Quick Answer

Choose the method that keeps net pay predictable and documentation usable every month, not just the one that looks cheapest. For US-to-Philippines VA payments, evaluate options against landed cost after FX and fees, timing reliability, exception recovery, and reconciliation evidence quality. Finalize terms in writing before the first send: payout date, who absorbs fees, and what event counts as completed payment. Then store one cycle file with invoice, reference ID, timestamp, and payment confirmation.

Who this guide is for and how to choose a payment method#

There is no single best way to pay Filipino virtual assistants. The right choice keeps payments on time, secure, and easy to verify, not just cheap on paper.

- Who this is for

This guide is for freelancers, creators, and small teams paying a Filipino VA, often in an independent-contractor setup. If your pain points are payout delays, transfer fees, unclear clearing time, or weak records, this guide is written for you.

- Who this is not for

This is not a salary-benchmark guide. It is a payment-operations guide focused on reliability, written terms, and documentation you can use when something goes wrong.

- How to choose a method

Start with your preferences, your VA's comfort level, and the amount being transferred. Then compare options using four practical checks:

- Total landed cost after transfer fees and exchange-rate effects

- Clearing-time predictability for your payout schedule

- Recovery path if transfers hit verification delays, banking cutoffs, or platform holds

- Proof-of-payment quality for reconciliation

For contractor-style workflows, keep a simple but complete record set: invoice, contract, and proof of payment.

- Decision lens

Optimize for fewer surprises, especially when cash flow is tight. A method with slightly higher fees can still be the better choice if it is more predictable and easier to document.

Set the payment schedule before hiring and put currency and fee handling in writing. Do not choose a payment method until you can answer three questions in writing: when you will pay, what amount the VA should receive, and what evidence will show that payment was completed. For related classification issues, see What to Do If You've Been Misclassified as an Independent Contractor.

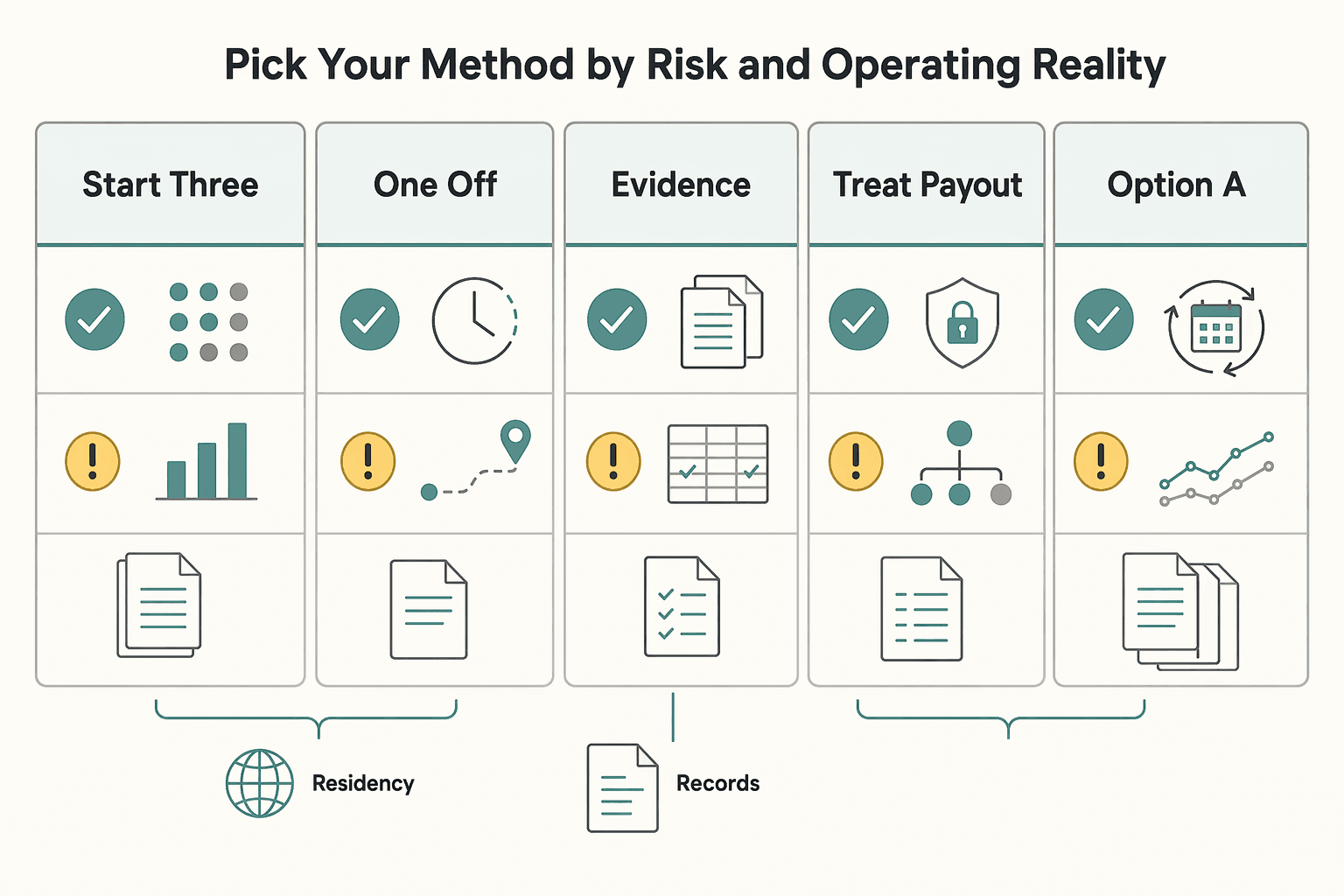

Pick your method by risk and operating reality#

Choose the rail by operational risk first, then by headline fees. If your team cannot reliably handle exceptions, the cheapest-looking option can become the most expensive to run.

- Start with your three real constraints

Decide based on monthly payout volume, urgency, and your tolerance for manual reconciliation before you compare providers. Volume can change economics. Wise says discounts start at 25,000 USD, can apply across one or multiple transfers, and reset on the first of the month. For urgency, focus on traceability and what records you will have if a payment needs follow-up.

- For one-off or irregular payments, compare admin burden first

For Wise, PayPal, and bank transfer, check setup and verification workload before percentage fees. Wise says pricing varies by currency, starts from 0.57%, uses the mid-market rate, and provides a regulator-standardized pricing view you can save before sending. PayPal defines an international transaction as sender and receiver being in different markets. Its US fees page, last updated February 19, 2026, notes that exchange-rate or bank/card-issuer fees may still apply, which can change the net received amount.

- For recurring, payroll-like payouts, optimize for status capture and records

Once payouts become monthly, consistency matters more than improvisation. Decide on the method only after you define the payout record you will keep each cycle: invoice, transfer reference, timestamp, sent amount, and recipient identifier. Save the fee artifact with each payout record, such as the standardized pricing view or a printable fee PDF, so you are not rebuilding terms during a dispute.

- Treat payout ownership as an operations commitment

Use a payout setup only if your team can own onboarding data collection, payout QA, and exception handling every cycle. If that ownership is not realistic yet, choose the option your team can run consistently at your current process maturity. Payment issues can come from missing invoice data, incorrect recipient details, or incomplete payout records.

Set fair compensation with context instead of a single number#

Set compensation from written scope and multiple reference points, not one number. If you want to pay a Filipino VA fairly and keep the relationship stable, triangulate your offer and lock the terms before the first transfer.

- Use multiple reference types, not one source

Compare more than one source type so a single outlier does not set your offer. Do not force them into one "correct" rate. Use them to check role framing, pay structure, bundled duties, and availability expectations.

Save the exact references you used, along with dated scope notes. That record helps if pay expectations are challenged later.

- Treat payment method as part of compensation design

How you pay can affect compliance exposure, total cost, and business reputation. Pressure-test your payment options before finalizing the offer so the net outcome is clear on both sides.

Keep scope constant when comparing options. If fees, timing, or responsibilities change, write that change into the role terms.

- Normalize terms in writing before you debate fairness

Write down expected hours, pay period, what fees are included, and what is out of scope. Clear wording prevents avoidable disputes.

Keep compliance language disciplined. The Wage and Hour Division item dated 02/27/2026 is a Proposed Rule, not final guidance. The FederalRegister.gov page says it is not the official legal edition. If you review it, verify against the linked official PDF on govinfo.gov rather than relying on XML alone.

Final check before sending: if "before or after fees?" is still unclear, the offer is not ready.

Best ways to pay Filipino VAs from the US#

For US-to-Philippines VA payouts, choose the method you can verify and run consistently. Wise is often a clear starting point for recurring payments, PayPal is practical for convenience, and bank transfer or an agency model may fit when your internal process is the real constraint.

| Method | Use when | Key control | Grounded note |

|---|---|---|---|

| Wise | You want repeatable payouts with pricing you can document before sending | Save the pricing output or regulator-standardized pricing view on the day payment is approved | Uses the live mid-market rate with a small upfront fee; fees vary by currency and start from 0.57%; discounts begin at 25,000 USD and reset on the first of each month |

| PayPal | Familiarity and convenience matter more than optimization, especially for a first payment if both sides already use it | Write down the gross amount, who absorbs fees, and what counts as completed payment | Defines an international transaction by sender and receiver being in different markets; the US consumer fees page says Last Updated: February 19, 2026 and includes a printable PDF |

| Bank transfer | Your team already runs payouts through bank processes and can enforce strict detail checks | Keep recipient account details in a formal written record, reconfirm them before the first transfer, and archive payment confirmation with the invoice | Do not assume cost or speed without checking your own bank terms for the exact route |

| Agency payout model | Your priority is reducing direct admin work on hiring and payouts | Require invoice detail, payment confirmation, remittance date, and an escalation contact after each payout | It may simplify monthly operations if the agency handles those steps end to end; choose this model when internal time is the main constraint |

1. Wise#

Use Wise when you want repeatable payouts with pricing you can document before sending. It says it uses the live mid-market rate with a small upfront fee. It also says send-money pricing is usage-based, with no subscription plans.

Check the exact route each time. It says fees vary by currency and lists sending and conversion fees starting from 0.57%. Save the pricing output, or the regulator-standardized pricing view, on the day you approve payment. That gives you a record if net-amount questions come up later.

If your monthly transfers may cross 25,000 USD or equivalent, recheck timing before month-end. It says volume discounts begin at that level and the window resets on the first of each month.

Also separate transfer completion from cash-access assumptions. For card ATM withdrawals, Wise states that after 2 free withdrawals there is a 1.5 USD per withdrawal fee. Above 100 USD per month, there is also 2% of the amount over 100 USD.

2. PayPal#

Use PayPal when familiarity and convenience matter more than optimization, especially for a first payment if both sides already use it. It defines an international transaction as one where sender and receiver are in different markets, which applies to a US payer and a VA in the Philippines.

Treat fee expectations as version-controlled, not memory-based. The US consumer fees page shows Last Updated: February 19, 2026, includes a downloadable printable PDF, and links to a Policy Updates Page.

Before sending, write down the gross amount, who absorbs fees, and what counts as completed payment. That keeps net-pay expectations clear.

3. Bank transfer#

Use bank transfer when your team already runs payouts through bank processes and can enforce strict detail checks. Keep recipient account details in a formal written record, reconfirm them before the first transfer, and archive payment confirmation with the invoice.

Do not assume cost or speed without checking your own bank terms for the exact route. This can work well when your payout schedule and documentation process are already stable.

4. Agency hire payout model#

Use an agency payout model when your priority is reducing direct admin work on hiring and payouts. It may simplify monthly operations if the agency handles those steps end to end.

The key control is contract clarity. Require the records you will receive after each payout: invoice detail, payment confirmation, remittance date, and an escalation contact. If those artifacts are vague, visibility can drop when a payment is questioned.

Choose this model when internal time is the main constraint. Choose direct payment methods when direct control is the main constraint. Related reading: The Philippines as a Freelance Hub: A Market Analysis.

Decide between direct hire and agency hire with clear rules#

Lean toward direct hire when your team needs direct control and record-level visibility, and toward agency hire when speed and delegated admin matter most. Use these five checkpoints as a practical decision screen for your team.

| Checkpoint | Direct hire | Agency hire |

|---|---|---|

| All-in cost | One direct-hire cost guide lists $500 to $800/month for a general or executive VA, plus 13th month pay at +8.3% annualized (~$42 to $66/month set aside) and $150 to $300 one-time for equipment | One agency-oriented guide reports $6.50 to $15/hour and about $1,040 to $2,400/month full-time, and says its figures are based on its own placement data, so treat them as directional |

| Contractual control | Set payment terms directly: invoice cadence, fee handling, and completion criteria | Confirm who controls rate changes, scope changes, and dispute handling before signing |

| Payout traceability | Define one clean proof chain each month: payment terms, invoice, transfer reference, and reconciliation record tied to the same amount and date | Verify what payout evidence you receive each cycle and how short-pay disputes are handled |

| Replacement risk | Can be a better fit when the role is long-term and business-critical | Can be a better fit when fast continuity is the priority; a practitioner account describes company models as providing preselection, hiring, onboarding, and generic qualification |

| Compliance workload | Map the recurring workload before deciding: onboarding, payment QA, recordkeeping, and exception handling | Can reduce day-to-day burden in some setups, but do not assume all obligations disappear |

1. All-in cost#

Choose direct hire if you want line-item cost control and can budget beyond base pay. One direct-hire cost guide lists $500 to $800/month for a general or executive VA, plus 13th month pay at +8.3% annualized (~$42 to $66/month set aside) and $150 to $300 one-time for equipment. Choose agency hire if you prefer bundled pricing and pre-vetted hiring support, even at a higher range in many cases. One agency-oriented guide reports $6.50 to $15/hour and about $1,040 to $2,400/month full-time, and says its figures are based on its own placement data, so treat them as directional. Keep ROI in view, not just the lowest headline price.

2. Contractual control#

Lean direct hire when you want to set payment terms directly: invoice cadence, fee handling, and completion criteria. Lean agency hire when speed matters more than custom terms, but confirm who controls rate changes, scope changes, and dispute handling before signing.

3. Payout traceability#

For either model, define one clean proof chain each month: payment terms, invoice, transfer reference, and reconciliation record tied to the same amount and date. If you use an agency, verify what payout evidence you receive each cycle and how short-pay disputes are handled.

4. Replacement risk#

Agency hire can be a better fit when fast continuity is the priority. A practitioner account describes company models as providing preselection, hiring, onboarding, and generic qualification. Direct hire can be a better fit when the role is long-term and business-critical, since the same practitioner view flags potential weaknesses in company models for critical long-term assignments.

5. Compliance workload#

Map the recurring workload before deciding: onboarding, payment QA, recordkeeping, and exception handling. Agency hire can reduce day-to-day burden in some setups, but do not assume all obligations disappear. This pairs well with our guide on The Best Way for an Australian Agency to Pay a US-Based Contractor.

Lock payment terms before the first transfer#

Lock the payout rules in writing before the first payment. That is the easiest way to reduce fee surprises, duplicate sends, and dispute confusion later.

| Term | What to define | Article note |

|---|---|---|

| Market scope | State this as a cross-border setup, then list payout currency, invoice currency, and scheduled payment date in plain terms | PayPal defines domestic vs international by sender and receiver market residency; save the fee-page checkpoint you relied on and the page update date used when you agreed terms |

| Fees and completion | Say whether pay is gross or net, who absorbs platform fees, currency conversion effects, and issuer or bank fees, and whether payment is completed when sent, credited, or funds are available | Do not treat checkout pricing lines such as 2.99% and $0.49 as contractor payout terms unless your payout flow is actually in that checkout context |

| Failure handling | Set the response path for delayed credit, returned transfers, and disputed PayPal payments, and require written confirmation of corrected recipient details before any resend | Assign dispute ownership and required records up front; PayPal documentation includes dedicated Dispute Fees and Chargeback Fees categories |

| Proof and identity | Use one proof package each cycle: transaction reference, timestamp, and an agreed proof of payment format, stored with invoice records | Confirm payer and payee identity details before the first payout, including exact business entity naming, and keep those names consistent across the agreement, invoice records, and payment profile |

- Name market scope, currencies, and pay date.

State this as a cross-border setup, then list payout currency, invoice currency, and scheduled payment date in plain terms. PayPal defines domestic vs international by sender and receiver market residency, and its US fee pages are scoped to the US market. Save the fee-page checkpoint you relied on, such as the printable PDF, and record the page update date used when you agreed terms.

- Define fee responsibility and the completion point.

Say whether pay is gross or net, and who absorbs platform fees, currency conversion effects, and issuer or bank fees. Keep "completed payment" explicit: transfer sent, transfer credited, or funds available. Do not treat checkout pricing lines such as 2.99% and $0.49 as contractor payout terms unless your payout flow is actually in that checkout context.

- Add failure clauses before the first failure.

Set the response path for delayed credit, returned transfers, and disputed PayPal payments. Require written confirmation of corrected recipient details before any resend. Assign dispute ownership and required records up front. PayPal documentation includes dedicated Dispute Fees and Chargeback Fees categories.

- Standardize proof and identity details.

Use one proof package each cycle: transaction reference, timestamp, and an agreed proof of payment format, stored with invoice records. Confirm payer and payee identity details before the first payout, including exact business entity naming. Keep those names consistent across the agreement, invoice records, and payment profile.

For a step-by-step walkthrough, see The Best Way to Pay an Indian Development Agency from the US.

Run a monthly payout sequence that is hard to break#

Use the same monthly sequence every time: approve, verify, lock assumptions, send, and archive. In a direct-hire setup, those controls sit with you. A job board model is not managed staffing. One published OnlineJobs.ph review describes no escrow or payment protection and employer-owned payroll operations, even with subscription pricing instead of a percentage cut from worker pay.

- Approve the invoice first

Start from one approved invoice for the cycle, aligned to your written terms: pay date, currency, fee responsibility, and completion point. If anything changed this month, document the exception before release.

- Verify recipient details before release

Run one clean checkpoint: payee name match, destination details check, and duplicate-payment check against the current cycle. If payout details change, pause and re-confirm in writing before sending.

- Lock the amount and foreign exchange assumption

Record the amount rule before execution: either a fixed send amount or a fixed local-currency target with conversion effects accepted. Put that assumption on the payout record so the agreed number is not ambiguous later.

- Execute from the approved record

Send from the approved invoice and verified recipient details, then capture payment confirmation details and status in the same record set.

- Archive proof for fast close

Keep one audit folder per VA in the Philippines with monthly payout records and exception notes. If a transfer fails and is resent, keep both attempts with a short reason note. If you use Gruv where enabled, tie payout events to audit-ready records and reconciliation exports for each payout cycle.

If a payout cannot be explained quickly from one approved record and one folder, tighten the process before next month. Any material change should trigger a fresh verification checkpoint before money moves.

For a full breakdown, read The Best Way to Pay an Offshore Development Team in Ukraine. Before you lock your default rail, run your actual amounts through this payment fee comparison to spot net-pay drift and choose the option you can reconcile every month.

Handle failures fast before they become cashflow problems#

When payout status is unclear, treat it as an exception immediately: open one record, escalate with the provider reference first, and do not resend until the first path is explained.

Triage the failure before you create a second one#

- Wrong recipient details

Pause if destination details changed, and re-confirm the change in writing before any resend. Until the first transfer is clearly failed, returned, or unrecoverable, a second send can create duplicate-payment risk.

- Delayed provider credit

If payment is still unclear after your internal timing threshold, escalate with the transaction reference and timestamp first, then attach supporting records.

- Returned transfer

Keep the original attempt, provider status, return notice, if available, and resend decision in one case record. If you resend, use a fresh approved record so reconciliation still explains both movements.

- Fee surprises that reduce net pay

Verify what happened before assuming "international fees." For PayPal, first confirm whether the transaction was treated as domestic or international, since classification is based on sender and receiver markets.

What to send when status is unclear#

Send a lean escalation pack: provider reference, send timestamp, invoice, proof of payment, and a short issue summary. If the recipient reports non-receipt, confirm the destination details they expected, but keep the original record intact until support responds.

Keep three statuses separate in your records: approved, sent, and credited. That distinction prevents "sent" from being treated as "resolved" when funds are not yet accessible to the recipient.

Build a proper PayPal case file#

For PayPal disputes or chargebacks, assemble one internal file early with the transaction context and core records, for example the invoice, proof of payment, payment timestamps, and transfer reference. The US business fee pages include dedicated Chargeback Fees and Dispute Fees sections, and Seller Protection is framed for eligible transactions only.

If a fee looks wrong, verify it against the page for your account market and save the page artifact. PayPal fee pages provide a downloadable printable PDF, and they point to the Policy Updates Page for fee changes and effective dates. Use the version that matches your account market, since fee pages can differ by region and update timing.

We covered this in detail in The Best Way for a German Agency to Pay a US-Based Freelancer.

Keep compliance and classification tight without overcomplicating it#

Keep this operational: run recurring payouts with one consistent documentation trail, not as ad hoc transactions. The goal is a current contractor file, consistent identity details, and current policy artifacts when you validate process language. A legal contractor-vs-employee test, a required record-retention period, or provider-specific payout timing rules are not established here.

- Keep one current contractor file

If you use the label independent contractor, use it the same way across the agreement, invoice, approval note, and payout record. Before release, confirm that payee identity details match across those records so the file is internally consistent. For signatures, keep electronic records as your default where feasible. VA Handbook 7002, transmittal sheet dated January 8, 2020, states electronic signatures are required except when not possible.

- Use your LLC identity consistently if you have one

If you operate through an LLC, keep the agreement, invoice approval, payout source, and bookkeeping under that same identity in your own records. Avoid mixing business and personal identities in the same payment trail.

- Use current primary-source policy artifacts when you validate process language

Avoid relying on copied snippets or old screenshots for policy references. On the USCIS side, the Policy Manual page marked current as of February 3, 2026 states updated Policy Manual content prevails over conflicting older AFM material, and officers are to follow the Policy Manual while retaining adjudicatory discretion. If you need to trace AFM carryover, use the official crosswalk PDF (304.67 KB) and save the official page artifact, since electronic format conversion can introduce errors or omissions. Treat these references as document-control guidance, not as direct legal instructions for US-to-Philippines VA payout classification.

If you want a deeper dive, read Separating Business and Personal Finances: An Important Step for LLCs.

Know when to move from one-off transfers to structured payout operations#

Move from one-off transfers to a structured monthly payout flow when tracking friction makes status and month-end reconciliation hard to manage, not at a fixed headcount.

- Treat timing drift as the trigger

If you cannot reliably tie each invoice approval to one transaction reference and one archived payment record, one-off handling is already getting fragile. Set one release cadence and one exception list so delays are visible before payout day.

- Formalize once multi-recipient coordination gets noisy

If you are paying multiple VAs across locations, use a single monthly checklist per recipient line: approved amount, destination details, and payout evidence. The goal is consistent status visibility, not a bigger tool.

- Standardize when you run mixed rails

Alternating between Wise and other payout rails can increase reconciliation work because fee and status records are split. Wise states pricing is usage-based, with no subscription, fees vary by currency from 0.57%, and you can see sender cost and recipient amount before sending. That only helps if you capture those details in one repeatable process.

- Use calendar-month batching when volume is close to discount thresholds

Wise states transfer-fee discounts apply when monthly volume goes over 25,000 USD or equivalent, including across multiple transfers, and the discount window resets on the first. If you are near that level, keep payouts inside one calendar month so you do not lose eligibility due to spillover timing.

You do not need a heavyweight setup for this shift. You need one payout window, one status view, and one consistent evidence trail for exceptions.

Related reading: The Best Way to Pay Freelance Collaborators in Europe from the US.

Build a payment system that stays predictable as you grow#

As payout volume grows, the right setup is the one that keeps net pay predictable, exceptions recoverable, and records clean. It's not about finding one perfect rail. It's about matching the method to the level of control your team can actually maintain.

1. Wise#

Choose Wise if your priority is strong pre-send control at scale. Wise says pricing is usage-based with no subscription plan, it uses the live mid-market rate with a separate upfront fee, and send-money fees can start from 0.57% depending on currency. That gives you a clear cost checkpoint before release. It also separates pricing by feature, including routes with a fixed fee per payment, such as 6.11 USD for receiving USD wire/Swift, which can make reconciliation easier.

For recurring payouts, add a monthly volume rule. Wise says discounts start after 25,000 USD or equivalent, can be reached through one or multiple transfers, and savings apply only for the rest of that month because eligibility resets on the first. If you are near the threshold, track cumulative monthly volume before approving sends.

2. PayPal#

Choose PayPal if it is the channel both sides can run consistently right now. The control point is not the rail itself, but the written rule around it. Keep amount, cadence, currency, and fee treatment explicit so the net outcome does not drift across months.

Before release, confirm the agreement amount, invoice, and sent amount all follow the same rule. If they do not, the problem is process, not the platform.

3. Bank transfer#

Choose bank transfer when your team already runs dependable bank-based controls and can enforce detail checks every cycle. Predictability comes from repeatable verification and complete payout evidence, not from the rail alone.

Keep one file per payout with the approved invoice, transfer confirmation, timestamp, and review ownership. If those records are scattered, bank transfer becomes harder to support than it looks.

4. Direct hire#

Choose direct hire when your team can reliably own terms, payout operations, and monthly reconciliation. This route can work well when responsibility is clear, data collection is stable, and someone is accountable for exceptions every month. If ownership is unclear, fix that before volume grows. Direct hire rewards discipline and exposes weak process quickly.

5. Agency hire#

Choose agency hire when your team cannot yet run onboarding, payout QA, and exception follow-up consistently in-house. You trade some direct control for operational coverage, so define what records you will receive and what counts as proof of payment. If direct operations are not stable yet, an agency can be a practical short-term choice. Just make sure visibility does not disappear once the payment leaves your account.

Start simple, then formalize early. Written terms, payout checks, and reconciliation should be in place before payout complexity outruns your team. If you are moving from one-off sends to repeatable monthly operations, review Gruv Payouts to see how compliance-gated batches and status tracking can reduce payout surprises.

Frequently Asked Questions

How much should I pay a Filipino virtual assistant in 2026 if I am hiring from the United States?

This guide does not provide a single defensible 2026 pay benchmark. Set the amount in your own agreement, then make sure the written terms also state payment cadence and fee treatment so expected pay does not drift after transfer costs.

What is usually cheaper for paying a Filipino VA from the US, Wise, PayPal, or bank transfer?

There is no universal cheapest rail across all cases. Wise states fees vary by currency and start from 0.57%, and it says it uses the live mid-market rate plus a separate upfront fee. PayPal classifies cross-border payouts as an international transaction when sender and receiver are in different markets, so check its current fees document each time instead of relying on old assumptions.

When does agency hire make more sense than direct hire for paying VAs in the Philippines?

There is no universal rule here. Agency or direct hire can each be workable depending on your internal constraints, so treat this as an operational choice rather than a fixed payment-rule answer.

What should I put in a payment agreement so payout disputes are easier to resolve?

There is no single required clause list in this guide. Keep terms specific and consistent with what you actually send (amount, cadence, currency, and fee treatment) so payment status is easier to reconcile.

Who should absorb transfer fees so net pay is predictable each month?

There is no universal rule, but there should be one written rule in your agreement. Define whether the agreed amount is gross sent or net received, then verify the transfer preview before release. If you use Wise and are near 25,000 USD in monthly volume, remember it says discount eligibility resets on the first of each month.

What evidence should I keep as proof of payment for compliance and bookkeeping?

Requirements vary, so this is not a definitive compliance checklist. Keep complete payout records plus the provider artifacts you rely on. Wise also provides pricing in a regulator's standardized format, and PayPal provides a downloadable fees PDF with a last-updated date of February 19, 2026.

How do I reduce chargeback and payout hold risk when paying contractors internationally?

You cannot fully remove hold or dispute risk. Focus on clean, consistent records so you can respond quickly if a payment is challenged. In practice, keep agreement terms, approval records, and transaction evidence together for each payout.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- atsu.edu/arizona-school-of-health-sciences/academics/...trusted

- congress.gov/bill/119th-congress/senate-bill/1071/texttrusted

- ecfr.gov/current/title-15/subtitle-B/chapter-VII/subc...trusted

- federalregister.gov/documents/2026/02/27/2026-03962/employee-or-...trusted

- files.eric.ed.gov/fulltext/ED471019.pdftrusted

- govinfo.gov/content/pkg/CHRG-113hhrg86727/html/CHRG-113h...trusted

- gradpathways.ucdavis.edu/fellowstrusted

- irs.gov/publications/p525trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How LLC Owners Separate Business and Personal Finances

For an LLC, separating business and personal money is best treated as a weekly habit, not a one-time bank setup. It keeps records cleaner, cuts month-end cleanup, and creates clearer boundaries as the company grows.

What to Do If You've Been Misclassified as an Independent Contractor

Treat this as a protection problem first, not a label debate. If your work was treated as an independent contractor arrangement even though the relationship functioned differently, your first goal is to protect pay, rights, and records while you choose the least risky escalation path. You can do that without making accusations on day one, which often keeps communication open while you document what happened.

Philippines Freelance Market Analysis for Cross-Border Teams

This is a decision memo, not a marketplace pitch. If you are looking at the Philippines freelance market as a freelancer or a small cross-border team, the useful question is not just whether demand exists. It is whether the channel, margin, screening burden, and payment path make sense for the kind of work you actually sell.