Quick Answer

Choose based on where your operational complexity sits. If your storefront is stable and recurring logic is the pain point, layer billing software; if speed and low engineering lift matter most, an all-in-one subscription ecommerce platform can be the faster start. In either case, lock a decision packet first, including ownership for KYC/KYB/AML, tax documents, and reconciliation exports. Then run migration edge-case tests before signing so margin risk shows up early, not after launch.

Why Billing Gaps Happen in Marketplace Recurring Revenue#

If you treat a subscription ecommerce platform like a checkout add-on, you can make the wrong call. Recurring revenue can change pricing and cash timing, add support work around renewals and plan changes, and require tighter finance coordination before you scale.

The platform is not just where someone buys. It also shapes customer service and how transactions are completed, which is why subscription decisions often spill into account management, billing operations, and reporting. That usually shows up in internal approvals and month-end cleanup.

Before you start#

Step 1: Treat subscriptions as an operating decision, not a feature request. Your first check is whether the team can explain, in plain terms, how renewals, plan changes, failed payments, and cancellation timing affect both margin and workload. If that answer is still fuzzy, do not start with vendor demos. A common failure mode is choosing for front-end speed, then finding out later that support queues, invoice states, or reconciliation exports do not match how the business actually runs.

Step 2: Align founders, product, and finance on what matters. This guide is built for those three groups because each sees a different kind of risk. Product tends to focus on account experience and plan logic. Finance needs clean cash timing, reporting, and enough legal and financial setup to launch without manual patchwork. Founders often focus on growth, but recurring revenue quality can matter more than headline signups if discounts, failed payments, and exceptions start eating margin.

Write down the few outcomes that would make rollout successful. For most teams, that means some mix of cleaner retention behavior, fewer billing surprises, lower support burden, and reporting finance can trust. If you cannot list those now, your comparison later will drift toward feature lists instead of operating fit.

Step 3: Verify coverage directly with vendors before rollout. Features, benefits, and costs vary by provider, so do not assume category labels mean the same thing across products. Even if you are reviewing a familiar vendor, confirm the exact market coverage, responsibilities, and commercial terms that apply to your case. Vendor pages can point you in the right direction, but they are not a substitute for written confirmation on the items that would block launch.

That scope note matters because some coverage depends on market or program details rather than broad product positioning. In practice, the rule is simple: if a capability would affect customer support ownership or finance reconciliation, get it confirmed before implementation starts. This guide is here to help you make that decision with fewer blind spots on operations and margin, not just pick the most polished demo.

Start with the monetization model you are actually running#

Start by mapping how money moves in your model, not by comparing tools, because buyer and seller subscriptions create different operating work.

Step 1: Separate buyer subscriptions from seller subscriptions before you look at tools. A buyer plan mainly changes recurring billing, renewals, cancellations, and account access. A seller plan changes who owes what, when fees are collected, and how payouts and exceptions are handled. If you run both, treat it as a dual model, not a small variation.

Write one plain sentence for each flow: who is charged, what they receive, whether the subscription is cancelable, and what happens on downgrade or non-payment. That alignment matters because some subscription models are cancelable and some are not.

Step 2: Define "win" as operating quality, not just headline MRR. For buyer plans, use retention quality, downgrade behavior, and failed payment recovery. For seller plans, include payout reliability and exception volume. If these outcomes are undefined, vendor review usually drifts into feature demos instead of operating fit.

A practical warning: renewal breakage can matter more than plan setup polish. A practitioner case points to plugin conflicts and failed renewals as real subscription-ops pain points.

Step 3: Lock constraints in writing before vendor calls. Document your cross-border scope, tax-handling expectations, and internal compliance gates you want reviewed. If seller payments are in scope, define your expectation for Form 1099-K reporting support, and keep in mind 1099-K reports gross payment totals, not profit.

If you reference published threshold guidance such as $2,500+ in 2025 sales or some state $600 rules, treat it as a verification item and confirm with primary IRS/state guidance or tax counsel before launch.

For more on handling plans, add-ons, coupons, and dunning, see Subscription Billing Platforms for Plans, Add-Ons, Coupons, and Dunning.

Prepare the decision packet before comparing vendors#

Build the packet before any demo so every vendor is tested against the same evidence, ownership, and failure rules.

- Build a minimum evidence pack from your live stack first.

List the storefront and billing tools still in your path, including dependencies you are not replacing (for example Shopify, WooCommerce, Magento, BigCommerce, and recurring layers like Recharge, PayWhirl, or MoonClerk). Document the edge cases already creating support load, then trace one renewal end to end: storefront event, charge attempt, and ledger/export handoff. If you cannot trace that path clearly, your shortlist is still assumption-driven.

- Document finance, tax, and risk as named ownership decisions.

Replace "do you support compliance?" with explicit requirements: what must happen, who owns it, what triggers it, and where records are stored. If relevant to your model, include KYC/KYB, AML review, VAT checks, and tax form flows (W-8, W-9, Form 1099) as owned items in the packet. If foreign accounts or foreign financial access may apply, add an FBAR note now. FinCEN says maximum account value is a reasonable approximation of the year's greatest value, converted to U.S. dollars, then rounded up to the next whole dollar (for example, $15,265.25 becomes $15,266). Also capture the filing-date split in your packet: some signature-authority filers were extended to April 15, 2027, while other individuals with FBAR obligations remain due April 15, 2026.

- Set integration boundaries before vendors set them for you.

Decide what must be API-first versus admin-managed, and define idempotent, audit-ready handling for renewal creation, retries, plan changes, and status updates. Specify which events need unique IDs, what must be replayable, and which export or log proves final state. "We have webhooks" is not enough if you need replay, deduplication, and reconciliation-grade traceability.

- Write red lines and manual fallback limits in advance.

State unacceptable outcomes directly: duplicate charges, missing renewal events, non-exportable history, or unreconcilable state changes. List required artifacts, such as charge exports, subscription status history, payout/settlement references, and exception logs. Define one manual fallback window up front (for example, tolerable for 24 hours but not multiple billing cycles). Also flag stale authority risk: the IRS retail audit guide excerpt often circulated was published in February 2009 and says "no guarantees are made concerning the technical accuracy after the publication date."

Related: How to Build a Subscription Billing Engine for Your B2B Platform: Architecture and Trade-Offs.

Should you buy all-in-one or layer billing on your existing stack?#

Pick the option that contains complexity where you can operate it reliably. If your storefront and catalog are stable but billing is the pain point, a billing layer is usually the better fit. If your priority is speed with minimal engineering lift, an all-in-one platform can be the better first move.

Step 1: Choose based on where complexity lives#

| Path | Better fit when | Implementation ownership | Operational overhead | Reversibility in 12-18 months |

|---|---|---|---|---|

| Subscription-first platform (for example, Subbly) | You want faster launch and fewer moving parts | More vendor-owned | Lower at first | Often lower if commerce and billing are tightly bundled |

| Billing-first layer (for example, Chargebee, Stripe Billing, Recurly) | Storefront is stable, but billing logic needs more control | More team-owned | Moderate | Often higher if data and account states are portable |

| Storefront plus modules (for example, Shopify + Recharge, WooCommerce plugins, Magento extensions) | You want to keep storefront and add recurring with targeted changes | Shared across team and vendors | Can rise over time | Mixed, depending on data portability |

Use decision rules, not brand preference. If your catalog and storefront change frequently, avoid taking on a second major storefront migration just to add recurring billing.

Step 2: Price the ownership model, not just the category#

If your model includes connected users or payouts, Stripe Connect's pricing ownership model changes your margin math:

| Pricing setup | Ownership note | Listed charges |

|---|---|---|

| Stripe handles pricing for your users | Pricing summary says no fees for your platform | No fees for your platform |

| You handle pricing for your users | You are responsible for Stripe processing fees, including Connect fees | 2.9% + 30¢ domestic cards; 1.5% international cards; 1% currency conversion; $2 per monthly active account; 0.25% + 25¢ per payout sent |

| Managed Payments | Treat as additive when modeling cost | 3.5% per successful transaction, in addition to standard Stripe processing fees |

Step 3: Test migration blast radius before signing#

Before approval, run a real-state migration check for paused plans, upgrades, downgrades, failed renewals, coupon carryover, and reactivation after non-payment. Verify from exports, not screenshots, that each option preserves:

- Customer account state

- Dunning behavior

- Invoicing flow

- Self-serve portal parity

Then score each option on implementation ownership, ongoing overhead, and reversibility in 12-18 months. If two options are close, favor the one with cleaner exports and a clearer rollback path.

For a step-by-step walkthrough, see Building Subscription Revenue on a Marketplace Without Billing Gaps.

Design pricing and packaging around unit economics, not feature menus#

Design pricing and packaging around the unit that reflects customer value and your operating reality, not around the longest feature list. That keeps recurring revenue growth tied to revenue quality instead of hidden margin drag.

Step 1 Anchor the pricing metric to real value and real cost#

Start with the pricing metric: the unit of consumption the buyer pays for. Pair it with the value driver: the part of the offer that creates measurable economic value. When those drift apart, packaging can look attractive up front but weaken economics over time.

Before you finalize packages, map each option to the cost drivers your team actually carries: payment failure recovery effort, support burden, payout complexity, and cross-border settlement friction. If a package only works when teams manually interpret edge cases, it is usually too fragile to scale cleanly.

Step 2 Stress-test package shape before scaling acquisition#

Pricing and packaging should be designed together around value and segmentation. In a subscription model, the package that converts first is not always the one that holds margin and retention later.

| Package shape | Typical pressure point | What to check before launch |

|---|---|---|

| High-frequency, low-ticket | Small renewal value can make operating load more sensitive | Failed-payment handling, support load, and payout exceptions |

| Bundled or heavily tiered | Can support subscriptions and retention, but may reduce ARPU and pressure profitability; revenue upside is uncertain | Eligibility logic, renewal behavior, and discount boundaries |

| Lower-frequency, higher-ticket | Fewer events, but each churn or dispute carries more revenue impact | Downgrade flow, pause/reactivation behavior, and billing-state clarity |

Use a clear tradeoff rule: if discount-led growth increases churn risk, tighten eligibility and renewal logic before expanding acquisition.

Step 3 Treat revenue quality and finance observability as launch criteria#

Packaging is not complete until post-purchase states work cleanly. Check downgrade paths, pause/reactivation behavior, and involuntary churn handling through recurring billing controls before rollout.

For each package, run scenario checks that include a downgrade, pause, reactivation, failed renewal, and discount expiration. Confirm customer-facing state, invoice-state changes, journal-posting consistency, and reconciliation readiness. If those are not reliable, treat the package as unfinished.

For help choosing when subscriptions make more sense than transaction fees, see Choosing Between Subscription and Transaction Fees for Your Revenue Model.

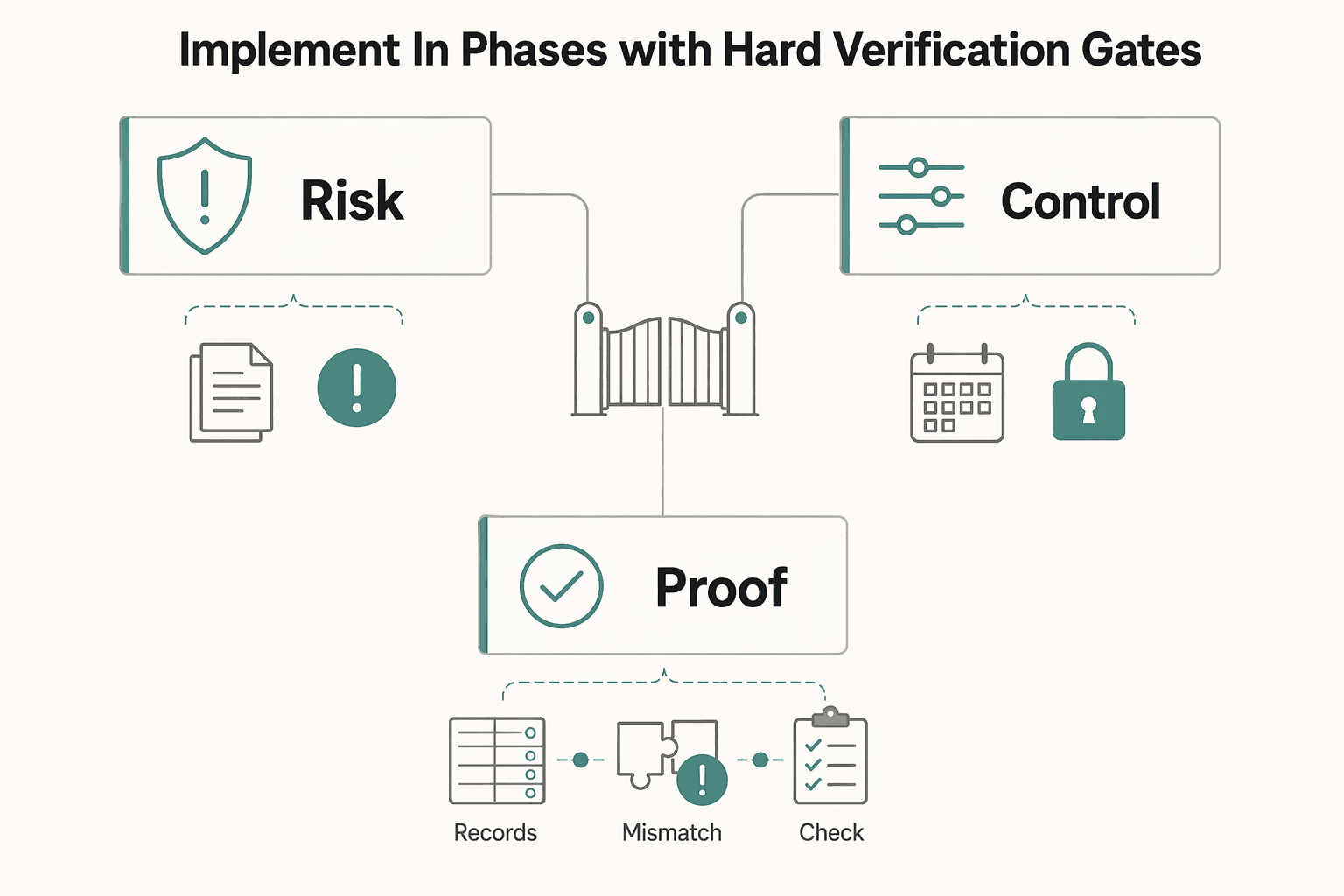

Implement in phases with hard verification gates#

Treat phased rollout as a risk-control tool, not a delivery ceremony. In billing-heavy products, a stage-gate mindset is useful, but it works best when you keep it lightweight and adapt it to a fast-moving team.

| Phase | Scope | Verification focus |

|---|---|---|

| 1 | Launch core recurring billing and account management | Correctness under real-world conditions, clear account and invoice state transitions, and reliable reconciliation paths |

| 2 | Add recovery automation and reporting | Core flows are stable |

| 3 | Expand geography and payout complexity | Earlier phases are consistently verifiable |

In practice, teams usually move through those phases in that order: launch core recurring billing and account management, add recovery automation and reporting once core flows are stable, then expand geography and payout complexity only after earlier phases are consistently verifiable.

Use explicit go/no-go criteria at each gate so product, engineering, and finance can make the same release decision from the same evidence. Keep those checks focused on correctness under real-world conditions, clear account and invoice state transitions, and reliable reconciliation paths.

Keep platform fit in view as scope expands. Subscription stacks are use-case dependent, so what works for a simple recurring model may not hold once you add hybrid usage patterns or more complex money movement.

Keep a rollback path for every phase before you ship it. You should be able to restore subscription state, correct billing records with clear ownership, and send customer communications quickly if a release misbehaves.

Build compliance and tax controls into product behavior#

Make compliance state part of product behavior, not a support cleanup lane. If risky actions can proceed before identity, tax, and reporting status are clear, manual exceptions will scale faster than your controls.

| Control area | What to define | Verification |

|---|---|---|

| Shared compliance state | Tie seller activation, payout access, plan upgrades, and similar actions to explicit KYC, KYB, and AML statuses | Test allowed, pending, restricted, and failed states across UI, API, and admin |

| Tax-document collection | Treat W-8 and W-9 collection as structured product objects with an owner, status, version history, and access controls | Finance can find the current document, prior version, and related account status in one flow |

| Jurisdiction and program limits | State limits in onboarding, contracts, and admin setup screens instead of implying universal VAT validation or global tax coverage | If 1099-K thresholds are mentioned, label them as variable and subject to current IRS/state verification |

| End-to-end audit trail | Use stable IDs across billing events, tax engine responses, provider records, and exports | Review one blocked onboarding, one successful renewal, one tax-document update, and one reportable seller case end to end |

- Gate risky actions with one shared compliance state.

Tie seller activation, payout access, plan upgrades, and similar actions to explicit KYC, KYB, and AML statuses. The key is consistency: the same status should drive UI, API, and admin outcomes. If an account is pending review, it should be limited the same way everywhere instead of relying on ad hoc overrides.

Verification: test allowed, pending, restricted, and failed states, then confirm the same request resolves the same way across surfaces. If payout is blocked in one place but a plan change succeeds in another, you have a control gap.

- Define tax-document collection and handling before launch.

Treat W-8 and W-9 collection as structured product objects with an owner, status, version history, and access controls, not inbox attachments. Set one agreed collection path and one source of truth so finance and compliance can retrieve what they need without engineering involvement.

For Form 1099 workflows, keep the reporting meaning explicit: Form 1099-K reports gross payments, not profit, and Third-Party Settlement Organizations (TPSOs) issue it. Verification: finance can find the current document, prior version, and related account status in one flow.

- State jurisdiction and program limits where users decide.

Do not imply universal VAT validation or global tax coverage if your stack supports only specific markets or program types. Because one source describes ecommerce tax compliance as spanning over 12,000 U.S. sales tax jurisdictions and 190+ countries, limitation copy should appear in onboarding, contracts, and admin setup screens.

If you mention 1099-K thresholds, label them as variable and subject to current IRS/state verification. One practitioner guide cites $2,500+ in 2025 sales, with some states using $600, but that is not universal.

- Require an end-to-end audit trail from request to export.

Each material event should be traceable from the original request to provider reference, ledger posting, and finance export row. Use stable IDs across billing events, tax engine responses, provider records, and exports so case-level reconciliation is possible.

Verification: review one blocked onboarding, one successful renewal, one tax-document update, and one reportable seller case. Finance and compliance should be able to trace each case end to end, not just reconcile summaries.

Common mistakes that kill subscription margin and how to recover#

Most margin leaks come from operating without control, not from revenue growth alone. If your process for choosing, migrating, and running the subscription stack is weak, sales can rise while profitability stays weak.

- Mistake: choosing tools by demos alone. Recovery: run a structured trial on edge cases.

Demos rarely show the exceptions that drive support load and churn risk. Run the same edge-case script across Subbly, Chargebee, and one incumbent-stack option, then score expected versus actual outcomes, self-serve resolution, and downstream finance impact.

- Mistake: treating migration as data copy only. Recovery: reconcile states, history, and entitlements before cutover.

Subscription operations run on a strict cadence, so state errors compound quickly. Validate status, invoicing history, and customer self-serve entitlements with sample accounts before go-live, because trust breaks when customers lose expected access or cannot understand invoice history.

- Mistake: splitting ownership between product and finance. Recovery: assign one cross-functional owner.

Margin decisions need one owner across pricing logic, reconciliation quality, and exception handling. That is how you keep profitability aligned across revenue growth, cost efficiency, and pricing strategy, and how you catch retention tradeoffs when add-ons or bundles boost acquisition but hurt long-term outcomes.

- Mistake: under-scoping abuse controls. Recovery: define checks and operational alerting early.

Put checks in place for trial abuse patterns, repeated low-value authorization attempts, and unusual signup bursts, then route failures to clear alerts with accountable responders. If failures stay buried in logs, you usually discover the issue only after support pressure or renewal performance deteriorates.

Conclusion#

The right choice is the one that keeps pricing logic, billing operations, and finance controls lined up as volume grows. A subscription platform does not win because it has the longest feature list. It wins if you can explain every charge, every status change, and every exception without pulling data from three different places.

That matters because growth alone is not a strategy. Juniper projected the subscription economy could reach $1.2 trillion by 2030, up 67% from a $722 billion 2025 baseline. Even that kind of market expansion does not change a basic truth: not every business is suited to subscriptions. If the model fit is weak, scale just makes the leakage bigger.

- Confirm model scope and success metrics.

Write down whether you are charging buyers, sellers, or both, then define what "good" looks like in operating terms: renewal rate, failed payment recovery, downgrade behavior, support contacts per 1,000 subscribers, and finance close accuracy. The goal is one page that product, finance, and support all read the same way. A common failure mode is optimizing for headline MRR while ignoring churn quality and exception handling costs.

- Finalize vendor comparison with migration and reversibility scores.

If you are deciding between platform options, score them on ownership questions first: who owns pricing logic, who owns invoice truth, and who owns fees and payout responsibilities. Then test reversibility. Verify how you would move active, failed payment, canceled, scheduled change, and grandfathered accounts if you had to switch in 12 months. If that answer is fuzzy, the migration risk is already too high.

- Approve compliance and tax gates with evidence artifacts.

Lock down who handles compliance checks, tax logic, and document collection before launch, not after the first exception queue builds up. Your evidence pack should include invoice history, provider references, ledger exports, and clear data-handling rules for sensitive tax information. A clear red flag is support teams manually overriding blocked actions with no audit trail.

- Pass phased verification before each expansion step.

Do not treat launch as one cutover. Verify sample accounts through core states first, then add recovery automation, then widen geography or payout complexity. Check next charge date, billed amount, invoice trail, proration output, refund behavior after partial use, retry behavior, and rollback steps. If finance cannot reconcile a failed renewal or a scheduled change from the system record alone, stop there.

- Validate economics after launch and adjust packaging before scaling spend.

Compare real results against your assumptions after the first billing cycles: payment fees, support burden, involuntary churn, and recovery rates. Juniper also flagged subscription fatigue as a risk, and highlighted flexible subscription management and bundling as important churn levers. If discounts raise churn or create messy renewal disputes, tighten eligibility and renewal rules before you buy more acquisition.

Keep this checklist close. It is how you avoid mistaking demand for durability. Related reading: How to Calculate and Manage Churn for a Subscription Business.

Frequently Asked Questions

What is the difference between a subscription ecommerce platform and subscription billing software?

A full subscription ecommerce platform can cover storefront, checkout, recurring plans, and customer self-serve in one place. Subscription billing software is narrower. It handles recurring billing and lifecycle actions such as upgrades, downgrades, renewals, and related account changes, while you keep more of your existing stack around it. If your storefront is already working, the billing layer may be the smaller move.

When should a marketplace choose an all in one platform instead of adding subscriptions to Shopify, WooCommerce, or Magento?

Choose all in one when speed to launch matters more than deep control and your recurring model is still simple enough to test with a tight edge-case script. If you already run a stable storefront and expect billing exceptions, seller fees, payout dependencies, or finance-heavy reconciliation, adding subscriptions to the current stack can be safer. A red flag is needing admin-only fixes for routine actions like pause, resume, or failed renewal recovery.

What minimum capabilities are table stakes before launching recurring revenue?

You need reliable recurring billing, customer account management for plan changes, and reconciliation artifacts finance can actually use. At minimum, verify next charge date, amount, invoice trail, and self-serve entitlement behavior on sample accounts before launch. If you cannot explain a failed renewal, a proration, or a refund after partial use from the system record alone, you are not ready.

What usually breaks first during subscription rollout: billing logic, account management, or operational reconciliation?

Operational reconciliation can hurt first because the customer-facing flow can look fine while finance cannot match invoices, status changes, and payouts later. Billing logic can also break early when edge cases like coupon removal or scheduled changes were only demoed, not tested. A useful checkpoint is to compare old and new state for active, failed payment, canceled, scheduled change, and grandfathered accounts before cutover.

What should founders and finance teams evaluate first when choosing between Chargebee, Stripe Billing, Recurly, or Subbly?

Start with ownership boundaries, not feature grids: who owns pricing logic, who owns invoice truth, and who owns payout and fee responsibility. If Stripe is part of the design, the exact Connect model matters. In “Stripe handles pricing,” Stripe says it sets and collects processing fees from your users, and the platform does not incur additional account, payout volume, tax reporting, or per-payout fees. In “You handle pricing,” you are responsible for Stripe processing fees, can collect fees from users, and listed charges include $2 per monthly active account plus 0.25% + 25¢ per payout sent.

How should teams validate pricing, integration effort, and total cost of ownership when vendor pages are vague?

Ask for a line-item quote tied to your model, then test that quote against real transaction paths. For Stripe Standard, for example, the published domestic card rate is 2.9% + 30¢ per successful transaction, but you should not assume one fee line applies across all products, countries, or payment methods. Also check for stacked fees: Managed Payments adds a separate 3.5% fee per successful transaction in addition to standard Stripe payment processing fees, and Stripe states that additional charges apply for subscription payments.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- bsaefiling.fincen.gov/docs/XMLUserGuide_FinCENFBAR.pdftrusted

- fincen.gov/reporting-maximum-account-valuetrusted

- fincen.gov/report-foreign-bank-and-financial-accountstrusted

- irs.gov/pub/irs-mssp/retail_industry_audit_technique...trusted

- stripe.com/connect/pricingtrusted

- stripe.com/pricingtrusted

- support.stripe.com/questions/managed-payments-pricingtrusted

- clarity-ventures.com/subscription-ecommerce-platformexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

How Marketplace Platforms Pay Third-Party Sellers Compliantly

Generic marketplace payout advice usually skips the part that breaks in production. Paying many sellers is not just moving money out. It is deciding who gets paid, when they become eligible, what happens when a buyer disputes a payment, and how finance proves every release later. If you are working on **ecommerce reseller payouts marketplace platforms pay third-party sellers**, this guide is for the marketplace operator, not for solo freelancer banking tips.

How to Build a Subscription Billing Engine for Your B2B Platform

If you are designing a B2B subscription billing engine, get the close and reconciliation model right before you chase product flexibility. A durable sequence is to define recurring billing scope (plans, billing periods, usage, and trials), then map settlement and payout reconciliation to transaction-level settlement outputs, and finally tie that discipline into month-end close controls. The real test is simple: finance should be able to trace invoices, payments, and payouts from source events through settlement records into reconciled close outputs without ad hoc spreadsheet rescue.

How Platforms Detect Free-Trial Abuse and Card Testing in Subscription Fraud

If your platform sells subscriptions while also handling contractor, seller, or creator payouts across markets, this is not just a signup filter issue. It is a control design issue that cuts across risk, finance, legal, compliance, and product. The damage often shows up later in the customer lifecycle, not only at account creation.