Quick Answer

Start with this: a politically exposed person is someone in a prominent public function, so the file gets higher-risk due diligence, not an automatic misconduct label. Screen for PEP links and close associates, verify identity and beneficial ownership, then decide whether standard CDD is enough or EDD is required before funds move. In U.S.-linked programs, record that BSA/AML does not define PEP and keep PEP and SFPF classifications separate.

What this guide will help you decide#

Use this guide to make one clear onboarding call each time: proceed with standard checks or escalate before funds move. The goal is simple: cleaner onboarding, fewer payout surprises, and AML records you can defend later.

If you came in asking what a politically exposed person is, treat the answer as a risk flag, not an accusation. A Politically Exposed Person (PEP) is someone who holds or held a prominent public function, and that status may require deeper review.

The legal context is not uniform. In U.S.-linked work, BSA/AML regulations do not define PEP, and there are no BSA regulations specific to foreign individual customers a firm designates as PEPs. Across jurisdictions, categories differ and there is no complete global list, so your control choice has to be reasonable and documented for the case in front of you.

What matters here is decision order. To reduce risk, do not jump from a screening hit to a payout decision without verifying identity, role context, and ownership. You can cut rework by moving each file through the same checkpoints in the same order:

- Screen for PEP status and close connections before transfer completion.

- Verify identity and role details, then confirm beneficial ownership for legal entities.

- Decide whether Customer Due Diligence (CDD) is enough or whether Enhanced Due Diligence (EDD) may be required.

- Escalate unclear or higher-risk files for second-level review before payout enablement.

- Record the decision trail so later suspicious activity reporting questions can be handled quickly.

A practical rule is to pause higher-risk payouts while status is unresolved. Keep dated notes on what you checked, what remains uncertain, who approved the outcome, and why the selected control level fit the facts.

That keeps this guide focused on outcomes you can use right away. By the end, you should be able to run one file from intake to decision and explain why that decision was made. You should also have enough evidence that a second reviewer can follow your logic without a live handover. Related: How to Automate Your Freelance Tax Preparation.

What a PEP is and what it is not#

A Politically Exposed Person (PEP) is someone who holds a prominent public position. In practice, it is a due diligence risk label, not proof of wrongdoing. It signals that a person's role and influence may create higher bribery and corruption risk, so review depth may need to increase.

This matters because the label is easy to misread. A PEP result does not say the person did anything illegal. It says your controls may need to be stronger, and that your file should show why those controls are proportionate for this relationship.

In U.S.-linked programs, keep labels precise. BSA/AML regulations do not define the term PEP, and FFIEC distinguishes PEP from Senior Foreign Political Figure (SFPF). SFPF is a narrower category, not a replacement for broader PEP treatment.

For day-to-day decisions, use a short written checkpoint:

- Public role and jurisdiction used for classification.

- Whether the file is PEP or SFPF, and why.

- Control level required, including whether EDD applies.

- What triggers re-review, such as role changes or adverse updates.

Two mistakes create avoidable risk. One is treating a screening hit as a final decision. The other is copying one country's logic across borders without adjustment. Definitions vary, so your rationale should always show jurisdiction and control choice.

A third mistake is letting language drift across internal notes. One reviewer writes PEP, another writes SFPF, and a third uses the terms interchangeably even when the file does not support that choice. Keep one classification line in the file header and reuse it across approvals, monitoring entries, and any escalation summary.

If you keep that discipline, later reviews get faster. You spend less time reinterpreting old notes and more time checking whether facts changed. That is the point of clear definitions: fewer judgment errors under time pressure. If you want a deeper dive, read Taxes in Germany for Freelancers and Expats.

Who should be screened as in scope#

Screen people with meaningful public-function influence, plus those closely linked to that influence through family or business relationships.

| Category | Why in scope | Article note |

|---|---|---|

| Direct roles entrusted with prominent national, EU, or international public functions | Meaningful public-function influence | Includes senior executives at a State-Owned Enterprise (SOE); use actual authority as the test, not title prestige |

| Family members | Can also be risk-relevant | Indirect exposure |

| Close business associates | Can also be risk-relevant | Indirect exposure |

| Officials in international organizations | May be in scope | Edge cases need explicit handling |

| People who previously held prominent roles | Can still carry influence | Edge cases need explicit handling |

Start with direct roles entrusted with prominent national, EU, or international public functions, including senior executives at a State-Owned Enterprise (SOE). Use actual authority as the test, not title prestige.

Then include indirect exposure. Family members and close business associates can also be risk-relevant.

Handle edge cases explicitly. Officials in international organizations may be in scope, and people who previously held prominent roles can still carry influence.

Your quality test is simple: can another reviewer see why this person was in scope without calling you? If the answer is no, your file probably needs stronger role notes, clearer relationship mapping, or both. Screening volume matters less than screening quality.

When role clarity is weak, use the same triage every time:

- Mark the file as potential PEP.

- Route it to enhanced due diligence review.

- Record the jurisdiction logic behind the final classification.

A useful habit is to separate confirmed facts from client-declared facts in the same section of the file. That keeps uncertainty visible and reduces accidental overconfidence. It also helps escalation reviewers focus on what still needs verification instead of rereading the full record.

Because definitions vary across jurisdictions, no single definitive global PEP list works in every case. Done well, scope decisions prevent two opposite errors: missing real exposure or over-flagging low-relevance profiles. The right balance is not broad or narrow by default. It is evidence-led and repeatable.

Why PEP status changes onboarding decisions#

PEP classification usually moves onboarding from baseline CDD to EDD with stricter review. That shift is preventive and risk-based, not a finding of criminal behavior.

CDD can open a file, but PEP-linked decisions often need additional AML/CFT measures before onboarding proceeds. The extra work usually shows up in verification depth, review steps, and ongoing monitoring.

| Onboarding area | Baseline CDD | PEP-linked EDD |

|---|---|---|

| Verification depth | Identity and basic background checks | Additional layers of scrutiny on risk context |

| Approval standard | Routine onboarding review | Additional risk review and controls before onboarding proceeds |

| Monitoring posture | Initial review | Ongoing monitoring for profile changes |

The real burden is file quality, not just one extra task. You need consistent identity and role details, clear risk context, and rationale notes that make escalation and reporting decisions defensible.

Before enablement, use this checkpoint:

- Confirm identity and role information is internally consistent.

- Document risk context clearly enough for escalation decisions.

- Record why the decision was made, what conditions apply, and what triggers escalation.

The tradeoff is straightforward: faster onboarding reduces friction, but weaker review increases regulatory and operational exposure. Keep unresolved files in enhanced review and continue monitoring after onboarding as risk signals change.

One way to manage this tradeoff is to split the file into two views. The first view is a short decision summary for approvers. The second view is full evidence. That structure keeps approvals moving while preserving detail for audit or later challenge.

Escalation quality depends on clarity, not length. A long note with unclear evidence is harder to review than a short note with clear facts, explicit gaps, and a direct recommendation. Good EDD files read like a sequence of checks, not a stream of commentary.

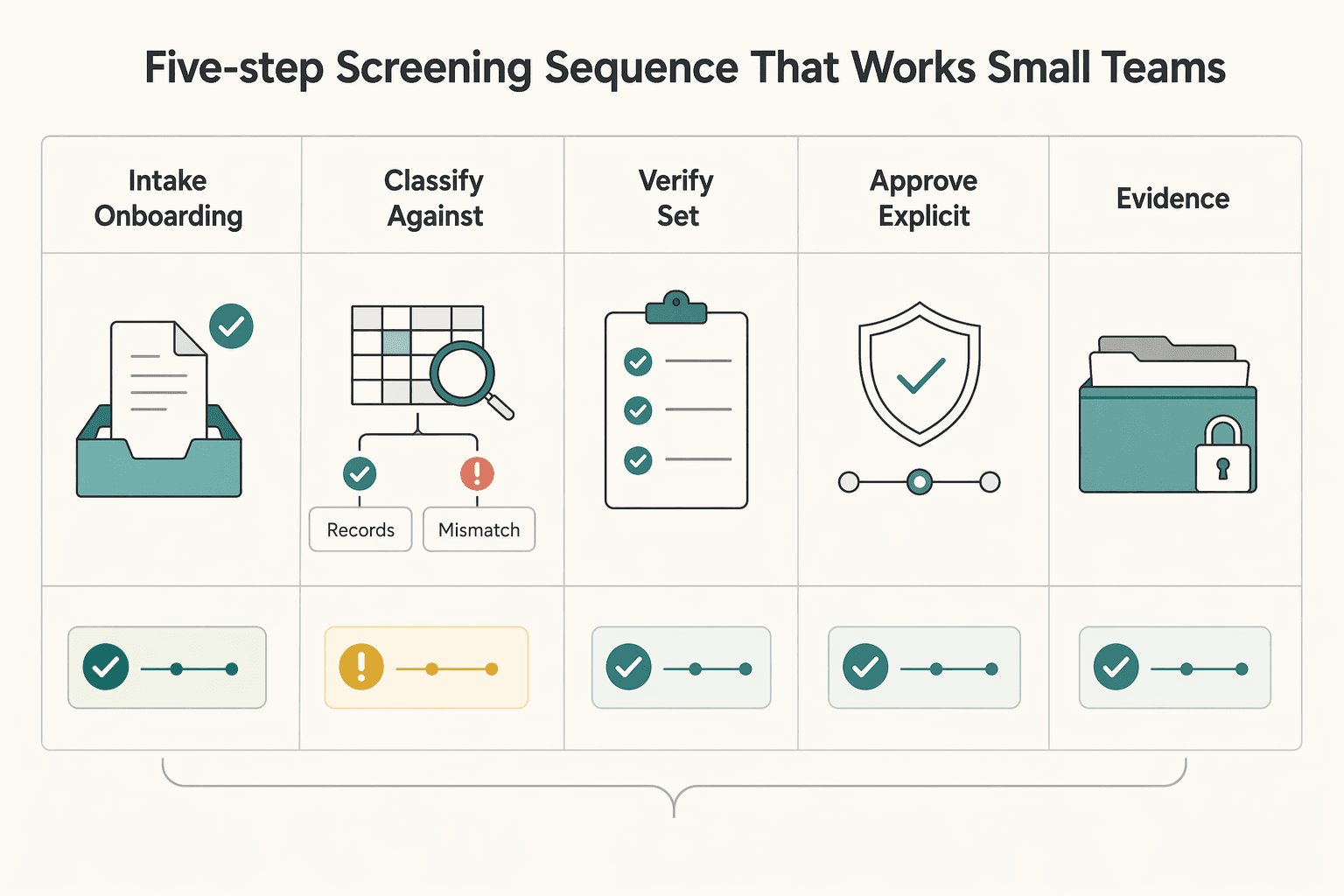

The five-step screening sequence that works in small teams#

Use one consistent internal path for every flagged file: collect, classify, verify, approve with conditions, and archive. Consistency makes decisions easier to defend and easier to revisit.

| Step | Main action | File should show |

|---|---|---|

| Intake for onboarding and ownership context | Capture core onboarding data according to your policy (for example, legal name, role, jurisdiction, and ownership links) | Add a quick completeness gate before moving to classification |

| Classify against your written policy | Map the file to your internal PEP criteria, including related and closely associated persons where relevant | One sentence that another reviewer can test: who is in scope, under which jurisdiction lens, and why |

| Verify and set standard due diligence versus EDD depth | Corroborate role and relationship details, then decide whether standard due diligence is sufficient or EDD is required | Keep unresolved points visible and tie each unresolved point to a follow-up action or escalation call |

| Approve with explicit conditions | Document who approved, why, what controls apply, and what will trigger re-review under AML risk handling | List which events force immediate reassessment, what temporary limits apply before reassessment, and who owns the next check |

| Archive a dated evidence file | Store intake records, classification notes, verification findings, approval rationale, and monitoring triggers in one place | The file should stand on its own for audit questions and possible escalation |

Small teams benefit from sequence discipline because handoffs are limited and context often lives in one person's memory. A fixed order helps prevent knowledge gaps from turning into control gaps.

- Intake for onboarding and ownership context.

Capture core onboarding data according to your policy, for example legal name, role, jurisdiction, and ownership links. Keep identity and business records aligned early so control lines are clear before later decisions.

At intake, quality matters more than speed. If legal name variants, entity names, or role details are incomplete, later checks become noisy and escalation quality drops. Add a quick completeness gate before moving to classification.

- Classify against your written policy.

Map the file to your internal PEP criteria, including related and closely associated persons where relevant. If your policy uses additional categories, apply only your documented definitions and jurisdiction notes.

Classification should end with one sentence that another reviewer can test: who is in scope, under which jurisdiction lens, and why. If that sentence is vague, the file is not ready for approval.

- Verify and set standard due diligence versus EDD depth.

Corroborate role and relationship details, then decide whether standard due diligence is sufficient or EDD is required. Treat PEP status as a risk signal, not proof of wrongdoing, and keep unresolved files in enhanced review.

Verification is where real failures show up. Name-only checks can over-flag or miss context. Ownership records can conflict. Role history can be unclear. Keep unresolved points visible and tie each one to a follow-up action or escalation call.

- Approve with explicit conditions.

Document who approved, why, what controls apply, and what will trigger re-review under AML risk handling. Clear conditions reduce inconsistent handling later.

Conditions should be operational, not abstract. Instead of writing monitor closely, list which events force immediate reassessment, what temporary limits apply before reassessment, and who owns the next check.

- Archive a dated evidence file.

Store intake records, classification notes, verification findings, approval rationale, and monitoring triggers in one place. The file should stand on its own for audit questions and possible escalation.

A dated archive is not just recordkeeping. It protects continuity when team members change, when a relationship is reviewed months later, or when a payout decision is questioned after the fact.

For Canada-linked programs, align this sequence with FINTRAC expectations and the sector guidance relevant to your activity. Move efficiently, but do not trade away evidence quality.

If capacity is tight, protect three things first: classification quality, verification quality, and signed decision records. Those three controls usually reduce downstream risk and avoidable rework.

Proceed escalate or decline with clear decision rules#

Use one decision rule: proceed, escalate, or decline based on evidence quality, not commercial pressure. A PEP flag increases scrutiny, but it does not require automatic rejection.

| Decision | Trigger pattern | Required action |

|---|---|---|

| Proceed | No credible PEP indicators and the file is coherent | Continue onboarding under standard controls and routine monitoring |

| Escalate | PEP indicators exist, or source-of-funds or source-of-wealth clarity is incomplete | Apply EDD with a risk-based, proportionate approach, obtain senior management approval, and increase monitoring intensity |

| Decline | Material contradictions remain after follow-up on key risk facts | Stop onboarding, record the rationale, and preserve the review file |

You should escalate when key facts are unresolved, especially around control of funds, wealth origin, or close-associate relationships. Senior approval should rest on a concise summary of what was verified, what remains unverified, and which controls apply if approved.

Decline when contradictions persist after reasonable follow-up, not because of a single missing document. If your workflow has payout enablement, keep a checkpoint so activation follows a documented proceed or escalate decision.

A useful test is to ask whether the file could survive an independent challenge. If a reviewer can trace the decision from facts to action without making assumptions, your call is probably defensible. If the reviewer has to infer key facts, escalate or hold.

Consistency also reduces drift risk. Similar files should get similar outcomes unless new evidence supports a different decision. Put that expectation in reviewer guidance so outcomes do not vary by individual style.

When pressure is high, protect the checkpoint order. Skipping one step may save hours now and create remediation work later.

Build an EDD evidence pack before first high-risk transaction#

Complete the EDD evidence pack before enabling a first high-risk transaction. The file should let a second reviewer understand why the relationship is manageable, which controls apply, and when escalation is required.

| Pack section | What to include | Why it matters |

|---|---|---|

| Prove identity, role, and relationship scope | Core identity details, the information used to establish PEP status, and relatives and close associates labeled as verified or client-declared | Another reviewer can reproduce your conclusion without extra context |

| Make beneficial ownership traceable | A clear control chain showing who in the end owns or controls the customer, which evidence supports each link, and where uncertainty remains | Control and benefit paths are visible from legal entity to natural person |

| Record risk rationale and reporting triggers | Why you proceeded, which controls are conditional, and what facts would trigger escalation or reporting review | Monitoring decisions stay consistent across reviewers |

| Lock the reviewer trail before release | Reviewer name, decision date, policy version used, the release checkpoint for first high-risk activity, and the conditions that require re-review | Removes ambiguity from later monitoring and reduces repeated review work |

Think of this pack as decision evidence, not document storage. A folder full of files is not enough if the links between facts and decisions are unclear. Your pack should show what was verified, what remains uncertain, and why the approval conditions are proportionate.

Prove identity, role, and relationship scope#

Record core identity details, then include the information used to establish PEP status. Map relatives and close associates tied to the account or entity, and label each relationship as verified or client-declared. Write this section so another reviewer can reproduce your conclusion without extra context.

This section should also show role context in plain language. If the person held a relevant public function, state that function and the jurisdiction lens used for classification. Avoid vague labels that force later reviewers to reopen basic scope questions.

Make beneficial ownership traceable#

Present ownership findings as a clear control chain. Show who in the end owns or controls the customer, which evidence supports each link, and where uncertainty remains. If ownership evidence conflicts, keep escalation active until the chain is coherent.

Ownership mapping should make control and benefit paths visible from legal entity to natural person. If any link is assumed rather than supported, flag it clearly.

Record risk rationale and reporting triggers#

State the decision logic in plain language: why you proceeded, which controls are conditional, and what facts would trigger escalation or reporting review. Keep triggers specific and observable so monitoring decisions stay consistent across reviewers.

Good trigger design reduces disputes later. Write triggers in terms that can be checked in records, transaction behavior, or role updates. Avoid broad language that different reviewers will interpret differently.

Lock the reviewer trail before release#

Close the file with reviewer metadata under your EDD program: reviewer name, decision date, and policy version used. Record the release checkpoint for first high-risk activity and the conditions that require re-review.

Before release, run a short file integrity check:

- All required fields are complete.

- Outstanding questions are either resolved or explicitly accepted with conditions.

- Approval conditions are clear enough for monitoring teams to apply without extra explanation.

- The next review date or trigger owner is recorded.

This takes extra effort at first approval, but it removes ambiguity from later monitoring and reduces repeated review work. You might also find this useful: A Guide to France's Micro-Entrepreneur Regime for Freelancers.

Monitor PEP relationships after onboarding#

Monitoring starts at onboarding. For PEP-linked relationships, institutions should apply additional AML/CFT measures at onboarding and continue monitoring so controls track current risk, not frozen onboarding assumptions.

Monitoring quality often decides whether early due diligence keeps its value. A strong onboarding file can still fail in practice if later changes are not captured and recorded in time.

Set review cadence by risk tier#

Set cadence at approval time using risk tier, policy, and jurisdictional requirements. Higher-risk files should typically have tighter review intervals than lower-risk files.

At each periodic review, confirm:

- current risk tier

- current public-role status

- current family and close-associate links

If core fields are missing, treat the file as incomplete and close gaps before changing risk treatment. A practical improvement is to predefine what complete means for each review tier, so reviewers do not spend time debating scope during each cycle.

Track trigger events between scheduled reviews#

Periodic reviews are necessary but not sufficient. Reopen review when material changes appear between cycles, such as:

- role changes that alter public-function exposure

- new family or close-associate links

- other updates that materially change the customer risk profile

When a trigger appears, reassess due diligence promptly and decide whether additional AML/CFT measures are now required. Fast trigger handling prevents stale approvals from being treated as current facts.

Refresh controls when risk rises#

If new information raises risk, tighten controls while reassessment is in progress. Document what changed, which control changed, and what evidence would support stepping controls down later.

PEP status remains a preventive risk signal, not proof of criminal behavior, and control changes should be reversible based on evidence. If risk drops and evidence supports that view, record the rationale for stepping down controls just as clearly as you record escalation.

Keep evidence current#

Append each monitoring outcome to the same client record so the history is easy to follow. For each entry, include:

- review date

- reviewer

- facts checked

- control decision

- next review date

Over time, this history shows that decisions were not one-time judgments and that risk handling evolved with facts.

Handle country and program differences without guessing#

Start with scope, not labels. PEP definitions can differ by jurisdiction and program, so classify each case by jurisdiction and program before you set controls.

Most confusion comes from mixing language across programs. One country label may look familiar but carry a different practical meaning elsewhere. Keep jurisdiction and program context visible at the top of each file to avoid that drift.

Anchor U.S. programs to BSA and FinCEN language#

For U.S.-linked programs, ground decisions in BSA context and FinCEN interagency language rather than a generic global definition. The interagency statement notes that BSA/AML regulations do not define PEPs, does not interpret PEPs to include U.S. public officials, and makes clear that not all PEPs are automatically higher risk. Your file should explain why risk is or is not elevated in this specific relationship and why control intensity matches those facts.

Keep PEP and SFPF separate in classification#

Do not treat PEP and SFPF as interchangeable. In U.S. interagency framing, SFPF is a subset of PEPs, not a synonym, and separate fields for PEP status and SFPF status help reviewers see which rule set was applied and why.

This separation can reduce downstream confusion in approvals, monitoring, and audit reviews. It can also help prevent overbroad treatment when only one category applies.

Use a conflict rule you can defend#

When jurisdiction guidance conflicts, apply the stricter control path first and record the rationale in the case file.

Use a short decision record:

- jurisdiction and program in scope

- classification terms used, including PEP and SFPF

- control level chosen and why

- approver and policy version date

Date-stamp the governing rule source in each case. Effective timelines and deadlines can differ by cohort. If your team cannot agree which rule controls the case, treat that disagreement as an escalation trigger. Resolve unclear rule ownership before activation.

Common mistakes that create avoidable compliance risk#

Most avoidable risk comes from execution gaps: treating checks as one-and-done, screening too narrowly, and keeping weak records.

-

Treating PEP checks as one-time onboarding. Weak onboarding due diligence can become a costly AML problem. Start with stronger CDD and keep records current through periodic review. If a file has no documented periodic review after approval, treat it as a potential control gap.

-

Relying on name-only screening. Name matching alone can miss relevant exposure. Go beyond names with screening that is accurate and data-driven. A clean name result should not be treated as sufficient on its own.

-

Letting speed override EDD. Fast onboarding is not lower-risk onboarding. A risk-based approach may require EDD for PEP exposure, high-risk industries, or higher-risk jurisdictions. If evidence is incomplete, do not weaken verification to move faster.

-

Collecting data without clear control logic. Tie collection to CDD or EDD purpose, then maintain retention and review discipline so records stay current. Data that is not maintained through retention and review can leave due diligence records out of date.

-

Failing to document why you proceeded. Record key due diligence decisions and keep the file current through periodic review and retention discipline. This helps keep due diligence records accurate and up to date.

One practical correction is to automate retention and periodic reviews so customer due diligence records remain accurate and current. Focus on verification evidence and review entries so recurring execution issues are easier to spot.

Use these controls in Gruv-enabled payment operations#

Apply policy gates before irreversible payment steps, and do not release funds until required checks are complete and recorded. In Gruv-enabled flows, that usually means clear controls at onboarding, payout enablement, and exception handling, with checks configured by market and program where supported.

A workable model is one owner and one required output per gate. If required data is missing, stop and escalate instead of moving forward on a verbal assurance.

- Onboarding gate: collect the identity and business-profile inputs your policy requires.

- Payout gate: require a recorded risk decision before higher-risk payout paths, and escalate when policy triggers are met.

- Exception gate: require second-level approval, a reason code, and an expiry date for any bypass.

Keep the audit trail traceable from request to ledger posting and reconciliation. Each posted payout should map to decision IDs, approver IDs, and timestamps so the file is defensible without later reconstruction.

For asynchronous events, align monitoring with status changes and rerun relevant checks if material fields change before release. If reruns cannot complete in time, hold settlement so stale approvals are not treated as current.

Use reference documents with precision. Definition material such as EAR Part 772 can clarify terminology, and technical framework submissions such as POLARIS 3.0 can inform implementation, but neither replaces the legal and compliance obligations that govern payment operations.

To reduce handoff gaps between teams, keep gate outputs short, structured, and visible to the next reviewer. That keeps decision context intact from intake through final posting.

If you need one operational rule to protect reliability, use this: no unresolved escalation items at payout release. That rule helps reduce avoidable reversals and supports both customer experience and compliance defensibility.

The bottom line for independent professionals#

Treat PEP status as a risk-management decision, not a character judgment. In practice, a PEP result tells you which controls to apply before onboarding or payout actions, not whether someone did anything wrong.

Because there is no single global definition, your standard should be jurisdiction-aware and explicit about scope. If your program uses both terms, keep SFPF separate from broader PEP treatment because they can overlap without being identical.

Use one repeatable CDD and EDD sequence:

- Classify the person and related parties, including family members or close associates when relevant.

- Verify core facts, including source of wealth or source of funds when risk is higher.

- Decide the control path: standard CDD or EDD, with senior approval for higher-risk relationships.

- Monitor the relationship over time, with tighter checks where risk is higher.

- Document the full decision path so your rationale is clear and defensible.

One failure point is relying on name matches alone. Commercial tools can over-flag less prominent roles, so test for truly prominent positions under your jurisdictional standard and record your rationale.

Keep lower-risk files lean, but do not compromise on evidence. If classification is unclear or verification is incomplete, pause, escalate to EDD, and require sign-off before funds move.

If you want one final rule to carry forward, use this: no evidence, no release. That single discipline helps protect risk posture, supports fair treatment, and keeps your decision record strong when it is reviewed later.

Frequently Asked Questions

What is a politically exposed person in plain language?

A politically exposed person is someone who holds a prominent public position. PEP status is used for risk and compliance review, not as a criminal label, and countries define PEP status differently rather than using one global list. The practical takeaway is that this label changes your due diligence depth, so you still need identity, role, and ownership checks before deciding whether standard controls are enough.

Is being a PEP illegal or automatically suspicious?

No. PEP status is a risk classification and not automatic evidence of wrongdoing. In U.S. guidance, BSA/AML regulations do not define the term PEP, and FFIEC notes there are no BSA regulations specific to foreign individual customers designated as PEPs. The right response is proportionate controls, better evidence, and clear approval rationale.

Who counts as a PEP besides politicians?

Scope can include more than elected officials, depending on jurisdiction. Many programs include related persons, such as family members, and may include people who previously held certain offices, including Canada's domestic approach for people who hold, or have held within the last 5 years, specified public offices. Related-person and ownership links can also affect practical risk assessment.

What is the difference between CDD and EDD for PEP cases?

CDD is the baseline due diligence layer used alongside customer identification, beneficial ownership, and suspicious activity reporting controls. EDD is the higher-scrutiny path for higher-risk cases, and many jurisdictions expect EDD with ongoing monitoring for PEP relationships. In practice, CDD may be enough for lower-risk files with clear facts, while EDD fits files with unresolved role or ownership questions.

What checks are required before I onboard or pay a PEP-linked client?

Start with a documented classification decision based on the relevant jurisdiction, and keep SFPF distinct from the broader PEP category. Complete required CDD elements, including identification and beneficial ownership details where applicable, then apply EDD when risk is higher and record the decision path before onboarding or payment actions proceed. Before payout enablement, document whether unresolved questions are closed or explicitly accepted with conditions and approval.

How often should I re-check a client after initial PEP screening?

There is no single universal re-screening interval to apply here. Use a risk- and jurisdiction-based schedule, with ongoing monitoring for higher-risk relationships, and apply local lookback rules only where they actually govern your case. Beyond calendar reviews, reassess when role or ownership information materially changes.

Watch

What Is a Politically Exposed Person?

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 3 external sources outside the trusted-domain allowlist.

- bsaefiling.fincen.gov/docs/XMLUserGuide_FinCENFBAR.pdftrusted

- fincen.gov/system/files/2025-12/FBAR-FBAR-Filing-Requir...trusted

- acgcs.org/articles/enhanced-due-diligence-for-high-ris...external

- amlsquare.com/blog/what-is-a-politically-exposed-person-pepexternal

- lawsociety.org.uk/contact-or-visit-us/helplines/practice-advic...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Taxes in Germany for Freelancers and Expats

Low-stress compliance in Germany comes from decision order, not tax tricks. Use this sequence: confirm core facts, apply conservative temporary assumptions, verify the few points that can break invoices or filings, and keep one evidence file that explains each decision.

How to Automate Your Freelance Tax Preparation

**To automate freelance taxes safely, automate the boring mechanics and keep human approval for the decisions that create real compliance risk.** You are the CEO of a business-of-one. Your job is to run a system that stays resilient while your clients, tools, and countries change.

How Freelancers Can Decide on France’s Micro-Entrepreneur Regime

Low-stress compliance starts with one question: does the Micro-entrepreneur regime match your real setup right now? It is often presented as a simplified option for lower-revenue activity, so use it as a fit test, not a shortcut.