Quick Answer

An income statement, or profit and loss statement, shows a payment business's performance over a specific period. For platform finance teams, it should tie revenue, fees, losses, and expenses to journal entries, provider reports, and bank activity so close-time numbers are complete, explainable, and usable for decisions. In payments, timing differences between transactions, settlements, and payouts make that operational discipline essential.

Why the income statement matters in a payment business#

For a payment business moving money at volume, the income statement needs to work as an operating tool, not just a textbook concept or a finance-only report.

This guide is for platform finance leaders, operations owners, and product teams who shape reporting quality before close, not just after the numbers are published. If you own controls around money movement, the goal is to make the P&L usable at close time.

The definitions are simple enough. The income statement shows performance over a period and sits alongside the balance sheet and cash flow statement in the core financial-statement set. The hard part in payments is turning high-volume activity into a period view that is complete, explainable, and consistent when transaction timing and payout timing do not line up cleanly.

The standard here is practical: use explicit evidence and repeatable checks. Numbers are only decision-ready when they trace to the general ledger and are supported by matching payment activity to bank statement activity. Unmatched bank movements and other close exceptions should trigger visible handoffs, not quiet workarounds.

By the end, you should be able to run a cleaner period-end close with explicit checkpoints, clear failure handling, and tighter finance-ops coordination. You should also be able to connect P&L lines to transaction activity, verify journals are posted before period-end reporting, and label exceptions clearly when data is incomplete at cutoff.

Define the statement before you operationalize it#

Start by fixing the definition. In most business settings, the income statement and profit and loss statement (P&L) are the same report of performance over a specific period.

What matters in practice is keeping the three core statements separate so position, cash movement, and period performance do not get mixed during close.

| Statement | What it shows | Practical use in payments |

|---|---|---|

| Income statement / P&L | Performance over a specific period | Revenue, fees, losses, and expenses for the month or quarter |

| Balance sheet | Financial condition at a specific point in time | Cash, receivables, payables, reserves, and unsettled balances at cutoff |

| Cash flow statement | Cash moving in and out of the entity | Whether cash changed through operating, investing, or financing activity |

For executive reporting, keep each metric anchored to the right statement and period so performance, position, and cash movement are reviewed in the correct context.

This define-first approach matters most when numbers move fast and review time is tight. It also matters for the Chief Financial Officer (CFO). In U.S. public company reporting, CFO and CEO certification applies to 10-K and 10-Q accuracy under SEC rules adopted under Sarbanes-Oxley Section 302. In private settings, teams may use similar discipline internally, but the SEC certification requirement itself is for public-company filings.

This pairs well with our guide on How to Read an Income Statement (P&L).

Map payment operations to P&L lines#

Map each payment event to one clear reporting outcome, then require two proofs before it enters close reporting: a journal family and a matching checkpoint. Use the table below as a reference structure, not as a universal journal design.

| Event | What it means operationally | Typical P&L effect | Required traceability checkpoint |

|---|---|---|---|

| Invoice payment | Customer payment is initiated or captured against an invoice or obligation | Revenue or no immediate P&L effect, depending on recognition policy | Payment event ID tied to a journal family and provider matching proof |

| PSP fee | Processor or network fee is assessed | Processing fee or direct cost expense line | Itemized fee report tied to fee journal family with transaction-level attribution |

| Settlement | Processed funds become accessible to the business | Often no new P&L effect by itself; supports cutoff and movement validation | Provider report matched to balance activity and bank movement where applicable |

| Chargeback or return | Payment is refunded, reversed, or disputed | Contra revenue, expense or loss, or dispute fee based on policy | Refund or dispute reference, negative transaction record, and open-item review |

| Payout execution | Funds move from provider or merchant balance to bank | Usually no new P&L effect by itself; mainly cash and balance sheet movement | Payout ID tied to bank statement match and payout-to-balance review |

Make source-to-report traceability non-negotiable#

Every material P&L line should drill down to event-level support. Fee totals should tie to fee records, dispute losses to dispute or refund references, and variance analysis to provider data plus bank match. If your finance system supports posting audit attributes, keep journal entry numbers and transaction details visible in review output.

Treat this as a control requirement, not a formatting preference. GAO has linked traceability gaps to financial reporting control deficiencies and to the risk of recording activity in the wrong general ledger accounts and line items. A useful close test is simple: a reviewer should be able to retrieve the event population, journal family, and matching proof without rebuilding the number from scratch.

Set timing rules up front as well. For example, Stripe documents transaction-level fee reporting, but also notes that fee data in that report can arrive with a delay, up to 96 hours after a fee affects your balance. If close depends on detail that has not arrived yet, you may need to delay close or rely on estimates.

Separate gross-vs-net policy from provider cash behavior#

Do not let PSP net funding drive revenue presentation. Net funding is a cash behavior. Gross-versus-net presentation is an accounting policy decision under GAAP or IFRS.

Under IFRS 15, principal-versus-agent judgment turns on control before transfer to the customer. Under U.S. GAAP ASC 606, the same principal-versus-agent area applies in multi-party arrangements and often requires significant judgment. Document the policy clearly: transaction flow, revenue line affected, gross or net conclusion, basis, approver, and review date.

Operationally, keep gross event visibility internally even when provider funding is net. Stripe's balance documentation notes that pending balances can reflect charge amounts net of fees before funds become available. If you follow only net cash, you can lose visibility into gross transaction amounts and fees in internal platform finance reporting. Keep separate fields and journal families for payment amount, provider fee, funded amount, and payout amount, then apply your GAAP or IFRS policy for external presentation. Related: How to Build a Deterministic Ledger for a Payment Platform.

Build classification rules that survive scale#

Once events are mapped, lock the classification policy before volume and edge cases multiply. Use one controlled map for revenue, direct costs, payment fees, FX impact, and operating expense. Apply it the same way across the accounting records, PSP reports, and bank statement review.

Start with one expense basis and keep it stable#

Classification churn usually starts when teams mix logic. Under IAS 1 paragraph 99, classify profit-or-loss expenses by either nature or function based on which is more reliable and relevant. Then keep that basis stable in your chart and reporting pack.

If you use a function view, define what belongs in direct costs versus operating expense. If you use a nature view, still define how processor fees, dispute fees, and FX differences are classified. Keep gross-versus-net revenue tied to your IFRS 15 principal assessment, not to PSP cash mechanics.

| Classification area | Policy anchor | Primary system evidence | Common failure mode |

|---|---|---|---|

| Revenue | IFRS 15 principal versus agent conclusion | Revenue journals plus PSP transaction detail | Net funding treated as net revenue without policy review |

| Direct costs | IAS 1 chosen basis, with approved cost definition | Expense journals plus itemized provider or partner cost files | Costs drift into opex during close because ownership is unclear |

| Payment fees | Approved fee policy under your expense basis | PSP batch or fee detail report, then matched to accounting records | Fees booked twice from both transaction feed and batch summary |

| FX impact | IAS 21 exchange-difference policy | FX entries plus PSP currency detail and provider data | FX buried inside fees because provider reports are netted |

| Operating expense | Residual category only after direct-cost test | Journals and invoice or accrual support | Manual journals used as a catch-all for unresolved payment items |

Make the three records agree to the same policy#

A classification policy is only real when all three records support the same treatment. The accounting records show the result, the bank statement supports cash movement, and PSP reports provide the event-level and batch detail behind both.

Bank matching guidance requires tying accounting records to bank evidence, but timing differences will still happen. During month-end close, have reviewers trace each material classified amount to three things: the journal family, the PSP reference, and either bank movement or a documented timing explanation.

Use the PSP artifact that best fits the rule. Stripe's payout reconciliation report is built for batch-level matching. Adyen's settlement details report supports transaction-level review and cost visibility. PayPal provides reconciliation reports for finance and accounting workflows.

Set red-line exceptions before close pressure hits#

Decide the escalation lines before close starts. Ops can resolve routine issues that do not change policy, such as missing references, expected bank timing differences, or report-format problems. Escalate to finance leadership when any of these apply:

| Escalation trigger | Article detail |

|---|---|

| Policy-impacting classification change | The case could change gross-versus-net treatment, reclassify between direct cost and operating expense, or introduce a new FX classification rule. |

| Manual top-side journal | A manual top-side journal is required because accounting, PSP, and bank evidence do not tie cleanly. |

| Role conflict | Posting, matching, and approval would fall to the same person. |

This supports sound control design. Reconciliations, verifications, approvals, and authorizations are core control activities, and identified deficiencies should be remediated on a timely basis. Keep an exception log with event IDs, journal entries, PSP extract, bank trace, owner, decision, and follow-up action.

Stricter classification rules can slow initial setup because categories, evidence requirements, and approvers need to be defined up front. Whether they reduce recurring tie-out breaks and close-time reclassification disputes depends on consistent application and timely remediation.

For a step-by-step walkthrough, see Real-Time Reporting Metrics Platform Finance Teams Can Actually Control.

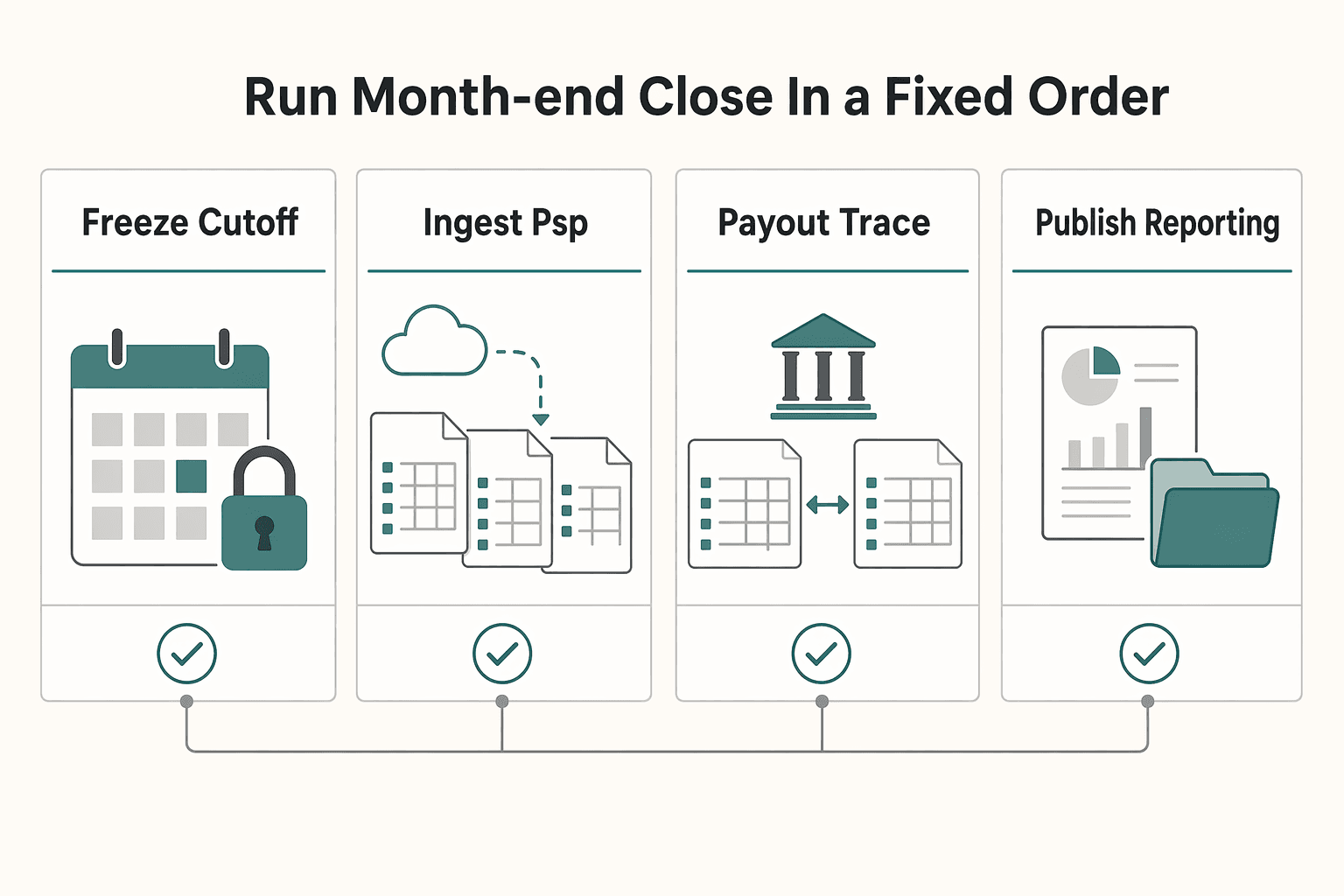

Run month-end close in a fixed order#

Close runs better when the sequence is fixed and reviewed numbers stay closed. Use the order as an operating control, not as a GAAP or IFRS mandate.

A practical sequence is: freeze cutoff, ingest PSP files, match provider cash activity to the bank statement, post required adjustments, then publish the reporting pack.

| Close step | What you are deciding | Primary evidence | Common break |

|---|---|---|---|

| Freeze cutoff | Which events belong in the period | Period-end transaction extract, close calendar, cutoff memo | Late events enter through manual uploads after review starts |

| Ingest PSP files | Whether provider data is complete for the period | Stripe payout reconciliation report, Adyen settlement details report, other PSP exports | Teams book from dashboard totals before final files arrive |

| Match settlement to bank | Whether settled cash ties to external movement | PSP batch or payout detail plus bank statement | Net deposits posted without separating fees, returns, or reversals |

| Post adjustments to Ledger | Whether accounting records reflect the matched position | Review output, journal support, adjustment approval | Differences stay in suspense or get forced through top-side journals |

| Publish reporting pack | Whether numbers are ready for executive use | Final variance log, sign-off record, management pack | Reporting goes out while unresolved items are still moving |

Use provider artifacts that fit the reconciliation level#

Match the artifact to the job. Use Stripe's payout reconciliation report for payout-batch review and Adyen's settlement details report for transaction-level review. Mixing batch-level and transaction-level logic in one pass usually creates noisier exceptions and slower clearance.

Before posting adjustments, compare internal cash movement to external bank evidence. Then post general-ledger adjustments on that matched basis. If provider cash does not tie out, stop before reporting.

Make owner handoffs explicit before exceptions pile up#

A fixed order only works when ownership is clear. One practical split is that finance owns accounting conclusions and journal decisions, while ops investigates provider references, payout status, returns, reversals, and bank trace details. Set explicit handoffs for recurring exceptions:

| Exception | Ops action | Finance action |

|---|---|---|

| Unmatched deposits | Researches payout ID, bank trace, and timing status | Decides timing difference versus posting gap versus adjustment |

| Returns and chargeback-related cash movement | Confirms event history and provider effect | Confirms treatment under policy |

| Payout reversals or payout failures | Confirms event timing context | Decides closed-period adjustment versus next-period treatment |

If information arrives after period end but before financial statements are authorized for issue, evaluate it under IAS 10 as adjusting or non-adjusting. Adjust when it provides evidence of period-end conditions. Otherwise treat it in the next period.

Add checkpoints before the CFO sees the pack#

Do not send the pack forward just because most of the work is done. Add a hard control point between "matched enough to work on" and "ready to publish." At minimum, that checkpoint should include open-item aging, an unresolved variance log, and defined sign-off criteria.

For aging, one external benchmark is U.S. Treasury guidance to resolve unmatched items within 2 months of occurrence. Whether or not you use that exact threshold, age items from open date and escalate recurring items across closes.

Before routing to the Chief Financial Officer (CFO), require sign-off on three points: material provider cash is matched to bank evidence or has documented timing support, required adjustments are posted or explicitly deferred, and remaining items are assigned and below approval thresholds. For SEC issuers, CFO certification sits in a specific regulatory context.

Have a failure path for late settlement data#

Late or incomplete provider data should not force improvised reporting. If your team issues a provisional pack, label it clearly and make the assumptions explicit. Include the missing source, affected period, exposed accounts or P&L lines, estimate basis, owner, and expected true-up window.

When late data arrives, assess updates under IAS 10 before changing period figures so period-end conditions and next-period conditions stay separate. Before finalizing your close checklist, map each handoff to system events and status transitions in the Gruv docs.

Make timing decisions explicit and repeatable#

Cutoff decisions should come from written policy each close, not from last-minute judgment calls. Once most provider cash is matched, the main remaining risk is usually inconsistent treatment of edge cases.

That policy anchor matters. IFRS requires accrual-basis preparation, and IAS 8 requires consistent application of accounting policies to similar transactions. Under whichever framework applies, U.S. GAAP or IFRS, document the policy you use, then apply it consistently to similar facts.

Use a short cutoff table for recurring edge cases#

Use one compact table so finance and ops do not re-litigate the same timing calls every month.

| Edge case | Current-period treatment question | Minimum evidence to decide | Follow-up control |

|---|---|---|---|

| Late Settlement | Did the underlying condition exist by period end, and does your policy allow accrual before bank receipt? | Final PSP detail, related journal entries, period-end cutoff log, note that bank receipt is still outstanding | Check next-period bank clearance and investigate if cash does not arrive as expected |

| Pending Payout execution | Is this only a payout request or payable batch, or has cash actually moved externally? | Payout ID and status at cutoff, provider balance state, payout batch report | Recheck batch closure and bank receipt next period before clearing transit items |

| Post-period PSP adjustments | Does the later adjustment give evidence about a condition that already existed at period end, or did it arise after? | PSP adjustment report, reason code, underlying transaction history, close memo | Apply IAS 10 logic and document whether it is adjusting or non-adjusting |

Provider status definitions matter. Stripe distinguishes pending versus available funds, and timing can vary by method. Adyen's settlement details and payout-batch timing help you tell the difference between supportable period-end evidence and a timing assumption.

Apply one house rule to Ledger versus bank timing#

Use a single house rule: if evidence exists in the accounting records but not yet in the Bank statement, classify the item under policy and flag it for next-period follow-up. Reversal is a case-by-case control outcome, not an assumption that every item will reverse.

Track those items in an exception report with the owner, source report, expected resolution, and whether the next step is cash clearance or an accounting reversal. This avoids a common failure mode: posting from status views and then not revisiting the item when payout timing or adjustments change.

Keep the rationale short, but write it down#

For each material timing judgment, keep a short rationale in the close memo or variance log: fact pattern, policy reference, evidence reviewed, and next-period checkpoint. Under IAS 10, the decision point is whether later information reflects conditions that existed at period end or conditions that arose after period end.

In a high-growth Payment business, a consistent cutoff policy usually supports more consistent period-to-period reporting than ad hoc attempts to perfect timing on each late item. When evidence is incomplete, follow policy, document the judgment, and move on.

Handle the failure modes competitors skip#

Once cutoff policy is in place, close noise often comes from repeatable breakage. Treat duplicate events, missing provider references, mismatched batch totals, and stale payout statuses as named incident types with preset paths. Use matching work to resolve traceability issues. Escalate anything that could change period classification, accruals, or reported numbers.

Separate operational fixes from accounting decisions#

Use one test: is this a traceability problem only, or does it change the accounting records and period results? Stripe notes that webhook deliveries can repeat, so deduplication is a baseline control. Log processed event IDs and do not process events that are already logged. Escalate when a duplicate has already created accounting impact and the correction could change the close.

Apply the same test to missing provider references. Stripe webhook events include a reference to the modified provider object, so first confirm whether the reference exists in raw payloads and survives downstream mapping. If you can restore the link without changing accounting results, keep it in review. If not, escalate instead of forcing a P&L classification guess.

| Failure mode | First response in Reconciliation | Finance escalation trigger | Verification detail |

|---|---|---|---|

| Duplicate webhook effect | Check event ID against processed-event log and suppress reposting | Duplicate already affected the Ledger or reported totals | Match event ID to journal entry IDs and confirm corrective reversal |

| Missing provider reference | Recover provider object reference from raw payload | Source object still cannot be tied to the recorded item | Confirm raw payload, mapped record, and final linked provider object |

| Mismatched Settlement total | Review at payout-batch level; compare provider credits, debits, and counts to bank receipt | Batch still does not explain the bank amount or could affect close reporting | Tie payout batch, provider report, and Bank statement line |

| Stale payout status | Recheck provider status and recent cash movement before clearing transit items | Status remains unresolved and could affect close classification | Confirm current provider status, expected payout path, and bank receipt outcome |

Investigate settlement mismatches at batch level#

Start at batch level, not at the dashboard. Match payout batches to the Bank statement, then validate composition, including credits, debits, and counts, to explain the payout amount. If totals still do not tie, inspect transaction and journal composition so fee, dispute, and other debit or credit activity is not missed.

For stale payout statuses, use real checkpoints. Stripe retries undelivered events for up to three days, and manual recovery is limited to events from the last 30 days. Wait through the retry window when appropriate, but do not let unresolved statuses sit unowned through close.

Require one evidence pack per incident#

For each incident that survives same-day cleanup, keep one pack with the event ID, related journal entries, provider reference, Bank statement trace if cash moved, and final corrective action. Include disputes and fee events where relevant so a reviewer can reconstruct the case from accounting-backed records without reopening it.

Run a recurring incident review tied to close-readiness goals for platform finance. Use lessons learned and root-cause review to reduce repeat breaks such as duplicate-post attempts, unmatched batches, and incidents still open at publish time.

Build the audit and compliance evidence pack#

Incident packs help resolve individual breaks. Your close pack should do the period-level job. Keep one reviewed package that shows policy, supporting evidence, open items, and who prepared, reviewed, and approved the numbers. Evidence quality and traceability matter more than volume.

PCAOB standards are written for auditors, but they are a useful benchmark for close documentation quality. Audit evidence supports conclusions, and documentation should preserve planning, procedures performed, evidence obtained, and conclusions reached. In practice, a reviewer should be able to answer three questions quickly: what policy was applied, what support was used, and who completed and reviewed the work.

What to include in your recommended minimum pack#

This is not a universal legal checklist for every company. It is a practical minimum that keeps a payment-close package defensible and reviewable.

| Artifact | Why it matters | What to verify before sign-off |

|---|---|---|

| Close memo | Records what happened in the period, key judgments, cutoff assumptions, and whether numbers are final or provisional | Confirm period, material judgments, true-up expectations, and links to supporting matches |

| Mapping policy | Shows how payment events map into the Ledger and reporting lines | Confirm each material P&L line ties to a journal family and current source fields |

| Unresolved-item log | Keeps open breaks visible and owned | Confirm owner, amount, aging, expected resolution date, and impact assessment for each item |

| Finance owner approval trail | Preserves preparer, reviewer, and approver traceability and timing | Capture preparer, reviewer, approval date, and the final export version approved |

Approval traceability supports control accountability. Documentation expectations include identifying who performed work and when it was completed, so approvals should tie directly to the final close memo, approved export version, and supporting files.

Tie controls to ledger impact#

If your payout process uses policy gates, document them as controls with a traceable accounting footprint. The close pack should show the gate condition, affected payout population, resulting accounting treatment, and the reporting export where those items appear.

Use one sample-based check: trace a gated payout end to end through trigger, approval or release, posting, and reporting output. If that trace fails, the control may work operationally but still be weak for compliance review.

Overcollecting files while underdocumenting conclusions leaves the pack weak for review. Multiple exports are not enough unless you state which file is authoritative, what period it covers, and how it affects financial statement reporting.

Document GAAP and IFRS choices explicitly#

Name the reporting framework used for policy decisions. For U.S. nongovernmental entities, authoritative GAAP is centralized in the FASB Codification. Under IFRS, standards are developed and published by the IASB. Treat GAAP and IFRS as distinct frameworks in policy design and review.

Policy outcomes can differ materially across GAAP and IFRS depending on facts and elections, so document the judgment rationale and review for presentation and classification decisions. If you are subject to ICFR reporting, management is expected to identify the framework used to evaluate control effectiveness, which reinforces the need to document control design decisions clearly.

If you report under IFRS, keep this date in view: IFRS 18 is effective for annual reporting periods beginning on or after 1 January 2027, with earlier application permitted. Related reading: Spending Controls for AI Agents in Platform Payment Operations.

Connect your finance system without breaking traceability#

If you implement Microsoft Dynamics 365, keep Dynamics 365 Finance aligned to your event-level accounting records, not just period totals. The General ledger can receive postings from other modules, and your close is more defensible when material P&L movements can be traced back to source records.

Set interface boundaries before you expand automation. Use posting profiles to control how subledger accounts map to main accounts. Preserve source-level traceability through import and posting so reviewers can drill from journal entries back to source information using the Accounting source explorer and General ledger inquiry pages.

Set the boundary before you automate more#

Make the split between automation and review deliberate, not accidental.

- Post automatically: high-volume, rule-stable entries, including routine subledger-to-ledger transfers, whether immediate asynchronous or queued scheduled-batch, as long as the rule is applied consistently.

- Require review: new event types, exceptions, manual true-ups, unresolved breaks, and any items above your internal review threshold.

- Keep evidence recheckable: use Advanced bank reconciliation when applicable, and keep import and validation records in Data management and staging.

Use one checkpoint before adding more automation: trace a posted journal through source import, posting profile, entry, and matching evidence. If that trace breaks, fix that path first.

Customize later than you want to#

Avoid heavy ERP mapping customization before month-end close rules are stable. Fit-to-standard analysis helps prevent costly and unnecessary recreation of legacy processes. Start with settings and configuration, then extend only where standard design cannot preserve your accounting logic. For deeper setup detail, use Microsoft Dynamics 365 for Payment Platforms.

We covered this in detail in How to Handle Payment Disputes as a Platform Operator.

Use a monthly scorecard that drives decisions#

Once your source-to-ledger trail is stable, a tight monthly scorecard can be more useful than adding more reporting. Keep the set small. A practical starting set is close duration, unresolved matching items, provider-cash-to-bank match rate, and post-close adjustment count. Add a metric only when it changes owner behavior.

A scorecard should drive action, not sit passively in reporting. CFO KPIs are useful when they help teams make decisions and are shared beyond finance so operating leaders can respond early. That is what makes the Income statement useful to the Chief Financial Officer (CFO) as an operating signal, not just a backward-looking report.

| KPI | How to define it | Primary owner | Action trigger |

|---|---|---|---|

| Close duration | Calendar days from initial trial balance to completed consolidated statements | Platform finance | If close timing slips versus plan, fix cutoff discipline and approval bottlenecks before adding reporting requests |

| Unresolved reconciliation items | Count of open reconciliations plus unmatched transactions unresolved at close | Platform finance + ops | Set an internal rule: if unresolved items keep rising, pause new reporting dimensions and fix core inputs first |

| Settlement-to-bank match rate | Share of expected settlement or payout items for the period linked to bank deposits, where provider data supports linkage | Ops with finance review | If the rate drops or timing exceptions widen, clear the unmatched queue before changing P&L presentation |

| Post-close adjustment count | Number of journals posted after close, with reason tags | Platform finance | If the same area needs repeated post-close adjustments, treat it as a process defect and remediate the upstream input |

Define each metric so it can be checked#

Make the metric definitions strict enough to survive review. For close duration, use calendar days from initial trial balance to completed consolidated statements. Do not stop the clock when a draft P&L is sent. If the consolidated package is still changing, the close is still open.

For unresolved items, track both open reconciliations and unmatched transactions. Both are measurable backlogs, and carryover matters. Separate items that are new this month from items that survived the prior close.

Make settlement matching an operations metric#

The provider-cash-to-bank rate can surface timing and data-quality issues, so it should not sit only with finance. Payout-to-bank matching can support monthly close, and some provider timing is batch-based. Define the denominator as items expected to reach the bank in-period under that provider's timing logic.

For each unmatched item, keep a checkable evidence pack: PSP batch or payout reference, bank trace or deposit identifier, journal entry, and expected arrival date. Without that, "timing difference" is not practical.

Use adjustments as a quality signal#

Post-close adjustment count is a practical quality signal even though it is not a GAAP or IFRS requirement. Track what changed after close and why. One late journal is not a pattern. Repeated late journals in the same area usually point to weak source mapping or weak matching inputs.

Used this way, the scorecard helps the CFO judge whether results are reliable, where close pressure is building, and whether finance and ops are fixing root causes before the next close.

Where country and program rules can change your approach#

Do not assume one global policy will hold across markets. Reporting choices, payout controls, and compliance steps can change by country, entity, and program, especially in cross-border payments where jurisdictions take different approaches to bank and non-bank PSPs.

| Area | Article note |

|---|---|

| U.S. GAAP basis | In the U.S., the FASB Codification is the authoritative GAAP source. |

| IFRS compliance claim | If an entity claims IFRS compliance, it must make an explicit and unreserved statement of that compliance in the notes. |

| EU authorization | In the EU, payment institution authorization sits with national competent authorities, not one universal approval body. |

| U.S. remittance transfers | In the U.S., remittance-transfer obligations can change when a provider moves from 500 or fewer to more than 500 remittance transfers in the calendar year. There is a transition period not to exceed six months. |

| EU PSD2 records | In the EU PSD2 context, payment institutions must keep appropriate records for at least 5 years. |

| U.S. MSB requirements | U.S. MSB requirements explicitly call for policies, procedures, internal controls, and creating and retaining records. |

Before rollout, two checks should happen:

- Accounting basis: in the U.S., the FASB Codification is the authoritative GAAP source; if an entity claims IFRS compliance, it must make an explicit and unreserved statement of that compliance in the notes.

- Regulatory perimeter: in the EU, payment institution authorization sits with national competent authorities, not one universal approval body.

If you enter a new market or launch a new program type, treat that as a policy review trigger, not just an ops rollout. Apply GAAP or IFRS as applicable, then confirm treatment with qualified finance and legal advisors before locking mapping, disclosure language, or payout-control logic.

A useful red flag is, "We already solved this in another country." That may hold for your internal accounting design, but not for local authorization scope, record retention, or customer-facing payment rules. In the U.S., remittance-transfer obligations can change when a provider moves from 500 or fewer to more than 500 remittance transfers in the calendar year. There is a transition period not to exceed six months. Do not generalize that threshold outside the U.S.

Across jurisdictions, keep operational discipline around:

- traceable records for accounting and compliance

- documented policies, procedures, and internal controls where required

- a clear, enforceable legal basis for material payment activities in each relevant jurisdiction

Keep a market or program evidence pack with the accounting basis used, timing assumptions, governing entity, and retention rule. That control is not cosmetic. In the EU PSD2 context, payment institutions must keep appropriate records for at least 5 years, and U.S. MSB requirements explicitly call for policies, procedures, internal controls, and creating and retaining records. A close may still finish on time without that documentation, but it is much harder to defend later.

Conclusion#

In a Payment business, a strong Income statement is the result of operating discipline, not report formatting. It reflects performance over a period, so it is most reliable when mapping, close rules, and review steps are consistent and repeatable.

Treat the P&L as the output of that discipline. The income statement shows what the business made and spent over the period, while the cash flow statement shows money movement. When those views blur in reporting, decision quality can drop.

Execution starts in the accounting design. Your chart of accounts defines reporting structure, account structures define how accounts and dimensions are entered, and those rules support controlled journal processing. Before publishing, confirm each material P&L line can be explained from recorded entries, reconciled accounts, and documented period assumptions, with unresolved differences clearly surfaced.

Matching comes before final reporting. Financial period closure should run from account reconciliation through statement finalization. Recurring post-close fixes often point to mapping or cutoff logic that needs tightening, not just a team that needs to move faster.

Timing can be a failure point in payments. Some rails run 24x7x365, and the FedNow cycle day is generally 7 p.m. to 7 p.m. ET. If close logic assumes a simple midnight cutoff, avoidable exceptions can follow. Apply one cutoff policy consistently, document judgments, and route late evidence through a defined review process.

Tooling matters, but sequence matters more. Design close processes early in ERP work to avoid bottlenecks, use close workspaces to track ownership, and use journal approval workflows to enforce review thresholds for adjustments.

Start with the fundamentals: align your P&L mapping and Month-end close checklist first, then optimize integrations and ERP automation. A practical baseline is this payment-platform month-end guide, with each task tied to evidence, owner, and decision rule.

When you are ready to operationalize this model across entities or regions, contact Gruv to confirm market and program fit.

Frequently Asked Questions

Is an Income statement different from a Profit and loss statement (P&L)?

No. In common finance usage, an income statement and a profit and loss, or P&L, statement are the same report. It shows how much the business made and spent over a period.

What does an income statement show that a Cash flow statement does not?

An income statement shows period performance. A cash flow statement shows cash moving in and out over that period. For payment teams, those are different views and should not be mixed during close.

How should a Payment service provider (PSP) fee appear in a payment platform P&L?

Start with principal-versus-agent analysis under Topic 606, because that drives gross-versus-net revenue presentation. If the platform is principal, revenue is presented gross. If it is an agent, revenue is presented at the net amount retained. Do not apply a universal PSP-fee placement rule without that analysis.

What is the minimum reconciliation proof needed before publishing month-end numbers?

At minimum, show that transactions were recorded to permit GAAP financial statements and that recorded amounts were compared with related assets, with differences addressed. For close reporting, material provider cash should tie to bank evidence or have documented timing support. Evidence should include corroborating and contradictory information, not only matching support.

How should teams treat late settlements that hit after period close?

Use IAS 10 logic. If a late provider file provides evidence of conditions that existed at period end, treat it as an adjusting event. If it reflects conditions that arose after period end, treat it as non-adjusting.

What should a platform team add beyond a basic accounting-template income statement?

Under IFRS presentation, add notes that summarize significant accounting policies and other explanatory information. For a payment-close package, keep supporting policy, open items, and approvals visible so reviewers can follow the numbers.

When should a finance leader escalate a classification decision to the Chief Financial Officer (CFO)?

This guide does not set a fixed numeric threshold. A practical trigger is when the judgment could significantly affect reported revenue or when the evidence is conflicting rather than one-sided.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- ecfr.gov/current/title-17/chapter-II/part-210/subject...trusted

- ecfr.gov/current/title-17/chapter-II/part-229/subpart...trusted

- gao.gov/assets/gao-25-106679.pdftrusted

- gao.gov/assets/gao-25-107721.pdftrusted

- guides.gaoinnovations.gov/greenbook/2025/principle-10-design-control-a...trusted

- guides.gaoinnovations.gov/greenbook/2025/principle-17-evaluate-issues-...trusted

- investor.gov/introduction-investing/general-resources/new...trusted

- investor.gov/introduction-investing/getting-started/resea...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: