Quick Answer

FinCEN is the U.S. Treasury bureau tied to FBAR filing through FinCEN Form 114. For freelancers and FinTech users, the practical question is whether foreign-account facts trigger action. Start by listing accounts and signature authority, then check if combined balances crossed $10,000 during the year. If they did, prepare filing support and timeline tracking; if ownership, control, or jurisdiction details conflict, pause and get professional review before you submit.

What FinCEN Means for Freelancers and FinTech Users#

If you are asking what is fincen, focus first on the decision in front of you. FinCEN, the Financial Crimes Enforcement Network, is tied to FBAR filing through FinCEN Form 114 when foreign financial accounts create reporting duties. By the end, you should know whether to act now, gather records, or escalate.

Keep the scope practical and immediate: account inventory, filing checks, and record quality across banks and platforms. The goal is clean decisions and clean records, not fear-driven guessing.

Start with the key checkpoint. If your foreign financial accounts exceeded an aggregate value of $10,000 at any point in the calendar year, that can trigger an annual FBAR filing. The FBAR due date is April 15, with an automatic extension to October 15. Whether an account produced taxable income does not decide whether it is a foreign financial account for FBAR purposes.

Use this decision path before your next transfer or filing window:

- List each foreign account or platform balance, the legal owner, and any signature authority.

- Check whether combined foreign balances exceeded $10,000 at any time during the year.

- Set status:

immediate action,gather evidence, orescalatewhen ownership or jurisdiction is unclear.

Do a quick sanity check before you move money again. If one account is under your personal name, another is under a business entity, and a platform profile uses a different display name, treat that mismatch as a documentation issue now. Resolve those mismatches early so your records stay consistent during filing checks.

For documentation, keep one dated pack with account statements, transaction exports, and a short ownership and purpose note. When you calculate maximum account value, record amounts in U.S. dollars and round up to the next whole dollar. Periodic statements are usable when they fairly reflect the yearly maximum.

If you cannot clearly explain who owns each account, who controls it, and why funds moved, escalate early. Not everyone with foreign activity files the same forms, but everyone benefits from consistent records and a clear decision trail. If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

What FinCEN is and what it is not#

Your filing decisions get easier when the agency role is clear. FinCEN sits within the U.S. Department of the Treasury and focuses on preventing and detecting financial crime through information sharing. It is not your personal filing coach.

| Situation | Deadline | Section note |

|---|---|---|

| Certain U.S. individuals with signature authority but no financial interest | April 15, 2026 | Notice FIN-2024-NTC7, issued November 20, 2024, extended the FBAR filing date |

| Some previously extended signature-authority deadlines | April 15, 2027 | Further extended |

| Other individuals with an FBAR obligation | April 15, 2026 | Due date remains April 15, 2026 |

A useful anchor is FinCEN's own description: it is "a network, a link between the law enforcement, financial, and regulatory communities." That framing helps explain why banks and regulators may ask for overlapping records even when their duties are different.

FinCEN describes money laundering as disguising financial assets so illegal origins are harder to detect. Those checks are generally built around that risk, not your convenience or filing timeline.

Keep three separate events distinct in your mind: a platform approves a payout, a bank asks follow-up questions, and you assess your own filing duty. Those events can occur on different dates and still all be valid. Conflating them can cause people to miss a personal filing action.

For your own compliance, keep one boundary explicit. FinCEN is not your tax preparer, and institution approval does not replace your filing analysis. Deadline treatment shows why filer category matters: Notice FIN-2024-NTC7, issued November 20, 2024, extended the FBAR filing date to April 15, 2026 for certain U.S. individuals with signature authority but no financial interest, and some previously extended signature-authority deadlines were further extended to April 15, 2027. For other individuals with an FBAR obligation, the due date remains April 15, 2026.

Use this quick check before assuming you are covered:

- Decide whether your question is about institution review or your own filing duty.

- If it is your duty, map your facts to the Report of Foreign Bank and Financial Accounts and FinCEN Report 114 filing requirements.

- If you have signature authority without financial interest, confirm your exact deadline category before filing.

If ownership, control, and money movement do not fit one consistent narrative, pause and get professional help before filing. Related: Portugal's NHR Regime vs. Spain's Beckham Law: A 2025 Tax Analysis for High-Earning US Expats.

How FinCEN gets legal authority#

FinCEN's authority is statutory and delegated. The chain starts with the Currency and Foreign Transactions Reporting Act of 1970 and related amendments commonly called the Bank Secrecy Act (BSA). It then runs through 31 U.S.C. 310, which establishes FinCEN as a Treasury bureau, and Treasury Order 180-01, which delegates implementation, administration, and enforcement of BSA compliance.

This legal chain has direct day-to-day effects. Under BSA authority, Treasury can impose reporting and related requirements on financial institutions and other businesses, including reporting certain cash transactions exceeding $10,000. That is why institutions ask for records that may feel repetitive.

When a bank or platform asks for the same ownership proof more than once, treat that as compliance work tied to this authority chain, not as a personal accusation. Clear records usually resolve these loops faster than arguing that review should not be happening.

Governance is layered. At a practical level, FinCEN executes responsibilities that Treasury delegates under this framework. You do not need every internal boundary to make sound filing decisions, but you do need to know which authority controls the rule you are applying.

One limit matters for freelancers and FinTech users: this structure does not mean every person files directly with FinCEN every year. Personal filing duties still depend on your facts, especially ownership and signature authority.

Deadline treatment is a practical example. Certain U.S. individuals with signature authority but no financial interest were further extended to April 15, 2027 because proposed rulemaking was not yet finalized. For other individuals with an FBAR obligation, the due date remains April 15, 2026.

Use this check before you act:

- Identify the controlling authority for your question: BSA, 31 U.S.C. 310, or Treasury Order 180-01.

- Separate institution compliance requests from your personal filing duty.

- If you have signature authority without financial interest, verify your deadline category before filing.

Is FinCEN a regulator, an intelligence unit, or both#

For practical compliance decisions, treat FinCEN as both. It functions as a regulator under BSA rules and as an intelligence-focused hub that receives, analyzes, and disseminates reported financial data for law-enforcement use.

On the regulatory side, FinCEN exercises its functions primarily under the Currency and Foreign Transactions Reporting Act of 1970 and later amendments commonly referred to as the BSA. That includes amendments such as Title III of the USA PATRIOT Act of 2001. The Secretary of the Treasury delegated authority to the Director of FinCEN to implement, administer, and enforce BSA compliance.

On the intelligence side, FinCEN receives and maintains reported transaction data, then analyzes and disseminates that information for law-enforcement purposes. In practice, reported data is collected, analyzed, and disseminated to support government and industry partners.

For freelancers and platform users, the practical takeaway is straightforward. As activity crosses institutions and countries, keep your records consistent so required information can be provided clearly when requested.

Cross-border activity can add coordination demands because FinCEN also builds cooperation with counterpart organizations in other countries and international bodies. If money moves across multiple jurisdictions or institutions, assume consistent records will matter in more than one context.

Use this rule before changing payout routes or filing:

- If activity touches multiple countries or institutions, plan for stronger documentation.

- Keep one dated evidence set covering key account, entity, and transaction details.

- Reconcile those details across your account and filing records before submitting updates.

Treating regulatory checks and intelligence functions as unrelated tracks creates avoidable inconsistencies. Keep records aligned to both realities from the start.

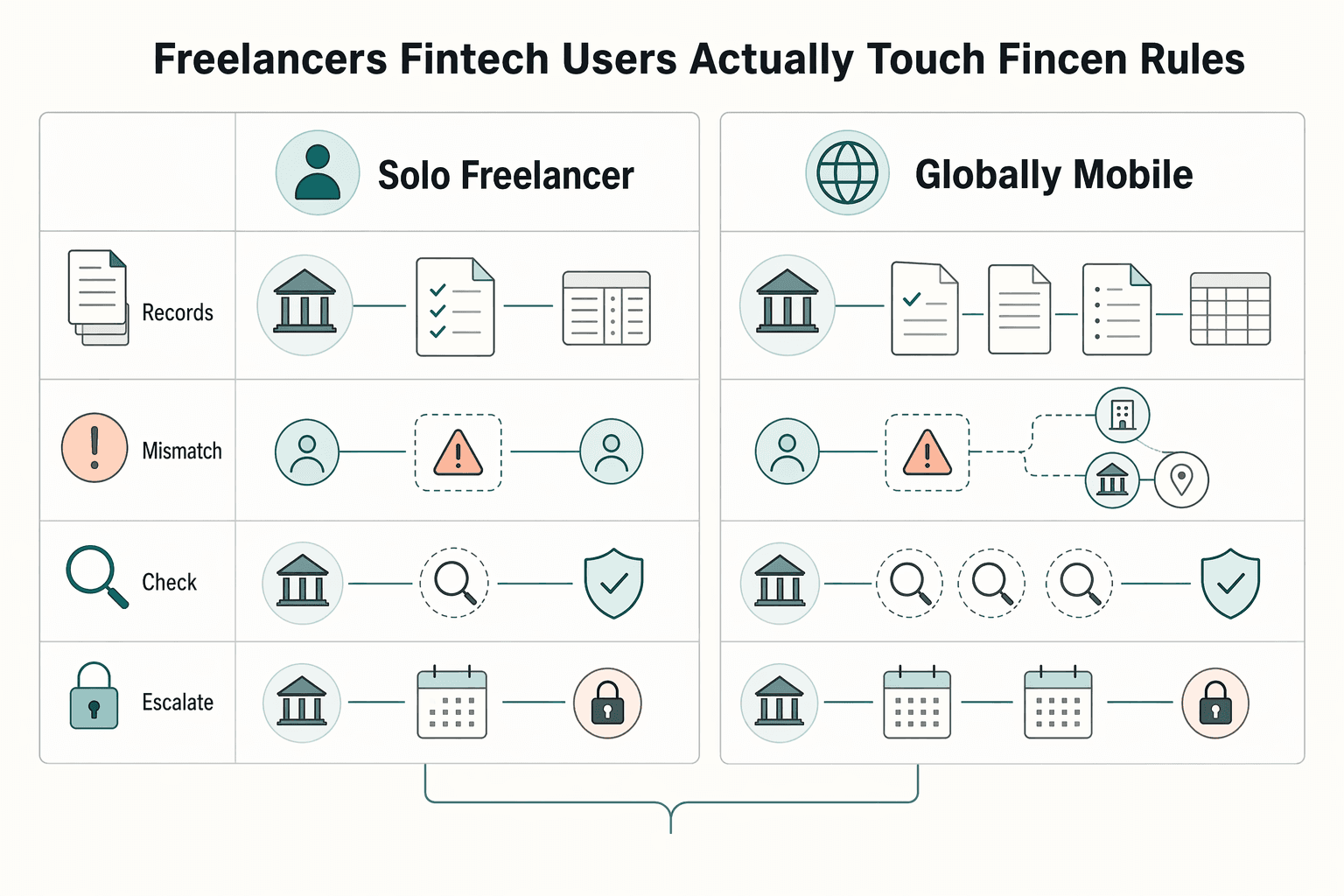

Where freelancers and FinTech users actually touch FinCEN rules#

Many freelancers and FinTech users encounter FinCEN-related rules through banks and payment platforms, rather than by dealing with FinCEN directly. FinCEN holds BSA enforcement and compliance authority, while institutions apply those requirements through their own compliance processes, which may include onboarding checks, transaction monitoring, payout holds, and account reviews. The same payment can face different review pressure depending on your account structure.

| Profile | Typical touchpoints | Review exposure | What to keep ready |

|---|---|---|---|

| Solo freelancer with one domestic account | Signup identity checks, occasional transaction questions, standard payout timing | Can be lower when activity patterns stay consistent | Government ID, matching legal name across invoices and account profile, clear payment-purpose notes |

| Globally mobile consultant using multi-country rails | Repeated ownership checks, cross-border transfer reviews, more frequent holds during pattern shifts | Can be higher when more institutions must reconcile the same activity | Account ownership records, consistent entity and beneficiary details across platforms, dated rationale for each cross-border flow |

A practical contrast helps here. Two people can receive the same project payment amount, but the one using multiple rails, mixed entities, and changing payout destinations may face more reconciliation questions. The difference is not the invoice by itself. The difference is how much effort an institution needs to confirm ownership and purpose.

A hold or restriction is not automatic proof of money laundering. It can mean the institution cannot quickly reconcile purpose, ownership, or flow pattern under BSA obligations.

When funds are delayed, treat it as a records-quality signal:

- Pause route changes until you can explain the transaction path clearly.

- Reconcile names, account owners, and payout destinations so the same legal identity appears everywhere.

- For foreign accounts, use periodic statements to prepare each account's maximum value for FBAR reporting.

- If a calculated maximum value is negative, enter zero for that field.

A short post-delay note can help prevent repeat friction. Record what was requested, what document resolved it, and where that document now lives in your evidence folder. You are building repeatability for the next review cycle.

This approach can reduce avoidable escalation. FinCEN can impose civil money penalties for BSA violations, so unclear flows may be stopped or reviewed early.

FinCEN reporting terms you must not mix up#

Common filing mistakes start with mixed labels. FBAR and Form 8938 are different obligations, and combining them in your head leads to wrong submissions.

| Filing item | Who handles it | Where it goes | Common mix-up |

|---|---|---|---|

| FinCEN Form 114 (FBAR) | Taxpayer (if required) | Filed directly with FinCEN | Assuming it is filed with the IRS as part of a tax return |

| Form 8938 | Taxpayer or certain specified domestic entities | Attached to the tax return | Assuming it replaces FBAR |

Naming is the main failure mode here. FinCEN Form 114 is the FBAR filing, and Form 8938 is a separate IRS form. These obligations can coexist, and filing Form 8938 does not replace or otherwise affect a FinCEN Form 114 obligation.

Keep your records separated by filing path. One folder for FinCEN Form 114 support and one folder for tax-return attachments. Separation reduces last-minute mix-ups when deadlines cluster.

Use one pre-filing check for each form: who files it, what triggers it, where it is submitted, and where confirmation is stored. Keep statements, ownership records, and filing confirmations together.

Red flag rule: if your reasoning is "I filed Form 8938, so I am covered," stop and verify whether a separate FinCEN Form 114 filing is required.

A 10-minute decision check for what to do now#

When facts are messy, sequence beats speed. Map accounts first, classify forms second, then assign one action status.

| Status | When to choose it |

|---|---|

| No action now | You can explain why FinCEN Form 114, Form 8938, and other return checks are not triggered this year |

| Gather evidence | You are near a threshold, ownership is mixed, or records conflict |

| Escalate | Control, ownership, or multi-jurisdiction structure is unclear |

- List every account, wallet, and platform by country and legal owner. Note who controls transfers and whether use is personal, business, or mixed. If control and legal identity do not match, flag it.

- Classify duties by form and authority. FinCEN Form 114 (FBAR) and Form 8938 are separate. Form 8938 is attached to your income tax return, and filing Form 8938 does not remove a FinCEN Form 114 duty when FBAR is otherwise required. Keep other return-attachment checks separate.

- Run threshold and exception checks, then set status. Form 8938 thresholds vary by filer context, with higher thresholds for some filers, including some joint return filers and taxpayers residing abroad. A commonly cited trigger is aggregate specified foreign financial assets above $50,000 for certain taxpayers. For specified domestic entities, instructions include a $50,000 last-day test and a $75,000 any-time test. Form 8938 is not required if no income tax return is required for that year, and some accounts maintained by a U.S. payer are excluded.

Do the three steps in one sitting when possible. A split process across several days can create version drift where account lists, form notes, and thresholds are no longer synced. A single pass gives you one dated snapshot you can defend.

After those steps, choose one status from the table above and date-stamp it.

If you cannot explain account ownership and flow purpose clearly, stop optimizing and document before your next transfer.

Build an evidence pack before problems appear#

Build your evidence pack before review pressure appears. Clear records can lower friction during reviews tied to filing obligations.

Start with a core set of artifacts in one dated folder per review period: account statements, platform transaction exports, invoice trail, and identity records. In the BSA context, institutions file SARs and other reports, and SAR materials describe collaboration among financial institutions, law enforcement, and regulators; clear owner, purpose, and timeline details can make review easier.

Keep the same sequence every time:

- Source records first. Pull raw statements and raw platform exports for the exact period. Keep files that show account holder name, account number, transaction ID, timestamps, and payout status when available.

- Reconciliation second. Match each transfer to an invoice, contract milestone, or payment note. If funds moved across two platforms, add one line linking both transaction IDs so the path is traceable end to end.

- Narrative memo third. Write a short, factual, date-stamped note with who paid, who received, what was delivered, and why that route was used. You are not filing a SAR yourself, but this structure can make review faster.

A maintenance habit makes this usable under pressure. At the end of each month, add only new records, keep prior files unchanged, and append one short update note for anything that changed in ownership, account control, or payout destination. This can preserve continuity and reduce rework before deadlines.

Add technical evidence when available. If your tools provide immutable logs, keep them in the same period folder. If they do not, keep unedited exports and payout status history with original timestamps.

Watch one failure mode: inconsistent account labels across institutions. Different naming across invoice, receiving account, and platform profile may trigger extra document requests.

Use one checkpoint before your next transfer: can you trace one payment from invoice to final settlement in under three minutes, with matching names and dates? If not, pause route changes and fix the evidence pack first.

Cross-border edge cases that should trigger professional help#

Escalate before filing when form boundaries or filing obligations are unclear. The largest avoidable errors are usually path and threshold mistakes, not bad intent.

| Trigger | Section detail | Why it matters |

|---|---|---|

| Residency and account complexity | Your filing context changed during the year, for example joint filing status or living abroad | You are no longer sure which thresholds apply |

| Form boundary confusion | Form 8938 is attached to your annual income tax return, while FBAR (FinCEN Form 114) is filed separately with FinCEN | One does not replace the other |

| Threshold uncertainty | Form 8938 thresholds vary by filer context, including higher thresholds for joint filers and taxpayers residing abroad | Each form needs its own check |

| Entity structure complexity | Accounts are held through a domestic corporation, partnership, or trust | Confirm whether Form 8938 rules for specified domestic entities apply |

If any of these triggers apply, get help before you file.

Two patterns deserve early escalation. First, you cannot clearly determine whether you need Form 8938, FBAR, or both. Second, you cannot confidently match each account to the correct threshold context. Both patterns are manageable, but they are poor candidates for rushed self-filing.

Pause self-filing and get qualified tax or compliance advice if you cannot map each account to the correct form and threshold.

Common mistakes that create avoidable compliance risk#

Most avoidable risk here comes from mixed filing boundaries and weak records, not from intent.

Mistake one is treating FATCA, Form 8938, and FinCEN Form 114 (FBAR) as interchangeable tasks. Keep the lines clear: Form 8938 is attached to your annual income tax return, and FBAR is filed separately with FinCEN, not with the IRS. Filing one does not replace the other. If you do not have to file an income tax return for the year, you do not need to file Form 8938. Also avoid assuming a universal threshold. Even the commonly cited $50,000 figure is only an example for certain taxpayers.

Mistake two is waiting for friction before organizing documentation. A hold or review request is a poor time to reconcile records.

Use this checkpoint before quarter-end:

- For each account, record legal owner, account country, and whether it is personal or business.

- For each foreign account, document the maximum account value for the calendar year using statements that fairly reflect the peak value.

- If a Treasury exchange rate is unavailable, use another verifiable rate and record the source.

- Round reported U.S. dollar values consistently, for example

$15,265.25becomes$15,266.

Mistake three is inconsistent naming across contracts, invoices, and payout accounts without a clear bridge. In practice, one useful fix is one canonical legal-name setup plus a short alias note when display names differ.

Mistake four is carrying prior-year assumptions into a changed year without re-checking facts. New account ownership, a location shift, or a platform change may change your filing analysis even when your revenue pattern looks similar. Re-run your decision check on current facts instead of copying last year's conclusions.

Treat policy friction as a review trigger, not a legal exemption. If your facts trigger U.S. reporting duties, complete the required filing path with consistent records.

How to verify rules safely when sources conflict#

When guidance appears to conflict, prioritize official Treasury and FinCEN materials and treat summaries as secondary. If a claim is not supported by current official guidance, treat it as unverified for filing decisions.

Check authenticity and recency before interpretation. Confirm the page is official (.gov or .mil) and secure (https://), then confirm you are reading the current notice or FAQ context. FinCEN is explicit that guidance can change: "FinCEN will issue additional FAQs and guidance as needed."

Use one repeatable checklist for each disputed requirement:

- Term definition: what is being reported, such as maximum account value for the calendar year.

- Filing owner: which filer category is responsible.

- Triggering condition: which facts activate the requirement, including subset limits.

- Responsible authority: which agency and official document control the rule.

- Effective timing: which notice date or instruction version applies.

A useful conflict test is scope before substance. Confirm whether two statements apply to the same filer category, same time period, and same form duty before deciding they conflict. Some apparent contradictions disappear once scope is aligned.

Apply filer-category checks to deadline claims. For FBAR, April 15, 2027 applies to a defined subset, while other individuals with an FBAR obligation keep an April 15, 2026 due date.

Use the same discipline for FinCEN Form 114 calculations. Use statements that fairly reflect the year's maximum account value. Use the Treasury Financial Management Service rate for conversion on the last day of the calendar year, round up to the next whole U.S. dollar, and enter 0 if the computed value is negative.

Keep a dated decision log for each conflict: the question, official pages reviewed, filer category chosen, and filing action taken. If two official items still conflict after category checks, pause and escalate rather than picking the easier interpretation.

Conclusion#

If asking what FinCEN is does not change your decisions or documentation, it is just trivia. The useful outcome is practical: show whether FBAR filing is required, how each FinCEN Report 114 value was calculated, and when to escalate before filing.

This week, move from awareness to proof.

- Run a decision check. List each foreign account and its highest value during the calendar year. If one account maximum or the aggregate maximum exceeds $10,000, treat FBAR filing as required. If values are uncertain, flag that now.

- Build an evidence pack for every reported value. Use a reasonable approximation of the highest yearly value, and rely on periodic statements when they fairly reflect that maximum. Record amounts in U.S. dollars, rounded up to the next whole dollar. For non-U.S. currency accounts, use the Treasury Financial Management Service year-end rate. If that rate is unavailable, use another verifiable rate and record its source. If a calculation is negative, enter 0 in item 15.

- Close your biggest documentation gap. Finish one blocker this week so your filing decision is supportable. For certain filers with fewer than 25 accounts who cannot determine whether aggregate maximums exceeded the threshold, complete the relevant account sections and check item 15a (

amount unknown).

Set your deadline rule in writing. For other individuals with an FBAR obligation, the due date remains April 15, 2026. The April 15, 2027 date applies only to certain signature-authority filers whose due date was already extended, for 2025 calendar-year reporting.

A practical final check is to draft a one-page filing rationale for your own records. State your filer category, whether you are filing FBAR, and the evidence used for each call. Keep that page with your documents so future-you, your advisor, or a reviewer can follow the logic without rebuilding it from memory.

When documentation duties overlap, choose traceable records over shortcuts. If you cannot explain your value method, conversion source, and due-date basis clearly, pause and get a compliance review before filing.

Frequently Asked Questions

What is **Financial Crimes Enforcement Network (FinCEN)** in one sentence, and why does it matter to freelancers?

FinCEN is a bureau of the U.S. Department of the Treasury that receives FinCEN Form 114 (FBAR) filings. It matters because FBAR filing is separate from your income-tax return process, so you need to route each obligation to the correct authority.

Is FinCEN a regulator, a **Financial Intelligence Unit (FIU)**, or both?

For filing decisions, the practical point is clear: FinCEN is the Treasury bureau that receives FBAR filings. You do not need to resolve agency-label debates to stay compliant, but you do need to match each requirement to the right form and filing channel.

Do I personally file with FinCEN, or is reporting mostly done by banks and platforms through **Suspicious Activity Report (SAR)** processes?

If you have an FBAR obligation, you file FinCEN Form 114 directly with FinCEN, not with the IRS. Evaluate your own filing duty directly instead of assuming another reporting process covers it.

What is the difference between **Foreign Bank Account Report (FBAR)**, **FinCEN Form 114**, **FATCA**, and **Form 8938**?

FBAR is the report, and FinCEN Form 114 is the form used to file it with FinCEN. Form 8938 is separate and attached to your tax return. Filing Form 8938 does not replace an FBAR obligation, so test each requirement separately and file one or both as needed.

How do I quickly decide whether I need action now or just better records?

Use a short checklist: confirm whether you are a specified person, confirm whether you must file an income-tax return, then test Form 8938 thresholds for your filer category and test FBAR separately. For certain U.S.-based filer categories, Form 8938 examples include $50,000/$75,000 and $100,000/$150,000 thresholds. If no income-tax return is required, Form 8938 is not required even if asset values are above threshold amounts.

When should I stop self-managing and hire a cross-border tax/compliance professional?

Escalate when you cannot clearly determine whether Form 8938, FinCEN Form 114, or both apply. Also escalate when you are unsure about specified-person status, filing thresholds, or where each form must be filed. If you are uncertain, consider a pre-filing review before you submit.

Watch

What Is FinCEN? Guide for Freelancers

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Portugal NHR vs Spain Beckham Law for High-Earning US Expats in 2026

Start with documentation, not tax projections. In the portugal nhr vs spain beckham law decision, the safer first move is to choose the path you can prove from end to end before you optimize for headline outcomes.

RRSP vs TFSA for Canadian Freelancers With Uneven Income

Start with cash stability, then optimize taxes. Freelance income can fluctuate year to year, profits are often reinvested, and many self-employed people do not receive employer pension contributions. That makes this a cash decision first and a tax decision second.