Quick Answer

Start by deciding whether your real constraint is expert access or payout execution. Use research-first networks for market insight, but do not approve launch until onboarding, payout visibility, and reconciliation evidence are all proven for the markets you plan to enter.

Expert-Access Strength Is Not the Same as Payout-Operability Readiness#

If you are expanding an accounting or tax platform into new markets, decide your bottleneck first: expert access, payout execution, or both. That is the right lens for this accounting platform payments expert network guide, because sourcing readiness is not the same as launch readiness once cross-border payout and reporting requirements show up.

A lot of the confusion comes from category mismatch. GLG describes an expert network as a way to connect clients with subject-matter experts for calls, events, and surveys, while AlphaSights positions its model as knowledge on demand. Those models can help with decision support, but they do not by themselves prove launch execution across target markets, including payouts and day-to-day operations.

- Buy for the bottleneck first

Start with the business reason for adding payments or expanding markets, then match the vendor category to that reason. Stripe’s platform-payments guidance makes that sequence explicit and says its recommendations were informed by interviews with 14 successful platforms.

- Defer bundled promises until the operating gap is clear

If your immediate need is expert access, research-oriented providers may belong on the shortlist. GLG says it has made accessing experts easy for over 25 years, and Third Bridge positions itself around expert insights and research for decision support. If your immediate constraint is execution, prioritize payment orchestration or global payouts, because programmatic payouts can reach more than 50 countries while payment method availability still varies by region.

- Verify launch evidence before you spend GTM budget

Use market-by-market checks before rollout, including payout method availability and whether your model triggers platform-operator reporting duties such as OECD MRDP rules. The risk is operational, not theoretical. On 12 December 2024, the Financial Stability Board said cross-border regulatory inconsistencies can create complex compliance processes, raise costs, and reduce processing speed. If critical evidence is missing, pause the launch.

One middle category matters too. Tools positioned closer to operations than pure research access can change the buying motion. ExpertNetPro, for example, says its platform is built to manage client requests, expert sourcing, compliance, and payments in one product. That changes the question from "Can this vendor find experts?" to "Can this product support the day-to-day model we need?"

The goal of this list is practical selection and launch discipline: what to buy first, what to defer, and what proof you need before rollout. Treat every "global" or "full-service" claim as a hypothesis until market-specific evidence confirms it.

Selection criteria and fit for this list#

Use this list when you are choosing across expert access, operating software, payment rails, or a modular mix, and you need evidence that payouts and reconciliation are covered at launch.

- You are a cross-category buyer

This section fits if you are comparing GLG, AlphaSights, ExpertNetPro, Paro, BlueSnap, or a stack that adds payout operations and accounting workflows. GLG describes expert interactions such as calls, events, and surveys, while AlphaSights describes project-based expert recruitment and says it has operated since 2008. The core distinction is simple: expert matching and payout execution can be different capabilities.

- You operate finance talent networks

Keep reading if your network includes finance and accounting or CPA talent and you need country-aware controls, not just introductions. Paro says it connects businesses with vetted finance and accounting talent and lists solutions for CPA firms. ExpertNetPro says its scope includes client requests, expert sourcing, compliance, and payments. If ownership of onboarding and payment handling is unclear, the operating layer may still be incomplete.

- Geography and payout mechanics can block rollout

BlueSnap is relevant when payout execution is your bottleneck, but only if its footprint fits your markets. It states Marketplace availability is limited to Israel, the United Kingdom, and the European Union with proper approvals, and payout methods vary by country. It also states default payout timing of Daily +2 business days and support for 14 payout currencies. Ask for a country-by-country payout-method matrix for your actual expert locations.

- Reconciliation is a launch requirement

A modular stack with an accounting system can be the practical choice when no single vendor proves the full flow. Cornell's reconciliation guidance describes the same core control: check whether bank balances and accounting balances match and identify errors when they do not. Ask for sample outputs, field mapping, and exception handling evidence rather than accepting a generic "ready" claim.

Category map and what each option is actually for#

Separate expert access from payout operations first, then judge depth inside each lane. That one step can prevent common buying mistakes in this market.

- GLG, AlphaSights, Tegus, Third Bridge, and CleverX are expert-access products first

Their documented positioning is access to experts, consultations, transcripts, research inputs, or participant recruitment, not a full payout system. GLG highlights one-on-one expert calls and reports a network of approximately 1.2 million experts, founded 1998. AlphaSights positions around expert-insight access and launched in 2008. Tegus centers expert transcripts, calls, and financial models and is now part of AlphaSense. Third Bridge focuses on expert insights, consultations, and a research library. CleverX describes a marketplace for recruiting business research participants.

Practical check: if ownership of payee onboarding, payout status, failed-payment handling, and reconciliation is unclear, you likely still need an operating layer.

- Payments Consulting Network and BlueSnap are payments-adjacent, but in different ways

Payments Consulting Network is advisory, covering strategy, market analysis, benchmarking, pricing tools, and RFP/RFI support, and reports presence in 17 cities and 14 countries. BlueSnap is embedded payments infrastructure, including onboarding, underwriting, compliance, reporting, and payment orchestration through a single integration.

Both can shape or enable payments, but neither automatically replaces your internal finance-ops model for expert payouts.

-

ExpertNetPro and Paro are closer to talent-network operations, but payments scope still needs validation

-

Use this decision filter when launch controls matter

If day-one success depends on owned payout controls and reconciliation, consider prioritizing the operating or payments layer before optimizing sourcing breadth. Before signing, require clear evidence of payee status tracking, failed-payment handling, and finance-review reporting outputs.

For a step-by-step walkthrough, see Choosing Value Pricing for Accounting and Bookkeeping Services.

Best options comparison for accounting platform payments teams#

For finance-ops-led teams, the decision starts with category fit. Research-first expert networks are not the same as payout execution platforms. In this set, GLG, AlphaSights, Tegus, Third Bridge, and CleverX are expert-access first. BlueSnap is payments infrastructure. ExpertNetPro and Paro are closer to operations and talent workflows. Payments Consulting Network is advisory.

| Option | Best for | Payment-ops depth | Compliance evidence | Integration readiness (accounting sync and ledger export fit) | Geographic coverage claims | Not for | Key unknowns to validate |

|---|---|---|---|---|---|---|---|

| GLG | Expert access (calls, surveys, events); over 25 years positioning | Low. Evidence supports expert compensation flow, not a dedicated payout-control layer | Not publicly documented | Not publicly documented | No concrete geography figure retrieved here | Teams needing owned CPA payout execution, retries, and reconciliation | Pricing model, payee status visibility, failed-payment handling, export/reporting outputs |

| AlphaSights | High-touch expert sourcing via custom search model; launched 2008 | Low / unknown. No retrieved payout-control or reconciliation evidence | No payment-operations proof retrieved | Not publicly documented | No concrete geography figure retrieved here | Teams that need payout rails more than expert discovery | Compensation mechanics, integration depth, finance review outputs, pricing |

| Tegus | Expert access (now part of AlphaSense) | Low / unknown. No retrieved payout-ops evidence | Not publicly documented | Not publicly documented | No concrete geography figure retrieved here | CPA network payout execution or accounting-close support | Pricing, compensation process, payout ownership, reconciliation evidence |

| Third Bridge | Expert insights and research for investors/business leaders | Low. Strong research/compliance positioning, limited payout evidence | Clear expert-call compliance/risk-management claim | Not publicly documented | 12 offices; 1.5 million expert relationships | Teams needing one vendor to source and pay accounting experts end to end | Payment mechanics, payee onboarding detail, reconciliation, pricing |

| CleverX | Marketplace-style expert/participant recruitment with subscription and pay-as-you-go options | Low / unknown. Pricing is documented; payout execution is not | Not publicly documented | Calendar/video integration evidence only; no accounting-sync or ledger evidence retrieved | No concrete geography figure retrieved here | Finance teams needing payout controls, exception handling, and close evidence | Expert payment flow, ledger export depth, finance reporting, contract economics |

| ExpertNetPro | Expert-network operators wanting sourcing, compliance, and payments in one product | Medium, vendor-asserted | Vendor self-description only; no independent validation retrieved | Not publicly documented | No concrete geography figure retrieved here | Buyers needing independently validated payout readiness today | Payout rails, retry logic, reporting fields, pricing, country constraints |

| Paro | Businesses/accounting firms matching with finance experts | Medium / unknown. Closer to talent operations than research networks, but payout depth is unclear | Not publicly documented | Claims sync with QuickBooks, Xero, and other tools | No concrete geography figure retrieved here | Teams assuming accounting sync alone proves payout/reconciliation readiness | Payout methods, failure handling, pricing, market coverage, finance audit trail |

| BlueSnap | Payments infrastructure with single integration/account model | High for infrastructure. Payment orchestration positioning, merchant-configured payout method, 16 payout currencies | Not publicly documented | Documented accounting-platform partner integration; ledger export depth unknown | Accept payments in over 200 regions with 100+ currencies; 16 payout currencies | Teams that also need expert sourcing or CPA recruiting | Custom pricing mechanics, payout exception ownership, ledger fields, onboarding effort |

| Payments Consulting Network | Advisory, benchmarking, strategy, and vendor selection | None for execution. Advisory, not payout rails | Independent/vendor-agnostic consulting claim, not ops controls | Not publicly documented | Presence in 17 cities and 14 countries; established 2013 | Teams expecting direct payout processing, expert sourcing, or built-in reconciliation | Deliverables, pricing, implementation ownership, how advice maps to your stack |

Where most teams should start#

Start by deciding whether your immediate constraint is expert supply or payout execution. If it is supply, shortlist GLG, AlphaSights, Third Bridge, Tegus, or CleverX and assume you still need a payments layer. If it is payout execution, BlueSnap is the clearest payments-specific option in this evidence set. ExpertNetPro and Paro are closer operational fits that need deeper validation.

Treat accounting-system connectivity as an initial filter, not final proof of month-end readiness. In this set, only Paro and BlueSnap explicitly claim that connectivity. Ask for evidence of export fields and payout-status handling before treating those claims as launch-ready.

Most procurement misses here are category errors: buying a research-first option and discovering payout ownership gaps, or buying infrastructure or advisory and assuming expert sourcing is included. Before final selection, require concrete proof of payout status tracking, failed-payment resolution flow, and ledger-ready output for your target operating flow.

Best choices when expert quality and coverage come first#

When expert access quality and coverage are the priority, treat these as research and diligence options first, not payout operations systems.

- GLG

Consider GLG when enterprise breadth and familiarity are the main filter. GLG was founded in 1998, reports a network of approximately 1.2 million, and says its clients span consulting, private equity, asset management, banks, law firms, and other large enterprise segments. It also describes direct expert interactions, mostly calls, as its core offering, which can be useful for validating a new tax advisory or accounting niche before building heavier payout infrastructure. In the reviewed evidence, payout status tracking, failed-payment handling, and reconciliation outputs are not proven.

- AlphaSights

This is a strong comparison if you want a curated sourcing model for institutional buyers. The firm says it has served top investment funds, consultancies, and businesses for over 17 years and launched in 2008. It also says it does not operate as a sign-up "network," which points to a more curated model than an open directory. The tradeoff is similar to GLG: strong expert discovery, unclear payout execution evidence.

- Third Bridge

Third Bridge is a fit when you want both live expert calls and a deep research library. It describes expert calls as direct conversations, says its library covers over 65,000 companies, and highlights 100,000+ expert transcripts. That may reduce live-call volume during early vertical validation, but transcript and call depth do not document payout and reconciliation operations by themselves.

- Tegus

Tegus is most relevant when transcript-led research is the priority. Tegus states its expert transcripts, expert calls, and financial models are now part of AlphaSense, and its compliance page cites over 260,000 transcripts across 27,000+ public and private companies. That supports research depth, not a verified payout-control layer for accounting platform operations.

- CleverX

CleverX is worth evaluating when you want access to subject-matter experts. Its materials describe expert networks as connecting decision-makers with experts who have deep domain knowledge. Use it as an expert-access option, and verify coverage for your exact profiles before treating it as a broad-coverage answer. In the reviewed evidence, payout depth remains unproven.

Use this shortlist to test expert quality, coverage, and diligence speed. Do not treat expert-network strength as proof of payout launch readiness. Confirm who pays experts, how payment failures are handled, and what finance-ready reconciliation outputs are provided.

We covered this in detail in Best Accounting and Tax Advisors for U.S. Expats: Pick the Right Support Level.

Best choices when you need expert network operations plus workflows#

If you need a platform that combines expert access with operational workflow tools, start with ExpertNetPro and Paro. Based on the evidence here, they are more operations-oriented than GLG and Tegus, whose documented strengths are expert interactions, calls, and transcript-led research. This section does not establish either platform as proven end-to-end payout infrastructure across markets.

- ExpertNetPro

ExpertNetPro is a strong first review when you want software described as purpose-built for expert network companies, with sourcing, workflows, scheduling, compliance, messaging, invoicing, payments, and analytics in one platform. Its published pricing is concrete enough for early qualification: $36/user/month annually (minimum 25 users) and $45/user/month annually (minimum 50 users).

Validate payout readiness before treating it as launch-ready. Country-specific payout coverage, native accounting sync including Xero, and finance-grade reconciliation and exception handling are not proven.

- Paro

Paro is directly relevant for finance and accounting talent supply, with claims of 1000+ finance and accounting experts, 60+ industries, 250+ skill sets, and 50-state coverage. It also presents formal vetting steps, background checks, onboarding support, and a practice-management platform positioned to replace multiple tools.

The remaining risk is proof depth on payments and finance ops. In this evidence, practice management and vetting are clear, but payout rails, retry behavior, and reconciliation outputs are not confirmed for market-by-market rollout.

If your model depends on CPA onboarding, assignment flow, and payment-adjacent operations in one place, these are sensible first demos. Keep the shortlist tight until each vendor can show the exact workflow and controls your launch requires.

Best choices when payment rails and control are the core bottleneck#

If sourcing already works, do not try to fix payout and reconciliation problems by adding another expert network. Prioritize BlueSnap as a payment-execution candidate and Payments Consulting Network as an advisory layer, then compare both with an internal build path.

That is a different buying motion from the previous section. Paro or CleverX can support talent access and research workflows, but payout controls, payout timing, and ledger traceability are a separate operations problem.

BlueSnap#

BlueSnap is a strong first review when you need a payments operating layer, not more expert access. Its published model is specific: one integration, one contract and one account, and it describes global payment orchestration and payment processing in a single solution.

Its main advantage is control scope. The company says services can be configured by country, by product, by issuer and more, which is directly relevant when payout and acceptance rules vary across markets or service lines. That is a different capability from AlphaSights’ knowledge-on-demand model or Third Bridge’s expert-insight model.

Treat implementation claims as test items, not assumptions. The provider says funds go to the payout method configured in the Merchant Portal, and that payout outcomes depend on your commercial terms. Validate exact contract terms before launch.

Also resolve the documentation mismatch early. One support page references 14 payout currencies, while a FAQ references 16 payout currencies. Confirm what is current for your contract and target markets.

For accounting operations, the vendor’s Xero claim should be validated with live evidence. It says it bidirectionally syncs with Xero for reconciliation and reporting. Ask to see mapping behavior, exception handling, and reconciliation outputs in a realistic flow. Related read: Xero Integration for Payout Platforms: How to Sync Contractor Payments with Your Accounting System.

Include ownership diligence in your review. Payroc announced a definitive agreement on July 31, 2025, and announced completion on October 9, 2025. Confirm any implications for support, roadmap, and contracting.

Payments Consulting Network#

Payments Consulting Network fits advisory needs, not payout-rail execution. In this evidence set, it is presented as merchant advisory and as a firm providing strategic advisory and market research since 2013.

That makes it useful when you need an independent architecture and vendor-selection lens before committing. It states it gives independent advice and receives no commercial benefit from referred providers, and it claims presence in 17 cities and 14 countries.

The tradeoff is straightforward: advisory can improve decision quality, but it does not replace execution ownership. Use it to sharpen vendor criteria, reconciliation design expectations, and rollout checkpoints, then verify who owns delivery in production.

If payment control is your bottleneck, use BlueSnap to test an operating layer. Use Payments Consulting Network for independent architecture pressure-testing. Keep internal build as a live option until ownership, reconciliation flow, and commercial terms are clear.

Related: Accounting and Bookkeeping Platform Payments: How to Pay CPAs and Bookkeepers at Scale.

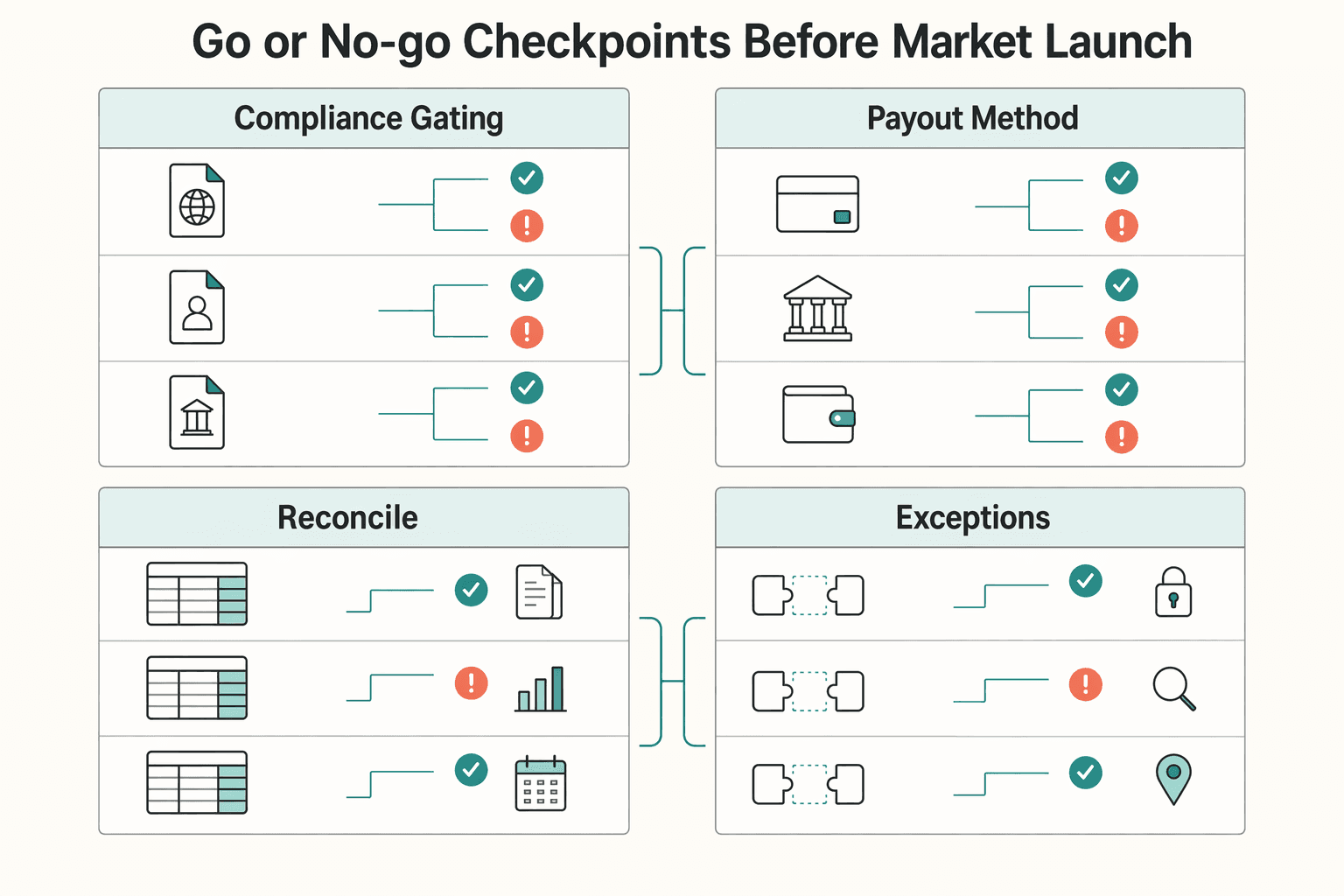

Go or no-go checkpoints before market launch#

Treat launch as a market-by-market proof decision. If critical proofs are missing for a country, keep that market in no-go, even if sourcing coverage (for example, GLG or AlphaSights) is strong. Use one checkpoint table per target market to separate sourcing confidence from payout-operability evidence.

| Checkpoint | What you verify for that market | Minimum proof artifact | No-go sign |

|---|---|---|---|

| Compliance gating | KYC/onboarding requirements for your CPA payout flow by location, business type, and capabilities | Written policy/onboarding requirements showing country-specific eligibility rules | Rules are only explained verbally or with a generic global checklist |

| Payout method availability | Whether your required route is actually supported in that country (send/receive/withdraw path) | Country feature/support documentation for the exact payout path | Vendor claims coverage but cannot map your country and method to a supported route |

| Reconciliation path | How each bank payout maps back to the underlying transaction batch and finance review flow | Sample payout reconciliation report output your accounting process will use | Only aggregate payout totals are available, with no transaction-level traceability |

| Exception handling | Event and status visibility, plus incident ownership when payouts fail or stall | Webhook/event payload examples, status fields, and support escalation contacts | No usable event contract, unclear status visibility, or unclear escalation ownership |

- Confirm compliance gating before anything else.

Payout enablement depends on onboarding and KYC completion, and required verification data changes by location, business type, and requested capabilities. That means your checklist cannot be one global template.

- Validate payout feasibility at country level, not brand level.

Country support can be tiered, for example 4 levels in one documented payout model, and cross-border support can be region-limited. Where cross-border applies, confirm both support boundaries and cost impact, for example 0.25% in one documented model, before approval.

- Require reconciliation evidence that supports close, not just operations monitoring.

The launch bar is the ability to reconcile each payout to the transaction batch it settles, then carry that into your finance review process. If reconciliation cannot reach your ledger workflow cleanly, treat that as no-go.

- Treat webhook and escalation evidence as mandatory launch artifacts.

Ask for real event payload samples and documented support paths so failures are diagnosable and owned. For BlueSnap checks, verify payout-status webhook coverage and confirm commercial constraints such as default payout timing (Daily +2 business days) and payout currency scope (16 payout currencies) against your target markets.

This pairs well with our guide on Deferred Revenue Accounting for Client Prepayments.

Before approving a new market, align your checklist to payout policy gates, failure handling, and reconciliation evidence with this payouts overview.

90-day rollout sequence for finance ops and product teams#

Use this 90-day sequence as a controlled rollout plan, not a universal standard: prove one market end to end before adding another.

- Days 1-30: lock the operating model and assign owners.

Choose the primary operating surface, ExpertNetPro, Paro, or BlueSnap, and add expert-insight networks only if you need deeper sourcing. Keep scope explicit: ExpertNetPro presents sourcing, compliance, and payments in one surface; Paro claims sync with Xero; and BlueSnap may fit best when payout execution and reporting are the constraint.

Make ownership explicit across product, finance ops, and compliance before the pilot starts. Stripe’s launch guidance frames this as cross-functional work, including staffing, risk, and success definition, and warns that deeper control usually means owning onboarding, underwriting, dispute management, compliance, support, and reporting workflows.

Exit this phase with a one-page responsibility map and a vendor proof-pack request list. Include pilot onboarding requirements, payout-status event samples, payout-detail exports, and the accounting fields finance will reconcile.

- Days 31-60: run one pilot market with a narrow expert cohort.

Keep the pilot narrow on purpose: one market, one bank route, and a limited CPA or tax specialist cohort. The goal is traceability, not volume.

Validate invoice-to-payout lineage with real artifacts. For BlueSnap, test payout detail output and whether records connect through Payment ID and Invoice ID for transaction-level reconciliation. For Paro, treat "Xero sync" as a hypothesis until you verify real pilot exports and statement-line mapping.

Use Xero as a hard gate. Reconciliation is matching statement lines to existing transactions, and the Bank Reconciliation report pack should show that bank balances and Xero balances match. Pilot exit evidence should include the report pack, payout export, and reviewed invoice-to-bank tracing samples.

- Days 61-90: add a second market only after controls pass.

Expand only after market one proves three things: payout failures are visible, policy gates behave as expected, and month-end close evidence is repeatable.

Require webhook or event payload coverage and clear ownership so failures are diagnosable. If BlueSnap is in scope, confirm operational settings that affect close timing and expectations, including default payout timing (Daily +2 business days) and payout currency scope (14 payout currencies).

Approval to add market two should include one successful payout-to-accounting trace, one failed payout case with status history, documented escalation contacts, and a finance-reviewed close sample.

- If exceptions remain unresolved, extend the pilot.

Unresolved reconciliation or exception-handling gaps are a reason to delay expansion, not post-launch cleanup.

Keep retry logic explicit and bounded. Stripe notes many failures are recoverable and documents a recommended default of 8 tries within 2 weeks for Smart Retries. That is useful only when your team also defines stop conditions and ownership for unresolved failures.

If you cannot explain outstanding exceptions with evidence, keep the pilot running and fix controls before entering market two.

Need the full breakdown? Read Document Management for Accounting Firms: Secure Intake, Retrieval, Retention, and Automation.

Red flags that should stop procurement or rollout#

Pause procurement or rollout if any of these appear. Brand strength and broad coverage claims do not compensate for missing payout evidence, unclear expert constraints, or unclear ownership when money movement fails.

- Brand-heavy pitch, evidence-light operations

Stop if a vendor leans on names like GLG, AlphaSights, or Third Bridge but cannot show concrete payout artifacts. Expert-network positioning is generally about access to expertise and consultations, not proven payout operations for your finance stack.

Ask for a payout reconciliation report, a payout-detail export, and one invoice-to-bank tracing sample. If they cannot show how a bank payout ties to underlying transactions, or they avoid sharing the fields finance will reconcile in Xero, you are being asked to trust marketing over controls. Documented reconciliation is an internal-control requirement.

- Coverage claims that fail your actual expert profile

Treat broad footprint claims as unproven until they map to your specific CPA, tax, and accounting-export requirements. BlueSnap’s "200+ regions" and "100+ currencies and payment types" claim is not, by itself, market-one readiness.

Check for concrete constraints early. Paro’s registration asks whether the applicant is a current U.S. resident, which can matter immediately if your rollout depends on non-U.S. accountants or cross-border tax specialists. The same applies to accounting outputs: a bidirectional Xero sync claim is not enough without sample records and field mapping.

- No written boundary between vendor scope and your scope

Stop when ownership is not explicit in writing across BlueSnap, Paro, and your internal team. Using third parties does not remove your responsibility, and roles can differ across parties.

This gap shows up in incidents: a payout fails, support points elsewhere, retries are undefined, and month-end close lacks defensible evidence. Require a written responsibility map, escalation contacts, and one failed-payout example with status history before signing or expanding.

Vendor diligence questions that remove the biggest unknowns#

The fastest way to reduce rollout risk is to force written ownership, a tested failure path, and finance-grade evidence before signature. In an accounting platform payments expert network model, unknowns usually come from blurred scope boundaries, weak incident visibility, and late reconciliation surprises.

Ask for a written scope split, not a sales summary#

Get each vendor to define ownership in three separate buckets: expert sourcing, compliance workflow, and payout operations. Start with AlphaSights, Third Bridge, CleverX, and Payments Consulting Network, and require a written boundary for each bucket.

That split matters because their public positioning differs. AlphaSights and Third Bridge market expert access and expert calls, while Payments Consulting Network presents itself as independent payments advisory rather than a processor. Those offerings do not by themselves prove ownership of payout execution, retries, or reconciliation evidence.

Request a one-page responsibility matrix across the vendor, BlueSnap, and your internal team. Map onboarding checks, payout initiation, status updates, exception handling, and month-end finance evidence. Any row with two owners or no owner is unresolved risk.

Make them walk a failed payout from trigger to closure#

Ask one direct question: "Show us one failed payout path end to end." Require the status sequence, retry behavior, customer and internal visibility, and exact handoff points across BlueSnap, your platform, and operations.

BlueSnap documentation gives concrete checks: vendor onboarding statuses, marketplace split-payments support, Reporting API data access, and payout or chargeback event updates via email and webhooks. It also documents an edge case where a scheduled payout with insufficient funds sends no payout notification. That is the kind of gap that can create reconciliation risk if exceptions are not monitored.

Also verify webhook delivery failure handling. The provider says it can retry delivery up to 11 times. Confirm where retries are logged, who owns monitoring, and what escalation happens after the final failed attempt.

Demand finance-grade integration proof for Xero#

Do not approve based on a generic "Xero integration" claim. Ask for export samples, reconciliation fields, and audit-trail completeness that finance can review.

At minimum, require identifiers, timestamps, amounts, status history, and traceability from earning or invoice records to payout and bank movement. Ask vendors to show alignment with Xero’s History and notes audit-trail output, including date-stamped and user-attributed changes. If they claim payment-service access inside Xero, confirm certification status because that API area is restricted to specifically certified payment service partners.

Before signature, require three artifacts:

- One payout-detail export and one reconciliation report.

- One failed-payout example with status history and resolution notes.

- One audit-trail sample finance can compare against Xero.

Conclusion#

For a go-or-no-go decision, prioritize the model that can demonstrate payout control, compliance behavior, and reconciliation readiness in your launch markets, not just brand recognition.

A key risk in an accounting-platform/payments-expert-network decision is operational: proving transaction authorization, periodic checks between recorded and existing assets, and reliable bank-to-ledger reconciliation. In practice, that means confirming your accounting records stay aligned with bank activity on a regular cadence.

- Get category clarity before vendor enthusiasm

A research-first network and a payments-first provider solve different problems. GLG highlights a network of approximately one million experts, and AlphaSights highlights 2,000+ professionals speaking 60+ languages. That supports expert access, but it does not by itself prove ownership of payout operations, compliance controls, or reconciliation evidence.

- Compare vendors using proof, not coverage language

Coverage is not launch proof. BlueSnap describes country-level payment-orchestration controls and local card acquiring in 50 countries, but those claims still require operational verification. Ask for concrete evidence: policy-gate documentation, failed-payout handling flow, available status events, and export outputs your finance team can test against accounting records.

- Pilot with strict checkpoints before expansion

A staged rollout is a practical operating pattern. Federal Reserve readiness framing treats adoption as a journey, and a July 2025 update references pilot work on additional network fraud risk mitigation while participation grew to more than 1,400 from 900. Keep your pilot narrow, then confirm payout exception handling, compliance gating behavior, and close-cycle reconciliation before adding markets.

- Document ownership gaps before signing

Ambiguity in control ownership creates avoidable risk. PCI DSS scope includes merchants, processors, acquirers, issuers, and service providers involved in payment card processing, so unclear boundaries can become costly. Use a written ownership matrix for onboarding checks, document collection, payout execution, exception handling, and reconciliation review.

A practical sequence is category clarity, evidence-based comparison, a pilot with control checkpoints, then expansion. For a deeper finance-side reconciliation workflow, use Xero integration for payout platforms.

When you’re ready to validate your target-market flow end to end, use the Gruv docs to confirm webhook events, statuses, and integration requirements.

Frequently Asked Questions

What is an accounting platform payments expert network?

An accounting platform payments expert network is more than expert introductions. It combines expert access with the operating layer needed for onboarding, compliance, payouts, and reporting. The practical test is whether the provider can show sourcing plus finance-grade payout and reconciliation evidence, not just consultations.

How is this different from using only an expert network like `GLG` or `AlphaSights`?

GLG describes an insight network with approximately one million experts, and AlphaSights emphasizes connecting clients with specialist experts. That supports sourcing, but it does not automatically cover payout execution, tax form collection, or reconciliation. If your main risk is expert access, a pure network can work. If your main risk is paying experts correctly across markets, you also need an operating payments layer.

What minimum capabilities are required before cross-border rollout?

Before adding countries, require evidence for onboarding, tax or compliance gates, payout visibility, and reconciliation. At minimum, verify handling for Form W-9 (U.S. payees) and Form W-8BEN (foreign individuals), and confirm sanctions or legal exposure has been reviewed for each target market. Also confirm your accounting flow can reconcile bank-side activity, since Xero’s BankTransactions endpoint does not return payments applied to invoices, expense claims, or transfers.

Should we validate compliance gates before sourcing quality, or in parallel?

Run both tracks in parallel, but treat compliance as the release gate. You can validate sourcing quality early with networks like GLG, AlphaSights, or Third Bridge while separately requiring operating proof for onboarding, required documents, and payout handling. Do not let strong expert coverage mask unresolved payment and compliance controls.

When does a multi-network strategy make sense versus a single provider?

Start with one provider when scope is narrow and ownership across sourcing, compliance, and payments is clear. Add another network when the first provider is strong in one layer but weak in another, or when you need broader expert coverage without replacing your payments stack. Keep ownership explicit in a written matrix so incidents do not bounce between the network, the payments provider, and your internal team.

Which metrics show this model is operationally viable after launch?

Use operational controls, not growth proxies. Reconciliation should consistently align bank balances with Xero records, and required tax-document coverage should remain current. If you use ACH, monitor unauthorized returns against Nacha’s 0.5% threshold over the preceding 60 days or two calendar months.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: