Quick Answer

Define your policy first: southeast asia ecommerce marketplace payouts work best when release timing, reserves, reversals, and exception ownership are set before provider selection. After that, map country rails and validate destination behavior, such as PayNow seller details in Singapore and domestic endpoints across Indonesia, Malaysia, Philippines, Thailand, and Vietnam. Use compliance status as a payout-release condition, and require every batch to reconcile from internal payout ID to provider reference to settlement or return.

Southeast Asia ecommerce is now large enough that payout design is no longer a back-office detail#

Southeast Asia ecommerce is now large enough that payout design is no longer a back-office detail. Antom describes the region's ecommerce market as being valued at nearly USD $100 billion and growing at over 10% annually. Citi estimates Southeast Asia cross-border ecommerce reached about $17 billion in 2024, or more than 11% of regional online sales. Those are different metrics, but they point to the same operating reality: money is moving at meaningful scale across more sellers, markets, and payment paths.

A lot of published material focuses on the buyer side. You will find plenty on checkout acceptance, wallets, and local payment preferences, but far less on what happens after the order is approved. That gap matters because seller disbursement choices affect real outcomes: when funds are released, what gets held back, which exceptions create support tickets, and whether finance can reconcile payouts without a month-end scramble.

This guide focuses on that gap. It is not about abstract payment trends. It is about the layer between collected funds and seller cash access: payout timing, reserves, compliance gates, reversals, and reconciliation. Get those decisions wrong and margin leaks through failed disbursements, manual reviews, refund confusion, and avoidable seller frustration. Get them right and you can usually reduce support load while making payout status clearer, without promising speed you cannot reliably deliver.

The regional complexity is real, but it is still manageable. The 2C2P and IDC digital payments brief draws on merchant research across six Southeast Asian markets: Indonesia, Malaysia, Philippines, Singapore, Thailand, and Vietnam. For operators, that is a useful planning frame. You do not need six completely different payout products. You do need clear rules on what stays standard across all markets, such as release policy, evidence requirements, and reconciliation controls, and what must be localized by country, such as rail endpoints, return handling, and some verification checks.

If you are building or refining a marketplace in these markets, start with a simple rule: standardize your control logic first, then localize how money actually moves. Before you promise faster seller access to funds, verify that you can track payout requests from provider references through settlement posting and that you have a defined response for returned or delayed transfers. The rest of this guide builds from that premise. Payout architecture is not a technical afterthought. It is part of your margin model, your seller experience, and your ability to scale without losing control.

If you want a deeper dive, read eCommerce Reseller Payouts: How Marketplace Platforms Pay Third-Party Sellers Compliantly.

Define the payout model before you pick providers#

Lock your payout policy first, then choose providers. Marketplace payouts are seller disbursements after funds clear and your platform applies release timing, fees, reserves, and reversals. That is different from checkout acceptance methods like mobile wallets or Buy Now, Pay Later.

| Step | Action | Article detail |

|---|---|---|

| 1 | Define | release timing, reserve logic, and reversal rules |

| 2 | Map | those rules to rail options in Indonesia, Philippines, Malaysia, Singapore, Thailand, and Vietnam |

| 3 | Confirm | each provider can support accurate settlement and reconciliation, including clear handling of returned transfers |

Provider coverage and payout control are not the same thing. A payment API is the protocol between your software and a processor, and Southeast Asia coverage is fragmented by country across local rails and wallets, including PayNow, DuitNow, GCash, and Maya. That tells you where money can move, not when sellers should receive it.

Domestic Payments and Real-time Payments describe rail behavior and speed, not your risk policy. In wallet-first economies, faster and more predictable transfers can raise expectations, but your policy still decides what gets released, held, or reversed.

Related: How to Pay Contractors in Southeast Asia: Philippines Indonesia Thailand Vietnam.

Why payout architecture matters more after the shift away from cash#

Once orders are prepaid, payout design stops being plumbing and starts shaping margin and control. Risk that used to sit in doorstep collection and delivery exceptions moves into seller release timing, reserve logic, and reconciliation quality.

In Southeast Asia, this is now a core operating issue, not an edge case. IMF staff report that ASEAN countries have made significant progress in domestic and cross-border digital payments, with preliminary evidence of benefits from stronger regional payment connectivity. Citi also estimates Southeast Asia cross-border ecommerce reached $17 billion in 2024, or more than 11% of online sales.

At that scale, the hard question is less "Did we collect the money?" and more "When can we safely release the seller share, and can we reconstruct the trail if something breaks?" Citi's March 2025 survey of 600 cross-border shoppers in Singapore, Indonesia, and Thailand reinforces how often cross-border flows span multiple ledgers, providers, or jurisdictions before funds land with the seller.

That is why payout clarity matters as much as payout speed. Your status model should map to real events such as funds cleared, reserve applied, payout submitted, payout paid, payout returned, and payout reversed. Before you scale, run a full payout batch and verify each seller payment against three records: your internal ledger entry, the provider transfer reference, and the settlement posting.

Treat payout architecture as a unit-economics lever, not a checkout add-on. Release timing, reserves, and reconciliation quality all affect downstream operating cost and cash control, especially in cross-border volume. You might also find this useful: How a Logistics Platform Scaled Driver Payouts Across Southeast Asia.

Localize rails by country but standardize controls#

Your safest scaling pattern is one payout control plane with country-local endpoints. Across Southeast Asia, local payment methods and e-wallets are described as dominant, with heavy use of QR payments, bank transfers, and mobile wallets, so a single cross-market payout route is usually a weak fit.

Keep the internals consistent across markets: ledger mapping, reserve logic, payout states, approvals, and reconciliation checks. Localize only the destination rail layer by country, and require pilot validation before you accelerate release windows.

Singapore is the clearest grounded example. PayNow is a real-time transfer rail, widely used for personal and business transactions, and supports addressing by mobile number or UEN. If Singapore is in scope, collect and validate seller UEN details during onboarding and before first payout.

| Country | Rail decision | What to verify before scale |

|---|---|---|

| Singapore | PayNow where seller profile supports it | UEN/mobile destination mapping, event-to-status mapping, and return/reversal handling |

| Malaysia | Primary domestic rail selected with your provider | Coverage for your seller destination types, event reliability, and payout-return handling |

| Philippines | Primary domestic rail selected with your provider | Coverage for your seller destination types, event reliability, and payout-return handling |

| Indonesia | Primary domestic rail selected with your provider | Coverage for your seller destination types, event reliability, and payout-return handling |

| Thailand | Primary domestic rail selected with your provider | Coverage for your seller destination types, event reliability, and payout-return handling |

| Vietnam | Primary domestic rail selected with your provider | Coverage for your seller destination types, event reliability, and payout-return handling |

When entering a new market, launch with one primary domestic rail and one fallback path. Shorten payout windows only after both are proven in live or pilot flows. Indonesia is a useful reminder: reported preferences include e-wallets and bank transfers, and mobile commerce is estimated at about 70% of e-commerce transactions, so verify local fit before assuming a card-first setup. If you cannot confirm rail coverage, reliable events, and return handling in-country, delay broad seller onboarding. For a related read, see How Blockchain and Smart Contracts Will Change Marketplace Payouts by 2030.

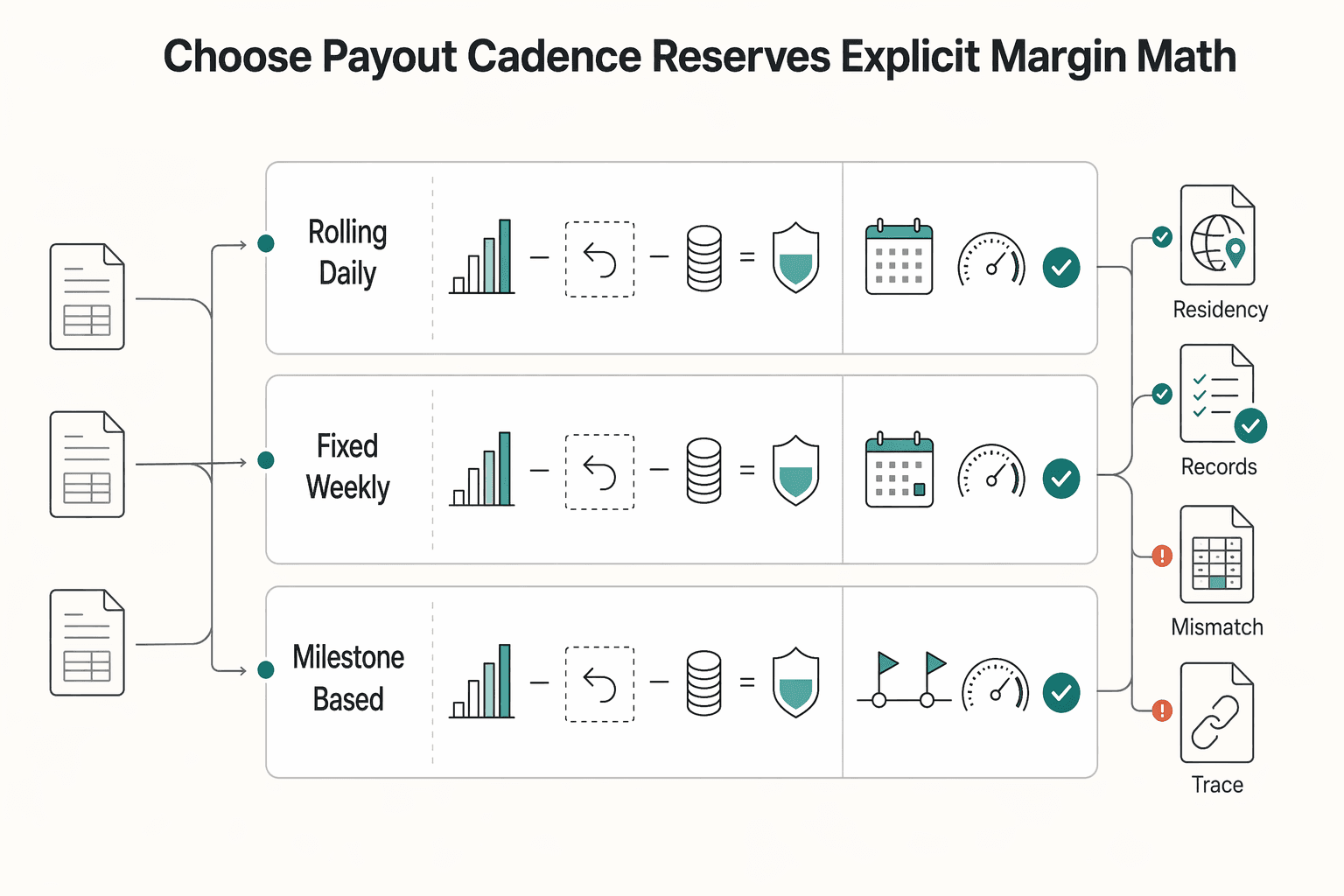

Choose payout cadence and reserves with explicit margin math#

Set payout cadence as a margin-control decision first, then position speed as a seller benefit within those limits. In a market where competition is tightening and digital performance is uneven across countries and firm sizes, one payout promise for every seller can hide real risk.

Model each cohort before you change release speed: what comes in, what may need to be returned, what it costs to process payouts, and what remains exposed before and after reserve release.

| Payout model | Typical use case | Seller trust implication | Finance workload implication |

|---|---|---|---|

| Rolling daily | Established, lower-risk cohorts with stable payout and refund patterns | Fast and predictable when execution is clean | Highest operational tempo for exceptions and reversals |

| Fixed weekly | Broad middle-risk cohorts where predictability matters | Clear expectations when cut-off and release rules are explicit | More manageable review and reconciliation cycles |

| Milestone-based release | New, higher-risk, or delayed-fulfillment cohorts | Can feel restrictive unless milestones are transparent | More policy setup, tighter exposure control |

Do not apply one reserve policy across Indonesia, Thailand, and Vietnam without your own operating evidence. Set reserve logic by seller risk cohort and product category, then update it as your refund, dispute, and payout-failure patterns become clear.

If seller churn is high, shorten cadence first for low-risk cohorts. If dispute costs are rising, tighten reserve release conditions before you promise faster payouts.

Define one written liability rule for refunds and chargebacks so reversals do not get handled ad hoc in support tickets. Make the recovery path explicit, for example debit balance, net from future payouts, reserve-only release, or temporary hold, and require consistent reversal records in your ledger.

We covered this in detail in How to Build a SaaS Marketplace That Manages Subscriptions and Contractor Payouts.

Put compliance gates in the payout path, not around it#

Once cadence and reserves are set, make compliance a hard payout-release condition, not a side review. Keep the rule explicit: no compliant status, no payout release, and any exception must be auditable, time-bound, and tied to a named approver and reason.

Gate the release event#

Run compliance checks at the payout decision point, not only at onboarding. Validate that the seller's current approval status still matches the current payout destination details, especially after destination changes, so you do not release funds on stale approvals.

If your program supports destination-account matching, use it as part of release controls instead of relying on manual support catch-up later.

Split seller activity from payout eligibility#

Do not use one switch for onboarding and payout. Keep separate states for operating, accruing balance, and receiving payout so you can pause disbursements without shutting down all seller activity.

This structure fits the region's reality: e-commerce tax rules are country-specific across Southeast Asia, so one regional pass flag is weak control. Thailand is a useful reference point because payment activity is treated as regulator-intensive, the licensing model is layered by service type and operating scale, and applicants are expected to show financial stability, technology and cybersecurity readiness, and customer protection.

Keep country evidence explicit#

For the Philippines, Indonesia, and Thailand, keep a country-level record that is visible and operational, not buried in tickets.

| Country | Evidence record to maintain | Core status fields | Owner | Escalation target |

|---|---|---|---|---|

| Philippines | Program-required documents and payout-destination evidence | compliance status, payout hold reason, last review date | Named compliance or payments ops owner | Internal, documented, and queue-visible |

| Indonesia | Program-required documents and destination verification evidence | compliance status, destination verification status, exception age | Named compliance or payments ops owner | Internal, documented, and queue-visible |

| Thailand | Program-required documents plus notes aligned to service type and scale | compliance status, legal/compliance review flag, payout eligibility | Named compliance or legal owner | Internal, documented, and queue-visible |

When you approve an exception, store the full case record: what was missing, who approved, expiry date, and what must be completed before the next release. For a related operating-control discussion, read How Small Teams Can Outsource IT Work in Southeast Asia Without Losing Control.

Reconciliation discipline is the real scale constraint#

After compliance gates are in place, reconciliation is what proves your payout controls actually hold at scale. Keep your internal ledger as the source of truth, and trace every payout batch from instruction, to provider reference, to final settlement or return posting.

At low volume, teams can patch gaps with dashboards, CSV exports, and inbox explanations. At scale, that breaks the close process. If finance cannot reproduce payout totals and fee attribution from internal records plus provider statements, without ad hoc spreadsheet stitching, control is still incomplete.

Make the ledger win every dispute#

Your ledger should connect three points for every batch: what you intended to send, what the provider acknowledged, and what in the end settled or failed. If any link exists only in email threads or manually renamed files, month-end turns into case reconstruction.

| Checkpoint | Detail | Record |

|---|---|---|

| Instruction | what you intended to send | internal ledger |

| Provider acknowledgement | what the provider acknowledged | provider reference |

| Settlement result | what in the end settled or failed | final settlement or return posting |

Provider acceptance is not the finish line. The real checkpoint is whether finance can tie batch totals, seller credits, returns, and net cash movement back to the ledger without manual gap filling.

Build a real month-end close checklist#

At close, force unresolved payout money into view:

| Item | Detail |

|---|---|

| open payouts | created but not fully settled |

| returned payouts | needing seller-balance correction or retry decisions |

| credits or debits | unmatched on bank or provider statements |

| pending reversals | not yet posted to seller balances |

| exception aging | by country |

Be strict about source quality#

Market and vendor reports are useful context, not control-grade evidence. Treat summaries from 2C2P, Antom, and "How Southeast Asia Buys and Pays" as directional inputs.

Apply the same standard to broader regional research. The e-Conomy SEA research programme, launched in 2016, with Bain as lead research partner from 2019, states its material is for informational purposes over a limited period and includes no warranty on accuracy or completeness. Use these reports to frame decisions, then validate your own payout data path through reconciled records, statement matching, and documented exceptions. This pairs well with our guide on Legal Marketplace Payouts: Trust Accounts and ABA Compliance.

Design an exception lane before volume forces one#

Design the exception lane now, before volume turns routine issues into an expensive queue. As demand scales and operations get more complex, the risk is not the happy path. It is unresolved payout exceptions that get handled inconsistently.

Published market context points to rising operational complexity, but it does not give you a universal retry taxonomy to copy. Build a simple internal model and keep it consistent across product, ops, and finance: each exception type should have one owner, one required next action, and one clock.

Keep the lane auditable in your ledger and queue from day one. Every exception record should carry the original payout ID, provider reference when available, current status, retry count, last action owner, and reason code. If these details live in chat threads or inboxes, the lane will fail under pressure.

Only automate fallback paths you can prove end to end. If you cannot reliably distinguish route-level outcomes and feed return events back into clean reversal or retry handling, keep that flow in controlled manual review until it is production-safe.

Conclusion#

The practical answer is to treat payouts as both a trust workflow and a margin-sensitive workflow. The platforms that age well are usually not the ones that move money fastest by default. They are the ones that standardize controls, localize rail choices, and can explain every release, hold, retry, return, and reversal after the fact.

That matters because the region is large enough for payout mistakes to become a finance problem quickly. The e-Conomy SEA 2025 excerpt says ASEAN is on track to surpass $300 billion in GMV by 2025, with over 60% of all payments already digital. That does not tell you what cadence or reserve policy to use. It does make one point hard to ignore: once volume rises, weak payout design can move from a back-office nuisance into a broader finance and operations risk.

A final scope check is worth keeping in mind. The recurring 2C2P and IDC InfoBrief has run since 2021 and, in the cited excerpt, covers six markets: Indonesia, Malaysia, Philippines, Singapore, Thailand, and Vietnam. It includes 600 enterprise-merchant respondents, with 65% identified as primary payments decision leaders. Use that as directional evidence for the six-country operating picture, not as proof that one payout policy fits every ASEAN market.

If you are tightening your next-quarter plan, do not start by debating providers. Start with the operating choices you will need to defend later:

- Define payout and hold logic in writing. Document release timing, hold conditions, and override authority so decisions are consistent and auditable.

- Document primary and fallback payout rails for each market in scope. For the six markets above, define expected status behavior and how failed or returned payouts are handled.

- Keep compliance gating explicit where required. If your program requires current verification or policy checks, make payout release depend on that status and track exceptions clearly.

- Build an exception lane before volume forces it. Separate major failure types and assign ownership so operational handling is traceable and repeatable.

- Make reconciliation a release gate, not a month-end rescue task. Ensure each payout can be traced from internal ID to provider reference, amount, and final settlement or return status.

Related reading: How to Choose a Reliable Southeast Asia Fintech Setup for Cross-Border Work.

Frequently Asked Questions

What are marketplace payouts in Southeast Asia, and how are they different from checkout payment methods?

In this section, marketplace payouts refers to seller disbursements after checkout, while checkout methods are buyer-facing ways customers pay online. The grounding evidence supports the checkout side: ecommerce payments are digital transactions in an online store or platform, and payment solutions let businesses accept digital methods. Keeping these as separate layers helps avoid design confusion.

How often should a marketplace pay sellers in Southeast Asia?

Checkout behavior varies by country and a one-size-fits-all international gateway can fall short. Confirm the right payout cadence with your payment provider and local market requirements.

Which payout model best balances seller retention and dispute risk?

Treat the choice of payout model as an internal policy decision based on your own risk, finance, and operational data.

What is the difference between domestic payout rails and cross-border disbursement rails?

The evidence here supports that cross-border digital payment solutions can accept multiple Asian wallets through one integration. It does not establish how domestic vs cross-border seller disbursement rails perform for payout reliability, failure handling, or reconciliation.

What data is required to reconcile marketplace payouts at scale?

Any mandatory fields or controls should come from your provider requirements and internal finance processes.

How should we localize payout rails across Singapore, Malaysia, Philippines, Indonesia, Thailand, and Vietnam?

Start from what is evidenced for checkout behavior: preferences are local, with examples including PayNow in Singapore, DuitNow QR or GrabPay in Malaysia, and GCash or InstaPay in the Philippines. The pack also indicates a one-size-fits-all international gateway can fall short. Use that as checkout guidance only, not as proof of the right seller-payout architecture in each country.

What should be checked before enabling faster payout windows for new seller cohorts?

Confirm payout release thresholds, reserve percentages, and operational SLA benchmarks with your payment provider and internal risk team before enabling faster payout windows for new seller cohorts.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- documents1.worldbank.org/curated/en/149301574840045883/pdf/Unleashing...trusted

- euro.ecom.cmu.edu/resources/elibrary/epay/whos-who-in-payments...trusted

- home.treasury.gov/system/files/246/2026-NMLRA.pdftrusted

- imf.org/-/media/files/publications/selected-issues-p...trusted

- oecd.org/en/publications/local-retail-global-trends_5...trusted

- scholarcommons.sc.edu/cgi/viewcontent.cgitrusted

- sec.gov/Archives/edgar/data/2047190/0001493152240505...trusted

- sec.gov/Archives/edgar/data/1099590/0001099590260000...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How Marketplace Platforms Pay Third-Party Sellers Compliantly

Generic marketplace payout advice usually skips the part that breaks in production. Paying many sellers is not just moving money out. It is deciding who gets paid, when they become eligible, what happens when a buyer disputes a payment, and how finance proves every release later. If you are working on **ecommerce reseller payouts marketplace platforms pay third-party sellers**, this guide is for the marketplace operator, not for solo freelancer banking tips.

Southeast Asia Contractor Payouts Across Philippines, Indonesia, Thailand, and Vietnam

Treat Southeast Asia as four separate launch decisions, not one regional rollout. If you approach the Philippines, Indonesia, Thailand, and Vietnam with a single APAC payout template, you can create avoidable rework in compliance, rail selection, and reconciliation.

How a Logistics Platform Scaled Driver Payouts Across Southeast Asia

Redesigning driver payouts is rarely just a payments project. For a logistics platform, it is often a margin decision hiding inside an ops problem. Do you fix driver uncertainty first, settlement speed first, or manual finance work first?