Quick Answer

Legal marketplaces can use electronic payments only if payout design is built around professional duty, jurisdiction-specific trust-account rules, and retrievable evidence before launch. Choose the money movement model before the processor, define who gets paid from which account, hold ambiguous cases for review, and require documented approvals, reconciliations, and launch gates for each jurisdiction.

How Trust Accounts Affect Legal Marketplace Payouts#

Treat payout design as a launch gate, not a checkout feature. Electronic payments are part of today's legal marketplace, but you still need to decide early who controls funds, what records you keep, and which trust-account questions need jurisdiction-specific answers before go-live.

If your platform may move money among clients, attorneys, firms, or third-party payers, the main risk is not the payment rail itself. The harder task is showing that the fund flow, approvals, and disclosures stay aligned with the lawyer's duty to the client while reducing avoidable trust-account risk.

Step 1 Start with professional duty before payment speed#

A third-party payer does not change who the lawyer serves. In the legal-finance framing, the lawyer's duty still runs to the client regardless of who pays, so your product and operations choices should reflect that from the start.

In practice, pressure-test any flow where a third-party payer could receive more client information than necessary or shape payment timing in ways that affect service delivery. Where third-party payment exists, design consent and confidentiality choices deliberately. Informed consent is a practical checkpoint for deciding what to collect and when to share client information.

Step 2 Verify the source material you are actually using#

Your baseline should be current and verifiable. The CFPB published a rule on general-use digital consumer payment applications on 12/10/2024 (89 FR 99582), which is relevant context for marketplace payment design.

That is context, not a substitute for legal-practice or trust-account guidance. When you use FederalRegister.gov, check the official PDF or printed version for legal or compliance review, because the site's XML presentation is informational and should be checked against an official edition.

Step 3 Define what you must prove before go live#

Set your proof standard before launch, not after the first transaction. We use this guide as a control framework, not a universal legal conclusion. It gives you a path for choosing a payout model, spotting risk, and capturing the evidence you will need.

Build that evidence trail up front: consent records, payout approvals, ledger history, and exception handling for disputed or edited payments. The ABA's updated civil legal aid standards point organizations to external guidance governing legal practice, which is a useful posture for founders working across payments rules, legal-practice duties, and jurisdiction-specific trust guidance.

Step 4 Use clear go or no-go gates#

Go-live should be evidence-based. If you cannot explain why a payment route exists, who approved it, what client-facing disclosures support it, and which sources back it, that flow is not ready.

The rest of this guide follows that order: payout model first, evidence second, then market-by-market launch gates so you can scale without retrofitting compliance after money starts moving.

For a closer look at referral fees and trust accounting, see Legal Marketplace Payouts: Attorney Referral Fees Trust Accounting and Compliance.

What to prepare before you build payout rails#

Write down your policy inputs and evidence checklist in Gruv Docs before you build processor logic. The goal is to separate what is known from what is still unresolved, so you do not hard-code a payout path that later conflicts with account-handling assumptions or role definitions.

Step 1 Define scope in writing#

Start with a plain-language scope sheet for users, funds, and accounts. List how you label participants, for example attorneys, paralegals, firms, and other providers, then note where account-routing treatment is still unresolved.

Treat ambiguity as an explicit open item. If a role or fund type is unclear, mark it unresolved instead of forcing it into one bucket.

Step 2 Gather legal and policy inputs first#

Build your legal and policy foundation before product specs. At minimum, collect the professional-conduct and state-bar materials you plan to review for launch jurisdictions.

Do this early because state-level lawyer regulation is uneven and the depth of guidance varies by jurisdiction. Keep a simple source register in Gruv Docs with jurisdiction, publication date, and document type, and track definitions, data sources, and limitations as part of intake.

- jurisdiction and exact source title

- publication or update date

- document type and authority level

- open questions that still need counsel review

Step 3 Clarify owners for controls and incidents#

Before implementation, document who approves payout-rule changes, handles incidents, and reviews your reconciliation approach.

Use a simple readiness check: every control has a primary owner and a backup.

Step 4 Create a minimum evidence pack template#

Create a lean evidence-pack template now. Include the records your team will rely on to reconstruct payout decisions and transaction history.

Run one mock transaction through the template before launch so you can confirm the evidence trail is complete and reconstructable.

Choose your money movement model before you choose a processor#

Choose the model based on fund-flow exposure first, then choose tooling. If your platform may touch client funds, treat control design as a gate and verify it with records before you optimize for payout speed.

Step 1 Score the model before vendor selection#

We use this as an architecture scorecard, not a legal conclusion.

| Model | Platform fund-flow touchpoint (working assumption) | Operational complexity | Launch speed | Exception and audit burden | Third-party payments handling | Founder read |

|---|---|---|---|---|---|---|

| Platform-directed payouts | Often higher when the platform is in routing/holds | High | Medium early, slower after controls | Higher, because more review paths sit with the platform | More edge cases to document and approve | Use only if you can sustain review operations and control evidence |

| Firm-directed payouts | Often lower when firms control routing/account selection | Medium | Medium to high | Lower for the platform, but dependent on firm execution quality | Simpler for the platform if firm-side evidence is reliable | Practical lower-exposure launch path for many teams |

| Hybrid routing | Mixed by flow branch | High | Medium | High, because branch logic increases reconciliation and review paths | Flexible, but rule-heavy | Useful for mixed matter types only when routing rules are explicit and testable |

The practical rule is simple: as platform touchpoints increase, exception handling and audit work can increase too. Test each model on paper first. Trace the payer, holding point, beneficiary, route owner, assumed account role, and where timestamped evidence lives. If you want to pressure-test that mapping, use a trust-accounting case study before live volume.

Step 2 Match the model to client-segment economics#

Client type changes operating pressure, not just positioning. The OCTOBER 2024 California legal market update describes a structural divide between PeopleLaw and organizational clients, and it flags both client-type economics and data limitations as checkpoints.

For PeopleLaw, price pressure can be tighter, and the report notes that more consumers may forgo legal services when affordable options are not available. That can favor simpler launch operations, but it does not remove money-movement risk.

For organizational clients, the same report describes coping patterns such as higher law-firm rates, legal-ops investment, and work diversion to ALSPs. It also references a 2018 finding that three-quarters of law firm receipts came from organizational clients. In practice, that can support more structured routing and documentation if buyers expect it.

Step 3 Separate vendor narratives from control evidence#

Vendor pages can help you map options, but they are not proof that your design works. They can inform workflow patterns. They do not validate your routing logic, approvals, or evidence chain.

Before processor selection, run a mock exception case, for example a recipient change after intake or a payer different from the beneficiary. Confirm you can reconstruct the original request, the change event, the approver, the final route, and the reason, all with timestamps.

Step 4 Choose the burden you can operate consistently#

Every model decides where the operational burden lives. Platform-directed centralizes control and cleanup. Firm-directed reduces direct platform touchpoints but relies on firm-side discipline. Hybrid gives you flexibility, but it adds policy branches.

Start with the model that keeps direct platform fund handling narrower unless your product requires otherwise. If you cannot avoid those steps, narrow scope, document routing rules in plain language, and prove reviewability before you pursue faster payouts in a legal marketplace payout program.

Define who gets paid from which account and why#

Define the payout matrix before live transactions begin so the same fact pattern gets the same route every time. That also keeps trust accounts from becoming the default route.

Step 1 Classify payees into internal roles before you map account paths#

If you use internal buckets (for example, attorney, paralegal, and non-legal service provider), treat them as payout-control labels, not legal conclusions about universal eligibility by role.

For each role label, document the default review lane and the allowed account path in your policy: trust account, operating account, or hold pending review. For each route, keep a minimum record of the role label, proposed funding source, rationale, and approver or policy reference so an auditor can trace why that path was used.

Step 2 Write a clear routing rule tied to IOLTA account duties#

Set a clear boundary: do not use trust accounts as a catch-all when ownership or entitlement is unclear.

Jurisdiction-specific guidance should drive escalation rules. In Washington, WSBA IOLTA guidance, updated Jan. 9, 2024, says lawyers must take reasonable steps to locate the person for whom funds are held, and if the person cannot be found, the funds are handled under RCW 63.30.

Step 3 Hold ambiguous cases instead of defaulting from a trust account#

When role classification or ownership is unclear, a conservative approach is to put the payout on hold until review resolves the route. That is slower, but it can reduce unsupported trust-account movement and cleanup later.

Each ambiguous case should end in a documented release decision or a documented continued hold with a named owner. If review identifies unidentified funds or an unlocatable owner, move the case to jurisdiction-specific unclaimed-property handling rather than normal payout processing.

Step 4 Link policy text to transaction evidence for auditability#

Route rationale should be visible in each payout record, not just in policy documents. Store the policy version, route code, chosen account type, reviewer, and supporting records so an audit can map policy text to transaction behavior.

Use external legal and accounting guidance as part of control design and review. Operationally, keep monthly trust-account reconciliations as the core control, and treat every six (6) month outstanding-check reviews as supplemental, not a replacement.

Build the minimum compliance controls before first live transaction#

Make compliance controls operational before go-live, not just policy statements. Assign individual accountability, require an entity-level control gate, and define what happens when controls fail.

A practical baseline is the governance logic from California's June 29, 2001 MDP Task Force: preserve professional core values through continued individual accountability and a required certification process, with enforceable consequences for noncompliance.

Step 1 Assign named accountability for each control#

Set control ownership at the person level, not only the team level. For each control, define who approves, who monitors, and who can stop the process when requirements are not met.

Step 2 Require a pre-launch certification gate#

Treat launch readiness as a certification decision, not an informal signoff. Document the required checks, confirm they are complete, and block launch if any required check is incomplete.

Step 3 Keep control-linked evidence, not detached policy claims#

Store approval and review evidence where operators can trace decisions to specific control checks. If evidence is missing or cannot be matched to the control decision, keep the flow unresolved until records are complete.

- control owner and backup

- latest approved configuration or rule version

- sample record showing the control fired

- exception-path record if the control blocks release

Step 4 Define enforcement consequences in advance#

Set explicit consequences for noncompliance before the first live transaction, including the ability to suspend affected operations until remediation is complete. That mirrors the report's decertification logic: controls are credible only when noncompliance triggers enforceable operational action.

Operationally, this fits current market pressure for stronger legal operations discipline in data, process, and technology (October 2024). If controls are not provable in records, they are not reliable in production.

Handle third-party payments without ethics drift#

Third-party-funded matters should have a separate review lane from ordinary client payments. We treat that lane as an ethics control, not just a routing label.

Step 1 Separate the lane at intake#

Classify third-party-funded payments at intake and keep that flag visible in payment, ledger, and payout review records. Late tagging can make ethics review harder because decision history is less clear.

Step 2 Require documented ethics checkpoints before release#

Model Rules and state counterparts can differ, so treat your sequence as an internal control standard rather than a universal legal formula. Require matter-linked ethics review records before you make disbursement decisions, and keep each record attributable and time-stamped.

For policy design evidence, log which formal materials were reviewed, for example ABA Formal Opinion 465 (Oct. 21, 2013) and Pennsylvania Bar Association Formal Opinion 2014-300 when relevant.

Step 3 Keep payer visibility within confidentiality boundaries#

Third-party funding does not remove confidentiality duties. Ethics rules are aimed at protecting clients, the legal system, the public, and justice, and competence expectations include protecting confidential information from cybersecurity threats.

As an internal control, expose only the payment-level fields needed for payment confirmation unless counsel approves broader access, and verify role-based payer access before launch.

Step 4 Use a hard operational stop for incomplete records#

Set a clear internal rule: if required ethics documentation for that matter is incomplete, pause payout actions in that trust-account-related lane until the record is complete and reviewed. This is a control decision to prevent ethics drift, not a claim that every jurisdiction imposes the same mandate.

For a practical example of compliant payouts to legal service providers, see How Legal Platforms Pay Interpreters and Court Reporters.

Design fee and dispute flows that do not contaminate trust funds#

Make those choices explicit controls.

The grounding for this section does not provide rule text that resolves chargebacks, reversals, partial refunds, or processor fee debits. Use the steps below as internal control design, not as a claim that one ABA or IOLTA provision answers every case.

Step 1 Predefine the fee source before the first transaction#

For each payment path, decide up front where processor fees are funded and encode that as a product rule. If funds are unearned or otherwise protected, consider designing the flow so fees come from a non-protected source, for example a designated operating balance, reserve, or separate platform charge, rather than silent netting on the client side.

Run an end-to-end test from authorization through payout prep and confirm fees post to the intended source. Default net settlement behavior can create balance drift if it is not explicitly tested.

Step 2 Route disputes by fund type, not only by payment method#

When a dispute involves funds that may still be protected, pause automated downstream movement on that amount and require documented review before release. Keep matter context attached so the decision is traceable.

In that review, focus on ethics risks that are actually grounded: who pays does not change the lawyer's duty to pursue the client's objectives, informed consent should govern information sharing with potential funders, confidentiality remains in scope, and funders should not interfere with independent professional judgment. The source also indicates these concerns are often overstated and does not offer a single easy answer.

Step 3 Record reversals and corrections as auditable journal events#

Post each reversal, correction, or refund as its own linked journal event instead of fixing balances in spreadsheets. Keep a clear chain from original posting to exception to final correction across trust-account and operating-account paths.

Store identifiers, timestamps, account classification, reason, approver, and hold or release actions so reconciliation and investigations can rely on the ledger itself.

Step 4 Test failure scenarios before launch#

Before go-live, run failure cases likely to break fund separation:

- duplicate disputes on one payment

- late reversals around payout timing

- partial refunds that span protected and operating-account amounts

For each case, verify that protected balances are not reduced by automatic netting, cross-account offsets get a documented decision, and the resulting delta is explainable from journal events alone. Rule 1.5 (fees) and Rule 1.8 (conflicts) indicate these are distinct professional-responsibility topics, so controls should stay explicit and reviewable.

Set jurisdiction gates before multi-state or cross-border rollout#

Gate each jurisdiction independently, and keep any market in research-only status until its legal and tax unknowns are closed.

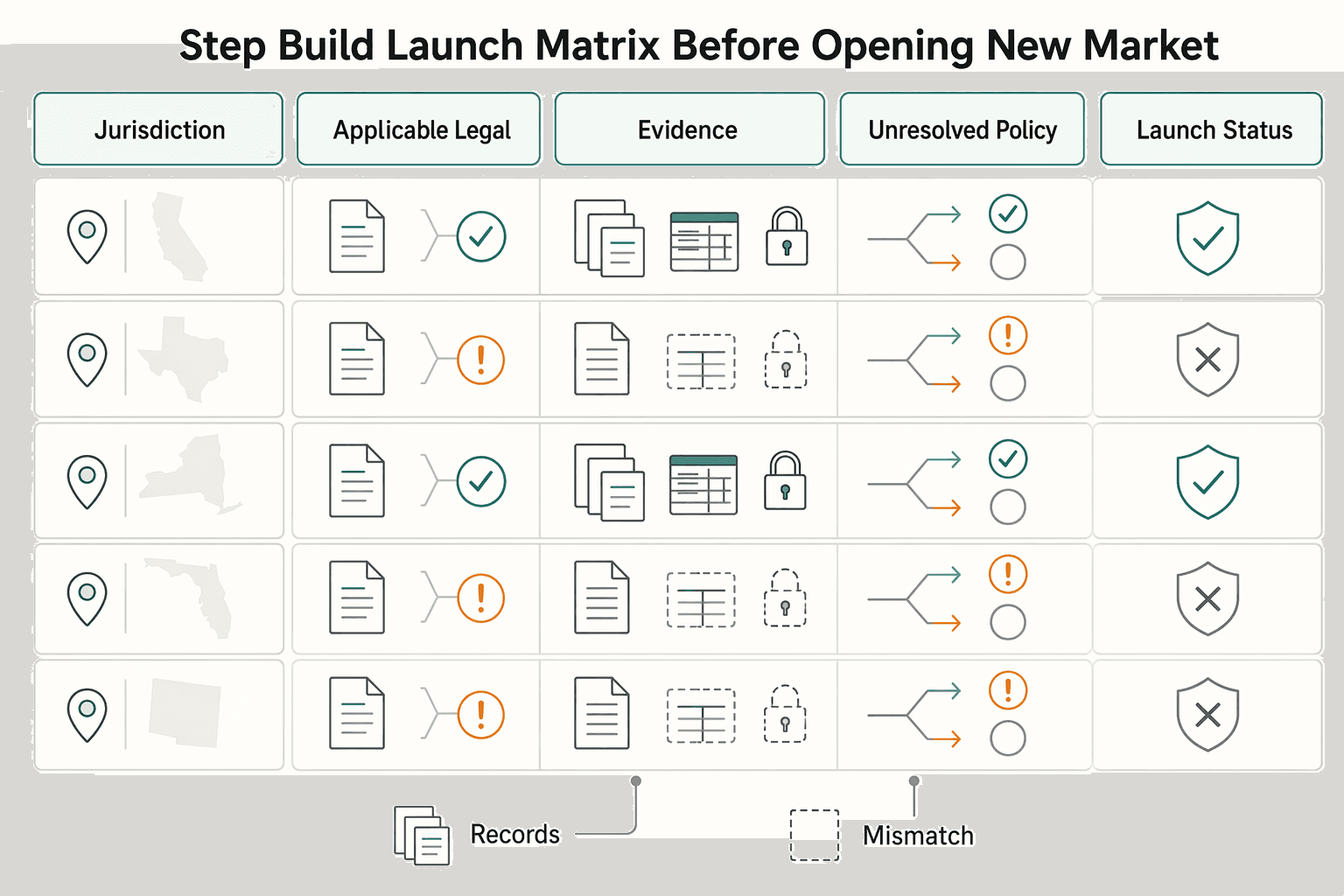

Step 1 Build a launch matrix before opening a new market#

Use one row per jurisdiction as a go or no-go control record.

| Launch-matrix field | What to record |

|---|---|

| jurisdiction | One row per jurisdiction as a go or no-go control record |

| applicable legal/tax guidance source identified | yes/no |

| documented counsel review for your payment flow | yes/no |

| unresolved policy unknowns | Record open risks instead of treating missing guidance as approval |

| launch status | approved, blocked, research-only |

| owner and last-reviewed date | Track accountability and review timing |

If one jurisdiction has clear guidance and another does not, record that gap as an open risk. Do not treat missing or generic guidance as implied approval.

Step 2 Require documented rule mapping before go-live#

Do not approve launch based on "we did not find a prohibition." Require documented counsel mapping of your actual payment flow, including collection, holding, payout, refund, and exception handling, to applicable legal and tax requirements in that jurisdiction.

If counsel cannot map the flow clearly, keep the market off production rails and mark it research-only.

Step 3 Add cross-border tax-data filters when foreign accounts or assets may be involved#

Use a separate tax-review gate when workflows may involve foreign financial assets or accounts. For this gate, keep checks explicit:

| Tax-review check | Grounded detail |

|---|---|

| Specified foreign financial assets threshold | Check whether a specified person may hold specified foreign financial assets above the appropriate reporting threshold for Form 8938 |

| Form 8938 filing timing | Form 8938 is attached to the annual return and filed by that return's due date, including extensions |

| No return required | If no income tax return is required, Form 8938 is not required |

| Excluded accounts | Some accounts are excluded from Form 8938 reporting, including accounts maintained by a U.S. payer |

| Separate FBAR obligation | Filing Form 8938 does not remove any separate FinCEN Form 114 (FBAR) requirement |

| Specified domestic entity thresholds | Form 8938 filing is triggered above $50,000 on the last day of the tax year or above $75,000 at any time during the tax year |

Do not generalize those dollar thresholds to every filer profile. The IRS indicates higher thresholds for joint filers and taxpayers residing abroad.

Step 4 Mark unknowns clearly and freeze launch while they remain open#

For each unknown, log the exact question, owner, and target resolution date. Keep each jurisdiction in research-only until those items are resolved and controls are validated.

Before final approval, re-check the current IRS Form 8938 page for instructions and latest information (last reviewed/updated 31-Mar-2026). If the answer is still unclear, do not launch that jurisdiction.

Prove compliance with ledger evidence auditors can actually use#

A control is only as strong as your ability to reconstruct a transaction end to end without manual detective work.

Step 1 Define an audit trail schema before volume hides gaps#

Use one canonical, exportable record shape for every payment event that can touch a trust account. The goal is evidence another reviewer can follow line by line, not a dashboard.

| Audit field | Purpose in the record |

|---|---|

| request ID and timestamp | Identify the payment event and when it began |

| who initiated the request | Show origin of the request |

| approval record and approver identity | Trace who approved the action |

| payee or provider reference used by the processor | Tie internal records to processor-side references |

| internal ledger posting ID | Link the request to ledger activity |

| payout status changes over time | Show how the payout progressed |

| reconciliation result | Record whether reconciliation closed or stayed open |

| linked exception or dispute ticket | Attach related exception history when applicable |

Use structured fields as the primary evidence layer. Free-text notes should be secondary. Billing and invoicing workflows already take time and leave little room for error, so consistency matters. Keep payment records centralized so the request, approval, processor reference, and ledger entry can be exported together for a random transaction, as in this legal marketplace compliance case study.

Step 2 Make reconciliation reproducible, not person-dependent#

If you use a three-way reconciliation workflow, treat it as a repeatable internal control, not a person-specific process. For each trust account transaction, tie together the provider record, internal ledger posting, and underlying account activity record with stable IDs.

A practical internal standard is for each ledger posting to include both the external provider reference and the internal request ID. That makes it easier to answer what was requested, what was approved, what settled, and whether reconciliation closed or stayed open. Reconcile at item level, not just totals, so exceptions do not require side logs to explain.

Step 3 Preserve exception history as events, not overwritten state#

Exceptions are where weak evidence shows up first. Keep a full event history so records show who changed what, when, and why.

Prioritize event capture for operationally risky changes, such as:

- edited beneficiaries

- payout retries

- dispute outcomes for chargebacks

For example, preserve prior and updated beneficiary references, first-failure status before retries, and dispute lifecycle states tied to the original transaction. Keep confidentiality constraints in mind: logs should support traceability without exposing unnecessary client-representation detail.

Step 4 Add a recurring rule-assumption review and record the version checked#

Run a fixed review cadence so operations do not drift from the legal assumptions your flow was built on.

Check whether actual payout behavior still matches counsel mapping, whether releases or vendor changes altered money movement, and whether approval or dispute artifacts still follow the expected record shape. Record the rule-version checkpoint you reviewed, not just "Legal reviewed." Rules text can be revised over time, so verify you are using a current published version before sign-off. If practice no longer matches those assumptions, freeze the affected flow and require updated counsel mapping before treating the control as effective again.

Implement integration controls that reduce operational risk#

Under stress, integration controls need to do two things well: prevent duplicate or misrouted payouts and preserve evidence you can reconstruct end to end.

The 2026 National Money Laundering Risk Assessment places both attorneys and third-party payment processors in a gatekeeper context. Treat that as an operational signal to apply the same control discipline in integrations that you apply in ledgering and approvals.

Step 1 Enforce idempotent payout requests#

A practical control is to use one idempotency key per payout intent and reuse it on retries instead of creating new requests. Keep retry fields consistent with the original intent (for example, request ID, amount, beneficiary reference, and source rail), and route conflicting retries to manual review.

This is a risk-control pattern, not a legal requirement stated in the cited materials.

Step 2 Capture webhook events as durable status history#

Treat webhook events as durable state history, not disposable notifications. Persist the event payload, receipt timestamp, related payout ID, and status transitions that affect downstream actions.

Design handlers to tolerate duplicate and out-of-order delivery without creating duplicate internal updates. Keep prior states visible rather than overwriting them in place.

Internal durability matters because external sources are not always reliable as sole evidence: FederalRegister.gov states its XML rendition is unofficial for legal research and should be verified against an official edition, and the excerpted page showed a 500 Server Error.

Step 3 Send policy breaks to a manual exception queue#

When an event conflicts with internal policy checks, route it to manual review.

Keep the queue decision-ready with the context needed to evaluate the exception and record the decision.

- payout or ledger reference

- policy rule that failed

- current owner and next review time

- release-or-hold decision once review ends

Step 4 Minimize sensitive data in logs while keeping traceability intact#

Keep logs traceable for investigation while limiting exposure of sensitive personal data.

This keeps reviewability high while respecting the privacy risk areas explicitly flagged in the source material, including Secure Private Information and Litigant Privacy.

Common mistakes and how to recover fast#

When a control fails, recover fastest by treating it as an evidence problem first. Pause the affected flow, narrow scope, and rebuild a defensible record before you resume volume.

Step 1 Rebuild the case-level pipeline before retrying#

A recurring failure mode is treating remediation as a one-time event instead of part of long-run preparation. Before reopening, maintain a case-level pipeline with stage, expected value, likelihood of success, and cycle time for each impacted matter.

If a record is incomplete, keep that item in manual review until the pipeline data is complete and documented.

Step 2 Block risky flows if core artifacts are missing#

Pause risky flows until the required operational artifacts are in place, including client notice templates, file transfer protocols, and cost-advance accounting support.

Treat this as a preparation gap, not a one-off incident. This excerpt does not establish trust-account-specific segregation or reconciliation requirements, so keep those rules counsel-defined.

Step 3 Validate confidence with your own documentation#

Do not rely on assurances alone when records are thin. Documentation quality should drive confidence: contingent work in progress is heavily discounted without clear documentation and realistic probability weighting.

Backfill missing records while they are still available, and label partially reconstructable events as partial.

Step 4 Freeze unclear consent lanes and retro-review#

If consent or notice handling is unclear, freeze that lane and document required records before resuming. Use documented client consent workflows where your legal standard requires them, including law-practice sale contexts that require client consent and notice.

Do the retro-review early. Many disputes are resolved before court or arbitration, so faster correction can reduce escalation risk. End each impacted item in one clear state: documentation complete, remediation required, or held pending review.

Related: Legal marketplace case study.

Go or no-go checklist before each market launch#

We default to no-go unless you can show four things: mapped jurisdiction references, production-ready controls, retrievable evidence, and written ownership of unresolved unknowns. If any one is missing, launch risk is still unmanaged.

Step 1 Map the jurisdiction sources before you schedule launch#

Build a market record that lists local bar or court ethics materials and formal opinions used by counsel. Do not mark items as merely "reviewed." Capture the specific references and identifiers, including jurisdiction-specific and ABA opinion identifiers such as Pennsylvania Formal Opinion 2014-300, Formal Opinion No. 2013-189, and ABA Formal Opinion 465.

Verification check: someone outside Legal should be able to open the launch record and see what was mapped, by whom, and when.

Step 2 Confirm the controls exist in production, not only on paper#

Treat this as a go or no-go control test, not a policy readout. For the controls defined in your launch record, require proof that each control is executable in production and produces evidence.

Verification check: each control has a named owner, current configuration evidence, and a recent sample output or exception-path record.

Step 3 Validate the evidence pack against retention expectations#

Before approval, retrieve the core records tied to launch decisions and client-file retention. The WSBA guidance, updated March 24, 2026, supports this pre-launch posture by emphasizing that teams should create policies and procedures in advance and maintain a strategy for retaining client-file-related documents.

If retrieval depends on memory or ad hoc reconstruction, evidence readiness is not met.

Step 4 Get explicit acceptance of unresolved unknowns#

Unresolved unknowns are acceptable only when they are explicit, bounded, and owned in writing. Document the unknown, likely impact, temporary control, and decision owner before launch.

Verification check: every unresolved item has a named accountable owner and written acceptance in the launch record.

- the unresolved question

- the temporary control in place

- the named owner

- the acceptance date and review deadline

Use this checklist as a hard launch gate, then map each control owner and evidence requirement into implementation tickets from Gruv Docs.

Conclusion#

Go live only when your fund paths, trust-account records, and open legal unknowns are documented well enough to defend. If you cannot show where funds were routed, how they were recorded, and why unresolved issues were accepted, treat that as a no-go.

Step 1#

Lock the money map before launch decisions. A lawyer trust account holds client funds separate from a lawyer's own funds, so your first proof is an explicit routing map with supporting records, not a policy statement.

Where fiduciary treatment depends on account setup, confirm trust status is disclosed in the account title and keep that evidence with ledger outputs. If your team cannot produce that packet quickly, readiness is not demonstrated.

Step 2#

Prove records in a reviewable format, not only in dashboards. For Washington-specific operations, WSBA provides concrete reconciliation artifacts, including the Monthly Reconciliation and Review Report and sample check register and client ledger templates.

Run a retrieval test on a transaction and confirm you can produce the trust-account record set and reconciliation output without manual reconstruction.

Step 3#

Treat unresolved exceptions and jurisdiction questions as launch blockers until ownership and decision records are complete. For third-party payment scenarios and other unresolved legal questions, route them to jurisdiction-specific legal review and store the decision basis.

Keep authority scope explicit: ABA Civil Legal Aid Standards apply to legal aid organizations and are not intended to govern every individual attorney context.

Step 4#

Use this closeout list and require evidence for each line item:

- Fund-routing paths and trust-account handling are explicitly documented with evidence.

- Third-party payment scenarios and unresolved legal questions are reviewed and decision records are stored.

- Reconciliation artifacts are produced on schedule and can be retrieved on demand.

- Jurisdiction unknowns are logged, owned, and explicitly accepted before go-live.

Start with account-path decisions, prove controls with records, then scale.

Before expanding to another state or cross-border lane, validate program coverage, policy gates, and rollout constraints for your flow through Contact.

Frequently Asked Questions

Can a legal marketplace use electronic payments and still stay compliant with ABA Model Rules of Professional Conduct?

Possibly, but not by default. Compliance depends on jurisdiction-specific rules and each lawyer's trust-account obligations, so validate the fund flow, account routing, and retrievable records before launch.

What is the minimum control set needed to protect an attorney trust account from commingling?

This article does not support a universal minimum control set. Use state-by-state legal review and document platform evidence for the rules that apply in each jurisdiction. If you cannot produce current configuration evidence and sample records, your controls are not yet demonstrated.

How should platforms handle third-party payments under ABA Model Rule 1.8(f)?

Do not assume standard payer handling is enough. Route third-party-funded matters to jurisdiction-specific legal review and store the decision basis with the mapped rule source. The article also recommends a separate review lane, confidentiality limits, and a hard stop when required ethics records are incomplete.

Do paralegal payouts follow the same trust-account logic as attorney payouts in every case?

No. The article does not support assuming paralegal and attorney payouts follow the same trust-account logic in every case. Classify payouts by role and fund type, and send unclear entitlement cases to manual review instead of default routing.

What should founders validate first when entering a new state with different IOLTA account rules?

Validate the state's actual filing and reporting obligations first, not vendor claims. In Washington, active licensed legal professionals file a Trust Account Declaration once a year during license renewal with current information, and the filing covers currently open IOLTA accounts. It requests the IOLTA bank and account number and says not to list individual client trust accounts or other non-IOLTA accounts.

What remains unknown when comparing processors like LawPay without independent implementation data?

Without independent implementation data, key readiness details remain unknown. You still need to verify your own configuration and the evidence you can produce. Public comparison detail can be limited, so treat vendor pages as option discovery rather than compliance proof.

Can teams use ABA materials as general operating guidance for every legal-payment question?

No, not automatically. The ABA Civil Legal Aid Standards in this article are scoped to legal aid organizations and are not intended for individual attorney efforts outside that scope. Confirm the scope of the authority you cite before using it in market-launch decisions.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- acus.gov/sites/default/files/documents/1986-01%20Nonl...trusted

- calbar.ca.gov/Portals/0/documents/accessJustice/2024-Legal...trusted

- calbar.ca.gov/portals/0/documents/reports/2001_MDP-Report.pdftrusted

- clp.law.harvard.edu/article/the-politics-of-lawyer-regulationtrusted

- ecf.vid.uscourts.gov/vidapps/Materials_for_Legal_Ethics_in_the_Ag...trusted

- federalregister.gov/documents/2024/12/10/2024-27836/defining-lar...trusted

- federalregister.gov/documents/2024/10/29/2024-24582/provisions-p...trusted

- home.treasury.gov/system/files/246/2026-NMLRA.pdftrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: