Quick Answer

Start by treating what is KYC as a payout-control design choice, not a one-time onboarding form. For payment platforms, the practical baseline is CIP and KYB capture at entry, then a deliberate choice among six operating models from onboarding-only checks to risk-tiered monitoring. Put owners in place for PEP and EDD handling, and make failed-check outcomes auditable as block, hold, review, or exit. If you span the United States, United Kingdom, and European Union, scope controls by entity before launch.

Introduction for platform teams deciding KYC scope#

For payment platforms, KYC scope is a product and operations decision, not just a paperwork step. The real question is where identity checks happen, how much manual review your team can absorb, and what you do when a person or business does not pass cleanly.

KYC starts with verifying the identity of new customers at onboarding. That means the way you design it affects first-touch experience and review queues.

For marketplace and B2B platform models, individual checks are only part of the work. Many teams also need Corporate KYC, or KYB, to confirm a business is legitimate, identify who controls it, and keep an auditable record of approval or denial decisions. Use this framing before you lock scope:

- KYC is a release gate

You decide where checks sit in onboarding and later review flows. That choice shifts friction around the user journey.

- KYC is one part of broader compliance duties

Identity verification sits inside broader financial-crime compliance, so exception ownership and recheck paths need to be defined up front.

- Manual review load is real

False positives create queues, so set clear owners, SLAs, and case outcomes such as block, hold, review, or exit before launch.

- There is no single US, UK, and EU rulebook

KYC foundations span multiple regions, and US teams often anchor discussion in the Customer Identification Program under the USA PATRIOT Act. Scope, evidence, and timing do not map one-to-one across jurisdictions, so country-specific legal advice is out of scope here.

This guide is for product, payments ops, finance, and engineering owners making that scope call under shipping pressure. It gives you a ranked set of implementation options, the tradeoffs behind them, and a practical way to choose.

You might also find this useful: What Is KYB? Know Your Business Verification for Marketplace Onboarding.

Selection criteria for choosing a KYC model#

For teams moving real money, the right KYC model is the one that holds up under exceptions, not the one that only looks smooth in a demo. This guide is for teams that own payout risk, list screening, and onboarding controls. It is not for brochure-stage products with no live payouts or for teams assuming one rulebook maps U.S. and UK expectations the same way.

| Criterion | What to assess | Checkpoint |

|---|---|---|

| Regulatory fit | Whether the model can support the jurisdictions and programs you actually operate | Map controls by entity because requirements vary by jurisdiction |

| Conversion impact | Where friction belongs in the journey: signup, pre-payout, or both | Favor models that add depth at higher-risk points instead of putting the same burden on everyone at step one |

| Operational load | Capacity for queue handling, retries, outreach, and final decisions | If ownership is unclear, the model is not operationally ready |

| Escalation speed | Named ownership for high-risk cases and EDD before launch | Fast escalation means outcomes are predefined, not improvised |

| Audit traceability | Whether a reviewer can reconstruct collected data, screening results, case handling, and decision | If sample cases cannot be reconstructed cleanly, the model needs work before live payouts |

- Regulatory fit

Start here: can the model support the jurisdictions and programs you actually operate in? In the U.S., financial institutions are expected to maintain an ongoing KYC/AML program, so a model built only around initial CIP checks may stop working as flows expand. If you operate across countries, map controls by entity because requirements vary by jurisdiction.

- Conversion impact

Decide where friction belongs in your journey: signup, pre-payout, or both. A lighter onboarding step can reduce early friction, but downstream checks still depend on core identity and business details such as directors, business address, national insurance or social security numbers, and company numbers. Favor models that add depth at higher-risk points instead of putting the same burden on everyone at step one.

- Operational load

Assume manual review is part of any serious model. KYC data is screened against lists tied to governments and law enforcement, so you need capacity for queue handling, retries, outreach, and final decisions. If that ownership is unclear, the model is not operationally ready.

- Escalation speed

Set named ownership for high-risk cases and EDD before launch. KYC/AML accountability is typically owned by a dedicated risk or compliance function, and weak oversight can materially harm the institution. Fast escalation means outcomes are predefined, not improvised.

- Audit traceability

Treat traceability as a release gate. A reviewer should be able to reconstruct what data was collected, what screening returned, who handled the case, and why it passed, failed, or escalated. If sample cases cannot be reconstructed cleanly, the model needs work before live payouts.

For a step-by-step walkthrough, see SOC 2 for Payment Platforms: What Your Enterprise Clients Will Ask For.

Comparison table of six KYC operating options#

Use this table to compare operating models for payout-risk control. FATF-aligned controls are a useful baseline, but implementation varies by country, so treat fit flags and risk levels as indicative operating guidance rather than legal determinations or universal benchmarks.

| Option | Best for | US fit | UK fit | EU fit | Key pros | Key cons | Review queue pressure | Sanctions/watchlist drag | Payout-delay risk | CIP/KYB capture | PEP/EDD handling | Reverification triggers | First implementation milestone |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1. Onboarding-only identity gate | Early, simpler domestic flows | Local adaptation required | Local adaptation required | Local adaptation required | Fast launch and lower signup friction | Weaker ongoing risk view after approval | Low initially, can spike on exceptions | Lower at start, can increase as lists change | Low early, can rise later from manual holds | Basic intake | Mostly manual escalation | Often none by default | Launch identity/business intake with case logging |

| 2. Onboarding + pre-payout step-up | Teams that want control closer to money movement | Local adaptation required | Local adaptation required | Local adaptation required | Better balance between conversion and payout control | Late-stage failures can block payout release | Medium | Medium to high near payout events | Medium | Basic at onboarding, deeper pre-payout | Escalation path defined before release | Triggered at payout events | Add a pre-payout decision checkpoint |

| 3. Risk-tiered continuous monitoring | Growing cross-border programs | Local adaptation required | Local adaptation required | Local adaptation required | Ongoing checks can keep risk posture current | Higher operating complexity | Medium to high | Can create recurring drag from repeated matches | Medium to high when alerts stack | Expanded identity/business data over time | Dedicated PEP/EDD lane | Risk-event and periodic triggers | Turn on ongoing watchlist monitoring with ownership |

| 4. Outsourced compliance stack through a provider model | Teams optimizing for speed with API-led delivery | Local adaptation required | Local adaptation required | Local adaptation required | One workflow can combine document checks, biometrics, and watchlist screening | Vendor constraints can limit policy flexibility | Medium | Medium | Medium | Strong packaged capture where configured | Built-in flows, policy still needs local rules | Provider-supported recurring checks | Complete API integration into existing internal systems |

| 5. Hybrid model with internal orchestration | Platforms that need tighter control over policy logic | Local adaptation required | Local adaptation required | Local adaptation required | Better control over routing, thresholds, and escalation design | More engineering and governance overhead | Medium to high | Medium to high | Medium to high | Custom capture and routing | Internal decisioning with specialist review | Configurable by risk signals | Implement policy orchestration and decision audit trail |

| 6. Enterprise multi-entity governance model | Programs run through separate legal entities | Local adaptation required | Local adaptation required | Local adaptation required | Reduces policy drift with a shared baseline and local overlays | Slower change approvals and more documentation overhead | Can rise when evidence standards differ by entity | Shared baseline still needs entity-specific handling | Medium to high when cross-entity approvals stall | One minimum evidence standard across entities | Shared escalation criteria with local overlays | Standardized baseline with entity-specific triggers | Define one control library, decision taxonomy, and minimum evidence standard |

Option 1 onboarding-only identity gate#

Use this model only as an early-stage starting point for simple domestic flows. It can get you live quickly, but it is not a durable control model for ongoing AML risk.

Teams choose it because it keeps the first release small. You run one-time verification at signup, collect basic KYC data, and avoid heavy engineering before the product proves out. In practice, the baseline capture is the core identity set at onboarding: name, address, date of birth, and an identification number.

Where it fits is narrow. Think of a single-country contractor platform with low transaction volume, where reviewers manually escalate obvious issues. What it misses matters just as much. Onboarding checks do not replace post-onboarding AML monitoring, so risk can emerge later through transaction behavior.

Before you launch, make two minimum controls explicit:

- Verification checkpoint: log every pass, fail, and manual review with submitted identity fields, match outcome, and reviewer notes.

- Escalation rule: define what happens when a verification result needs manual review before payout.

If near-term expansion is likely, do not overbuild this model. An onboarding-only setup may require re-engineering once reverification and ongoing monitoring are needed in new markets with changing compliance standards.

Option 2 onboarding plus pre-payout step-up checks#

Use this model when onboarding-only checks are not enough. You verify identity at onboarding, then treat payout release or withdrawal as a second decision gate.

Best fit#

This fits platforms where users onboard quickly but funds move later. Run KYC at signup (often called CIP in US contexts). Then re-screen sanctions and PEP-list status before a withdrawal or payout batch is released. That keeps onboarding lighter while adding AML control at the point of funds movement.

Why teams choose it#

The advantage is timing. KYC starts at account opening, but checks can recur after onboarding, and a pre-payout step-up is a practical way to do that. In some cases, the step-up includes extra verification before withdrawal, such as Proof of Address, instead of sending every user through a high-friction flow on day one.

Operationally, make payout decisions auditable. Log the screening result used for each release, with timestamp, provider or list response, account state, and reviewer notes for manual clears. If a sanctions or PEP-list result changes after onboarding, you should be able to show whether funds were held, blocked, or released, and why.

Where it breaks#

The main downside shows up late in the flow. A PEP hit or name mismatch just before payout can create user friction and operational pressure, and manual periodic reviews are often slow and expensive. If review capacity is thin, payout runs can become a bottleneck.

Do not assume one compliance setup works across every jurisdiction. Requirements vary by market, so define pre-payout triggers by legal entity and country before you scale volume.

Need the full breakdown? Read Crypto Payouts for Contractors: USDC vs. USDT - What Platforms Must Know.

Option 3 risk-tiered continuous monitoring#

If step-up checks are catching issues too late, this is the upgrade. Risk-tiered continuous monitoring can be a stronger default than onboarding-only checks because it keeps reassessing risk after identity is first approved.

Best fit#

Use this model when an account can look low risk at onboarding and materially different soon after. Common patterns include new activity, session-origin changes, or behavior shifts after activation. You still run KYC at onboarding, but you do not treat that first decision as final.

The differentiator is the risk-based approach. Verification depth follows customer and transaction risk instead of forcing every user through the same checks. That aligns with the FATF risk-based principle reflected in the source material.

Why teams choose it#

The main advantage is timing. Continuous monitoring keeps profiles current after onboarding, so new activity or behavior shifts can surface quickly and be handled before risk compounds.

In practice, teams often use real-time risk scoring with live signals such as device history, IP reputation, and network-path context. Those signals are checkpoints, not standalone verdicts. They help you decide when to keep a low-friction flow versus trigger additional verification or manual review.

What good implementation looks like#

You do not need many tiers. You need clear triggers and clear evidence for why risk status changed.

- Start with a small tier set, for example standard, elevated, and restricted.

- Define behavior-change triggers before launch, such as unusual session context, a meaningful transaction-pattern shift, or a change in where sessions originate.

- Route higher-risk cases into a documented higher-scrutiny review path instead of leaving them in the standard queue.

For each tier change or reverification, log the trigger event, signals used, prior and new risk state, timestamp, outcome, and reviewer notes when applicable. If a decision is questioned later, the record should show how and why it was made.

Where it breaks#

This model can improve control, but it adds operational load if alert handling is weak. Fast user expectations can pressure compliance teams, and noisy triggers can overwhelm reviewers.

The tradeoff is straightforward: improve detection without adding unnecessary friction. If alerts rise but action rules stay vague, you get both high friction and weak decisions. Run this model only when you can support alert tuning, clear review ownership, and a written policy for false positives and risk-change outcomes.

This pairs well with our guide on Continuous KYC Monitoring for Payment Platforms Beyond One-Time Checks.

Option 4 outsourced compliance stack through a provider model#

If your priority is faster execution and more standardized operations, a provider-led model can work, but you should expect less control over edge cases and interpretation.

The closest grounded pattern in the source material is the EU One Stop Shop, or OSS. It is not a KYC program, but it is a useful example of the centralization tradeoff: one registration point for qualifying activity. For eligible taxable persons, OSS allows registration in one single Member State of identification for VAT declaration and payment on qualifying cross-border distance sales across the EU.

Best fit#

Use this model when you want centralized execution instead of handling every registration, return, and payment step through separate local processes. In the OSS VAT context, the EU cites red-tape reduction of up to 95% for covered use cases. That does not prove the same result for other compliance domains, but it does illustrate the centralization-versus-control tradeoff.

What you gain#

What you gain first is structure. You get predefined checkpoints and cadence instead of designing each process from scratch:

- OSS returns are submitted electronically with declared supplies and VAT due.

- Filing cadence is fixed by scheme: quarterly for non-Union and Union, and monthly for import.

- Registration is centralized through one Member State of identification.

Centralization does not remove your record obligations. The EU applies record-keeping requirements to marketplaces and platforms, including cases where the platform is not the deemed supplier.

Where it breaks#

Centralization can simplify operations, but local interpretation still matters in complex cases. For VAT Cross-border Rulings, requests must follow national VAT-ruling conditions in the relevant participating EU country.

There is also lock-in and access risk under OSS:

- The Member State of identification choice can bind you for the current calendar year plus the two following years.

- A Member State can exclude a taxable person or intermediary from a scheme.

Practical recommendation#

Use the provider for standardized intake and filing flow, but keep your internal record trail as the system of record. Keep, at minimum:

- provider status, timestamp, and the scheme or rule applied

- declared supplies and VAT due for OSS submissions

- platform record-keeping artifacts, including cases where you facilitate a supply but are not the deemed supplier

If you want a deeper dive, read What is a Politically Exposed Person (PEP)? A Compliance Guide.

Option 5 hybrid model with internal orchestration#

This is the middle ground when you need vendor speed but tighter internal policy control. You keep vendor coverage for identity verification, while your team owns the orchestration layer for decisioning and audit trails.

Best fit#

Use this model when one provider's fixed flow is too rigid, but building everything in-house is not practical. In practice, it sits between build-only and buy-only. The vendor handles core verification, while your platform applies KYC and KYB decisions by segment.

What you gain#

The main benefit is control where it matters. You keep vendor strengths on agility, scalability, and compliance resilience, while adding internal ownership of decisioning. A practical setup is a single internal rules layer that ingests provider API or webhook outcomes and maps them into your own states, such as pass, review, or retry.

Use traceability as the checkpoint. You should be able to connect provider output, internal rule path, timestamp, and resulting internal decision outcome. If that chain is weak, your auditability is weak.

Also plan for ongoing manual work. In ongoing due diligence, nearly half of client refreshes at leading institutions still rely on manual tasks.

Where it breaks#

A common risk area is post-onboarding change management, not just the initial integration. Late webhook events, changed identity outcomes, and retries can create reconciliation pressure quickly.

Provider choice also matters day to day. The wrong KYC API can increase drop-off, create manual bottlenecks, and raise regulatory risk. Hybrid still requires continuous upgrades and security patching to keep the integrated environment stable.

Concrete use case#

A common pattern is external identity verification at onboarding plus internal decisioning after onboarding. When risk signals change later, your internal layer can route the account to review based on your policy.

Practical recommendation#

If one provider covers your markets and your policy needs are mostly standard, Option 4 is usually simpler. If you expect multi-provider coverage, assess whether early internal decisioning orchestration would reduce reconciliation across provider-specific sources of truth later.

Option 6 enterprise multi-entity governance model#

If you run separate legal entities in the United States, United Kingdom, and European Union, this model can be a safer way to reduce policy drift. It can improve consistency for KYC, AML, and CTF controls across entities, but it can also slow change approvals and increase documentation overhead.

This is the point where operating model matters more than individual checks. Once you are managing multiple entities, the hard part is not collecting more data. It is keeping evidence, decisions, and local overlays consistent enough that a regulator, banking partner, or internal audit can follow the same story across regions.

Best fit#

Use this when you have outgrown a single compliance owner or a single-country rule set. KYC rules vary by jurisdiction even when the core goal is the same, so a shared global standard with local overlays can be more reliable than market-by-market improvisation.

The core design is a global baseline for identity verification, due diligence, risk assessment, ongoing monitoring, and sanctions or watchlist screening, with each entity mapped to its local requirements.

What good governance actually standardizes#

At minimum, define one evidence standard for every onboarded customer or business across entities. In practice, that can mean consistent requirements for identity verification, KYB where relevant, risk rating, sanctions or watchlist checks, escalation criteria, and reverification triggers.

A practical checkpoint is evidence completeness by entity. For one customer, you should be able to retrieve identity result, KYB result if applicable, sanctions or watchlist outcome, risk decision, escalation notes if any, and the approving legal entity. If each entity stores different evidence shapes, audit friction rises quickly.

Where it earns its keep and where it hurts#

This model is most useful when regulators, banking partners, or internal audit ask the same cross-region question. Who approved this customer, under which policy, with what evidence, and what ongoing monitoring applies? Centralized policy ownership makes that answer clearer.

The tradeoff is slower change velocity. Even small onboarding updates can require product, legal, compliance, and cross-entity alignment. Manual KYC handling makes this worse, and incomplete or inconsistent documentation can delay approvals and downstream operating plans.

Concrete use case#

A practical setup is one global policy with local overlays for U.S., U.K., and EU entities. The global layer defines minimum evidence and screening standards. Each local layer adds the extra steps that entity needs for local requirements.

Execution remains hard because documents, address formats, and language vary by region. A verification setup that works cleanly across all 50 states may still be weaker for international users, so avoid treating one entity's document assumptions as the default everywhere.

Practical recommendation#

Choose this model when cross-entity consistency matters more than speed. Build one control library, one decision taxonomy such as pass, review, retry, reject, and one minimum evidence standard before you optimize local flows.

A simple decision rule: if each entity can explain local obligations but cannot produce the same minimum customer evidence pack, fix the documentation model first, then approvals, then automation.

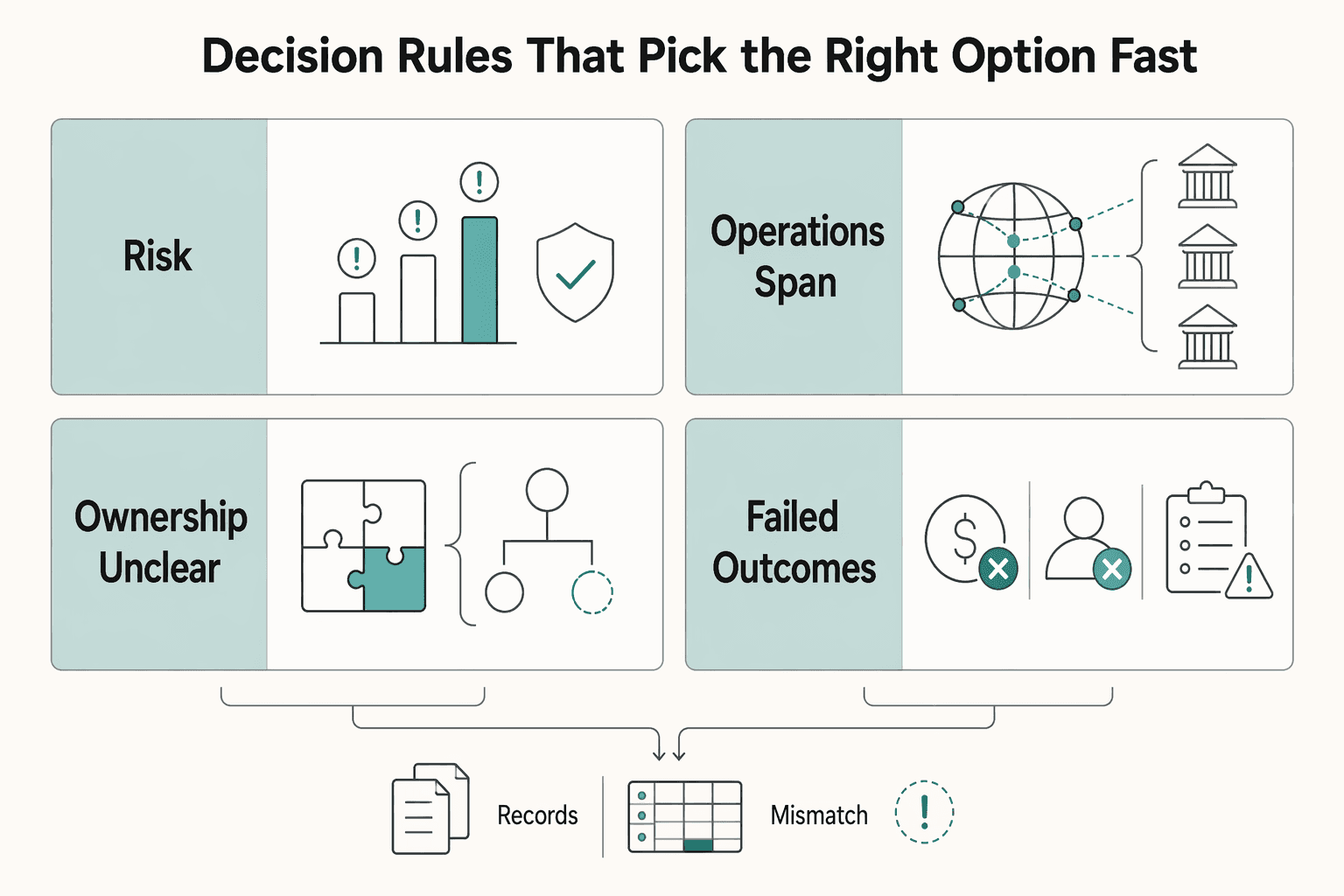

Decision rules that pick the right option fast#

Choose your model based on the failure that would hurt you most, not on a feature checklist. Once you know whether your main risk is payout loss, onboarding drop-off, or policy drift across entities, the right option becomes easier to spot.

| Situation | Recommended direction | Why |

|---|---|---|

| Payout fraud is the primary risk | Prioritize ongoing controls with sanctions list screening and a clear escalation path before funds move | One-time onboarding checks leave gaps because KYC also extends to in-life customer monitoring |

| Onboarding drop-off is the primary risk | Start with onboarding plus step-up checks | Use a risk-based approach so checks deepen only when signals justify it |

| Operations span the United States, United Kingdom, and European Union | Map requirements by entity and confirm the same minimum evidence pack can be produced for a case | KYC and AML obligations vary by country |

| Ownership is unclear across product, ops, and legal | Pause rollout and assign clear KYC/AML escalation ownership before launch | Responsibility for KYC and AML usually sits with a dedicated risk or compliance owner or team |

| Failed-check outcomes are not defined and auditable | Do not launch until explicit internal outcomes are set and each case is logged consistently | The checkpoint is whether you can retrieve the identifiers collected, list-screening outcome, final decision, and accountable approver for a failed case |

- If payout fraud is your primary risk, prioritize ongoing controls.

Favor a setup that supports sanctions list screening and a clear escalation path before funds move. One-time onboarding checks leave gaps because KYC also extends to in-life customer monitoring.

- If onboarding drop-off is your primary risk, start with onboarding plus step-up checks.

Apply a risk-based approach so checks deepen only when signals justify it, instead of running full-depth checks on every applicant on day one. Keep initial collection focused on core identity or business data, then escalate when risk indicators appear.

- If you operate across the United States, United Kingdom, and European Union, map by entity.

Do not assume one rulebook works everywhere. KYC and AML obligations vary by country, and U.S. institutions are expected to maintain an ongoing KYC/AML program. Before scaling, confirm each entity can produce the same minimum evidence pack for a case: collected identity or business data, list-screening result, decision, and accountable owner. If you need a country view, use the KYC/KYB requirement mapper.

- If ownership is unclear across product, ops, and legal, pause rollout.

Responsibility for KYC and AML usually sits with a dedicated risk or compliance owner or team. Assign clear ownership for KYC/AML escalation decisions before launch.

- Do not launch until failed-check outcomes are defined and auditable.

Use explicit internal outcomes and log each case consistently. The checkpoint is simple: can you retrieve the identifiers collected, list-screening outcome, final decision, and accountable approver for a failed case?

Turn your chosen option into an execution plan with clear decision states and webhook handling in the Gruv docs.

Implementation checklist by function and sequence#

KYC implementation works when ownership, escalation, and payout rules are defined before tooling details. Use the sequence below so product sets evidence points, engineering keeps outcomes consistent, ops makes decisions defensible, and finance plus compliance control fund movement.

| Function | Primary focus | Practical checkpoint |

|---|---|---|

| Product | Define where evidence is collected in the journey and where CIP or business-verification evidence is required | Show when evidence is collected, when deeper review is triggered, and what happens on refusal or failure |

| Engineering | Keep case outcomes consistent across retries, delayed responses, and status changes while limiting sensitive data exposure | Retrieve one case end to end with collected inputs, list-screening results, status history, timestamps, and approver or change history |

| Ops | Turn screening output into audit-ready decisions with review timelines, escalation paths, additional evidence requirements, and approver authority | Case notes should let another reviewer or auditor reconstruct why a case was cleared, held, blocked, or exited |

| Finance and compliance | Align payout release logic to AML policy and keep reporting and recordkeeping responsibilities explicit | Define which outcomes release funds, which hold funds, and which require compliance signoff |

- Product sequence

Start by defining where evidence is collected in the journey, then map checks to those points. Set where CIP or business-verification evidence is required, at account creation, pre-payout, or both, and define artifact requirements by path, such as director names, business addresses, social security or national insurance identifiers where applicable, and company numbers.

Treat KYC as ongoing, not only onboarding. In the U.S., programs are expected to be ongoing, and country requirements differ. Document entity-specific events that trigger renewed review and publish them in your customer acceptance policies.

Practical checkpoint: for each onboarding path, can product show when evidence is collected, when deeper review is triggered, and what happens on refusal or failure? Over-collecting on day one can increase manual review and slow onboarding.

- Engineering sequence

Build for consistent case outcomes across retries, delayed responses, and status changes. Consistent case-state handling and reconciliation controls help keep one stable case history instead of conflicting records.

Keep sensitive data exposure limited while preserving decision evidence. Operational views should still support screening, escalation, and later review.

Engineering checkpoint: can one case be retrieved end to end with collected inputs, list-screening results, status history, timestamps, and approver or change history?

- Ops sequence

Ops turns screening output into audit-ready decisions. Define internal review timelines, escalation paths for higher-risk cases, required additional evidence, and approver authority by outcome.

Decision quality depends on case-note quality. Notes should explain why a case was cleared, held, blocked, or exited, so another reviewer or auditor can reconstruct the reasoning without relying on the original analyst. If a reviewer cannot distinguish a data mismatch from a higher-risk match, escalate before payout release.

- Finance and compliance sequence

Align payout release logic to AML policy before encoding treasury or payout rules. Define which outcomes release funds, which hold funds, and which require compliance signoff.

Keep reporting and recordkeeping responsibilities explicit. Operational duties include suspicious-activity reporting and customer recordkeeping, and weak controls can lead to penalties and reputational damage. Use customer acceptance policies as the control anchor: document them formally, publish them internally, and review them regularly.

| Done criterion | What to verify before launch | Why it matters |

|---|---|---|

| Owners assigned | Named product, engineering, ops, and compliance owners for CIP intake, list-screening review, escalation, and payout holds | KYC/AML responsibility is typically assigned to a dedicated risk/compliance lead or team |

| Failure states implemented | Clear internal outcomes such as block, hold, review, or exit, and who can apply each | Reduces ad hoc decisions in higher-risk cases |

| Audit trail test passed | A sample case is retrievable end to end with evidence, screening result, notes, timestamps, and final decision | Supports defensible recordkeeping and review |

| Country and program caveats documented | Entity-specific notes for U.S., U.K., and EU programs where rules or evidence expectations differ | KYC/AML requirements vary by country |

Before launch, test one failed case and one cleared case across product, engineering, ops, and finance. If any team cannot quickly explain the decision and produce the record, the implementation is not ready.

Related reading: Sequencing Your Payment Product Roadmap: What to Build First When Launching a New Platform.

What to do next for your platform#

Move now with a clear operating model, clear ownership, and records you can defend. You do not need a perfect global policy first, but you do need a documented way to show how KYC and AML decisions are made and reviewed.

- Pick the option that matches your real exposure.

Lower-risk, narrow programs can start with onboarding checks. Recurring or cross-border payout programs often need deeper controls, including continuous monitoring, because KYC is ongoing, not only account opening. In the U.S., BSA framing is an ongoing KYC/AML program, not a one-time form.

- Build the minimum evidence trail now.

Define your CIP intake fields, where records are stored, how data is screened against official lists, who handles escalations, and how suspicious activity is documented for reporting. For business onboarding, grounded examples include directors' names, business addresses, national insurance or social security numbers, and company numbers. Keep the decision path, not just the outcome: what matched, what was cleared, what required enhanced review, and who approved it. If you cannot replay a decision from records alone, the process is too fragile.

- Confirm provider and market coverage in writing before launch.

Country rules vary, so "supported market" is not enough on its own. Confirm exactly what data is collected, whether official-list screening is included, whether continuous monitoring is available, and which party owns escalations and record retention. Then have legal and compliance confirm the obligated entity for each market you launch. If coverage differs by country, start with a country-level reference like the KYC/KYB Requirement Mapper, not a reused setup from another market.

Reported fraud losses reached $12.7 billion in 2024, up 25% year over year. Weak execution raises fraud exposure, fine risk, and trust loss, and poor KYC/AML oversight can seriously damage operations.

Related: The Compliance Cost of Going Global: What Platforms Spend on Tax KYC and Licensing Per Country.

If your rollout spans multiple entities or markets, validate coverage and control design before go-live with the Gruv team.

Frequently Asked Questions

What is KYC in one sentence for a payment platform?

Know Your Customer is a due diligence process used to verify customer identity and assess risk. For platforms, it is not just a signup step because it also includes ongoing monitoring after onboarding.

Is KYC only required for banks, or also for fintech and marketplace payout programs?

It is not only a bank concept. The grounded sources explicitly name banks, credit unions, and other financial institutions as subject to strict standards. Whether a fintech or marketplace program is in scope can depend on the regulated setup behind it. Confirm the obligated legal entity before go-live.

What information is usually collected in KYC and KYB checks?

A Customer Identification Program commonly collects and verifies name, date of birth, address, and identification number. In banking contexts, proof of identity and proof of address are also commonly required. For KYB, exact document requirements are not universal in this material and can vary by country.

How is KYC different from AML, CTF, and due diligence?

KYC is part of a broader AML and CTF framework, not the whole framework by itself. A practical split is CIP for core identity collection, CDD for risk assessment, and ongoing monitoring after onboarding. The full legal boundary between AML, CTF, and due diligence is jurisdiction-specific.

When should a platform repeat KYC or trigger enhanced due diligence?

The grounded rule is that KYC is ongoing, not one-and-done at onboarding. Exact reverification or enhanced-due-diligence triggers are not specified here, so teams typically define policy-based, risk-based trigger events before launch.

What happens operationally when a user fails KYC or appears on sanctions lists?

What is clear is that weak or noncompliant KYC is associated with fines, higher fraud exposure, and loss of trust. In practice, teams usually handle failures through controlled policy decisions rather than ad hoc overrides.

How should teams handle country differences across the United States, United Kingdom, and European Union?

Start from the assumption that KYC strictness varies by geography. For U.S., U.K., and E.U. programs, map requirements by entity and market instead of applying one global rulebook unchanged. A country-specific reference point such as the KYC/KYB Requirement Mapper can be more reliable than copying one market’s approach everywhere.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- digitalcommons.law.lsu.edu/cgi/viewcontent.cgitrusted

- epar.evans.uw.edu/wp-content/uploads/2024/08/EPAR_UW_Request_3...trusted

- federalregister.gov/documents/2025/01/08/2024-31486/preventing-a...trusted

- sec.gov/comments/s7-2024-02/s7202402-489683-1406226.pdftrusted

- sec.gov/files/ctf-written-input-daniel-bruno-corvelo...trusted

- taxation-customs.ec.europa.eu/archives/taxable-persons/vat-cross-border-ru...trusted

- vat-one-stop-shop.ec.europa.eu/index_entrusted

- vat-one-stop-shop.ec.europa.eu/one-stop-shop_entrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

What Is a Politically Exposed Person and How to Decide Next Steps

Use this guide to make one clear onboarding call each time: proceed with standard checks or escalate before funds move. The goal is simple: cleaner onboarding, fewer payout surprises, and AML records you can defend later.

What Platforms Spend Per Country to Stay Compliant in Global Expansion

Per-country compliance cost planning starts with the operating model, and that choice needs to happen early. Use this guide if you are a compliance, legal, finance, or risk owner making country launch decisions before go-live. It helps you test assumptions before they turn into delays, rework, or avoidable spend.

KYC KYB Requirements by Country for Platform Onboarding Decisions

---