Quick Answer

Start with signed contracts, not payout speed: confirm recourse status, Notice of Assignment, reserve or holdback rights, and dispute ownership before releasing funds. Then run one sample transaction packet end to end with approval evidence, payment instruction, posting record, and final payout status. If that packet cannot be rebuilt from your own records, pause launch. Pilot one cohort first, and treat any unanswered contract cell as unresolved risk.

Why this matters for platform operators#

For platform operators, the real decision is control quality, not payout speed. Paying before delivery only works when each release is tied to verified approval evidence and a complete document trail.

1. Delayed buyer settlement creates a real cash gap#

Payment delays are common enough that liquidity pressure becomes an operating reality. A 2024 study cited by NetSuite found that 82% of contractors regularly experience payment delays exceeding 30 days, up from 49% in 2022. It also found that 95% of general contractors and 75% of subcontractors frequently float payments while waiting for disbursements. When settlement is delayed, the strain increases on whoever fronts funds.

Delay pressure does not reduce the need for strong approval signals.

2. Thin margins punish loose approval rules#

In contractor-heavy flows, release decisions should follow milestone validation, not invoice presence alone. NetSuite describes construction payment management as validating progress and paying against contractual milestones and timelines, and typical subcontractor margins are often only 5% to 10%. With margins that thin, an early funding mistake is hard to absorb.

A practical control is a required document pack before release: progress reports, insurance coverage, licensure, and payment details. In construction-adjacent flows, lien waivers also matter because they confirm payment receipt and support clean-title outcomes at completion. A common failure mode is billing ahead, where payment applications exceed completed work and front-load profit before equivalent delivery. Stronger programs are anchored to approval artifacts and milestone evidence, not submitted invoices alone.

3. Model choice is really a risk and operations choice#

Choosing an advance model is mostly an operating-risk decision. Enterprise contractor-payment programs face higher fraud exposure when systems and teams are fragmented. Contractor payment fraud can include fake invoices or other dishonest attempts to extract extra payment. Advance payment guarantees can improve security, but they also add diligence, dispute-management burden, and trust sensitivity.

Use a simple decision rule: if your team cannot reconstruct who approved the work, which document supported that approval, and when payout was released, your controls are not ready yet.

Who this list is for and the selection criteria that actually matter#

This category is only worth evaluating if you can enforce approval evidence and maintain one clean record of what was approved and paid. If you cannot do that, speed claims are not the priority.

- Best fit

These options fit platforms where delayed payments are already creating cash-flow stress for contractors or suppliers. They are especially relevant in progress-payment models, where work is billed as it advances and part of each payment may be retained until substantial completion. The fit is stronger when each funding request ties back to clear documentation: approved billing, progress evidence, and a payment record.

- Poor fit

Skip this category for now if approvals are fragmented or not consistently documented. Payment validation depends on large, changing datasets tied to billed work and contract terms, so weak controls raise the chance of funding against incomplete evidence.

- Use five filters before you compare vendors

Ask every provider the same five questions, in writing:

- What exact approval checkpoint triggers payment? - Which documents are required before funds are released? - How are invoice and payment records centralized and maintained? - How does the process validate billed work against contract terms as project data changes? - If you operate across countries or currencies, how does the process handle compliance and operational complexity?

- Red flags that save you time

Treat "faster pay" as non-credible if the provider cannot clearly show approval checkpoints and centralized invoice and payment record-keeping. Treat broad coverage claims, such as country or currency reach, the same way. They are items to verify, not proof that your control requirements are met.

Related: Intake-to-Procure for Platforms: How to Simplify Request-to-Pay Before a PO Is Raised.

Compare the four models before choosing any vendor#

Start this comparison as a contract-diligence exercise, not a positioning exercise. In this evidence pack, model-specific mechanics are not fully substantiated, so the only defensible comparison is what signed documents confirm versus what is still an assumption.

Treat vendor pages and pitch decks the way FederalRegister.gov treats its prototype edition for the Defense Department rule dated 10/15/2024 (89 FR 83092). They are useful for orientation, not final legal reliance, and should be verified against the official PDF on govinfo.gov. Use that same standard here. If a detail is not in the signed contract set, it is not settled.

Scan the models, but mark every unproven field#

| Model | Best for | Risk holder | Trigger event | Contractor UX | Buyer UX | Typical failure mode |

|---|---|---|---|---|---|---|

| Candidate model 1 | Not established in this evidence pack; define in signed terms | Not established in this evidence pack; name the exact party in signed terms | Verify the exact documented event that releases funds | Verify required proof and the exceptions that stop funding | Verify whether approvals, acknowledgements, or remittance steps change | Teams assume key terms are standard, then contract exceptions change outcomes |

| Candidate model 2 | Not established in this evidence pack; define in signed terms | Not established in this evidence pack; name the exact party in signed terms | Verify the exact documented event that releases funds | Verify required proof and the exceptions that stop funding | Verify whether approvals, acknowledgements, or remittance steps change | Teams assume key terms are standard, then contract exceptions change outcomes |

| Candidate model 3 | Not established in this evidence pack; define in signed terms | Not established in this evidence pack; name the exact party in signed terms | Verify the exact documented event that releases funds | Verify required proof and the exceptions that stop funding | Verify whether approvals, acknowledgements, or remittance steps change | Teams assume key terms are standard, then contract exceptions change outcomes |

| Gruv modular build with Virtual Accounts, Payouts, and MoR | Confirm fit for your workflow; module availability varies by market/program and what is enabled | Confirm in signed terms which entity is merchant, which entity moves funds, and which entity carries default exposure | Verify which state change in your records authorizes payout | Verify evidence requirements, retry behavior, and payout status visibility | Verify what buyers see when collection, ledgering, and payout are split across modules | Risk ownership can blur across platform, MoR, and payout layers when contracts are split |

Use this table to remove ambiguity, not to pick a winner. If a provider cannot answer a cell with a document reference, treat that cell as open risk.

Compare contract mechanics before product mechanics#

If you cannot clearly name who pays when a buyer defaults, do not launch that model.

| Model | Recourse / Non-Recourse | Notice of Assignment | Reserve Account / Holdback usage | Dispute path |

|---|---|---|---|---|

| Candidate model 1 | Verify recourse terms in signed documents | Verify whether notice is required, optional, or conditional | Verify whether reserves or holdbacks can be imposed, and who controls release | Verify who handles disputes and when ownership changes |

| Candidate model 2 | Verify recourse terms in signed documents | Verify who receives notice and when | Verify whether reserves are standing or event-based | Verify who owns collections, credit memos, and post-funding disputes |

| Candidate model 3 | Verify recourse terms in signed documents | Verify whether assignment or payment-redirection notice is embedded in terms | Verify whether failed or exception transactions create reserve requirements | Verify what happens if fulfillment is accepted but payment later fails for a documented reason |

| Gruv modular build with Virtual Accounts, Payouts, and MoR | Verify recourse at each layer, not only in one headline agreement | Verify whether assignment language sits in MoR terms, payout terms, or your buyer agreement | Verify where reserves sit in the stack and who can debit them | Verify which counterparty owns dispute operations, write-offs, and reporting |

The verification standard that matters#

Before you score any vendor, request the official contract set rather than a marketing PDF. At minimum, that means the master agreement, order form or program schedule, assignment language, reserve or holdback schedule, and clauses naming collections and dispute ownership. Ask for one sample transaction packet too: approval evidence, payment instruction, posting record, and final payout status.

One avoidable failure pattern looks like this: product expects faster pay, finance assumes provider-held loss, legal finds recourse in a later schedule, and ops learns post-launch that an approval reversal reopens exposure. Keep the same line FederalRegister.gov uses for unofficial material: useful for orientation, never enough for legal reliance.

Use one decision rule for speed. Do not compare speed, fees, or experience until the risk holder, trigger event, and dispute path are each named in signed documents. Until then, you are comparing assumptions, not models.

Related reading: Transaction Monitoring for Platforms: How to Detect Fraud Without Blocking Legitimate Payments.

Billd style buyer approved pay app advance#

Treat this as a design pattern to verify in contract, not a settled product fact about Billd. The real question is whether you can tie funding decisions to a documented approval event without creating unclear liability exposure later.

- Best fit

Use this pattern only when you can point to one explicit approval record that changes a request from pending to eligible for funding. The outline references construction pay apps and GC approval, but those specifics are not supported in this evidence pack and should be treated as assumptions until signed documents confirm them. Payment methods vary by customer, product, and location, so validate fit by cohort rather than assuming one approval-led flow works for everyone.

- Why operators consider it

Teams sometimes consider this pattern to connect approval evidence and payment operations in one flow, but this evidence pack does not substantiate specific speed or cost outcomes. A useful parallel from installment programs is that execution depends on platform and payment-gateway integration. If approval evidence lives outside that flow, operations can shift back to manual follow-up.

- Hidden economics usually sit in documents, not demos

The failure path matters more than the happy path. In this evidence pack, recourse terms, holdbacks, reserve rules, and default-loss ownership for a Billd-style program are not substantiated, so treat them as open risk until contract language names them. Installment programs flag a related downside: late or unpaid obligations can trigger added fees and interest. In this model, a similar concern is unclear post-funding liability when disputes or reversals happen.

- Concrete use case and operator checkpoint

Use one sample transaction as an evidence test, not a sales demo. Confirm each step with signed terms and records:

- master agreement, order form or program schedule, assignment language, and any reserve or holdback schedule - one complete packet with approval evidence, payment instruction, posting record, and final payout status

If your team cannot reconstruct that packet end to end, pause rollout. If you need to tighten that control layer first, start with invoice verification.

Vendor Pay Express style supplier early payment program#

This pattern can fit when buyer payment terms stay fixed and supplier cash timing is the real constraint. Buyers can remain on Net 30 or Net 60, but the model is safer when your contract and invoice records make timing rules explicit.

| Clock basis | What it means | What to confirm |

|---|---|---|

| Net 30 | Full payment is due within 30 calendar days | Define the start point in the agreement and on invoice artifacts |

| Net 60 example | Full payment is due within 60 calendar days from invoice date | Confirm that invoice date is the clock start |

| Shipment date start | Some vendors start the clock from shipment date instead | Spell out shipment as the start point |

| Delivery date start | Some vendors start the clock from delivery date instead | Spell out delivery as the start point |

1. Best fit#

Use this when invoices are approved, suppliers need cash sooner, and buyers still expect trade-credit terms. The operating goal is simple: the supplier gets paid earlier while the buyer timeline stays standard.

Define payment terms precisely in the agreement and on invoice artifacts:

- Net 30 means full payment is due within 30 calendar days.

- In the cited Net 60 example, full payment is due within 60 calendar days from invoice date.

- Some vendors start the clock from shipment or delivery date instead, so you need that start point spelled out.

2. Why operators consider it#

Teams look at this model when they want earlier supplier payout without forcing buyers to change how they pay. Any "simple" or "lower-friction" promise should be validated in the actual process flow.

Treat simplicity as something you have to prove. If payment instructions or date reconciliation still require manual intervention, the admin burden comes back fast.

3. Hidden economics usually sit in documents, not demos#

Most of the real risk shows up in contract wording and fee logic, not in a high-level walkthrough.

Before launch, request one complete evidence set. Include:

- master agreement, fee schedule, and supplier terms

- one settled transaction trail with invoice date, approval date, payout date, buyer due date, and final settlement amount

- a clear statement of when the payment clock starts, whether invoice date, shipment, or delivery date

Also check for embedded pricing logic. At least one provider markets separate cash and card prices, with acceptance cost added into card pricing. Verify that method-based economics are visible in contract terms and settlement reporting.

4. Concrete use case and operator checkpoint#

One common use case is an approved supplier invoice paid early while the buyer remains on Net 30 or Net 60 terms. Confirm responsibilities in signed documents rather than a sales narrative.

Your main checkpoint is the due-date clock start. If teams misread whether timing runs from invoice, shipment, or delivery date, late payments can happen unintentionally and hurt cash flow and credit standing. Under Net 60 terms, paying on time typically avoids fees or interest, so clock-start clarity matters.

If you are also setting payout timing policy, see Net-30 Payment Terms for Platforms: How to Set Vendor Payment Terms Without Killing Contractor Cash Flow.

CrossCheck style guaranteed funds at fulfillment#

Use this pattern cautiously when failure risk is concentrated at handoff, not after invoice approval. Treat model mechanics as contract-specific: pre-dispatch approval checks, delivery checkpoints, or fulfillment-triggered release should be considered unverified unless your agreement states them explicitly. Field execution and finance controls still need to operate as one process.

1. Best fit#

This model fits when high-value handoffs repeatedly create reversals, disputes, or delayed settlement. The goal is to tighten control around handoff and settlement risk, not extend post-invoice terms.

Treat the word "guaranteed" as a contract question, not a sales label. Some merchant agreements describe proceeds as provisional credits and allow debits from the Settlement Account to recover those credits or other owed amounts.

2. Where certainty holds and where it breaks#

Certainty depends on complete contract terms and a consistent transaction record trail. At minimum, keep these records tied to one transaction ID:

- authorization or order record

- delivery or fulfillment record with amount match

- settlement record and statement mapping

- dispute or adjustment records tied to statement dates

If that trail is incomplete, the flow becomes a dispute and recovery problem.

3. Contract controls that matter#

Start with three terms: whether funds are provisional, whether the provider can debit your Settlement Account, and whether a reserve account can be required. Those terms determine how much reversal risk can return to your balance sheet.

Check the dispute window and term length in the same pass. At least one agreement requires dispute notice within 30 days of the statement date, and may default to a three-year initial term unless the application says otherwise.

4. Failure modes and tradeoff call#

Most breakdowns are operational: missing records, amount mismatch, or incomplete fulfillment documentation. Any of these can turn a clean handoff into a reversible or disputed payment.

Apply stricter controls to higher-risk cohorts and route lower-risk buyers under clear eligibility rules.

Gruv build option with modular rails#

Choose this route when you want direct control over decisioning, reconciliation, and exceptions, and you are ready to own stricter governance. The upside is flexibility. The cost is more responsibility for document quality, review thresholds, and launch discipline.

Treat this as a design path, not a pre-verified bundle. Do not assume a fixed Gruv module sequence or universal rail coverage without confirmation for your specific market and program.

1. Start with the evidence chain, not the rail#

In a modular build, control comes from deciding exactly what facts must exist before money moves. That matters because approved facts can still change. Change orders are commonplace, and they can alter original contract amount or completion dates.

Make version control around the payable event your first operating rule. If a later change order modifies scope, the advance request should reference both the prior approval and the updated record, not overwrite history. A reliable trail should let finance reconstruct request time, approver, amount, change history, and payout result from one traceable record set.

If you cannot produce that quickly, the model is not launch-ready. Previously approved scope changes can still require further design development, so treat older approvals as potentially incomplete until revalidated.

2. Put formal review thresholds on exceptions#

A modular model only works if exception governance is explicit before launch. Use named escalation tiers with written rationale for large or unusual advances.

A practical benchmark from change-order controls:

| Trigger | Governance action |

|---|---|

$1 million or more | Change Control Committee review and verification |

$25 million or more | Reported to full Board |

Use the same structure even if your thresholds differ: define who reviews, what evidence is required, and what gets escalated. For out-of-policy cases, require a brief Finding-of-Fact style note covering what changed, why policy still permits payout, what documents support it, and who approved.

3. Use rail combinations as optional lanes#

Modular rails are most useful when they stay optional and context-specific. Evaluate lanes such as MoR structures and other payout methods where supported, and keep stricter fulfillment-tied controls for higher-friction cases.

The key is not universality. Confirm availability, onboarding requirements, compliance constraints, and realistic payout timing for each country, entity type, and method before you make launch commitments. If ACH is in scope for your program, see Same-Day ACH for Platforms.

4. Make reconciliation and retry discipline a launch requirement#

A modular build is only an upgrade if traceability is tighter than a packaged alternative. Set transaction classifications from day one so you can clearly separate invoice advances, scope adjustments, reversals, fees, and manual corrections.

Use the same reporting mindset seen in standardized procurement coding: records should clearly show what each funded event represents. Then test retry behavior before rollout by replaying events in staging and confirming no duplicate financial outcome and one coherent audit trail per originating request.

For a step-by-step walkthrough, see How Platforms Reconcile Foreign Contractor Payments in QuickBooks Online.

Pick recourse structure before you talk about growth#

Decide risk ownership before growth planning. If an approved invoice is later disputed or unpaid, this choice can change your dispute posture and operating model.

- Treat risk ownership as the first contract test

Start with one question: after approval and payout, who is exposed if the buyer does not pay or the invoice is contested? If that answer is unclear, stop and resolve it. A useful benchmark from the June 6, 2023 interagency guidance is discipline across the full third-party relationship lifecycle, not assumptions from a contract label.

- If a contract uses Non-Recourse language, verify carve-outs in writing

The label alone is not enough. Confirm that eligibility, exclusions, dispute triggers, and controlling documents are explicit in the agreement, and escalate gaps before launch.

- Calibrate controls to risk profile and relationship context

Do not apply one blanket rule across all contractor segments. Consistent with the June 2023 principle, oversight should match risk level, complexity, size, and the nature of the third-party relationship.

- Clarify dispute and collections ownership before launch

"Approved invoice" is not the end of risk. Make sure the agreement clearly assigns who handles dispute communication, collections steps, and record updates. Keep a traceable record chain from approval artifact to payout record to dispute timestamp.

- Red-line ambiguity and verify legal references against official sources

FederalRegister.gov states its XML is not legal notice and that legal research should be verified against an official edition. It also links to the official PDF on govinfo.gov. Treat date updates seriously, for example a page published on 11/03/2023 and a newer related item on 01/22/2024. If responsibility language is ambiguous, force explicit allocation in the signed agreement.

Before signing any provider agreement, turn your risk-allocation and dispute-ownership terms into an implementation checklist in the Gruv docs.

Price the product so margin survives real losses#

Price the product so each cohort covers its own risk and operating load, not just the speed of payout.

- Build a full pricing table before setting any headline fee

Use one table with core inputs for every advance: payment-term length, expected cash-flow benefit, potential supplier price response, and target margin. If any key input is missing, treat the result as incomplete. Make the table segment-specific at minimum by supplier/category and payment-term bucket.

- Choose a fee shape that matches risk concentration

Flat pricing can work when segments behave similarly. If term behavior or supplier price responses differ by segment, use segment-based pricing and eligibility.

| Variant | Best fit | Main risk | | --- | --- | --- | | Flat fee | Similar suppliers, terms, and cost behavior | Strong segments subsidize weak ones | | Segment-based fee | Clear differences by supplier or category | Commercial friction if segment logic is unclear | | Term-bucket pricing | Meaningful mix of shorter and longer terms | Margin drift if hidden costs are not tracked by term bucket |

- Stress-test term mix and concentration before launch

Longer terms can support cash flow, but hidden costs can offset expected gains, including supplier price increases after term extensions. Scenario-test shorter- and longer-term mixes and concentration cases where one segment drives most volume and exposure. Given payment terms nearly doubled from 2019 to 2021 and remained materially above prepandemic levels, treat longer-term exposure as a normal operating condition.

- Use a clear decision rule for pricing and eligibility

If one segment drives most volume and most hidden-cost exposure, pricing and eligibility should be segment-specific, not global. Run reviews on a single operating view with account setup, monitoring, and issue-resolution data so margin pressure is visible early.

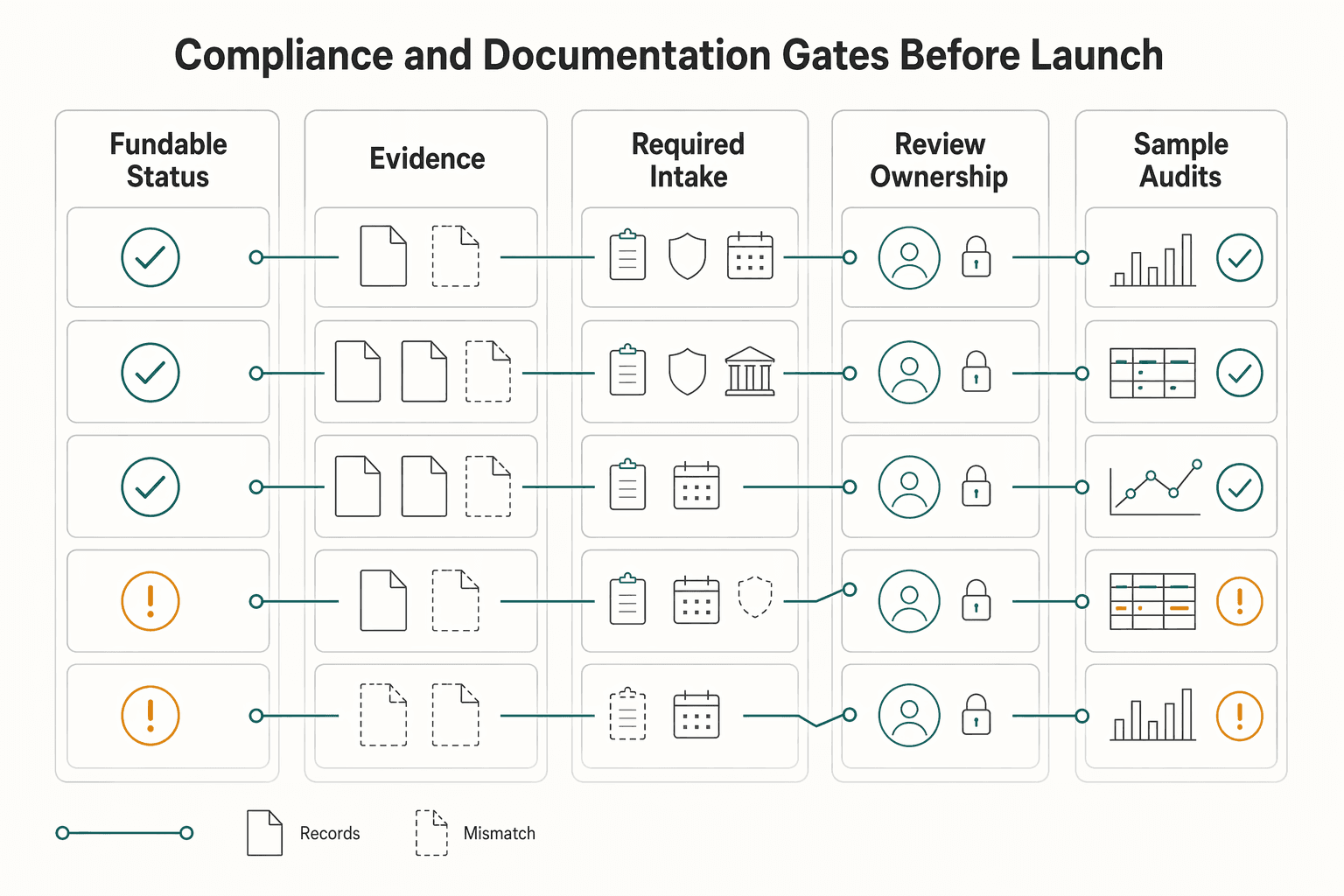

Compliance and documentation gates before launch#

Before launch, fund only the transactions you can justify from records in your own system, with a clear decision trail from review to payout.

| Gate | Requirement | Why it matters |

|---|---|---|

| Fundable status | Define one explicit state that means "eligible to fund" and make every payout path use it | Fast payout should follow that completed state, not bypass it through side workflows |

| Minimum evidence pack | Keep the approved invoice, supporting documents, contract records, and key timestamps in one reconstructible record | Documentation gaps and manual checks consume time and can escalate disputes |

| Required intake fields | Define the payment and invoice data needed before approval | This avoids chasing missing details after the first payout request |

| Review ownership | Keep a clear audit trail of who reviewed and approved each transaction | If teams can change records without clear accountability, tighten the process before launch |

| Sample audits | Pull funded samples and verify each can be rebuilt from request, review, approval, payout, and outcome | If a funded transaction cannot be reconstructed, it is not launch-ready |

-

Set one fundable status and make every payout path use it. If your program includes payment or invoice compliance reviews, define one explicit state that means "eligible to fund." Fast payout should follow that completed state, not bypass it through side workflows.

-

Require a minimum evidence pack for every funded transaction. Keep the approved invoice, supporting documents, contract records, and key timestamps in one reconstructible record. This directly addresses a known failure mode: documentation gaps and manual checks consume time and can escalate disputes.

-

Document required intake fields before funds move. Define the payment and invoice data your team needs before approval, instead of chasing missing details after the first payout request. The goal is operational clarity, not one vague path that creates preventable exceptions.

-

Define review and approval ownership up front. Treat record handling as a product and operations decision, with a clear audit trail of who reviewed and approved each transaction. If teams can change records without clear accountability, tighten the process before launch.

-

Run pre-launch sample audits for end-to-end traceability. Pull funded samples and verify each can be rebuilt from request, review, approval, payout, and outcome. A checklist-style review artifact is useful here: one example marks a payment accepted only after confirming GST at 10%, with subtotal $44,970, GST $4,497, and total $49,467.

If a funded transaction cannot be reconstructed from documents, statuses, and timestamps, it is not launch-ready.

Rollout sequence for the first 90 days#

Use the first 90 days to prove one narrow, controllable funding lane before you expand. Vendor material may claim 90 days to production versus 9-18 months and $500k+ for a custom build. Your launch decision should still come down to one question: can you fund, reconcile, and explain one cohort cleanly?

| Stage | Scope | Gate |

|---|---|---|

| Phase 1 | One cohort, one buyer segment, one funding trigger | Validate approval-to-payout timing on live transactions and keep eligibility strict |

| Phase 2 | Add batching, retries, and exception handling | Treat GL reconciliation and audit trail completeness as a gate |

| Phase 3 | Expand corridors and terms one change at a time | Expand only when dispute handling, recovery flow, and margin behavior remain stable in your own operating data |

| Adjacent levers | Keep rail speed and spend controls separate from the first advance-payment proof point | Avoid confusing faster money movement with sound eligibility and control design |

| Weekly dashboard | Track approval lag, funding lag, dispute aging, and reconciliation completeness in a single view | Operators should be able to explain a specific funding event quickly |

-

Phase 1: one cohort, one buyer segment, one funding trigger. Start with a single contractor cohort and a buyer segment where the trigger is operationally clear. In an Early Payment Program-style flow, GC invoice approval before subcontractor payment is a concrete trigger you can timestamp and audit. Keep eligibility strict, and validate approval-to-payout timing on live transactions before repeating acceleration claims like "30 to 90 days earlier." If your lane includes a fee tied to invoice amount, verify that fee is correctly recorded on each funded transaction.

-

Phase 2: add batching, retries, and exception handling before scale. Once the first lane is stable, enable payout batches and a finance-owned exception queue. Treat GL reconciliation and audit trail completeness as a gate, not a nice-to-have. Finance ops should be able to trace the approval artifact to payout to ledger outcome without manual reconstruction. Stress the lane with rejected payouts, retries, and delayed events, then confirm ownership and closure for each exception.

-

Phase 3: expand corridors and terms only after stability is clear. Add new corridors or terms one change at a time, then compare outcomes against the baseline cohort. Expand only when dispute handling, recovery flow, and margin behavior remain stable in your own operating data. Keep rollback simple if the new lane increases dispute pressure or slows recovery.

-

Adjacent levers: keep rail speed and spend controls separate from core proof. Treat faster payment-rail options and spend-control features as separate switches from the first advance-payment proof point. This avoids confusing faster money movement with sound eligibility and control design. If off-contract risk is already visible, tighten that first with Maverick Spend in Platforms: How to Stop Off-Contract Contractor Payments Before They Drain Margin.

-

Run one weekly operator dashboard that supports transaction-level answers. Track approval lag, funding lag, dispute aging, and reconciliation completeness in a single view. Each metric should drill into the underlying funding event, approval artifact, payout attempts, exception status, and reconciliation trail. If operators cannot explain a specific funding event quickly, expansion is early.

Red flags that mean pause expansion#

If funded volume is rising but your controls are getting harder to explain transaction by transaction, pause expansion.

-

Adoption rises, but economic risk is less clear. In repeat-billing setups, higher usage alone does not prove the lane is healthy. Repeat billing patterns, including monthly/quarterly cycles, can still carry chargeback risk, so pause expansion until dispute controls are clear.

-

Onboarding controls lag program complexity. If risk review relies on exceptions instead of clear onboarding guidelines, pause and tighten the process, because multi-merchant programs become harder to scale safely as onboarding complexity increases.

-

Volume grows faster than fraud prevention. On-demand payment flows can create risk pressure because higher transaction volume requires strong fraud prevention measures. If volume is scaling ahead of those controls, pause expansion and close the control gap first.

-

Operational integration is not ready for scale. Where funding depends on delivery or fulfillment events, confirm the PSP integrates cleanly with logistics systems to reduce transaction and tracking errors before broadening the program.

For the broader cash flow model behind payout timing, see How Payment Platforms Use DPO to Improve Cash Flow Without Reconciliation Risk.

The decision to make next#

Choose one model for one cohort, and do not scale until risk ownership, economics, and traceability are clear. If you test multiple models at once, demand can hide weak controls.

- Choose one pilot lane, not several

Start with the lane that matches the approval evidence you already collect. In construction-heavy flows, that often means milestone-driven approvals, since payment management is tied to contractual milestones and project timelines. Keep the first cohort tight enough that finance can manually review every funded transaction if needed.

- Validate operations before you treat demand as success

Demand for faster payouts can show up quickly because contractors often cover materials, crews, and equipment before client funds arrive, and many wait 30 to 90 days or longer for payment. The delay pressure is real: 82% of contractors reported delays over 30 days in 2024, up from 49% in 2022, and 95% of general contractors plus 75% of subcontractors report frequently floating payments.

Before scaling, confirm you can reconstruct each funded event end to end: progress reports, insurance coverage, licensure, payment details, and lien waivers where relevant. Missing documentation is a control failure, not a growth win.

- If you need control and cross-border flexibility, keep Gruv modular from day one

Use a modular Gruv setup when you want payout logic, compliance gates, and reconciliation visibility to remain explicit in your own operating model. That matters more as coverage expands, because platform governance is framed against public policy goals, including AML/CFT expectations, not speed alone.

Next step: align finance, product, and legal on contract red lines and the first launch dashboard before signing any provider agreement. If your team cannot clearly state who authorizes funding, which document releases payout, and how exceptions escalate, pause launch and fix that first.

If you are deciding between a single-vendor program and a modular build, validate coverage, compliance gates, and payout availability for your first cohort with Gruv.

Frequently Asked Questions

How can a platform pay contractors before delivery without taking credit risk?

A non-recourse structure can shift default risk off your balance sheet, but you should verify any carve-outs, reserves, or holdbacks in the agreement. Keep transaction evidence, including progress and retainage tracking where construction workflows apply.

What is the practical difference between early pay, Factoring, and guaranteed-funds models?

The practical difference is not the label. It is what the agreement and workflow define for payment timing, collections ownership, and dispute handling. If those points are unclear, two models with different names can create the same operational risk.

Who bears the loss if the buyer never pays after an invoice is approved?

Do not infer this from marketing copy. Loss ownership has to be explicit in the agreement, including whether reserve, holdback, or clawback terms can shift exposure back to you. If that is ambiguous, pause launch.

When should we choose Recourse instead of Non-Recourse?

Use recourse only when you can tolerate collections activity and potential loss exposure. Prefer non-recourse when lower credit-risk exposure is the goal, and verify carve-outs before assuming risk is fully transferred.

What should founders verify in contracts before enabling advances?

Verify payment-timing terms, loss ownership, dispute path, and any reserve or holdback rights in writing. Also check payment-timing commitments against prompt payment laws, because timing rules and non-compliance penalties vary by location. Use a location-based prompt payment requirements check before making rollout promises across mixed jurisdictions.

How do we price contractor advances so we do not destroy margin?

Do not price on payout speed alone. A high-overdue environment and wide term ranges need to be reflected in your economics. A headline like 90% within 24 hours is not a margin model by itself.

Which controls are mandatory before cross-border rollout?

Run a location-by-location legal and contract review of payment timing rules and non-compliance exposure before rollout. Treat those jurisdiction checks as a pre-launch gate before scaling.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- acquisition.gov/afars/appendix-aa-table-contentstrusted

- acquisition.gov/sites/default/files/manual/PSC%20Manual%20Ap...trusted

- clintontwpnj.gov/_Content/pdf/2026-03-12-Transmittal-of-Amend...trusted

- comptroller.war.gov/portals/45/documents/fmr/current/10/10_10.pdftrusted

- connect.ncdot.gov/letting/Design%20Build%20Program/R-5777C/R-5...trusted

- dodcio.defense.gov/Portals/0/Documents/CMMC/AG_Level2_MasterV2....trusted

- dot.ca.gov/-/media/dot-media/programs/design/documents/...trusted

- dot.ga.gov/PartnerSmart/DesignManuals/Program%20Deliver...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Same-Day ACH for Platforms: How to Speed Up Contractor Payments Without Wire Transfer Fees

---

Maverick Spend in Platforms: How to Stop Off-Contract Contractor Payments Before They Drain Margin

Off-contract contractor payments become dangerous when they repeat. Small off-policy spend adds up, fragments data, and weakens compliance. Teams usually discover it later during invoice review, audit, or reconciliation.

Virtual Credit Cards for Platforms: How to Issue Single-Use Cards for Contractor and Vendor Payments

Single-use virtual cards are often positioned as a fit for controlled vendor payments, but not for every contractor payout. This guide helps product, Payments Ops, and AP teams decide whether virtual cards fit their operating model, or whether cards belong alongside ACH, checks, or other payout rails.