout platform for CPA and Bookkeeper networks?

Accounting software supports core accounting workflows like invoicing, billing, expense and time tracking, inventory, project accounting, transaction classification, and reconciliation. A payout platform handles how your network pays CPAs and bookkeepers repeatedly as volume grows. Software coverage alone is not evidence that payout operations are ready.

What are the minimum capabilities required before paying experts across multiple countries?

At minimum, records should stay current, bank, credit card, and loan balances should reconcile to accounting software, and transactions should be classified correctly. If those controls are not consistently visible in real records, multi-country payout readiness is not established.

What should we evaluate before entering a new market for payouts?

Before entering a new market, create a market file, segment payees, define tax artifacts, map finance-system steps, and set explicit go or no-go criteria. If compliance, payout handling, reconciliation expectations, ownership, or critical artifacts are still unresolved, keep that market out of the first launch wave.

When should we switch from single payouts to payout batches?

Switch to payout batches when manual one-by-one handling starts creating reconciliation risk, not just when the team feels busy. Common signals are status blind spots across systems, unreconciled items carrying into close, recurring close delays, and unresolved items lasting for months. Set an internal switch point tied to your reconciliation process and apply it consistently.

What are the most common failure points when scaling payouts to CPAs and bookkeepers?

The most common failure points are records-control gaps such as unreconciled balances, misclassified transactions, stale books, and fragmented records across tools. Other recurring problems include unclear service scope, late tax-document gaps, and workflow records that cannot explain a case end to end. Those gaps weaken discrepancy detection, audit readiness, and month-end close.

How should we prioritize rollout order across countries and vertical segments?

Prioritize rollout order with an operations-first market scorecard, not revenue ambition or generic country rankings. Put launchable markets first when compliance alignment, integration depth, implementation complexity, exception handling, confidence, and ownership are clear. If key risks are still unknown, use a narrow pilot before a broader rollout.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- clame.nyu.edu/HomePages/E09H7E/312588/Wave%20Accounting%20...trusted

- courses.cs.duke.edu/spring17/compsci101/lects/170418/sec02/words...trusted

- cs.cornell.edu/courses/cs1132/2015fa/assignment2/randPermDi...trusted

- occ.gov/publications-and-resources/publications/comp...trusted

- onlinetraining.pct.edu/training-programs/bookkeeping-certificationtrusted

- op.nysed.gov/sites/op/files/2023-01/Public_Packet_Jan2023...trusted

- articsledge.com/post/ai-accounting-toolsexternal

- arxiv.org/pdf/1411.4633external

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: