Quick Answer

The best international payment gateway in 2026 depends on your operating model, not brand recognition. Stripe fits product-led teams that need custom checkout control, Adyen fits multi-region enterprise standardization, PayPal fits fast launch with public fee references, 2Checkout by Verifone fits lighter implementation, GoCardless fits recurring bank-based collection, and Payoneer fits payout-heavy cross-border operations.

Choose an international gateway for operating fit, not brand gravity#

Choose an international gateway for operating fit, not brand gravity. In cross-border platforms, the wrong match can strain operations before it shows up at checkout. The failure often appears as extra compliance work, higher integration effort, and reconciliation pain after launch.

An international payment gateway processes electronic payments across national borders, but selection is not just about accepting a card abroad. Coverage, currencies, and payment methods vary by provider, and those differences add friction and cost when they do not match your target markets. A recognizable name like Stripe, Adyen, PayPal, 2Checkout by Verifone, GoCardless, or Payoneer is not enough on its own.

That gap gets wider when you are not running a simple retail checkout. A plug-and-play storefront widget is a different need from a cross-border contractor platform, creator marketplace, or embedded-payments product. In those models, product, engineering, finance, and compliance all carry risk, so a gateway that demos well can still be expensive to run.

This guide is for teams evaluating the best international payment gateways 2026 and trying to make a decision they can execute, not just a popularity pick. If you collect from global buyers, pay out to international sellers or contractors, or need embedded controls, you need clear tradeoffs on provider strengths, ownership burden, and what to verify before signing.

One practical red flag is letting headline pricing or checkout polish decide the outcome. Public examples show why. One Stripe comparison lists 2.9% + 30¢ for successful card charges, while ACH direct debit is listed at 0.8% with a $5.00 cap. The point is not that one method is always better. It is that cost and fit change by payment type, so you should test your real payment mix.

Apply the same standard to compliance artifacts. Gateways often handle currency conversion and part of compliance and security handling, but the details are not interchangeable. If your flow includes India-export payments, verify early whether you need e-FIRC/FIRA documentation and purpose codes for each foreign payment. The goal is simple: make a decision you can execute with fewer surprises in integration effort, compliance handling, and reconciliation overhead. For adjacent controls work, see 8 Resilient Compliance Controls for Payment Platforms in 2026.

Who this ranking is for and the decision criteria that matter#

This ranking is for teams evaluating Stripe, Adyen, PayPal, 2Checkout by Verifone, GoCardless, and Payoneer for cross-border operations where both launch risk and post-launch operating risk matter. If your use case is mostly single-country checkout, this level of evaluation may be unnecessary. Hard rule: if pay-ins and payouts both matter, do not decide on checkout UX alone. Use the same six criteria, in order, for every provider.

| Criterion | What to validate | Grounded detail |

|---|---|---|

| Coverage | Real market footprint and account-residency assumptions | Domestic and international are defined by where sender and receiver are registered, and some cross-border cases can still be fee-treated as domestic. |

| Payment methods | Method-level fit by market | Public Stripe pricing shows 2.9% + 30¢ domestic cards, 0.8% ACH Direct Debit with a $5.00 cap, +1.5% for international cards, and +1% when currency conversion is required. |

| Pricing clarity | Total landed cost against your actual mix | Rates can be market-scoped, such as US-resident accounts on US pages, and custom pricing can be country-specific. |

| Integration depth | Post-launch ownership for product and engineering | Score how much ownership product and engineering will carry after launch, not just how fast a demo goes live. |

| Payout support | Outbound money movement as a separate criterion | One business fee structure separates PayPal Payouts from acceptance pricing. |

| Dispute operations | Disputes as a standalone operating function | The same public pricing structure also separates Dispute Fees. |

- Coverage

Start with your real market footprint and account-residency assumptions. One public fee framework shows why: domestic and international are defined by where sender and receiver are registered, certain markets are grouped for international rate calculations, and some cross-border cases can still be fee-treated as domestic.

- Payment methods

Check method-level fit by market, not just whether cards are supported. Public Stripe pricing illustrates the spread: 2.9% + 30¢ domestic cards, 0.8% ACH Direct Debit with a $5.00 cap, +1.5% for international cards, and +1% when currency conversion is required.

- Pricing clarity

Validate total landed cost against your actual mix before sign-off. Rates can be market-scoped, for example US-resident accounts on US pages, and Stripe notes custom pricing can be country-specific.

- Integration depth

Score how much ownership product and engineering will carry after launch, not just how fast a demo goes live.

- Payout support

Treat outbound money movement as a separate criterion. One business fee structure separates PayPal Payouts from acceptance pricing, which supports evaluating payouts separately.

- Dispute operations

Treat disputes as a standalone operating function. The same public pricing structure also separates Dispute Fees, which reinforces that dispute handling should be scored directly.

As a change-control checkpoint, save reviewed fee pages as PDFs and record their last-updated dates, for example PayPal US business fees February 9, 2026 and US consumer fees February 19, 2026. Monitor policy-update notices as well. Also account for residual costs even when a specific fee is waived, since exchange-rate and issuer or bank charges may still apply.

For the payables side of a two-sided payment stack, use Key Best Practices for Improving Accounts Payable on a Two-Sided Payment Platform.

Comparison table you can scan in five minutes#

Use this table as a diligence filter, not a final ranking. In the material reviewed here, only PayPal has verifiable public detail, so every other provider row stays intentionally unscored.

| Provider | Best for | Key strengths | Key tradeoffs | Integration lift | Where coverage or features vary by market |

|---|---|---|---|---|---|

| Stripe | Shortlist only after direct validation of your pay-in, payout, and reconciliation requirements | Keep in scope if it fits your product and engineering goals | Confirm landed cost and operations detail with the provider directly | Verify with each provider directly | Validate account country, corridors, currencies, methods, and payout eligibility directly |

| Adyen | Shortlist only after direct validation against your entity structure and operating model | Include if it is a real procurement contender | Confirm detailed comparison terms with the provider directly | Verify with each provider directly | Validate market scope and feature availability by entity and method |

| PayPal | Teams that want a public, market-scoped fee reference and will review pay-ins, payouts, disputes, and chargebacks separately | US business fees page has dedicated PayPal Payouts, Dispute Fees, and Chargeback Fees sections; PayPal fee pages include a downloadable printable PDF | Scope is market-specific; domestic vs international is based on whether sender and receiver are in the same or different markets; certain markets are grouped for international rate calculations; card-issuer or bank exchange-rate fees may still apply | Fee pages alone are not enough for full operational readiness testing | Cited pages are for US-resident accounts; consumer page shows Last Updated: February 19, 2026; business page shows Last Updated: February 9, 2026 |

| Braintree | Shortlist only after direct validation of checkout, payouts, disputes, and reporting fit | Keep in view if already shortlisted | Confirm strengths and tradeoffs with the provider directly | Verify with each provider directly | Confirm country and method support directly |

| 2Checkout / Verifone | Shortlist only after direct validation of checkout scope and finance-close outputs | Include if commercially relevant to your model | Public detail is not grounded in this pack for fair comparison | Verify with each provider directly | Validate corridor, currency, and account-residency assumptions directly |

| GoCardless | Shortlist only after direct validation of payment-flow fit and reporting outputs | Consider only if aligned with your billing model | Confirm cross-provider ranking criteria with each provider directly | Verify with each provider directly | Validate market support, method eligibility, and payout implications directly |

| Payoneer | Shortlist only after direct validation of your acceptance, payout, and reporting requirements | Include if commercially relevant to your stack | Confirm exact acceptance and payout scope with the provider directly | Verify with each provider directly | Confirm supported markets, currencies, and account setups for your flow |

| Operator checks (all providers) | Any provider that survives first-pass screening | Request documented retry behavior, webhook handling, reconciliation outputs, and support escalation model | Public pages may not answer these items at operator depth | Run a pilot focused on event recovery, duplicate handling, and close-ready exports | Verify whether support and reporting differ by market, entity, or product variant |

| Public-page unknowns (all providers) | Pre-contract diligence guardrails | Prevents false confidence in shortlist scoring | Confirm approval-rate variance, FX spread transparency, and dispute-handling depth with each provider directly | Escalate these items to solution review, contract review, and pilot validation | Record the exact fee page, account market, and document date reviewed |

If pay-ins and payouts both matter, reject any option that does not clearly separate acceptance terms from payout terms. PayPal is the only provider in this pack where that separation is explicit, through PayPal Payouts, Dispute Fees, and Chargeback Fees.

Before you sign off, save the fee-page PDF, capture the last-updated date, and note market scope in your approval record. That checkpoint keeps pricing review traceable and reduces scope confusion later in implementation and finance close.

Stripe for product-led platforms with custom checkout#

Stripe is worth a serious look when engineering control is central to the product. It is not an automatic winner. In the material reviewed here, the supported signal is fit for developer-led builds rather than a definitive cross-provider rank.

Helcim's guide, published March 24, 2026, places Stripe with "SaaS & developer teams" and highlights "Powerful APIs, global tools." The same guide looks beyond transaction fees and includes security, scalability, global reach, and long-term cost efficiency. If checkout is part of your product experience, that is the right lens.

Why this fit can be real#

The practical reason to keep Stripe in scope is control for developer-led teams. That matters more as payment operations get more complex across markets.

Corefy's February 5, 2026 article describes that environment as multi-PSP, region-specific, and regulation-heavy. In that context, developer-oriented depth can matter, but only if your team will actually use it.

Operator checks before sign-off#

Do not decide on API reputation alone. Validate integration depth directly with operator evidence.

| Checkpoint | Why it matters | What to ask for |

|---|---|---|

| Routing rules | Cross-border flows often need market-specific logic | Can your team define rules by region, payment method, risk profile, or provider performance? |

| Failover behavior | Integration depth should include failover, not just basic connector behavior | What happens when a path fails, times out, or returns an unclear state? |

| Data access | Operations need reporting, reconciliation, and fee transparency, not just successful checkout | What event data, reconciliation fields, and status history are available without custom work? |

Ask for evidence, not slides. Request sample event payloads, failure-state examples, retry behavior, and finance-ready exports.

Tradeoff to treat as a verification item#

More customization can improve product fit, but it can also increase ongoing implementation and operational ownership. If you are comparing Stripe with lower-code options such as 2Checkout / Verifone, verify that burden directly instead of assuming it.

The grounded risk is clear. The wrong provider choice can drive avoidable declines, unnecessary fees, and operational issues at scale. A workable rule is to keep Stripe in consideration when product differentiation depends on payment control, then verify the control points in implementation. If your priority is fastest launch with fewer moving parts, verify whether that extra control is actually needed. For a SaaS-specific gateway comparison, read The Best Payment Gateways for SaaS Businesses.

Adyen for enterprise platforms with multi-region complexity#

Adyen can make the most sense when your core problem is consolidating payments operations across regions, entities, and teams, not just improving checkout control. Keep it on your shortlist if you need a more unified operating layer for acceptance and risk handling across markets.

A useful signal comes from Helcim's March 24, 2026 comparison table. Adyen is listed as interchange-plus, best for enterprise & multinational, with strengths in global acquiring and risk management. That framing is useful if your current setup is turning into regional fragmentation.

Why this fit appears at enterprise scale#

Enterprise requirements are different for a reason. G2's enterprise payment gateway category requires at least 10 reviews from enterprise businesses for inclusion and explicitly distinguishes enterprise needs across features, pricing, setup, and installation.

For multi-region platforms, the value is operational consistency. You are standardizing how payments are approved and how risk is handled across markets.

What to verify before committing#

At higher transaction volume, common failure modes include authorization failures, rising cross-border costs, slower settlement cycles, and limits around payouts or recurring billing. Treat authorization performance as a core checkpoint: approval rates, retry logic, and routing. Ask for inspectable evidence:

- Authorization reporting by region and payment method: confirm approval behavior, retry visibility, and routing control.

- Failure-state examples: review failed authorization paths and how those outcomes are surfaced for investigation.

- Reconciliation outputs: validate exports by currency, entity, and settlement view for multi-entity operations.

Tradeoff to keep explicit#

Adyen is not automatically wrong for smaller teams. The risk is buying enterprise-grade capability before your payments, product, and finance ownership model is ready to govern it.

Use a simple rule: choose Adyen when cross-region standardization is the priority. If your near-term goal is faster launch, compare it directly with simpler options before deciding.

For multi-gateway approval-rate strategy, read Gateway Routing for Platforms: How to Use Multiple Payment Gateways to Maximize Approval Rates.

PayPal and Braintree for fast launch with strong buyer recognition#

Choose PayPal when your immediate constraint is launching checkout with PayPal payments and card processing in one setup. Treat Braintree as a separate follow-up evaluation rather than an assumed upgrade path.

The provider explicitly positions checkout so you can offer PayPal payments, process cards, or both in one setup. It also frames Expanded Checkout as a way to tailor risk management and checkout experience, making it the more configurable option.

If you are validating cross-border demand, model fees early. This is not one flat rate, and product choice changes the economics.

| PayPal option on US business pricing page | Starting rate shown |

|---|---|

| Expanded Checkout credit/debit cards | 2.89%* + $0.29 per transaction |

| PayPal Checkout credit/debit cards | 2.99% + $0.49 per transaction |

| PayPal/Venmo checkout | 3.49%* + $0.49 per transaction |

| Pay Later | 4.99%* + $0.49 per transaction |

Before signing, lock your model to the exact product and relevant market page. Published rates are market and region dependent. Domestic vs international classification is based on whether sender and receiver are in the same market, with some region-specific cases treated as domestic for fee purposes. Use a tight review checklist:

- Save the current fee artifacts, including the downloadable PDF, during vendor review.

- Check the Policy Updates Page for upcoming rate and fee changes and timing.

- Confirm chargeback-fee and payout-related terms in the merchant fee documentation.

- Test representative cross-border scenarios so your domestic and international assumptions match how fees are applied.

Keep the tradeoff explicit. Fast launch does not remove fee complexity across products and regions, and exchange rates or fees charged by a card issuer or bank may still apply even when a fee waiver exists.

2Checkout and Verifone for broad reach with lighter implementation lift#

If you want to avoid an enterprise-style build at the start, 2Checkout (now Verifone) belongs on a cautious shortlist. The practical case in API-first comparison material is faster go-live through self-serve onboarding, documented APIs, and test tooling, not proven depth or guaranteed parity with Stripe or Adyen.

This is most relevant for product-led teams that want quick integration and iteration with limited engineering capacity. Those comparisons frame the benefit as less enterprise-first implementation friction, but that is positioning, not a guaranteed implementation outcome in your stack.

Use this decision split:

- Keep it in scope if your near-term need is standard checkout flows and you can defer deeper product-specific control decisions early.

- Pressure-test it directly against Stripe and Adyen if your roadmap already depends on tailored checkout logic, complex event handling, or fine-grained risk controls.

Before treating it as a serious option for your case, run a tight verification pass:

- Confirm product lineage in writing,

2CheckoutunderVerifone, so docs, support paths, and contract terms align. - Validate sandbox fundamentals called out in API-first sources: sandboxes, webhooks, SDKs, and clear error handling, not only happy-path authorization.

- Save an evidence pack: API doc version, webhook samples, and failure logs for declined or interrupted payments.

The main risk to scrutinize is operational confidence. A Quora report alleged weak email support, outdated docs, and missing historical data before July 2018 during an Avangate transition. That is anecdotal, not provider-confirmed, but it justifies deeper support and documentation checks.

Another user-reported range of 6.5% to 8.2% of turnover is also anecdotal. It is still a reason to model your own transaction mix instead of relying on generic pricing assumptions.

For a broader Stripe-alternatives shortlist, read The best alternatives to Stripe for international businesses.

GoCardless for recurring bank-based collection in supported markets#

Keep GoCardless in scope only if your decision is specifically about recurring collection and you are prepared to validate the operating details in writing. If your revenue still depends on mixed checkout behavior or one-off purchases, you may want to keep a card-led gateway in scope rather than forcing one setup to cover both patterns.

What to verify before you get attached#

The grounding here does not establish GoCardless pricing, market coverage, or operational behavior, so treat those as contract-stage checks, not assumptions. Build an evidence pack before sign-off:

- current fee schedule or quote

- supported countries and currencies for your entities

- sample finance exports

- failure and exception handling docs for missed or rejected collections

Use a live card baseline, not a generic assumption#

If your business case depends on lower cost than cards, benchmark it against current published card-path pricing. On the US business pricing page for PayPal, expanded checkout credit/debit cards are 2.89% + $0.29 per transaction. PayPal/Venmo is 3.49% + $0.49, and Pay Later is 4.99% + $0.49.

Before approval, save the provider's printable fee PDF and record freshness dates: PayPal US consumer fees, February 19, 2026, and PayPal US business fees, February 9, 2026. For scope, PayPal notes those US consumer rates apply to US-resident accounts. Also model non-headline costs: exchange rates or fees charged by a customer's card issuer or bank may still apply, and fee treatment can vary by market grouping.

Payoneer for cross-border disbursement-heavy use cases#

Payoneer can be a candidate when your hardest problem is cross-border payouts, not checkout. If you pay contractors, creators, affiliates, or suppliers across markets, evaluate payout depth and checkout depth as separate decisions.

Best fit#

Use it in payout-heavy operations where outbound payments are core and time-sensitive exceptions can occur. In that setup, provider choice affects cost predictability, operational efficiency, treasury visibility, and scaling confidence.

Payout-heavy stacks can fail differently from checkout-heavy stacks. A smooth pay-in flow does not solve payout issues if your team cannot quickly escalate time-sensitive cases.

Why teams keep it in scope#

Payoneer is included in at least one published side-by-side comparison with Sokin, Airwallex, and WorldFirst. That does not make it the automatic choice, but it does keep Payoneer in the evaluation set for international business payments.

Payoneer's own resource, published February 18, 2026, frames method choice as SWIFT vs ACH vs wire. For payout design, that is a practical lens when corridor, method, and timing tradeoffs matter.

What to verify before you choose it#

The main risk is assuming payout capability means full gateway fit. If inbound checkout is also critical, test that separately against checkout-first providers. Before sign-off, verify:

- Pricing transparency: written FX margins, transfer fees, and account charges.

- Currency and country coverage: exact hold, pay, and receive coverage for your entities and target corridors.

- Integration fit: compatibility with accounting systems, marketplaces, and internal finance tools.

- Support and reliability: escalation readiness for urgent payments, especially where latency or downtime creates business risk.

Concrete operator recommendation#

Run a live pilot with exception scenarios, not just happy-path transfers. Include at least one support escalation and confirm finance can reconcile outcomes.

Build an evidence pack with current fee schedules, corridor coverage by entity, payout status reporting samples, support escalation contacts, and accounting export samples. If these stay unclear, keep Payoneer in the payout lane and pair it with a separate checkout-first provider.

For contractor payout operations in Latin America, read The Best Way to Pay a Team of Contractors in Latin America.

When a gateway alone is not enough for platform payments#

A gateway is often necessary, but it is not always sufficient for platform payments. An international payment gateway helps you accept money from customers in other countries. Many platforms also need payout execution, settlement controls, and day-to-day operational visibility beyond checkout.

| Model | What to verify | Key differentiator |

|---|---|---|

| Inbound checkout only | Verify the exact integrations your stack needs and get full fee components in writing. | Acceptance depth drives the decision. |

| Two-sided platforms and mass payouts | Ask vendors to show payout timing clarity, settlement options, and reconciliation outputs before approval. | You are selecting for full money movement operations, not just checkout performance. |

| Compliance-gated onboarding | Confirm market licensing fit and settlement behavior for the countries you operate in. | Compliance checks become a core operating requirement, not a secondary feature. |

| Operational reality after go-live | Build a pre-approval evidence pack with sample reconciliation exports, settlement reports, written fee schedules, and proof of required APIs or plugins. | Choose the stack your product, finance, and compliance teams can run without detective work. |

- Inbound checkout only

If your scope is mostly customer acceptance, Stripe or PayPal can stay on your shortlist. Make that choice on international fit, not brand familiarity. Payment-method coverage, currency handling, and checkout localization all affect conversion, and card-only or forced conversion can reduce sales.

Before signing, verify the exact integrations your stack needs, for example Shopify, Magento, or WooCommerce, and get full fee components in writing. In cross-border flows, total cost can include more than a headline transaction rate. Key differentiator: acceptance depth drives the decision.

- Two-sided platforms and mass payouts

If you also need to pay creators, contractors, sellers, or affiliates, evaluate payouts as a separate workstream, not as an automatic extension of checkout. Slow or unclear payouts can create cash-flow pressure and more admin work, even when pay-in conversion is strong.

Ask vendors to show payout timing clarity, settlement options, and reconciliation outputs before approval. Key differentiator: you are selecting for full money movement operations, not just checkout performance.

- Compliance-gated onboarding

When compliance gates are strict, treat onboarding and payment controls as a separate evaluation area. Do not assume those controls are robust just because a provider supports cross-border payments.

Also confirm market licensing fit and settlement behavior for the countries you operate in. Key differentiator: compliance checks become a core operating requirement, not a secondary feature.

- Operational reality after go-live

Forcing one provider to cover every payment job can hide failure modes until scale exposes them. The issues usually show up in payout clarity, settlement tracking, and reconciliation effort.

Build a pre-approval evidence pack: sample reconciliation exports, settlement reports, written fee schedules, and proof of required APIs or plugins. If a provider is strong on acceptance but weak on these operating controls, keep it in the gateway lane and add separate payout or treasury support as needed. Key differentiator: choose the stack your product, finance, and compliance teams can run without detective work.

For payout operations in one common offshore-services corridor, read The Best Way to Pay Filipino Virtual Assistants from the US.

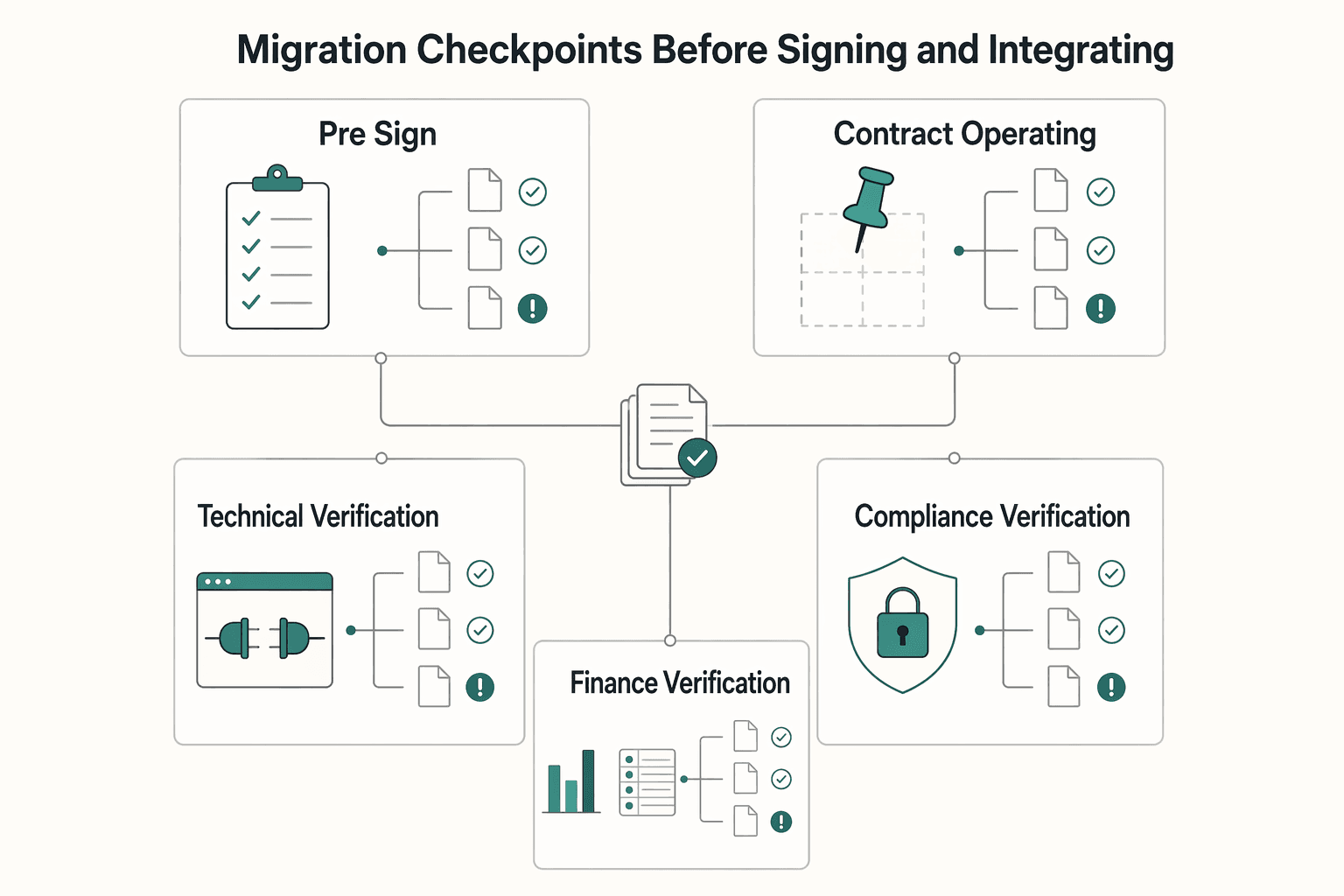

Migration checkpoints before signing and integrating#

Do not sign on checkout demos alone. Use a pre-sign checkpoint process across product, engineering, finance, and compliance so sales momentum does not outrun operational proof.

| Checkpoint | What to confirm | Decision lens |

|---|---|---|

| Pre-sign checklist with named owners | Product approves checkout behavior and edge cases; engineering approves integration readiness; finance approves reporting and close impact; compliance approves control visibility and liability boundaries. | Choose based on business model, target regions, product complexity, and team bandwidth, not brand familiarity. |

| Contract and operating terms you can run | Clarify expected settlement timing, reserve behavior, dispute handling, and support escalation paths. | Validate operating terms, not just commercial terms. |

| Technical verification under failure, not only success | Verify idempotency, webhook retries, failure-state visibility, and missing-event recovery using real artifacts: APIs, SDKs, webhooks, and docs. | Pick the provider your team can operate during failure conditions, not just happy-path demos. |

| Finance verification for multi-currency operations | Validate exports, settlement and dispute reporting, and reconciliation traceability from authorization through settlement. | Reduce downstream reconciliation overhead for finance and support teams. |

| Compliance verification where coverage varies | Require documented compliance policy gates, onboarding decision visibility, record-keeping approach, and regional support limits. | Auditable compliance visibility over generic "we're compliant" language. |

| Go/no-go rule with one pilot market | No production migration until one pilot market passes checkout outcomes, payout outcomes if in scope, and finance reconciliation sign-off. | Approve only after customer flow, money movement, and close operations work together in a real pilot. |

- Pre-sign checklist with named owners

Start with a written approval checklist and explicit acceptance criteria by function. Product approves checkout behavior and edge cases, engineering approves integration readiness, finance approves reporting and close impact, and compliance approves control visibility and liability boundaries. Key differentiator: choose based on business model, target regions, product complexity, and team bandwidth, not brand familiarity, including Stripe, Adyen, or PayPal.

- Contract and operating terms you can run

Before you sign, clarify expected settlement timing, reserve behavior, dispute handling, and support escalation paths. Treat pricing examples like 4% + 40c US, +1.5% intl, +0.5% subs or 5% + 50c pay-as-you-go as prompts to demand full fee disclosure, not as assumptions. Key differentiator: validate operating terms, not just commercial terms.

- Technical verification under failure, not only success

A successful test payment is not enough. Verify how idempotency, webhook retries, failure-state visibility, and missing-event recovery are documented for your integration, using real artifacts: APIs, SDKs, webhooks, and docs. Key differentiator: pick the provider your team can operate during failure conditions, not just happy-path demos.

- Finance verification for multi-currency operations

Finance should validate exports, settlement and dispute reporting, and reconciliation traceability from authorization through settlement. If a provider advertises broad coverage, including examples like 17 currencies, confirm exact currency, entity, and report-field fit for your close process. Key differentiator: reduce downstream reconciliation overhead for finance and support teams.

- Compliance verification where coverage varies

Require documented compliance policy gates, onboarding decision visibility, record-keeping approach, and regional support limits. A weak global payment acceptance setup can increase declines and erode trust, so confirm whether target markets can use domestic-looking processing where available instead of assuming a single model fits all. Key differentiator: auditable compliance visibility over generic "we're compliant" language.

- Go/no-go rule with one pilot market

Set a hard cutover gate: no production migration until one pilot market passes checkout outcomes, payout outcomes if in scope, and finance reconciliation sign-off. Key differentiator: approve only after customer flow, money movement, and close operations work together in a real pilot.

If you are turning this checklist into implementation tickets, map your retries, webhooks, and reconciliation flow against the Gruv docs.

Final recommendation for choosing in 2026#

Choose by operating model first, then by provider brand. If two finalists look equally strong, pick the one your team can run reliably through compliance checks, incident response, and month-end reconciliation without hidden manual work.

A generic top-10 list is not enough. Use one side-by-side comparison table for your real use case, then one migration checklist so product, engineering, finance, and compliance sign off on the same risks.

Decision table#

| Operating model | Usually shortlist first | What matters most | Red flag to test before signing |

|---|---|---|---|

| Checkout-only | Checkout-first gateway options | Local payment method display, cross-currency handling, and checkout flows that do not force unnecessary conversion | If the flow effectively forces cards or conversion, conversion can drop. Also test FX impact, since public guides note many gateways add 1 to 2% on conversion. |

| Mixed platform flows | Options that can support both pay-ins and downstream operations | How pay-ins, payment states, settlement output, and finance reporting work together | A polished demo is not enough if your team cannot operate exceptions and month-end close cleanly. |

| Payout-heavy or disbursement-led | Payout-first options, sometimes with a separate acceptance stack | Payout visibility, exception handling, and whether a checkout gateway is central to your model at all | Slow or unclear payouts create cash-flow pressure, and some businesses do not need checkout pages as the center of the stack. |

Use that table as the decision lens. If you mainly sell online, start with checkout-first criteria. If you both collect and distribute funds, prioritize mixed or payout-heavy criteria early, because operations can become the constraint.

Your highest-value checkpoint is not a homepage feature list. It is whether the provider can show a credible operating path for your real corridors, currencies, and payment methods. Treat examples like 2.9% + fixed fee or 1-3 business days as prompts for deeper questions, not final contract terms.

Migration checklist#

- Build one live comparison sheet for your top two options: countries, currencies, payment methods, who gets paid, settlement timing, and where FX applies.

- Ask for evidence, not just a demo: sample exports or reports finance can reconcile, plus concrete exception flows.

- Price the full path: transaction pricing, FX, and payout or settlement friction that affects cash planning.

- Run one pilot corridor end to end, including checkout behavior and payout behavior where relevant.

- Set a hard tiebreaker: if options are commercially close, choose the one your current team can support reliably during incidents and month-end close.

Make the final decision from the work your team must do after go-live, not from brand familiarity.

If your final choice includes both pay-ins and global payouts, validate market coverage and compliance gates with Gruv before production rollout.

Frequently Asked Questions

What is the difference between an international payment gateway and broader cross-border payments infrastructure?

A gateway is the intermediary between your business, payment methods, and financial institutions for cross-border acceptance. Broader infrastructure also covers FX handling, settlement flows, payout operations, and compliance documentation. If you need more than checkout acceptance, you are usually evaluating infrastructure, not only a gateway.

Which gateway is best for marketplaces versus SaaS checkout in 2026?

There is no single best gateway for every marketplace and SaaS case. The right choice depends on your target countries, currencies, payment methods, and whether you need simple checkout or a broader operating flow. A retail-style card widget and a B2B cross-border gateway can require different decisions.

What fees matter most beyond the headline transaction rate?

Look at total economics, not just the top-line card fee. FX markups and payout behavior can materially affect margin and cash flow, and flat-rate pricing can become expensive at higher volume compared with interchange-plus structures. Treat example rates as starting points and request full corridor-level pricing.

How should we validate country and currency coverage before committing?

Treat coverage as a testable matrix, not a marketing claim. Confirm exact country, currency, and payment-method support for your real corridors, then verify whether localized checkout is available. Also confirm the actual integration path before signing, including native plugins or APIs for your platform or custom stack.

When should we combine a gateway with a separate payout stack?

Combine them when checkout acceptance and payout operations have different requirements. A gateway can be strong for pay-ins while still leaving gaps in payout handling, settlement flows, or compliance outputs. If your flow includes India-export payments, confirm whether required artifacts like e-FIRC and purpose codes are generated automatically.

What should we test in a pilot before full migration?

Run one pilot corridor end to end and judge operational outcomes, not demo performance. Test localized checkout behavior, currency handling, fee outcomes, and settlement or reporting output against your finance process. If the pilot still creates forced conversion, cart drop-off, higher fees, or higher admin overhead, treat that as a no-go signal.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- federalregister.gov/documents/2026/03/27/2026-05959/regulatory-c...trusted

- federalreserve.gov/aboutthefed/boardmeetings/enhanced-transpare...trusted

- medpac.gov/wp-content/uploads/2025/08/January-2026-publ...trusted

- paypal.com/us/business/paypal-business-feestrusted

- paypal.com/us/digital-wallet/paypal-consumer-feestrusted

- stripe.com/pricingtrusted

- wise.com/gb/blog/best-startup-payment-gatewaystrusted

- wise.com/us/blog/best-payment-gatewaytrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: