Quick Answer

Choose a Source-to-Pay approach that matches your main operational constraint, then prove it can connect sourcing, contracts, purchasing, invoice handling, and payment in one traceable flow. For source to pay procurement automation platform lifecycle decisions, the fastest way to avoid rework is to require linked records, exportable ledger journals, and tested webhook plus idempotency behavior before selection. Use a phased first 90 days to validate controls, reconciliation outputs, and ownership before broad rollout.

How source-to-pay works across the procurement lifecycle#

For platform teams, the pain usually does not sit in one isolated procurement task. It shows up in the handoff between finance, ops, product, and engineering as a supplier relationship moves from evaluation to agreement, purchasing, invoice review, and payout. A credible S2P platform should support that path end to end, not just the last mile of AP. In practical terms, the scope includes strategic sourcing, contract lifecycle management, procurement, invoice processing, and payment. You can frame S2P as four linked decisions:

- Source: You identify and evaluate suppliers before money moves. The differentiator is upstream control, because S2P starts with supplier sourcing rather than with an invoice arriving in a shared inbox.

- Contract: Terms, pricing, and obligations need to follow the commercial relationship. The differentiator is continuity, since contract management belongs in the same chain as purchasing and payment, not in a separate legal silo that finance cannot easily see.

- Buy: Requests, approvals, and purchasing activity turn intent into committed spend. The differentiator is operational traceability, because procurement is the bridge between strategic sourcing and downstream invoice processing.

- Pay: Invoice processing and payment close the loop. The differentiator is completeness, since payment without the earlier sourcing and contract context is AP efficiency, not full S2P coverage.

The first mistake to avoid is assuming any AP tool with invoice automation qualifies as Source-to-Pay. If a vendor cannot show how sourcing and contracting connect to buying and paying in one integrated process, your team will still be stitching together the truth across boundaries. That is where finance and procurement alignment starts to break down, especially when different owners need the same history for approval, spend review, and exception handling.

Before demos, use one checkpoint. Ask the vendor to walk a single supplier record from sourcing through contract, procurement, invoice processing, and payment, with the same history visible throughout. If the story depends on manual exports, side systems, or a separate payment handoff, that is a real red flag. The AP screen may still be useful, but it is not the same as unified S2P.

The rest of this guide is written for teams operating across multiple programs and markets where coverage may vary by context. The goal is not to force one architecture on every case, but to help you choose a model that keeps spend control, compliance, reconciliation, and implementation effort in balance. Related reading: How Platform Operators Pay Creators Globally Across YouTube, Twitch, and Substack.

Selection Criteria That Separate Real S2P Platforms From Basic AP Tools#

If you need full Source-to-Pay coverage, filter for provable control across the whole lifecycle, not just a polished AP interface. A credible platform should carry one operational history from supplier sourcing through contract, purchase order, invoice, and payment, and let you export that history when exceptions happen.

- Integrated lifecycle coverage

Use end-to-end coverage as your first gate. Real S2P suites keep sourcing and procurement in one integrated system, with data flowing across upstream and downstream steps. In demos, ask for one supplier record to move from sourcing to contract to PO to invoice to payment without CSV handoffs or split status trails.

- Compliance gates before payout

For regulated payout programs, onboarding controls must be enforceable before funds move. KYC checks may be required before payout, and KYB is a separate business-entity check from individual KYC. Focus on whether the platform can actually block or release activity based on those checks and preserve those decisions for review, including AML controls where they are part of your risk model.

- Exportable audit trail for finance

Visual dashboards are not enough for close and audit. You need API- and webhook-level status history plus journal records finance can reconcile. Webhook events can provide machine-readable payment updates, and posting journals are part of the audit trail for ledger entries. If journals or event history are not exportable, reconciliation risk rises quickly.

- Retry safety and reconciliation detail

Engineering and finance need the same reliable record. Require idempotency for create/update API calls so retries do not create duplicate effects. Ask vendors to replay the same request twice and show consistent results, then provide reconciliation exports linking supplier, invoice, journal, and payout references.

If you are only solving a domestic AP inbox issue, a narrower AP tool may be enough. If supplier management, payout complexity, or cross-border controls are in scope, these criteria help you avoid buying a tool that is too narrow. For teams considering a more outsourced model, see What Is Procurement as a Service? How Platforms Can Outsource Vendor Sourcing and Contracting.

The 5 S2P Automation Models Platform Teams Actually Buy#

Pick the model that removes your tightest constraint first. If invoice workflow is the issue, start there. If payout control and reconciliation are the issue, start there.

- AP-first add-ons

Best when you need invoice automation and AP efficiency now, not deep sourcing or contract control. AP automation covers the end-to-end payment lifecycle, while automated invoice processing is only one subset, so do not assume an invoice tool gives you full procurement coverage.

The upside is a narrower rollout focused on invoice intake, coding, and approvals. The tradeoff is weaker upstream control. In demos, confirm supplier record, contract reference, and PO are first-class objects linked to the invoice, not just free-text fields.

- Procurement-first suites

Best when supplier management, spend analysis, e-procurement, and PO control are the main gaps. These suites are built for integrated coverage across source, contract, request, procure, receive, and pay.

The tradeoff is that payments may be a downstream integration, which can duplicate parts of an existing payout stack. Require one end-to-end walkthrough from sourcing through payment handoff with no manual rekeying, or you risk strong procurement governance with weak payout visibility.

- Payment-led infrastructure with procurement extensions

Best when payout execution, retry safety, and status visibility are the bottleneck. Look for API-level payout objects, webhook events, and idempotent request handling for safe retries. Operational detail matters here: idempotency keys can be up to 255 characters, and key pruning can occur after 24 hours.

The tradeoff is lighter upstream tooling for sourcing, vendor evaluation, and contract management. Validate early that procurement approvals can actually gate payout readiness, instead of living in a separate system with no enforcement link.

- Modular hybrid stack

Best when no single product fits every business line and you are prepared to own integrations. Modular S2P architecture lets teams activate only needed functions, often combined with payment-layer components like virtual accounts or a Merchant of Record model.

The upside is flexibility during phased migration. The tradeoff is data-boundary risk. Define system ownership for supplier status, payment responsibility, and reconciliation on day one, especially if one entity is the Merchant of Record and carries legal and compliance responsibility for payment processing.

- Outsourced procurement with embedded payments

Best when your immediate gap is operating capacity, not software features. Procurement outsourcing is a real model where activities such as sourcing, category management, and transaction management move to a third party.

The upside is external execution support while payments run on embedded rails. The tradeoff is dependency risk and weaker direct process control. Before you sign, set escalation paths, approval boundaries, and evidence access so you do not lose critical operating knowledge.

Once you match the model to your dominant problem, shortlisting gets simpler and tradeoff comparisons become more useful. Related: What Is AP Automation? A Platform Operator's Guide to Eliminating Manual Payables.

Comparison Table for Fast Shortlisting#

Use this table to cut weak fits before demos. If a vendor cannot answer the compliance and integration checks below in writing, treat it as a no for now.

| Model | Best for | Core strengths | Main tradeoff | Must-verify before selection |

|---|---|---|---|---|

| AP-first add-ons | Fast AP cleanup | Invoice automation, accounts payable | Thin supplier sourcing depth | Contract management and purchase order controls |

| Procurement-first suites | Complex sourcing governance | Supplier management, spend analysis, e-Procurement | Slower payout-native execution | API/Webhooks maturity and payout handoff quality |

| Payment-led infrastructure | High-volume payout operations | Payout batches, virtual accounts, idempotency | Lighter upstream procurement UX | Procurement lifecycle coverage and approval logic |

| Modular hybrid stack | Phased modernization | Flexibility across MoR and procurement components | Integration and ownership complexity | Single source of truth via ledger journals |

| Outsourced procurement + embedded payments | Lean teams scaling quickly | Faster vendor evaluation and sourcing operations | Dependency on external operators | Escalation paths, SLA clarity, compliance boundaries |

Score each row against three separate needs: Source-to-Pay, Procure-to-Pay, and payout execution. A common miss is over-scoring invoice or supplier strengths while payment status, reconciliation, or tax handling still depends on manual handoffs.

Use record linkage as an early proof test. Ask the vendor to show contract, purchase order, invoice, and payment reference in one connected chain (for example, a purchase order linked to its related contract). If linkage depends on free text or CSV export, lifecycle control is still partial.

Compliance questions that should kill deals early#

Late launch risk often sits in document and verification gaps, not headline features. Require explicit answers on KYC, KYB, AML, VAT validation, and tax-document support where those controls are enabled for your program and jurisdictions. Ask with exact document names:

| Artifact | What it is | What to confirm |

|---|---|---|

| Form W-9 | Correct TIN provided to a requester filing IRS information returns | Can the platform collect, validate, store, update, and export these records with transaction linkage? |

| Form W-8 BEN | Foreign beneficial owner form for a withholding agent or payer | Can the platform collect, validate, store, update, and export these records with transaction linkage? |

| Form 1099-NEC | Nonemployee compensation reporting | Can the platform collect, validate, store, update, and export these records with transaction linkage? |

| VIES VAT validation | EU cross-border VAT registration check | Ask whether validation uses VIES and whether the result is stored as evidence. |

Then move from collection to operations: can the platform collect, validate, store, update, and export these records with transaction linkage? For VAT, ask whether validation uses VIES and whether the result is stored as evidence. For AML in US-regulated contexts, ask how controls map to Bank Secrecy Act obligations.

Integration checks worth doing before technical review#

Run these checks before deep architecture work. Webhooks are useful because they push real-time event data, but webhook support alone does not prove audit readiness.

| Check | Details |

|---|---|

| API coverage | Supplier, contract, purchase order, invoice, payment, and status history |

| Webhook quality | Event types, retry behavior, and payload fields your ops team can act on |

| Ledger journals granularity | Trace between general ledger, subledgers, and originating transactions |

| Idempotency behavior under retries | Repeat requests do not execute the same operation twice during failures or timeouts |

Use one failure test in the demo: replay a webhook and retry the same payment or state-change request. Idempotency supports safe retries, but you still need to see how the product handles duplicate events, stale states, and reconciliation exceptions.

For modular hybrid stacks, make ledger-journal traceability the deciding check. If no one can name the source of truth for journal entries, approval status, and payout references, operating complexity will rise after go-live.

For a closer look at the sourcing and vendor-management side, see What Procurement Means for Platform Operators Managing Strategic Sourcing and Vendors.

Decision Rules for Choosing Without Analysis Paralysis#

Choose the model that removes your current bottleneck first, not the one with the longest feature list.

- Choose payment-led when execution reliability is the pain.

If payout failures, retries, and status blind spots are driving operational noise, prioritize payment-led infrastructure. Verify idempotency and usable status history by asking the vendor to replay a webhook and retry the same payment request. If that produces duplicate state changes, stale statuses, or manual exception cleanup, treat it as a core risk.

- Choose procurement-first when sourcing control is the pain.

If uncontrolled onboarding, contract drift, weak purchase order discipline, or limited spend visibility is your issue, procurement-first is usually the better fit. Confirm users can trace contract, purchase order, invoice, and payment reference in one chain, not via free text or CSV exports. Visibility gaps can slow controls and tasks, which is how policy exceptions stay hidden until late.

- Avoid modular hybrid if no one can own the joins.

Hybrid can cover more of the lifecycle, but only when your team can own APIs, webhooks, retries, and journal mapping across tools. Require a named owner and a written source of truth for ledger journals, approval status, and payout references. If that ownership is unclear, implementation risk rises toward overruns, misalignment, and delays.

- Reject vague cross-border compliance answers early.

When cross-border tax and compliance are in scope, require explicit support for VIES VAT validation, Form W-8 BEN, Form W-9, and Form 1099-NEC artifacts where supported. Ask whether VAT validation results are stored as evidence, and account for the edge case that VIES stopped validating UK (GB) VAT numbers as of 01/01/2021. For US reporting, ask how reportable transactions link to recipient records and how Form 1099-NEC outputs and recipient copies are handled by January 31.

- Phase by risk if you need both control and speed.

If you need fast launch and tighter controls, phase implementation instead of changing everything at once. Stabilize accounts payable and invoice automation first, then expand to supplier sourcing and contract management once status history, journals, and tax-document handling are reliable.

For a deeper look at the AP portion of source-to-pay, see Accounts Payable Automation for Dummies for Platform Operators.

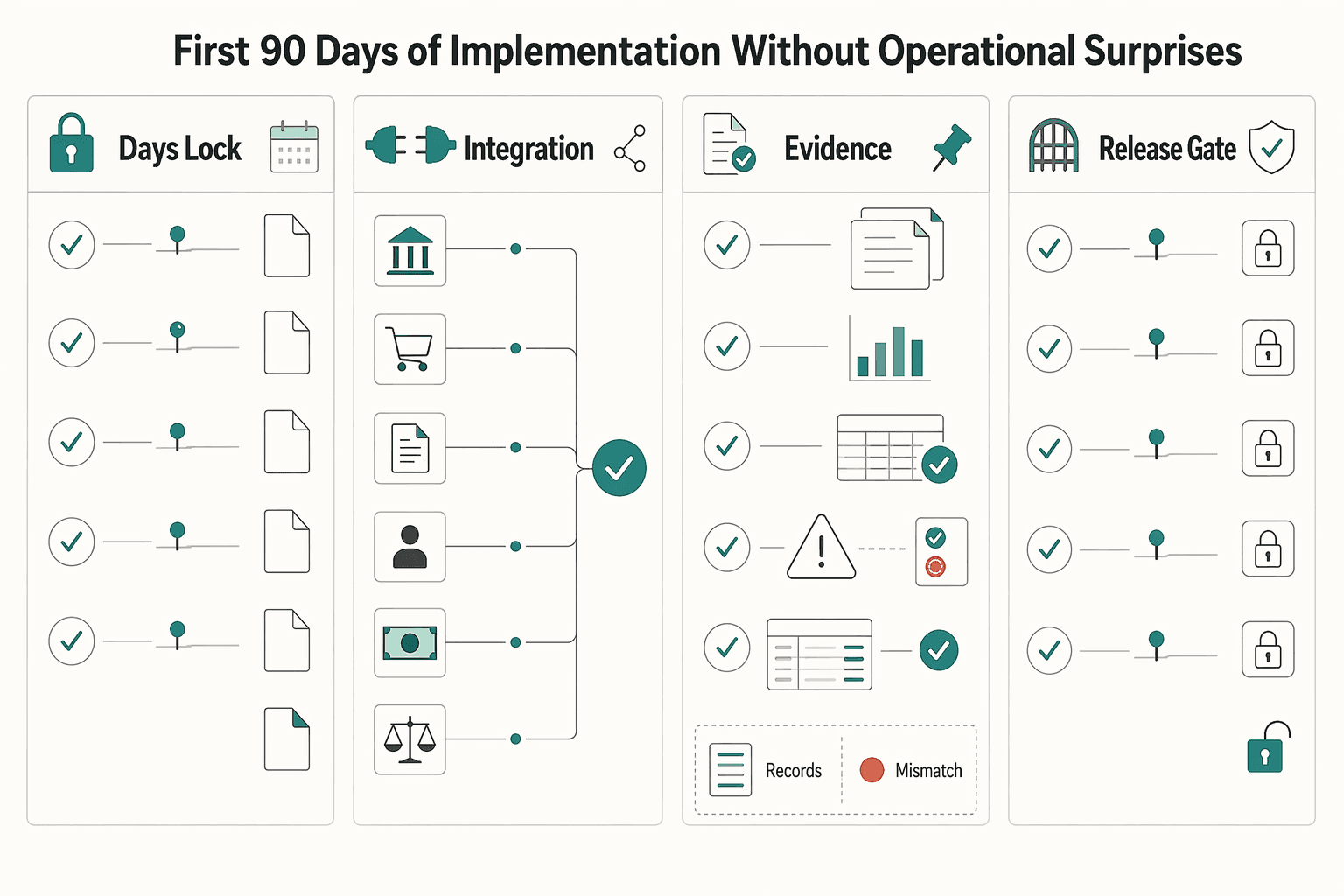

First 90 Days of Implementation Without Operational Surprises#

The first 90 days should prove control and reliability, not activate every feature. Keep scope risk-based and verify that ownership, retries, event handling, reconciliation, and compliance gates work predictably before you expand.

| Phase | Primary focus | Checkpoint |

|---|---|---|

| Days 1 to 30 | Lock ownership and phase-one scope around the real workflow | Trace one sample transaction from supplier setup to final payout reference without spreadsheet stitching or tribal knowledge |

| Days 31 to 60 | Implement integrations in a retry-safe sequence | Resend the same webhook and retry the same API request with the same idempotency key; you should see one business outcome, one stable transaction reference, and a clear audit trail |

| Days 61 to 90 | Run parallel operations until cutover evidence is complete | Define explicit cutover criteria: acceptable exception volume, end-to-end status visibility, and evidence outputs finance can use |

- Days 1 to 30: lock ownership and phase-one scope around the real workflow.

Map how work actually moves across Source-to-Pay and Procure-to-Pay: supplier management, purchase order creation, invoice automation, approvals, payout initiation, and reconciliation. Assign a named owner to each step, including tax document review, payment exceptions, and ledger export checks. Your checkpoint is simple: can you trace one sample transaction from supplier setup to final payout reference without spreadsheet stitching or tribal knowledge? If not, tighten the scope before moving on.

- Days 31 to 60: implement integrations in a retry-safe sequence.

Build in this order: API auth, webhook event consumption, idempotency keys for create/update actions, then ledger journal reconciliation and exception queues. This sequence reduces duplicate or missing state and gives finance a usable trail. Run live replay tests by resending the same webhook and retrying the same API request with the same idempotency key. You should see one business outcome, one stable transaction reference, and a clear audit trail.

- Days 61 to 90: run parallel operations until cutover evidence is complete.

Use a go-live checklist to confirm the solution meets business needs and works as expected before broad rollout. Define explicit cutover criteria: acceptable exception volume, end-to-end status visibility, and evidence outputs finance can use. If AML/KYC/KYB gates are configured, test real decision paths (holds, manual review, approvals). Where applicable, verify risk-based identity procedures and legal-entity checks are documented, stored, and tied to payment-release controls.

- Use failure drills as a go-live gate, not a status meeting.

Include drills for duplicate webhook replay, stale status handling, unmatched payout or deposit investigations, and rollback triggers. Confirm reconciliation can surface open exceptions for the current period and route them to a named owner. A practical readiness test: if an event arrives twice or a payout settles without a matching record, can your team pull request history, event history, ledger journal entries, and exception notes quickly?

Controls and Evidence Finance and Auditors Will Ask For#

After the pilot, the test is proof, not possibility. Your baseline should be clear: for every transaction chain, you can show what happened end to end without digging through chat threads or raw logs.

- Require one linked evidence pack for each transaction chain.

For each purchase order, invoice, and payout flow, retain five linked records: the original request record, the policy decision record (KYC, KYB, or AML where applicable), the provider reference, the ledger journals, and the reconciliation export used by finance. Linkage is the control. If a payout settles and you cannot retrieve the matching provider reference and journal entries quickly, you have fragments, not an audit trail.

Run a sample retrieval check before each phase gate: start from the payout reference and trace back to invoice and request without engineering intervention. Keep event detail, not just final status.

- Assign explicit ownership for tax and compliance artifacts up front.

Treat W-9, Form W-8 BEN, Form 1099 workflows, FBAR questions, and FEIE-related document handling as owned workflows, not shared inbox work. Form W-9 provides taxpayer identification data for information reporting, Form W-8 BEN is submitted when requested by the withholding agent or payer, and FBAR reporting is filed on FinCEN Form 114 for qualifying foreign financial accounts. These are different artifacts with different operational handling, so ownership should be named.

A practical split is: one team collects, one team reviews, and one team decides what blocks payment release.

- Make status-transition history visible across PO, invoice, and payout states.

A current status field is not enough. You need transition history showing when a purchase order changed state, when an invoice was approved or held, when a payout moved to submitted or settled, and which webhook event triggered each update. Webhooks help synchronize status changes, but logs alone are incomplete unless each event is mapped to an operational action and closure note.

Validate this with replay plus case review: resend an event, confirm no duplicate business outcome, and confirm the case record shows who reviewed the exception and why it was closed.

- Use phase gates based on control evidence, not confidence.

Before moving to broader rollout, verify three checks: control effectiveness, exception resolution time, and completeness of audit-trail exports. If your model is covered by U.S. AML beneficial ownership rules under 31 CFR 1010.230, written procedures and resulting records for identifying and verifying beneficial owners of legal-entity customers must be inspectable.

If any one of these checks is weak, hold the gate. Early tolerance for weak exception handling usually becomes a month-end reconciliation problem later.

Common Failure Modes in S2P Automation and How to Catch Them Early#

Most S2P failures come from fragmented ownership, unclear transaction truth, and retry behavior that was never tested. Before cutover, pressure-test these four areas across the full lifecycle, not just invoice intake.

- AP-first automation with manual upstream controls

Automating invoices and parts of accounts payable while leaving supplier sourcing and contract management in separate workflows keeps the same fragmentation that integrated Procure-to-Pay is meant to reduce. Manual handoffs across steps get harder to manage as volume grows, and control gaps usually appear upstream first.

Catch this early with an end-to-end timing check. Sample recent transactions from supplier selection through purchase order, contract signoff, invoice approval, and payout release. If upstream approvals still sit outside the platform, expect slower decisions and inconsistent policy application.

- No agreed transaction truth between procurement and payout

If procurement and payout tools show different outcomes for the same chain, AP ends up reconciling two versions of reality. You need one defensible financial record for settled outcomes, with ledger journals linked to provider references and reconciliation exports.

Catch this with a three-way sample test: invoice record, payout reference, and ledger journals should align for the same transaction chain. If state can change in one system without matching journal or provider linkage, reconciliation churn is already built in.

- Webhook handling without idempotency

Webhook consumers should assume duplicate delivery and retry behavior, so handlers must be idempotent. If every delivery mutates business state, retries can reopen cases, duplicate approvals, or trigger another payout attempt.

Catch this with replay and retry tests. Resend the same event and force an uncertain outbound request outcome, then retry with idempotency controls. You should get one business outcome, one journal effect, and one closure path.

- Compliance added after the happy path works

KYC and AML policy gates should be designed as core flow logic, not a late add-on. Payment and payout capabilities can be blocked until KYC requirements are fulfilled, depending on setup and jurisdiction.

Catch this before launch by testing exception paths such as missing verification data, review-required states, and post-resubmission approval. Your evidence should show the policy decision, the blocked action, and the release event from hold to recovery.

For more on scaling AP operations without adding headcount, see Finance Automation and Accounts Payable Growth: How Platforms Scale AP Without Scaling Headcount.

Conclusion#

If you keep one rule from this guide, make it this: choose by your dominant constraint, not by the vendor category on the homepage. When upstream supplier sourcing and contract management are part of the problem, you need Source-to-Pay coverage because the real distinction from Procure-to-Pay is scope. When the pain is mostly transactional purchasing, invoice handling, and payment, a narrower approach can work, but only if you know exactly where supplier and contract decisions will live.

-

Scope first. Start by deciding whether you need the full lifecycle or only the transactional flow. S2P includes P2P but starts earlier with strategic sourcing and contract management, so your first checkpoint is simple: can one team trace a supplier decision, contract approval, purchase order, invoice, and payment without switching to disconnected records? A common failure mode is buying polished invoice automation, then discovering that supplier selection and contract drift still sit in email and shared drives.

-

Integration reliability second. Full-lifecycle coverage only helps if the product integrates with the source systems that already hold supplier, contract, purchasing, and finance data. Early in implementation, verify the handoffs that matter: status updates, exception handling, duplicate prevention, and whether finance records line up with reconciliation outputs. A red flag is a vendor that can demo approvals but cannot show how finance and procurement stay aligned once exceptions and retries hit production.

-

Compliance evidence throughout. Do not treat compliance as the cleanup phase after go-live. The automation value worth paying for is not just less manual effort, but stronger compliance and clearer visibility into spend. That means your evidence pack should be available at transaction level: request record, policy decision, transaction reference, accounting record, and reconciliation export. If tax or onboarding controls are in scope, confirm document ownership and auditability before rollout.

That order is not a universal law for every architecture. It is a strong operating rule for most platform teams: decide the lifecycle boundary first, prove the integration path next, and keep evidence visible from day one. Teams that work this way tend to make cleaner tradeoffs because they know what they are actually buying, what must integrate, and what auditors or finance leads will ask for later. That is the practical path to an S2P lifecycle that stays useful after the demo and holds up under real operational pressure.

For a step-by-step walkthrough, see What Is Vendor Management? A Platform Operator's Guide to Supplier Lifecycle Control.

Frequently Asked Questions

What stages are included in the full S2P lifecycle?

A full lifecycle usually includes need identification, supplier sourcing, contracting, purchasing, invoice processing, and payment. If a vendor only shows you invoice capture and approval screens, you are likely looking at a narrower Procure-to-Pay or AP tool, not full S2P coverage.

How is Source-to-Pay different from Procure-to-Pay?

The practical difference is that S2P starts earlier. Procure-to-Pay covers execution from requisitioning goods and services through invoice processing and payment, while S2P adds the upstream strategic sourcing work before that transactional flow begins. If supplier selection and contract decisions still happen outside the platform, you likely have P2P with add-ons, not true end-to-end coverage.

What does an S2P automation platform actually automate versus a basic AP tool?

A basic AP tool usually automates invoice intake, routing, and payment steps. A broader platform should also cover sourcing, contracting, purchasing, and the controls that tie those steps to payment-status visibility and auditability. A useful checkpoint is whether you can trace one transaction across those stages without leaving the product.

What should platform teams evaluate first when selecting a vendor?

Start with your biggest friction point, not the longest feature checklist. If your pain is reconciliation and payout-status blind spots, verify payment-status visibility and audit trails. If your pain is sourcing chaos, test supplier and contract controls first. Red flag: a vendor demos polished approvals but cannot show clear auditability or status history.

How long does a realistic first implementation phase usually take?

There is no universal timeline, and you should be suspicious of one. What is well supported is the rollout pattern: phase it instead of trying a disruptive big bang launch. In practice, keep the first phase scoped and validated before broad rollout.

What controls prove the process is audit-ready, not just automated?

Look for embedded controls, complete auditability, and clear payment-status visibility. At the transaction level, three-way matching for purchase orders, invoices, and receipts is a strong baseline. If tax onboarding is in scope, confirm document handling for Form W-9, Form W-8 BEN when requested by the payer or withholding agent, and Form 1099-NEC workflows where supported.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- docs.stripe.com/api/idempotent_requeststrusted

- docs.stripe.com/webhookstrusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- fdic.gov/banker-resource-center/anti-money-laundering...trusted

- federalregister.gov/documents/2024/07/03/2024-14414/anti-money-l...trusted

- irs.gov/forms-pubs/about-form-w-8-bentrusted

- irs.gov/forms-pubs/about-form-w-9trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How Platform Teams Scale AP Volume Without Adding Headcount

Use this as a decision list for operators scaling Accounts Payable, not a generic AP automation explainer. In these case-study examples, invoice volume can grow faster than AP headcount when the platform fit is right, but vendor claims still need hard validation.

What Is AP Automation? A Platform Operator's Guide to Eliminating Manual Payables

AP stops feeling like a back-office admin task once your platform is processing more supplier and vendor payables. At that point, **ap automation for platform operators** is about controlling operational risk as much as efficiency. Manual AP is slower, more error-prone, and more expensive, and those weaknesses surface fast as volume rises.

What Is Procurement as a Service? How Platforms Can Outsource Vendor Sourcing and Contracting

If you are evaluating procurement as a service for vendor sourcing, start by drawing control boundaries before you outsource anything. Hosted services can scale quickly, but faster access to vendors or contracts does not automatically mean better procurement. The harder question is still who owns approvals, evidence, and exceptions.