Quick Answer

Platforms should run contractor classification as a repeatable, documented process that starts with current U.S. FLSA and WHD guidance, then adds triage, scoring, reassessment triggers, escalation, and an audit-ready file. A contractor misclassification risk assessment should produce a clear status decision with a dated rationale, named approver, and retained evidence showing actual working conditions, not just labels or contract text.

For platforms, contractor misclassification risk assessment is a recurring control, not a one-time legal task#

For platforms, contractor misclassification risk assessment is a recurring control, not a one-time legal task. When your work model, oversight, or market footprint changes, classification risk can change with it.

In the U.S., the enforcement baseline is moving in a very specific way. On May 1, 2025, WHD issued a Field Assistance Bulletin on employee-versus-independent-contractor status for FLSA enforcement. WHD also said investigators are directed not to apply the 2024 final rule's analysis in current enforcement matters.

The 2024 final rule was published on 01/10/2024 at 89 FR 1638. Current WHD enforcement guidance points investigators to longstanding Fact Sheet #13 principles, further informed by reinstated Opinion Letter FLSA2019-6 for virtual marketplace platforms. WHD also states this bulletin is enforcement guidance and does not change existing regulations.

The practical takeaway is simple. If your internal questionnaire or scoring sheet cites only the 2024 rule, update the legal basis, not just the form.

This article turns that moving baseline into an operating model. First, it ranks six assessment approaches. Then it shows how to run them in a quarterly rhythm with clear owners, escalation paths, and audit-ready outputs.

The goal is not to overbuild the process. It is to move lower-risk cases quickly, escalate borderline cases before they harden into bad precedent, and keep a documented rationale for each final decision.

Scope guardrails:

- U.S. legal detail here is anchored to DOL, WHD, and FLSA materials in the available sources.

- Non-U.S. legal specifics vary by country and should be checked with local counsel.

- If you rely on FederalRegister.gov material for legal research, verify it against an official edition. Its XML rendition says it does not provide legal notice to the public or judicial notice to the courts.

Treat this as a living process. WHD posted a new proposed rule on Feb 27, 2026, with comments due by Apr 28, 2026 at 11:59 PM EDT, so your assessment workflow should include review dates and versioned rationale updates.

Related reading: Contractor Advance Payments for Platforms Without Taking Credit Risk.

How this list was judged and who should use it#

If you cannot show why a worker was treated as an independent contractor rather than an employee under the FLSA, your process is too thin. That remains true even if a quiz shows low risk.

| Criterion | Key requirement | Notes |

|---|---|---|

| Legal defensibility under FLSA and 29 CFR Part 795 | Document the employment-relationship rationale | Do not just apply a "1099" or "W-2" label |

| Operational feasibility for repeat use at platform scale | Work in real operations with recurring onboarding and mixed worker populations | Collect inputs consistently and escalate cases that need deeper review |

| Evidence quality for Internal Revenue Service inquiries | Retain evidence mapped to behavioral control, financial control, and relationship of the parties | Include contracts, benefit-related signals, and notes on who controls the work and the financial/business aspects of the job |

| Clear fit and clear non-fit | Use this ranking if you need documentation, ownership, and escalation paths that will still make sense later | Do not use it if the goal is only a five-minute Employee Misclassification Calculator output with no retained rationale or named approver |

This ranking is for teams that need a repeatable process with documentation, ownership, and escalation paths that will still make sense later. It is not the right fit if all you want is a five-minute Employee Misclassification Calculator output with no retained rationale or named approver.

The weighting is straightforward: favor approaches you can defend under the FLSA and 29 CFR Part 795, repeat at platform scale, and support with retained evidence mapped to behavioral control, financial control, and relationship of the parties.

If you want a deeper dive, read How to Handle Termination of an International Contractor.

Quick comparison of the six assessment options#

Use these six options as a stack, not as standalone tools. Start with a U.S. legal baseline, add triage and retained evidence, then layer in scoring and trigger-based reassessment.

| Option | Best for | Core inputs | Pros | Cons | Failure mode | Legal references | Required artifacts | What it misses | Operator lift (not quantified here) |

|---|---|---|---|---|---|---|---|---|---|

| 1. Legal baseline check anchored to U.S. rules | Contested or high-exposure U.S. roles where teams disagree on status | Actual work facts, contract terms, pay structure, benefit signals, and who controls work and business terms | Defensible starting point under current U.S. guidance | Requires judgment, not box-checking; not a non-U.S. answer | Teams rely on a 1099 label or contract label even when facts point elsewhere | FLSA, WHD, 29 CFR Part 795, Fact Sheet 13, Small Entity Compliance Guide | Fact memo, contract, scope of services, payment terms, supervision notes, final rationale with approver and date | Does not catch post-onboarding drift unless reassessed | Team-specific |

| 2. Questionnaire triage using 1099 and W-2 signals | Large inbound populations and periodic health checks | Standard questions on control, autonomy, supervision, benefits signals, pay setup, insurance, 1099/W-2 indicators | Fast, repeatable, easy to run at scale | Weights are often opaque; answers can be shallow or inconsistent; not legal clearance on its own | Low scores can create false comfort when files show conclusions without supporting facts | IRS three categories, with FLSA/WHD as escalation anchor | Completed questionnaire, source answers, reviewer notes, risk band, escalation decision | Can miss the real working relationship behind yes/no answers and later change | Team-specific |

| 3. Weighted scoring model your platform can defend | Teams that need consistency across business units or repeated role types | Explicit factor weights mapped to behavioral control, financial control, and relationship of the parties, plus override rules | Makes tradeoffs visible and reduces purely subjective calls | Needs calibration, version control, and governance | Score can become the decision even when evidence is mixed, outdated, or thin | IRS, FLSA, 29 CFR Part 795, WHD | Scoring matrix version, factor-level evidence, override record, named owner, change log | A stronger scorecard is not, by itself, an employment-relationship rationale | Team-specific |

| 4. Trigger-based reassessment instead of annual checkbox reviews | Roles that change quickly after onboarding | Event signals such as expanded scope, tighter supervision, longer duration, employee-like access, or payment-model changes | Can catch drift earlier than periodic reviews | Requires ownership across ops, product, finance, and legal | Work reality changes but no one flags it, so the original decision goes stale | FLSA, WHD, Fact Sheet 13 | Trigger log, reassessment notes, updated facts, status freeze or approval record, revised contract or scope | Cannot fix weak initial classification if baseline documentation was thin | Team-specific |

| 5. Escalation lane for medium- and high-risk cases | Disputed facts, urgent business requests, or clear employee-like signals | Risk band, disputed facts, legal questions, payment impact, remediation options | Prevents ad hoc exceptions and clarifies approval rights | Without response times and ownership, it becomes backlog | Relationship continues while review stalls, increasing potential FLSA wage/overtime exposure and possible IRS employment-tax exposure if status is wrong | FLSA, WHD, IRS | Escalation ticket, evidence bundle, counsel request, remediation plan, final disposition | Does not detect low-grade drift in "low-risk" files or improve intake quality on its own | Team-specific |

| 6. Audit evidence pack and leadership reporting | Internal audit, counsel review, and recurring governance reporting | Final status, rationale, source evidence, timestamps, owner, open issues, reversals | Converts scattered notes into a defensible record for repeat review | Can bloat if teams store volume but not reasoning | File is large but weak because it does not explain why the decision was made | FLSA, 29 CFR Part 795, IRS, WHD | Single case file with questionnaire output, contract, benefit signals, control notes, decision memo, approver, review date, version history | Reporting is retrospective; it does not guarantee sound intake or reassessment controls | Team-specific |

Tool-only approaches often underperform for two reasons. They record an outcome, not the underlying employment-relationship analysis, and they miss drift. Your framework should therefore track both the governing materials you relied on and the version used at the time, rather than freezing the process around one rule snapshot.

A practical checkpoint is to sample closed cases. Confirm each file includes intake records, contract and pay terms, notes tied to behavioral control, financial control, and relationship of the parties, plus the final decision, approver, and decision date.

That evidence matters later if status is challenged, including IRS worker-status determinations and potential use of Form 8919 by workers after determination.

This pairs well with our guide on How Availability Heuristic Distorts Risk Assessment for Freelancers.

Option 1 legal baseline check anchored to U.S. rules#

Start with a U.S. legal baseline before any internal scoring model. This is the most defensible first step because it anchors the review to the FLSA analysis of the actual working relationship, not a tool output.

What makes this option worth using#

It is strong because it starts with the governing U.S. materials in the file. The question is the economic realities of the entire relationship, including whether the worker is economically dependent on the company or in business for themself.

For disputed roles, that keeps the discussion on the full record. Labels and narrow snapshots may be part of the file, but they are not determinative on their own.

How to use it on a real disputed role#

Use this when teams disagree on classification and you need a clear, auditable rationale. Review the engagement under Employee or Independent Contractor Classification Under the Fair Labor Standards Act. Tie notes to 29 CFR part 795 and current WHD materials in your source set. Document whether the facts indicate an employment relationship under the FLSA.

For each file, keep the evidence pack tight:

- actual work facts, not just labels

- how the full relationship supports the economic-realities analysis

- final rationale, approver, and decision date

- rule citation metadata, including 89 FR 1638 and the official PDF link

Do not rely on FederalRegister.gov XML alone as the legal source. It is informational and should be verified against an official Federal Register edition or PDF.

Where teams get this wrong#

The main failure is treating common-law control concepts as the primary test. Fact Sheet 13 states FLSA employment is broader, so a narrow control-only approach can misstate status.

Another is weak source discipline. If the file does not preserve the governing rule citation and official-source checkpoint, the record is harder to defend later.

Best use and decision rule#

Use this option first for contested and high-exposure U.S. roles. If facts are mixed, the legal memo should control over any calculator output.

When you sample closed files, confirm each one explains why the relationship does or does not indicate employment under the FLSA, cites 29 CFR part 795, references Fact Sheet 13, and records the source date or version used. Because the 2024 rule is subject to current litigation and enforcement posture can shift, version tracking is part of a defensible file.

Related: How to Classify a Worker as an Employee vs. an Independent Contractor in the US.

Option 2 questionnaire triage using 1099 and W-2 signals#

Use a questionnaire as a repeatable triage layer, not the decision itself. Its job is to capture relevant data in a consistent format so teams can compare records and prioritize follow-up review.

Why this option earns a place#

This option helps when multiple teams touch the same engagements and need one intake pattern. A disciplined questionnaire supports risk assessment by using the same question categories, in the same order, with the same answer rules across records. Keep it short, but make sure a reviewer can reconstruct what happened.

At minimum, each file should preserve:

- the internal intake label used for the record

- a plain-language description of the services

- who completed the questionnaire and when

- supporting documents or links for non-obvious answers

- brief rationale where judgment was required

- questionnaire version used for that file

Version control helps. If wording or answer logic changes over time, stamp each file with the version so differences can be interpreted consistently.

Where teams get false confidence#

A common failure is opacity: teams can see the output but cannot explain how it was produced. Sample closed files and confirm an independent reviewer can trace each question, answer, supporting material, and form version. If only a final output is visible, the triage record may be too thin to support risk decisions.

Option 3 weighted scoring model your platform can defend#

Use a weighted model when you need consistency across teams and repeated role types, and you need to explain each decision line by line. The value is not a prettier score. It is making judgment calls visible, documented, and reviewable.

Why this option is worth the extra effort#

A weighted model surfaces real disagreements. If legal emphasizes control, finance emphasizes tax exposure, and operations emphasizes contract labels, weighting makes those tradeoffs explicit instead of burying them in opaque outputs.

Anchor factors to recognized authority, not internal convenience. The IRS says classification generally considers three categories: behavioral control, financial control, and relationship of the parties. DOL/WHD materials point employers to current FLSA guidance, including 29 CFR Part 795. Use IRS categories as structured inputs, then cross-check against the FLSA analysis rather than assuming one score resolves everything.

Do not let intake labels decide the outcome. A 1099 tag or a contract title can route a file, but those labels do not establish the underlying relationship.

| Factor | Relative weight | Evidence required | Override authority | Mandatory escalation trigger |

|---|---|---|---|---|

| Behavioral control | High | Statement of work, instructions to the worker, records showing who decides how the work is done | Named legal or compliance reviewer with written rationale | Contract says independent contractor, but day-to-day facts show the company directs methods, schedule, or process |

| Financial control | High | Payment terms, invoices, reimbursement records, documents showing who controls business aspects of the work | Named legal or compliance reviewer with written rationale | Finance records and operating facts conflict on who bears costs or controls the business side of the work |

| Relationship of the parties | Medium to high | Written contract, benefit records if relevant, engagement duration, evidence on continuity and business integration | Named legal or compliance reviewer with written rationale | Contract language points one way, but continuity, benefits, or role centrality point the other way |

| FLSA cross-check under 29 CFR Part 795 | Required for every file | Short memo linking the score to current WHD guidance and rule version used | Legal review required for any override | Model outcome depends on assumptions from the rescinded 2021 rule or cannot be reconciled with current FLSA analysis (effective March 11, 2024) |

Build evidence into each score band#

Treat every meaningful score input as an evidence-backed claim. If behavioral control is scored low risk, the file should show why. If relationship-of-the-parties is scored low risk, the file should point to contract terms and relevant records on benefits, continuity, or business integration.

This matters because the IRS says classification depends on the relationship between the worker and the business, and DOL says employers are responsible for determining whether a worker is an employee under the FLSA. A model that accepts unchecked label-based answers is hard-coding assumptions. Require documents, dated records, or brief reviewer notes for non-obvious facts.

Log the model version in every audit record. If decisions are not tied to the rule version used, historical scores are harder to defend.

Where weighted models usually fail#

The main failure mode is false precision. Teams trust the number and stop checking whether the facts are complete, current, and relevant to the FLSA question. Poor weighting can also encode business preference, such as overweighting contract labels while underweighting how work is actually controlled.

Overrides are another warning sign. Some are necessary, but they should be rare, reasoned, and evidence-backed. Repeated overrides in the same direction usually point to weak factor definitions, weak evidence rules, or poor calibration. If the score and legal analysis diverge, escalate the file. Record why, then recalibrate later if the same pattern repeats.

What to verify before trusting the model#

Sample closed files and ask an independent reviewer to reconstruct each decision from the record alone. They should be able to see factor scores, supporting evidence, model version, reviewer, and the 29 CFR Part 795 cross-check without relying on informal context.

Test disputed files separately. Where worker-status challenges are already in motion, treat the model as decision support, not final proof. IRS notes there is a worker-status determination process for disputed classification before Form 8919. Contested cases should move through escalation rather than routine approval.

You might also find this useful: Contractor Misclassification at Platform Scale: Legal and Financial Risks.

Option 4 trigger based reassessment instead of annual checkbox reviews#

Use trigger-based reassessment when relationship facts change between scheduled reviews. In the materials cited here, there is no source-backed legal rule that defines trigger standards or requires a trigger cadence over an annual one.

A practical internal approach is to reopen a file when a material fact behind the prior decision appears to have changed, then document what changed and whether the prior rationale still holds.

- Reopen only on material fact changes tied to your existing assessment factors.

- Assign a clear owner for intake and review so signals are not lost.

- Require fresh, dated evidence in the case file before re-review.

- Route uncertain or higher-risk changes for specialist legal review under your internal process.

Where teams usually get this wrong#

The biggest failure is treating non-official source material as final legal authority. In the materials cited here, FederalRegister.gov is presented as a prototype edition that is not an official legal edition, and its XML rendition does not provide legal or judicial notice. For legal verification, use the linked official PDF on govinfo.gov and retain that version in your file.

A second failure is assuming every mention of misclassification in a legislative excerpt provides reassessment criteria. Here, the Minnesota excerpt mentions misclassification but does not provide usable trigger standards, and the Kentucky entry is only a timeline record.

What to retain after each reopen#

Keep a before-and-after audit trail in one record so the decision path is reconstructable:

- prior decision and date

- new fact that triggered reopen

- new dated evidence reviewed

- reviewer and review date

- exact legal or reference documents relied on, using official versions

Need the full breakdown? Read How to Conduct an Annual AML Risk Assessment for Your Payment Platform.

Option 5 escalation lane for medium and high risk cases#

When a reopened case lands in medium or high risk, move it out of routine ops and into a defined escalation lane. At that point, the risk is not just documentation quality. Under the FLSA, minimum wage and overtime protections depend on whether an employment relationship exists, and the IRS can hold a business liable for employment taxes if an employee was misclassified.

A formal lane prevents ad hoc decisions under pressure. Without clear internal turnaround targets, required artifacts, and decision authority, escalation becomes backlog noise instead of risk reduction. This is an internal operating model, not a U.S. legal requirement.

A practical three lane design#

| Lane | Use it when | Required artifacts | Main touchpoint | Close only when |

|---|---|---|---|---|

| Ops remediation | The issue looks fixable without a final status call | Prior score or trigger note, current agreement, scope of work, access list, manager instruction samples, remediation owner and date | IRS behavioral-control factor (as one part of a relationship-based analysis), including who controls what work is done and how | Updated evidence shows the control signal changed, or the case is escalated |

| Legal review | Facts suggest possible employee status, or the record conflicts with day-to-day reality | Full case file, dated fact summary, contract or amendments, supervision evidence, payment facts, legal rationale tied to 29 CFR Part 795 | DOL/WHD guidance and 29 CFR Part 795 | Authorized legal reviewer records rationale, decision date, and required remediation |

| Executive exception | Business wants to continue or expand the relationship with unresolved risk | Legal summary, exposure summary covering minimum wage, overtime, and tax, interim controls, named approver, review date | Combined FLSA and IRS exposure view | Named executive accepts the exception in writing and sets re-review date |

Legal review is the anchor lane for medium- and high-risk files. If your team references the 02/27/2026 proposed-rule page, verify against the official Federal Register edition. Do not treat a proposal as final law.

What to verify before you escalate#

Do not escalate on score alone. IRS worker status depends on the full worker-business relationship, so confirm the file includes the trigger fact pattern, dated evidence of actual working conditions, and the exact legal and tax references the reviewer will apply.

Also avoid delay disguised as caution. Leaving a case unresolved can increase exposure where FLSA minimum wage or overtime protections would apply if the worker is an employee. If a worker later challenges classification through the IRS process, worker-status determination is generally required before Form 8919 is used, so each escalation file should be complete, dated, and defensible.

For a step-by-step walkthrough, see Vendor Risk Assessment for Platforms: How to Score and Monitor Third-Party Payment Risk.

Option 6 audit evidence pack and leadership reporting#

Use one minimum evidence pack per case so a second reviewer can reconstruct the decision quickly and trust what happened. The goal is not to store everything. It is to preserve the facts used, the decision made, and the rule status on that date.

This option is most useful when internal audit, counsel, or regulators may review your process later. The common failure mode is bloat: too many emails, duplicate screenshots, and draft noise that bury the actual basis for the call.

Build one minimum file, not an archive dump#

Treat this as an internal control format, not a claim that WHD or DOL requires your exact schema. For each case, keep one record with a short index and only decision-relevant artifacts:

- questionnaire or intake output used to open review

- dated summary of actual working conditions, not only contract text

- legal rationale tied to the rule set your team applied

- final status decision, named owner, and timestamp

- rule-tracking note for relevant Federal Register developments

If you monitor the 2026 WHD notice of proposed rule, label it as a proposal, not final law. A short note such as "NPRM tracked only" plus Docket No. WHD-2026-0001 and RIN 1235-AA46 is usually enough to show clear rule tracking without overstating legal status.

Before closing a file, verify two things: a reviewer can separate case facts from legal interpretation in minutes, and any status reversal has a dated rationale. Independent contractors are described as outside FLSA overtime requirements, and contractor classification is described as carrying significant risk.

Keep rule tracking separate from case facts#

Keep case evidence and live rulemaking updates adjacent but separate. Track proposal metadata, possible impact, and comment plans, but do not let an NPRM silently replace the legal basis used for a current decision.

If your organization submits comments, document process controls in the file. Comments become public record, including personal information. Late comments are not considered. This notice describes a 60-day proposed window with an 11:59 p.m. ET cutoff on the deadline date.

Use the table below as an internal reporting example, not a mandated KPI list.

| Reporting item | What leadership should see | Red flag to flag early |

|---|---|---|

| Case volume | Opened, closed, and carried cases for the period | Rising backlog with no owner |

| Risk mix | Low, medium, and high risk distribution | High-risk concentration in one business unit |

| Escalations | Cases moved to legal review or executive exception | Escalations growing faster than closures |

| Reversals | Status changes after review | Reversals without dated rationale |

| Open actions | Remediation tasks, owner, target date | Past-due actions with active contractor use |

| Unresolved jurisdiction questions | Pending legal interpretations or monitored rule changes | Teams treating a WHD proposal as settled law |

Related reading: Contractor misclassification risk overview.

Building the evidence pack and escalation workflow? Use Gruv docs to map payout states, policy gates, and webhook events into your review controls.

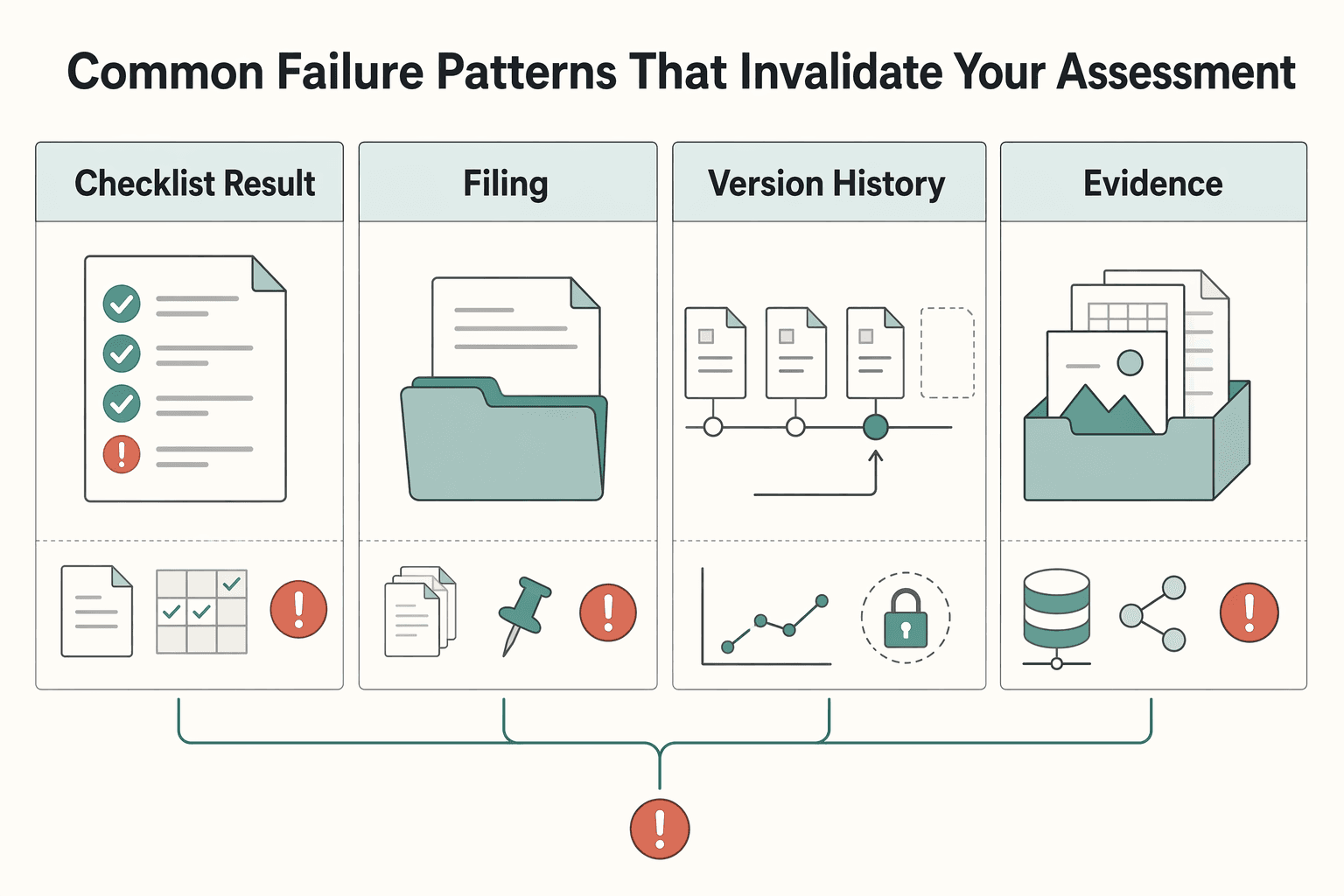

Common failure patterns that invalidate your assessment#

If the file shows an outcome but not the reasoning behind it, the assessment is hard to defend. A reviewer should be able to see the facts used, the rule set applied, and the version in effect on the decision date.

| Failure pattern | What the article says | Consequence |

|---|---|---|

| Checklist result treated as legal clearance | A short Independent Contractor vs. Employee Classification Checklist can support intake, but it is not legal signoff on its own | If the file has only the score and no dated rationale tied to real working conditions, the assessment is weak |

| Unrelated tax filings mixed into classification evidence | Form 8938 and FinCEN Form 114 (FBAR) are separate foreign-asset/account reporting filings | Keep them clearly labeled for tax-reporting context, not as proof of a classification decision |

| No version history when criteria change | If your team updates its criteria over time, keep a dated version trail | When teams overwrite prior rationale, they cannot show which version supported the original call |

| Decision recorded without rationale | "Approved as contractor" is a result, not an assessment | Record which facts increased risk, which reduced risk, and why the final judgment was reasonable |

In practice, these failures lead to the same problem: a file that shows an answer without a defensible path to that answer.

90 day rollout sequence for compliance legal finance and ops#

Use this 90 day sequence as an internal rollout plan, not a legal timetable. The goal is to make worker-classification reviews consistent, current, and auditable across teams; the provided source supports these compliance checkpoints but does not validate this exact 90-day phasing.

| Phase | Timing | What to do | Checkpoint |

|---|---|---|---|

| Standardize intake and records | Days 1-30 | Set one intake path and one case-file standard for compliance, legal, finance, and ops | Make sure each file captures the same core facts and supports recordkeeping and retention from the start |

| Test consistency through case reviews | Days 31-60 | Run a limited pilot and check whether teams reach similar outcomes from similar facts | Use periodic inspections and audits of case files to find gaps in documentation and handoffs before scaling |

| Move to repeatable monitoring | Days 61-90 | Shift from one-time reviews to a repeatable operating cadence with scheduled file checks and leadership visibility | Keep the process focused on risk control and current practices, especially where compliance stakes are stricter |

| Day 90 checkpoint | Day 90 | Sample closed cases | Confirm each one has complete records and a documented rationale for the decision; if records are incomplete, treat the case as operationally unresolved until follow-up is complete |

A practical checkpoint at day 90 is to sample closed cases and confirm each one has complete records and a documented rationale for the decision. If records are incomplete, treat the case as operationally unresolved until follow-up is complete.

Conclusion#

The practical answer is not one tool. A defensible assessment is a stacked process: legal baseline, triage, weighted scoring, event-triggered reassessment, escalation, and evidence reporting.

-

Anchor each decision to current U.S. guidance. For FLSA employee-versus-contractor decisions, use the current FLSA framework, including 29 CFR Part 795 and related WHD materials, not a contract label or score alone. Your file should state which WHD materials were used and when, whether that is the rulemaking page, Fact Sheet 13, FAQs, or the Small Entity Compliance Guide. Employers are responsible for this determination.

-

Make the file prove the judgment. Keep one case record that shows who decided, why, which facts were used, and when the case was last rechecked. Include the questionnaire output, reviewer, date, rationale, and evidence of actual practice. If the reasoning cannot be reconstructed from the file, treat the case as incomplete.

-

Use periodic and event-triggered review. A portfolio cadence can support leadership reporting, but cases should reopen when facts change, especially around behavioral control, financial control, or the type of relationship. Medium- or high-risk outcomes should move to legal or compliance review rather than staying as a scoring discussion.

If status is wrong, risk grows quickly: enforcement and litigation exposure can increase, and affected workers may lose minimum wage and overtime protections under the FLSA. When someone is moved into an employee population, make sure downstream records are handled correctly, including properly completed Form I-9 records on file for employees.

If you can show who made the decision, why, which U.S. guidance informed it, and when it was rechecked, you are operating at platform grade. This structure reduces surprise while staying lean enough for a periodic management view.

If you need to validate whether your current contractor payment flow can support audit-ready reassessment and controlled escalations, talk with Gruv.

Frequently Asked Questions

What is a contractor misclassification risk assessment and what decision should it produce?

It is a documented review of whether the facts support independent contractor or employee status. As an internal governance practice, it should end with a clear status decision and a short dated rationale that shows why the decision was made.

Which factors matter most in a practical checklist and which are only secondary signals?

In the proposed-rule materials cited here, control over the work and the worker's opportunity for profit or loss are identified as core factors. Contract labels and paperwork alone are weaker signals because actual practice is treated as more relevant than what is only contractual or theoretical.

What changed in U.S. guidance from the WHD final rule and why does it affect platform controls?

The 2024 final rule revised FLSA employee versus independent contractor analysis, but current WHD enforcement guidance says investigators are directed not to apply that rule's analysis in current enforcement matters. Instead, WHD points investigators to longstanding Fact Sheet 13 principles, informed by reinstated Opinion Letter FLSA2019-6 for virtual marketplace platforms. The article also notes a 2026 NPRM that would rescind the 2024 rule and replace it with an economic reality analysis. Because the baseline is moving, platform controls should track the rule version used and review control-related operating choices.

How often should a platform reassess classification risk if annual reviews are not enough?

The cited U.S. materials do not set a fixed legal reassessment cadence such as annual or quarterly. A practical internal approach is to reopen a file when material facts change and document whether the prior rationale still holds.

What should happen immediately after a medium-risk or high-risk result?

The cited materials do not mandate a specific medium-risk or high-risk escalation workflow. Treat score outputs as triage inputs and move those cases through your internal legal or compliance process with complete, dated evidence.

What evidence should we retain so legal and finance can defend the decision later?

Retain records that show the actual working relationship and the rationale for the decision, not just contract text or labels. The file should include intake records, contract and pay terms, evidence tied to behavioral control, financial control, and relationship of the parties, plus the final decision, approver, date, and rule version used. If you use FederalRegister.gov for legal research, verify it against an official Federal Register edition.

Can a free calculator replace legal review for cross-border platform operations?

No. A free calculator can support intake triage, but it is not legal clearance. The source documents here are U.S. FLSA and WHD specific, and non-U.S. legal specifics vary by country and should be checked with local counsel.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- dol.gov/agencies/whd/flsa/misclassificationtrusted

- dol.gov/newsroom/releases/whd/whd20250501trusted

- federalregister.gov/documents/2024/01/10/2024-00067/employee-or-...trusted

- federalregister.gov/documents/2022/05/09/2022-09375/medicare-pro...trusted

- gao.gov/assets/a293684.htmltrusted

- irs.gov/newsroom/worker-classification-101-employee-...trusted

- irs.gov/pub/irs-pdf/i8938.pdftrusted

- public-inspection.federalregister.gov/2026-03962.pdftrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: