Quick Answer

Use the treaty sequence first: center of vital interests tax treaty analysis matters only after domestic-law overlap is plausible in both countries. Under Article 4(2), test permanent home before vital interests, then move to habitual abode, nationality, and mutual agreement only when needed. End the analysis when one test resolves residence, and keep a dated memo that shows both-country facts, contradictions, and the reason your conclusion is supportable.

Start Here and Make One Defensible Residency Call#

Start by making one defensible tax residency call based on facts, not on a preferred country outcome. Use the treaty tie-breaker in order, document why each step does or does not resolve residence, and stop at the first clear result.

Treaty logic matters only when dual residency is a real issue. The Center of Vital Interests test can be part of that process, but only after you are plausibly resident in both countries under their domestic rules for the same period.

Confirm you actually have a dual residency problem#

Confirm the issue first, then work in sequence:

- Analyze the U.S. residency claim.

- Analyze the treaty-country residency claim.

- Apply the treaty tie-breaker rules.

That IRS practice flow is useful, but it is not binding law. The order still matters. Article 4(2) assigns exclusive treaty residence only when you actually have a dual-resident fact pattern. For U.S. analysis, that may include the substantial presence test. If either country's domestic-law status is unclear, resolve that before you run tie-breakers.

Apply the treaty test in sequence, not by instinct#

Treat Article 4(2) as a sequence of tests, not a menu. Do not jump straight to Center of Vital Interests because it feels intuitive.

For each step, keep a short memo with:

- facts supporting Country A

- facts supporting Country B

- why this step does or does not resolve residence

Stop at the first clear result. Later tests are fallback tests, not extra arguments you stack onto a conclusion you already reached. Day counting alone does not produce an automatic treaty outcome.

Build a file you can defend later#

Your goal is a position you can explain and defend. In tie-breaker cases, documentation quality, narrative precision, and filing consistency all matter.

Build a dated, plain-language file with:

- records supporting domestic-law residency analysis in each country

- records supporting each treaty step you actually used

- a short written explanation that reconciles conflicting facts directly

Ask yourself: could a third party reproduce your Article 4(2) conclusion from your file without filling in missing facts?

Know when to stop and when to escalate#

Escalate when domestic-law residency is unclear, when treaty steps remain genuinely mixed, or when downstream exposure is meaningful. Treaty residence does not rewrite domestic law, so filing obligations and exposure can still require separate review.

When you escalate, hand over a clean packet with the treaty text, your step-by-step memo, dated records, and any unresolved contradictions.

Related reading: A Deep Dive into the 'Dividend' Article of the US-Germany Tax Treaty for LLC Owners.

Define Center of Vital Interests Before You Start#

Treat Center of Vital Interests as a treaty-text question first, not as shorthand. Start with the signed bilateral treaty you are actually filing under.

Use model materials as orientation, not as controlling authority. The U.S. Model Income Tax Convention of September 20, 1996 says it is drawn from multiple sources, and its Technical Explanation says it references OECD commentaries to note similarities and differences. It also describes the model as an ambulatory document that can be updated over time.

Before you make a residency call, run this quick check:

- pull your actual treaty text and open the residence article

- compare that wording with the model language you are using as a guide

- record any wording differences in your memo before you finalize your position

A common failure mode is treating model language or blog shorthand as if it were your treaty text. Treasury's model materials explicitly warn that the model is not complete for every treaty context, and negotiated treaty text can differ in numerous respects.

Confirm Dual Residency Risk Before Running Tie-Breakers#

Do not run treaty tie-breaker analysis unless dual residency is genuinely plausible under both countries' domestic law. If overlap is not plausible, there is no treaty tie-breaker issue to solve.

| Record type | Details |

|---|---|

| Presence dates | travel records |

| Address and lease | move-in and move-out dates |

| Tax status | tax registrations, residency notices, and filed return positions |

| Residency-certificate steps | including a U.S. Form 8802 request when relevant |

Start with a simple gate check:

- confirm whether U.S. domestic residency rules are in play for your facts

- confirm the other country's domestic residency rule for your facts

- if either status is unclear, pause and validate domestic-law status before treaty analysis

Once dual residency looks plausible, build a two-column country file and log facts by date, not by memory. For each country, track:

- presence dates and travel records

- address, lease, and move-in and move-out dates

- tax registrations, residency notices, and filed return positions

- residency-certificate steps, including a U.S. Form 8802 request when relevant

Treat Form 8802 as documentation, not as a tie-breaker outcome. It is part of a U.S. treaty-context residency certification process, but it does not decide treaty residence on its own.

Avoid forcing treaty tie-breaker clauses before you establish domestic-law overlap. Treaty frameworks are meant to reduce double taxation and prevent avoidance or evasion. Your file should show a consistent, dated domestic-law basis before you move to the residence article.

We covered this in detail in What is the 'Limitation on Benefits' (LOB) Clause in a US Tax Treaty?.

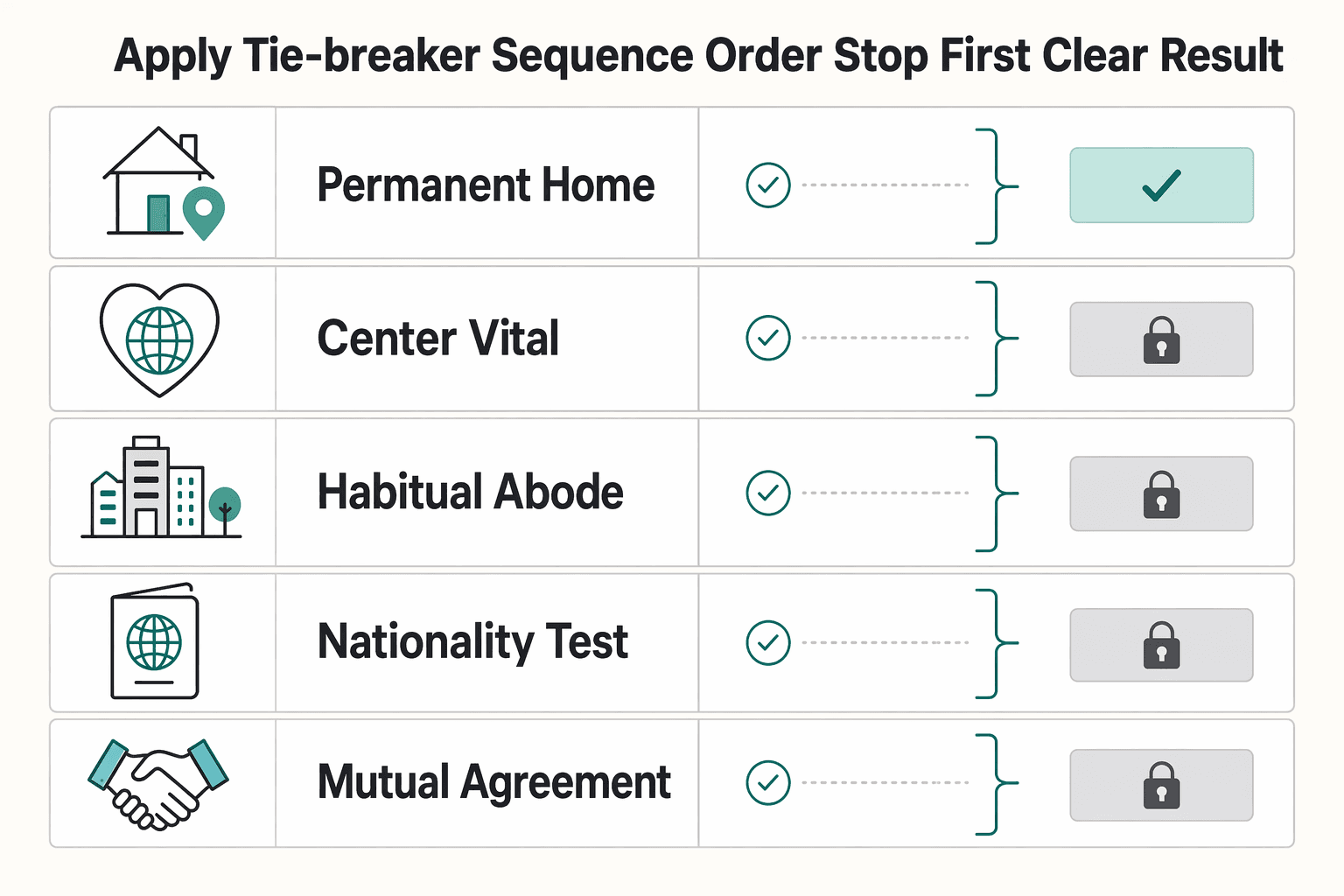

Apply the Tie-Breaker Sequence in Order and Stop at First Clear Result#

Use Article 4(2) as a sequence, not a menu, when you are liable to tax in both treaty states. Apply each test in order, and stop when a step clearly resolves residence. Later tests are fallback steps only.

Do not jump straight to Center of Vital Interests if the permanent-home test already decides the outcome. If only one state has a permanent home available to you, residence is deemed there for tie-breaker purposes.

| Article 4(2) step | What you test | Move forward only if |

|---|---|---|

| Permanent home test | Whether only one state has a permanent home available to you | You have a permanent home in both states (then test Center of Vital Interests), or in neither (then test habitual abode) |

| Center of Vital Interests | Which state has closer personal and economic relations | Closer relations cannot be determined |

| Habitual abode test | Where you have a habitual abode | You have a habitual abode in both states, or in neither |

| Nationality test | Whether nationality resolves the tie | You are a national of both states, or of neither |

| Mutual agreement procedure | Competent authorities settle the question | Earlier tests did not resolve residence |

Document each step the same way#

For every step, record:

- facts that support Country A

- facts that support Country B

- why this step did or did not decide the issue

This keeps your file reviewable and helps keep the sequence consistent. If a step is inconclusive, say exactly why before you move on.

Apply vital interests only when required#

Use the Center of Vital Interests step only after the permanent-home step does not resolve the case because permanent homes exist in both states. At that point, assess personal and economic relations as a whole, including factors like family and social relations, occupations, activities, and place of business. Avoid single-factor conclusions when facts are mixed.

Treat later steps as escalation#

Move forward only when the current step does not produce a clear result:

- if permanent home in only one state decides it, stop

- if permanent homes are in both states, test closer personal and economic relations

- if those closer relations cannot be determined, or if there is no permanent home in either state, test habitual abode

- if habitual abode is in both states or neither, test nationality

- if nationality still does not resolve it, competent authorities settle by mutual agreement under Article 25

Administrative guidance can reflect this outcome logic in practice. For example, CRA guidance notes that treaty tie-breaker rules may deem someone not resident in Canada in some cases. The main point is procedural discipline: stop at the first clear result, and document why.

Related: Tbilisi, Georgia: The Ultimate Digital Nomad Guide (2025).

Build an Evidence Pack That Can Survive Scrutiny#

Build the file so a third party can reproduce what you filed, not just read your conclusion. Keep it date-stamped and explicit about conflicting records.

Map records to the filing checkpoints you are weighing#

Use consistent buckets, and tag every document with the tax year and date range so the analysis is easy to review.

| Filing checkpoint | Keep evidence | Why it helps |

|---|---|---|

| Form 8938 filing status | confirmation that an income tax return is required for the year, and whether you are a specified person | Establishes whether Form 8938 may be required |

| Form 8938 timing | annual return filing calendar and extension records | Form 8938 is attached to the annual return and filed by that return due date, including extensions |

| Separate FBAR track | FinCEN Form 114 workpapers and filing records | Form 8938 does not replace the separate FBAR requirement |

| Threshold review | year-end and in-year asset value workpapers, with filing-status context | Thresholds are not one-size-fits-all, and some cases have higher thresholds |

| Form 8938 data fields | account inventory showing number of deposit accounts, maximum value, closed accounts, and assets acquired or sold | Matches key checklist fields requested on Form 8938 |

Unsupported assertions are weak. If records conflict, show both sides and explain how you resolved the difference.

Add a short memo that reconciles mixed facts. Write a brief rationale that lists key facts, then explains why your filing position is supportable or where uncertainty remains. Do not hide contradictions.

Run a reproduction check before you finalize. Before you close the file, verify that a reviewer can follow your filing logic:

- each material fact links to a source document and date

- the reason for your filing decision is explicit

- conflicting facts are explained, not buried

Flag U.S. filing consistency risk early. If U.S. filings are in scope, run a consistency pass across your return, Form 8938, and FBAR.

- Form 8938 is used to report specified foreign financial assets and, when required, is attached to the annual return and filed by that return due date, including extensions.

- Filing Form 8938 does not remove the separate requirement to file FinCEN Form 114, FBAR.

- If no income tax return is required for the year, Form 8938 is not required.

- Thresholds are not one-size-fits-all. Higher thresholds can apply in some cases, including some joint filers or taxpayers residing abroad.

- For specified domestic entities, for tax years beginning after December 31, 2015, triggers include $50,000 on the last day of the tax year or $75,000 at any time during the tax year.

- Form 8938 asks for items like number of foreign deposit accounts, maximum value, whether accounts were closed, and whether foreign assets were acquired or sold during the year.

Safe default: your evidence file, written rationale, and U.S. reporting timeline should tell the same story.

Need the full breakdown? Read Understanding the Independent Personal Services Article in Tax Treaties.

For a repeatable workflow, see the Tax Residency Tracker.

Resolve Split-Tie Cases With Explicit Decision Rules#

Treat split-tie cases as high-friction. If your personal ties and economic ties point to different states, do not force certainty at the Center of Vital Interests step.

That step looks at close personal and economic ties together, and tax authorities can decide these cases on a fact-specific basis. Avoid winner-take-all reasoning based on one strong fact.

Use a clear split-tie rule. If personal ties and economic ties point in opposite directions, and neither side is clearly stronger on the facts as a whole, mark Center of Vital Interests as unresolved. Then prepare for the next tie-breaker step in the treaty you are applying.

That does not mean every split automatically fails this step. Some cases still resolve here when one side is materially stronger and better documented across the full record.

Write the conclusion in facts-as-a-whole language. Write your memo as a weighed judgment, not as an absolute claim. For example: "On the facts as a whole, personal ties are stronger in Country A, while economic ties are materially connected to Country B. Neither side clearly outweighs the other, so the analysis does not reliably stop at Center of Vital Interests."

This keeps your position aligned with DTA tie-breaker logic and reduces the risk of overclaiming from a single factor like family location, income activity, or property records.

Pre-check fallback steps early. If the split looks genuine, pre-check fallback steps before you need them. Review whether later treaty tie-breaker criteria are likely to be clearer than your tie analysis. If they are also mixed, check your treaty text for what comes before Mutual Agreement Procedure (MAP).

Treaty mechanics are not uniform. MAP is Article 25 in the U.S. Model Convention and Article 26 in the U.S.-France treaty, so confirm numbering and sequence in the treaty you are actually applying.

If U.S. filings are in scope, keep your treaty position and reporting aligned. In one litigated dual-resident case, treaty benefits were disclosed on Form 8833. Amended returns were filed on Form 1040-NR for 2012 and 2013, while FBAR penalty exposure still became central. Practitioners have also debated how broadly that ruling should be relied on.

Handle Country Variation Without Guessing#

Start with your signed bilateral treaty, not model language. Model conventions and commentary are useful working references, but the negotiated treaty text is what controls your position.

| Order | Review |

|---|---|

| 1 | Read the residence article in your signed bilateral treaty, plus any protocol or technical explanation for that treaty |

| 2 | Compare that text with OECD model materials and commentary to identify where your treaty aligns or diverges |

| 3 | Where available, review local guidance for additional context in your jurisdiction |

| 4 | If uncertainty remains in edge cases, get adviser confirmation before filing |

Start with the document that governs#

Model materials are designed to evolve. The OECD Council adopted a 2025 update to the OECD Model Tax Convention on 18 November 2025, and the U.S. Technical Explanation describes model texts as negotiation tools that help identify policy differences. It also states that the final agreed treaty can differ from the model in numerous respects.

Use that as your baseline. Read the treaty wording first, then use model commentary to check similarities and differences.

Use a practical reading order#

Use the same sequence in practice to reduce guesswork:

- Read the residence article in your signed bilateral treaty, plus any protocol or technical explanation for that treaty.

- Compare that text with OECD model materials and commentary to identify where your treaty aligns or diverges.

- Where available, review local guidance for additional context in your jurisdiction.

- If uncertainty remains in edge cases, get adviser confirmation before filing.

This is a practical sequence, not a legally required one.

Treat differences as controlling#

If treaty wording differs from model wording, treat the treaty text as controlling and rewrite your rationale around that text. Do not assume model phrasing carries over automatically.

A useful check is simple: can you point to the exact treaty sentence you relied on, rather than a model summary or informal commentary?

What to keep in your file#

Keep a short comparison pack with:

- the signed bilateral treaty text you relied on

- any protocol or technical explanation you used

- a marked comparison showing where treaty wording aligns with or departs from model text

- a brief note on any uncertainty that still needs confirmation

This pairs well with our guide on A Deep Dive into the 'Services PE' Clause in Modern Tax Treaties.

Avoid the Mistakes That Trigger Residency Disputes#

Residency disputes get harder when your treaty position, evidence trail, and reporting forms do not match.

Do not let day count become your whole answer. Day counts can be part of your records, but the IRS excerpts here do not establish treaty tie-breaker ordering. If you rely on treaty language (for example, Article 4(2) in your signed treaty), document your reasoning step by step against your treaty text instead of stopping at travel totals.

Do not overstate treaty conclusions without evidence on both sides. Keep dated support for the facts you rely on, including facts that cut against your preferred outcome. Statements without documentation are hard to defend later. Keep your wording anchored to your treaty text and your documented facts.

Keep treaty positions aligned with U.S. reporting forms#

For U.S. filers, make sure your treaty position and foreign-asset or account reporting tell the same story.

| Item | What to check before filing |

|---|---|

| FBAR, FinCEN Form 114 | File if aggregate foreign financial accounts exceeded $10,000 at any time in the calendar year; due April 15 with automatic extension to October 15. Whether an account produced taxable income does not change FBAR classification. |

| Form 8938 | Report specified foreign financial assets by attaching the form to your annual return and filing by that return due date, including extensions. IRS materials note a $50,000 trigger point for certain U.S. taxpayers, and instructions state $75,000 at any time during the tax year for specified domestic entities. If you do not have to file an income tax return for the year, you do not need to file Form 8938 for that year. |

Also keep the non-substitution rule clear. Filing Form 8938 does not remove an FBAR filing duty when FBAR rules apply.

Preserve your own dated evidence trail. Advisor summaries are useful, but your file should still contain your own dated facts, documents, and reasoning. If you cannot reconstruct your conclusion later from your own records, the file is too thin. Your treaty claim, tax return position, and any IRS or FinCEN reporting should stay internally consistent.

Add U.S. Overlay Checks When Relevant#

If U.S. facts are in your file, keep two separate conclusions: U.S. domestic-law status and treaty tie-breaker status. Then run one final consistency check so your memo and forms tell the same story.

Separate U.S. status from the treaty result#

Start with U.S. domestic-law status, then document treaty tie-breaker status separately. Do not merge them into one conclusion.

That separation keeps your file defensible. A treaty tie-breaker outcome is not the same as saying domestic-law status never applied. If your facts resemble a treaty tie-breaker pattern, use it as a structure check only, not as a guaranteed precedent.

Do not treat treaty residence as a filing shortcut#

A treaty residence outcome does not automatically resolve every U.S. filing obligation.

For Form 8938, keep the IRS checkpoints separate from treaty analysis. Attach it to your annual return and file by that return due date, including extensions. Also remember that you do not file Form 8938 for a year when you are not required to file an income tax return. Keep the non-substitution rule explicit too: filing Form 8938 does not replace FinCEN Form 114 (FBAR).

Run one consistency check across the U.S. file#

Before filing, verify alignment across:

- your domestic-law residence conclusion

- your treaty tie-breaker conclusion and supporting facts

- Form 8938 reporting, where applicable

- FBAR or FinCEN account reporting, where applicable

Use the forms as a verification tool, not just a filing task. For example, Form 8938 asks whether foreign assets were acquired or sold during the tax year. That helps you confirm that your timeline and reporting are internally consistent. If you use a U.S. entity to hold foreign assets, separately review Form 8938 instructions for certain specified domestic entities, including the cited $75,000 at-any-time threshold for some entities.

Know When to Escalate and What to Bring to a Pro#

Escalate when your documented facts still point in different directions, or when U.S. residency certification is part of your filing path. In those cases, expert review is usually more practical than forcing a solo conclusion.

| Packet item | Details |

|---|---|

| Treaty text | the treaty text you are relying on, with your notes |

| Step-by-step memo | including where facts remain uncertain |

| Evidence index | with dates, document names, and what each item supports |

| Contradiction log | for facts that cut the other way |

| U.S. certification materials | Form 8802 draft or copy, payment records, signer details, and IRS correspondence |

If U.S. certification is in scope, treat it as its own workstream. The IRS handles U.S. residency certification through Form 8802, and that process includes signer-eligibility rules, processing-time checkpoints, and user fee or payment-validation checks, including partial-payment handling. Even with a solid analysis, certification can stall if paperwork is incomplete or signer authority is unclear.

Bring the packet in a form your adviser can review quickly:

- the treaty text you are relying on, with your notes

- your step-by-step memo, including where facts remain uncertain

- an evidence index with dates, document names, and what each item supports

- a short contradiction log for facts that cut the other way

- if U.S. certification is relevant, Form 8802 draft or copy, payment records, signer details, and IRS correspondence

Ask for a written opinion that follows your checklist structure so future-year updates are faster. For support channels, do not rely on 800-829-VITA (8482) for this issue. Publication 5683 labels that tax-law hotline for volunteers only.

For a step-by-step walkthrough, see What is a 'Habitual Abode' in a Tax Treaty?.

Use Gruv Records to Reduce Documentation Friction#

Use records to reduce review friction, not to make the legal decision for you. If you include records in your file, keep dates and labels consistent across your memo, summary, and source documents.

Keep chronology consistent. Start with timing. Use records to anchor dates and catch mismatches early. If a source record conflicts with your draft timeline, fix the timeline before you circulate the packet.

Build a review-friendly summary. Create a short evidence summary that maps each statement back to a source record so reviewers can verify it quickly:

- date of activity

- short description of what happened

- document name or record ID

- why the item is in the file

Minimize sensitive data in shared summaries. Keep summaries lean and retain full source records for verification when needed. Before uploading sensitive information, confirm the destination is official and secure.

For U.S. government sites, a .gov domain indicates an official government organization, and https:// indicates a secure connection. Share sensitive information only on official, secure websites.

Keep evidence and conclusions separate. A clean record set improves clarity and verification, but records are still inputs. Keep your legal conclusion as a separate step in your process.

Make the Call, Document It, and Recheck Each Year#

Your goal is a documented, reproducible residency position, not a one-line conclusion. Confirm your domestic-law status first, and if you are resident in both treaty countries for the same tax year, apply Article 4(2) in your bilateral treaty to assign exclusive treaty residence.

Build a file someone else can follow#

A defensible file should show your path from domestic-law status to any dual-residency analysis, then to one treaty residence under Article 4(2) when that framework applies.

At minimum, keep:

- the treaty text you relied on

- a dated memo with your year-specific conclusion

- a short note for each test you applied, with the facts you used and what that test did or did not resolve

- contradictory facts stated plainly, not buried

If someone reviews the file later and cannot reproduce your logic, tighten it before you file on that position.

Run the sequence in order, and escalate mixed facts#

Do not skip steps because one factor feels decisive. Article 4(2) is a series of tie-breaker tests used to determine one exclusive residence for treaty purposes, so apply the sequence as written in your treaty text when you are a dual resident taxpayer.

When facts point in different directions, say that directly in your memo and continue through the treaty framework. If multiple tests remain unclear, escalate for specialist review instead of forcing certainty.

Match the label to tax consequences#

Treaty-residency conclusions can change tax scope, so confirm domestic status first. In U.S. tax treatment, resident aliens are generally taxed on worldwide income, while nonresident aliens are generally taxed only on U.S.-source income.

If you are resident in both countries for the same tax year, Article 4(2) is used to assign one exclusive treaty residence. Keep your filing position aligned with that outcome.

Recheck when your facts change#

Recheck your position before filing whenever material facts change. Update your memo and evidence map so the reasoning still supports your filing position.

You might also find this useful: What is a 'Permanent Home' in the Context of a Tax Treaty?.

If your facts stay mixed after running the full tie-breaker sequence, contact Gruv to confirm whether our compliance-first records and payout workflows fit your setup.

Frequently Asked Questions

Is `Center of Vital Interests` the same as where I spent the most days?

No. Center of Vital Interests is not a day-count shortcut. Use documented facts and the specific treaty text rather than a single metric.

What comes before and after `Center of Vital Interests` in the treaty tie-breaker order?

This grounding pack does not establish a generic sequence. Confirm the exact order in your signed bilateral treaty and apply that residence article as written. If you want a refresher, see Using DTA Tie-Breaker Clauses to Resolve Dual Tax Residency.

Can family location outweigh where I earn most of my freelance income?

This grounding pack does not support a one-factor rule you can safely reuse across cases. If your facts point in different directions, document both sides and avoid claiming certainty from a single headline fact. When the outcome drives meaningful tax exposure, get specialist review.

What if my ties are split and no clear center can be determined?

Treat it as unresolved and state that plainly in your memo. List the strongest facts on each side and identify what is still missing or contradictory.

Does every country define `Center of Vital Interests` in domestic law?

Check the treaty article and local authority guidance for each jurisdiction involved.

If I claim treaty residency, do U.S. reporting items like `FBAR` or `Form 8938` automatically disappear?

No. Form 8938 is a separate IRS filing for specified foreign financial assets when you exceed the applicable reporting threshold, and it is attached to your annual return by that return’s due date, including extensions. Filing Form 8938 does not replace FinCEN Form 114 (FBAR) if FBAR is otherwise required. If you are not required to file an income tax return for the year, you do not need Form 8938. For certain specified domestic entities, filing can apply for tax years beginning after December 31, 2015, when total specified foreign financial assets exceed $50,000 on the last day of the tax year or $75,000 at any time during the year.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Tbilisi Digital Nomad Guide for 2026 Long Stays in Georgia

Start with sequence, not excitement. If your income depends on delivering work on schedule, secure your legal footing, assemble your documents, and keep month one reversible before you optimize comfort.

Using DTA Tie-Breaker Clauses to Resolve Dual Tax Residency

If two countries can both claim you as a tax resident, the safer move is a treaty position you can prove and keep consistent across filings, not a one-year optimization that may fall apart later. DTA tie-breaker rules help allocate treaty residence, but only after you confirm that dual-residency risk is real under domestic law on both sides.