Quick Answer

Validate contractor bills before payment by making invoice verification a payout gate. Confirm the invoice is proper, contract performance is satisfactory, payee details have passed the separate payee check path, matching and math checks are within tolerance, duplicates are cleared, coding is complete, and all exceptions or holds are resolved before payout authorization is available.

Why this matters before you release contractor payouts#

Treat invoice verification as a payout gate, not a back-office cleanup step. If a contractor bill can reach payout authorization before it clears your checks, you do not just have an AP process gap. You have a release-control gap.

Step 1 Treat validation as a release decision#

The core question is simple: should this bill be allowed to release money right now? That frame carries through the rest of this guide.

In SAP, Logistics Invoice Verification is described as checking invoice content, prices, and arithmetic before posting, and the process updates records in both Materials Management and Financial Accounting. That ties verification to financial state, not just document intake.

Oracle reflects the same control pattern through invoice holds. Invoices cannot be paid until holds are released. For platform payouts, your validation result should determine whether payout authorization is available at all, not whether AP sees a warning after payment is already scheduled.

One practical red flag is easy to spot. If invoice review sits in the back office but Engineering can still trigger payout on receipt, your control order is backwards.

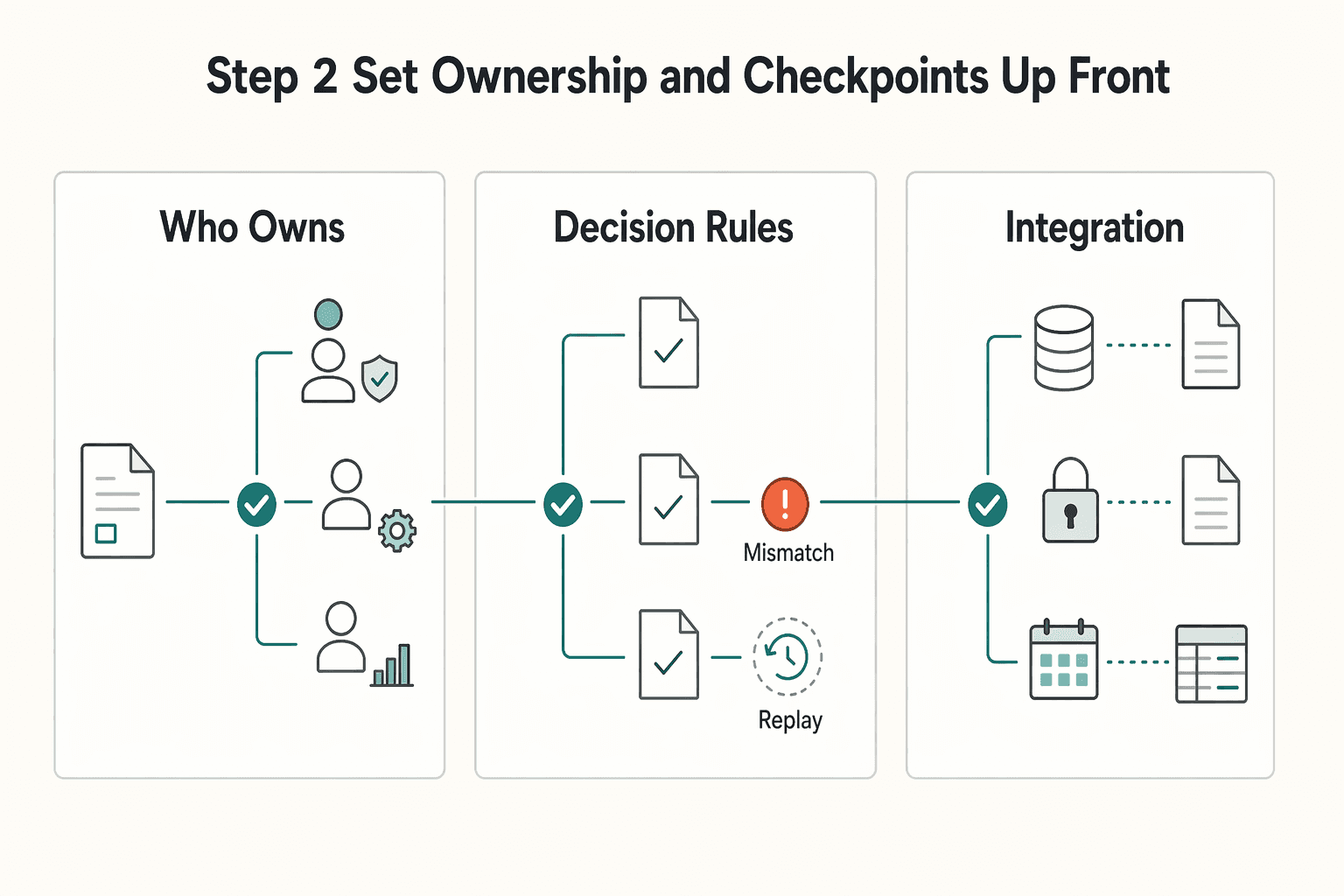

Step 2 Set ownership and checkpoints up front#

The job here is controlled release, not nicer bookkeeping. You need a clear path from bill intake to approval workflow to payout authorization, with an audit trail you can defend later. Use three operating checkpoints:

| Checkpoint | What it covers |

|---|---|

| Who owns release decisions | Finance Ops defines pass criteria, hold conditions, and exception override authority |

| What the decision rules are | Set explicit pass, hold, reroute, and release rules, including how to handle missing support or mismatched amounts |

| Where integration checkpoints sit | Approval must occur before payout authorization, and retries must not create duplicate releases |

Auditability belongs inside release control, not after it. Oracle Payables documents a full audit trail for current and released invoice holds, so your process should preserve traceable hold and release records.

Event reliability is another common failure point. Stripe notes webhooks can be delivered more than once, and its API idempotency model exists to prevent duplicate operations. If approval or payout-ready events replay, deduplicate them before funds move.

Step 3 Keep scope tight#

This article covers validating contractor bills before payment. It does not replace payee verification, which answers a different question: who receives funds. Adyen states account holders must pass verification checks before payouts are enabled, and Stripe Connect states charges and payouts are not enabled until verification requirements are met. For that layer, see Payee Verification at Scale: How Platforms Validate Bank Accounts Before Sending Mass Payouts.

It is also not a vendor bake-off. Public evidence does not support a like-for-like pricing or performance benchmark across this segment. BILL publishes at least one list price tier ($49 per user/month for Essentials), while Stampli and ServiceTitan use request-led pricing pages. So this guide stays focused on control design, ownership, and release logic.

If off-contract work is part of the problem, Maverick Spend in Platforms: How to Stop Off-Contract Contractor Payments Before They Drain Margin shows how platforms stop those invoices earlier in the flow.

What invoice verification means in a platform payments stack#

In a platform payments stack, invoice verification is a pre-release control. The bill needs a clear outcome before payout authorization is available. In practice, teams often use explicit validation outcomes such as pass, hold, or exception, and only a clean outcome should move forward.

Step 1 Define the handoff from bill check to payout release#

Bill checks answer one question: what should be paid now, if anything. Payout authorization answers another: can funds move now.

Keep those controls separate but tightly linked. Even if an invoice is approved in AP or ERP, it should stay non-payable until any required payment-approval stage clears and the payout system receives release.

Step 2 Separate payee checks from invoice checks#

Payee verification and invoice verification are adjacent controls, not substitutes.

| Control | What it confirms | When it runs |

|---|---|---|

| Payee verification | Who gets paid, including recipient account and name details | Before payment is sent |

| Invoice matching and validation | What should be paid, including invoice, PO, and receipt matching, tolerances, duplicate checks, and exception handling | Before payment or accounting release |

If you need both outcomes, run both control paths.

Step 3 Anchor the table-stakes checks#

An AP-only view is incomplete. Fast payout rails can be final and irrevocable, and you still have to reconcile approved invoices to what the payout provider settled, often through settlement batches.

At minimum, pre-release checks should confirm:

- recipient or payee details have passed the separate payee check path

- invoice matching and math checks pass, including quantity checks against receipts and price tolerance checks where configured

- duplicate-invoice checks pass

- all exceptions are resolved before processing continues

- the invoice is validated and any required payment-approval review is complete, not just captured in AP

That is the release decision before contractor funds leave your platform.

Related: What Is Invoice Factoring? How Platforms Can Offer Early Payment to Contractors in Cash Flow Crunch.

Assign ownership before you automate any rule#

Once you have pass, hold, and exception states, assign explicit owners before you automate release. If release policy is fuzzy, automation will only make bad decisions faster.

Step 1 Name one accountable owner and one technical owner#

Set one accountable owner for release policy and one technical owner for execution across invoice, ERP, and payout integrations. Teams often put these roles in different functions, but titles matter less than clear authority.

This follows basic internal-control design: assign responsibility, delegate authority, and separate duties to reduce fraud and abuse risk. Even when invoice review is delegated, one role should remain end-to-end accountable for funds released. Keep a single approval matrix, config registry, or control document that names both owners, backups, and dispute escalation contacts.

Step 2 Split policy decisions from execution decisions#

Write the boundary down. Policy decides what must be true before payment. Execution makes sure the system enforces that policy correctly. Policy decisions include required evidence, approvers, tolerance logic, and when an invoice goes to Approval workflow versus Exception handling.

Execution decisions include retry safety and event sequencing. Retries should not create duplicate release actions, and systems that depend on sequence should define how ordering is preserved. If policy can change in one system while payout gating still runs old logic somewhere else, the process is not fully controlled yet.

Step 3 Use a temporary manual control until ownership conflicts are resolved#

If release authority is split and there is no clear tie-breaker, consider a temporary manual hold or review gate until ownership is resolved. This is an operational control choice, not a universal legal rule.

Be strict when AP approval and payout release happen in different systems. "Approved" in one tool is not enough unless a named owner confirms that the same invoice version is still eligible for release now. Take one disputed invoice and confirm who can approve, who can deny, and who can override. If that answer is unclear, ownership is still incomplete.

Step 4 Define a dispute path so exceptions do not block everything#

Exceptions need a route, an owner, and a response expectation. Without that, every disputed invoice becomes a one-off case and clean invoices get dragged into the same queue.

Create a named dispute path with routing, response timing, and a decision owner. Defined reporting lines are part of control design, and they matter most when invoices are contested.

Keep disputed invoices in a separate exception flow with visible status ownership, so clean invoices can continue through normal release controls. As a process design reference, federal disputes language shows that unresolved or disputed payment requests can escalate. FAR 52.233-1 includes a 60-day decision timeline for certain written contractor claims of $100,000 or less. You do not need to adopt federal rules directly, but you should set internal escalation triggers and response targets.

If you are redesigning the broader payout workflow, Build a Contractor Payment Flow for Home Services Marketplaces walks through the end-to-end contractor payment flow in more detail.

Gather prerequisites and evidence before first rollout#

Do not turn on blocking or auto-release rules until your evidence set, intake fields, and audit history are defined. Early rollout issues often come from weak inputs and missing records, not rule logic.

Before you start: treat this as intake design and controls design. If invoices enter your flow without the required fields or support documents, automation will only scale bad input.

Step 1 Prepare the records you will treat as canonical#

Pick the records that prove an invoice is payable, and make sure an operator can retrieve them under one invoice reference. For purchasing-led flows, that commonly includes the Purchase order and the invoice, plus any contract or rate record your team relies on. If your process depends on delivery or completion, also link receipt or acceptance proof. Add timesheets or prior change approvals only when they are part of your control model.

Set matching depth based on the evidence you actually keep. Oracle documents 2-way / 3-way / 4-way matching, from invoice-to-PO through receipt and acceptance-document checks. Your Line-item matching control should reflect the records you maintain, not the records you wish you had.

Verification point: sample five historical invoices and confirm an operator can retrieve the full support set in minutes. Red flag: if support depends on Slack, email, or memory, keep those invoices out of auto-approval until records are captured in a durable system.

Step 2 Define required intake fields before enabling automation#

Write the required fields for imported invoices before validation runs, and map each field to a system of truth and an owner. A practical baseline can include supplier identifier, document currency, and GL coding distribution data, then any additional fields your stack requires, for example tax or cost-center coding.

Oracle import runs one row per invoice and can reject records when required-field values are invalid. Oracle documentation also includes VENDOR_ID for supplier identifier. SAP S/4HANA supplier invoice metadata includes explicit inputs like COMPANYCODE and DOCUMENTCURRENCY. Use that pattern to decide what must be valid before payment logic runs.

Verification point: for every required field, document where it comes from and who corrects bad values. Failure mode: teams defer cost-center or tax data, then discover invoices can pass review but still fail clean posting.

Step 3 Confirm every system touchpoint and its history record#

Before you automate release, map the path from source invoice tool to ERP to payout engine, and confirm which status and evidence records survive each handoff. If intake starts in a portal, EDI feed, or another source tool, document how that record becomes an ERP invoice and what history stays visible.

Require audit history that supports dispute review. SAP documents read-only invoice audit trail history with events like submission, approval or payment-status changes, comments, and exception generation. Oracle audit tracking can capture who changed invoice fields and when. That level of history makes blocked-bill investigation workable.

Step 4 Build a minimal dispute evidence pack#

Once the records and touchpoints are clear, standardize what reviewers need for a blocked invoice. Keep the pack compact and consistent so disputes do not depend on who happens to pick up the case. Start with:

- invoice image or source invoice record

- linked PO, receipt, or acceptance proof, as applicable

- contract excerpt or approved rate reference, if used

- timesheet or change approval, if applicable

- exception reason

- actor, timestamp, and comment history from the audit trail

Verification point: give one disputed invoice to someone outside AP and check whether they can understand the hold reason without extra context. If not, tighten the pack before expanding automation.

For a step-by-step walkthrough, see How to Build a Payment Sandbox for Testing Before Going Live.

Build the minimum pre-payment control set#

Once your evidence pack is stable, turn it into a short control matrix and gate payout on matrix results, not reviewer habit. Authorization to pay should depend on a small set of critical checks that are visible, owned, and repeatable right before money moves.

Step 1 Build a control matrix operators can run consistently#

Use a decision sheet for each invoice state change, with columns for control name, trigger, pass criteria, block criteria, owner, and release SLA. That exact structure is not universal, but it helps prevent vague approvals from turning into payout decisions.

Run controls at the points where they matter: identity at intake, duplicate checks again at posting or approval submission, and a final release-state check right before payout. If invoice data changes after approval, force revalidation.

Define pass and block criteria against canonical records. FAR 32.905 is a useful anchor. Payment is based on receipt of a proper invoice and satisfactory contract performance, and proper invoice content includes contractor identity, invoice date and number, and contract or order reference.

Step 2 Set minimum controls and make the logic explicit#

Use the smallest set that still covers payee identity, billing entitlement, billed amount, duplicate risk, and posting readiness.

| Control | Trigger | Pass criteria | Block criteria | Owner | Release SLA |

|---|---|---|---|---|---|

| Identity and vendor validity | Intake, pre-payout recheck | Contractor record is valid, invoice includes identity fields, payee details map to approved payee record | Missing or mismatched identity, invalid vendor, unresolved payee mismatch | Finance Ops with platform ops support | No release until corrected |

Contract or Purchase order linkage | Intake or approval submission | Invoice references approved contract, order, or other authorization with line context where required | Missing valid linkage or unsupported billing basis | Finance Ops or procurement owner | No release until linked evidence is added |

Line-item matching | Posting or approval submission | Invoice lines match approved order and, where used, receipt or acceptance records within tolerance | Quantity, price, or amount variance exceeds tolerance | Accounts Payable or Finance Ops | Route to manual review |

| Duplicate detection | Intake, posting, pre-payout recheck | No duplicate found after normalized checks | Suspected duplicate based on supplier plus invoice attributes or normalized invoice fingerprint | Accounts Payable | Immediate hold |

GL coding completeness | Before posting | Accounting distributions are complete and valid for posting | Missing or invalid distributions needed for ledger entries | Finance Ops or accounting | No posting, no release |

Keep invoice validation and payee pre-validation separate, but connected. BIS describes confirmation of payee as pre-validation before payment initiation and associates pre-validation with fewer rejections and less manual intervention.

For linkage, do not treat "service completed" on its own as enough. FAR 32.905 ties payment to a proper invoice and satisfactory performance, including contract or order reference and line context.

Use tolerances for matching, then enforce them. Microsoft documents two-way and three-way line matching and tolerance-based discrepancy handling. SAP documents payment blocking when configured upper limits are exceeded.

Run duplicate controls beyond invoice-number equality. Oracle documents duplicate checks using supplier, invoice type, amount, currency, and date. It also warns that duplicates can still slip through supplier-name variation or invoice-number case differences.

Treat GL coding as a release control, not admin cleanup. Accounting distributions allocate invoice amounts to ledger accounts and support journal creation. Incomplete distributions can break clean posting.

Step 3 Add a release-state gate before Payout authorization#

Approval status alone is often not enough. Set a clear policy for Payout authorization: define which critical controls must pass and how unresolved critical exceptions are handled. Release should depend on control status, not approval status by itself.

Keep Exception handling state visible on each invoice: critical-controls status, unresolved critical exception count, and last validation timestamp. Re-run critical checks when any release-relevant data changes after approval.

Verification point: trace three passed and three blocked invoices from intake to payout decision. You should be able to show the pass or block reason, the exception owner, and that payout state never advanced before critical checks cleared.

Step 4 Tier hard blocks and soft warnings deliberately#

Do not let everything become a warning. Failures that affect who gets paid, whether the bill is payable, or how much is paid are common hard-block candidates. Identity mismatch, duplicate suspicion, and over-tolerance amount variance are often handled in this tier.

Use warnings for gaps that do not change entitlement, amount, or posting readiness. If a field gap prevents valid posting, treat it as a block condition. If a control affects payee identity, payable amount, billing entitlement, or clean posting, consider blocking until it is resolved.

If your team is turning this control matrix into enforceable payout gates, map each pass or block rule to your payout states and retry behavior in the Gruv docs.

Set auto-approve and manual-review rules that teams can enforce#

Once hard blocks are in place, make routing explicit. Invoices that meet your required controls can auto-approve. Invoices missing evidence or needing judgment should route to manual review with a named owner. Write that logic in plain language first, then implement the same rule in your Approval workflow.

Step 1 Write the rule in business language before configuration#

Use one testable policy sentence across finance, Accounts Payable, and engineering: if required controls pass and required evidence is present, the invoice can auto-approve under your risk policy. Otherwise, it routes to review or is blocked.

This keeps you out of the common trap where ERP conditions exist but no one can explain the actual approval policy. Oracle's invoice approval guidance shows this pattern directly: convert business requirements into explicit rules, including spreadsheet rules, before system setup. Microsoft makes the dependency just as clear: touchless processing requires a configured Vendor invoice workflow.

Checkpoint: replay five historical invoices with known outcomes and document why each was approved or routed. If reviewers disagree on the reason, tighten the rule before automating it.

Step 2 Define clear auto-approve, review, and block paths#

Amount can be a trigger, but it should not be the whole decision. Route by evidence quality and policy, not by amount alone. The real question is whether entitlement and posting readiness are provable from your records.

| Scenario | Required evidence at decision time | Route |

|---|---|---|

| Clean invoice with complete evidence and control passes | Valid contract or order linkage, acceptance support where needed, no duplicate hold, complete coding | Auto-approve if it meets your low-risk policy |

| Invoice that meets core controls but needs human judgment | Control results are complete, but threshold or exception policy requires approver judgment | Manual review |

| Invoice missing required authorization details | Missing requester, authorizing detail, or other required approval evidence | Block or reject per policy |

Oracle's sample rule set illustrates this structure. Invoices below USD 5000 can auto-approve, and invoices at USD 5000 and above can route to finance approval. Some Purchase order-matched invoices can bypass specific rules, and unmatched invoices without requester details can be auto-rejected.

Step 3 Define when two-person control is required#

Use two-person approval where one person could override a meaningful protection on their own. NIST defines the two-person rule as a Separation of Duty mechanism.

For invoices that already passed controls, decide whether a second approver is required by your policy and risk tolerance. A practical policy is to require two-person approval for defined override scenarios, with a reason code in the audit trail.

Step 4 Expire stale approvals so old tasks cannot drive release#

Old approvals can create release risk. Set explicit expiration policies for approval tasks and require revalidation when release-relevant fields change after approval. Do not rely on due dates alone.

Oracle is clear that due dates do not expire tasks by themselves. A task due in 14 days can still remain open, and Oracle notes a 180-day withdrawal reference for still-open tasks when expiration is not configured. Use expiration plus revalidation so outdated approvals cannot be reused for late Vouchering or payout release.

Verification point: confirm an approval outside your policy window is in a final expired state. Then edit a release-relevant field and verify prior approval is no longer valid for release.

Step 5 Track manual-review backlog as an operating control metric#

The review queue is not just admin work. It is a control signal. Track backlog by count, value, and age, plus oldest-item age, and watch end-to-end cycle time from invoice receipt to payment.

AP benchmarking tracks cycle-time performance, and AP training material treats backlog growth as a bottleneck signal. Also account for blocked items that may not re-enter automated follow-up until manual action. If queue age rises, inspect root causes such as intake quality, requester data, rule design, and capacity.

Handle exceptions without slowing payout SLAs#

Exception handling should be fast, predictable, and strict where it needs to be. The goal is to route issues into clear classes, block payment for critical risk, and keep the same exception language across finance, ops, and engineering.

Step 1 Classify exceptions by recoverability#

Use four stable buckets:

- Missing document: required evidence is missing, for example receipt or acceptance support.

- Rate or quantity mismatch: a matching discrepancy between invoice,

Purchase order, and receipt data. - Duplicate suspicion: the invoice may already exist, and duplicate checks can return warning or error outcomes based on configuration.

- Payee mismatch: the invoice may be valid, but payee details do not align with

Payee verificationresults.

Default payee mismatch and strong duplicate suspicion to critical. Treat missing documents and some matching discrepancies as recoverable only if evidence can be supplied and rechecked before release.

Step 2 Attach one default recovery action to each class#

Give each class one standard next step so the queue does not turn into ad hoc casework.

| Exception class | Default handling | Recovery action |

|---|---|---|

| Missing document | Recoverable only if evidence can be supplied and rechecked before release | Request the artifact with owner and timestamp; if a required receipt is missing, keep payment authorization blocked until receipt entry |

| Rate or quantity mismatch | Some matching discrepancies are recoverable only if evidence can be supplied and rechecked before release | Fix the actual source issue, then re-run Line-item matching; update GL coding only when coding is the real gap |

| Duplicate suspicion | Strong duplicate suspicion is critical | Use a stricter path for higher-risk cases, meaning error or payment hold, not routine reviewer dismissal |

| Payee mismatch | Critical | Route to pre-payment payee verification resolution before release |

Step 3 Enforce timer-based actions and payout blocks#

Critical exceptions should place the invoice on hold or keep it blocked until resolved. If an exception is unresolved, payout does not proceed.

For non-critical exceptions, allow overrides only where configured privileges permit them, and require a complete Audit trail of hold and release actions. Use workflow escalation when assignees do not act in the allotted time.

Verification point: test one invoice per class to confirm a critical payee mismatch cannot be released and a permitted non-critical override records complete hold and release history.

Step 4 Review false positives and rule drift on a set cadence#

Review exception outcomes on a fixed cadence so exception handling does not become a hidden drag on payout speed. Focus on alerts that are technically valid but operationally low-value, for example repeat duplicate warnings that are later cleared.

Track by class: volume, resolution without override, and reopen rate after initial resolution. If volume rises while confirmed issues stay flat, tighten or prune rules before reviewers drift into alert fatigue.

Integrate ERP and payout systems without duplicate releases#

The safest integration pattern is simple: make retries idempotent, require upstream finance states before payout, and reconcile payout outcomes against ledger postings every cycle.

Step 1 Design one idempotent release key and reuse it on retries#

Create one unique key for one intended release, then send that same key on retries for each endpoint that supports idempotency. Stripe supports idempotency for safe retries without double execution, and PayPal warns that omitted request IDs can lead to duplicate requests.

Keep the key deterministic and stable across systems. Some APIs cap idempotency values at 64 characters, so avoid long composite keys that may truncate differently across services.

Reuse a key only for the same intended operation. If payable amount, payee, or currency changes, issue a new versioned key and store both the key and the final outcome in your internal release record.

Verification point: in staging, force a timeout on the first call and retry with the same key. Confirm one downstream payout object and one recorded release decision.

Step 2 Enforce state order before payout can fire#

Do not let payout fire from an approval event alone. It should run only after required upstream states are complete, and the release path should check current persisted finance state before moving funds.

Oracle Payables states invoice validation is required before payment or accounting entries. JD Edwards states a voucher must exist before supplier payment. Use those gates in your orchestration so release attempts without the expected validated invoice state, and voucher state where applicable, are rejected.

Step 3 Document ERP mappings before you ship the connector#

Different ERPs do not need field-identical mappings, but they do need explicit mappings for statuses, document references, and ownership when retries or sync issues happen.

| ERP target | Mapping point to document | Why it matters |

|---|---|---|

| SAP ERP | Logistics Invoice Verification result and posted invoice reference | SAP LIV verifies invoice content, price, and arithmetic, and posting updates Materials Management and Financial Accounting records |

| JD Edwards | Voucher creation status and voucher number | Voucher creation is required before payment, and 3-way voucher matching can create a voucher |

| Infor Lawson | AP Invoice Automation integration point into Infor Lawson Financials | Infor documentation explicitly describes integration to Infor Lawson Financials |

Document at least the source field, target field, allowed statuses, retry owner, and authoritative status when systems disagree.

Step 4 Reconcile ledger postings to payout states every cycle#

Approval logs alone do not prove completeness. Reconcile voucher or ledger posting records to payout authorization, then to settlement batches or provider reconciliation reports.

Stripe provides payout reconciliation reporting for transactions in each payout batch. Adyen and PayPal also provide reconciliation reporting for payout tracking and finance/accounting reconciliation needs. Use those outputs with ERP posting extracts so each release ties invoice ID, voucher or posting ID, payout ID, settlement batch, and final status.

Include unmatched items in month-end evidence, not just matched items. Investigate one-sided outcomes immediately: posted but not paid, or paid without the expected voucher or posting reference.

Choose tooling based on control depth and integration reality#

Choose tooling based on where your payout risk actually sits. Buy for strong review queues and integration depth, and build only the narrow controls you cannot buy cleanly. If your team is not strong at exception handling, start with software that gives reviewers a clear queue, durable history, and exportable evidence before you add custom automation.

Step 1 Score tools on the few capabilities that decide payout risk#

Do not score vendors on broad AP messaging alone. For payout-gated invoice review, focus on the capabilities that change release risk:

- Rule configurability for hard blocks versus soft warnings

- Exception queue quality so reviewers can clear backlogs predictably

- ERP connectors that match your real environment, including on-premises needs

- API and webhook maturity for status sync and payout gating

- Audit trail exportability so Finance can show who did what and when

Ask for a demo on your messiest invoice type, not a happy path. Have the vendor show a failed match, reviewer handoff, correction, and exported evidence you would retain at month end.

Step 2 Separate scope categories before you shortlist vendors#

These references are different scope categories, not like-for-like substitutes.

| Reference | What the public evidence supports | Likely fit |

|---|---|---|

| Stampli | AP/P2P scope, approval queue, invoice audit trails, and 70+ ERP integrations with API and bridge options | Teams that need strong approval handling plus broad ERP connectivity |

| BILL | Financial operations platform across AP/AR/spend-expense, with webhooks and approval-audit CSV export | Teams that want programmable finance events but still validate payout correctness outside webhook delivery alone |

| ServiceTitan | Service-business AP with approval routing, 3-way matching, and bill/credit/payment export to XLSX | Teams operating in service-business workflows |

| Beam.ai | AI-agent invoice processing positioned around automation and compliance improvements | Teams exploring automation support that still need to verify control depth |

| IntelliChief | Older 2017 AP/ERP automation evidence | Historical reference, not a current capability benchmark here |

Step 3 Test integration reality, not feature lists#

Feature lists are the easy part. What matters is whether the tool works in your actual environment. Stampli's API and bridge positioning plus 70+ ERP support matters if your finance stack is mixed cloud and on-premises. BILL's developer platform and webhooks matter if you need event-driven gates.

Do not release funds from webhook events alone. BILL explicitly warns webhooks are not the only source of truth, so require a second check against system records before payout.

Step 4 Build only when the missing gap is narrow and high-control#

If you already run mature internal controls and clear approval ownership, a targeted build can be a practical alternative to replacing your full AP layer. Keep the existing review process and build only the missing payout gate, status normalization, and reconciliation links.

If reviewer operations and evidence export are weak, start with tooling that gives you strong queues. Before signing, run one export test and confirm you can pull review history and transaction outputs into month-end evidence.

Fix common failure modes before they become finance incidents#

Common payout failures are stale approvals, duplicate risk, and payable-state gaps that often show up after money moves. Treat release as a fresh control point so you catch them before funds leave the platform.

Step 1 Revalidate approvals right before release#

Check the live invoice state at release time instead of trusting an older approval. If key fields changed after approval, send the invoice back through review before payout.

PeopleSoft supports this control pattern: an approved but unpaid voucher can return to pending when certain fields change. If you use approval tokens, treat them as an internal design choice and compare them against the live payable record before release.

If payout requests can retry, use idempotency keys so retries do not create duplicate effects. Also keep your own audit trail, because API idempotency windows are not a substitute for payment-history evidence.

Step 2 Normalize duplicate checks before the ERP sees a "different" invoice#

Native duplicate checks help, but they can miss edge cases. SAP's duplicate logic uses fields like supplier, currency, and gross amount, and SAP also documents a recreate-after-cancel case where a duplicate message may not appear.

Add a normalized duplicate check in your release flow to reduce the chance that formatting differences bypass controls. Compare normalized invoice identifiers together with payee and amount, and retain both original and normalized values so reviewers can explain why a duplicate was flagged or cleared.

Step 3 Gate payout on successful payable approval and hold state#

Do not release payout from validation alone. Release only when the payable record exists, is approved, and is not on hold.

PeopleSoft is explicit that a voucher cannot be paid unless approved. Oracle Payables also blocks held scheduled payments until holds are removed and provides hold history, which gives Finance evidence for review and audit.

Step 4 Triage exception handling before the queue becomes permanent#

Exception queues become operational debt fast if no one owns them and no one tracks age. Assign one accountable team, classify exception types, and watch queue staleness as an operating metric.

If your queue runs on SQS, ApproximateAgeOfOldestMessage is a practical staleness signal. When backlog stays high while consumer concurrency stays low, fix capacity or intake quality before adding more rules.

Related reading: Webhook Payment Automation for Platforms: Production-Safe Vendor Criteria.

Execute a 30-day rollout with verification checkpoints#

Run this as a staged launch, not a day-one hard block. Use a 30-day operating cadence, or similar, to prove that validation, holds, approval routing, and payout gating work in production before you rely on them to stop or release money.

| Stage | Focus | Output |

|---|---|---|

| Week 1 | Lock ownership, publish the control matrix, and define the evidence pack for blocked invoices | For every high-risk rule, show one pass case, one blocked case, and the supporting artifacts |

| Week 2 | Run checks in production as read-only and measure noise | Sample each major alert type and compare rule output to human decisions; track legitimate issues versus noise |

| Week 3 | Enable blocking for duplicate risk, major tolerance mismatches, and exception conditions that should create holds | Monitor Exception handling throughput, queue age, and SLA breach risk daily |

| Week 4 | Use controlled cutover to broader payout gating after readiness review | Verify end-to-end reconciliation is clean from invoice decision through Payout authorization and audit export |

| Month one close | Publish an operating report, not a status note | Pass rate, exception aging, duplicate-prevention outcomes, and unresolved risks |

Oracle sets the control baseline: invoice validation must happen before payment or accounting entries. So this rollout is a release-control change, not just a process improvement.

Step 1 Lock ownership and test against known outcomes#

Use week 1 to lock ownership, publish the control matrix, and define the evidence pack for blocked invoices. If ownership or evidence standards are still moving, delay launch.

Dry-run a sample of historical invoices with known outcomes where available. For each high-risk rule, confirm that it fired when it should, stayed quiet when it should, and left a clear audit record a reviewer can defend.

Week 1 checkpoint: for every high-risk rule, show one pass case, one blocked case, and the supporting artifacts.

Step 2 Turn on read-only checks and measure noise#

In week 2, run checks in production as read-only. Measure noise, including false positives, and confirm Approval workflow sends questionable invoices to review without over-routing clean invoices.

NetSuite's model is a practical benchmark: routing criteria decide whether approval is needed, and only incorrect or questionable invoices require supervisor or billing-manager review.

Week 2 checkpoint: sample each major alert type and compare rule output to human decisions. Track legitimate issues versus noise.

Step 3 Block only the highest-risk cases first#

In week 3, enable blocking for the highest-risk conditions first: duplicate risk, major tolerance mismatches, and exception conditions that should create holds.

Oracle supports holds for exception conditions, and SAP documents payment blocking for tolerance breaches, including R in Payment block. But do not assume identical SAP behavior in every setup. Verify that downstream payment is actually stopped.

Week 3 checkpoint: monitor Exception handling throughput, queue age, and SLA breach risk daily. If age rises as blockers rise, tune rules or increase reviewer capacity before expanding blocks.

Step 4 Go live on payout gating and verify end-to-end traceability#

Use week 4 for controlled cutover to broader payout gating after readiness review. Treat go-live as a formal step sequence, not an ad hoc switch.

Verify the full chain from decision to payout: invoice decision, approval completion, hold or block behavior, payout authorization, and Audit trail export. Also validate retry safety now. If payout or invoice requests can retry, use idempotency keys so retries do not create duplicate side effects.

Week 4 checkpoint: end-to-end reconciliation is clean from invoice decision through Payout authorization and audit export.

Step 5 Publish month-end control results and unresolved risks#

Close month one with an operating report, not a status note: pass rate, exception aging, duplicate-prevention outcomes, and unresolved risks.

Use your own breach lines and state them clearly. The point is shared visibility across Finance, Ops, and Engineering on whether too many good invoices are blocked, risky invoices still pass, exceptions are aging, or manual gaps remain.

Put payout safety and speed on the same operating standard#

Use one release standard across Finance, Ops, and Engineering: no payout path should go live unless shared controls, owners, and gates are enforced end to end.

- Define accountable owners for release policy and rule execution.

- Publish a control matrix with pass criteria, hold or block criteria, and exception-handling ownership.

- Configure decision rules for automated checks, manual review, hold placement, and hold release.

- Test idempotency on every retryable payout authorization path.

- Set and document exception response expectations by severity.

- Lock pre-release gates so payout cannot bypass validation or approval.

Treat the release path as a sequence: Invoice validation -> Approval workflow -> Vouchering -> Payout authorization. If validation places a hold, including tolerance-driven holds or invalid-account conditions, payment should not proceed until that hold is explicitly released.

Before rollout, test at least three scenarios: a clean pass, a tolerance-based hold, and a retry using the same idempotency key. In each case, confirm the approval or rejection history is recorded, voucher state matches the invoice decision, and your audit trail captures the field-level changes you rely on for review.

Keep scope explicit before enforcement. If coverage differs by country, platform-country setup, connected-account program, or enabled features, document that in the controls and rollout notes rather than presenting one global standard.

Align finance, ops, and engineering, then run a read-only validation pilot before turning on hard blocks. Let checks run and exceptions log first, review the outcomes, then enforce blocking in phases once the path is stable.

When you are ready to operationalize these checks in live money movement, review how Gruv Payouts supports compliance-gated releases, status tracking, and audit-ready payout flows. ---

Frequently Asked Questions

What must be validated before releasing payment to a contractor?

Before releasing payment, validate that you have a proper invoice and satisfactory contract performance. Match the invoice to the supporting records you rely on, typically the invoice, purchase order, and receipt or acceptance records. If price or quantity discrepancies exceed your tolerance settings, hold the invoice instead of releasing payment.

How is `Payee verification` different from `Invoice verification`?

Payee verification confirms that money is going to the correct account. Invoice verification confirms that the bill is valid, matched, and approved for payment. You need both because account correctness and bill correctness are different risks.

When should a platform auto-approve a bill versus send it to manual review?

Auto-approve only when the invoice is proper, performance is confirmed, required documents match, and results stay within tolerance. Send the bill to manual review when documents are missing, mismatches remain unresolved, or policy requires human judgment. If an over-tolerance condition is configured as a payment block, do not release funds until it is resolved.

What is the minimum control set for pre-payment approval in a marketplace?

Use a minimum control set that covers a proper invoice, satisfactory performance, payee account validation, document matching, and tolerance-based hold or block rules. Where purchase order and receipt data exist, match invoice price and quantity against those records. Configure tolerances so exceptions are held instead of silently passing.

How do you handle exceptions without breaking payout SLAs?

Handle exceptions by severity so the queue stays workable. Keep high-risk failures, such as payee-account issues or over-tolerance discrepancies, on hold or blocked, and route lower-risk issues to review. Use idempotency keys on retry paths so repeated requests do not create duplicate payment releases.

What evidence should be stored to support disputes and audits?

Store the business records behind each payment decision. Core records include invoices, paid bills, receipts, deposit slips, and canceled checks because they support accounting and tax records. Keep the related verification outcome with those records so reviewers can confirm why payment was released, held, or blocked.

When should a platform build invoice validation logic versus buy software?

There is no universal build-versus-buy winner. Decide based on whether you can reliably operate the required controls end to end, including proper-invoice and performance gating, matching with tolerances, payee validation, exception handling, and retry safety. If you cannot run those controls with clear evidence, treat that as a readiness gap before choosing either path.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- acquisition.gov/far/32.905trusted

- acquisition.gov/far/52.233-1trusted

- bis.org/cpmi/publ/brief9.htmtrusted

- csrc.nist.gov/glossary/term/Separation_of_Dutytrusted

- docs.stripe.com/api/idempotent_requeststrusted

- energy.gov/sites/prod/files/32.1_Reviewing_and_Approvin...trusted

- gao.gov/products/gao-25-107753trusted

- guides.gaoinnovations.gov/greenbook/2025/principle-3-establish-structu...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: