Quick Answer

KYB is the business-verification control used to decide whether a company can enter a financial relationship on your marketplace. In practice, it means more than checking registration data: it includes resolving UBO ownership, linking risk signals to approval outcomes, and holding money-moving access when records are incomplete. It sits beside KYC in CDD, with separate branches for entities and individuals.

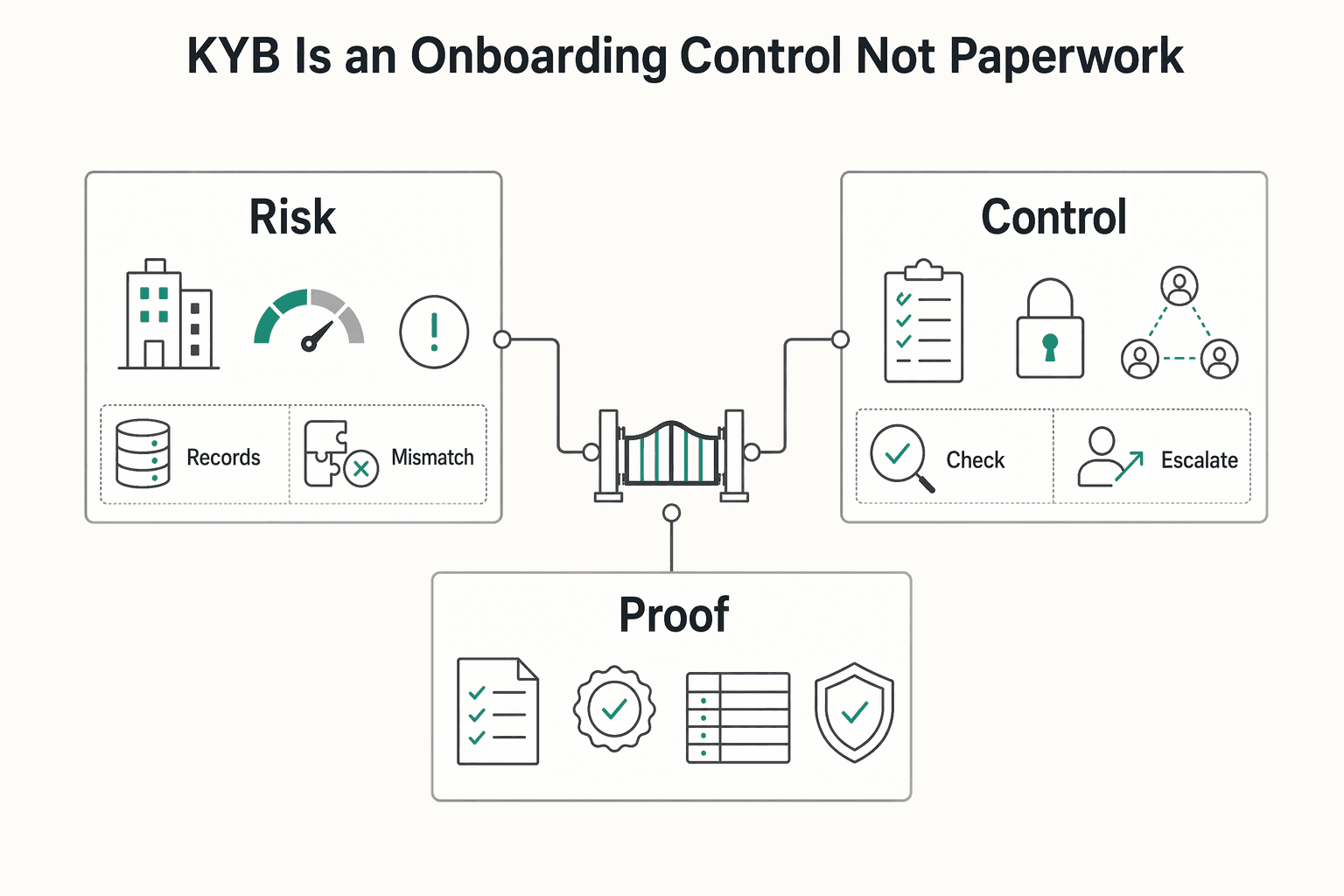

KYB is an onboarding control, not paperwork#

Marketplace onboarding usually breaks in one of two ways: the team treats Know Your Business (KYB) as a compliance label with no product consequences, or it rushes activation and discovers business-identity or risk issues when money is about to move. For platforms running embedded payments, KYB is better understood as an operating gate for business customers. It is a documented decision on whether the entity is understood well enough to enter a financial relationship.

At a basic level, KYB is the verification process financial institutions use to assess business counterparties. It sits alongside Know Your Customer (KYC), which verifies natural persons, within broader AML and CFT controls. That definition matters, but the practical question is not only the definition. It is where the business check sits in your onboarding path, what evidence supports approval, and who handles exceptions when the record is incomplete or contradictory.

That shift from definition to execution is where teams either gain control or create rework. A marketplace can make signup feel smooth, but if ownership and registration records are not captured in a way compliance can trust, the friction shows up later. The usual failure mode is not "we forgot a form." It is "we let the account look complete in product, but finance or compliance cannot explain why it was approved."

The first checkpoints are simple and worth stating explicitly. You need a policy that says which account types are treated as legal entities and therefore require business verification. You need a product flow that collects the right business details once, in the right order, instead of scattering them across support tickets and back-office follow-ups. You also need a review path for cases that are not clean on first pass, including unresolved ownership or other elevated risk signals.

One early detail matters more than teams expect: evidence retention. A green status in the UI is not enough. If you cannot later show what registration data was checked, what screening result was returned, and why an analyst approved or held the account, you do not really have a reliable control. The same goes for escalation design. If ownership cannot be reconciled to credible records, do not improvise at go live. Decide in advance whether the account pauses, moves to manual review, or is limited to non-financial activity.

This guide takes that practical view. It moves from KYB basics into the decisions platform teams actually face in production: where KYB and KYC meet, what the minimum evidence pack should contain, how to tier risk, what varies by jurisdiction and program, and how to keep onboarding fast without weakening AML controls. Related reading: What Is FinCEN for Freelancers and FinTech Users.

What KYB means in marketplace onboarding#

In marketplace onboarding, Know Your Business (KYB) is the business-entity check within Customer Due Diligence (CDD) that confirms whether a company is legitimate, who owns or controls it, and whether the relationship risk is acceptable. It sits alongside Know Your Customer (KYC), but the scope is different: KYC verifies individuals, while KYB verifies the business those individuals represent.

For platform teams, KYB is a decision point, not just a signup label. A case is only meaningfully complete when the legal entity and ownership structure can be validated, including directors and the Ultimate Beneficial Owner (UBO).

This is where weak onboarding shows up: the account looks complete in product, but ownership and control are still unclear. If someone reopens the file later, they should be able to see what business details were verified, what ownership data was collected, and why the account moved forward.

KYB is designed to reduce concrete risk, including shell company misuse and hidden ownership that can create downstream AML and CTF exposure. When ownership cannot be reconciled to credible records, treat the case as unresolved and move it to review instead of guessing.

KYB and KYC decisions in one onboarding flow#

Run KYB for legal entities and Know Your Customer (KYC) for natural persons; inside Customer Due Diligence (CDD), they are complementary rather than interchangeable.

Many marketplace flows need both checks in one case. For a business account, KYB verifies the entity, and due diligence also covers the people tied to ownership or control, including directors and Ultimate Beneficial Owner (UBO) records. If you stop at entity-only verification, you leave a common AML gap.

Map the decision before you build the form#

Define KYC and KYB branches by account type at design time, then tie each branch to activation rules. Do not leave that choice unresolved just to move faster once the funnel is live. At minimum, your map should answer:

| Decision point | What to define |

|---|---|

| Counterparty type | Whether the counterparty is a natural person or a legal entity |

| Related people for legal entities | Which related people also require person-level verification |

| Locked capabilities | Which product capabilities remain locked until each check is complete |

Your audit trail should also show why KYC ran, why KYB ran, and which person profiles were linked to the business record.

The common failure mode#

A frequent mistake is treating entity registration as enough and skipping ownership/control-linked people. That usually surfaces later during money movement or risk review, when the team cannot clearly show who owns or controls the company. The opposite error is forcing business verification on individual counterparties and adding avoidable friction.

If account type is unclear, treat it as a gating issue and resolve it before you enable sensitive features.

Keep a separate branch for MoR and direct models#

If you run both Merchant of Record (MoR) and direct-platform programs, keep a distinct policy branch for each model and validate the decision logic with legal or compliance before you merge flows.

You might also find this useful: KYC KYB CIP Explained for Cross-Border Freelancers and Small Teams.

The minimum KYB evidence pack you need before activation#

Treat your minimum Know Your Business (KYB) file as an activation gate, not a checklist. Before any money movement, you should be able to verify legal-entity legitimacy and resolve who in the end owns or controls the business through credible Ultimate Beneficial Owner (UBO) records. If ownership cannot be resolved, keep the account in a no-money state or hold it.

At minimum, the file should include legal name, registration status, business address, directors, UBO ownership/control data, and screening results from your policy checks. The point is to show legal existence, ownership/control visibility, and a risk review record under your AML and CTF control framework.

Build the file for audit, not just approval#

A UI approval state alone is not enough. Your record should let a reviewer see what was checked, when it was checked, what matched, and what was reviewed or overridden.

Store decision artifacts, not just pass/fail outcomes. Keep the underlying business and ownership records you relied on, screening outputs with timestamps, and notes for manual review decisions. If the case file only says "passed KYB," your Customer Due Diligence (CDD) trail is still thin.

Set the gate by product stage#

Define evidence requirements by stage so standards do not drift:

| Evidence item | Required for account creation | Required before first payout | Required for higher limits |

|---|---|---|---|

| Legal name and registration status | Capture and verify | Must still be valid | Refresh if stale or changed |

| Business address | Capture | Verify mismatches or missing detail | Refresh on material change or risk signal |

| Directors | Capture directors or controlling persons | Confirm the record is complete for review | Refresh on change |

| UBO ownership and control data | Capture submitted ownership/control data | Must be resolved to credible UBO records | Re-review complex or changing structures |

| Screening results | Record policy-check results | Results should be current and retained in the case file | Re-screen before raising exposure |

The UBO row is the critical gate. Basic registration checks can confirm an entity exists, but unresolved ownership/control is where risk tends to remain hidden.

If ownership data is incomplete or contradictory, do not move the account into financial use. Keep no-money features only, or hold the account until the case is resolved. Also tie KYB to a named case record with status history from created to reviewed to payout-eligible, so each stage has clear supporting evidence.

How to tier KYB risk and when to escalate#

After the minimum file is complete, move beyond a pass/fail mindset to explicit risk tiers tied to product permissions. A risk-based KYB model lets lower-risk businesses move faster while higher-risk cases get deeper review before money movement.

Build tiers from the file#

Use the signals your KYB checks already produce: ownership analysis, legitimacy checks, and screening against adverse media, watchlists, and PEP lists.

| Risk tier | What the file looks like | Operational treatment |

|---|---|---|

| Low | Ownership and control are clear, legitimacy checks are consistent, and screening shows no material concerns | Progress through onboarding with standard controls |

| Medium | The file is plausible but still has unresolved risk signals (for example, ownership opacity, adverse indicators needing context, or shell-company patterns) | Allow constrained activity only and hold payout access until review is complete |

| High | Serious unresolved risk signals (for example, watchlist/PEP concerns your policy escalates, or conflicting registration records you cannot reconcile) | Block financial actions and route to manual compliance review with full case evidence |

Define escalation triggers before the queue fills up#

Set escalation rules in advance so product, ops, and compliance make the same decision from the same evidence. At minimum, define triggers for:

| Escalation trigger | Condition from the section |

|---|---|

| Watchlist or PEP results | Not auto-cleared by policy |

| Registration records | Conflicting or incomplete |

| Ownership structures | Cannot be tied to credible UBOs |

| Adverse indicators | Remain unresolved after initial review |

This is where teams avoid fragmented KYB decisions: medium risk stays controlled, and high risk stays blocked until disposition is clear. Keep the evidence trail complete so a reviewer can quickly see why a case was advanced, constrained, or escalated.

What is mandatory vs what varies by country and program#

The mandatory-versus-policy split starts with one hard anchor: FinCEN lists Customer Due Diligence Requirements for Financial Institutions as an Action Type Final Rule with a Release Date of May 11, 2016. Beyond that, confirm specifics about PATRIOT Act KYB duties, EU AMLD duties, UBO depth, monitoring cadence, or penalties with the relevant authority.

That is the rule for this section: when someone says a control is mandatory, require the exact rule, the jurisdiction, and the entity in your stack that is bound.

The one hard anchor and what stays unknown#

Use the FinCEN CDD item above as the named U.S. basis. Confirm with the relevant authority whether your platform is directly covered, which entity types are in scope for your flow, what UBO depth is required, or how often files must be refreshed.

Before launch, keep a short legal-basis memo per country and program with four fields:

| Memo field | What to record |

|---|---|

| Rule or directive | The rule or directive |

| Bound entity | The entity in your stack that is bound |

| Affected product capability | The affected product capability |

| Control basis | Whether the control is mandatory, partner-imposed, or internal policy |

If those fields are incomplete, do not present the control as legally required.

Europe is usually an interpretation problem#

In Europe, "AMLD requires this" is usually too vague for implementation. You need to separate the claim source: directive-level language, including 4AMLD, 5AMLD, and 6AMLD, versus country-level implementation and program design. You can name those regimes, but confirm their specific KYB obligations with the relevant national authority.

| Jurisdiction or program view | Legal basis you can name | Entity types covered | UBO depth expectation | Monitoring cadence | Unresolved legal questions |

|---|---|---|---|---|---|

| U.S. flow involving a regulated financial institution | FinCEN Customer Due Diligence Requirements for Financial Institutions (Final Rule; May 11, 2016) | Confirm with the relevant authority | Confirm with the relevant authority | Confirm with the relevant authority | Is your platform directly covered or only the partner institution? Which controls are mandatory vs partner policy? |

| U.S. flow where the USA PATRIOT Act is cited | Named regime only; no operative KYB requirement specified | Confirm with the relevant authority | Confirm with the relevant authority | Confirm with the relevant authority | Which section is being relied on? Does it apply to your product design and sector? What penalties attach? |

| Europe at directive level | EU Anti-Money Laundering Directives named, including 4AMLD, 5AMLD, 6AMLD | Confirm with the relevant authority | Confirm with the relevant authority | Confirm with the relevant authority | Which directive version controls your case, and what does it require for your sector? |

| Europe at country and program level | Local AMLD implementation and partner program terms need separate confirmation | Country- and program-specific | Unknown until local review | Unknown until local review | Exact sector scope, exact penalties, and whether a control is mandatory or best practice |

If your evidence file has ownership and screening data but no clear legal basis for each control, expect rework at payout time. Keep country rules and product rules separate, and validate both before rollout. For country-by-country implementation planning, see KYC/KYB Requirement Mapper: What Each Country Demands for Platform Onboarding.

How to implement KYB without stalling growth#

Implement KYB as a decision workflow tied to activation gates, not as a document inbox. Keep straightforward cases moving with minimal manual review, and route higher-risk cases into a clear review path with traceable evidence.

This sequencing matters because manual or outdated handling becomes a bottleneck, and every extra day in onboarding increases drop-off risk and delays time-to-value. For embedded payments, that usually shows up as onboarding progress without usable money movement.

Start with policy, then lock the data model#

Start with policy before UI work. Define clear outcomes, for example approved, approved with limits, or pending review, what evidence supports each outcome, and what triggers escalation.

Then align your data model to that policy. Use a persistent business identity profile: one internal record that acts as a single source of truth for business identity, verification outputs, and review decisions. Without that, teams end up piecing together fragmented data across tools and creating avoidable operational drag.

Only then wire API and UI capture. Ask for a strict minimum evidence pack for the first decision, and collect additional data when risk, country, or product usage requires it.

Orchestrate checks so product controls follow the decision#

Use a consistent sequence: capture data, run verification and screening, route exceptions to manual review, then apply activation gates for embedded payments. Tie KYB outcomes directly to product controls so permissions are predictable.

| Product capability | Pending or incomplete verification | Approved | Escalated or blocked |

|---|---|---|---|

| Create invoices | Limited or conditional access | Allow | Restrict based on policy |

| Use Virtual Accounts | Hold | Allow | Block |

| Execute payout batches | Hold | Allow within approved limits | Block until resolved |

Launch narrow first: strict minimum evidence pack, conservative automation, and explicit manual-review routing. Expand automation after false-positive and review-volume baselines stabilize.

Build for retries, status history, and audit export#

Design screening integrations for idempotent retries and webhook-driven status updates so repeat events update the same case instead of creating duplicates. Keep a reconciled status history from submission to final decision.

Before activation, finance and ops should be able to confirm traceable decision logs and exportable audit artifacts. The implementation is working when compliance status, product permissions, and finance release logic stay aligned.

Mistakes that cause KYB rework and compliance incidents#

Most KYB rework comes from one pattern: teams treat approval as final even while risk, ownership, and product scope keep changing.

Treat approval as a dated decision#

Treat each approval as time-bound, not permanent. A business record is a snapshot, so if you approve once and never revisit, controls can drift while the account still moves money.

FinCEN lists the Customer Due Diligence Requirements for Financial Institutions as a final rule with a release date of May 11, 2016. That is a practical reminder that due diligence is not just a signup artifact. Your internal record should show the approval date, the evidence used, and the next refresh trigger.

A practical checkpoint is simple: every approved business should have both a status and a freshness state. If status is approved but ownership or registration evidence is stale, finance should see that before funds are released.

Documents are not the same as ownership resolution#

A document set alone does not resolve Ultimate Beneficial Owner (UBO) ambiguity. Teams often collect registration files and close the case, then hit rework at payout or downstream review when ownership and control must be explicit.

If policy does not define how ownership must be resolved, analysts will improvise case by case. That creates inconsistent approvals and weak audit defense. If the ownership chain is incomplete or contradictory, hold money-moving features pending review.

Your evidence bundle should show:

- the ownership snapshot used for the decision

- unresolved gaps or assumptions

- who approved any exception

Do not automate away judgment#

Over-automation creates incidents when ambiguous cases pass or block without clear human escalation criteria. The issue is not automation itself; it is missing rules for when near matches or higher-risk flags must stop for review.

Apply the same discipline to legal scope. Do not promise product access in a new country or flow while AMLD interpretation or applicability of FinCEN CDD requirements is still under assessment. If you need a country-level starting point, use KYC/KYB Requirement Mapper: What Each Country Demands for Platform Onboarding.

Conclusion#

The clearest test is simple: if your team cannot explain, in plain English, why a business was approved, limited, or held, your process is not ready. Know Your Business (KYB) works best when it acts as an activation control tied to money movement, not as a glossary term sitting beside signup.

For marketplace teams, the practical win comes from combining business checks, individual checks, and product controls instead of treating them as separate tracks. KYB verifies the entity. KYC verifies the relevant people behind it. Customer Due Diligence (CDD) ties those checks to a decision you can defend later under AML expectations. That combination can help you move faster without giving full financial access to accounts you cannot actually explain.

A good operating standard is straightforward. Keep a defined evidence pack for approval, keep the artifacts that supported the decision, and define the exact cases that must go to manual review. The checkpoint that matters most is not whether the UI shows "verified." It is whether the case file shows the business details, ownership evidence, and review results that support the outcome. If the only record left behind is a pass flag, expect rework when payouts, audit questions, or partner reviews catch up with you.

The common failure mode is predictable. Teams try to speed up onboarding with manual PDFs, email threads, or thin document collection, then discover gaps too late in the process, including ownership clarity issues near payout activation. That slows users down and weakens controls at the same time. A better tradeoff is to allow low-risk setup steps first, then hold payouts, account upgrades, or other money movement until the business record and control picture are complete.

If you want a concrete next step, do this in order:

- Map your current onboarding flow from account creation to first payout and mark where KYB, KYC, and escalation decisions actually happen.

- For each gate, write down the evidence required, who can approve exceptions, and what is stored for audit.

- Before enabling new payout or account capabilities in a country or program, confirm the minimum KYC and KYB data required for that region and sponsoring bank.

That last step matters because requirements are not universal. The minimum data can vary by jurisdiction and bank partner, so do not treat one market's checklist as globally portable. If you need a place to start that review, use the KYC/KYB Requirement Mapper: What Each Country Demands for Platform Onboarding.

KYB is more than business verification. It is the decision point that should control access, capture evidence, and hold the line when the ownership or risk picture is still incomplete.

Frequently Asked Questions

What is KYB in simple terms?

Know Your Business means verifying that a company is real and understanding who is behind it. In practice, that usually means checking the entity's registration details and the identities of its directors or owners as part of risk and onboarding controls.

How is KYB different from KYC for marketplace onboarding?

KYC focuses on an individual. KYB focuses on a business entity. In business onboarding, teams may use both, because a company account can still involve real people who own or control it.

Which documents and checks are usually required in KYB?

A common starting set is registration documents, business address details, and identity information for directors and owners.

Why is UBO identification central to KYB decisions?

Because a valid company record does not always show who ultimately owns or controls the entity. KYB checks director and owner identities to determine Ultimate Beneficial Ownership (UBO), which helps make the control picture clearer for risk decisions.

Is KYB legally required in every country and every program?

No universal rule fits every country or program. Requirements can vary significantly by jurisdiction. Financial companies are commonly described as required to complete KYB, but you should confirm the rule for your specific market and product.

Can we allow partial onboarding before KYB is complete?

This grounding does not define universal rules for partial onboarding permissions. Whether partial access is allowed depends on jurisdiction-specific requirements and your program's compliance design.

When should a KYB case be escalated to manual review?

This grounding does not specify exact escalation triggers. In practice, unresolved ownership/control details or inconsistent core business records are common reasons to require additional review.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 3 external sources outside the trusted-domain allowlist.

- fincen.gov/resources/statutes-regulations/federal-regis...trusted

- fincen.gov/report-foreign-bank-and-financial-accountstrusted

- complyadvantage.com/insights/kyb-vs-kyc-differenceexternal

- moodys.com/web/en/us/kyc/resources/insights/what-is-kyb...external

- taktile.com/articles/what-is-kyb-onboarding-how-to-balan...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

KYC KYB Requirements by Country for Platform Onboarding Decisions

---

Permanent Home Test in a Tax Treaty: Meaning, Evidence, and Tie-Breaker Rules

For the elite global professional, "permanent home" is not a term of comfort; it is a high-stakes legal definition that can trigger crippling double taxation. While other guides offer academic theory, this is a strategic playbook. We will transform your compliance anxiety into agency with a clear, three-step framework to audit your footprint, build your evidence, and early control your tax residency.

What is the 'Center of Vital Interests' in a Tax Treaty?

Start by making one defensible tax residency call based on facts, not on a preferred country outcome. Use the treaty tie-breaker in order, document why each step does or does not resolve residence, and stop at the first clear result.